Comparative Financial Analysis of Sainsbury and Tesco: 2018-2019

VerifiedAdded on 2023/01/03

|14

|3777

|26

Report

AI Summary

This report provides a comprehensive financial analysis of Sainsbury and Tesco, two major UK supermarket chains, for the years 2018 and 2019. It begins with a detailed presentation of key financial ratios, including liquidity, profitability, efficiency, gearing, and investor ratios, calculated from the companies' financial statements. The analysis delves into the performance and financial positions of both companies, highlighting their strengths and weaknesses based on the calculated ratios. The report then offers recommendations for improving the financial performance of the companies, focusing on strategies to enhance profitability and liquidity. Finally, it acknowledges the limitations of relying solely on financial ratios for performance interpretation, such as the dependence on historical data and the exclusion of market conditions. The report concludes by assessing the investment potential of each company based on the financial analysis conducted.

MANAGERIAL FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PORTFOLIO 1.................................................................................................................................3

a) Financial Ratios of Sainsbury and Tesco for the year ending 2018 & 2019...........................3

b) Analysis of performance, financial position and the investment potential of Sainsbury and

Tesco............................................................................................................................................5

c. Recommendation on improving the financial performance of company.................................8

d. Limitation of relying over financial ratios in interpreting performance of company..............9

PORTOFOLIO 2..............................................................................................................................9

a. Use of appropriate investment appraisal techniques for project A and project B....................9

b. Limitation of using the investment appraisal techniques in long term decision making.......13

REFERENCES..............................................................................................................................15

PORTFOLIO 1.................................................................................................................................3

a) Financial Ratios of Sainsbury and Tesco for the year ending 2018 & 2019...........................3

b) Analysis of performance, financial position and the investment potential of Sainsbury and

Tesco............................................................................................................................................5

c. Recommendation on improving the financial performance of company.................................8

d. Limitation of relying over financial ratios in interpreting performance of company..............9

PORTOFOLIO 2..............................................................................................................................9

a. Use of appropriate investment appraisal techniques for project A and project B....................9

b. Limitation of using the investment appraisal techniques in long term decision making.......13

REFERENCES..............................................................................................................................15

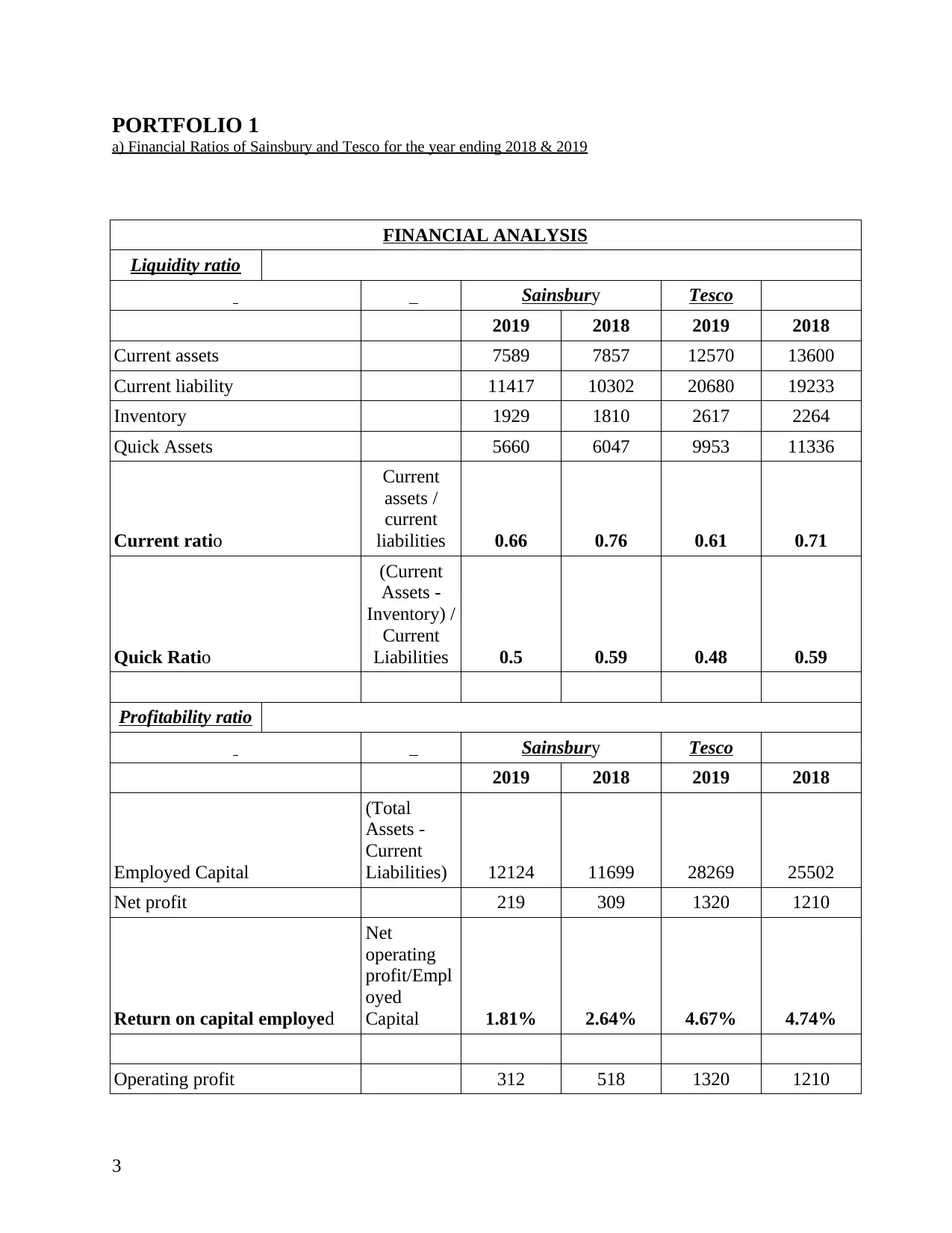

PORTFOLIO 1

a) Financial Ratios of Sainsbury and Tesco for the year ending 2018 & 2019

FINANCIAL ANALYSIS

Liquidity ratio

Sainsbury Tesco

2019 2018 2019 2018

Current assets 7589 7857 12570 13600

Current liability 11417 10302 20680 19233

Inventory 1929 1810 2617 2264

Quick Assets 5660 6047 9953 11336

Current ratio

Current

assets /

current

liabilities 0.66 0.76 0.61 0.71

Quick Ratio

(Current

Assets -

Inventory) /

Current

Liabilities 0.5 0.59 0.48 0.59

Profitability ratio

Sainsbury Tesco

2019 2018 2019 2018

Employed Capital

(Total

Assets -

Current

Liabilities) 12124 11699 28269 25502

Net profit 219 309 1320 1210

Return on capital employed

Net

operating

profit/Empl

oyed

Capital 1.81% 2.64% 4.67% 4.74%

Operating profit 312 518 1320 1210

3

a) Financial Ratios of Sainsbury and Tesco for the year ending 2018 & 2019

FINANCIAL ANALYSIS

Liquidity ratio

Sainsbury Tesco

2019 2018 2019 2018

Current assets 7589 7857 12570 13600

Current liability 11417 10302 20680 19233

Inventory 1929 1810 2617 2264

Quick Assets 5660 6047 9953 11336

Current ratio

Current

assets /

current

liabilities 0.66 0.76 0.61 0.71

Quick Ratio

(Current

Assets -

Inventory) /

Current

Liabilities 0.5 0.59 0.48 0.59

Profitability ratio

Sainsbury Tesco

2019 2018 2019 2018

Employed Capital

(Total

Assets -

Current

Liabilities) 12124 11699 28269 25502

Net profit 219 309 1320 1210

Return on capital employed

Net

operating

profit/Empl

oyed

Capital 1.81% 2.64% 4.67% 4.74%

Operating profit 312 518 1320 1210

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shareholder's Equity 8456 7411 14858 10502

Return on Equity

Net Income

/

Shareholder

's Equity 2.57% 4.43% 7.62% 7.21%

Sainsbury Tesco

2019 2018 2019 2018

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Gross Margin

Total Sales –

COGS/Total

Sales 6.92% 6.61% 6.48% 5.83%

Net profit 219 309 1320 1210

Sales 29007 28456 63911 57493

Net profit ratio

Operating

Income/ Net

Sales 0.75% 1.09% 2.07% 2.10%

Efficiency Ratios

Sainsbury Tesco

2019 2018 2019 2018

Trade Payables 4444 4322 9354 8994

Trade Receivables 661 744 1640 1504

Net Assets 8456 7411 14858 10502

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Inventory turnover ratio

Inventory/

Cost of

Sales *365 26 25 16 15

Accounts Payable Days

Accounts

payable

/Cost of

Sales *365 60 59 57 61

Account receivable days

Accounts

Receivable /

Cost of Sales

* 365 9 10 10 10

Gearing Ratios

Sainsbury Tesco

4

Return on Equity

Net Income

/

Shareholder

's Equity 2.57% 4.43% 7.62% 7.21%

Sainsbury Tesco

2019 2018 2019 2018

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Gross Margin

Total Sales –

COGS/Total

Sales 6.92% 6.61% 6.48% 5.83%

Net profit 219 309 1320 1210

Sales 29007 28456 63911 57493

Net profit ratio

Operating

Income/ Net

Sales 0.75% 1.09% 2.07% 2.10%

Efficiency Ratios

Sainsbury Tesco

2019 2018 2019 2018

Trade Payables 4444 4322 9354 8994

Trade Receivables 661 744 1640 1504

Net Assets 8456 7411 14858 10502

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Inventory turnover ratio

Inventory/

Cost of

Sales *365 26 25 16 15

Accounts Payable Days

Accounts

payable

/Cost of

Sales *365 60 59 57 61

Account receivable days

Accounts

Receivable /

Cost of Sales

* 365 9 10 10 10

Gearing Ratios

Sainsbury Tesco

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

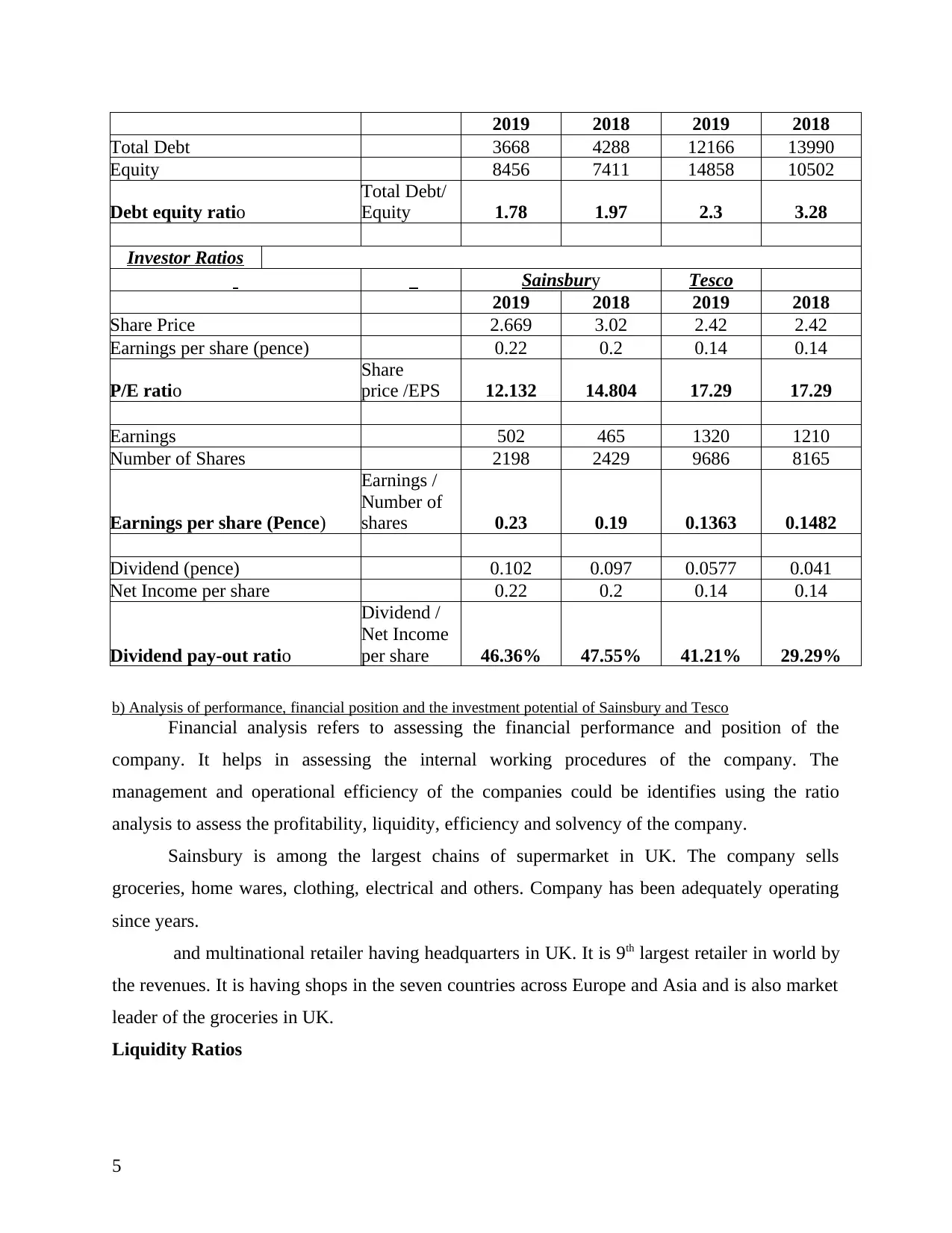

2019 2018 2019 2018

Total Debt 3668 4288 12166 13990

Equity 8456 7411 14858 10502

Debt equity ratio

Total Debt/

Equity 1.78 1.97 2.3 3.28

Investor Ratios

Sainsbury Tesco

2019 2018 2019 2018

Share Price 2.669 3.02 2.42 2.42

Earnings per share (pence) 0.22 0.2 0.14 0.14

P/E ratio

Share

price /EPS 12.132 14.804 17.29 17.29

Earnings 502 465 1320 1210

Number of Shares 2198 2429 9686 8165

Earnings per share (Pence)

Earnings /

Number of

shares 0.23 0.19 0.1363 0.1482

Dividend (pence) 0.102 0.097 0.0577 0.041

Net Income per share 0.22 0.2 0.14 0.14

Dividend pay-out ratio

Dividend /

Net Income

per share 46.36% 47.55% 41.21% 29.29%

b) Analysis of performance, financial position and the investment potential of Sainsbury and Tesco

Financial analysis refers to assessing the financial performance and position of the

company. It helps in assessing the internal working procedures of the company. The

management and operational efficiency of the companies could be identifies using the ratio

analysis to assess the profitability, liquidity, efficiency and solvency of the company.

Sainsbury is among the largest chains of supermarket in UK. The company sells

groceries, home wares, clothing, electrical and others. Company has been adequately operating

since years.

and multinational retailer having headquarters in UK. It is 9th largest retailer in world by

the revenues. It is having shops in the seven countries across Europe and Asia and is also market

leader of the groceries in UK.

Liquidity Ratios

5

Total Debt 3668 4288 12166 13990

Equity 8456 7411 14858 10502

Debt equity ratio

Total Debt/

Equity 1.78 1.97 2.3 3.28

Investor Ratios

Sainsbury Tesco

2019 2018 2019 2018

Share Price 2.669 3.02 2.42 2.42

Earnings per share (pence) 0.22 0.2 0.14 0.14

P/E ratio

Share

price /EPS 12.132 14.804 17.29 17.29

Earnings 502 465 1320 1210

Number of Shares 2198 2429 9686 8165

Earnings per share (Pence)

Earnings /

Number of

shares 0.23 0.19 0.1363 0.1482

Dividend (pence) 0.102 0.097 0.0577 0.041

Net Income per share 0.22 0.2 0.14 0.14

Dividend pay-out ratio

Dividend /

Net Income

per share 46.36% 47.55% 41.21% 29.29%

b) Analysis of performance, financial position and the investment potential of Sainsbury and Tesco

Financial analysis refers to assessing the financial performance and position of the

company. It helps in assessing the internal working procedures of the company. The

management and operational efficiency of the companies could be identifies using the ratio

analysis to assess the profitability, liquidity, efficiency and solvency of the company.

Sainsbury is among the largest chains of supermarket in UK. The company sells

groceries, home wares, clothing, electrical and others. Company has been adequately operating

since years.

and multinational retailer having headquarters in UK. It is 9th largest retailer in world by

the revenues. It is having shops in the seven countries across Europe and Asia and is also market

leader of the groceries in UK.

Liquidity Ratios

5

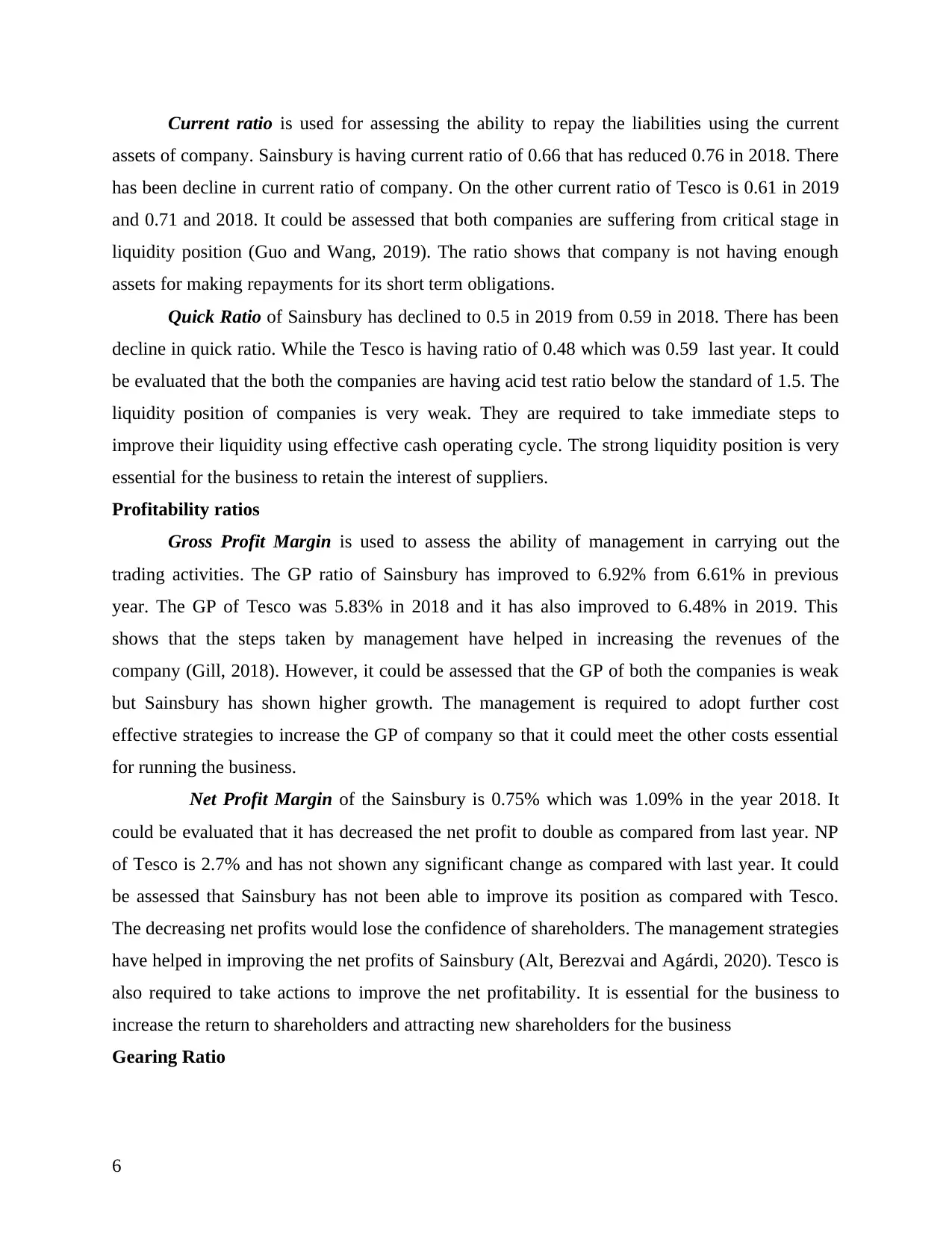

Current ratio is used for assessing the ability to repay the liabilities using the current

assets of company. Sainsbury is having current ratio of 0.66 that has reduced 0.76 in 2018. There

has been decline in current ratio of company. On the other current ratio of Tesco is 0.61 in 2019

and 0.71 and 2018. It could be assessed that both companies are suffering from critical stage in

liquidity position (Guo and Wang, 2019). The ratio shows that company is not having enough

assets for making repayments for its short term obligations.

Quick Ratio of Sainsbury has declined to 0.5 in 2019 from 0.59 in 2018. There has been

decline in quick ratio. While the Tesco is having ratio of 0.48 which was 0.59 last year. It could

be evaluated that the both the companies are having acid test ratio below the standard of 1.5. The

liquidity position of companies is very weak. They are required to take immediate steps to

improve their liquidity using effective cash operating cycle. The strong liquidity position is very

essential for the business to retain the interest of suppliers.

Profitability ratios

Gross Profit Margin is used to assess the ability of management in carrying out the

trading activities. The GP ratio of Sainsbury has improved to 6.92% from 6.61% in previous

year. The GP of Tesco was 5.83% in 2018 and it has also improved to 6.48% in 2019. This

shows that the steps taken by management have helped in increasing the revenues of the

company (Gill, 2018). However, it could be assessed that the GP of both the companies is weak

but Sainsbury has shown higher growth. The management is required to adopt further cost

effective strategies to increase the GP of company so that it could meet the other costs essential

for running the business.

Net Profit Margin of the Sainsbury is 0.75% which was 1.09% in the year 2018. It

could be evaluated that it has decreased the net profit to double as compared from last year. NP

of Tesco is 2.7% and has not shown any significant change as compared with last year. It could

be assessed that Sainsbury has not been able to improve its position as compared with Tesco.

The decreasing net profits would lose the confidence of shareholders. The management strategies

have helped in improving the net profits of Sainsbury (Alt, Berezvai and Agárdi, 2020). Tesco is

also required to take actions to improve the net profitability. It is essential for the business to

increase the return to shareholders and attracting new shareholders for the business

Gearing Ratio

6

assets of company. Sainsbury is having current ratio of 0.66 that has reduced 0.76 in 2018. There

has been decline in current ratio of company. On the other current ratio of Tesco is 0.61 in 2019

and 0.71 and 2018. It could be assessed that both companies are suffering from critical stage in

liquidity position (Guo and Wang, 2019). The ratio shows that company is not having enough

assets for making repayments for its short term obligations.

Quick Ratio of Sainsbury has declined to 0.5 in 2019 from 0.59 in 2018. There has been

decline in quick ratio. While the Tesco is having ratio of 0.48 which was 0.59 last year. It could

be evaluated that the both the companies are having acid test ratio below the standard of 1.5. The

liquidity position of companies is very weak. They are required to take immediate steps to

improve their liquidity using effective cash operating cycle. The strong liquidity position is very

essential for the business to retain the interest of suppliers.

Profitability ratios

Gross Profit Margin is used to assess the ability of management in carrying out the

trading activities. The GP ratio of Sainsbury has improved to 6.92% from 6.61% in previous

year. The GP of Tesco was 5.83% in 2018 and it has also improved to 6.48% in 2019. This

shows that the steps taken by management have helped in increasing the revenues of the

company (Gill, 2018). However, it could be assessed that the GP of both the companies is weak

but Sainsbury has shown higher growth. The management is required to adopt further cost

effective strategies to increase the GP of company so that it could meet the other costs essential

for running the business.

Net Profit Margin of the Sainsbury is 0.75% which was 1.09% in the year 2018. It

could be evaluated that it has decreased the net profit to double as compared from last year. NP

of Tesco is 2.7% and has not shown any significant change as compared with last year. It could

be assessed that Sainsbury has not been able to improve its position as compared with Tesco.

The decreasing net profits would lose the confidence of shareholders. The management strategies

have helped in improving the net profits of Sainsbury (Alt, Berezvai and Agárdi, 2020). Tesco is

also required to take actions to improve the net profitability. It is essential for the business to

increase the return to shareholders and attracting new shareholders for the business

Gearing Ratio

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

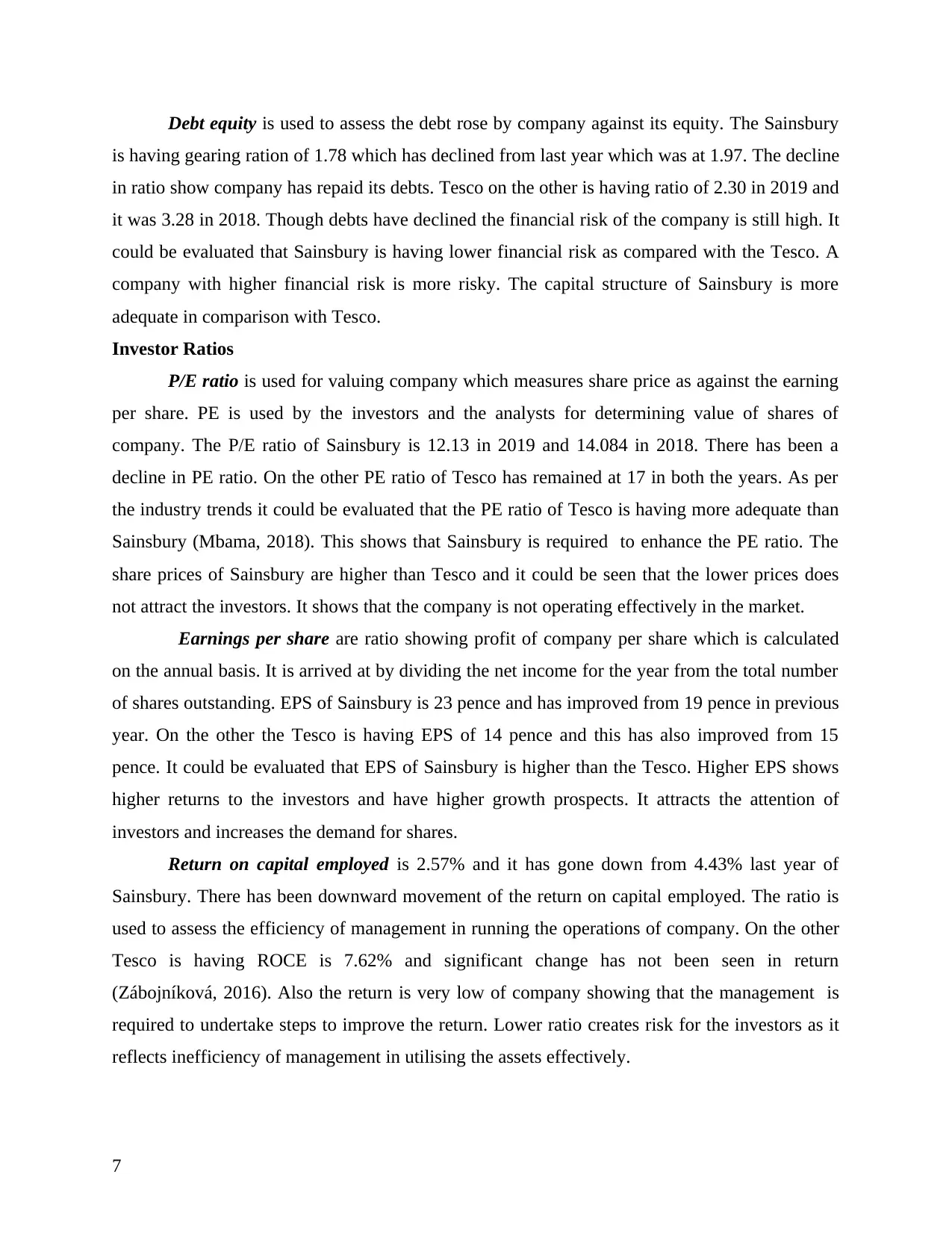

Debt equity is used to assess the debt rose by company against its equity. The Sainsbury

is having gearing ration of 1.78 which has declined from last year which was at 1.97. The decline

in ratio show company has repaid its debts. Tesco on the other is having ratio of 2.30 in 2019 and

it was 3.28 in 2018. Though debts have declined the financial risk of the company is still high. It

could be evaluated that Sainsbury is having lower financial risk as compared with the Tesco. A

company with higher financial risk is more risky. The capital structure of Sainsbury is more

adequate in comparison with Tesco.

Investor Ratios

P/E ratio is used for valuing company which measures share price as against the earning

per share. PE is used by the investors and the analysts for determining value of shares of

company. The P/E ratio of Sainsbury is 12.13 in 2019 and 14.084 in 2018. There has been a

decline in PE ratio. On the other PE ratio of Tesco has remained at 17 in both the years. As per

the industry trends it could be evaluated that the PE ratio of Tesco is having more adequate than

Sainsbury (Mbama, 2018). This shows that Sainsbury is required to enhance the PE ratio. The

share prices of Sainsbury are higher than Tesco and it could be seen that the lower prices does

not attract the investors. It shows that the company is not operating effectively in the market.

Earnings per share are ratio showing profit of company per share which is calculated

on the annual basis. It is arrived at by dividing the net income for the year from the total number

of shares outstanding. EPS of Sainsbury is 23 pence and has improved from 19 pence in previous

year. On the other the Tesco is having EPS of 14 pence and this has also improved from 15

pence. It could be evaluated that EPS of Sainsbury is higher than the Tesco. Higher EPS shows

higher returns to the investors and have higher growth prospects. It attracts the attention of

investors and increases the demand for shares.

Return on capital employed is 2.57% and it has gone down from 4.43% last year of

Sainsbury. There has been downward movement of the return on capital employed. The ratio is

used to assess the efficiency of management in running the operations of company. On the other

Tesco is having ROCE is 7.62% and significant change has not been seen in return

(Zábojníková, 2016). Also the return is very low of company showing that the management is

required to undertake steps to improve the return. Lower ratio creates risk for the investors as it

reflects inefficiency of management in utilising the assets effectively.

7

is having gearing ration of 1.78 which has declined from last year which was at 1.97. The decline

in ratio show company has repaid its debts. Tesco on the other is having ratio of 2.30 in 2019 and

it was 3.28 in 2018. Though debts have declined the financial risk of the company is still high. It

could be evaluated that Sainsbury is having lower financial risk as compared with the Tesco. A

company with higher financial risk is more risky. The capital structure of Sainsbury is more

adequate in comparison with Tesco.

Investor Ratios

P/E ratio is used for valuing company which measures share price as against the earning

per share. PE is used by the investors and the analysts for determining value of shares of

company. The P/E ratio of Sainsbury is 12.13 in 2019 and 14.084 in 2018. There has been a

decline in PE ratio. On the other PE ratio of Tesco has remained at 17 in both the years. As per

the industry trends it could be evaluated that the PE ratio of Tesco is having more adequate than

Sainsbury (Mbama, 2018). This shows that Sainsbury is required to enhance the PE ratio. The

share prices of Sainsbury are higher than Tesco and it could be seen that the lower prices does

not attract the investors. It shows that the company is not operating effectively in the market.

Earnings per share are ratio showing profit of company per share which is calculated

on the annual basis. It is arrived at by dividing the net income for the year from the total number

of shares outstanding. EPS of Sainsbury is 23 pence and has improved from 19 pence in previous

year. On the other the Tesco is having EPS of 14 pence and this has also improved from 15

pence. It could be evaluated that EPS of Sainsbury is higher than the Tesco. Higher EPS shows

higher returns to the investors and have higher growth prospects. It attracts the attention of

investors and increases the demand for shares.

Return on capital employed is 2.57% and it has gone down from 4.43% last year of

Sainsbury. There has been downward movement of the return on capital employed. The ratio is

used to assess the efficiency of management in running the operations of company. On the other

Tesco is having ROCE is 7.62% and significant change has not been seen in return

(Zábojníková, 2016). Also the return is very low of company showing that the management is

required to undertake steps to improve the return. Lower ratio creates risk for the investors as it

reflects inefficiency of management in utilising the assets effectively.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventories Turnover of Sainsbury is 26 days and on the other of Tesco it is 16 days.

Inventory turnover of both the companies have increased as compared with previous year. It

could be evaluated that Tesco is having high turnover ratio in comparison with Sainsbury.

Higher turnover reflects management efficiency to generate sales.

Dividend Payout ratio of the Sainsbury is 46.36% any major changes has not been seen.

The Tesco is having payout of 44.38%. Higher payout ratio shows that investors are getting

adequate returns over their investments.

From the above analysis it could be evaluated that financial performance, position and the

investor ratios of Sainsbury are adequate as compared with Tesco.

c. Recommendation on improving the financial performance of company

With the above analysis it is clear that company is having low financial performance as

compared to the other company. Thus, for this some of the major recommendation to improve

the financial position are as follows-

The major recommendation to the company is to manage and try to decrease the expenses

of the company. This is majorly required because of the reason that when the company will limit

their expenses then this will increase the profitability of the company.

Another major recommendation for the company in improving the financial position is to

hire a professional or an expert in the field of investment management. This is particularly

because of the reason that when the company will hire a professional then this will increase the

efficiency of the company in taking decision relating to the better allocation of the limited funds.

Along with this another major recommendation for the company is that they must

increase their current assets so that the current liabilities can be paid off easily. Further it is

advisable to company that they must maintain the ideal current ratio of 2: 1 so that they have

enough liquidity of the funds.

In addition to this another major recommendation to improve the financial position of the

company is that try to increase net profit ratio of the company. This is particularly because of the

reason that when the company will have higher net profit ratio then it reflects that the company is

earning higher profits.

8

Inventory turnover of both the companies have increased as compared with previous year. It

could be evaluated that Tesco is having high turnover ratio in comparison with Sainsbury.

Higher turnover reflects management efficiency to generate sales.

Dividend Payout ratio of the Sainsbury is 46.36% any major changes has not been seen.

The Tesco is having payout of 44.38%. Higher payout ratio shows that investors are getting

adequate returns over their investments.

From the above analysis it could be evaluated that financial performance, position and the

investor ratios of Sainsbury are adequate as compared with Tesco.

c. Recommendation on improving the financial performance of company

With the above analysis it is clear that company is having low financial performance as

compared to the other company. Thus, for this some of the major recommendation to improve

the financial position are as follows-

The major recommendation to the company is to manage and try to decrease the expenses

of the company. This is majorly required because of the reason that when the company will limit

their expenses then this will increase the profitability of the company.

Another major recommendation for the company in improving the financial position is to

hire a professional or an expert in the field of investment management. This is particularly

because of the reason that when the company will hire a professional then this will increase the

efficiency of the company in taking decision relating to the better allocation of the limited funds.

Along with this another major recommendation for the company is that they must

increase their current assets so that the current liabilities can be paid off easily. Further it is

advisable to company that they must maintain the ideal current ratio of 2: 1 so that they have

enough liquidity of the funds.

In addition to this another major recommendation to improve the financial position of the

company is that try to increase net profit ratio of the company. This is particularly because of the

reason that when the company will have higher net profit ratio then it reflects that the company is

earning higher profits.

8

d. Limitation of relying over financial ratios in interpreting performance of company

Financial ratio analysis is most common technique used to interpret company's

performance (Michael and et.al., 2020). It helps the company to depicts the important financial

parameters, however being useful tool it has some limitation also.

a) Based on only Historical:

Financial ratios are based on historical information which is irrelevant because the technique

assumes that history repeat but it’s not accurate when business model and product line has

changed.

b) Does not considered the market condition:

Financial Ratios analysis does not corporate with changing market condition. Its Interpretation is

based on only previous data so its interpretation is neither accurate nor practical (Sriram, 2020).

c)Considered the position of Business on particular date:

Financial ratio analysis uses the company's balance sheet information to interpret the company's

position which not accurate as its figures are based on historical data.

d)Does not considered the impact of inflation:

Ratio analysis does not consider the price rise and uses only historical prices that tend to predict

historical position only which is biggest limitation of financial ratio analysis. Ratio analysis is

based on financial statements prepared by company so it only considered quantitative data and

not qualitative which is biggest limitation (Kadim, Sunardi and Husain, 2020).

PORTOFOLIO 2

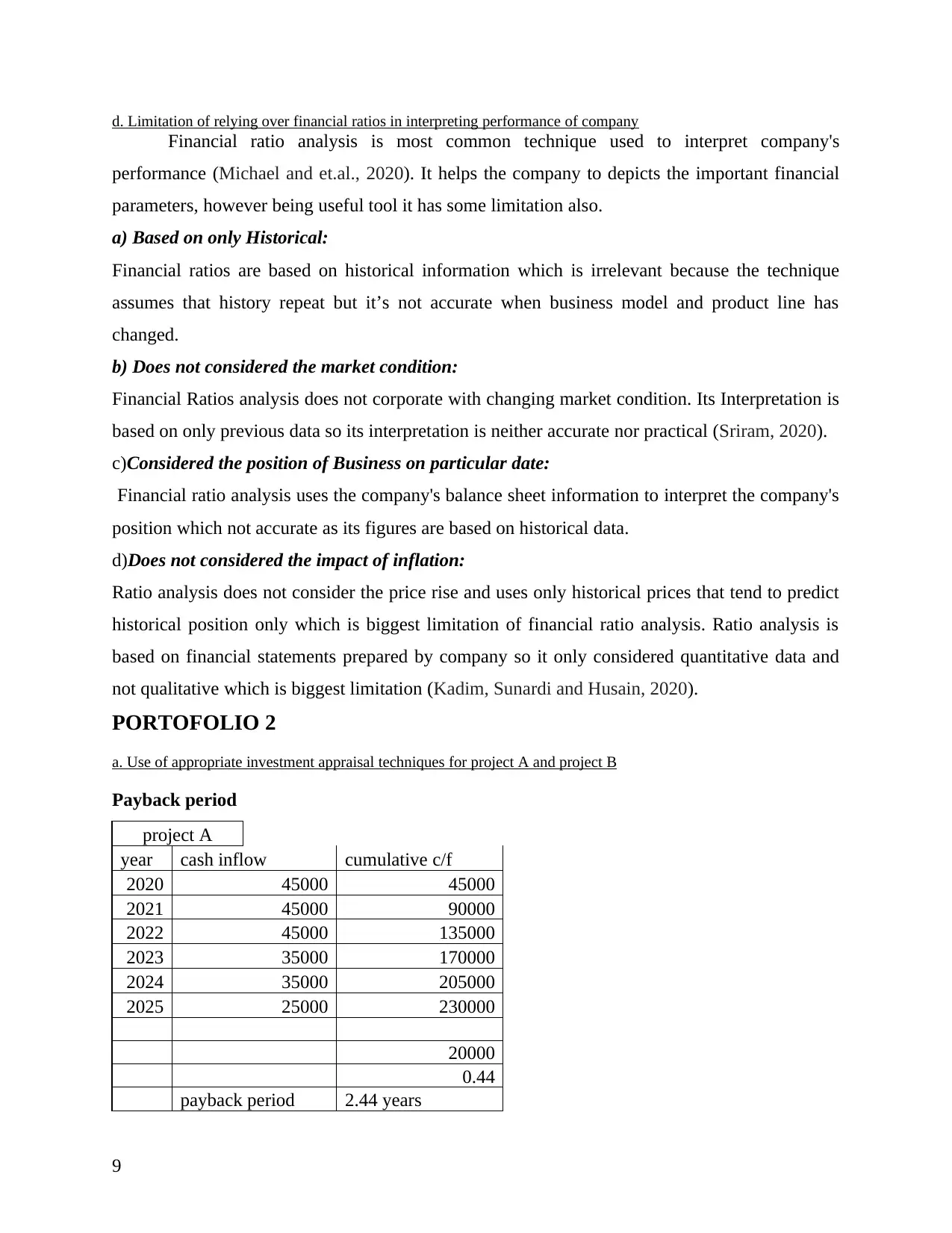

a. Use of appropriate investment appraisal techniques for project A and project B

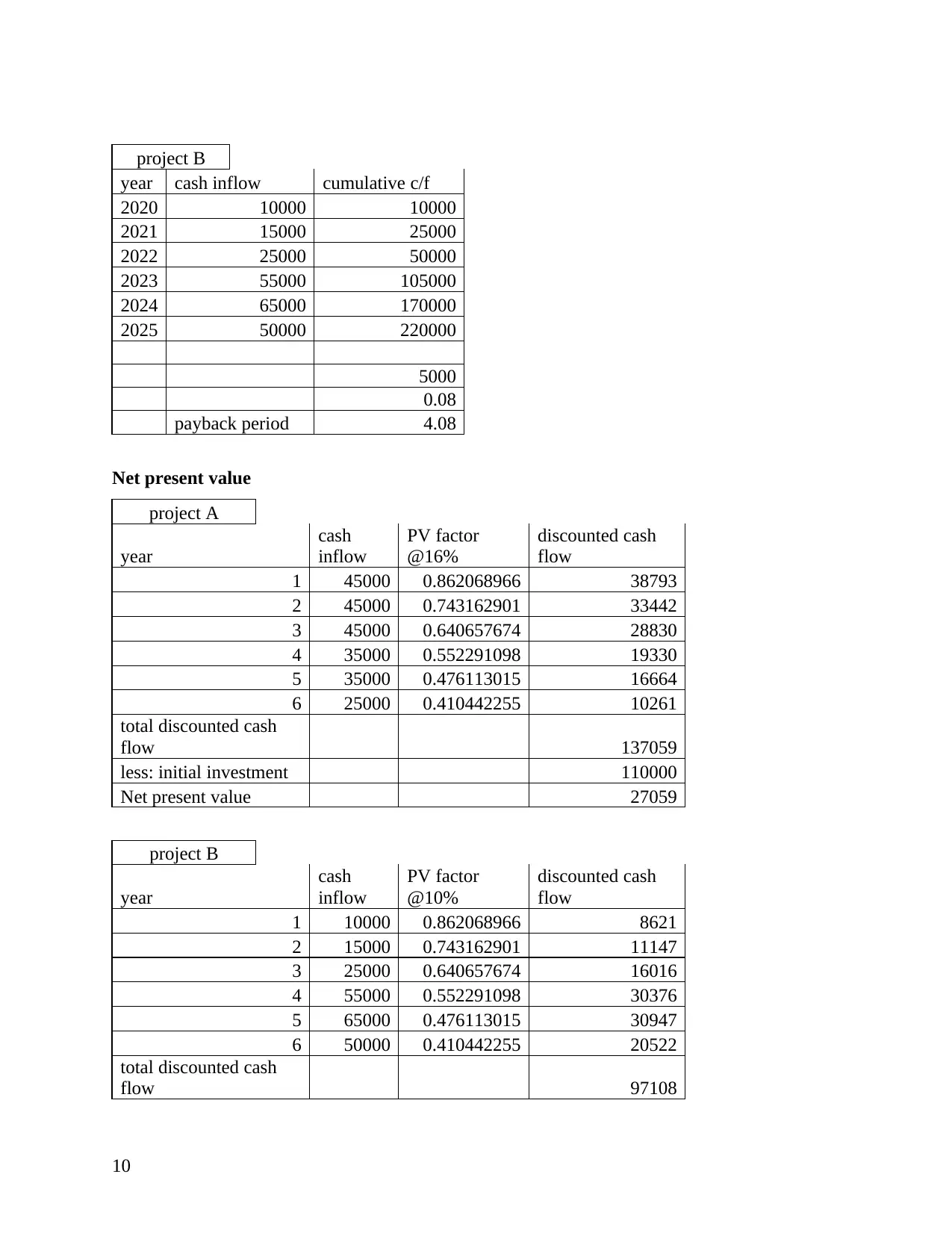

Payback period

project A

year cash inflow cumulative c/f

2020 45000 45000

2021 45000 90000

2022 45000 135000

2023 35000 170000

2024 35000 205000

2025 25000 230000

20000

0.44

payback period 2.44 years

9

Financial ratio analysis is most common technique used to interpret company's

performance (Michael and et.al., 2020). It helps the company to depicts the important financial

parameters, however being useful tool it has some limitation also.

a) Based on only Historical:

Financial ratios are based on historical information which is irrelevant because the technique

assumes that history repeat but it’s not accurate when business model and product line has

changed.

b) Does not considered the market condition:

Financial Ratios analysis does not corporate with changing market condition. Its Interpretation is

based on only previous data so its interpretation is neither accurate nor practical (Sriram, 2020).

c)Considered the position of Business on particular date:

Financial ratio analysis uses the company's balance sheet information to interpret the company's

position which not accurate as its figures are based on historical data.

d)Does not considered the impact of inflation:

Ratio analysis does not consider the price rise and uses only historical prices that tend to predict

historical position only which is biggest limitation of financial ratio analysis. Ratio analysis is

based on financial statements prepared by company so it only considered quantitative data and

not qualitative which is biggest limitation (Kadim, Sunardi and Husain, 2020).

PORTOFOLIO 2

a. Use of appropriate investment appraisal techniques for project A and project B

Payback period

project A

year cash inflow cumulative c/f

2020 45000 45000

2021 45000 90000

2022 45000 135000

2023 35000 170000

2024 35000 205000

2025 25000 230000

20000

0.44

payback period 2.44 years

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

project B

year cash inflow cumulative c/f

2020 10000 10000

2021 15000 25000

2022 25000 50000

2023 55000 105000

2024 65000 170000

2025 50000 220000

5000

0.08

payback period 4.08

Net present value

project A

year

cash

inflow

PV factor

@16%

discounted cash

flow

1 45000 0.862068966 38793

2 45000 0.743162901 33442

3 45000 0.640657674 28830

4 35000 0.552291098 19330

5 35000 0.476113015 16664

6 25000 0.410442255 10261

total discounted cash

flow 137059

less: initial investment 110000

Net present value 27059

project B

year

cash

inflow

PV factor

@10%

discounted cash

flow

1 10000 0.862068966 8621

2 15000 0.743162901 11147

3 25000 0.640657674 16016

4 55000 0.552291098 30376

5 65000 0.476113015 30947

6 50000 0.410442255 20522

total discounted cash

flow 97108

10

year cash inflow cumulative c/f

2020 10000 10000

2021 15000 25000

2022 25000 50000

2023 55000 105000

2024 65000 170000

2025 50000 220000

5000

0.08

payback period 4.08

Net present value

project A

year

cash

inflow

PV factor

@16%

discounted cash

flow

1 45000 0.862068966 38793

2 45000 0.743162901 33442

3 45000 0.640657674 28830

4 35000 0.552291098 19330

5 35000 0.476113015 16664

6 25000 0.410442255 10261

total discounted cash

flow 137059

less: initial investment 110000

Net present value 27059

project B

year

cash

inflow

PV factor

@10%

discounted cash

flow

1 10000 0.862068966 8621

2 15000 0.743162901 11147

3 25000 0.640657674 16016

4 55000 0.552291098 30376

5 65000 0.476113015 30947

6 50000 0.410442255 20522

total discounted cash

flow 97108

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

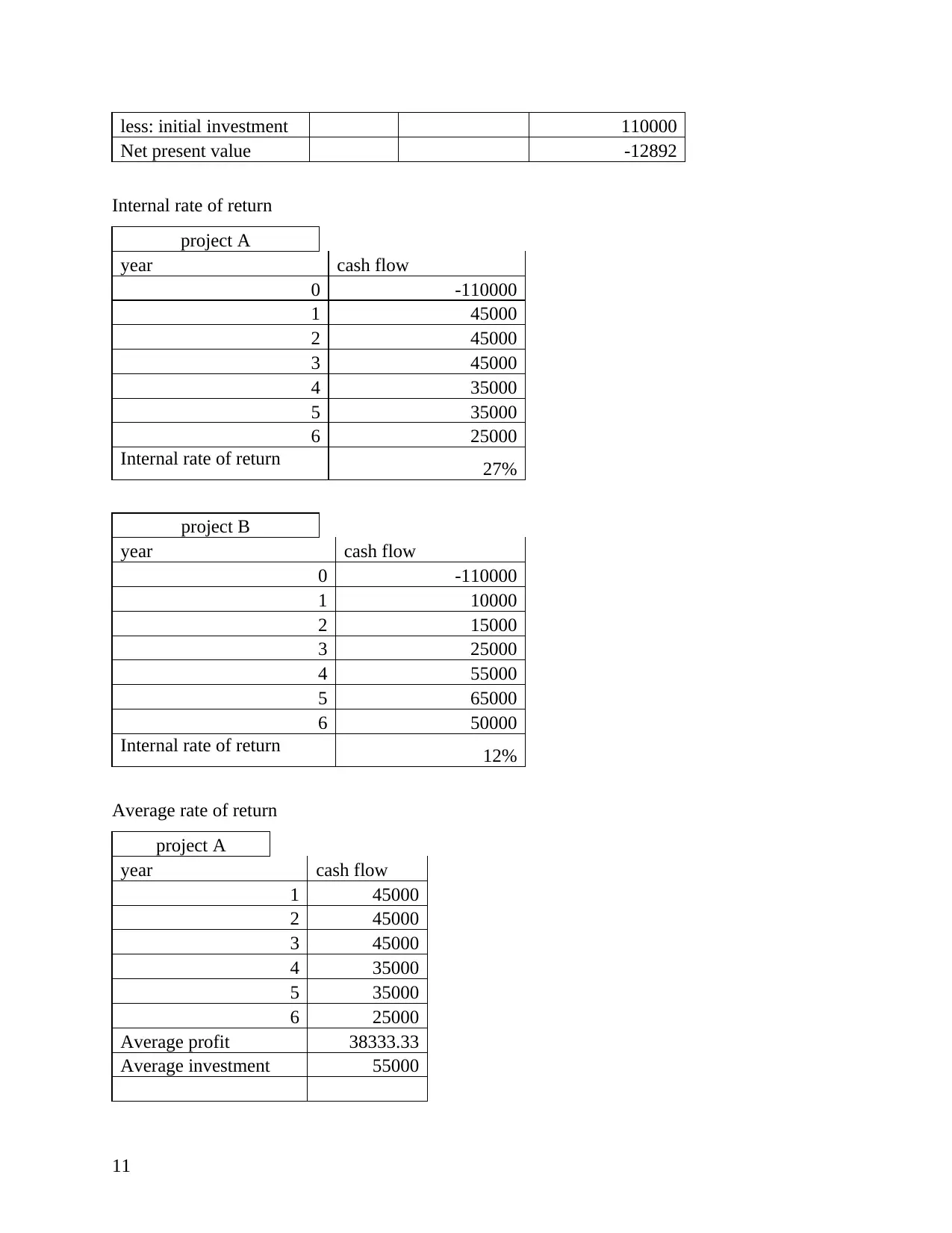

less: initial investment 110000

Net present value -12892

Internal rate of return

project A

year cash flow

0 -110000

1 45000

2 45000

3 45000

4 35000

5 35000

6 25000

Internal rate of return 27%

project B

year cash flow

0 -110000

1 10000

2 15000

3 25000

4 55000

5 65000

6 50000

Internal rate of return 12%

Average rate of return

project A

year cash flow

1 45000

2 45000

3 45000

4 35000

5 35000

6 25000

Average profit 38333.33

Average investment 55000

11

Net present value -12892

Internal rate of return

project A

year cash flow

0 -110000

1 45000

2 45000

3 45000

4 35000

5 35000

6 25000

Internal rate of return 27%

project B

year cash flow

0 -110000

1 10000

2 15000

3 25000

4 55000

5 65000

6 50000

Internal rate of return 12%

Average rate of return

project A

year cash flow

1 45000

2 45000

3 45000

4 35000

5 35000

6 25000

Average profit 38333.33

Average investment 55000

11

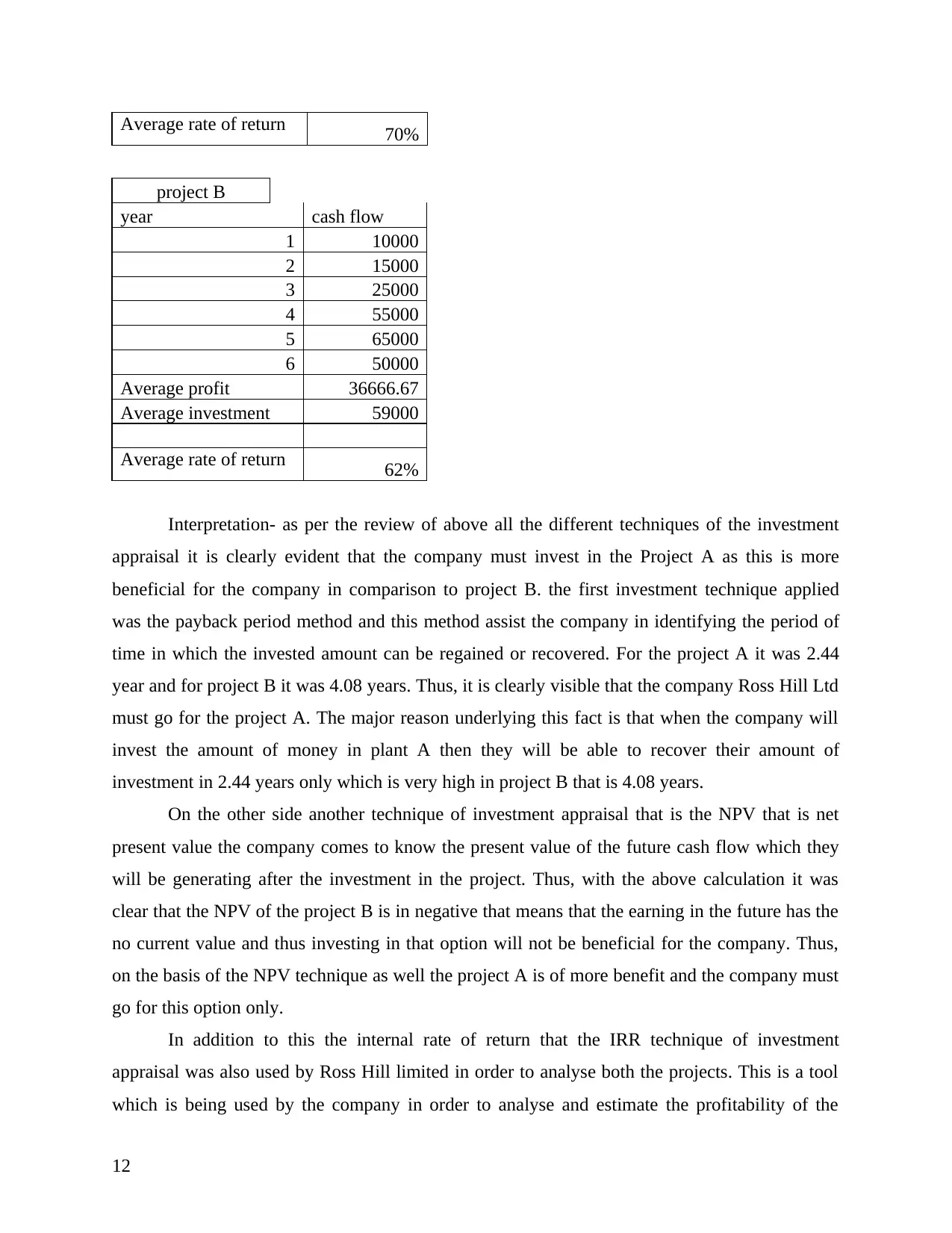

Average rate of return 70%

project B

year cash flow

1 10000

2 15000

3 25000

4 55000

5 65000

6 50000

Average profit 36666.67

Average investment 59000

Average rate of return 62%

Interpretation- as per the review of above all the different techniques of the investment

appraisal it is clearly evident that the company must invest in the Project A as this is more

beneficial for the company in comparison to project B. the first investment technique applied

was the payback period method and this method assist the company in identifying the period of

time in which the invested amount can be regained or recovered. For the project A it was 2.44

year and for project B it was 4.08 years. Thus, it is clearly visible that the company Ross Hill Ltd

must go for the project A. The major reason underlying this fact is that when the company will

invest the amount of money in plant A then they will be able to recover their amount of

investment in 2.44 years only which is very high in project B that is 4.08 years.

On the other side another technique of investment appraisal that is the NPV that is net

present value the company comes to know the present value of the future cash flow which they

will be generating after the investment in the project. Thus, with the above calculation it was

clear that the NPV of the project B is in negative that means that the earning in the future has the

no current value and thus investing in that option will not be beneficial for the company. Thus,

on the basis of the NPV technique as well the project A is of more benefit and the company must

go for this option only.

In addition to this the internal rate of return that the IRR technique of investment

appraisal was also used by Ross Hill limited in order to analyse both the projects. This is a tool

which is being used by the company in order to analyse and estimate the profitability of the

12

project B

year cash flow

1 10000

2 15000

3 25000

4 55000

5 65000

6 50000

Average profit 36666.67

Average investment 59000

Average rate of return 62%

Interpretation- as per the review of above all the different techniques of the investment

appraisal it is clearly evident that the company must invest in the Project A as this is more

beneficial for the company in comparison to project B. the first investment technique applied

was the payback period method and this method assist the company in identifying the period of

time in which the invested amount can be regained or recovered. For the project A it was 2.44

year and for project B it was 4.08 years. Thus, it is clearly visible that the company Ross Hill Ltd

must go for the project A. The major reason underlying this fact is that when the company will

invest the amount of money in plant A then they will be able to recover their amount of

investment in 2.44 years only which is very high in project B that is 4.08 years.

On the other side another technique of investment appraisal that is the NPV that is net

present value the company comes to know the present value of the future cash flow which they

will be generating after the investment in the project. Thus, with the above calculation it was

clear that the NPV of the project B is in negative that means that the earning in the future has the

no current value and thus investing in that option will not be beneficial for the company. Thus,

on the basis of the NPV technique as well the project A is of more benefit and the company must

go for this option only.

In addition to this the internal rate of return that the IRR technique of investment

appraisal was also used by Ross Hill limited in order to analyse both the projects. This is a tool

which is being used by the company in order to analyse and estimate the profitability of the

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.