ACC30010 Audit Plan: Accounts Payable for Reliable Printers Ltd (RPL)

VerifiedAdded on 2023/01/12

|11

|1746

|66

Report

AI Summary

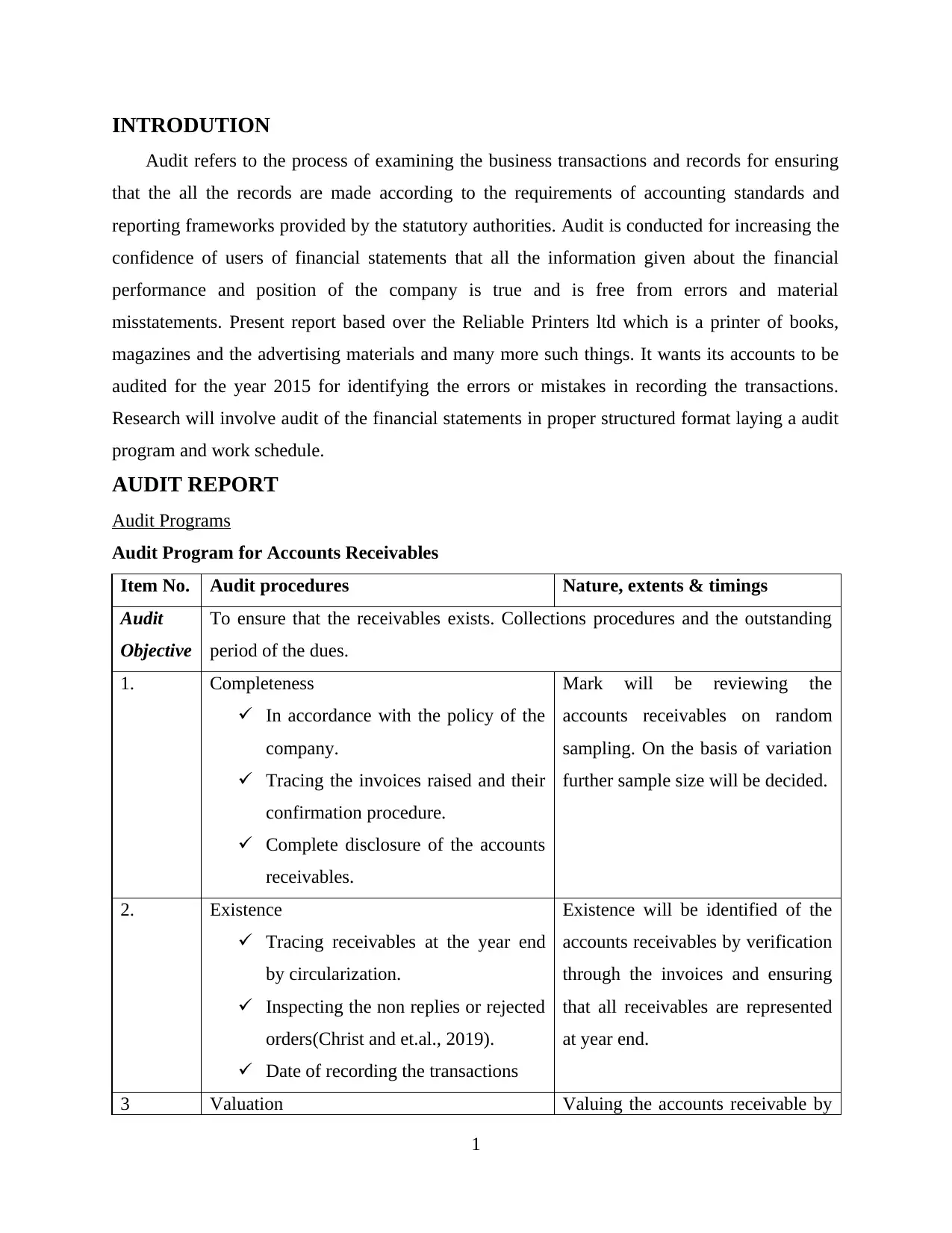

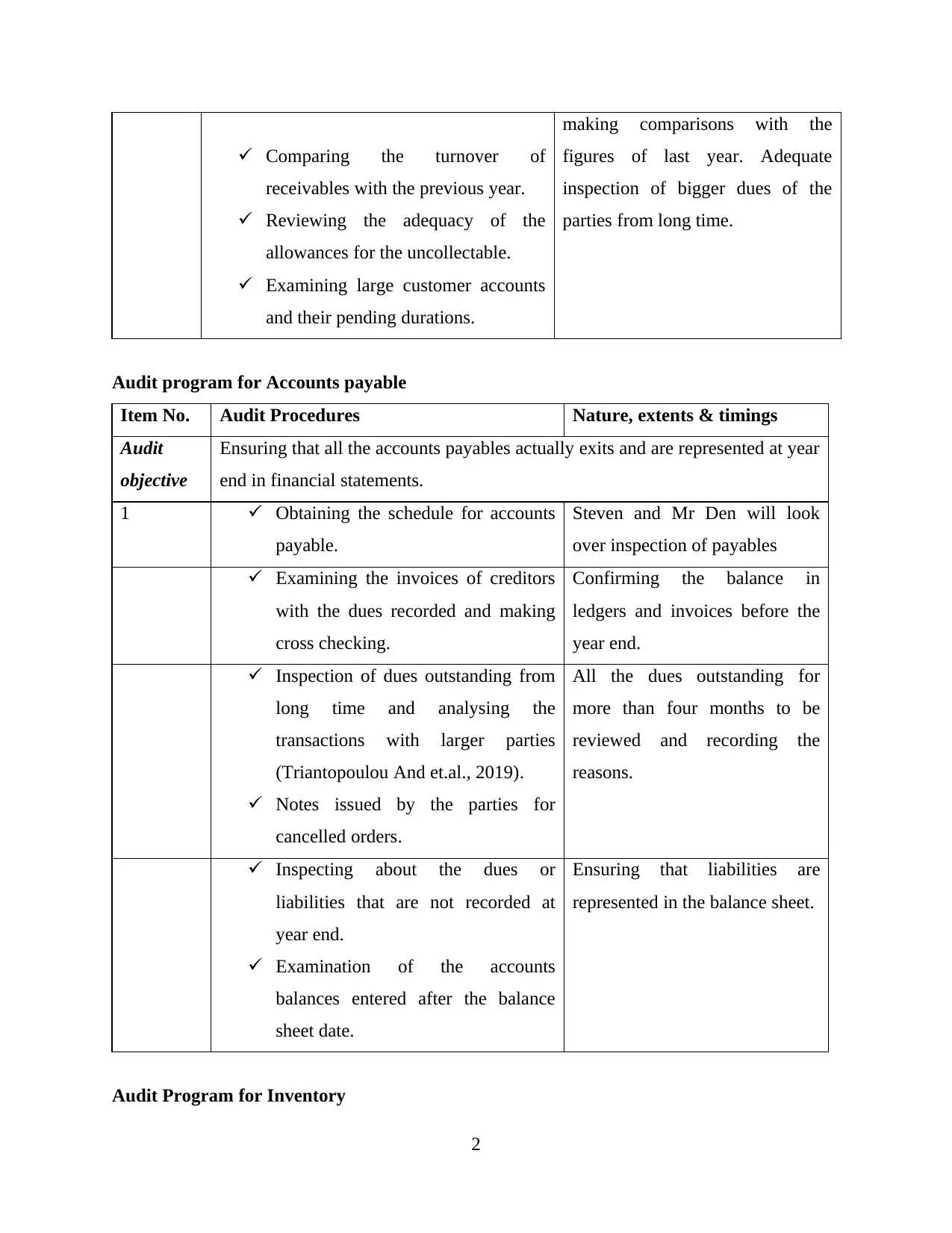

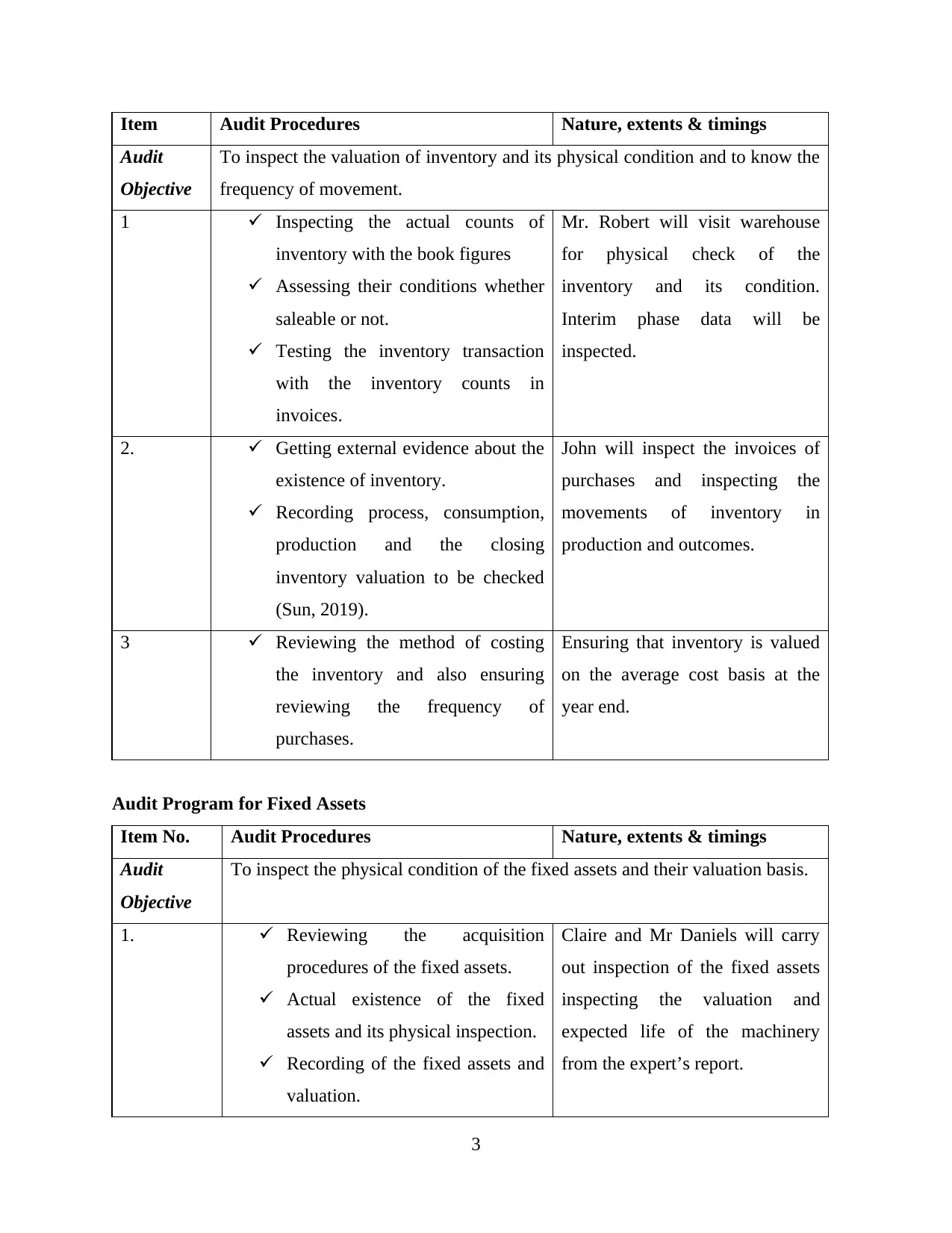

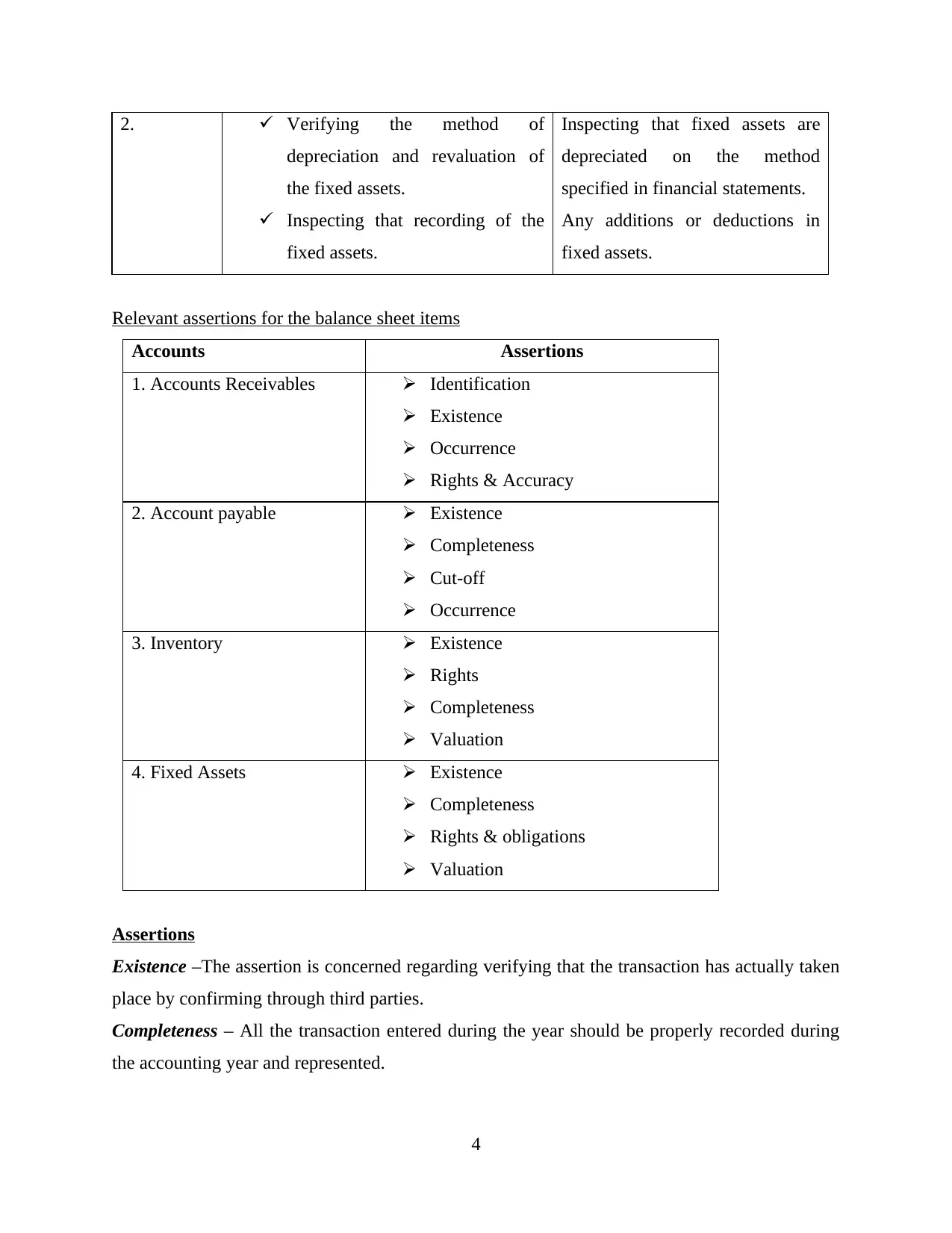

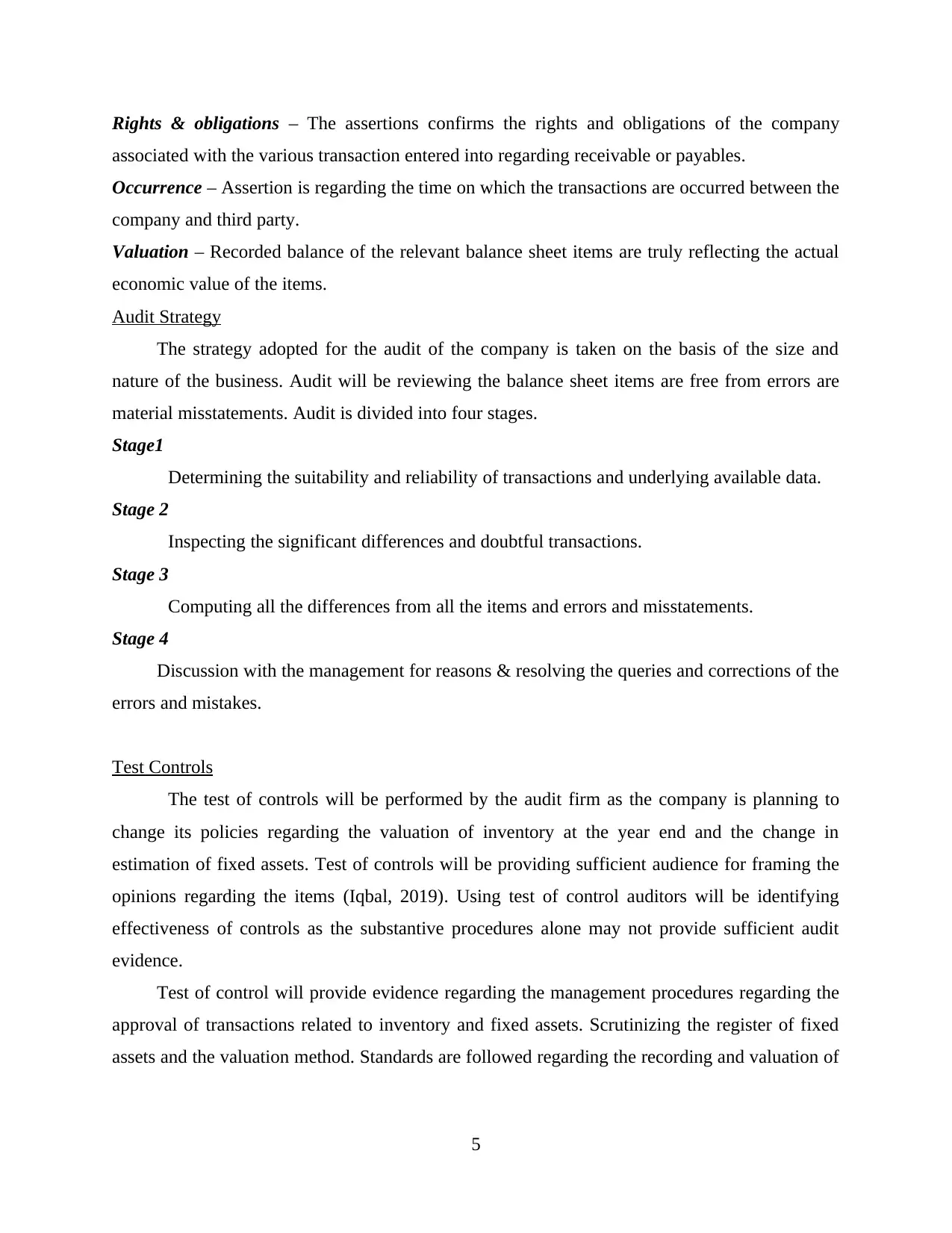

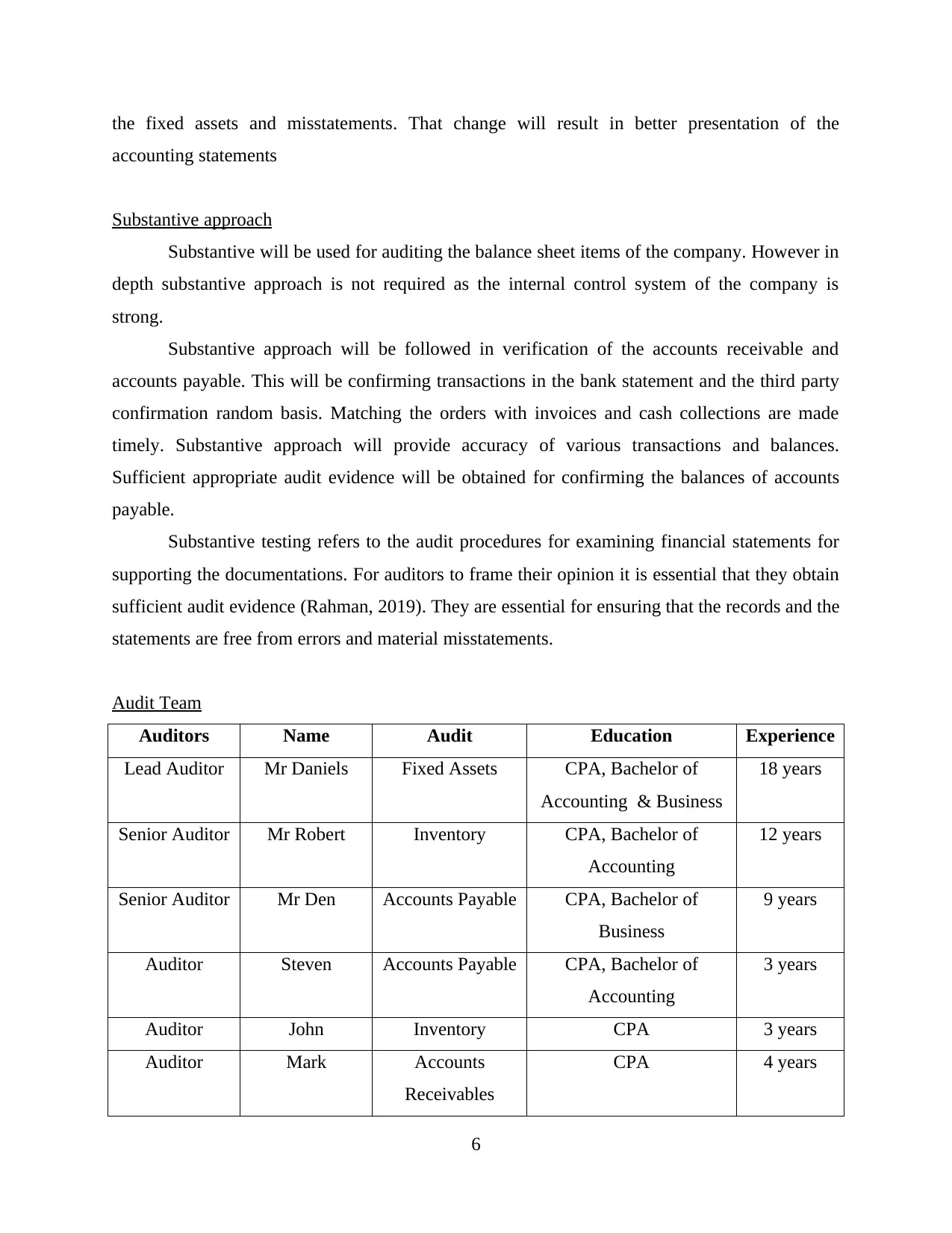

This report presents an audit plan for Reliable Printers Ltd (RPL), a printing company, focusing specifically on the accounts payable section for the year ended June 30, 2019. The plan, developed by an imaginary audit team from Luccia and Jansen (L&J), addresses the specific requirements outlined in the ACC30010 assignment. It details audit procedures, including the nature, extent, and timing of tests, designed to ensure the accuracy and reliability of accounts payable balances. The plan includes an examination of invoices, confirmation of balances with creditors, and inspection of outstanding dues. The report also addresses relevant assertions, the audit strategy, the use of test controls, and the substantive approach. Furthermore, the report outlines the composition of the audit team, including their roles, education, and experience, and culminates in a conclusion summarizing the key aspects of the audit plan and its importance in ensuring the integrity of financial statements. References to relevant books and journals are provided.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.