Management Accounting Report: Costing and Budgeting for Ryanair

VerifiedAdded on 2020/10/05

|14

|3910

|422

Report

AI Summary

This report provides a detailed analysis of management accounting principles as applied to Ryanair, a major player in the aviation industry. It begins by defining management accounting, its different systems, and various methods of accounting reporting, specifically within the context of Ryanair's business operations. The report then delves into a comparative analysis of marginal and absorption costing techniques to determine the cost per unit for Ryanair, evaluating which method yields a more favorable outcome for the company. Furthermore, the report examines different planning tools used for budgetary control, outlining their respective advantages and disadvantages. Finally, it presents a report on the organizational adaptation of Ryanair's management accounting system, comparing it to that of Easyjet to highlight industry best practices and strategic differences.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Defining management accounting and its different accounting systems ............................3

P2. Different methods of management accounting reporting.....................................................5

TASK 2 ...........................................................................................................................................6

P.3 determination of cost per unit of Ryanair from marginal and absorption costing techniques

.....................................................................................................................................................6

TASK 3............................................................................................................................................8

P.4 Different types of planning tools for budgetary control and their advantages and

disadvantages..............................................................................................................................8

TASK 4..........................................................................................................................................11

P.5 Report on organisational adaptation of management accounting system and comparison

with Two Easy jet Airline.........................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Defining management accounting and its different accounting systems ............................3

P2. Different methods of management accounting reporting.....................................................5

TASK 2 ...........................................................................................................................................6

P.3 determination of cost per unit of Ryanair from marginal and absorption costing techniques

.....................................................................................................................................................6

TASK 3............................................................................................................................................8

P.4 Different types of planning tools for budgetary control and their advantages and

disadvantages..............................................................................................................................8

TASK 4..........................................................................................................................................11

P.5 Report on organisational adaptation of management accounting system and comparison

with Two Easy jet Airline.........................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a process of consideration of financial and non-financial

information by managers for decision making. To manage the overall business of an

organisation, people at top level have to consider and take decision in respect of different

functional areas. For the decision making process, they need all the relevant information which is

provided by various accounting reports. In this assignment, a discussion about the management

accounting, its different types of systems and methods of accounting reporting are done for the

aviation business of RAYNAIR. Further, a comparison of income statements as per marginal and

absorption costing is done to know which option is better and shall be taken into consideration.

An in-depth evaluation is carried out to control budgets by analysing different types of planning

tools. Also, comparison with different organisations is done to see how different firms are

adapting management accounting.

TASK 1

P1. Defining management accounting and its different accounting systems

Management accounting can be defined as a part of the accounting system of a business.

It is a process of preparation of management and accounting reports that provides accurate and

appropriate financial and statistical information to the management. This information helps the

management to take day to day decisions.

The management accounting reports give a detailed information about the availability of

cash and cash equivalents, sales revenues, status of accounts receivables and payables, inventory,

raw material and debtors.

Management accounting is a technique which considers only relevant data and

information (Cooper, Ezzamel and Qu, 2017). There is no set format for information that passes

the same to management. This provides the management with data and information not with

decision. This mainly focuses on the future of company and analyses different variables.

The scope of management accounting is vast. It includes all the information that has to be

provided to the management for financial analysis and interpretation of operations of the

business. It includes financial and cost accounting, budgeting and forecasting, cost control

procedures, reporting, methods and procedures to use its resources, tax accounting, internal

Management accounting is a process of consideration of financial and non-financial

information by managers for decision making. To manage the overall business of an

organisation, people at top level have to consider and take decision in respect of different

functional areas. For the decision making process, they need all the relevant information which is

provided by various accounting reports. In this assignment, a discussion about the management

accounting, its different types of systems and methods of accounting reporting are done for the

aviation business of RAYNAIR. Further, a comparison of income statements as per marginal and

absorption costing is done to know which option is better and shall be taken into consideration.

An in-depth evaluation is carried out to control budgets by analysing different types of planning

tools. Also, comparison with different organisations is done to see how different firms are

adapting management accounting.

TASK 1

P1. Defining management accounting and its different accounting systems

Management accounting can be defined as a part of the accounting system of a business.

It is a process of preparation of management and accounting reports that provides accurate and

appropriate financial and statistical information to the management. This information helps the

management to take day to day decisions.

The management accounting reports give a detailed information about the availability of

cash and cash equivalents, sales revenues, status of accounts receivables and payables, inventory,

raw material and debtors.

Management accounting is a technique which considers only relevant data and

information (Cooper, Ezzamel and Qu, 2017). There is no set format for information that passes

the same to management. This provides the management with data and information not with

decision. This mainly focuses on the future of company and analyses different variables.

The scope of management accounting is vast. It includes all the information that has to be

provided to the management for financial analysis and interpretation of operations of the

business. It includes financial and cost accounting, budgeting and forecasting, cost control

procedures, reporting, methods and procedures to use its resources, tax accounting, internal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial control, interpretation of financial data, office services as well as evaluation of

performance by management.

Therefore, it can be concluded that management accounting is not only a tool for

evaluation, it also provides methods and techniques to management of overall business of the

organisation.

Different types of management accounting systems:

The accounting systems are designed to give management a variety of information based

on their information needs for decision making. These are:

Cost accounting system

Inventory management system

Job costing system

Price optimisation system

Cost accounting system: It is a system to estimate the cost of product for evaluating

profits of the organisation. Inventory valuation and cost control is also a part of this system. This

aids the management in measuring financial performance of the company. It classifies cost

according to information need of the management. A firm must know which product is profitable

and which ones are not (Liu and Kuang, 2014). It helps in estimating the closing value of

material inventory, work in progress and finished goods for the purpose of preparation of

financial statements. The two main cost accounting systems are job order costing and process

costing. RYANAIR has kept its operating cost low for aircraft equipment, personnel expenses,

customer services cost and aircraft access as well as handling cost which ensure a good profit

margin.

Inventory management system: An inventory management system is the combination of

procedures and processes to monitor and maintain the stocked products of an organisation. This

is system of properly maintaining the inventory from the stage of its manufacturing up to the

stage of its sale to consumers (FKlychova and et.al., 2014). To maintain proper inventory is a

challenge for companies and for this, a proper channel is followed to keep an eye on the

inventories. This is done for raw material, work in progress and finished goods. Ryanair has

maintained its inventory by purchasing a new aircraft.

Job costing system: This a method of recording the costs of manufacturing job rather

than process. With job costing system, the managers keep a record of costs of each job which is

performance by management.

Therefore, it can be concluded that management accounting is not only a tool for

evaluation, it also provides methods and techniques to management of overall business of the

organisation.

Different types of management accounting systems:

The accounting systems are designed to give management a variety of information based

on their information needs for decision making. These are:

Cost accounting system

Inventory management system

Job costing system

Price optimisation system

Cost accounting system: It is a system to estimate the cost of product for evaluating

profits of the organisation. Inventory valuation and cost control is also a part of this system. This

aids the management in measuring financial performance of the company. It classifies cost

according to information need of the management. A firm must know which product is profitable

and which ones are not (Liu and Kuang, 2014). It helps in estimating the closing value of

material inventory, work in progress and finished goods for the purpose of preparation of

financial statements. The two main cost accounting systems are job order costing and process

costing. RYANAIR has kept its operating cost low for aircraft equipment, personnel expenses,

customer services cost and aircraft access as well as handling cost which ensure a good profit

margin.

Inventory management system: An inventory management system is the combination of

procedures and processes to monitor and maintain the stocked products of an organisation. This

is system of properly maintaining the inventory from the stage of its manufacturing up to the

stage of its sale to consumers (FKlychova and et.al., 2014). To maintain proper inventory is a

challenge for companies and for this, a proper channel is followed to keep an eye on the

inventories. This is done for raw material, work in progress and finished goods. Ryanair has

maintained its inventory by purchasing a new aircraft.

Job costing system: This a method of recording the costs of manufacturing job rather

than process. With job costing system, the managers keep a record of costs of each job which is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

relevant to operations of business. This system accumulates information about the costs

associated with a specific product or job. This helps in accurately determining cost of a product

and can quote the price accordingly. This information can be used to assign inventory costs to

manufacture goods. Ryanair has reduced its labour cost to increase the profits.

Price optimisation system: It is s system to adapt a best price for product /service of an

organisation. Price optimization means the way in which consumers will react to a particular

price for a particular product. The Ryanair has reduced the prices of meal on board, this will

increase the profits.

P2. Different methods of management accounting reporting

Management accounting reports are used for planning, regulating decision making and

measuring the performance. These reports are generated to analyse useful information for the use

of management. These reports are:

Budget report: The budget managerial accounting report is very important for

measuring company’s performance. These are generated department wise and for whole of the

organisation. The budget report is made on estimates of previous period and experiences

(Chenhall and Moers 2015). A great budget always caters for unforeseen circumstances and

contingencies that might arise in the future. A company's budget considers all the sources of

revenue and expenditures. A budget is prepared to achieve the mission and goal of the business

with the budgeted amount. These reports guide the managers to offer better employment

incentives, cut the cost and renegotiate them with suppliers.

Account receivable report: A business generally extends its business on credits. So,

accounts receivables report is vital for a business which rely heavily on credits. Breaking down

remaining balance of clients into specific time period allows the managers to identify defaulters

as well as issues in collection process. In case the list of defaulters is increasing, company shall

change its credit policies and make it more rigid. If creditors don't pay on time, business will not

be left with any operational money as well as working capital. Proper functioning of a business

can be assured by timely checking the defaulters.

Cost reports: This is a report which calculates the cost of products that are manufactured

or services which are provided. The cost of raw material, direct expenses, administrative

expenses and any other costs are into consideration. The total cost is divided by the amounts of

products produced. The cost report clearly reflects the actual cost of production of the product

associated with a specific product or job. This helps in accurately determining cost of a product

and can quote the price accordingly. This information can be used to assign inventory costs to

manufacture goods. Ryanair has reduced its labour cost to increase the profits.

Price optimisation system: It is s system to adapt a best price for product /service of an

organisation. Price optimization means the way in which consumers will react to a particular

price for a particular product. The Ryanair has reduced the prices of meal on board, this will

increase the profits.

P2. Different methods of management accounting reporting

Management accounting reports are used for planning, regulating decision making and

measuring the performance. These reports are generated to analyse useful information for the use

of management. These reports are:

Budget report: The budget managerial accounting report is very important for

measuring company’s performance. These are generated department wise and for whole of the

organisation. The budget report is made on estimates of previous period and experiences

(Chenhall and Moers 2015). A great budget always caters for unforeseen circumstances and

contingencies that might arise in the future. A company's budget considers all the sources of

revenue and expenditures. A budget is prepared to achieve the mission and goal of the business

with the budgeted amount. These reports guide the managers to offer better employment

incentives, cut the cost and renegotiate them with suppliers.

Account receivable report: A business generally extends its business on credits. So,

accounts receivables report is vital for a business which rely heavily on credits. Breaking down

remaining balance of clients into specific time period allows the managers to identify defaulters

as well as issues in collection process. In case the list of defaulters is increasing, company shall

change its credit policies and make it more rigid. If creditors don't pay on time, business will not

be left with any operational money as well as working capital. Proper functioning of a business

can be assured by timely checking the defaulters.

Cost reports: This is a report which calculates the cost of products that are manufactured

or services which are provided. The cost of raw material, direct expenses, administrative

expenses and any other costs are into consideration. The total cost is divided by the amounts of

products produced. The cost report clearly reflects the actual cost of production of the product

and its sell ling price. Through this report profits margins are estimated and monitored, as this

provide a clear picture of pricing of the each product. The cost determined are inventory waste

cost, hourly labour cost and overhead costs.

Performance reports: This report evaluate the overall performance of the company and

also of the individual employees, managers and directors on the company at the end of a term.

The reports are also generated for each departments to evaluate there performances. These

reports helps manager in making strategic decisions about the performance and futures of the

organisation. And also deals with the problems related to personnel of the organisation. This

report point outs the flaws in the area where the performance is not up to the mark. This report

keeps an accurate measure of the strategies to achieve the mission of the organisation.

Project reports: The project report is prepared to keep a close look on the projects

undertaken by the organisation. The details of particular projects are mentioned in the reports.

For different projects different reports are prepared and sometimes a combine report is also

prepared. This shows the details like what is the projects, when it is assigned, when is the

deadline, what are the resources used and required for completion of the project. It also evaluates

the finished projects that hoe the project is working and what are the problems coming in

performance of such projects.

Activity reports: This report is related to the various activities performed within an

organisation. It shows the day to day activities in relation to the operational performance of the

business. The day to day activities are production related, employment related

Other reports: The other information reports are, report on analysis of competitors,

report on the debtors and their managements. These reports play a vital role in the performance

ans success of the company as they analyse ans evaluate key functional area of a business.

TASK 2

P.3 determination of cost per unit of Ryanair from marginal and absorption costing techniques

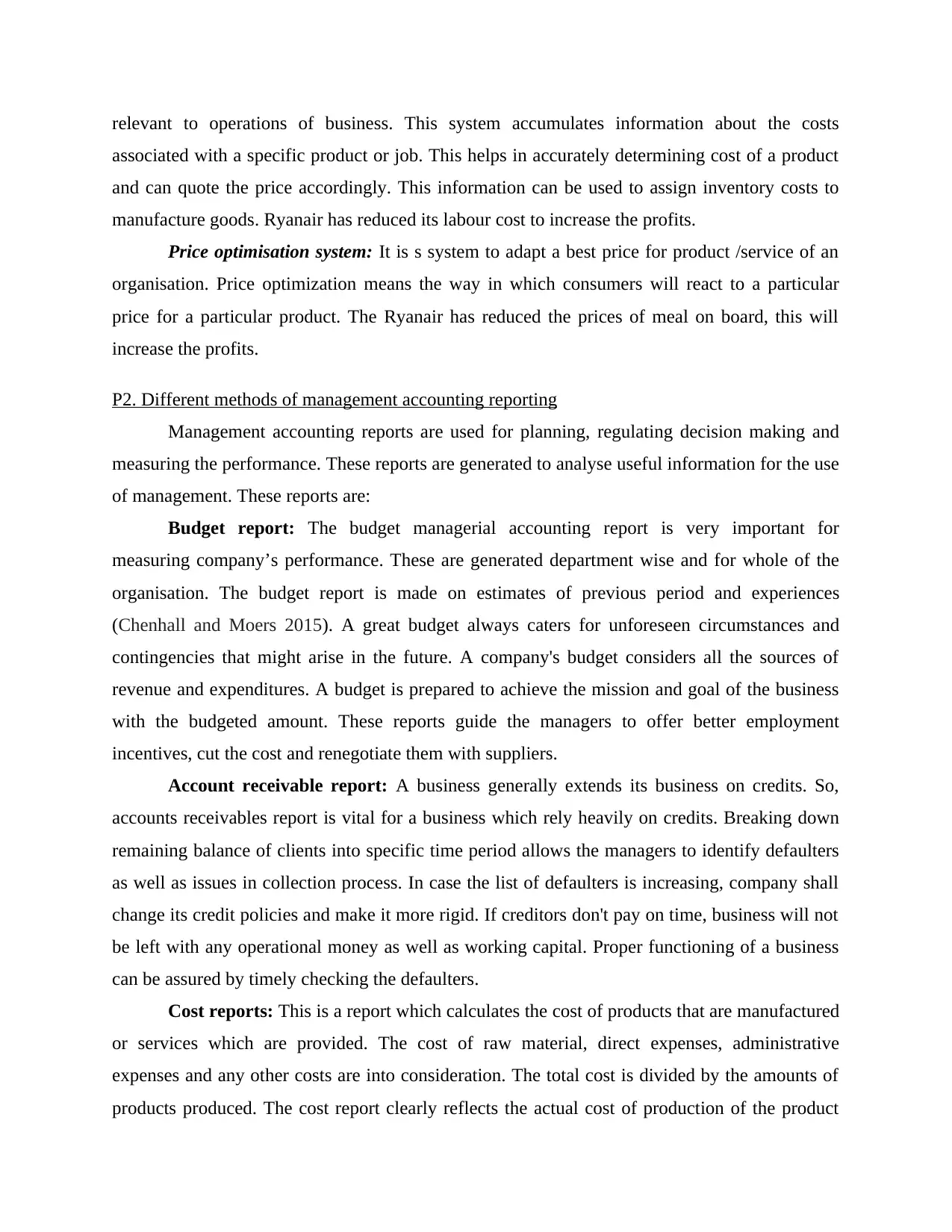

Marginal costing method: In this method the fixed cost remain unchanged in a time

period weather or not there is a change in sales volume. The variable cost changes with change in

the sales but fixed cost remains unchanged (McLean, McGovern and Davie 2015). The fixed cost

for the period is written off in full amount from aggregate contribution.

provide a clear picture of pricing of the each product. The cost determined are inventory waste

cost, hourly labour cost and overhead costs.

Performance reports: This report evaluate the overall performance of the company and

also of the individual employees, managers and directors on the company at the end of a term.

The reports are also generated for each departments to evaluate there performances. These

reports helps manager in making strategic decisions about the performance and futures of the

organisation. And also deals with the problems related to personnel of the organisation. This

report point outs the flaws in the area where the performance is not up to the mark. This report

keeps an accurate measure of the strategies to achieve the mission of the organisation.

Project reports: The project report is prepared to keep a close look on the projects

undertaken by the organisation. The details of particular projects are mentioned in the reports.

For different projects different reports are prepared and sometimes a combine report is also

prepared. This shows the details like what is the projects, when it is assigned, when is the

deadline, what are the resources used and required for completion of the project. It also evaluates

the finished projects that hoe the project is working and what are the problems coming in

performance of such projects.

Activity reports: This report is related to the various activities performed within an

organisation. It shows the day to day activities in relation to the operational performance of the

business. The day to day activities are production related, employment related

Other reports: The other information reports are, report on analysis of competitors,

report on the debtors and their managements. These reports play a vital role in the performance

ans success of the company as they analyse ans evaluate key functional area of a business.

TASK 2

P.3 determination of cost per unit of Ryanair from marginal and absorption costing techniques

Marginal costing method: In this method the fixed cost remain unchanged in a time

period weather or not there is a change in sales volume. The variable cost changes with change in

the sales but fixed cost remains unchanged (McLean, McGovern and Davie 2015). The fixed cost

for the period is written off in full amount from aggregate contribution.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

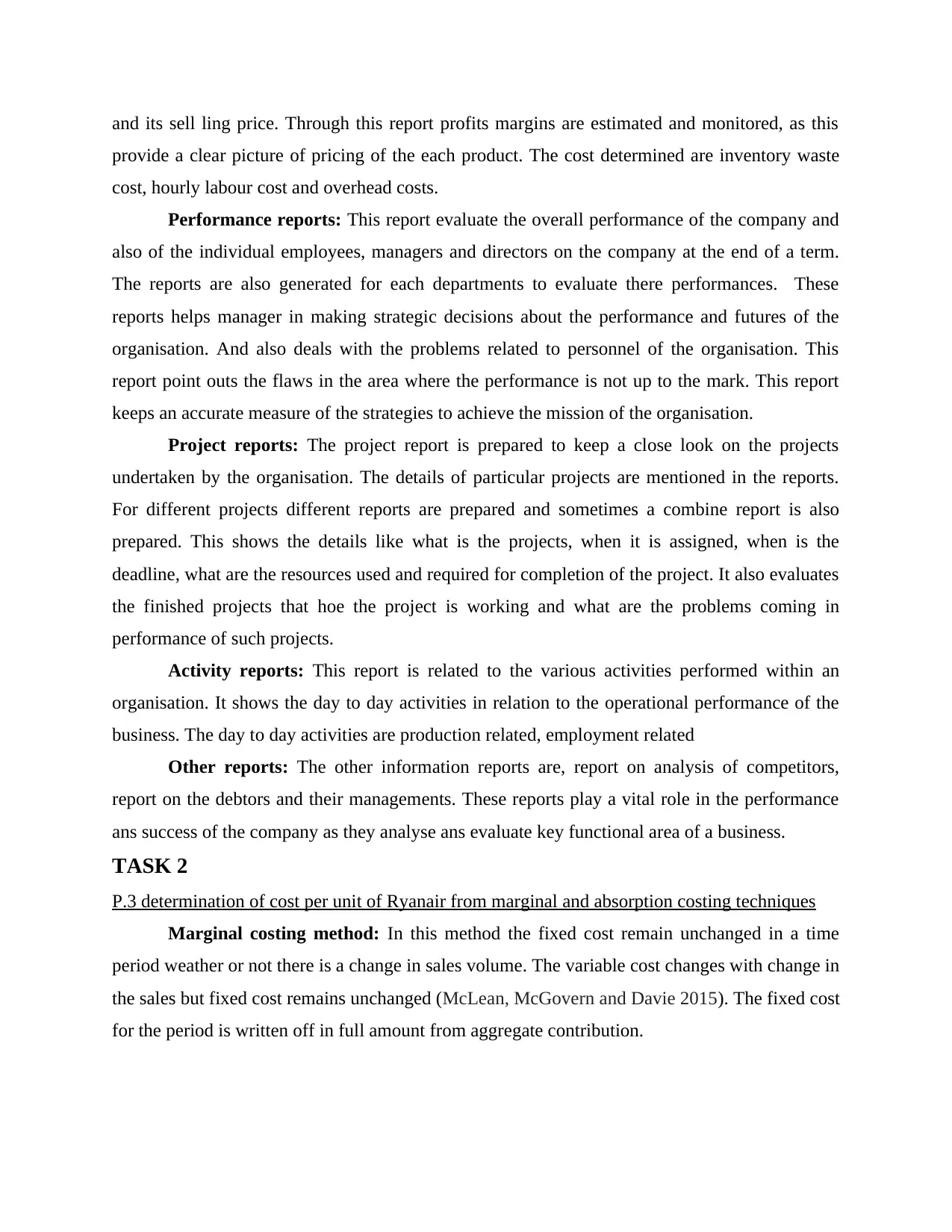

Absorption costing method: In this method all the manufacturing costs are absorbed by

the units produced in the firm. This means the unit cost of the product includes all the direct

material, overhead, labour cost both variable and fixed manufacturing overheads. The fixed cost

is absorbed and apportioned in the unit cost of product only.

Interpretation: Both the methods have given different results in respect of net profits. In

marginal costing method the fixed cost of 300 is absorbed from the contribution as a result of

which net profit of the firm is very less. With the change in the sales the variable cost also

changes but the fixed cost remain unchanged. The fixed cost is deducted as a part profit and

decreasing the profits.

In absorption costing method the fixed cost that is fixed overhead and non manufacturing

cost are deducted after calculating the gross profit which did not result in loss of profit. The

profits calculated by this method are way too high as compared to profits calculated by marginal

costing method.

the units produced in the firm. This means the unit cost of the product includes all the direct

material, overhead, labour cost both variable and fixed manufacturing overheads. The fixed cost

is absorbed and apportioned in the unit cost of product only.

Interpretation: Both the methods have given different results in respect of net profits. In

marginal costing method the fixed cost of 300 is absorbed from the contribution as a result of

which net profit of the firm is very less. With the change in the sales the variable cost also

changes but the fixed cost remain unchanged. The fixed cost is deducted as a part profit and

decreasing the profits.

In absorption costing method the fixed cost that is fixed overhead and non manufacturing

cost are deducted after calculating the gross profit which did not result in loss of profit. The

profits calculated by this method are way too high as compared to profits calculated by marginal

costing method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Ryanair must follow the absorption costing method which gives higher profits to the

company. The higher profits means higher return to the investors and shareholder of the

company (Jones, D, Gebbens and Terhorst, 2015). More the return more company gain

competitive advantages over its competitors in the market. This will give company a strong

position in the industry and a ruling power over the industry.

Between the two methods of costing the company shall follow the absorption method to

increase the profits and by apportioning the fixed cost among the units produced.

TASK 3

P.4 Different types of planning tools for budgetary control and their advantages and

disadvantages

Budgetary control is a system of management control actual revenues generated and

expenses done are compared with planned income and expenditures. So the gap between the

actual and budgeted can be seen (Callaghan and Mignerey, 2014). The changes are then

evaluated to know the resin for such deviation and tools and techniques are applied to control

such deviation.

Types of budgeting:

Zero based budgeting- This is budget that involves determining what management

wants and then development of a budget according to that requirement to achieve that outcome.

The budget in this method of budgeting is prepared in which expenses for each new period shall

be justified (Adebayo and Taofeek 2014). This starts from Zero base, and the needs and costs for

every function in the organisations are analysed. Ryanair can use this tool for new economeal

project and expenses related to it.

Advantages of Zero based Budgeting:

The operations which are inefficient and obsolete can be identified and discontinued.

This leads to increase in involvement of staff at all level.

A timely response to business environmental changes.

Understanding and knowledge the Cost behaviour pattern will be enhanced. Resources are allocated efficiently and effectively.

Disadvantages of Zero based budgeting:

company. The higher profits means higher return to the investors and shareholder of the

company (Jones, D, Gebbens and Terhorst, 2015). More the return more company gain

competitive advantages over its competitors in the market. This will give company a strong

position in the industry and a ruling power over the industry.

Between the two methods of costing the company shall follow the absorption method to

increase the profits and by apportioning the fixed cost among the units produced.

TASK 3

P.4 Different types of planning tools for budgetary control and their advantages and

disadvantages

Budgetary control is a system of management control actual revenues generated and

expenses done are compared with planned income and expenditures. So the gap between the

actual and budgeted can be seen (Callaghan and Mignerey, 2014). The changes are then

evaluated to know the resin for such deviation and tools and techniques are applied to control

such deviation.

Types of budgeting:

Zero based budgeting- This is budget that involves determining what management

wants and then development of a budget according to that requirement to achieve that outcome.

The budget in this method of budgeting is prepared in which expenses for each new period shall

be justified (Adebayo and Taofeek 2014). This starts from Zero base, and the needs and costs for

every function in the organisations are analysed. Ryanair can use this tool for new economeal

project and expenses related to it.

Advantages of Zero based Budgeting:

The operations which are inefficient and obsolete can be identified and discontinued.

This leads to increase in involvement of staff at all level.

A timely response to business environmental changes.

Understanding and knowledge the Cost behaviour pattern will be enhanced. Resources are allocated efficiently and effectively.

Disadvantages of Zero based budgeting:

Emphasizes on short term benefits for determination of long term goal.

The process may sometimes become rigid ans can avoid future uncertainties.

No requirement of management skills.

Demotivation to the managers due to more time spending on budgeting process.

Difficult ranking of different types of activities.

Incremental based budgeting: This is budget based on small changes in the existing

budget for arriving to new budget (Zaman And et.al, 2014). Only the incremental amounts are

added to existing budget to reach new budget.

Advantages of Incremental based budgeting:

This ensures continuity of funding for departments without much detailed analysis.

Impact of the change can be seen immediately.

No large deviation in the budget of last financial year which ensures stability in

budgeting system of a company.

A very method to implement no complex calculations are required.

This method is used to eliminate rivalry and build value of equality.

Disadvantages of Incremental based budgeting:

It can lead to a scenario of budgetary slack.

This type budgets disconnect the firm from the reality.

Can lead to lack of innovation and no incentive to managers due to less working on

budgets.

Turns the business to run in conservative mode as no risk is taken and considered while

preparing the budget.

This budgeting subconsciously encourages higher spending to maintain the budget for

next year.

Activity based budgeting: This is a method of budgeting in which budget are made

using the activity base costing while considering the expenses. This does not consider last year's

budget to reach current years budget

Advantages Activity based budgeting:

Evaluation of each and every cost driver and all the activities.

The process may sometimes become rigid ans can avoid future uncertainties.

No requirement of management skills.

Demotivation to the managers due to more time spending on budgeting process.

Difficult ranking of different types of activities.

Incremental based budgeting: This is budget based on small changes in the existing

budget for arriving to new budget (Zaman And et.al, 2014). Only the incremental amounts are

added to existing budget to reach new budget.

Advantages of Incremental based budgeting:

This ensures continuity of funding for departments without much detailed analysis.

Impact of the change can be seen immediately.

No large deviation in the budget of last financial year which ensures stability in

budgeting system of a company.

A very method to implement no complex calculations are required.

This method is used to eliminate rivalry and build value of equality.

Disadvantages of Incremental based budgeting:

It can lead to a scenario of budgetary slack.

This type budgets disconnect the firm from the reality.

Can lead to lack of innovation and no incentive to managers due to less working on

budgets.

Turns the business to run in conservative mode as no risk is taken and considered while

preparing the budget.

This budgeting subconsciously encourages higher spending to maintain the budget for

next year.

Activity based budgeting: This is a method of budgeting in which budget are made

using the activity base costing while considering the expenses. This does not consider last year's

budget to reach current years budget

Advantages Activity based budgeting:

Evaluation of each and every cost driver and all the activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This considers business as a single unit not as different departments as a result

managements feels more involvement.

Budget is prepared after deep research and analysis that removes unnecessary activities.

Removal of unnecessary activities leads to saving in cost and improving competitive edge

in the market. Improves relationship between business and its customers.

Disadvantages Activity based budgeting:

This requires a deep understanding of various functional areas of business.

This is complex in nature, as it requires research and analysis of various factors.

This consumes a lot of resources of organisation. Need involvement of top level

management as well.

Focuses on short term goals of business. Does not take in account long term scenario.

Requirement of trained employables for making the budget.

Planning tools:

Net present value: This is method to analyse the profitability of an investment in a

company. The net present value considers the present value of future cash flows in excess of the

present valve of investment outlet.

Advantages of Net present value:

This takes into account the present valve of a future cash flow. The cash flows are

discounted by another period of capital cost.

This tell the company weather or not the project will generate money.

This considers cost of capital and risk inherent for future projections.

Disadvantages of Net present value:

Not useful for comparison of two projects of different size.

The size of NPV output is determined by the size of input.

Internal rate of return: Internal rate of return is a formula used in capital budgeting to

estimate profitability of potential investment. This is a discount rate that makes the net present

value of all cash flow from a particular project.

Advantages of Internal rate of return:

This considers time valve of money in evaluation of the projects.

It is very simple to interpret IRR.

managements feels more involvement.

Budget is prepared after deep research and analysis that removes unnecessary activities.

Removal of unnecessary activities leads to saving in cost and improving competitive edge

in the market. Improves relationship between business and its customers.

Disadvantages Activity based budgeting:

This requires a deep understanding of various functional areas of business.

This is complex in nature, as it requires research and analysis of various factors.

This consumes a lot of resources of organisation. Need involvement of top level

management as well.

Focuses on short term goals of business. Does not take in account long term scenario.

Requirement of trained employables for making the budget.

Planning tools:

Net present value: This is method to analyse the profitability of an investment in a

company. The net present value considers the present value of future cash flows in excess of the

present valve of investment outlet.

Advantages of Net present value:

This takes into account the present valve of a future cash flow. The cash flows are

discounted by another period of capital cost.

This tell the company weather or not the project will generate money.

This considers cost of capital and risk inherent for future projections.

Disadvantages of Net present value:

Not useful for comparison of two projects of different size.

The size of NPV output is determined by the size of input.

Internal rate of return: Internal rate of return is a formula used in capital budgeting to

estimate profitability of potential investment. This is a discount rate that makes the net present

value of all cash flow from a particular project.

Advantages of Internal rate of return:

This considers time valve of money in evaluation of the projects.

It is very simple to interpret IRR.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages of Internal rate of return:

It does not consider economies of scale.

It assumes that the positive future cash flows are reinvested in IRR.

TASK 4

P.5 Report on organisational adaptation of management accounting system and comparison with

Two Easy jet Airline

The performance of an organisation can be evaluated from following tools:

1. KPI (Key performance indicator): This is applied at both organisational and individual

level. This is a quantifiable metric that reflects how well an organisation is achieving its

stated objectives and goals. Ryanair is achieving its objective by introduction of

Economeal to its and other airlines, While two Easy jet is charging the same price fas

earlier for meals ion board.

2. Benchmark: This is a way to discover what is the best performance being achieved to

gain comparative advantage. This information is used to identify the gab in process of the

organisation in order to achieve competitive advantages. To gain the competitive

advantage over the industry Ryanair have adopted the policy of low fare for tickets to

passengers. This have emerged into an advantage to the company as Two Easy jet is

charging same fare from the passengers for same journey.

3. Balanced scorecard: This helps managers to make better allocation and prioritizing

decisions ans enables them to see exactly what initiatives are necessary for organisation

to meet its goal. Ryanair has emphasised on productivity based incentives including

commission onboard sales. This improved employees performance and also sales

onboard, which results in increasing revenue of the company. Two Easy Jets have no

such policies so Ryanair gain competitive advantage over Two Easy Jet.

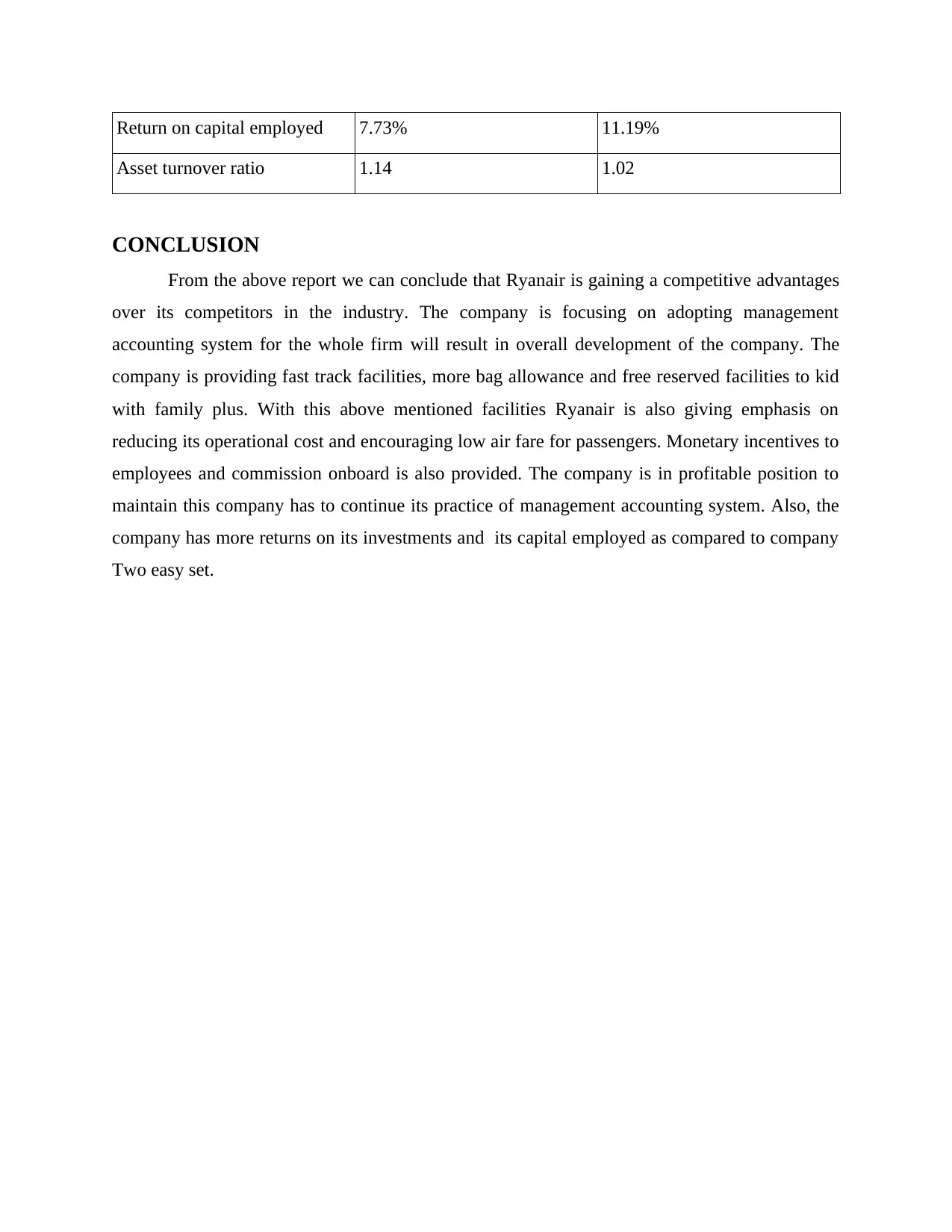

4. Financial Analysis: The four ratio to ascertain profitability are – return on investment,

liquidity ratios, leverage ratios and operating efficiency ratios.

Ratio (average ratio for a

period from 2014-2017)

Ryanair Two East Jet

Operating profit margin 7.09% 21.01%

It does not consider economies of scale.

It assumes that the positive future cash flows are reinvested in IRR.

TASK 4

P.5 Report on organisational adaptation of management accounting system and comparison with

Two Easy jet Airline

The performance of an organisation can be evaluated from following tools:

1. KPI (Key performance indicator): This is applied at both organisational and individual

level. This is a quantifiable metric that reflects how well an organisation is achieving its

stated objectives and goals. Ryanair is achieving its objective by introduction of

Economeal to its and other airlines, While two Easy jet is charging the same price fas

earlier for meals ion board.

2. Benchmark: This is a way to discover what is the best performance being achieved to

gain comparative advantage. This information is used to identify the gab in process of the

organisation in order to achieve competitive advantages. To gain the competitive

advantage over the industry Ryanair have adopted the policy of low fare for tickets to

passengers. This have emerged into an advantage to the company as Two Easy jet is

charging same fare from the passengers for same journey.

3. Balanced scorecard: This helps managers to make better allocation and prioritizing

decisions ans enables them to see exactly what initiatives are necessary for organisation

to meet its goal. Ryanair has emphasised on productivity based incentives including

commission onboard sales. This improved employees performance and also sales

onboard, which results in increasing revenue of the company. Two Easy Jets have no

such policies so Ryanair gain competitive advantage over Two Easy Jet.

4. Financial Analysis: The four ratio to ascertain profitability are – return on investment,

liquidity ratios, leverage ratios and operating efficiency ratios.

Ratio (average ratio for a

period from 2014-2017)

Ryanair Two East Jet

Operating profit margin 7.09% 21.01%

Return on capital employed 7.73% 11.19%

Asset turnover ratio 1.14 1.02

CONCLUSION

From the above report we can conclude that Ryanair is gaining a competitive advantages

over its competitors in the industry. The company is focusing on adopting management

accounting system for the whole firm will result in overall development of the company. The

company is providing fast track facilities, more bag allowance and free reserved facilities to kid

with family plus. With this above mentioned facilities Ryanair is also giving emphasis on

reducing its operational cost and encouraging low air fare for passengers. Monetary incentives to

employees and commission onboard is also provided. The company is in profitable position to

maintain this company has to continue its practice of management accounting system. Also, the

company has more returns on its investments and its capital employed as compared to company

Two easy set.

Asset turnover ratio 1.14 1.02

CONCLUSION

From the above report we can conclude that Ryanair is gaining a competitive advantages

over its competitors in the industry. The company is focusing on adopting management

accounting system for the whole firm will result in overall development of the company. The

company is providing fast track facilities, more bag allowance and free reserved facilities to kid

with family plus. With this above mentioned facilities Ryanair is also giving emphasis on

reducing its operational cost and encouraging low air fare for passengers. Monetary incentives to

employees and commission onboard is also provided. The company is in profitable position to

maintain this company has to continue its practice of management accounting system. Also, the

company has more returns on its investments and its capital employed as compared to company

Two easy set.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.