Evaluating the Russian Tax System's Role in Economic Growth

VerifiedAdded on 2023/05/29

|19

|4789

|437

Essay

AI Summary

This essay critically analyzes the Russian taxation law and its implications on economic growth and development, comparing it with tax principles of other nations. It examines the historical context, including the economic changes after Vladimir Putin's election, and Russia's economic goals. While acknowledging the positive impact of the Russian taxation law, the essay explores queries regarding the rigidity of certain policies and the over-reliance on natural resource taxation. It suggests reshaping the taxation policy to tap into citizen's potential, drawing a comparison with the United States' taxation system. The essay also discusses the importance of research in tax administration, risk assessment, and regulatory enforcement to improve market surveillance and reduce corruption. It concludes by mentioning the Russian government's efforts to amend the tax code and broaden the power of legislative entities.

Running head: TAX LAW1

Tax Law

Student’s Name

Institutional Affiliation

Tax Law

Student’s Name

Institutional Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAX LAW 2

Tax Law

Introduction

The implementation of tax policy in a state is propagated by the government due to the

choices it makes as to the taxes it should charge its citizens thus covered in both the micro

economics and the macroeconomics fields1. In the macroeconomics part, taxation policy

concerns the entire amount of taxes that is supposed to be collected to affect the level of

economic activities in nation hence covers the aspect of fiscal policy in details. Furthermore, the

micro economics aspect as well talks about the issue of fairness in accordance to the type of

people that should be taxed and a locative efficiency. Similarly, implementation of the tax policy

has at times been a difficult business since there will be other concerned parties that will support

the initiative and the other will reject the proposal by all means despite the fact that it’s for the

better part of the countries wellbeing. On the hand, overreliance on the consumption taxes and

there is no avenue of the continuous personal income tax in many nations neutralizes the benefits

that the poor working class receive from refundable low income tax credits2. Moreover, in order

to have a strong, sustained and inclusive economic development, a reliable and good functioning

taxation policy system must be put in place since the revenue fund on the administrative

infrastructure and the public expenditure depends solemnly on the cost tax collected in the

1 Aivazian, S. and Brodsky, B., 2006. Macroeconometric modeling: modern trends, problems, an

example of the econometric model of the Russian economy. Applied econometrics, 2(2), pp.85-

111.

2 Granville, B. and Oppenheimer, P., 2001. Russia's post-communist economy. Oxford University

Press.

Tax Law

Introduction

The implementation of tax policy in a state is propagated by the government due to the

choices it makes as to the taxes it should charge its citizens thus covered in both the micro

economics and the macroeconomics fields1. In the macroeconomics part, taxation policy

concerns the entire amount of taxes that is supposed to be collected to affect the level of

economic activities in nation hence covers the aspect of fiscal policy in details. Furthermore, the

micro economics aspect as well talks about the issue of fairness in accordance to the type of

people that should be taxed and a locative efficiency. Similarly, implementation of the tax policy

has at times been a difficult business since there will be other concerned parties that will support

the initiative and the other will reject the proposal by all means despite the fact that it’s for the

better part of the countries wellbeing. On the hand, overreliance on the consumption taxes and

there is no avenue of the continuous personal income tax in many nations neutralizes the benefits

that the poor working class receive from refundable low income tax credits2. Moreover, in order

to have a strong, sustained and inclusive economic development, a reliable and good functioning

taxation policy system must be put in place since the revenue fund on the administrative

infrastructure and the public expenditure depends solemnly on the cost tax collected in the

1 Aivazian, S. and Brodsky, B., 2006. Macroeconometric modeling: modern trends, problems, an

example of the econometric model of the Russian economy. Applied econometrics, 2(2), pp.85-

111.

2 Granville, B. and Oppenheimer, P., 2001. Russia's post-communist economy. Oxford University

Press.

TAX LAW 3

nation. This essay is therefore set to critically analyze the Russian taxation law, express its

implication on economic growth and development, and discuss the relevant corrective measures

that can make the policy effective in promoting economic development while comparing the law

with the principles of the other nations across the globe.

Russian economic growth has changed more rapidly and unexpectedly due to the

implementation of the tax policy3. When Putin Vladimir was elected as the Russian people’s

president, the country was really suffering in the state of bankruptcy with plenty of depts. Russia

had obtained a virtual economic development and it becomes one of the huge creditors of the

U.S. debt across the globe.

In the beginning of 2009, the MET published a strategy that portrays Russian 2020

economic development goals and if the goals are to be put into actions or transformed to reality

then Russia would lead the economic stability in Europe and the fifth largest in the across the

globe being closely followed by the US, India, China, and Japan4. Despite the fact that the

Russian taxation law has enhanced economic growth and development in the country, several

queries circumnavigate the rigidity of some of the policies in Russia. The government of Russia

is pursuing policies that are likely to constrain the rate of growth and thus when one closely

examines its economy then there is need to put into consideration the current growth trends5.

Russia has never been more successful or integrated in the global economy like in the current

3 Orlova, M. and Khafizova, A., 2014. The tax component of innovative activity assessment in

the Russian Federation. Life Science Journal, 11(11), pp.328-333.

4 Lavrenchuk, E.N., 2013. Characteristics of taxes in Russian Federation. American Journal of

Economics and Control Systems Management, 2(2), pp.018-024

5

Gaddy, C.G. and Ickes, B.W., 2005. Resource rents and the Russian economy. Eurasian

Geography and Economics, 46(8), pp.559-583.

nation. This essay is therefore set to critically analyze the Russian taxation law, express its

implication on economic growth and development, and discuss the relevant corrective measures

that can make the policy effective in promoting economic development while comparing the law

with the principles of the other nations across the globe.

Russian economic growth has changed more rapidly and unexpectedly due to the

implementation of the tax policy3. When Putin Vladimir was elected as the Russian people’s

president, the country was really suffering in the state of bankruptcy with plenty of depts. Russia

had obtained a virtual economic development and it becomes one of the huge creditors of the

U.S. debt across the globe.

In the beginning of 2009, the MET published a strategy that portrays Russian 2020

economic development goals and if the goals are to be put into actions or transformed to reality

then Russia would lead the economic stability in Europe and the fifth largest in the across the

globe being closely followed by the US, India, China, and Japan4. Despite the fact that the

Russian taxation law has enhanced economic growth and development in the country, several

queries circumnavigate the rigidity of some of the policies in Russia. The government of Russia

is pursuing policies that are likely to constrain the rate of growth and thus when one closely

examines its economy then there is need to put into consideration the current growth trends5.

Russia has never been more successful or integrated in the global economy like in the current

3 Orlova, M. and Khafizova, A., 2014. The tax component of innovative activity assessment in

the Russian Federation. Life Science Journal, 11(11), pp.328-333.

4 Lavrenchuk, E.N., 2013. Characteristics of taxes in Russian Federation. American Journal of

Economics and Control Systems Management, 2(2), pp.018-024

5

Gaddy, C.G. and Ickes, B.W., 2005. Resource rents and the Russian economy. Eurasian

Geography and Economics, 46(8), pp.559-583.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAX LAW 4

state thus an achievement and a positive development in the in the Russian federation since the

collapse of the soviet republics.

Similarly, due to the stunning economic growth that has been propagated by the rising

prices of commodity and the cheap foreign credit, has attracted Russia an attractive seat of

foreign investment. The Organization for Economic Co- operation and Development (OECD)

focuses on establishing stable laws for better future life by initiating a platform that collects and

share ideas, knowledge and experiences thus finding solutions for common problems that is

facing majority of the countries6. OECD has better policies that provide an outline of the key

challenges that are being encountered by individual states and the primary principle

recommendation to curb them regarding the taxation operations.

Russia has made rapid development in minimizing the poverty levels and competing the

income level countries thus majority of the citizens have good paying jobs thus improving their

living standards. It is fundamental to realize the fact that the current development of the country

relies fundamentally on the revenue generated from taxation. Similarly, improvement in the

standards of living requires a low dependency on the natural resources, economy modernization

and ensuring a collaborative and reliable economic growth. Russia possess plenty assets that it

can depend on them to bring about of low debt, employee participation and numerous energy

resources since it has potential in areas like space technology and other untapped potentials in

the economy sector. Nevertheless, Russia face major policy challenges that may include:

financial sector, competition, fiscal framework, business framework, innovation, governance of

6 Silka, D.N., 2014. On priority measures for creating the basis for the development of the russian

economy. Life Science Journal, 11(7s), pp.310-313.

state thus an achievement and a positive development in the in the Russian federation since the

collapse of the soviet republics.

Similarly, due to the stunning economic growth that has been propagated by the rising

prices of commodity and the cheap foreign credit, has attracted Russia an attractive seat of

foreign investment. The Organization for Economic Co- operation and Development (OECD)

focuses on establishing stable laws for better future life by initiating a platform that collects and

share ideas, knowledge and experiences thus finding solutions for common problems that is

facing majority of the countries6. OECD has better policies that provide an outline of the key

challenges that are being encountered by individual states and the primary principle

recommendation to curb them regarding the taxation operations.

Russia has made rapid development in minimizing the poverty levels and competing the

income level countries thus majority of the citizens have good paying jobs thus improving their

living standards. It is fundamental to realize the fact that the current development of the country

relies fundamentally on the revenue generated from taxation. Similarly, improvement in the

standards of living requires a low dependency on the natural resources, economy modernization

and ensuring a collaborative and reliable economic growth. Russia possess plenty assets that it

can depend on them to bring about of low debt, employee participation and numerous energy

resources since it has potential in areas like space technology and other untapped potentials in

the economy sector. Nevertheless, Russia face major policy challenges that may include:

financial sector, competition, fiscal framework, business framework, innovation, governance of

6 Silka, D.N., 2014. On priority measures for creating the basis for the development of the russian

economy. Life Science Journal, 11(7s), pp.310-313.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAX LAW 5

the public enterprise, employment, social policies, health, education, energy, green policies and

agriculture7. Additionally, OECD focuses on creating the relationship and tightening the bond

with Russia through accessing process that facilitate in making the Russian economy modern,

vibrant and inclusive.

Russian economy tends to be modernized hence requires more effort to cover for it to

attain the living standards of the most advanced market oriented countries despite its tremendous

improvement in the economic growth in the previous years8. In order for it to narrow the gap, it

has to modernize the economy and reduce the rate of dependency of revenues from natural

resource extraction and thus focus on having abroad based growth that is sustainable. The bigger

crisis of the Russian taxation law revolves around emphasizing on the taxation of the natural

resources. Regarding such an ideology, Russia has potential to use its citizen’s great potential

and enhance economic growth beyond its natural resource utilization by reshaping the taxation

policy. A typical example of countries with stable taxation policies that cover wide areas of

citizen’s potential to generate revenue for economic development is the United States of

America. Russia would be more effective if it applies such principles in the taxation law.

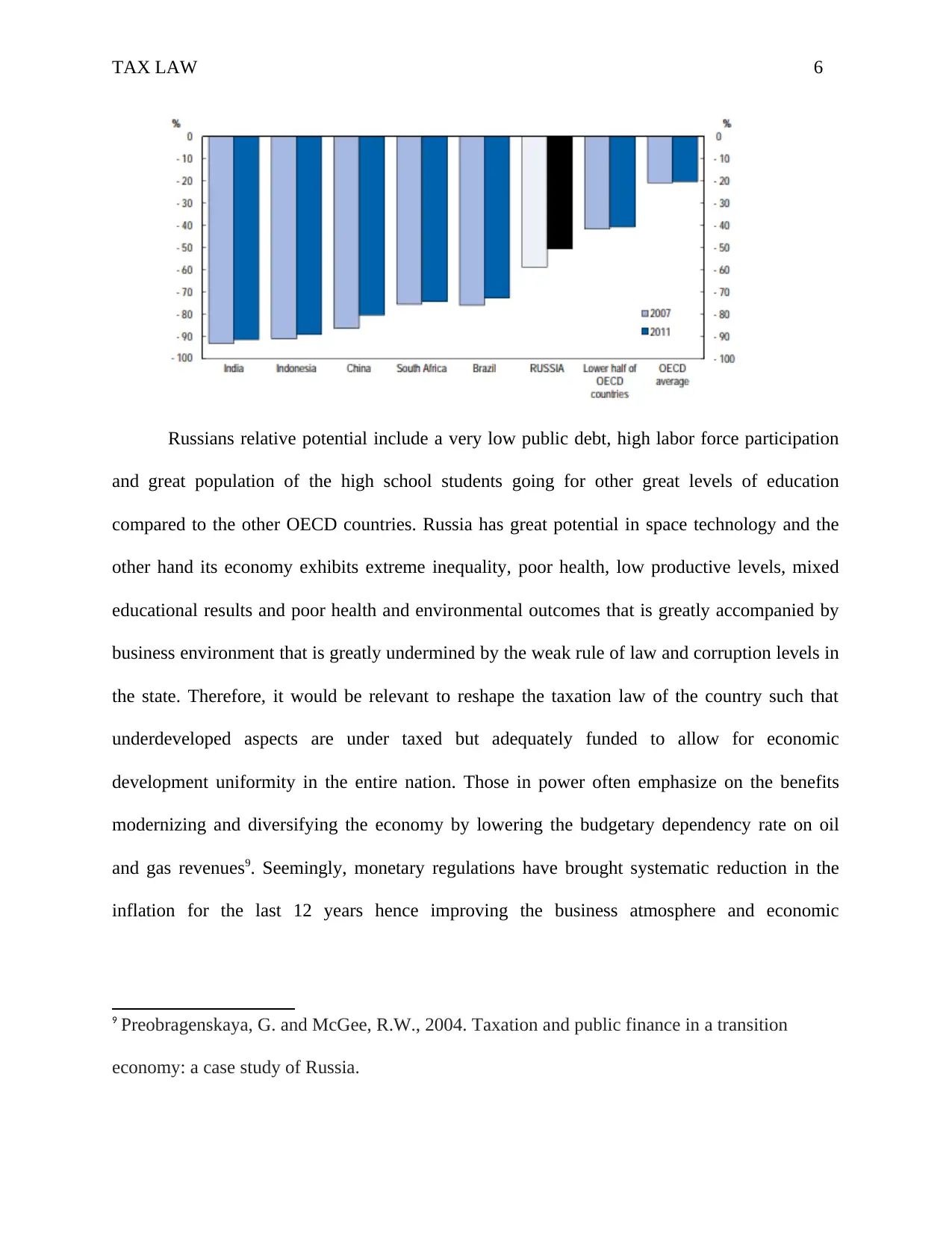

The figure below demonstrates the percentage of GDP per capital gap being equated with

the upper half of OECD states

7 Pogorletskiy, A.I. and Bashkirova, N.N., 2015. The dynamics of tax system and tax

administration development in the Russian Federation. Journal of Tax Reform. 2015. Т. 1.№

1, 1(1), pp.4-24.

8 King, C., 52004. A Rose among Thorns-Georgia Makes Good. Foreign Aff., 83, p.13.

the public enterprise, employment, social policies, health, education, energy, green policies and

agriculture7. Additionally, OECD focuses on creating the relationship and tightening the bond

with Russia through accessing process that facilitate in making the Russian economy modern,

vibrant and inclusive.

Russian economy tends to be modernized hence requires more effort to cover for it to

attain the living standards of the most advanced market oriented countries despite its tremendous

improvement in the economic growth in the previous years8. In order for it to narrow the gap, it

has to modernize the economy and reduce the rate of dependency of revenues from natural

resource extraction and thus focus on having abroad based growth that is sustainable. The bigger

crisis of the Russian taxation law revolves around emphasizing on the taxation of the natural

resources. Regarding such an ideology, Russia has potential to use its citizen’s great potential

and enhance economic growth beyond its natural resource utilization by reshaping the taxation

policy. A typical example of countries with stable taxation policies that cover wide areas of

citizen’s potential to generate revenue for economic development is the United States of

America. Russia would be more effective if it applies such principles in the taxation law.

The figure below demonstrates the percentage of GDP per capital gap being equated with

the upper half of OECD states

7 Pogorletskiy, A.I. and Bashkirova, N.N., 2015. The dynamics of tax system and tax

administration development in the Russian Federation. Journal of Tax Reform. 2015. Т. 1.№

1, 1(1), pp.4-24.

8 King, C., 52004. A Rose among Thorns-Georgia Makes Good. Foreign Aff., 83, p.13.

TAX LAW 6

Russians relative potential include a very low public debt, high labor force participation

and great population of the high school students going for other great levels of education

compared to the other OECD countries. Russia has great potential in space technology and the

other hand its economy exhibits extreme inequality, poor health, low productive levels, mixed

educational results and poor health and environmental outcomes that is greatly accompanied by

business environment that is greatly undermined by the weak rule of law and corruption levels in

the state. Therefore, it would be relevant to reshape the taxation law of the country such that

underdeveloped aspects are under taxed but adequately funded to allow for economic

development uniformity in the entire nation. Those in power often emphasize on the benefits

modernizing and diversifying the economy by lowering the budgetary dependency rate on oil

and gas revenues9. Seemingly, monetary regulations have brought systematic reduction in the

inflation for the last 12 years hence improving the business atmosphere and economic

9 Preobragenskaya, G. and McGee, R.W., 2004. Taxation and public finance in a transition

economy: a case study of Russia.

Russians relative potential include a very low public debt, high labor force participation

and great population of the high school students going for other great levels of education

compared to the other OECD countries. Russia has great potential in space technology and the

other hand its economy exhibits extreme inequality, poor health, low productive levels, mixed

educational results and poor health and environmental outcomes that is greatly accompanied by

business environment that is greatly undermined by the weak rule of law and corruption levels in

the state. Therefore, it would be relevant to reshape the taxation law of the country such that

underdeveloped aspects are under taxed but adequately funded to allow for economic

development uniformity in the entire nation. Those in power often emphasize on the benefits

modernizing and diversifying the economy by lowering the budgetary dependency rate on oil

and gas revenues9. Seemingly, monetary regulations have brought systematic reduction in the

inflation for the last 12 years hence improving the business atmosphere and economic

9 Preobragenskaya, G. and McGee, R.W., 2004. Taxation and public finance in a transition

economy: a case study of Russia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAX LAW 7

performance by stabilizing regulations, reducing the rate of corruption and expanding the

competition levels through a less bureaucratic product market policy.

Effective research in the tax administration provides natural context of cross disciplinary

study as it functions at the intersection of several disciplines. There are also significant benefits

on the research outputs and the impacts thus providing developing frame works and measure of

good tax administration practice. On the hand monitoring, evaluation of program effectiveness

and risk assessment are one of the effective procedures to ensure that the ethics and the rule of

law are followed. This is practically done by monitoring and auditing to realize criminal

operations or the individuals that are not compliant to the tax policies in the state10. Periodically

the risk assessment is done to recognize criminal conduct and to establish publicize strategies

that allows anonymous and a very confidential reporting that will facilitate the agents and

employees to report or sort for assistance on the issue pertaining criminal conduct without the

retaliation feeling.

They are regulatory standards that will be implemented and enforced on regular basis

through a well-publicized and accessible disciplinary measures and guidelines. There is response

that will be put into place to detect criminal offenses and corrective action plans have already

been put into place through appropriate disciplinary mechanism to prevent similar

occurrence11.The criminal conducts are supposed to be conveyed and the organizations should

10 Gorodnichenko, Y., Martinez-Vazquez, J. and Sabirianova Peter, K., 2009. Myth and reality of

flat tax reform: Micro estimates of tax evasion response and welfare effects in Russia. Journal of

Political economy, 117(3), pp.504-554.

11 Bykov, S.S., 2012. The role of counteraction against tax evasion in the Russian tax law

system. Nalogi i finansovoe pravo–Taxes and Financial Law, (9), pp.124-129.

performance by stabilizing regulations, reducing the rate of corruption and expanding the

competition levels through a less bureaucratic product market policy.

Effective research in the tax administration provides natural context of cross disciplinary

study as it functions at the intersection of several disciplines. There are also significant benefits

on the research outputs and the impacts thus providing developing frame works and measure of

good tax administration practice. On the hand monitoring, evaluation of program effectiveness

and risk assessment are one of the effective procedures to ensure that the ethics and the rule of

law are followed. This is practically done by monitoring and auditing to realize criminal

operations or the individuals that are not compliant to the tax policies in the state10. Periodically

the risk assessment is done to recognize criminal conduct and to establish publicize strategies

that allows anonymous and a very confidential reporting that will facilitate the agents and

employees to report or sort for assistance on the issue pertaining criminal conduct without the

retaliation feeling.

They are regulatory standards that will be implemented and enforced on regular basis

through a well-publicized and accessible disciplinary measures and guidelines. There is response

that will be put into place to detect criminal offenses and corrective action plans have already

been put into place through appropriate disciplinary mechanism to prevent similar

occurrence11.The criminal conducts are supposed to be conveyed and the organizations should

10 Gorodnichenko, Y., Martinez-Vazquez, J. and Sabirianova Peter, K., 2009. Myth and reality of

flat tax reform: Micro estimates of tax evasion response and welfare effects in Russia. Journal of

Political economy, 117(3), pp.504-554.

11 Bykov, S.S., 2012. The role of counteraction against tax evasion in the Russian tax law

system. Nalogi i finansovoe pravo–Taxes and Financial Law, (9), pp.124-129.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAX LAW 8

work closely with the statutory administrative to ensure justice is delivered and no individual

should evade paying taxes despite the authority or influence he has with the citizens or the

government in place12. Thus the compliance program should be amended in order to prevent any

criminal act from erupting.

The Russian government has put more efforts and embarked on forming regulatory

enforcement systems and business inspections devices to improve the market surveillance

outcome while moving away from unnecessary regulations, rent seeking behavior and inefficient

enforcement. It is important to do the business reports in order to simplify and streamline

business processes to avoid any form of malpractice that may be going on. Similarly, the

introduction of electronic services has reduced the levels of in person interaction between

businesses and government agencies which intern will reduce the possible possibility for

corruption and thus focus on increasing the level of efficiency and transparency in business

services.

Some of the challenges in the Russian taxation law have been addressed within the

Russian Taxation Bill13. The Russian government has handed over to the State of Duma a bill

that amends chapters of Russian tax code that outlines special tax regime that involves the

Simplified Taxation System, Patent Taxation System and Imputed Income Tax14. Moreover, the

bill has to undergo the standard legislative process for it to be effective. In the Russia

12 Kotsonis, Y., 2004. “Face-to-Face”: The State, the Individual, and the Citizen in Russian

Taxation, 1863-1917. Slavic Review, 63(2), pp.221-246.

13 Aguzarova, F.S., 2014. On changes in the Russian tax law. Finance and credit, (21), pp.46-51.

14 Stepanyan, V., 2003. Reforming tax systems: experience of the Baltics, Russia, and other

countries of the former Soviet Union (No. 3-173). International Monetary Fund.

work closely with the statutory administrative to ensure justice is delivered and no individual

should evade paying taxes despite the authority or influence he has with the citizens or the

government in place12. Thus the compliance program should be amended in order to prevent any

criminal act from erupting.

The Russian government has put more efforts and embarked on forming regulatory

enforcement systems and business inspections devices to improve the market surveillance

outcome while moving away from unnecessary regulations, rent seeking behavior and inefficient

enforcement. It is important to do the business reports in order to simplify and streamline

business processes to avoid any form of malpractice that may be going on. Similarly, the

introduction of electronic services has reduced the levels of in person interaction between

businesses and government agencies which intern will reduce the possible possibility for

corruption and thus focus on increasing the level of efficiency and transparency in business

services.

Some of the challenges in the Russian taxation law have been addressed within the

Russian Taxation Bill13. The Russian government has handed over to the State of Duma a bill

that amends chapters of Russian tax code that outlines special tax regime that involves the

Simplified Taxation System, Patent Taxation System and Imputed Income Tax14. Moreover, the

bill has to undergo the standard legislative process for it to be effective. In the Russia

12 Kotsonis, Y., 2004. “Face-to-Face”: The State, the Individual, and the Citizen in Russian

Taxation, 1863-1917. Slavic Review, 63(2), pp.221-246.

13 Aguzarova, F.S., 2014. On changes in the Russian tax law. Finance and credit, (21), pp.46-51.

14 Stepanyan, V., 2003. Reforming tax systems: experience of the Baltics, Russia, and other

countries of the former Soviet Union (No. 3-173). International Monetary Fund.

TAX LAW 9

government system, the power of legislative comprise of the entities and representative

authorities of the municipal entities which need to be broadened. Those authorities in place

independently determine the variety of entrepreneur activities to which Special Tax regime may

be implemented by establishing tax benefits, tax rates and the thresholds.

This kind of taxation system in Russia is simplified in way that when the amount of

income is taxed, the tax rate could drop from 6% to 1% and for the tax payers the difference

between the income and the expenditure will be 5% -15% that will be constant15. Freshly

registered individuals providing consumer services will be paying taxes for the first2 years of

engaging in business since the law in place only provides beneficiaries to those individuals that

are involved in the production, social and scientific activities.

Finally, for Imputed Income Tax, the legislative authority of Moscow Sevastpol and St

Peterburg will have the authority and mandate to reduce the current rate of tax from 15% - 7.5%

on income imputed. Nevertheless, the patent taxation system has a series of activities in the

extension list that may include software development, software adaptation, computer repair,

waste disposal, production of milk and bread16. When considering the case of simplified taxation

system, the bill supports the newly- registered sole proprietors who provide consumer services

not to pay taxes for the first two years hence several small businesses will get a lot of tax benefits

compared to the large business operatives. Such a strategy is very significant in promoting the

development of the infant companies in the country. The strategy also helps to enhance

competition rather than promoting monopoly that may hinder the entry of new entrants in the

15 Alexeev, M. and Conrad, R.F., 2013. The Russian Tax System. In The Oxford Handbook of the

Russian Economy.

16 Carragher, N. and Chalmers, J., 2011. What are the options? Pricing and taxation policy

reforms to redress excessive alcohol consumption and related harms in Australia.

government system, the power of legislative comprise of the entities and representative

authorities of the municipal entities which need to be broadened. Those authorities in place

independently determine the variety of entrepreneur activities to which Special Tax regime may

be implemented by establishing tax benefits, tax rates and the thresholds.

This kind of taxation system in Russia is simplified in way that when the amount of

income is taxed, the tax rate could drop from 6% to 1% and for the tax payers the difference

between the income and the expenditure will be 5% -15% that will be constant15. Freshly

registered individuals providing consumer services will be paying taxes for the first2 years of

engaging in business since the law in place only provides beneficiaries to those individuals that

are involved in the production, social and scientific activities.

Finally, for Imputed Income Tax, the legislative authority of Moscow Sevastpol and St

Peterburg will have the authority and mandate to reduce the current rate of tax from 15% - 7.5%

on income imputed. Nevertheless, the patent taxation system has a series of activities in the

extension list that may include software development, software adaptation, computer repair,

waste disposal, production of milk and bread16. When considering the case of simplified taxation

system, the bill supports the newly- registered sole proprietors who provide consumer services

not to pay taxes for the first two years hence several small businesses will get a lot of tax benefits

compared to the large business operatives. Such a strategy is very significant in promoting the

development of the infant companies in the country. The strategy also helps to enhance

competition rather than promoting monopoly that may hinder the entry of new entrants in the

15 Alexeev, M. and Conrad, R.F., 2013. The Russian Tax System. In The Oxford Handbook of the

Russian Economy.

16 Carragher, N. and Chalmers, J., 2011. What are the options? Pricing and taxation policy

reforms to redress excessive alcohol consumption and related harms in Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAX LAW 10

country. In so doing, the development of the industrial sector and infrastructure of the economy

is enhanced through the expanded business operation.

Usually, foreign investors are exploitative to the economic development of an economy

as they carry their revenues back to the home countries. Therefore, the ideology of overtaxing

the huge companies in the country focus majorly on the foreign huge firms which should

contribute fully to the economic development of the country by compensating for the utilization

of the available resources. The funds raised from taxation of such companies are further utilized

in the economic development of the nation.

Russia has been on the run of building modern fiscal institutions that has basically been

formed tax system. The annual results have been over the last twelve years and the public

financial assets have greatly exceeded the gross public debt as compared to the most OECD

countries. Nevertheless, the fiscal policy has continually encountered a lot of major challenges

and shortages that is connected to the Russian natural resource wealth, real exchange rate

volatility and notably commodity of prices. The challenge has been intergenerational equity, pro-

growth and social spending and optimal balance between fiscal stability. The additional

challenge rendered in the fiscal policy is the uneven distribution of wealth and extremely high

levels of income inequality that have slightly reduced due to tax and benefit systems.

The outcome of fiscal policy improved tremendously in the past ten years as compared to

the 1998 period that leads to the government partial collapse17. These has been reflected by the

rising prices of oil and the initial commitment to restrain the amount of expenditure that have no

fundamental gains and this aspect has been seconded by the institutional mechanism that

17 Desai, R., Freinkman, L.M. and Goldberg, I., 2003. Fiscal federalism and regional growth:

Evidence from the Russian Federation in the 1990s. The World Bank.

country. In so doing, the development of the industrial sector and infrastructure of the economy

is enhanced through the expanded business operation.

Usually, foreign investors are exploitative to the economic development of an economy

as they carry their revenues back to the home countries. Therefore, the ideology of overtaxing

the huge companies in the country focus majorly on the foreign huge firms which should

contribute fully to the economic development of the country by compensating for the utilization

of the available resources. The funds raised from taxation of such companies are further utilized

in the economic development of the nation.

Russia has been on the run of building modern fiscal institutions that has basically been

formed tax system. The annual results have been over the last twelve years and the public

financial assets have greatly exceeded the gross public debt as compared to the most OECD

countries. Nevertheless, the fiscal policy has continually encountered a lot of major challenges

and shortages that is connected to the Russian natural resource wealth, real exchange rate

volatility and notably commodity of prices. The challenge has been intergenerational equity, pro-

growth and social spending and optimal balance between fiscal stability. The additional

challenge rendered in the fiscal policy is the uneven distribution of wealth and extremely high

levels of income inequality that have slightly reduced due to tax and benefit systems.

The outcome of fiscal policy improved tremendously in the past ten years as compared to

the 1998 period that leads to the government partial collapse17. These has been reflected by the

rising prices of oil and the initial commitment to restrain the amount of expenditure that have no

fundamental gains and this aspect has been seconded by the institutional mechanism that

17 Desai, R., Freinkman, L.M. and Goldberg, I., 2003. Fiscal federalism and regional growth:

Evidence from the Russian Federation in the 1990s. The World Bank.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAX LAW 11

manages wealth resource. Russia has put into place associations that promote annual policy and

the primary features of budgetary formulation that has OECD best practice interest18. Measures

that have been put in place for the three-year budget are: fiscal reporting, macroeconomics

forecasting, limiting the scope by parliament budgetary amendments and financial risking.

Therefore, the current efforts undertaken by Russia regarding the fiscal policy concept are

promising while interpreting the ideology of taxation law in correlation with the economic

growth and development of the nation.

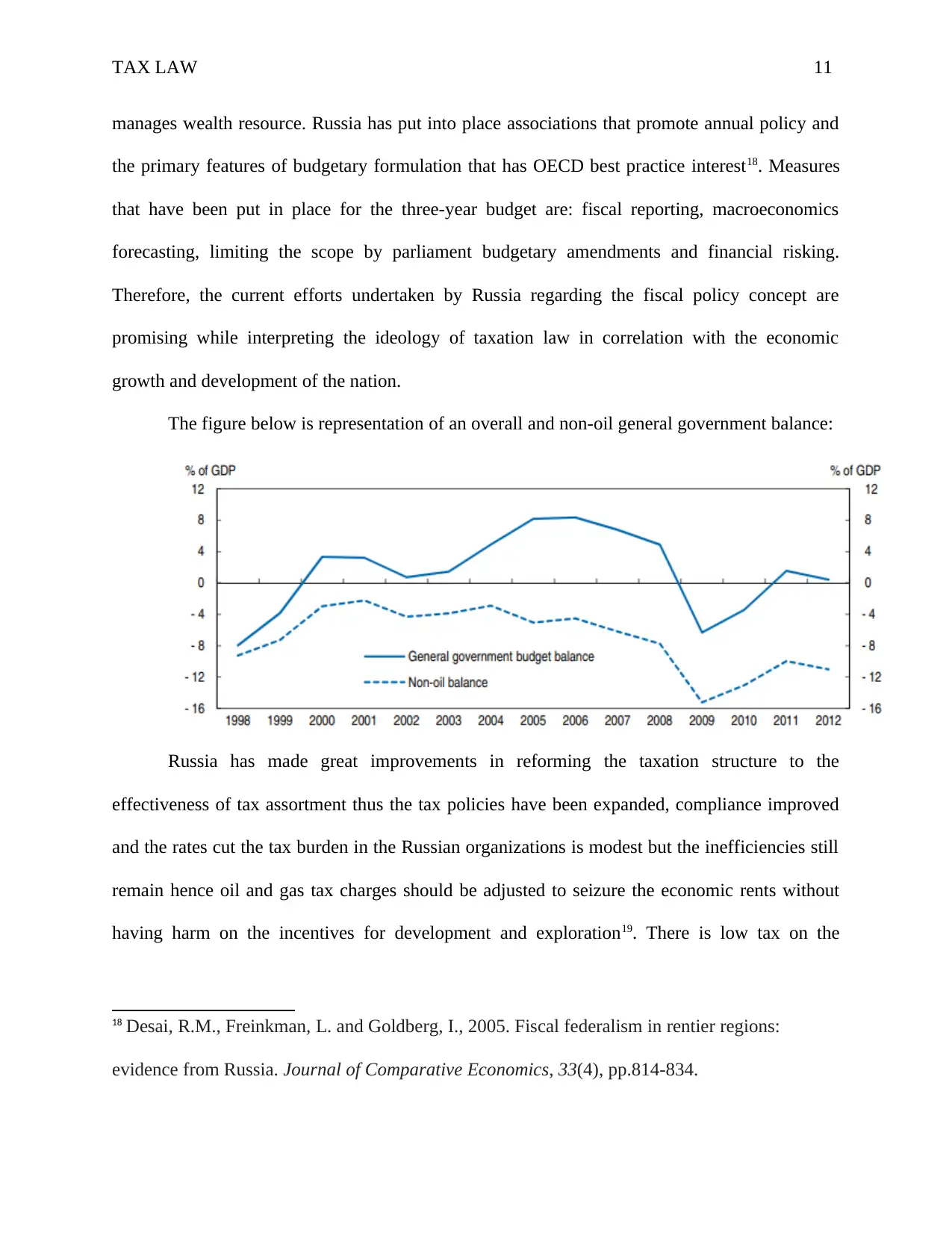

The figure below is representation of an overall and non-oil general government balance:

Russia has made great improvements in reforming the taxation structure to the

effectiveness of tax assortment thus the tax policies have been expanded, compliance improved

and the rates cut the tax burden in the Russian organizations is modest but the inefficiencies still

remain hence oil and gas tax charges should be adjusted to seizure the economic rents without

having harm on the incentives for development and exploration19. There is low tax on the

18 Desai, R.M., Freinkman, L. and Goldberg, I., 2005. Fiscal federalism in rentier regions:

evidence from Russia. Journal of Comparative Economics, 33(4), pp.814-834.

manages wealth resource. Russia has put into place associations that promote annual policy and

the primary features of budgetary formulation that has OECD best practice interest18. Measures

that have been put in place for the three-year budget are: fiscal reporting, macroeconomics

forecasting, limiting the scope by parliament budgetary amendments and financial risking.

Therefore, the current efforts undertaken by Russia regarding the fiscal policy concept are

promising while interpreting the ideology of taxation law in correlation with the economic

growth and development of the nation.

The figure below is representation of an overall and non-oil general government balance:

Russia has made great improvements in reforming the taxation structure to the

effectiveness of tax assortment thus the tax policies have been expanded, compliance improved

and the rates cut the tax burden in the Russian organizations is modest but the inefficiencies still

remain hence oil and gas tax charges should be adjusted to seizure the economic rents without

having harm on the incentives for development and exploration19. There is low tax on the

18 Desai, R.M., Freinkman, L. and Goldberg, I., 2005. Fiscal federalism in rentier regions:

evidence from Russia. Journal of Comparative Economics, 33(4), pp.814-834.

TAX LAW 12

corporate profits due to the 20% cut, but any possibility of further reduction cannot be ruled out

despite that indirect taxation on products that can be increased20

The Russian taxation law can also be made more effective in enhancing economic growth

and development through the execution of the OECD recommendation. The major OECD

recommendation include: further reformation of the taxation system by enlightening the rate of

taxation of rents from the natural resource utilization hence shifts the tax charges from labor

income to indirect taxation and decreasing the entire framework and workability21. Similarly, it

forms a broad and robust agreement around the freshly formed prices of oil to protect the

economy from price inflation. Furthermore, there will be need to increase budget limpidity to

avoid eruption of additional financial plans and support the executions of performance budget

reform. On the other hand, it addresses the weakness or failure in the municipal and regional

funding regimes that promote the answerability for economic development and regional levels

making federal annual relations more rule based.

Russia can easily be compared to other nations regarding the taxation law concept

following the aspect of the economic growth due taxation. Russia is ranked top 20 worldwide on

these two indicators that include: property registration and enforcing contracts thus it takes less

19 Gordon, R. ed., 2010. Taxation in Developing Countries: Six Case Studies and Policy

Implications. Columbia University Press.

20 Krasovsky, K.S., 2010. " The lobbying strategy is to keep excise as low as possible"-tobacco

industry excise taxation policy in Ukraine. Tobacco induced diseases, 8(1), p.10.

21 Weinthal, E. and Luong, P.J., 2001. Energy wealth and tax reform in Russia and

Kazakhstan. Resources Policy, 27(4), pp.215-223.

corporate profits due to the 20% cut, but any possibility of further reduction cannot be ruled out

despite that indirect taxation on products that can be increased20

The Russian taxation law can also be made more effective in enhancing economic growth

and development through the execution of the OECD recommendation. The major OECD

recommendation include: further reformation of the taxation system by enlightening the rate of

taxation of rents from the natural resource utilization hence shifts the tax charges from labor

income to indirect taxation and decreasing the entire framework and workability21. Similarly, it

forms a broad and robust agreement around the freshly formed prices of oil to protect the

economy from price inflation. Furthermore, there will be need to increase budget limpidity to

avoid eruption of additional financial plans and support the executions of performance budget

reform. On the other hand, it addresses the weakness or failure in the municipal and regional

funding regimes that promote the answerability for economic development and regional levels

making federal annual relations more rule based.

Russia can easily be compared to other nations regarding the taxation law concept

following the aspect of the economic growth due taxation. Russia is ranked top 20 worldwide on

these two indicators that include: property registration and enforcing contracts thus it takes less

19 Gordon, R. ed., 2010. Taxation in Developing Countries: Six Case Studies and Policy

Implications. Columbia University Press.

20 Krasovsky, K.S., 2010. " The lobbying strategy is to keep excise as low as possible"-tobacco

industry excise taxation policy in Ukraine. Tobacco induced diseases, 8(1), p.10.

21 Weinthal, E. and Luong, P.J., 2001. Energy wealth and tax reform in Russia and

Kazakhstan. Resources Policy, 27(4), pp.215-223.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.