Ryder Architecture: A Report on Management Accounting Practices

VerifiedAdded on 2023/03/23

|24

|5586

|73

Report

AI Summary

This report delves into the application of management accounting within Ryder Architecture, a UK-based small-scale enterprise. It examines various management accounting techniques, including lean accounting, throughput accounting, traditional accounting, and transfer pricing, highlighting their benefits and requirements in the context of Ryder Architecture's business operations. The report further analyzes the advantages and disadvantages of budgetary control planning tools and explores methods to tackle financial issues, such as benchmarking and key performance indicators. Practical applications, like marginal and absorption costing, are calculated and compared, providing a comprehensive understanding of how management accounting can aid Ryder Architecture in future planning, decision-making, cash flow prediction, and cost reduction.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

This report is based on the implementation of management accounting in the conduction of

business for Ryder Architecture. The various aspects of management accounting and the

importance of management accounting will be discussed in this report in detail. Furthermore,

two tables have been created for the purpose of calculations which are used to identify the

differences between marginal and absorption costing techniques of management accounting.

Page 1 of 24

This report is based on the implementation of management accounting in the conduction of

business for Ryder Architecture. The various aspects of management accounting and the

importance of management accounting will be discussed in this report in detail. Furthermore,

two tables have been created for the purpose of calculations which are used to identify the

differences between marginal and absorption costing techniques of management accounting.

Page 1 of 24

Table of contents

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

Introduction......................................................................................................................................4

Description of management accounting and highlighting the necessary requirements of various

types of management accounting systems to the chosen scenario..................................................5

Lean accounting...........................................................................................................................6

Throughput accounting................................................................................................................6

Traditional accounting.................................................................................................................7

Transfer pricing............................................................................................................................7

Inventory management system.....................................................................................................7

Benefits of Management Accounting..............................................................................................7

Plan for the future........................................................................................................................8

Decision making for the future....................................................................................................8

Predict cash flow..........................................................................................................................8

Reducing cost of production and increasing rate of return..........................................................8

Description of the various methods used for management accounting that can also be beneficial

for the chosen scenario....................................................................................................................9

Financial Planning........................................................................................................................9

Evaluation of the financial statements.........................................................................................9

Controlling budget.......................................................................................................................9

Marginal costing..........................................................................................................................9

Making decision.........................................................................................................................10

Statements of cash flow.............................................................................................................10

Page 2 of 24

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

Introduction......................................................................................................................................4

Description of management accounting and highlighting the necessary requirements of various

types of management accounting systems to the chosen scenario..................................................5

Lean accounting...........................................................................................................................6

Throughput accounting................................................................................................................6

Traditional accounting.................................................................................................................7

Transfer pricing............................................................................................................................7

Inventory management system.....................................................................................................7

Benefits of Management Accounting..............................................................................................7

Plan for the future........................................................................................................................8

Decision making for the future....................................................................................................8

Predict cash flow..........................................................................................................................8

Reducing cost of production and increasing rate of return..........................................................8

Description of the various methods used for management accounting that can also be beneficial

for the chosen scenario....................................................................................................................9

Financial Planning........................................................................................................................9

Evaluation of the financial statements.........................................................................................9

Controlling budget.......................................................................................................................9

Marginal costing..........................................................................................................................9

Making decision.........................................................................................................................10

Statements of cash flow.............................................................................................................10

Page 2 of 24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Representation of graphs and statistics......................................................................................10

Conclusion.....................................................................................................................................10

Task 2.............................................................................................................................................11

Introduction....................................................................................................................................11

Computation of the net profit percentage using Absorption Costing method...............................11

Computation of the net profit percentage using Marginal method................................................13

Differences between the Marginal and Absorption management accounting techniques.............15

Conclusion.....................................................................................................................................16

Task 3.............................................................................................................................................17

Introduction....................................................................................................................................17

Evaluation of the application of planning tools of budgetary control and understanding their

advantages and disadvantages.......................................................................................................17

Budget........................................................................................................................................17

Master budget.............................................................................................................................17

Operating budget........................................................................................................................18

Cash flow budget.......................................................................................................................18

Financial budget.........................................................................................................................18

Behavioural implications of budgeting..........................................................................................18

Pricing strategy..........................................................................................................................19

Supply and demand....................................................................................................................19

Applications of the various methods of Management accounting that can be used by

organisations to tackle financial issues..........................................................................................19

Benchmark.................................................................................................................................20

Key Performance Indicator (KPI)..............................................................................................20

Budgetary targets.......................................................................................................................20

Financial governance.................................................................................................................20

Page 3 of 24

Conclusion.....................................................................................................................................10

Task 2.............................................................................................................................................11

Introduction....................................................................................................................................11

Computation of the net profit percentage using Absorption Costing method...............................11

Computation of the net profit percentage using Marginal method................................................13

Differences between the Marginal and Absorption management accounting techniques.............15

Conclusion.....................................................................................................................................16

Task 3.............................................................................................................................................17

Introduction....................................................................................................................................17

Evaluation of the application of planning tools of budgetary control and understanding their

advantages and disadvantages.......................................................................................................17

Budget........................................................................................................................................17

Master budget.............................................................................................................................17

Operating budget........................................................................................................................18

Cash flow budget.......................................................................................................................18

Financial budget.........................................................................................................................18

Behavioural implications of budgeting..........................................................................................18

Pricing strategy..........................................................................................................................19

Supply and demand....................................................................................................................19

Applications of the various methods of Management accounting that can be used by

organisations to tackle financial issues..........................................................................................19

Benchmark.................................................................................................................................20

Key Performance Indicator (KPI)..............................................................................................20

Budgetary targets.......................................................................................................................20

Financial governance.................................................................................................................20

Page 3 of 24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting skills and their usefulness..................................................................20

Conclusion.....................................................................................................................................21

Conclusion.....................................................................................................................................21

Reference List................................................................................................................................22

Page 4 of 24

Conclusion.....................................................................................................................................21

Conclusion.....................................................................................................................................21

Reference List................................................................................................................................22

Page 4 of 24

Introduction

Management accounting is a technique used by the organisations to retrieve the correct data

regarding the amount of sales in a financial year, stock in hand or left in the inventory, raw

materials bought by the company, salary and wages of the staffs and so on. Therefore, it can be

said that applications and contributions of management accounting is huge in a business

organisation. In this report, the benefits of the applications of management accounting will be

discussed along with the advantages and disadvantages of the various tools of management

accounting.

The report is conducted as the General Manager of a company and the discussion on

management accounting of the company will be identified and evaluated in details. For better

understanding of the project the company that has been chosen is Ryder Architecture, which is a

small-scaled enterprise of the United Kingdom and the impact of the applications of management

accounting on the business conduction process and managing other records will be discussed.

Ryder Architecture is a company which is aiming at improving the internal and the external

architectural designs of properties of their clients and currently they are focusing on enhancing

their skills to serve their clients better.

Task 1

Introduction

This portion of the report will focus on the management accounting system of Ryder

Architecture and will also emphasise on the various types of management accounting that can be

incorporated by the company to be more effective in maintaining their books of accounts and

also planning on monitoring their allocated budget. Furthermore, the benefits of management

accounting used by Ryder Architecture that can help the company grow in the market will also

be discussed in this portion.

Page 5 of 24

Management accounting is a technique used by the organisations to retrieve the correct data

regarding the amount of sales in a financial year, stock in hand or left in the inventory, raw

materials bought by the company, salary and wages of the staffs and so on. Therefore, it can be

said that applications and contributions of management accounting is huge in a business

organisation. In this report, the benefits of the applications of management accounting will be

discussed along with the advantages and disadvantages of the various tools of management

accounting.

The report is conducted as the General Manager of a company and the discussion on

management accounting of the company will be identified and evaluated in details. For better

understanding of the project the company that has been chosen is Ryder Architecture, which is a

small-scaled enterprise of the United Kingdom and the impact of the applications of management

accounting on the business conduction process and managing other records will be discussed.

Ryder Architecture is a company which is aiming at improving the internal and the external

architectural designs of properties of their clients and currently they are focusing on enhancing

their skills to serve their clients better.

Task 1

Introduction

This portion of the report will focus on the management accounting system of Ryder

Architecture and will also emphasise on the various types of management accounting that can be

incorporated by the company to be more effective in maintaining their books of accounts and

also planning on monitoring their allocated budget. Furthermore, the benefits of management

accounting used by Ryder Architecture that can help the company grow in the market will also

be discussed in this portion.

Page 5 of 24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

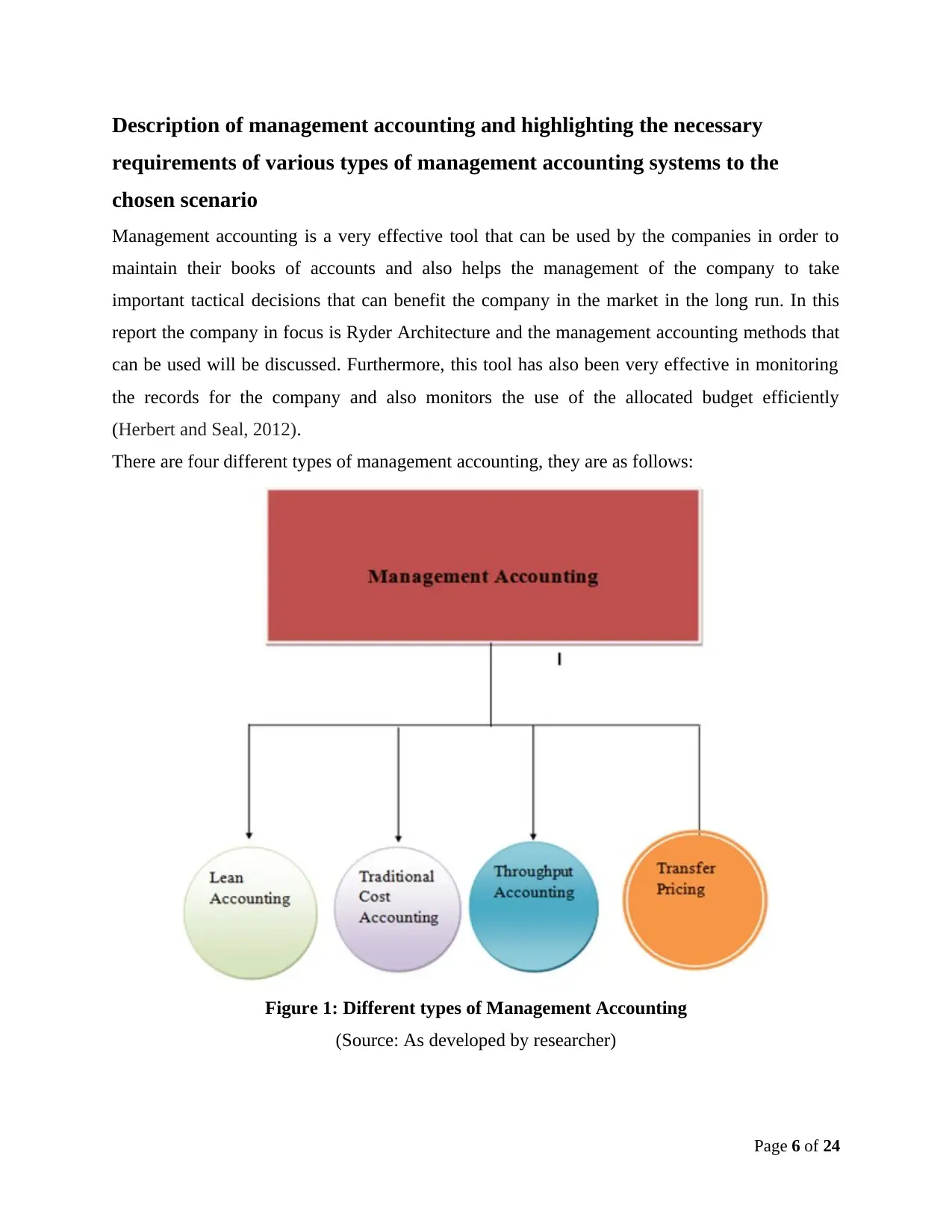

Description of management accounting and highlighting the necessary

requirements of various types of management accounting systems to the

chosen scenario

Management accounting is a very effective tool that can be used by the companies in order to

maintain their books of accounts and also helps the management of the company to take

important tactical decisions that can benefit the company in the market in the long run. In this

report the company in focus is Ryder Architecture and the management accounting methods that

can be used will be discussed. Furthermore, this tool has also been very effective in monitoring

the records for the company and also monitors the use of the allocated budget efficiently

(Herbert and Seal, 2012).

There are four different types of management accounting, they are as follows:

Figure 1: Different types of Management Accounting

(Source: As developed by researcher)

Page 6 of 24

requirements of various types of management accounting systems to the

chosen scenario

Management accounting is a very effective tool that can be used by the companies in order to

maintain their books of accounts and also helps the management of the company to take

important tactical decisions that can benefit the company in the market in the long run. In this

report the company in focus is Ryder Architecture and the management accounting methods that

can be used will be discussed. Furthermore, this tool has also been very effective in monitoring

the records for the company and also monitors the use of the allocated budget efficiently

(Herbert and Seal, 2012).

There are four different types of management accounting, they are as follows:

Figure 1: Different types of Management Accounting

(Source: As developed by researcher)

Page 6 of 24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lean accounting

The concept of Lean accounting highlights the fact that when changes are necessary within an

organisation, the management of the organisation adopts the principles of Lean accounting

methods. In the scenario regarding Ryder Architecture, the management of the company and

other organisational heads of the company can implement the concept of Lean accounting to

bring the necessary organisational changes. In addition to this, the concept of Lean accounting

does not focus the traditional methods wherein the focus was on mass production. Furthermore,

the concept of Lean accounting principle will help the management of Ryder Architecture in

maximising the profit margin by reducing the cost of production.

Figure 2: Principles of Lean accounting method

(Source: (Herbert and Seal, 2012).)

Throughput accounting

It is a simplified accounting system which is based on the Theory of Constraints. Throughput

accounting can be very effective and can also help the management of Ryder Architecture to take

better decisions for achieving growth in the market. The operations of throughput accounting

will help the management of Ryder Architecture to understand the basic concept of accounting.

Furthermore, this accounting method will also help the management of Ryder Architecture to

understand the market situation and take decisions related to investment and taking decisions for

making strategic changes (Hilmola and Gupta 2015).

Page 7 of 24

The concept of Lean accounting highlights the fact that when changes are necessary within an

organisation, the management of the organisation adopts the principles of Lean accounting

methods. In the scenario regarding Ryder Architecture, the management of the company and

other organisational heads of the company can implement the concept of Lean accounting to

bring the necessary organisational changes. In addition to this, the concept of Lean accounting

does not focus the traditional methods wherein the focus was on mass production. Furthermore,

the concept of Lean accounting principle will help the management of Ryder Architecture in

maximising the profit margin by reducing the cost of production.

Figure 2: Principles of Lean accounting method

(Source: (Herbert and Seal, 2012).)

Throughput accounting

It is a simplified accounting system which is based on the Theory of Constraints. Throughput

accounting can be very effective and can also help the management of Ryder Architecture to take

better decisions for achieving growth in the market. The operations of throughput accounting

will help the management of Ryder Architecture to understand the basic concept of accounting.

Furthermore, this accounting method will also help the management of Ryder Architecture to

understand the market situation and take decisions related to investment and taking decisions for

making strategic changes (Hilmola and Gupta 2015).

Page 7 of 24

Traditional accounting

The traditional accounting method is the oldest form of accounting method. The calculations

which are done in traditional accounting is based on the primitive method of calculations. Many

people consider the traditional accounting method to be advantageous and more flexible as

compared to other accounting methods. In scenarios, wherein Ryder Architecture is facing issues

with their business conduction process, then the management of the company can opt for

switching to the traditional accounting for better maintaining their books of accounts (Elsukova,

2015).

Transfer pricing

Transfer pricing is another type of management accounting wherein companies can control and

stabilise the prices for their manufactured products in all of their branches across the world (Tice

et al. 2015). For a company like Ryder Architecture, which has stock inventories in various

destinations across the borders, so the management of Ryder Architecture has to incorporate the

strategy of transfer pricing to reduce the cost of cross border control, taxation rules and other

issues which are associated with the transfer of the products across the borders like issues with

the custom clearance and so on.

Inventory management system

The management of Ryder Architecture can monitor the purchases and the sales made by the

company and can also manage the stock that is present in their inventory. Since, Ryder

Architecture business is spread across borders, so the management of the company needs to

monitor the stock that they have and also needs to monitor the amount of sales the company has

made along with the revenue earned by the company from sales. Therefore, this would allow the

management of Ryder Architecture to reduce the loss of stock and make use of the available

resources (Müller et al. 2015).

Benefits of Management Accounting

A company which adopts the management techniques of accounting reaps a number of benefits

which ranges from monitoring the stock in hand to making important decisions for the business.

This portion of the report focuses on discussing the benefits of management accounting that

Ryder Architecture can get if the management of the company implements the technique. In

Page 8 of 24

The traditional accounting method is the oldest form of accounting method. The calculations

which are done in traditional accounting is based on the primitive method of calculations. Many

people consider the traditional accounting method to be advantageous and more flexible as

compared to other accounting methods. In scenarios, wherein Ryder Architecture is facing issues

with their business conduction process, then the management of the company can opt for

switching to the traditional accounting for better maintaining their books of accounts (Elsukova,

2015).

Transfer pricing

Transfer pricing is another type of management accounting wherein companies can control and

stabilise the prices for their manufactured products in all of their branches across the world (Tice

et al. 2015). For a company like Ryder Architecture, which has stock inventories in various

destinations across the borders, so the management of Ryder Architecture has to incorporate the

strategy of transfer pricing to reduce the cost of cross border control, taxation rules and other

issues which are associated with the transfer of the products across the borders like issues with

the custom clearance and so on.

Inventory management system

The management of Ryder Architecture can monitor the purchases and the sales made by the

company and can also manage the stock that is present in their inventory. Since, Ryder

Architecture business is spread across borders, so the management of the company needs to

monitor the stock that they have and also needs to monitor the amount of sales the company has

made along with the revenue earned by the company from sales. Therefore, this would allow the

management of Ryder Architecture to reduce the loss of stock and make use of the available

resources (Müller et al. 2015).

Benefits of Management Accounting

A company which adopts the management techniques of accounting reaps a number of benefits

which ranges from monitoring the stock in hand to making important decisions for the business.

This portion of the report focuses on discussing the benefits of management accounting that

Ryder Architecture can get if the management of the company implements the technique. In

Page 8 of 24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

addition to these benefits, management accounting can help an organisation in numerous ways

which are as follows:

Plan for the future

The principles of Management accounting can help the management of Ryder Architecture to

take necessary decisions for the company which can be related to investment in business or

acquiring business or collaborating with other companies and so on. Furthermore, the

management accounting techniques can also help the management of Ryder Architecture to

understand the tastes and preferences of the customers and likewise the company can undertake

strategies and allocate budget to develop relevant products (Lavia López and Hiebl 2014).

Decision making for the future

As per the market data, most of the managers of the companies are more inclined to the

qualitative information in order to take important decisions for the future of the business. The

dependence on the qualitative data for the managers have proved to be not so efficient as the data

provided has numerous gaps. This is where management accounting comes into action as it can

fill the gaps and help the management of Ryder Architecture to take decisions to meet the future

demands (Crutzen et al. 2016).

Predict cash flow

Predicting the cash flow is one of the most important phases in a business organisation, the

management and the hierarchy of the managers of Ryder Architecture has to monitor the cash

flow to understand the use of allocated budget and predicting the amount of revenue that can be

generated and setting the price of the products per unit accordingly.

Reducing cost of production and increasing rate of return

The applications of Management accounting can also be understood wherein the management of

Ryder Architecture can optimise the available resources by reducing the cost of production and

increasing the margin of profit by stabilising the price at a certain range (Adenike and Michael

2016).

Page 9 of 24

which are as follows:

Plan for the future

The principles of Management accounting can help the management of Ryder Architecture to

take necessary decisions for the company which can be related to investment in business or

acquiring business or collaborating with other companies and so on. Furthermore, the

management accounting techniques can also help the management of Ryder Architecture to

understand the tastes and preferences of the customers and likewise the company can undertake

strategies and allocate budget to develop relevant products (Lavia López and Hiebl 2014).

Decision making for the future

As per the market data, most of the managers of the companies are more inclined to the

qualitative information in order to take important decisions for the future of the business. The

dependence on the qualitative data for the managers have proved to be not so efficient as the data

provided has numerous gaps. This is where management accounting comes into action as it can

fill the gaps and help the management of Ryder Architecture to take decisions to meet the future

demands (Crutzen et al. 2016).

Predict cash flow

Predicting the cash flow is one of the most important phases in a business organisation, the

management and the hierarchy of the managers of Ryder Architecture has to monitor the cash

flow to understand the use of allocated budget and predicting the amount of revenue that can be

generated and setting the price of the products per unit accordingly.

Reducing cost of production and increasing rate of return

The applications of Management accounting can also be understood wherein the management of

Ryder Architecture can optimise the available resources by reducing the cost of production and

increasing the margin of profit by stabilising the price at a certain range (Adenike and Michael

2016).

Page 9 of 24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Description of the various methods used for management accounting that can

also be beneficial for the chosen scenario

The other management accounting tool that can be used to benefit Ryder Architecture to perform

better in the market are as follows:

Financial Planning

This type of planning is associated with the planning related to the budget of Ryder Architecture.

The management of Ryder Architecture has to undertake the changes and make decisions based

on the financial situation of the company. Therefore, the management of Ryder Architecture has

to make decisions which would make the company achieve the organisational goals as well.

Evaluation of the financial statements

The phase that is associated with the analysis of the financial statements will help the

management of Ryder Architecture to understand the cost that the company has to incur and the

revenue that would be generated from the sales as per the prices set per unit. The analysis also

helps the company to analyse the opportunities and risks, evaluate and understand the cash flow,

income statements and balance sheet for the business in a financial year (Kansal et al. 2013).

Controlling budget

The management of Ryder Architecture has to identify the possible ways they can save money

and make use of the allocated budget for maximising production and profit. When the company

controls the budget, wastage of resources is minimised and the company can boost their

production in the entire process (Yao et al. 2014).

Marginal costing

This is a term associated with management accounting where the production for Ryder

Architecture can get affected if there is any increase or decrease in the production of the products

by Ryder Architecture. Therefore, the expense that has been incurred by the company due to

change in production of one unit of the product is referred to as marginal costing.

Page 10 of 24

also be beneficial for the chosen scenario

The other management accounting tool that can be used to benefit Ryder Architecture to perform

better in the market are as follows:

Financial Planning

This type of planning is associated with the planning related to the budget of Ryder Architecture.

The management of Ryder Architecture has to undertake the changes and make decisions based

on the financial situation of the company. Therefore, the management of Ryder Architecture has

to make decisions which would make the company achieve the organisational goals as well.

Evaluation of the financial statements

The phase that is associated with the analysis of the financial statements will help the

management of Ryder Architecture to understand the cost that the company has to incur and the

revenue that would be generated from the sales as per the prices set per unit. The analysis also

helps the company to analyse the opportunities and risks, evaluate and understand the cash flow,

income statements and balance sheet for the business in a financial year (Kansal et al. 2013).

Controlling budget

The management of Ryder Architecture has to identify the possible ways they can save money

and make use of the allocated budget for maximising production and profit. When the company

controls the budget, wastage of resources is minimised and the company can boost their

production in the entire process (Yao et al. 2014).

Marginal costing

This is a term associated with management accounting where the production for Ryder

Architecture can get affected if there is any increase or decrease in the production of the products

by Ryder Architecture. Therefore, the expense that has been incurred by the company due to

change in production of one unit of the product is referred to as marginal costing.

Page 10 of 24

Making decision

Based on the expenditures that Ryder Architecture has to incur during the production phase,

management accounting would help the management of the company to make strategic changes

to gain competitive advantage over the rivals (Venugopalan et al. 2014).

Statements of cash flow

A company should always analyse its cash in hand and the amount of credit the company has in

the market in terms of liquidity. Therefore, it is important for the company to maintain its

liquidity so that the management can pay when the necessity arises. The same goes for Ryder

Architecture, the management of the company should maintain the cash reserve to maintain a

balance between the various types of assets and cash in hand (Zhu et al. 2016).

Representation of graphs and statistics

The management of Ryder Architecture can use management accounting to develop different

types of statistical representations and data interpretation. This information proves to be relevant

and helps the company to understand the market situation and demands and take necessary steps

to respond to the changes in the market.

Conclusion

After completing the studies and the researches on the various aspects of management

accounting, the importance of management accounting and its various tools has been identified.

This portion of the report also focuses on the explanation of the various concepts associated with

the aspects of management accounting and the ways by which Ryder Architecture can make full

use of management accounting and benefit from it. In addition to this, the importance and

various types of management accounting implemented by the different organisations has also

been explained in the aforementioned points.

Page 11 of 24

Based on the expenditures that Ryder Architecture has to incur during the production phase,

management accounting would help the management of the company to make strategic changes

to gain competitive advantage over the rivals (Venugopalan et al. 2014).

Statements of cash flow

A company should always analyse its cash in hand and the amount of credit the company has in

the market in terms of liquidity. Therefore, it is important for the company to maintain its

liquidity so that the management can pay when the necessity arises. The same goes for Ryder

Architecture, the management of the company should maintain the cash reserve to maintain a

balance between the various types of assets and cash in hand (Zhu et al. 2016).

Representation of graphs and statistics

The management of Ryder Architecture can use management accounting to develop different

types of statistical representations and data interpretation. This information proves to be relevant

and helps the company to understand the market situation and demands and take necessary steps

to respond to the changes in the market.

Conclusion

After completing the studies and the researches on the various aspects of management

accounting, the importance of management accounting and its various tools has been identified.

This portion of the report also focuses on the explanation of the various concepts associated with

the aspects of management accounting and the ways by which Ryder Architecture can make full

use of management accounting and benefit from it. In addition to this, the importance and

various types of management accounting implemented by the different organisations has also

been explained in the aforementioned points.

Page 11 of 24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.