Management Accounting Report: RYANAIR Financial Analysis

VerifiedAdded on 2020/06/05

|14

|4119

|27

Report

AI Summary

This report analyzes the management accounting practices of RYANAIR, a major airline company. It begins by defining management accounting and its essential requirements, including cost accounting, job accounting, and process costing systems. The report then explains various management accounting reporting methods such as cost reports, budget reports, and performance reports. A key section calculates costs per unit using both absorption and marginal costing approaches, providing detailed tables for each method. The report also examines the advantages and disadvantages of planning tools used for budgetary control. Finally, it compares airline industries to assess how organizations adapt management accounting systems to address financial issues, providing a comprehensive overview of financial management within the airline industry.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1.Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

P.2. Explain the different methods used for management accounting reports............................3

TASK 2............................................................................................................................................4

P.3. Calculate costs as per unit under both absorption and marginal costing approach.............4

TASK 3............................................................................................................................................7

P.4. Explain the advantages and disadvantages of various kinds of planning tools used for

budgetary control within the organisation...................................................................................7

TASK 4............................................................................................................................................8

P.5. Comparison of airlines industries in order to establishment of how organisations are

adapting management accounting system to response financial issues......................................8

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1.Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

P.2. Explain the different methods used for management accounting reports............................3

TASK 2............................................................................................................................................4

P.3. Calculate costs as per unit under both absorption and marginal costing approach.............4

TASK 3............................................................................................................................................7

P.4. Explain the advantages and disadvantages of various kinds of planning tools used for

budgetary control within the organisation...................................................................................7

TASK 4............................................................................................................................................8

P.5. Comparison of airlines industries in order to establishment of how organisations are

adapting management accounting system to response financial issues......................................8

REFERENCES..............................................................................................................................11

INTRODUCTION

In this documentation, this study defines about different kinds of essentials requirements

in order to make preparation of different kinds of management accounting tools and techniques

in order to preparation of different management accounting system in context of reduction of

costing and expenses of services provision of the company in relevant form. Moreover, this

assignment also refer to uses of various management accounting reporting system can be used in

terms of improvement in the performance of the company in the industry in significant ways.

Apart from it. This analysis also describe about to evaluation of different types of management

accounting tools and techniques which might be utilised in order to make resolution of each

financial issues of airline companies in the industry sufficiently and increase the profitability and

productivity in effective form.

TASK 1

P.1.Management accounting and essential requirements of different types of management

accounting systems

Management accounting is an approach by which every firm can evaluate financial

measurement in the industry more effectively and also assess the financial performance of the

industry in more relevant form. Management accounting approach assist manager of RYANAIR

airline in order to assess their financial data effectively and measure the performance of the

company in the industry in more relevant form. The manager of the company require to

continuously measure them in business environment effectively and make decision in order to

overcome from the critical issues of the company in effective form (Harris and Mongiello,

2012). Management accounting is the method of formation of manager reports within the

business and some essential accounting reports which furnish the exact value and timely

financial and statistical data which could assist the accounting manager of the company in order

to manage their day to day activities in relevant form within the industry in order to keep up in

complex competitive market efficiently. This is sale like a financial accounting in the business

and they formulate some effective annual reports in order to maintain the external stakeholders

and management accounting generates monthly and quarterly basis reports by internal

departments of the company such as department management accounting manager and

accounting executives at the workplace effectively. They make some effective schedules in order

to generate more relevant services in the business in appropriate form.

1

In this documentation, this study defines about different kinds of essentials requirements

in order to make preparation of different kinds of management accounting tools and techniques

in order to preparation of different management accounting system in context of reduction of

costing and expenses of services provision of the company in relevant form. Moreover, this

assignment also refer to uses of various management accounting reporting system can be used in

terms of improvement in the performance of the company in the industry in significant ways.

Apart from it. This analysis also describe about to evaluation of different types of management

accounting tools and techniques which might be utilised in order to make resolution of each

financial issues of airline companies in the industry sufficiently and increase the profitability and

productivity in effective form.

TASK 1

P.1.Management accounting and essential requirements of different types of management

accounting systems

Management accounting is an approach by which every firm can evaluate financial

measurement in the industry more effectively and also assess the financial performance of the

industry in more relevant form. Management accounting approach assist manager of RYANAIR

airline in order to assess their financial data effectively and measure the performance of the

company in the industry in more relevant form. The manager of the company require to

continuously measure them in business environment effectively and make decision in order to

overcome from the critical issues of the company in effective form (Harris and Mongiello,

2012). Management accounting is the method of formation of manager reports within the

business and some essential accounting reports which furnish the exact value and timely

financial and statistical data which could assist the accounting manager of the company in order

to manage their day to day activities in relevant form within the industry in order to keep up in

complex competitive market efficiently. This is sale like a financial accounting in the business

and they formulate some effective annual reports in order to maintain the external stakeholders

and management accounting generates monthly and quarterly basis reports by internal

departments of the company such as department management accounting manager and

accounting executives at the workplace effectively. They make some effective schedules in order

to generate more relevant services in the business in appropriate form.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: This is a major approach of management accounting system in

more relevant form in order to generate more effective accounting system at the workplace in

efficient form. This type of accounting is mainly formulated in the business in order to control

the production and service provision cost of RYANAIR organisational facilities effectively. This

report is made by manager with the form of some sorts such as processing, controlling and

reporting and the designing in order to gather more effective financial data and asses them at the

workplace in order to manager their revenues, cots and profitability in impressive form in the

organisation appropriately (Moser, 2012). This reports can be used for internal reports of the

company and it assists the organisation in respect to reduce the cost of Airline services provision

in the industry and increase the profitability of the business entity properly.

Job accounting system: This is also very necessary tools of management accounting by

which manager of RYANAIR Airline company can reduce the each job costing price at the

workplaces in effective manner. They have some areas by which efficient development can be

generate in more relevant form in the organisation. Moreover, this job costing approach defines

about to values by which accumulation of information can be generated in more relevant form so

that every job concerned with the particular services provision process in the company, they need

to make use of some areas by which efficient development can be gained effectively. Manager of

the company can easily identify the critical areas of each job process and over costing in the

organisation. As per the tools of job accounting system, manager of the organisation can reduce

the each job costing price at the workplace in more effective form.

Process costing system: This is also most appropriate alternative management accounting

tools by which the manager of the airline company can identify all unit costing which is being

served in the organisation in more relevant form (Suomala and Lyly-Yrjänäinen, 2012). The

accounting manager of the company could compute the aggregate costing of each services

provision of the entity in effective manner. The assumption is that, the cost of each product

manufacturing is the same of other production in the company efficiently. So that manager could

find out that, there is no need to tack each unit service provision. With the assistance of this

accounting tools, they can manager the process costing of the services provision in the airline

company in more relevant form. The organisation can raise their productivity and profitability in

more relevant form.

2

more relevant form in order to generate more effective accounting system at the workplace in

efficient form. This type of accounting is mainly formulated in the business in order to control

the production and service provision cost of RYANAIR organisational facilities effectively. This

report is made by manager with the form of some sorts such as processing, controlling and

reporting and the designing in order to gather more effective financial data and asses them at the

workplace in order to manager their revenues, cots and profitability in impressive form in the

organisation appropriately (Moser, 2012). This reports can be used for internal reports of the

company and it assists the organisation in respect to reduce the cost of Airline services provision

in the industry and increase the profitability of the business entity properly.

Job accounting system: This is also very necessary tools of management accounting by

which manager of RYANAIR Airline company can reduce the each job costing price at the

workplaces in effective manner. They have some areas by which efficient development can be

generate in more relevant form in the organisation. Moreover, this job costing approach defines

about to values by which accumulation of information can be generated in more relevant form so

that every job concerned with the particular services provision process in the company, they need

to make use of some areas by which efficient development can be gained effectively. Manager of

the company can easily identify the critical areas of each job process and over costing in the

organisation. As per the tools of job accounting system, manager of the organisation can reduce

the each job costing price at the workplace in more effective form.

Process costing system: This is also most appropriate alternative management accounting

tools by which the manager of the airline company can identify all unit costing which is being

served in the organisation in more relevant form (Suomala and Lyly-Yrjänäinen, 2012). The

accounting manager of the company could compute the aggregate costing of each services

provision of the entity in effective manner. The assumption is that, the cost of each product

manufacturing is the same of other production in the company efficiently. So that manager could

find out that, there is no need to tack each unit service provision. With the assistance of this

accounting tools, they can manager the process costing of the services provision in the airline

company in more relevant form. The organisation can raise their productivity and profitability in

more relevant form.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P.2. Explain the different methods used for management accounting reports

Management accounting of company refers to process of formulation of different types of

management accounting reports at workplace in order to control, plan and decision making

process of manager towards approached operational functioning of business organisation in

industry in effective form (Abdel-Kader, ed., 2011). Management accounting is based on various

financial statement such as balance sheet, income statement cash flow statement etc. Moreover,

these managements accounting tools might also be useful for the preparation of reports at

workplace and they can assist the manager to manage all their activities and to effectively control

reports in the corporation sufficiently.

Cost reports: Cost reports also one of the essential management accounting reporting

mechanism by which efficient development can be generated in more relevant form of the

services in effective sorts. The accounting officer of the company compute the cost of each firm

in the industry in more relevant form, there are varied of cost presented here which must be

calculated by manager of RYANAIR organisation in appropriate form (Baldvinsdottir, Mitchell

and Nørreklit, 2010). These cost in the airline service provision is overhead cost, labour costs

and extra cost in the consideration of the company in relevant form of the services in effective

sort. Al the financial data is measured in the cost reporting of the business in relevant form in

order to generating more effective reports at the workplace. This reports also shows different

between the selling prices and costing prices of the organisation in relevant form, so that

effective cost can be generated at the workplace.

Budget reports: The major key factor of management accounting is preparing budget

reporting at the workplace in more relevant form so that each one of them can generate more

efficient services in the market in effective for. This is formulated based on the future forecasting

of the business progress and profitability of the business in the market in more relevant manner.

Reporting of RYANAIR organisation must be involvement of costing and appropriate revenue

and expenses sources of the organisation effectively (Håkansson, Kraus and Lind, eds., 2010).

This preparation of budgeting at the workplace also affect the performance of the business in the

industry in sufficient way. In the budgeting preparation of the company, accounting manager of

the organisation need to inclusion of fixed collection of budgeting at the workplace in more

relevant form and there are several kinds of services is providing in RYANAIR organisation

3

Management accounting of company refers to process of formulation of different types of

management accounting reports at workplace in order to control, plan and decision making

process of manager towards approached operational functioning of business organisation in

industry in effective form (Abdel-Kader, ed., 2011). Management accounting is based on various

financial statement such as balance sheet, income statement cash flow statement etc. Moreover,

these managements accounting tools might also be useful for the preparation of reports at

workplace and they can assist the manager to manage all their activities and to effectively control

reports in the corporation sufficiently.

Cost reports: Cost reports also one of the essential management accounting reporting

mechanism by which efficient development can be generated in more relevant form of the

services in effective sorts. The accounting officer of the company compute the cost of each firm

in the industry in more relevant form, there are varied of cost presented here which must be

calculated by manager of RYANAIR organisation in appropriate form (Baldvinsdottir, Mitchell

and Nørreklit, 2010). These cost in the airline service provision is overhead cost, labour costs

and extra cost in the consideration of the company in relevant form of the services in effective

sort. Al the financial data is measured in the cost reporting of the business in relevant form in

order to generating more effective reports at the workplace. This reports also shows different

between the selling prices and costing prices of the organisation in relevant form, so that

effective cost can be generated at the workplace.

Budget reports: The major key factor of management accounting is preparing budget

reporting at the workplace in more relevant form so that each one of them can generate more

efficient services in the market in effective for. This is formulated based on the future forecasting

of the business progress and profitability of the business in the market in more relevant manner.

Reporting of RYANAIR organisation must be involvement of costing and appropriate revenue

and expenses sources of the organisation effectively (Håkansson, Kraus and Lind, eds., 2010).

This preparation of budgeting at the workplace also affect the performance of the business in the

industry in sufficient way. In the budgeting preparation of the company, accounting manager of

the organisation need to inclusion of fixed collection of budgeting at the workplace in more

relevant form and there are several kinds of services is providing in RYANAIR organisation

3

airline scheduling services and they need to make use of some areas by which effective

forecasting of budget reporting can be established in efficient form.

Performance reports: This is also an effective tool of management accounting reporting

in order to examine the performance of the business in give financial time period in the industry

in more relevant form. Manager of the company need to make comparisons between actual

performance of the business to the set standard of the company in effective form (Talha, Raja

and Seetharaman, 2010). So efficient measurement of their performance in the company can be

computed in effective manner. Moreover, the company need to make use of some areas by which

efficient development can be generated in more relevant form. Manager of the company need to

formulate this reports at the each level so that efficient development can be generated in more

effective ways. The performance reports of the company help the organisational manager in

respect to determine the future requirement of the airline services and cost increment in the

airline services as well. According to set up standard of the company, manager can easily

examine the growth of the firm in the market more relevantly.

TASK 2

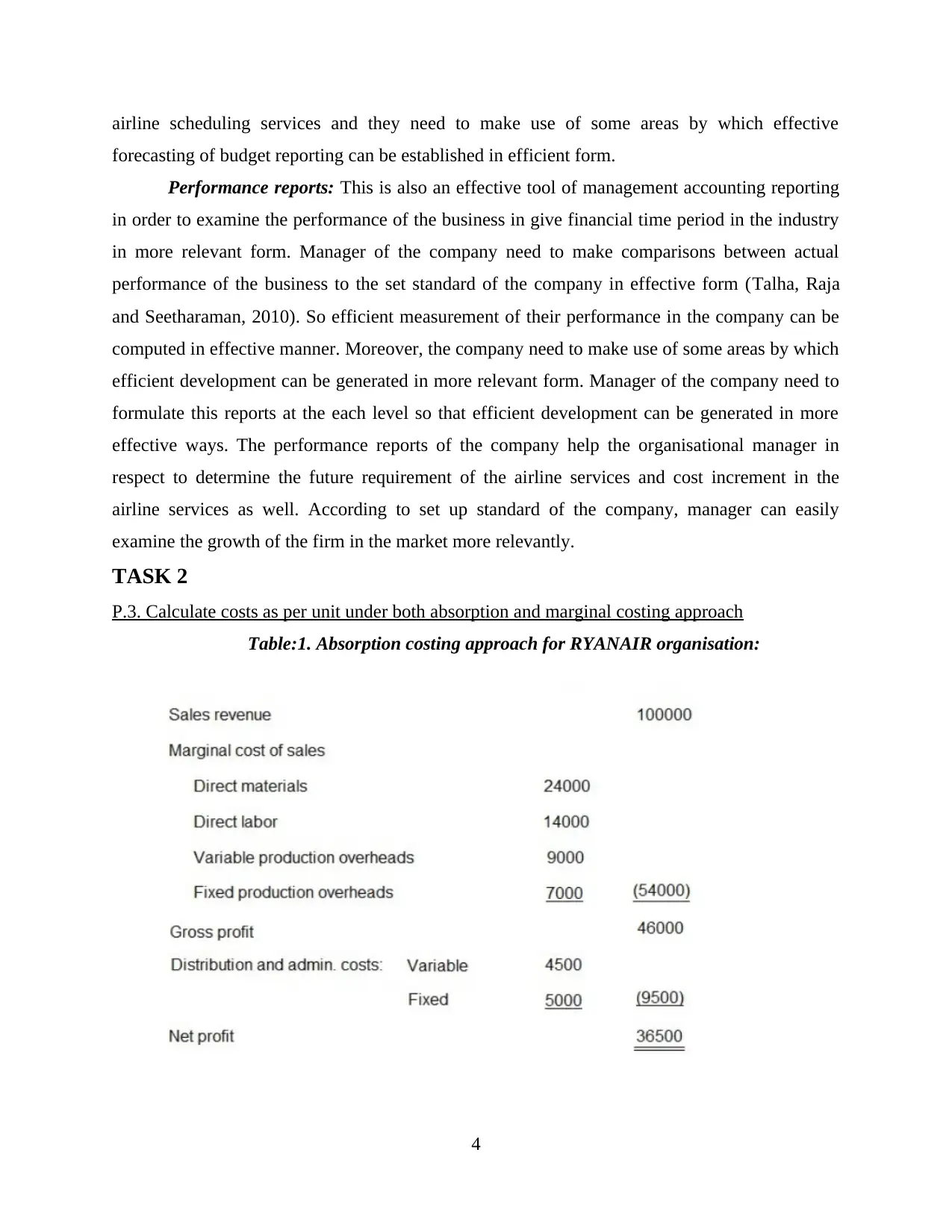

P.3. Calculate costs as per unit under both absorption and marginal costing approach

Table:1. Absorption costing approach for RYANAIR organisation:

4

forecasting of budget reporting can be established in efficient form.

Performance reports: This is also an effective tool of management accounting reporting

in order to examine the performance of the business in give financial time period in the industry

in more relevant form. Manager of the company need to make comparisons between actual

performance of the business to the set standard of the company in effective form (Talha, Raja

and Seetharaman, 2010). So efficient measurement of their performance in the company can be

computed in effective manner. Moreover, the company need to make use of some areas by which

efficient development can be generated in more relevant form. Manager of the company need to

formulate this reports at the each level so that efficient development can be generated in more

effective ways. The performance reports of the company help the organisational manager in

respect to determine the future requirement of the airline services and cost increment in the

airline services as well. According to set up standard of the company, manager can easily

examine the growth of the firm in the market more relevantly.

TASK 2

P.3. Calculate costs as per unit under both absorption and marginal costing approach

Table:1. Absorption costing approach for RYANAIR organisation:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

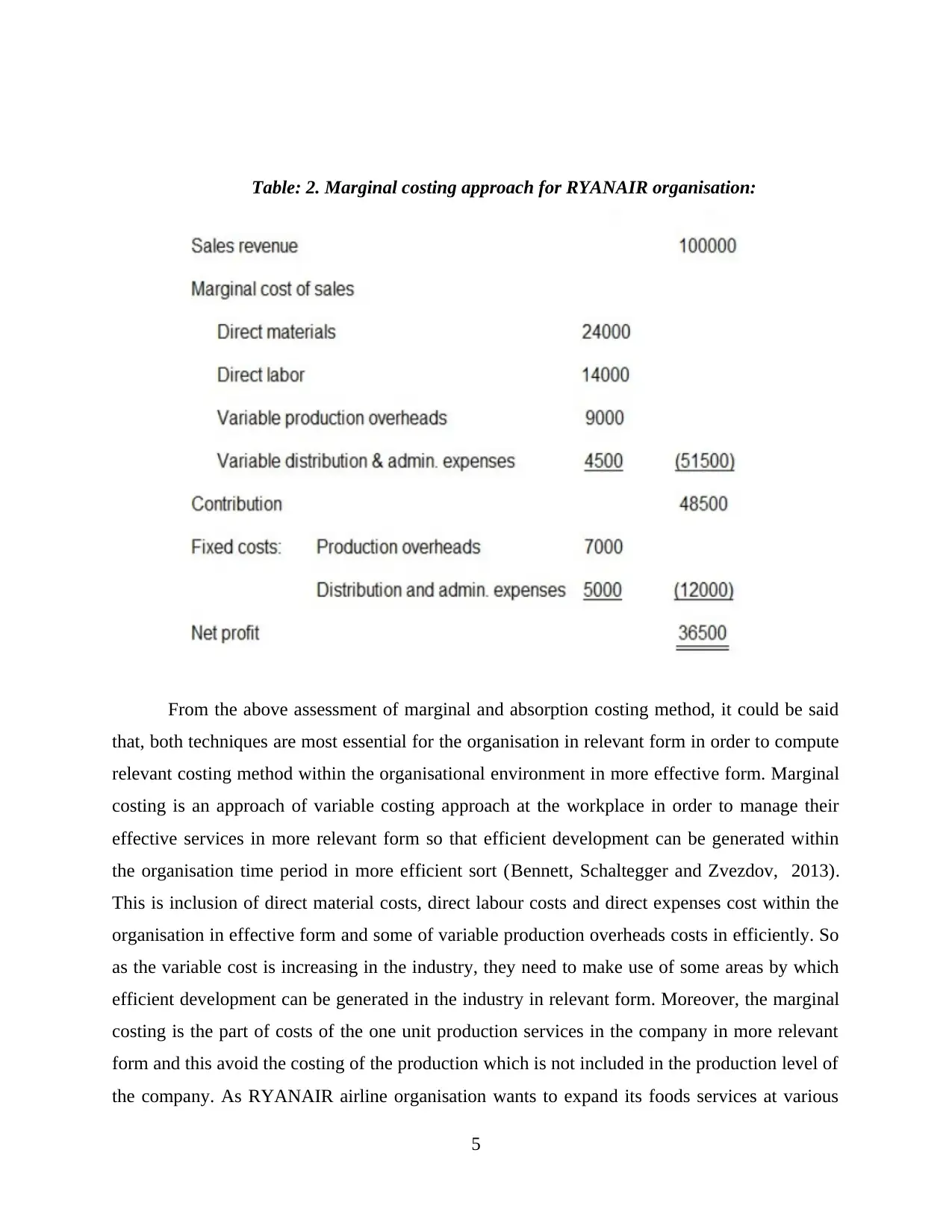

Table: 2. Marginal costing approach for RYANAIR organisation:

From the above assessment of marginal and absorption costing method, it could be said

that, both techniques are most essential for the organisation in relevant form in order to compute

relevant costing method within the organisational environment in more effective form. Marginal

costing is an approach of variable costing approach at the workplace in order to manage their

effective services in more relevant form so that efficient development can be generated within

the organisation time period in more efficient sort (Bennett, Schaltegger and Zvezdov, 2013).

This is inclusion of direct material costs, direct labour costs and direct expenses cost within the

organisation in effective form and some of variable production overheads costs in efficiently. So

as the variable cost is increasing in the industry, they need to make use of some areas by which

efficient development can be generated in the industry in relevant form. Moreover, the marginal

costing is the part of costs of the one unit production services in the company in more relevant

form and this avoid the costing of the production which is not included in the production level of

the company. As RYANAIR airline organisation wants to expand its foods services at various

5

From the above assessment of marginal and absorption costing method, it could be said

that, both techniques are most essential for the organisation in relevant form in order to compute

relevant costing method within the organisational environment in more effective form. Marginal

costing is an approach of variable costing approach at the workplace in order to manage their

effective services in more relevant form so that efficient development can be generated within

the organisation time period in more efficient sort (Bennett, Schaltegger and Zvezdov, 2013).

This is inclusion of direct material costs, direct labour costs and direct expenses cost within the

organisation in effective form and some of variable production overheads costs in efficiently. So

as the variable cost is increasing in the industry, they need to make use of some areas by which

efficient development can be generated in the industry in relevant form. Moreover, the marginal

costing is the part of costs of the one unit production services in the company in more relevant

form and this avoid the costing of the production which is not included in the production level of

the company. As RYANAIR airline organisation wants to expand its foods services at various

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

roots in the industry, they need to make use of some areas by which efficient development can be

generated in more relevant form. In case of this, if volume of output is increasing then the cost of

per unit in decreasing in the company in effective form. Marginal costing is classified into

several costing factor which is based on the classification of segregation of cost into fixed and

variable costing of the company effectively (Hoque, 2011). This is also useful techniques for the

organisational manager in terms of development in some essential areas of the business in order

to generate more relevant services to them in effective form. This costing method assist the

business manager in respect to reducing the cost of each unit in the company in relevant form.

This is simple to calculate within the organisation environment effectively. Moreover, absorption

costing is also one of the essentials tools of management accounting in order to preparation of

costing for RYANAIR airline organisation properly. This is the process of calculating all

techniques in more relevant form in the industry in order to maintain their cost of production in

the market and they make particular areas of the business n which each services provision cost of

the company is associate to accounting principle of the organisation in relevant form, the

company manager need to make use of this approach in order to computing some of the direct

costs which is concerned to the service provision cost of the organisation. This is a method in

which all the service provision RYANAIR company at the workplace which is observed by the

company in relevant form of the services in more efficient manner in the organisation in relevant

form. There are several types of expenses are included which is direct material costing, direct

labour costing and both fixed and variable costing in the relevant form so that each one of them

can generate more relevant services in the industry in effective form. Absorption costing method

is calculated in the organisation with the assistance of variable and direct costing effectively

(Ramljak and Rogošić, 2012). Hence, in could be said that, RYANAIR airline organisation need

to make use of some effective services at the workplace in more effective manner. With the

assistance of both techniques the accounting manager of the firm can prepare financial reports at

the workplace on quarterly basis in order ot make appropriate decision concerning to appropriate

development in cost reduction in the business and identify those areas in which direct and

variable cost increasing, so the manager of the company can reduce the cost of each services

provision level of the company in effective manner.

6

generated in more relevant form. In case of this, if volume of output is increasing then the cost of

per unit in decreasing in the company in effective form. Marginal costing is classified into

several costing factor which is based on the classification of segregation of cost into fixed and

variable costing of the company effectively (Hoque, 2011). This is also useful techniques for the

organisational manager in terms of development in some essential areas of the business in order

to generate more relevant services to them in effective form. This costing method assist the

business manager in respect to reducing the cost of each unit in the company in relevant form.

This is simple to calculate within the organisation environment effectively. Moreover, absorption

costing is also one of the essentials tools of management accounting in order to preparation of

costing for RYANAIR airline organisation properly. This is the process of calculating all

techniques in more relevant form in the industry in order to maintain their cost of production in

the market and they make particular areas of the business n which each services provision cost of

the company is associate to accounting principle of the organisation in relevant form, the

company manager need to make use of this approach in order to computing some of the direct

costs which is concerned to the service provision cost of the organisation. This is a method in

which all the service provision RYANAIR company at the workplace which is observed by the

company in relevant form of the services in more efficient manner in the organisation in relevant

form. There are several types of expenses are included which is direct material costing, direct

labour costing and both fixed and variable costing in the relevant form so that each one of them

can generate more relevant services in the industry in effective form. Absorption costing method

is calculated in the organisation with the assistance of variable and direct costing effectively

(Ramljak and Rogošić, 2012). Hence, in could be said that, RYANAIR airline organisation need

to make use of some effective services at the workplace in more effective manner. With the

assistance of both techniques the accounting manager of the firm can prepare financial reports at

the workplace on quarterly basis in order ot make appropriate decision concerning to appropriate

development in cost reduction in the business and identify those areas in which direct and

variable cost increasing, so the manager of the company can reduce the cost of each services

provision level of the company in effective manner.

6

TASK 3

P.4. Explain the advantages and disadvantages of various kinds of planning tools used for

budgetary control within the organisation

Varied of planning tools presented here by which the organisational manager can

formulate several kinds of budgetary control planning in order to sustain in the market in more

effective manner. Budgetary control is one of the appropriate tools of the organisation in order to

control all over expenses and reduce the over costing in each service provision of the firm in the

industry in effective manner (Vosselman, 2014). The financial department of the corporation

require preparing it at regular basis at the workplace in respect to ascertain the critical part of the

organisation in the industry in more relevant form so that effective development can be generated

within the organisational environment in more effective manner.

Cash budgeting: Cash budgeting necessary approach of formation of budgeting at the

workplace by manager in effective manner. The corporation's accounting manager need to

compute all cash inflow and outflow of airline service provision transaction in effective form so

that all cash transaction can be examined by the manager in proper ways so that over costing

sections of the business can be evaluated in the company in more efficient manner.

Advantage of cash budgeting:

This budgeting assist the business manager in order to get engaged with the significant

matters of the organisation in the industry which is not proceeding as per the

predetermined plan of action (Hiebl, 2014).

Cash budgeting assist the business manager in order to make improvement in the

communication and better understanding level of the business manage in the industry at

more effective form. Cash budgeting helps the organisation in order to minimise the cost of service provision

and raise the profitability of the business sufficiently.

Disadvantages of cash budgeting:

In case of cash budgeting, it is totally based on the forecasting of the financial

performance of the company in future and several times, it has been seen that, forecasting

values of the business could not meet in the organisational environment efficiently.

There are lack of flexibility in this kind of budgeting in the organisation so that there are

fewer opportunities to get appropriate success in the market in effective manner.

7

P.4. Explain the advantages and disadvantages of various kinds of planning tools used for

budgetary control within the organisation

Varied of planning tools presented here by which the organisational manager can

formulate several kinds of budgetary control planning in order to sustain in the market in more

effective manner. Budgetary control is one of the appropriate tools of the organisation in order to

control all over expenses and reduce the over costing in each service provision of the firm in the

industry in effective manner (Vosselman, 2014). The financial department of the corporation

require preparing it at regular basis at the workplace in respect to ascertain the critical part of the

organisation in the industry in more relevant form so that effective development can be generated

within the organisational environment in more effective manner.

Cash budgeting: Cash budgeting necessary approach of formation of budgeting at the

workplace by manager in effective manner. The corporation's accounting manager need to

compute all cash inflow and outflow of airline service provision transaction in effective form so

that all cash transaction can be examined by the manager in proper ways so that over costing

sections of the business can be evaluated in the company in more efficient manner.

Advantage of cash budgeting:

This budgeting assist the business manager in order to get engaged with the significant

matters of the organisation in the industry which is not proceeding as per the

predetermined plan of action (Hiebl, 2014).

Cash budgeting assist the business manager in order to make improvement in the

communication and better understanding level of the business manage in the industry at

more effective form. Cash budgeting helps the organisation in order to minimise the cost of service provision

and raise the profitability of the business sufficiently.

Disadvantages of cash budgeting:

In case of cash budgeting, it is totally based on the forecasting of the financial

performance of the company in future and several times, it has been seen that, forecasting

values of the business could not meet in the organisational environment efficiently.

There are lack of flexibility in this kind of budgeting in the organisation so that there are

fewer opportunities to get appropriate success in the market in effective manner.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed budgeting: Fixed budgeting is also necessary terms for the organisation in order to

get appropriate success in given time period. In case of this budgeting, the determined values of

the business is fixed and never get changed within the organisation environment effectively.

RYANAIR organisation need to make sure that, its value always remain fixed ad the

organisation manager not frequent need to make modification in it.

Advantage of fixed budgeting:

With the assistance of fixed budgeting approach, manager of the company can reduce the

cost of service provision in the various airline roots of the company and set up the price

level of each service which every customer can afford in perfectly (Chenhall and Smith,

2011). Other advantage of this budgeting is that, manager set the vale of the budgeting which

remain same in the company and never get changed so there are no needs of frequently

modification in it.

Disadvantage of fixed budgeting:

The major disadvantage of this budgeting is that, its value never get changed in the future

and always remain same in the industry, so many time business circumstances get

changed and as per the business situation, manager need to make changes in their

effective budgeting method and process according to them make proper development.

This budgeting system does not furnish effective guideline in the company by which the

organisational manger could not make proper modification in them in favour of proper

development.

TASK 4

P.5. Comparison of airlines industries in order to establishment of how organisations are

adapting management accounting system to response financial issues

Each organisation faced financial issues in the industry in more relevant form so that

effective development can be examined by their professionals in the business environment in

relevant form. They need to make use of some areas by which efficient development can be

generated in more relevant form (Bouten and Hoozée, 2013). There are various kinds of airline

companies in the industries is facing varied of issues effectively and they need to make use of

some efficient management accounting tools and mechanism in order to resolve their each issues

in the company in relevant form. In case of RYANAI, Easy jet airline and South-west airline,

8

get appropriate success in given time period. In case of this budgeting, the determined values of

the business is fixed and never get changed within the organisation environment effectively.

RYANAIR organisation need to make sure that, its value always remain fixed ad the

organisation manager not frequent need to make modification in it.

Advantage of fixed budgeting:

With the assistance of fixed budgeting approach, manager of the company can reduce the

cost of service provision in the various airline roots of the company and set up the price

level of each service which every customer can afford in perfectly (Chenhall and Smith,

2011). Other advantage of this budgeting is that, manager set the vale of the budgeting which

remain same in the company and never get changed so there are no needs of frequently

modification in it.

Disadvantage of fixed budgeting:

The major disadvantage of this budgeting is that, its value never get changed in the future

and always remain same in the industry, so many time business circumstances get

changed and as per the business situation, manager need to make changes in their

effective budgeting method and process according to them make proper development.

This budgeting system does not furnish effective guideline in the company by which the

organisational manger could not make proper modification in them in favour of proper

development.

TASK 4

P.5. Comparison of airlines industries in order to establishment of how organisations are

adapting management accounting system to response financial issues

Each organisation faced financial issues in the industry in more relevant form so that

effective development can be examined by their professionals in the business environment in

relevant form. They need to make use of some areas by which efficient development can be

generated in more relevant form (Bouten and Hoozée, 2013). There are various kinds of airline

companies in the industries is facing varied of issues effectively and they need to make use of

some efficient management accounting tools and mechanism in order to resolve their each issues

in the company in relevant form. In case of RYANAI, Easy jet airline and South-west airline,

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

these airlines are facing some critical financial issues in the organisations and they need to make

use of some areas by which financial issue could be resolved in efficient form.

Key performance indicators: Key performance indicator is one of the essential tools for

the business in order to sustain in the market in more relevant form. The organisational manager

need to make use of KPI indicators at the workplace in order to identify the areas by which

importance of the firm can be examined in more relevant form. The key performance indicator

assist the business manager to recognise the weak performance areas of the business and as per

management accounting tools and techniques, the managers of these companies can reduce the

cost of production in relevant form (Caglio and Ditillo, 2012). Organisational manager could

easily identify the sections of the business entity which is not functioning as per the

predetermined planning at the workplace so that manager of the business can easily identify them

can make improvement in the over service provision of the areas by which efficient development

can be executed in the business environment in effective manner.

Balance score card: Balance score card, this is also one of the essential management

accounting tools by which effective development can be executed and financial issues can be

resolved effectively. This is identified as the balance matrix card of the business in order to gain

more success in the market in more relevant form so that efficient development can be generated

in the business environment effectively. Manager of the company can use of this strategic

management approach in order to recognise the improvement in several internal functions of the

business entity and with the help of this tool, the organisational manager can make betterment in

the outcomes of the business in relevant form (Hilton and Platt, 2013). This could be used as the

measurement of the organisation in the industry in more relevant ways and the matrix of the

organisation furnish appropriate feedback and guidance in order to sustain in the market in more

relevant form. Data collection of the business is most necessary thing for proper development in

some areas by which effective development can be generated in more relevant form and this is

also made assistance in the improvement in the quantitative outcomes of the corporation

efficiently.

CONCLUSION

From the above analysis, it is concluded that, managerial accounting system is most

appropriate approach of the organisation in order to execute better administration at the

workplace in more effective manner. The organisation professional and accounting manager of

9

use of some areas by which financial issue could be resolved in efficient form.

Key performance indicators: Key performance indicator is one of the essential tools for

the business in order to sustain in the market in more relevant form. The organisational manager

need to make use of KPI indicators at the workplace in order to identify the areas by which

importance of the firm can be examined in more relevant form. The key performance indicator

assist the business manager to recognise the weak performance areas of the business and as per

management accounting tools and techniques, the managers of these companies can reduce the

cost of production in relevant form (Caglio and Ditillo, 2012). Organisational manager could

easily identify the sections of the business entity which is not functioning as per the

predetermined planning at the workplace so that manager of the business can easily identify them

can make improvement in the over service provision of the areas by which efficient development

can be executed in the business environment in effective manner.

Balance score card: Balance score card, this is also one of the essential management

accounting tools by which effective development can be executed and financial issues can be

resolved effectively. This is identified as the balance matrix card of the business in order to gain

more success in the market in more relevant form so that efficient development can be generated

in the business environment effectively. Manager of the company can use of this strategic

management approach in order to recognise the improvement in several internal functions of the

business entity and with the help of this tool, the organisational manager can make betterment in

the outcomes of the business in relevant form (Hilton and Platt, 2013). This could be used as the

measurement of the organisation in the industry in more relevant ways and the matrix of the

organisation furnish appropriate feedback and guidance in order to sustain in the market in more

relevant form. Data collection of the business is most necessary thing for proper development in

some areas by which effective development can be generated in more relevant form and this is

also made assistance in the improvement in the quantitative outcomes of the corporation

efficiently.

CONCLUSION

From the above analysis, it is concluded that, managerial accounting system is most

appropriate approach of the organisation in order to execute better administration at the

workplace in more effective manner. The organisation professional and accounting manager of

9

the company need to utilise of various accounting tools and techniques at the workplace in

respect to better preparation of management accounting reporting at the workplace in better

manner so that effective development can be executed and organisational objectives could be

improved in better manner in the industry. The organisational manger need to use of several

types of management accounting budgeting preparation tools and mechanism in order to sustain

in the market in more relevant form.

10

respect to better preparation of management accounting reporting at the workplace in better

manner so that effective development can be executed and organisational objectives could be

improved in better manner in the industry. The organisational manger need to use of several

types of management accounting budgeting preparation tools and mechanism in order to sustain

in the market in more relevant form.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.