ACFI1203: Financial Accounting Assignment - Sainsbury's Analysis

VerifiedAdded on 2022/09/11

|7

|982

|28

Homework Assignment

AI Summary

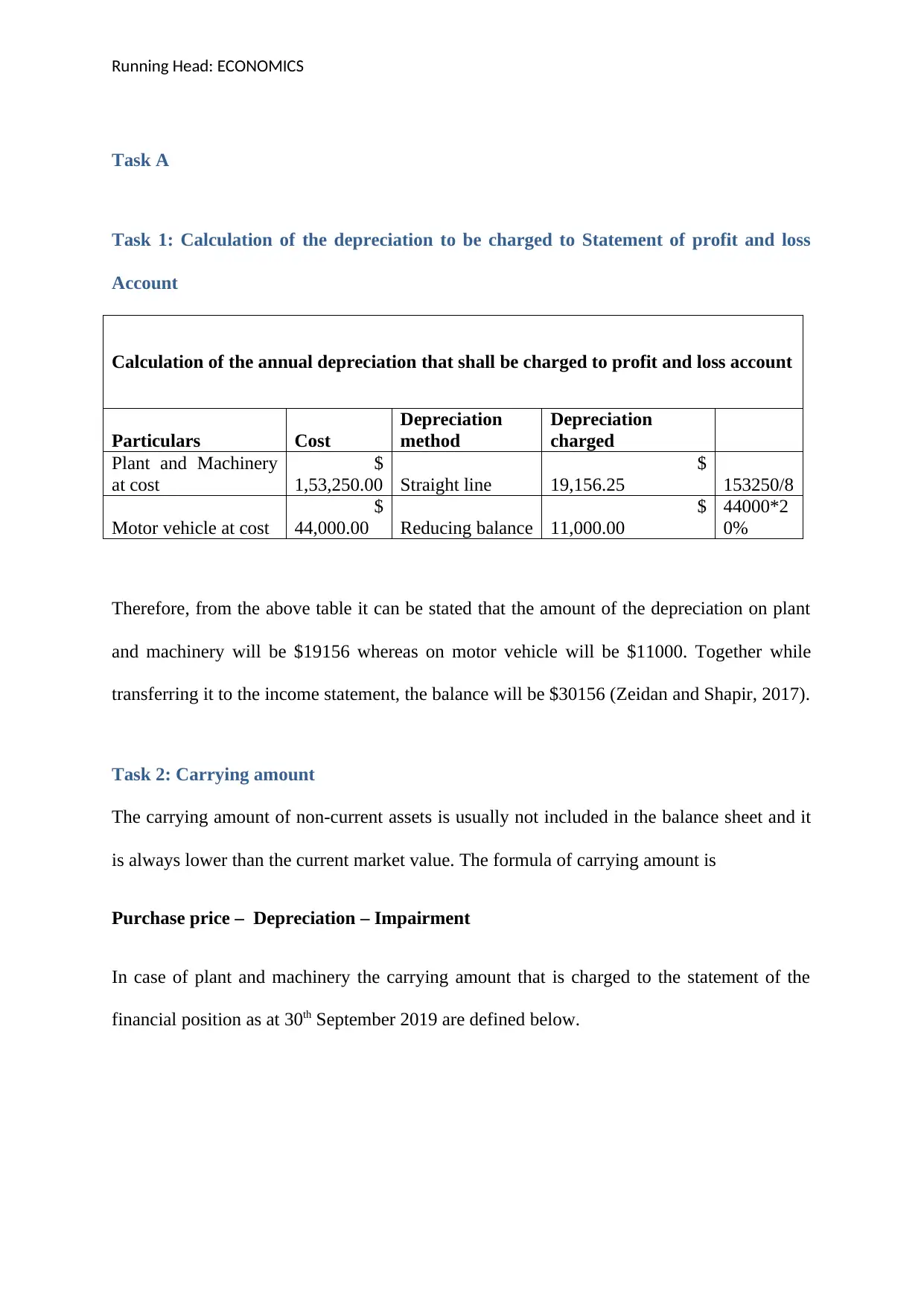

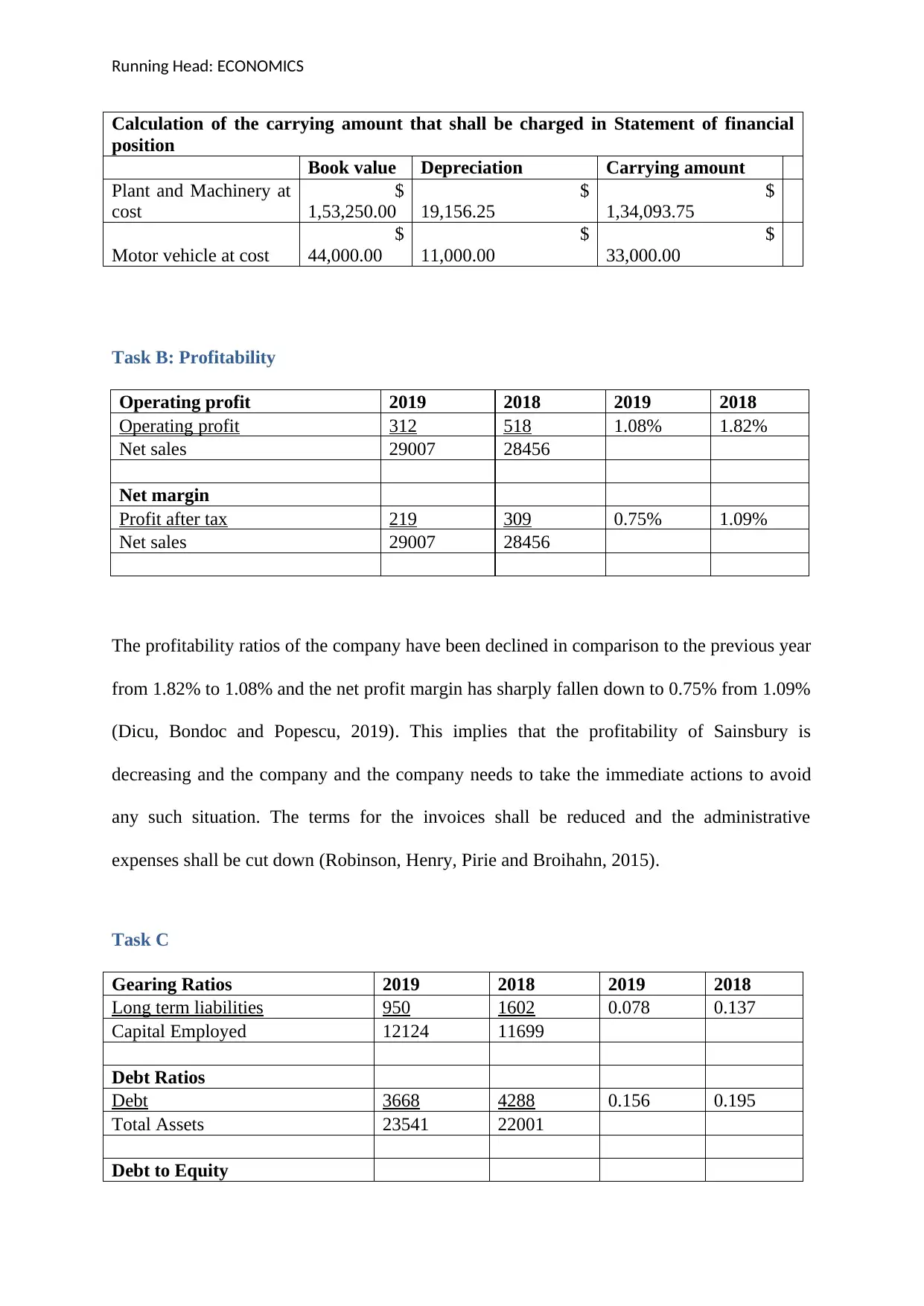

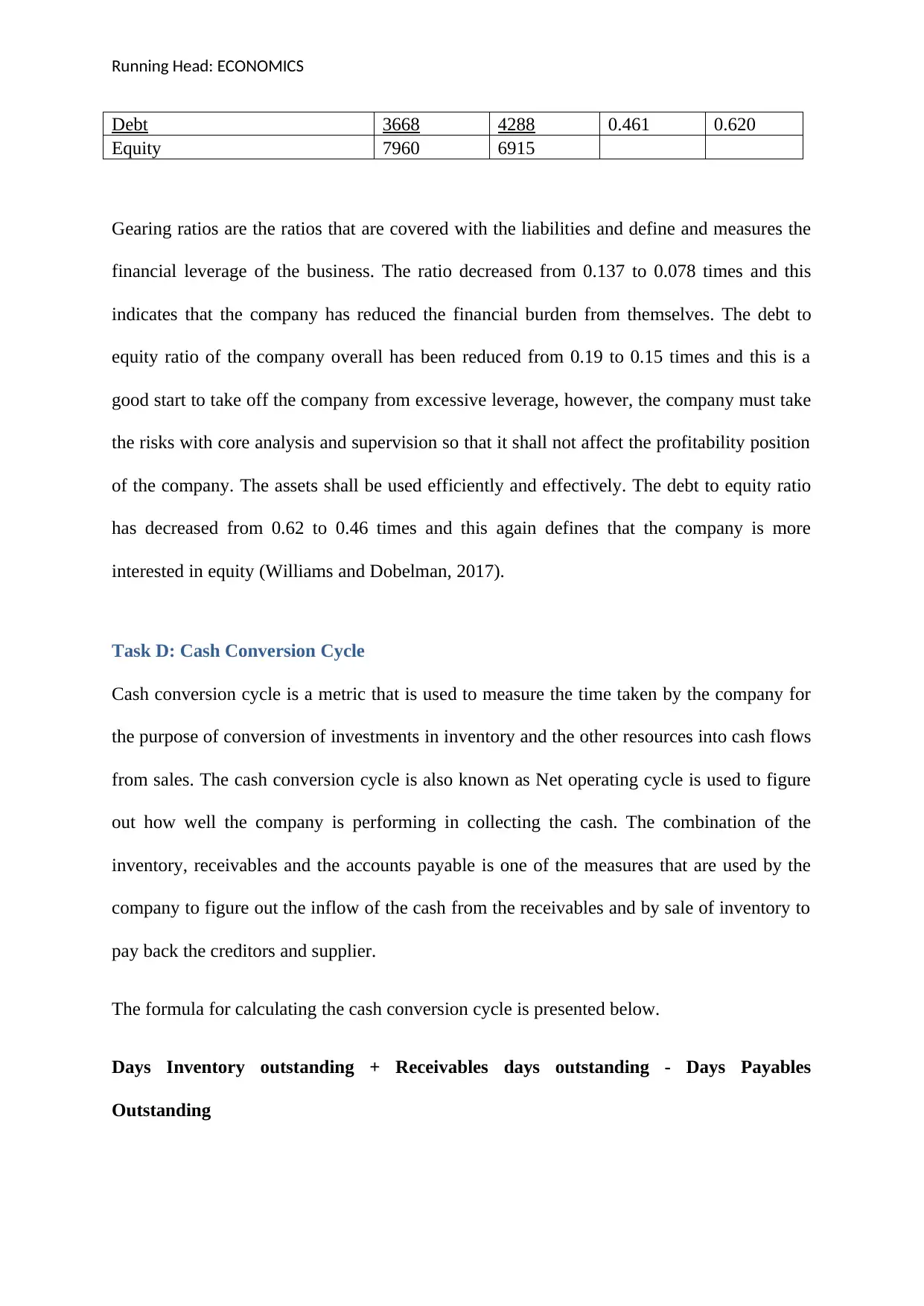

This assignment analyzes the financial performance of Sainsbury's Group Plc based on its 2019 financial statements, as part of the ACFI1203 course. It begins with the calculation of depreciation for plant and machinery and motor vehicles, determining carrying amounts. The assignment then examines Sainsbury's profitability, comparing operating profit and net profit margins for 2018 and 2019, revealing a decline in profitability ratios. Gearing ratios are then calculated and interpreted, assessing the company's financial leverage and debt-to-equity ratio, indicating a reduction in financial burden and increased equity. Finally, the cash conversion cycle is analyzed, revealing a negative cycle, indicating that the company is not efficiently managing its cash flows. The assignment provides a detailed analysis of the company's financial position, including key financial ratios and their implications.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.