FSBM: Ryanair's Cost Management - A Management Accounting Report

VerifiedAdded on 2023/06/12

|14

|3031

|149

Report

AI Summary

This management accounting report analyzes Ryanair's cost management strategies, budgeting techniques, and financial reporting methods. It examines cost accounting systems, inventory management, and job costing within Ryanair's operational context. The report discusses the advantages and disadvantages of various budgeting tools and their implementation in Ryanair, comparing them with Southwest Airlines. It also includes an analysis of product costs under absorption and marginal costing techniques, presenting income statements under both methods. The report concludes with a cash budget analysis, providing insights into Ryanair's cash flow management. Desklib offers similar solved assignments and past papers for students.

0

MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Task 1...............................................................................................................................................2

Introduction to Management Accounting....................................................................................2

Methods used for Management Accounting Reporting...............................................................3

Benefits of Management Accounting System in Ryanair............................................................4

Integrating Management Accounting System and Report in Ryanair.........................................4

Task 2...............................................................................................................................................5

Product Cost Under Absorption and Marginal Costing Techniques...........................................5

Income Statement under Marginal and Absorption Costing.......................................................6

Task 3...............................................................................................................................................7

Advantages and Disadvantages of Budgeting tools.....................................................................7

Use of Different Planning tools...................................................................................................9

Task 4.............................................................................................................................................10

Comparison between Ryanair and Southwest Airlines.............................................................10

Implementation of the Budgeting policy...................................................................................10

Reference.......................................................................................................................................12

MANAGEMENT ACCOUNTING

Table of Contents

Task 1...............................................................................................................................................2

Introduction to Management Accounting....................................................................................2

Methods used for Management Accounting Reporting...............................................................3

Benefits of Management Accounting System in Ryanair............................................................4

Integrating Management Accounting System and Report in Ryanair.........................................4

Task 2...............................................................................................................................................5

Product Cost Under Absorption and Marginal Costing Techniques...........................................5

Income Statement under Marginal and Absorption Costing.......................................................6

Task 3...............................................................................................................................................7

Advantages and Disadvantages of Budgeting tools.....................................................................7

Use of Different Planning tools...................................................................................................9

Task 4.............................................................................................................................................10

Comparison between Ryanair and Southwest Airlines.............................................................10

Implementation of the Budgeting policy...................................................................................10

Reference.......................................................................................................................................12

2

MANAGEMENT ACCOUNTING

Task 1

Introduction to Management Accounting

Management accounting is the process of analyzing the costs which are incurred by the

business and also the activities of the business in order to prepare internal business reports,

accounts and records which can be of help in the decision-making process (Hilton & Platt, 2013).

In simple words it is the process of analyzing financial and cost related data for the purpose of

taking important decisions.

Nowadays management accounting System are widely used in businesses for the purpose

effective reporting and decision-making process. There are many kinds of management

accounting system with different objective and components (Fullerton, Kennedy & Widener,

2013). However, the basic purpose of following such a system is to analyze the data and

communicate the same. Some of the management accounting process are given below:

1. Cost accounting system: in case of cost accounting system cost allocation to the products

are done on the basis of either activity based costing or traditional method of costing

(DRURY, 2013). Cost accounting enables the business to identify the production costs

and step by step departmental cost associated with the product. The system measures and

records costs of the product then compare the results with the standard set by the

management for analyzing the performance of the company.

2. Inventory Management: Inventory management refers to the process of keeping track or

records of the stocks or inventory of the business (Dekker et al., 2013). It involves

keeping track of the inventory through all process such as sales, purchase (Wild, 2017).

The objective of inventory management is to accurately understand the present inventory

level of the organization.

MANAGEMENT ACCOUNTING

Task 1

Introduction to Management Accounting

Management accounting is the process of analyzing the costs which are incurred by the

business and also the activities of the business in order to prepare internal business reports,

accounts and records which can be of help in the decision-making process (Hilton & Platt, 2013).

In simple words it is the process of analyzing financial and cost related data for the purpose of

taking important decisions.

Nowadays management accounting System are widely used in businesses for the purpose

effective reporting and decision-making process. There are many kinds of management

accounting system with different objective and components (Fullerton, Kennedy & Widener,

2013). However, the basic purpose of following such a system is to analyze the data and

communicate the same. Some of the management accounting process are given below:

1. Cost accounting system: in case of cost accounting system cost allocation to the products

are done on the basis of either activity based costing or traditional method of costing

(DRURY, 2013). Cost accounting enables the business to identify the production costs

and step by step departmental cost associated with the product. The system measures and

records costs of the product then compare the results with the standard set by the

management for analyzing the performance of the company.

2. Inventory Management: Inventory management refers to the process of keeping track or

records of the stocks or inventory of the business (Dekker et al., 2013). It involves

keeping track of the inventory through all process such as sales, purchase (Wild, 2017).

The objective of inventory management is to accurately understand the present inventory

level of the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

3. Job costing: Job costing refers to the allocation of costs on different batches of product or

individual products. This type of costing method is applied when the products which are

to be produced are different from one another (Braun, 2013). The costing technique

considers the three major costs which are direct material, direct labour and overhead

costs.

Methods used for Management Accounting Reporting

The different methods which are used for management accounting reporting are given

below in details:

1. Cost Reports: In such types of reports management computes and records costs of the

goods which are manufactured. The computation is done considering direct material

costs, labour costs and overhead expenses of the product (Dale & Plunkett, 2017). The

cost reports present the management with insights of costs of the product and thereby

estimate the profit associated with the product.

2. Budgets: One of the most used tools of management accounting is budgets. It helps the

management to forecast the expenses which the business will incur in near future and also

plan for the same. Budgeting techniques are used by the management to plan for the

future of the business and also measure the current performance of the business

(Midrigan & Xu, .2014). There are various types of budgets which are prepared by the

management such as sales budget, master budget, cost budget and similar other kinds of

budgets.

3. Performance Reports: The management utilizes budgets such that they are able to

measure the actual results in terms of income and expenses of the company with the

budgeted figures. The difference is than computed and for the purpose of evaluation is

MANAGEMENT ACCOUNTING

3. Job costing: Job costing refers to the allocation of costs on different batches of product or

individual products. This type of costing method is applied when the products which are

to be produced are different from one another (Braun, 2013). The costing technique

considers the three major costs which are direct material, direct labour and overhead

costs.

Methods used for Management Accounting Reporting

The different methods which are used for management accounting reporting are given

below in details:

1. Cost Reports: In such types of reports management computes and records costs of the

goods which are manufactured. The computation is done considering direct material

costs, labour costs and overhead expenses of the product (Dale & Plunkett, 2017). The

cost reports present the management with insights of costs of the product and thereby

estimate the profit associated with the product.

2. Budgets: One of the most used tools of management accounting is budgets. It helps the

management to forecast the expenses which the business will incur in near future and also

plan for the same. Budgeting techniques are used by the management to plan for the

future of the business and also measure the current performance of the business

(Midrigan & Xu, .2014). There are various types of budgets which are prepared by the

management such as sales budget, master budget, cost budget and similar other kinds of

budgets.

3. Performance Reports: The management utilizes budgets such that they are able to

measure the actual results in terms of income and expenses of the company with the

budgeted figures. The difference is than computed and for the purpose of evaluation is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

recorded in a new budget which is known as performance report (Boons et al., 2013).

Such reports are prepared on yearly basis, quarterly basis or semi-annual basis as per the

requirement of the company.

Benefits of Management Accounting System in Ryanair

Ryanair is engaged in providing passenger airline services and is one of the most

successful airline brands in UK. The business model of the company is to maintain the costs of

the business as low as possible. The benefits which are associated with the management

accounting system which are applicable to Ryanair are given below:

1. Cost accounting system: The business model of Ryanair is minimization of costs which

are associated with the business. The cost accounting system will be useful for the

business as it will help the management to keep the costs which is incurred by the

business under check. The personnel costs and customer services cost of Ryanair can be

maintained with the help of budgets relating to costs. Another benefit of the same, is to

forecast the costs for future periods.

2. Inventory Management: The main advantage of using inventory management system is

that it keeps the aircraft equipment under check and maintains the records for the same.

Another benefit which can be pointed out is that the management with the inventory

records is able to estimate accurately how much more equipment might be required and

the costs associated with the same.

Integrating Management Accounting System and Report in Ryanair

In the case of Ryanair, the management of the company needs to implement management

accounting techniques such as cost accounting system, inventory management system. The

management can use the cost accounting system to keep the costs of the business in further in

MANAGEMENT ACCOUNTING

recorded in a new budget which is known as performance report (Boons et al., 2013).

Such reports are prepared on yearly basis, quarterly basis or semi-annual basis as per the

requirement of the company.

Benefits of Management Accounting System in Ryanair

Ryanair is engaged in providing passenger airline services and is one of the most

successful airline brands in UK. The business model of the company is to maintain the costs of

the business as low as possible. The benefits which are associated with the management

accounting system which are applicable to Ryanair are given below:

1. Cost accounting system: The business model of Ryanair is minimization of costs which

are associated with the business. The cost accounting system will be useful for the

business as it will help the management to keep the costs which is incurred by the

business under check. The personnel costs and customer services cost of Ryanair can be

maintained with the help of budgets relating to costs. Another benefit of the same, is to

forecast the costs for future periods.

2. Inventory Management: The main advantage of using inventory management system is

that it keeps the aircraft equipment under check and maintains the records for the same.

Another benefit which can be pointed out is that the management with the inventory

records is able to estimate accurately how much more equipment might be required and

the costs associated with the same.

Integrating Management Accounting System and Report in Ryanair

In the case of Ryanair, the management of the company needs to implement management

accounting techniques such as cost accounting system, inventory management system. The

management can use the cost accounting system to keep the costs of the business in further in

5

MANAGEMENT ACCOUNTING

control and such can also be used for preparation of cost reports which can be used by the

management of Ryanair to analyze the performance of the business.

In addition to this, the management can also implement inventory valuation techniques so

that the company can keep track records of the equipment purchased, discarded, loss with their

respective costs as well. This will help a great deal in the effective management of the business.

The management accounting system and management reporting techniques can go hand in hand

and effectively help the management in taking decisions.

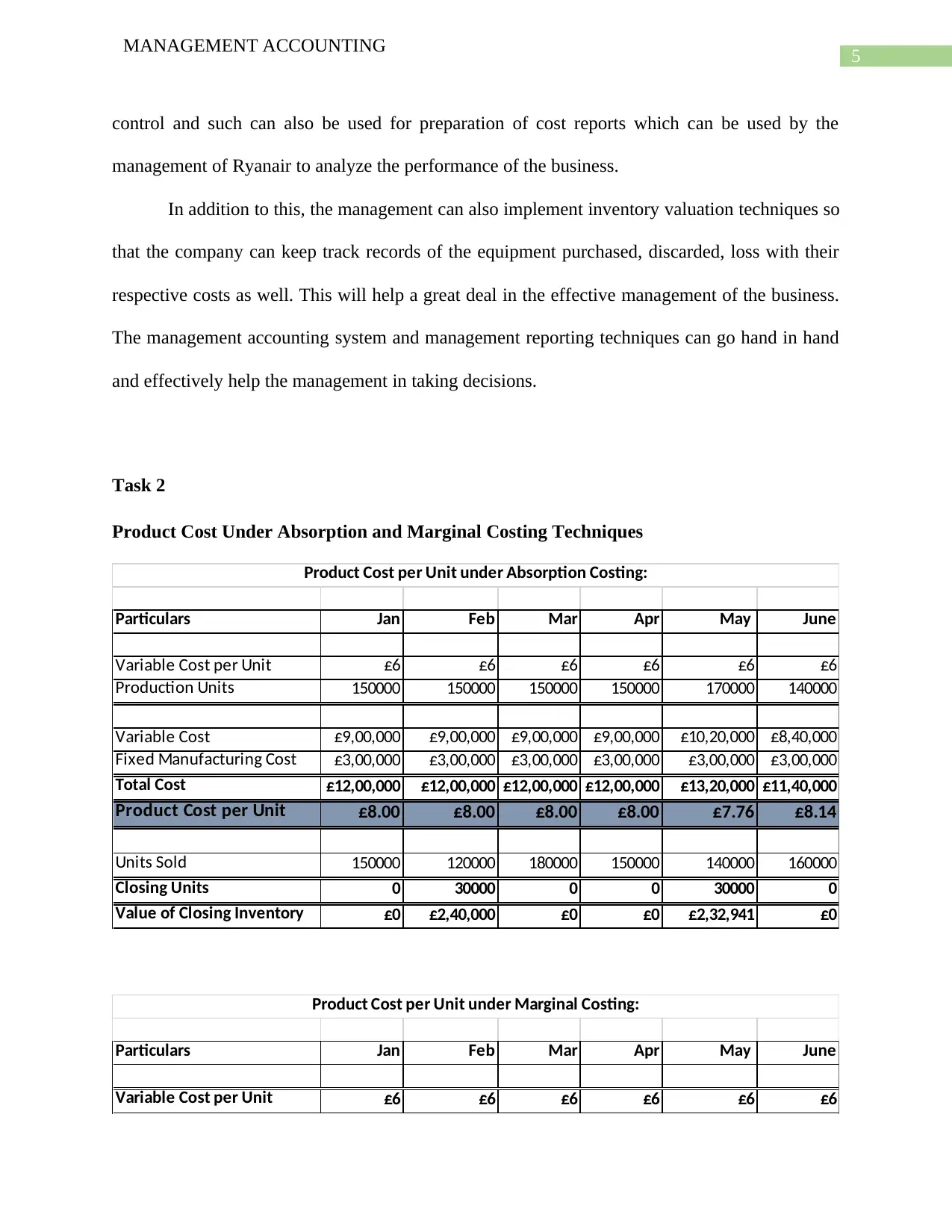

Task 2

Product Cost Under Absorption and Marginal Costing Techniques

Particulars Jan Feb Mar Apr May June

Variable Cost per Unit £6 £6 £6 £6 £6 £6

Production Units 150000 150000 150000 150000 170000 140000

Variable Cost £9,00,000 £9,00,000 £9,00,000 £9,00,000 £10,20,000 £8,40,000

Fixed Manufacturing Cost £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000

Total Cost £12,00,000 £12,00,000 £12,00,000 £12,00,000 £13,20,000 £11,40,000

Product Cost per Unit £8.00 £8.00 £8.00 £8.00 £7.76 £8.14

Units Sold 150000 120000 180000 150000 140000 160000

Closing Units 0 30000 0 0 30000 0

Value of Closing Inventory £0 £2,40,000 £0 £0 £2,32,941 £0

Product Cost per Unit under Absorption Costing:

Particulars Jan Feb Mar Apr May June

Variable Cost per Unit £6 £6 £6 £6 £6 £6

Product Cost per Unit under Marginal Costing:

MANAGEMENT ACCOUNTING

control and such can also be used for preparation of cost reports which can be used by the

management of Ryanair to analyze the performance of the business.

In addition to this, the management can also implement inventory valuation techniques so

that the company can keep track records of the equipment purchased, discarded, loss with their

respective costs as well. This will help a great deal in the effective management of the business.

The management accounting system and management reporting techniques can go hand in hand

and effectively help the management in taking decisions.

Task 2

Product Cost Under Absorption and Marginal Costing Techniques

Particulars Jan Feb Mar Apr May June

Variable Cost per Unit £6 £6 £6 £6 £6 £6

Production Units 150000 150000 150000 150000 170000 140000

Variable Cost £9,00,000 £9,00,000 £9,00,000 £9,00,000 £10,20,000 £8,40,000

Fixed Manufacturing Cost £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000

Total Cost £12,00,000 £12,00,000 £12,00,000 £12,00,000 £13,20,000 £11,40,000

Product Cost per Unit £8.00 £8.00 £8.00 £8.00 £7.76 £8.14

Units Sold 150000 120000 180000 150000 140000 160000

Closing Units 0 30000 0 0 30000 0

Value of Closing Inventory £0 £2,40,000 £0 £0 £2,32,941 £0

Product Cost per Unit under Absorption Costing:

Particulars Jan Feb Mar Apr May June

Variable Cost per Unit £6 £6 £6 £6 £6 £6

Product Cost per Unit under Marginal Costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

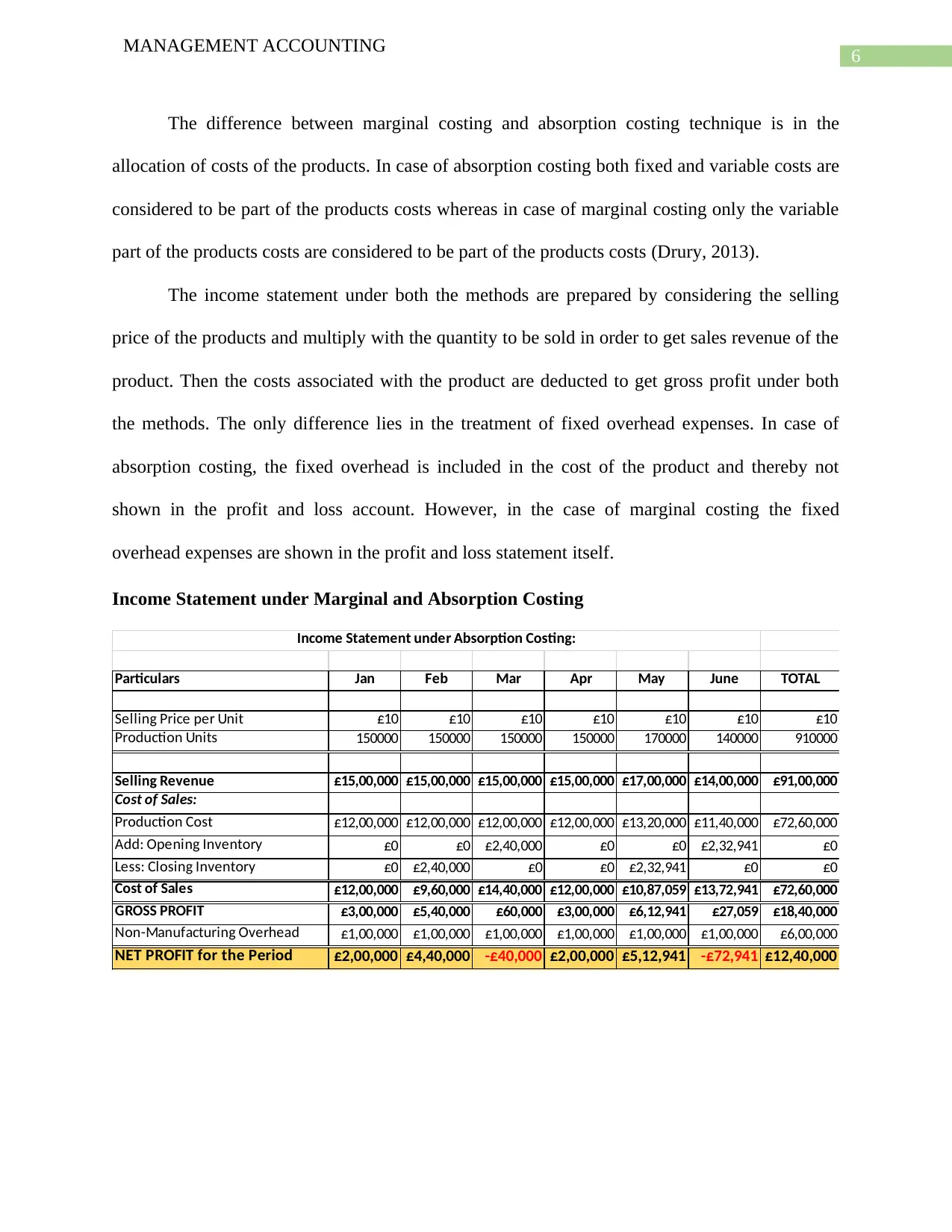

The difference between marginal costing and absorption costing technique is in the

allocation of costs of the products. In case of absorption costing both fixed and variable costs are

considered to be part of the products costs whereas in case of marginal costing only the variable

part of the products costs are considered to be part of the products costs (Drury, 2013).

The income statement under both the methods are prepared by considering the selling

price of the products and multiply with the quantity to be sold in order to get sales revenue of the

product. Then the costs associated with the product are deducted to get gross profit under both

the methods. The only difference lies in the treatment of fixed overhead expenses. In case of

absorption costing, the fixed overhead is included in the cost of the product and thereby not

shown in the profit and loss account. However, in the case of marginal costing the fixed

overhead expenses are shown in the profit and loss statement itself.

Income Statement under Marginal and Absorption Costing

Particulars Jan Feb Mar Apr May June TOTAL

Selling Price per Unit £10 £10 £10 £10 £10 £10 £10

Production Units 150000 150000 150000 150000 170000 140000 910000

Selling Revenue £15,00,000 £15,00,000 £15,00,000 £15,00,000 £17,00,000 £14,00,000 £91,00,000

Cost of Sales:

Production Cost £12,00,000 £12,00,000 £12,00,000 £12,00,000 £13,20,000 £11,40,000 £72,60,000

Add: Opening Inventory £0 £0 £2,40,000 £0 £0 £2,32,941 £0

Less: Closing Inventory £0 £2,40,000 £0 £0 £2,32,941 £0 £0

Cost of Sales £12,00,000 £9,60,000 £14,40,000 £12,00,000 £10,87,059 £13,72,941 £72,60,000

GROSS PROFIT £3,00,000 £5,40,000 £60,000 £3,00,000 £6,12,941 £27,059 £18,40,000

Non-Manufacturing Overhead £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £6,00,000

NET PROFIT for the Period £2,00,000 £4,40,000 -£40,000 £2,00,000 £5,12,941 -£72,941 £12,40,000

Income Statement under Absorption Costing:

MANAGEMENT ACCOUNTING

The difference between marginal costing and absorption costing technique is in the

allocation of costs of the products. In case of absorption costing both fixed and variable costs are

considered to be part of the products costs whereas in case of marginal costing only the variable

part of the products costs are considered to be part of the products costs (Drury, 2013).

The income statement under both the methods are prepared by considering the selling

price of the products and multiply with the quantity to be sold in order to get sales revenue of the

product. Then the costs associated with the product are deducted to get gross profit under both

the methods. The only difference lies in the treatment of fixed overhead expenses. In case of

absorption costing, the fixed overhead is included in the cost of the product and thereby not

shown in the profit and loss account. However, in the case of marginal costing the fixed

overhead expenses are shown in the profit and loss statement itself.

Income Statement under Marginal and Absorption Costing

Particulars Jan Feb Mar Apr May June TOTAL

Selling Price per Unit £10 £10 £10 £10 £10 £10 £10

Production Units 150000 150000 150000 150000 170000 140000 910000

Selling Revenue £15,00,000 £15,00,000 £15,00,000 £15,00,000 £17,00,000 £14,00,000 £91,00,000

Cost of Sales:

Production Cost £12,00,000 £12,00,000 £12,00,000 £12,00,000 £13,20,000 £11,40,000 £72,60,000

Add: Opening Inventory £0 £0 £2,40,000 £0 £0 £2,32,941 £0

Less: Closing Inventory £0 £2,40,000 £0 £0 £2,32,941 £0 £0

Cost of Sales £12,00,000 £9,60,000 £14,40,000 £12,00,000 £10,87,059 £13,72,941 £72,60,000

GROSS PROFIT £3,00,000 £5,40,000 £60,000 £3,00,000 £6,12,941 £27,059 £18,40,000

Non-Manufacturing Overhead £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £6,00,000

NET PROFIT for the Period £2,00,000 £4,40,000 -£40,000 £2,00,000 £5,12,941 -£72,941 £12,40,000

Income Statement under Absorption Costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

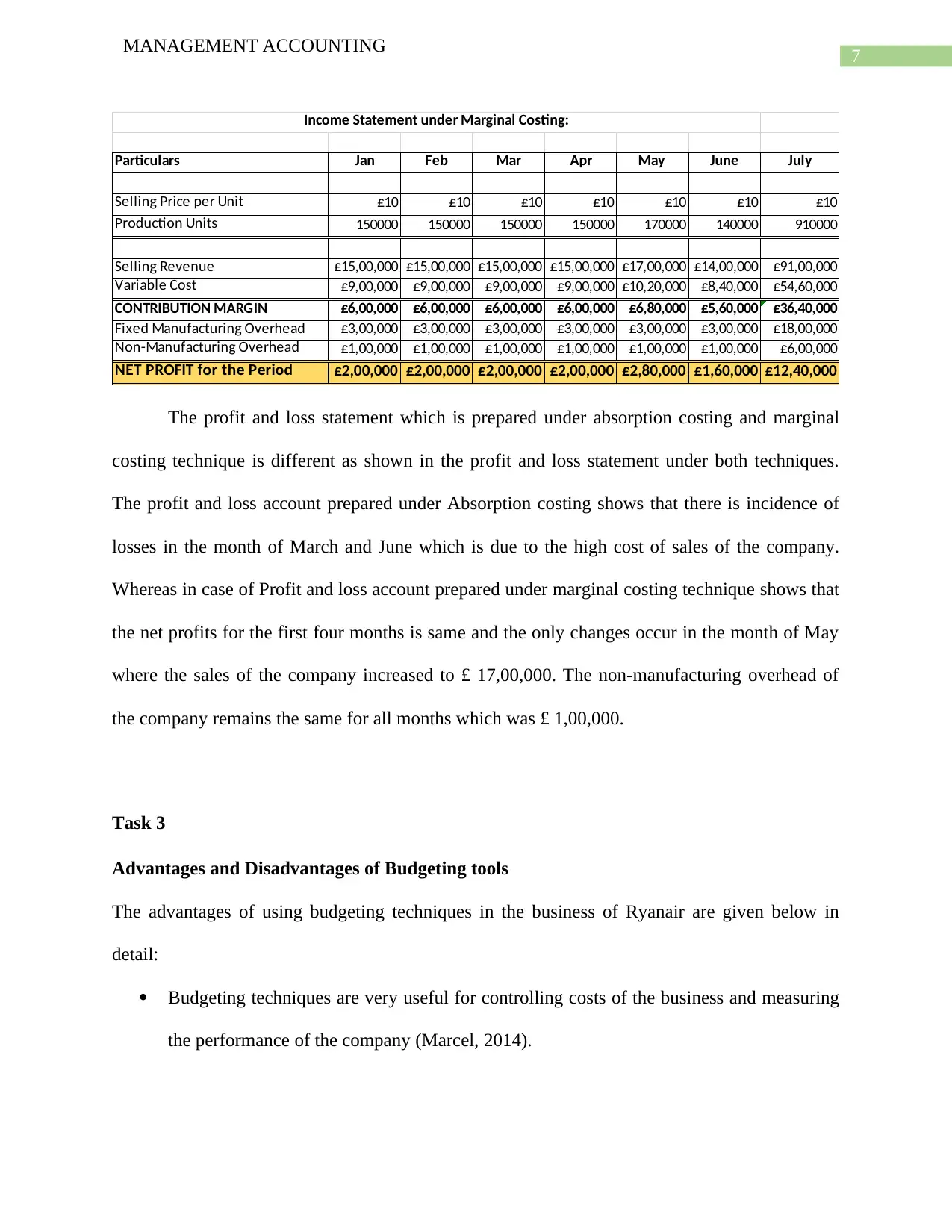

Particulars Jan Feb Mar Apr May June July

Selling Price per Unit £10 £10 £10 £10 £10 £10 £10

Production Units 150000 150000 150000 150000 170000 140000 910000

Selling Revenue £15,00,000 £15,00,000 £15,00,000 £15,00,000 £17,00,000 £14,00,000 £91,00,000

Variable Cost £9,00,000 £9,00,000 £9,00,000 £9,00,000 £10,20,000 £8,40,000 £54,60,000

CONTRIBUTION MARGIN £6,00,000 £6,00,000 £6,00,000 £6,00,000 £6,80,000 £5,60,000 £36,40,000

Fixed Manufacturing Overhead £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000 £18,00,000

Non-Manufacturing Overhead £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £6,00,000

NET PROFIT for the Period £2,00,000 £2,00,000 £2,00,000 £2,00,000 £2,80,000 £1,60,000 £12,40,000

Income Statement under Marginal Costing:

The profit and loss statement which is prepared under absorption costing and marginal

costing technique is different as shown in the profit and loss statement under both techniques.

The profit and loss account prepared under Absorption costing shows that there is incidence of

losses in the month of March and June which is due to the high cost of sales of the company.

Whereas in case of Profit and loss account prepared under marginal costing technique shows that

the net profits for the first four months is same and the only changes occur in the month of May

where the sales of the company increased to £ 17,00,000. The non-manufacturing overhead of

the company remains the same for all months which was £ 1,00,000.

Task 3

Advantages and Disadvantages of Budgeting tools

The advantages of using budgeting techniques in the business of Ryanair are given below in

detail:

Budgeting techniques are very useful for controlling costs of the business and measuring

the performance of the company (Marcel, 2014).

MANAGEMENT ACCOUNTING

Particulars Jan Feb Mar Apr May June July

Selling Price per Unit £10 £10 £10 £10 £10 £10 £10

Production Units 150000 150000 150000 150000 170000 140000 910000

Selling Revenue £15,00,000 £15,00,000 £15,00,000 £15,00,000 £17,00,000 £14,00,000 £91,00,000

Variable Cost £9,00,000 £9,00,000 £9,00,000 £9,00,000 £10,20,000 £8,40,000 £54,60,000

CONTRIBUTION MARGIN £6,00,000 £6,00,000 £6,00,000 £6,00,000 £6,80,000 £5,60,000 £36,40,000

Fixed Manufacturing Overhead £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000 £3,00,000 £18,00,000

Non-Manufacturing Overhead £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £1,00,000 £6,00,000

NET PROFIT for the Period £2,00,000 £2,00,000 £2,00,000 £2,00,000 £2,80,000 £1,60,000 £12,40,000

Income Statement under Marginal Costing:

The profit and loss statement which is prepared under absorption costing and marginal

costing technique is different as shown in the profit and loss statement under both techniques.

The profit and loss account prepared under Absorption costing shows that there is incidence of

losses in the month of March and June which is due to the high cost of sales of the company.

Whereas in case of Profit and loss account prepared under marginal costing technique shows that

the net profits for the first four months is same and the only changes occur in the month of May

where the sales of the company increased to £ 17,00,000. The non-manufacturing overhead of

the company remains the same for all months which was £ 1,00,000.

Task 3

Advantages and Disadvantages of Budgeting tools

The advantages of using budgeting techniques in the business of Ryanair are given below in

detail:

Budgeting techniques are very useful for controlling costs of the business and measuring

the performance of the company (Marcel, 2014).

8

MANAGEMENT ACCOUNTING

It helps to define the goals, plans and policies of the company and also used for the

purpose of communicating the same plans to different departments.

The technique is useful in measuring the performance of the departments which is done

by setting respective targets which the business has to achieve.

The disadvantage associated with the use of budgetary control are given below in point form:

The accuracy of the budget is the major concern as due to inflation the prices and

costs are continuously rising and therefore budgeting might not be effective.

In addition to this, application of effective budgeting technique is costly and therefore

not suited for small business concerns.

The success of the budget depends on the management’s implementation of the plans

incorporated in the budget and also on the judgement and estimation of the

management.

Cash Budget

MANAGEMENT ACCOUNTING

It helps to define the goals, plans and policies of the company and also used for the

purpose of communicating the same plans to different departments.

The technique is useful in measuring the performance of the departments which is done

by setting respective targets which the business has to achieve.

The disadvantage associated with the use of budgetary control are given below in point form:

The accuracy of the budget is the major concern as due to inflation the prices and

costs are continuously rising and therefore budgeting might not be effective.

In addition to this, application of effective budgeting technique is costly and therefore

not suited for small business concerns.

The success of the budget depends on the management’s implementation of the plans

incorporated in the budget and also on the judgement and estimation of the

management.

Cash Budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

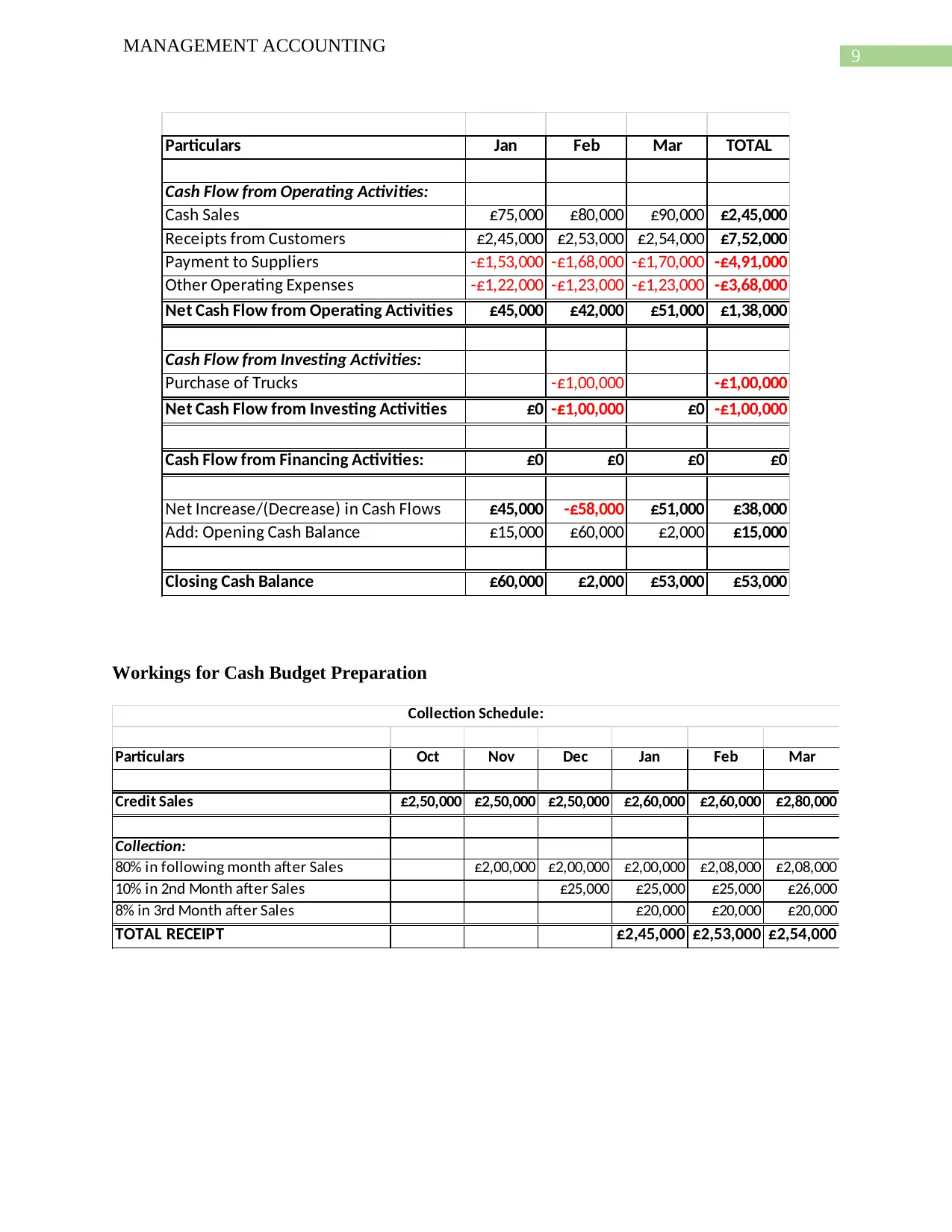

Particulars Jan Feb Mar TOTAL

Cash Flow from Operating Activities:

Cash Sales £75,000 £80,000 £90,000 £2,45,000

Receipts from Customers £2,45,000 £2,53,000 £2,54,000 £7,52,000

Payment to Suppliers -£1,53,000 -£1,68,000 -£1,70,000 -£4,91,000

Other Operating Expenses -£1,22,000 -£1,23,000 -£1,23,000 -£3,68,000

Net Cash Flow from Operating Activities £45,000 £42,000 £51,000 £1,38,000

Cash Flow from Investing Activities:

Purchase of Trucks -£1,00,000 -£1,00,000

Net Cash Flow from Investing Activities £0 -£1,00,000 £0 -£1,00,000

Cash Flow from Financing Activities: £0 £0 £0 £0

Net Increase/(Decrease) in Cash Flows £45,000 -£58,000 £51,000 £38,000

Add: Opening Cash Balance £15,000 £60,000 £2,000 £15,000

Closing Cash Balance £60,000 £2,000 £53,000 £53,000

Workings for Cash Budget Preparation

Particulars Oct Nov Dec Jan Feb Mar

Credit Sales £2,50,000 £2,50,000 £2,50,000 £2,60,000 £2,60,000 £2,80,000

Collection:

80% in following month after Sales £2,00,000 £2,00,000 £2,00,000 £2,08,000 £2,08,000

10% in 2nd Month after Sales £25,000 £25,000 £25,000 £26,000

8% in 3rd Month after Sales £20,000 £20,000 £20,000

TOTAL RECEIPT £2,45,000 £2,53,000 £2,54,000

Collection Schedule:

MANAGEMENT ACCOUNTING

Particulars Jan Feb Mar TOTAL

Cash Flow from Operating Activities:

Cash Sales £75,000 £80,000 £90,000 £2,45,000

Receipts from Customers £2,45,000 £2,53,000 £2,54,000 £7,52,000

Payment to Suppliers -£1,53,000 -£1,68,000 -£1,70,000 -£4,91,000

Other Operating Expenses -£1,22,000 -£1,23,000 -£1,23,000 -£3,68,000

Net Cash Flow from Operating Activities £45,000 £42,000 £51,000 £1,38,000

Cash Flow from Investing Activities:

Purchase of Trucks -£1,00,000 -£1,00,000

Net Cash Flow from Investing Activities £0 -£1,00,000 £0 -£1,00,000

Cash Flow from Financing Activities: £0 £0 £0 £0

Net Increase/(Decrease) in Cash Flows £45,000 -£58,000 £51,000 £38,000

Add: Opening Cash Balance £15,000 £60,000 £2,000 £15,000

Closing Cash Balance £60,000 £2,000 £53,000 £53,000

Workings for Cash Budget Preparation

Particulars Oct Nov Dec Jan Feb Mar

Credit Sales £2,50,000 £2,50,000 £2,50,000 £2,60,000 £2,60,000 £2,80,000

Collection:

80% in following month after Sales £2,00,000 £2,00,000 £2,00,000 £2,08,000 £2,08,000

10% in 2nd Month after Sales £25,000 £25,000 £25,000 £26,000

8% in 3rd Month after Sales £20,000 £20,000 £20,000

TOTAL RECEIPT £2,45,000 £2,53,000 £2,54,000

Collection Schedule:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

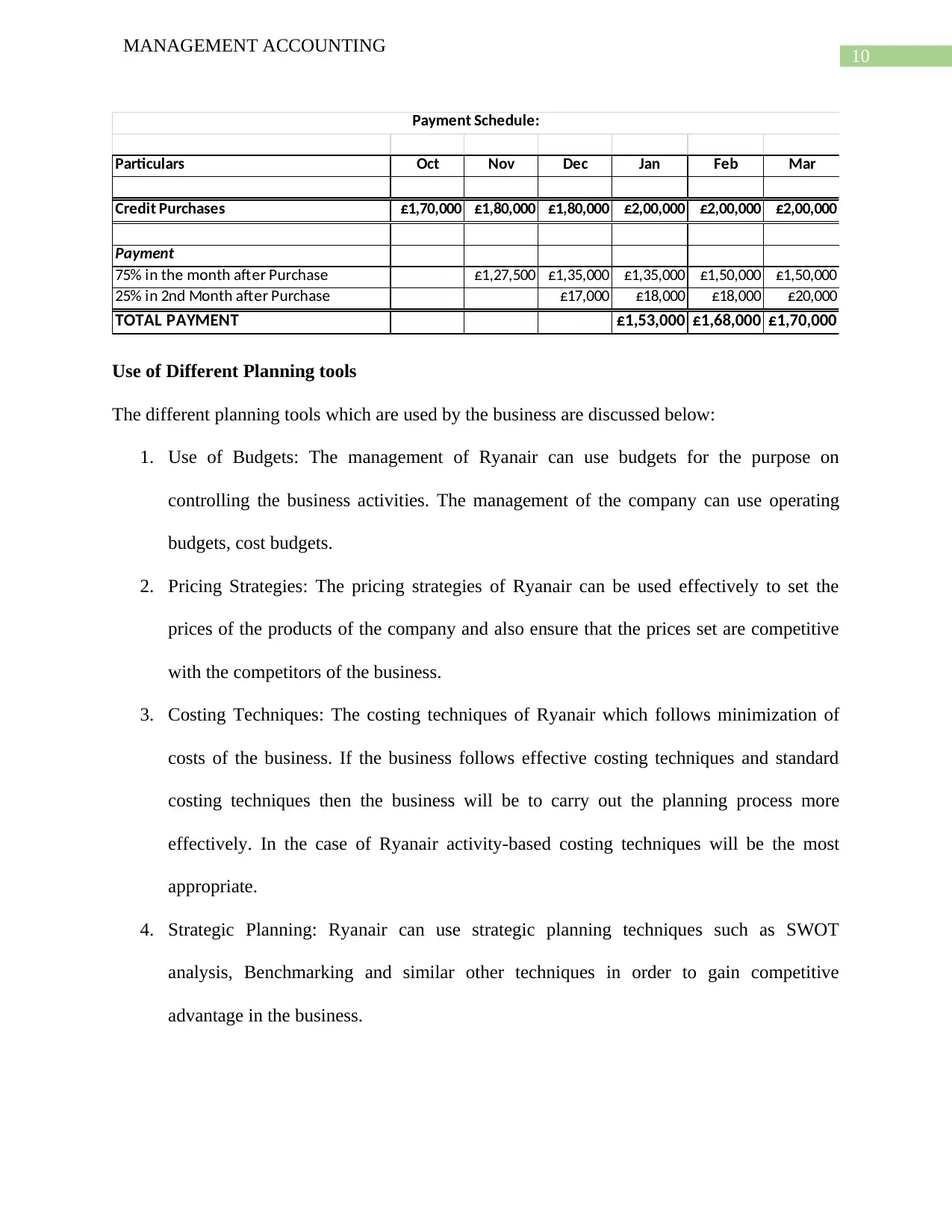

Particulars Oct Nov Dec Jan Feb Mar

Credit Purchases £1,70,000 £1,80,000 £1,80,000 £2,00,000 £2,00,000 £2,00,000

Payment

75% in the month after Purchase £1,27,500 £1,35,000 £1,35,000 £1,50,000 £1,50,000

25% in 2nd Month after Purchase £17,000 £18,000 £18,000 £20,000

TOTAL PAYMENT £1,53,000 £1,68,000 £1,70,000

Payment Schedule:

Use of Different Planning tools

The different planning tools which are used by the business are discussed below:

1. Use of Budgets: The management of Ryanair can use budgets for the purpose on

controlling the business activities. The management of the company can use operating

budgets, cost budgets.

2. Pricing Strategies: The pricing strategies of Ryanair can be used effectively to set the

prices of the products of the company and also ensure that the prices set are competitive

with the competitors of the business.

3. Costing Techniques: The costing techniques of Ryanair which follows minimization of

costs of the business. If the business follows effective costing techniques and standard

costing techniques then the business will be to carry out the planning process more

effectively. In the case of Ryanair activity-based costing techniques will be the most

appropriate.

4. Strategic Planning: Ryanair can use strategic planning techniques such as SWOT

analysis, Benchmarking and similar other techniques in order to gain competitive

advantage in the business.

MANAGEMENT ACCOUNTING

Particulars Oct Nov Dec Jan Feb Mar

Credit Purchases £1,70,000 £1,80,000 £1,80,000 £2,00,000 £2,00,000 £2,00,000

Payment

75% in the month after Purchase £1,27,500 £1,35,000 £1,35,000 £1,50,000 £1,50,000

25% in 2nd Month after Purchase £17,000 £18,000 £18,000 £20,000

TOTAL PAYMENT £1,53,000 £1,68,000 £1,70,000

Payment Schedule:

Use of Different Planning tools

The different planning tools which are used by the business are discussed below:

1. Use of Budgets: The management of Ryanair can use budgets for the purpose on

controlling the business activities. The management of the company can use operating

budgets, cost budgets.

2. Pricing Strategies: The pricing strategies of Ryanair can be used effectively to set the

prices of the products of the company and also ensure that the prices set are competitive

with the competitors of the business.

3. Costing Techniques: The costing techniques of Ryanair which follows minimization of

costs of the business. If the business follows effective costing techniques and standard

costing techniques then the business will be to carry out the planning process more

effectively. In the case of Ryanair activity-based costing techniques will be the most

appropriate.

4. Strategic Planning: Ryanair can use strategic planning techniques such as SWOT

analysis, Benchmarking and similar other techniques in order to gain competitive

advantage in the business.

11

MANAGEMENT ACCOUNTING

Task 4

Comparison between Ryanair and Southwest Airlines

The basic problem with the management of the Ryanair faces is related to the estimating

the revenues and costs of the business. In many cases the management is underestimating and

such brings about undesired changes. The use of proper budget plan along with standard cost

enables the company tom measure the performance and variances between estimated figures and

actual results.

In the case of Southwest Airlines, the management of the company faces problems which

relates cost increasing which is affecting the revenues of the business. Therefore for the

management to estimate clearly the costs and reasons for such costs, costs reports are prepared

for measuring the costs of the business and also identifying the sources to which maximum cost

accrue.

Implementation of the Budgeting policy

If the management of the Ryanair effectively implements the budgeting techniques along

with standard costing techniques then the management can analyze the variances and also

identify the reasons for such variances. This will help the management of Ryanair in effective

estimation process as well (Thurmaier & Willoughby, 2014). This will ensure the budgets which

are prepared in future are prepared accurately. Therefore, it appears clearly that effective

implementation of management accounting tools the business of Ryanair can improve both

planning process of the company and also improve the overall management of the company.

MANAGEMENT ACCOUNTING

Task 4

Comparison between Ryanair and Southwest Airlines

The basic problem with the management of the Ryanair faces is related to the estimating

the revenues and costs of the business. In many cases the management is underestimating and

such brings about undesired changes. The use of proper budget plan along with standard cost

enables the company tom measure the performance and variances between estimated figures and

actual results.

In the case of Southwest Airlines, the management of the company faces problems which

relates cost increasing which is affecting the revenues of the business. Therefore for the

management to estimate clearly the costs and reasons for such costs, costs reports are prepared

for measuring the costs of the business and also identifying the sources to which maximum cost

accrue.

Implementation of the Budgeting policy

If the management of the Ryanair effectively implements the budgeting techniques along

with standard costing techniques then the management can analyze the variances and also

identify the reasons for such variances. This will help the management of Ryanair in effective

estimation process as well (Thurmaier & Willoughby, 2014). This will ensure the budgets which

are prepared in future are prepared accurately. Therefore, it appears clearly that effective

implementation of management accounting tools the business of Ryanair can improve both

planning process of the company and also improve the overall management of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.