Managerial Finance Report: Ratio Analysis and Investment Appraisal

VerifiedAdded on 2022/12/30

|18

|3910

|1

Report

AI Summary

This managerial finance report delves into the financial performance of Sainsbury's and Tesco, two major UK supermarket competitors. It begins with an introduction to managerial finance, emphasizing its role in evaluating company financial health and investment potential. The report is divided into two portfolios. Portfolio 1 conducts a detailed financial analysis using various ratios (current, quick, net profit margin, gross profit margin, gearing, P/E ratio, return on capital employed, inventory turnover, and dividend payout) for both companies across two years, followed by an interpretation of the ratios, recommendations for poorly performing businesses, and a discussion of the limitations of financial ratios. Portfolio 2 focuses on capital investment appraisal, applying techniques like Net Present Value (NPV) to determine the best investment project. The report provides detailed calculations and analysis to guide managerial decision-making, making it a comprehensive resource for understanding financial analysis and investment strategies.

MANAGERIAL FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Portfolio 1:.......................................................................................................................................1

a. Ratios of Sainsbury's and Tesco ..............................................................................................1

b. Interpretation of ratios of Sainsbury's and Tesco:...................................................................4

c. Recommendations to poorly performing business for improving performance and financial

position.........................................................................................................................................6

d. Limitations of financial ratios in determining company's performance..................................7

Portfolio 2: ......................................................................................................................................8

Capital Investment Appraisal.......................................................................................................8

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Books and Journals....................................................................................................................14

Online.........................................................................................................................................15

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Portfolio 1:.......................................................................................................................................1

a. Ratios of Sainsbury's and Tesco ..............................................................................................1

b. Interpretation of ratios of Sainsbury's and Tesco:...................................................................4

c. Recommendations to poorly performing business for improving performance and financial

position.........................................................................................................................................6

d. Limitations of financial ratios in determining company's performance..................................7

Portfolio 2: ......................................................................................................................................8

Capital Investment Appraisal.......................................................................................................8

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Books and Journals....................................................................................................................14

Online.........................................................................................................................................15

INTRODUCTION

Managerial finance is the most important subject of finance which include various financial

functions performed by the management of the company in carrying out their financial manager's

role. Finance is considered to be the blood of every and the decision regarding the same require a

high level of managerial expertise (De Souza and Lunkes, 20160. The present report includes

various financial techniques of usually incorporated in the course of evaluating financial position

and performance of the companies. The first portfolio of this report is all about financial analysis

by the potential investors in order to analyse performance, financial position and investment

potentiality of Tesco and Sainsbury's with the help of various financial ratios. Both the

companies are competitors of each other in the UK' supermarket industry. The second part is all

about investment in capital assets which require clear suggestions and recommendations to

managers and for this they resort to some investment appraisal techniques. These techniques

provide them with clear guidance about various available alternatives in terms of their future

profitability.

MAIN BODY

Portfolio 1:

a. Ratios of Sainsbury's and Tesco

Current Ratio

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Current assets 7857 7581 13600 12570

Current liability 10320 11417 19233 20680

Current ratio Current

asset/current

liability

0.76 0.66 0.7 0.6

Quick Ratio

Particulars Formula Sainsbury's Tesco

1

Managerial finance is the most important subject of finance which include various financial

functions performed by the management of the company in carrying out their financial manager's

role. Finance is considered to be the blood of every and the decision regarding the same require a

high level of managerial expertise (De Souza and Lunkes, 20160. The present report includes

various financial techniques of usually incorporated in the course of evaluating financial position

and performance of the companies. The first portfolio of this report is all about financial analysis

by the potential investors in order to analyse performance, financial position and investment

potentiality of Tesco and Sainsbury's with the help of various financial ratios. Both the

companies are competitors of each other in the UK' supermarket industry. The second part is all

about investment in capital assets which require clear suggestions and recommendations to

managers and for this they resort to some investment appraisal techniques. These techniques

provide them with clear guidance about various available alternatives in terms of their future

profitability.

MAIN BODY

Portfolio 1:

a. Ratios of Sainsbury's and Tesco

Current Ratio

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Current assets 7857 7581 13600 12570

Current liability 10320 11417 19233 20680

Current ratio Current

asset/current

liability

0.76 0.66 0.7 0.6

Quick Ratio

Particulars Formula Sainsbury's Tesco

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018 2019 2018 2019

Quick Assets 5303 4991 9832 9313

Current liability 10320 11417 19233 20680

Quick Ratio Quick

assets/current

liability

0.51 0.43 0.51 0.4

Net Profit margin

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Net profit 309 219 1210 1320

sales 28456 29007 57493 63911

Net Profit

margin

Net

profit/sales*100

1.08 0.75 2.1 2.06

Gross profit margin

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Gross profit 1882 2007 3352 4144

Revenue 28456 29007 57493 63911

Gross profit

margin

Gross

profit/Revenue

*100

6.61 6.91 5.83 6.48

2

Quick Assets 5303 4991 9832 9313

Current liability 10320 11417 19233 20680

Quick Ratio Quick

assets/current

liability

0.51 0.43 0.51 0.4

Net Profit margin

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Net profit 309 219 1210 1320

sales 28456 29007 57493 63911

Net Profit

margin

Net

profit/sales*100

1.08 0.75 2.1 2.06

Gross profit margin

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Gross profit 1882 2007 3352 4144

Revenue 28456 29007 57493 63911

Gross profit

margin

Gross

profit/Revenue

*100

6.61 6.91 5.83 6.48

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

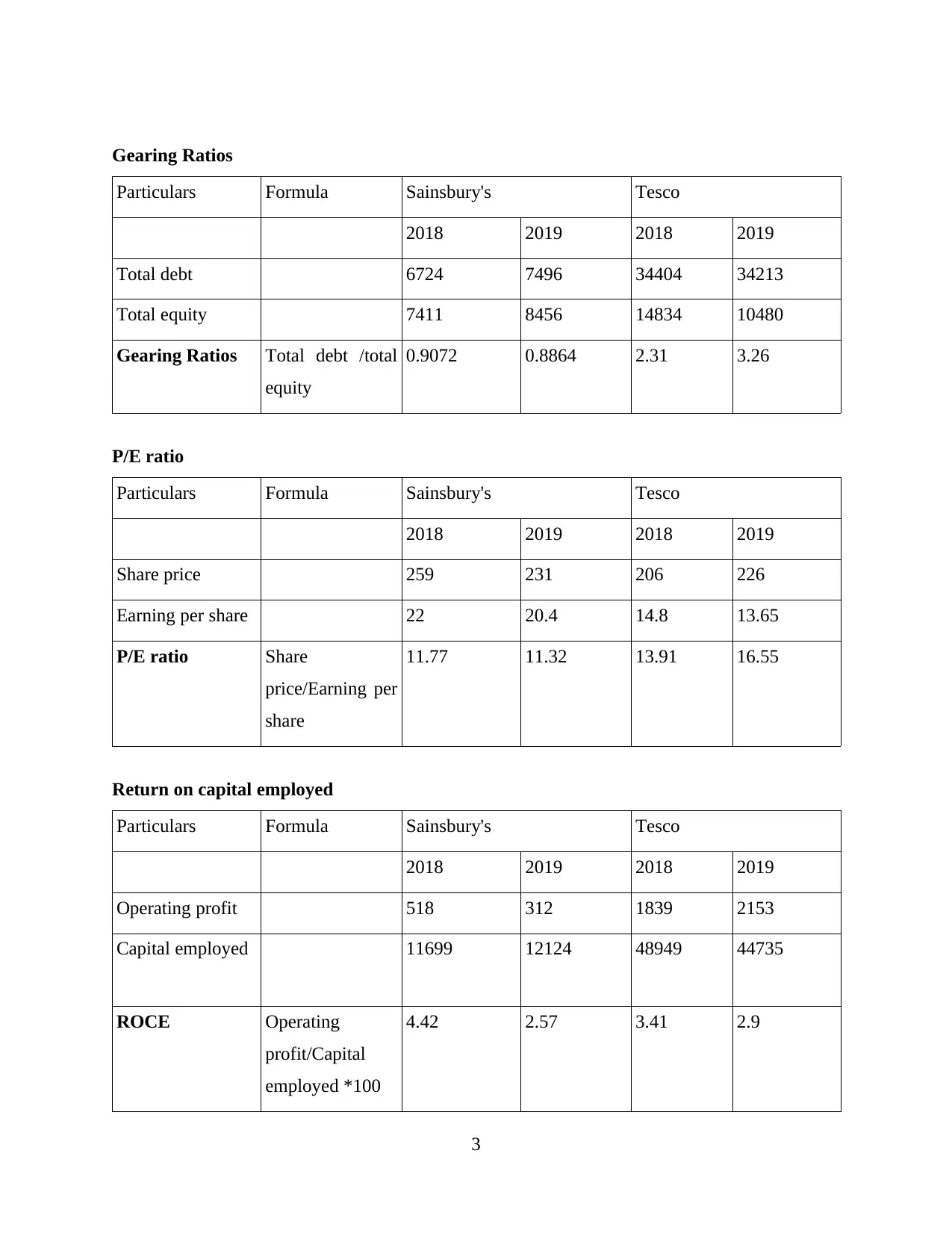

Gearing Ratios

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Total debt 6724 7496 34404 34213

Total equity 7411 8456 14834 10480

Gearing Ratios Total debt /total

equity

0.9072 0.8864 2.31 3.26

P/E ratio

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Share price 259 231 206 226

Earning per share 22 20.4 14.8 13.65

P/E ratio Share

price/Earning per

share

11.77 11.32 13.91 16.55

Return on capital employed

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Operating profit 518 312 1839 2153

Capital employed 11699 12124 48949 44735

ROCE Operating

profit/Capital

employed *100

4.42 2.57 3.41 2.9

3

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Total debt 6724 7496 34404 34213

Total equity 7411 8456 14834 10480

Gearing Ratios Total debt /total

equity

0.9072 0.8864 2.31 3.26

P/E ratio

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Share price 259 231 206 226

Earning per share 22 20.4 14.8 13.65

P/E ratio Share

price/Earning per

share

11.77 11.32 13.91 16.55

Return on capital employed

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Operating profit 518 312 1839 2153

Capital employed 11699 12124 48949 44735

ROCE Operating

profit/Capital

employed *100

4.42 2.57 3.41 2.9

3

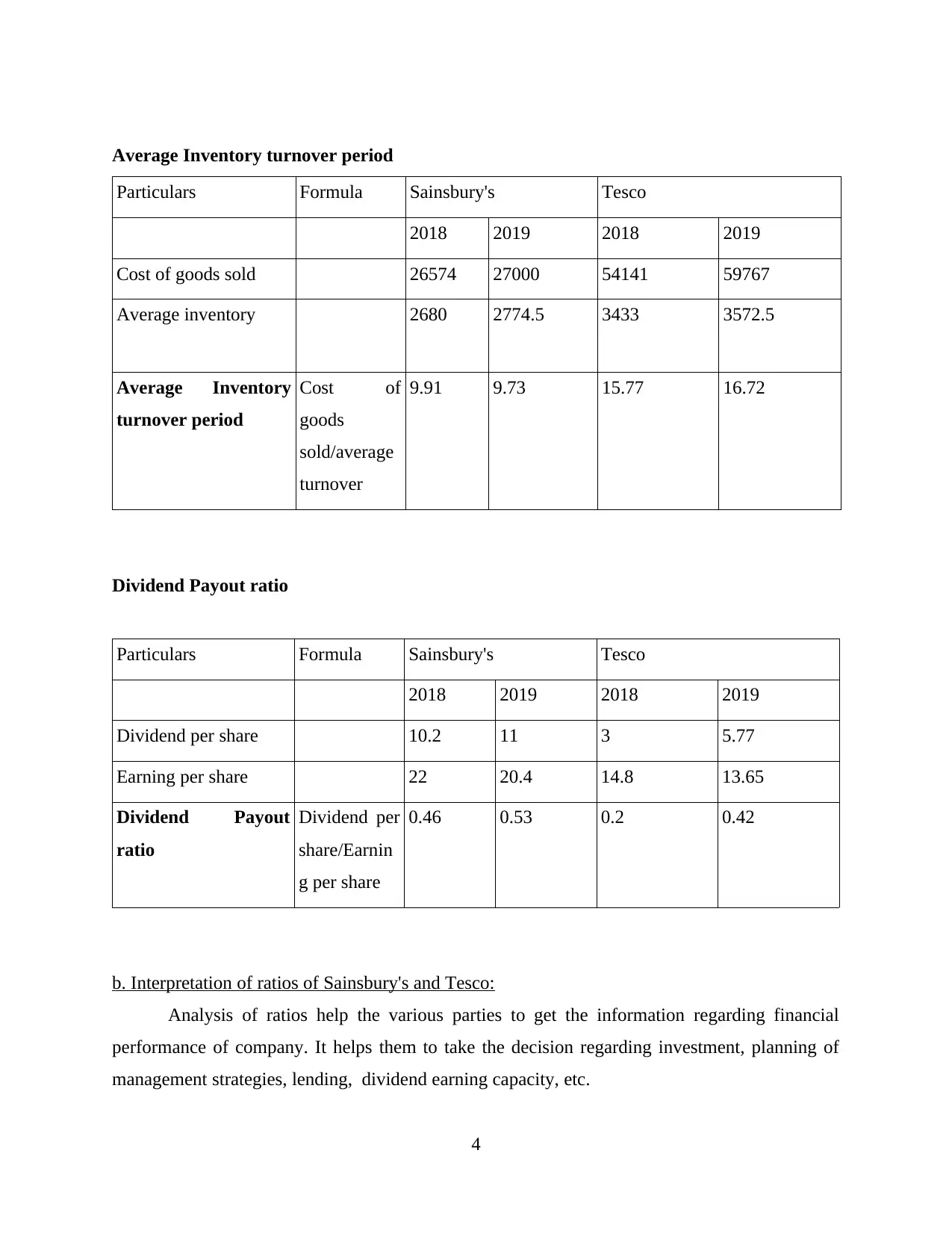

Average Inventory turnover period

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Cost of goods sold 26574 27000 54141 59767

Average inventory 2680 2774.5 3433 3572.5

Average Inventory

turnover period

Cost of

goods

sold/average

turnover

9.91 9.73 15.77 16.72

Dividend Payout ratio

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Dividend per share 10.2 11 3 5.77

Earning per share 22 20.4 14.8 13.65

Dividend Payout

ratio

Dividend per

share/Earnin

g per share

0.46 0.53 0.2 0.42

b. Interpretation of ratios of Sainsbury's and Tesco:

Analysis of ratios help the various parties to get the information regarding financial

performance of company. It helps them to take the decision regarding investment, planning of

management strategies, lending, dividend earning capacity, etc.

4

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Cost of goods sold 26574 27000 54141 59767

Average inventory 2680 2774.5 3433 3572.5

Average Inventory

turnover period

Cost of

goods

sold/average

turnover

9.91 9.73 15.77 16.72

Dividend Payout ratio

Particulars Formula Sainsbury's Tesco

2018 2019 2018 2019

Dividend per share 10.2 11 3 5.77

Earning per share 22 20.4 14.8 13.65

Dividend Payout

ratio

Dividend per

share/Earnin

g per share

0.46 0.53 0.2 0.42

b. Interpretation of ratios of Sainsbury's and Tesco:

Analysis of ratios help the various parties to get the information regarding financial

performance of company. It helps them to take the decision regarding investment, planning of

management strategies, lending, dividend earning capacity, etc.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

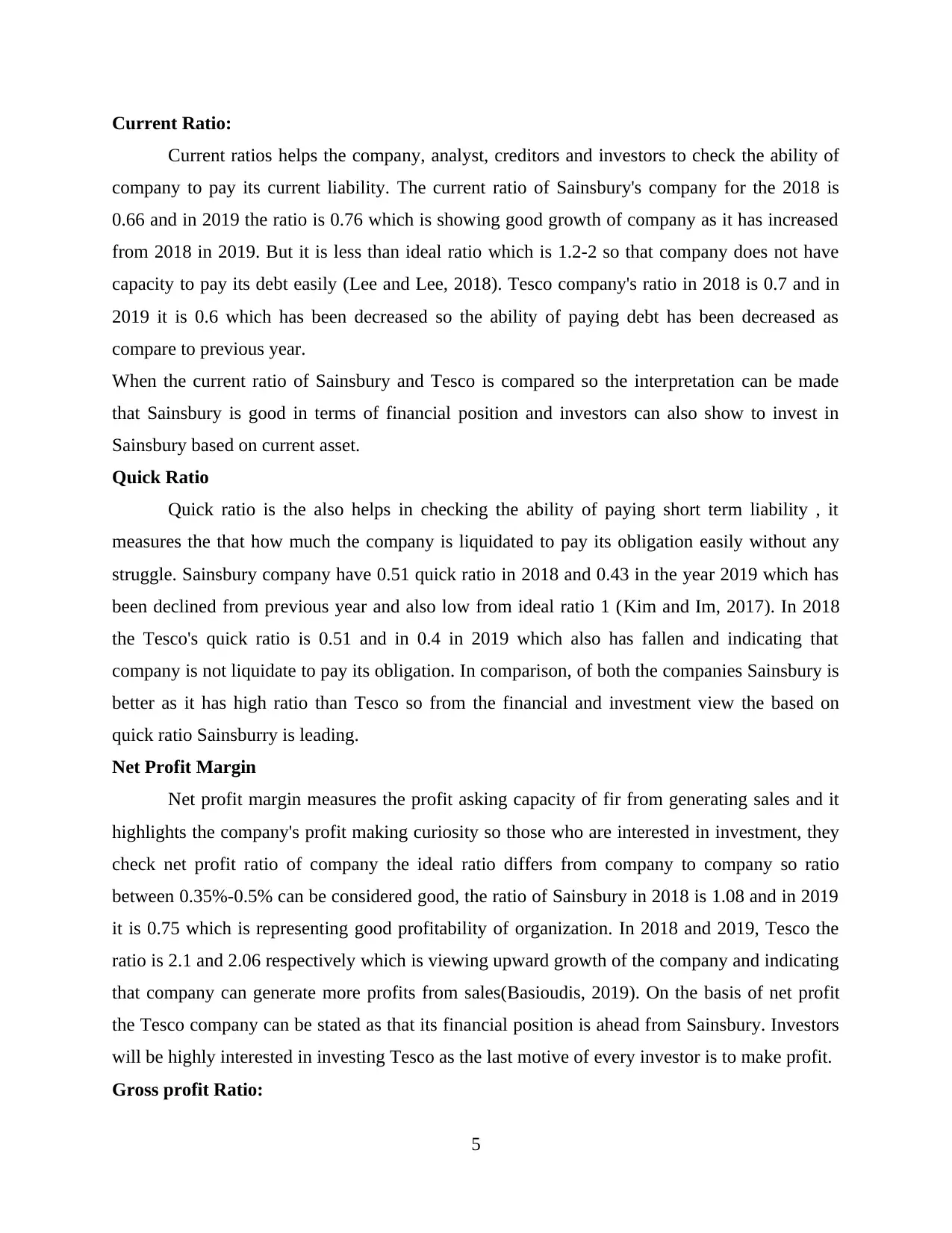

Current Ratio:

Current ratios helps the company, analyst, creditors and investors to check the ability of

company to pay its current liability. The current ratio of Sainsbury's company for the 2018 is

0.66 and in 2019 the ratio is 0.76 which is showing good growth of company as it has increased

from 2018 in 2019. But it is less than ideal ratio which is 1.2-2 so that company does not have

capacity to pay its debt easily (Lee and Lee, 2018). Tesco company's ratio in 2018 is 0.7 and in

2019 it is 0.6 which has been decreased so the ability of paying debt has been decreased as

compare to previous year.

When the current ratio of Sainsbury and Tesco is compared so the interpretation can be made

that Sainsbury is good in terms of financial position and investors can also show to invest in

Sainsbury based on current asset.

Quick Ratio

Quick ratio is the also helps in checking the ability of paying short term liability , it

measures the that how much the company is liquidated to pay its obligation easily without any

struggle. Sainsbury company have 0.51 quick ratio in 2018 and 0.43 in the year 2019 which has

been declined from previous year and also low from ideal ratio 1 (Kim and Im, 2017). In 2018

the Tesco's quick ratio is 0.51 and in 0.4 in 2019 which also has fallen and indicating that

company is not liquidate to pay its obligation. In comparison, of both the companies Sainsbury is

better as it has high ratio than Tesco so from the financial and investment view the based on

quick ratio Sainsburry is leading.

Net Profit Margin

Net profit margin measures the profit asking capacity of fir from generating sales and it

highlights the company's profit making curiosity so those who are interested in investment, they

check net profit ratio of company the ideal ratio differs from company to company so ratio

between 0.35%-0.5% can be considered good, the ratio of Sainsbury in 2018 is 1.08 and in 2019

it is 0.75 which is representing good profitability of organization. In 2018 and 2019, Tesco the

ratio is 2.1 and 2.06 respectively which is viewing upward growth of the company and indicating

that company can generate more profits from sales(Basioudis, 2019). On the basis of net profit

the Tesco company can be stated as that its financial position is ahead from Sainsbury. Investors

will be highly interested in investing Tesco as the last motive of every investor is to make profit.

Gross profit Ratio:

5

Current ratios helps the company, analyst, creditors and investors to check the ability of

company to pay its current liability. The current ratio of Sainsbury's company for the 2018 is

0.66 and in 2019 the ratio is 0.76 which is showing good growth of company as it has increased

from 2018 in 2019. But it is less than ideal ratio which is 1.2-2 so that company does not have

capacity to pay its debt easily (Lee and Lee, 2018). Tesco company's ratio in 2018 is 0.7 and in

2019 it is 0.6 which has been decreased so the ability of paying debt has been decreased as

compare to previous year.

When the current ratio of Sainsbury and Tesco is compared so the interpretation can be made

that Sainsbury is good in terms of financial position and investors can also show to invest in

Sainsbury based on current asset.

Quick Ratio

Quick ratio is the also helps in checking the ability of paying short term liability , it

measures the that how much the company is liquidated to pay its obligation easily without any

struggle. Sainsbury company have 0.51 quick ratio in 2018 and 0.43 in the year 2019 which has

been declined from previous year and also low from ideal ratio 1 (Kim and Im, 2017). In 2018

the Tesco's quick ratio is 0.51 and in 0.4 in 2019 which also has fallen and indicating that

company is not liquidate to pay its obligation. In comparison, of both the companies Sainsbury is

better as it has high ratio than Tesco so from the financial and investment view the based on

quick ratio Sainsburry is leading.

Net Profit Margin

Net profit margin measures the profit asking capacity of fir from generating sales and it

highlights the company's profit making curiosity so those who are interested in investment, they

check net profit ratio of company the ideal ratio differs from company to company so ratio

between 0.35%-0.5% can be considered good, the ratio of Sainsbury in 2018 is 1.08 and in 2019

it is 0.75 which is representing good profitability of organization. In 2018 and 2019, Tesco the

ratio is 2.1 and 2.06 respectively which is viewing upward growth of the company and indicating

that company can generate more profits from sales(Basioudis, 2019). On the basis of net profit

the Tesco company can be stated as that its financial position is ahead from Sainsbury. Investors

will be highly interested in investing Tesco as the last motive of every investor is to make profit.

Gross profit Ratio:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

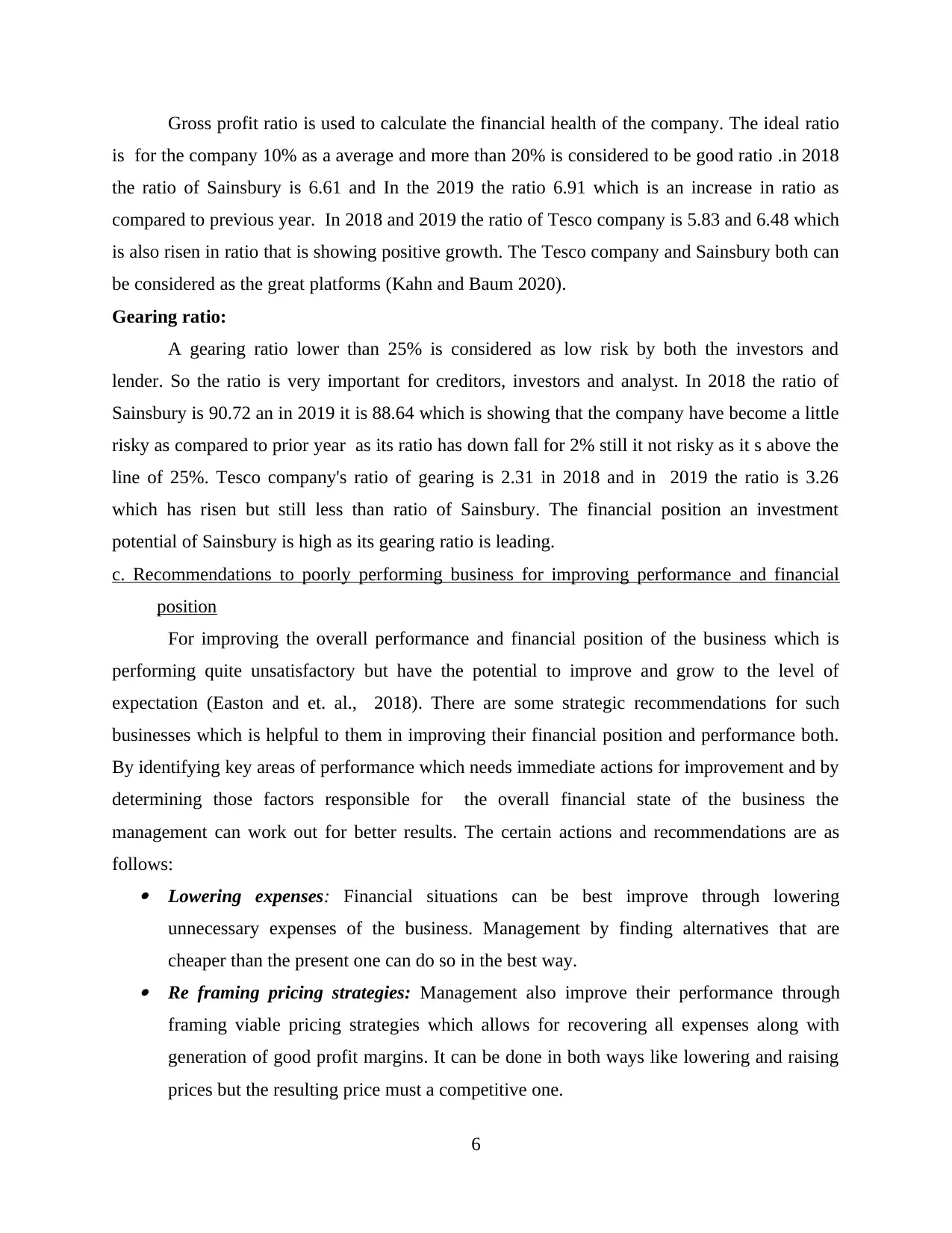

Gross profit ratio is used to calculate the financial health of the company. The ideal ratio

is for the company 10% as a average and more than 20% is considered to be good ratio .in 2018

the ratio of Sainsbury is 6.61 and In the 2019 the ratio 6.91 which is an increase in ratio as

compared to previous year. In 2018 and 2019 the ratio of Tesco company is 5.83 and 6.48 which

is also risen in ratio that is showing positive growth. The Tesco company and Sainsbury both can

be considered as the great platforms (Kahn and Baum 2020).

Gearing ratio:

A gearing ratio lower than 25% is considered as low risk by both the investors and

lender. So the ratio is very important for creditors, investors and analyst. In 2018 the ratio of

Sainsbury is 90.72 an in 2019 it is 88.64 which is showing that the company have become a little

risky as compared to prior year as its ratio has down fall for 2% still it not risky as it s above the

line of 25%. Tesco company's ratio of gearing is 2.31 in 2018 and in 2019 the ratio is 3.26

which has risen but still less than ratio of Sainsbury. The financial position an investment

potential of Sainsbury is high as its gearing ratio is leading.

c. Recommendations to poorly performing business for improving performance and financial

position

For improving the overall performance and financial position of the business which is

performing quite unsatisfactory but have the potential to improve and grow to the level of

expectation (Easton and et. al., 2018). There are some strategic recommendations for such

businesses which is helpful to them in improving their financial position and performance both.

By identifying key areas of performance which needs immediate actions for improvement and by

determining those factors responsible for the overall financial state of the business the

management can work out for better results. The certain actions and recommendations are as

follows: Lowering expenses: Financial situations can be best improve through lowering

unnecessary expenses of the business. Management by finding alternatives that are

cheaper than the present one can do so in the best way. Re framing pricing strategies: Management also improve their performance through

framing viable pricing strategies which allows for recovering all expenses along with

generation of good profit margins. It can be done in both ways like lowering and raising

prices but the resulting price must a competitive one.

6

is for the company 10% as a average and more than 20% is considered to be good ratio .in 2018

the ratio of Sainsbury is 6.61 and In the 2019 the ratio 6.91 which is an increase in ratio as

compared to previous year. In 2018 and 2019 the ratio of Tesco company is 5.83 and 6.48 which

is also risen in ratio that is showing positive growth. The Tesco company and Sainsbury both can

be considered as the great platforms (Kahn and Baum 2020).

Gearing ratio:

A gearing ratio lower than 25% is considered as low risk by both the investors and

lender. So the ratio is very important for creditors, investors and analyst. In 2018 the ratio of

Sainsbury is 90.72 an in 2019 it is 88.64 which is showing that the company have become a little

risky as compared to prior year as its ratio has down fall for 2% still it not risky as it s above the

line of 25%. Tesco company's ratio of gearing is 2.31 in 2018 and in 2019 the ratio is 3.26

which has risen but still less than ratio of Sainsbury. The financial position an investment

potential of Sainsbury is high as its gearing ratio is leading.

c. Recommendations to poorly performing business for improving performance and financial

position

For improving the overall performance and financial position of the business which is

performing quite unsatisfactory but have the potential to improve and grow to the level of

expectation (Easton and et. al., 2018). There are some strategic recommendations for such

businesses which is helpful to them in improving their financial position and performance both.

By identifying key areas of performance which needs immediate actions for improvement and by

determining those factors responsible for the overall financial state of the business the

management can work out for better results. The certain actions and recommendations are as

follows: Lowering expenses: Financial situations can be best improve through lowering

unnecessary expenses of the business. Management by finding alternatives that are

cheaper than the present one can do so in the best way. Re framing pricing strategies: Management also improve their performance through

framing viable pricing strategies which allows for recovering all expenses along with

generation of good profit margins. It can be done in both ways like lowering and raising

prices but the resulting price must a competitive one.

6

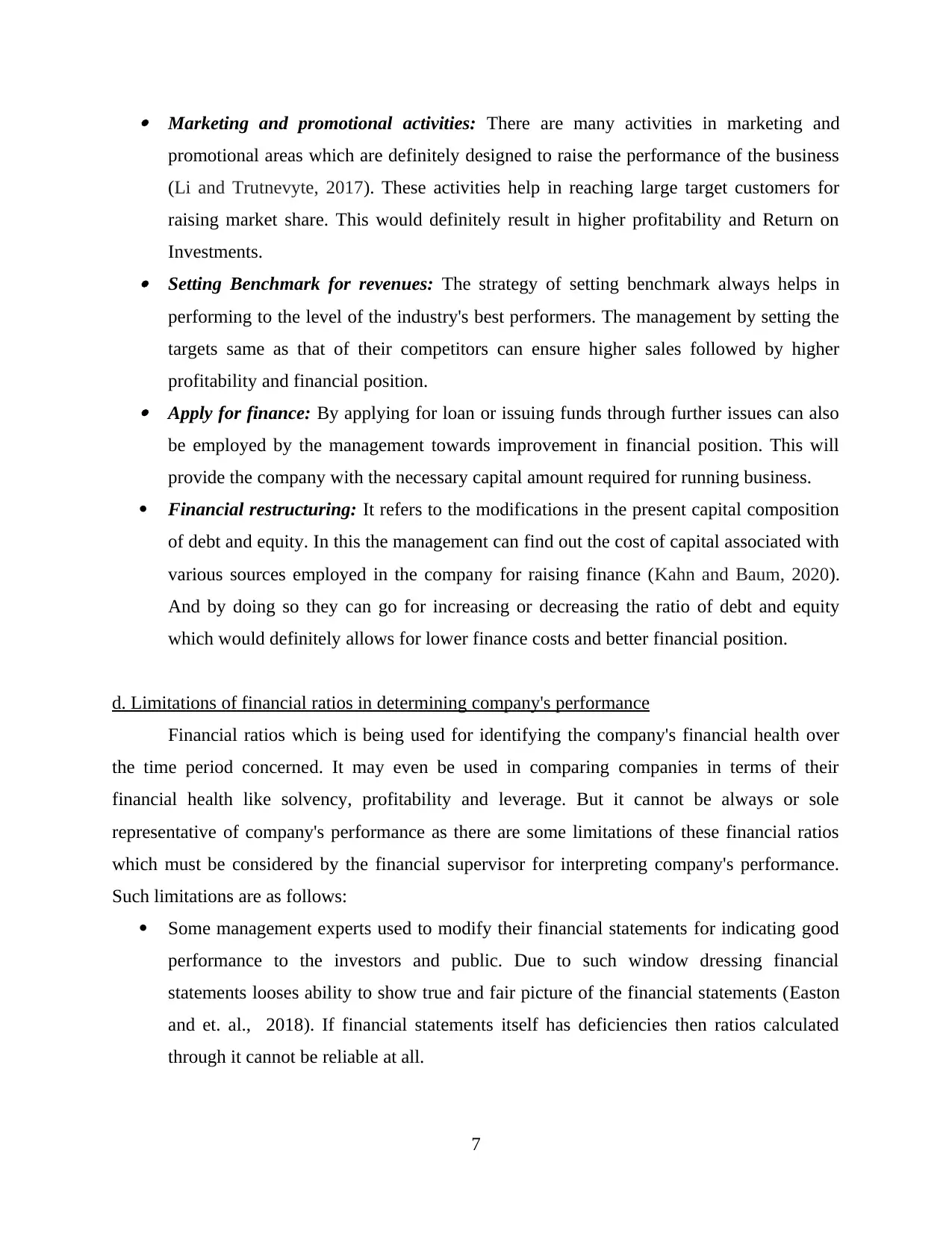

Marketing and promotional activities: There are many activities in marketing and

promotional areas which are definitely designed to raise the performance of the business

(Li and Trutnevyte, 2017). These activities help in reaching large target customers for

raising market share. This would definitely result in higher profitability and Return on

Investments. Setting Benchmark for revenues: The strategy of setting benchmark always helps in

performing to the level of the industry's best performers. The management by setting the

targets same as that of their competitors can ensure higher sales followed by higher

profitability and financial position. Apply for finance: By applying for loan or issuing funds through further issues can also

be employed by the management towards improvement in financial position. This will

provide the company with the necessary capital amount required for running business.

Financial restructuring: It refers to the modifications in the present capital composition

of debt and equity. In this the management can find out the cost of capital associated with

various sources employed in the company for raising finance (Kahn and Baum, 2020).

And by doing so they can go for increasing or decreasing the ratio of debt and equity

which would definitely allows for lower finance costs and better financial position.

d. Limitations of financial ratios in determining company's performance

Financial ratios which is being used for identifying the company's financial health over

the time period concerned. It may even be used in comparing companies in terms of their

financial health like solvency, profitability and leverage. But it cannot be always or sole

representative of company's performance as there are some limitations of these financial ratios

which must be considered by the financial supervisor for interpreting company's performance.

Such limitations are as follows:

Some management experts used to modify their financial statements for indicating good

performance to the investors and public. Due to such window dressing financial

statements looses ability to show true and fair picture of the financial statements (Easton

and et. al., 2018). If financial statements itself has deficiencies then ratios calculated

through it cannot be reliable at all.

7

promotional areas which are definitely designed to raise the performance of the business

(Li and Trutnevyte, 2017). These activities help in reaching large target customers for

raising market share. This would definitely result in higher profitability and Return on

Investments. Setting Benchmark for revenues: The strategy of setting benchmark always helps in

performing to the level of the industry's best performers. The management by setting the

targets same as that of their competitors can ensure higher sales followed by higher

profitability and financial position. Apply for finance: By applying for loan or issuing funds through further issues can also

be employed by the management towards improvement in financial position. This will

provide the company with the necessary capital amount required for running business.

Financial restructuring: It refers to the modifications in the present capital composition

of debt and equity. In this the management can find out the cost of capital associated with

various sources employed in the company for raising finance (Kahn and Baum, 2020).

And by doing so they can go for increasing or decreasing the ratio of debt and equity

which would definitely allows for lower finance costs and better financial position.

d. Limitations of financial ratios in determining company's performance

Financial ratios which is being used for identifying the company's financial health over

the time period concerned. It may even be used in comparing companies in terms of their

financial health like solvency, profitability and leverage. But it cannot be always or sole

representative of company's performance as there are some limitations of these financial ratios

which must be considered by the financial supervisor for interpreting company's performance.

Such limitations are as follows:

Some management experts used to modify their financial statements for indicating good

performance to the investors and public. Due to such window dressing financial

statements looses ability to show true and fair picture of the financial statements (Easton

and et. al., 2018). If financial statements itself has deficiencies then ratios calculated

through it cannot be reliable at all.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inflationary factors are usually ignored by the financial statements as they are prepared

on the basis of his historical costs then same the would be carried over on ratios too

(Myšková and Hájek, 2017). Such historical costing doesn't reflect present financial

situation.

The financial ratios is concerned about quantitative aspect only and doesn't take into

consideration non monetary aspects like quality, expertise and experience of management

of the company, their employee's talent, market share and market image.

Sometimes it happens where the company changes their accounting policies. This change

in policies of accounting may result in unmatch between financial results of two

accounting years or two companies with different accounting policies (Abor, 2017). And

if the ratios are calculated on the basis of such differential financial statements then the

ratios so calculated looses its capability to be compared.

Portfolio 2:

Capital Investment Appraisal

a) Various capital investment appraisal techniques have been applied to the data of Rose Hill

Limited. With the help of these techniques it can ascertain which plant should be purchased

among the two mutually exclusive projects. The decision shall be made in respect of the project

that is generating higher returns in its useful life (Abor, 2017).

Net Present Value

Computation of NPV (Plant 1)

Year Cash inflows PV factor @ 16%

Discounted

cash inflows

1 45000 0.862

38793.103448

2759

2 45000 0.743

33442.330558

8585

3 45000 0.641 28829.595309

8

on the basis of his historical costs then same the would be carried over on ratios too

(Myšková and Hájek, 2017). Such historical costing doesn't reflect present financial

situation.

The financial ratios is concerned about quantitative aspect only and doesn't take into

consideration non monetary aspects like quality, expertise and experience of management

of the company, their employee's talent, market share and market image.

Sometimes it happens where the company changes their accounting policies. This change

in policies of accounting may result in unmatch between financial results of two

accounting years or two companies with different accounting policies (Abor, 2017). And

if the ratios are calculated on the basis of such differential financial statements then the

ratios so calculated looses its capability to be compared.

Portfolio 2:

Capital Investment Appraisal

a) Various capital investment appraisal techniques have been applied to the data of Rose Hill

Limited. With the help of these techniques it can ascertain which plant should be purchased

among the two mutually exclusive projects. The decision shall be made in respect of the project

that is generating higher returns in its useful life (Abor, 2017).

Net Present Value

Computation of NPV (Plant 1)

Year Cash inflows PV factor @ 16%

Discounted

cash inflows

1 45000 0.862

38793.103448

2759

2 45000 0.743

33442.330558

8585

3 45000 0.641 28829.595309

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

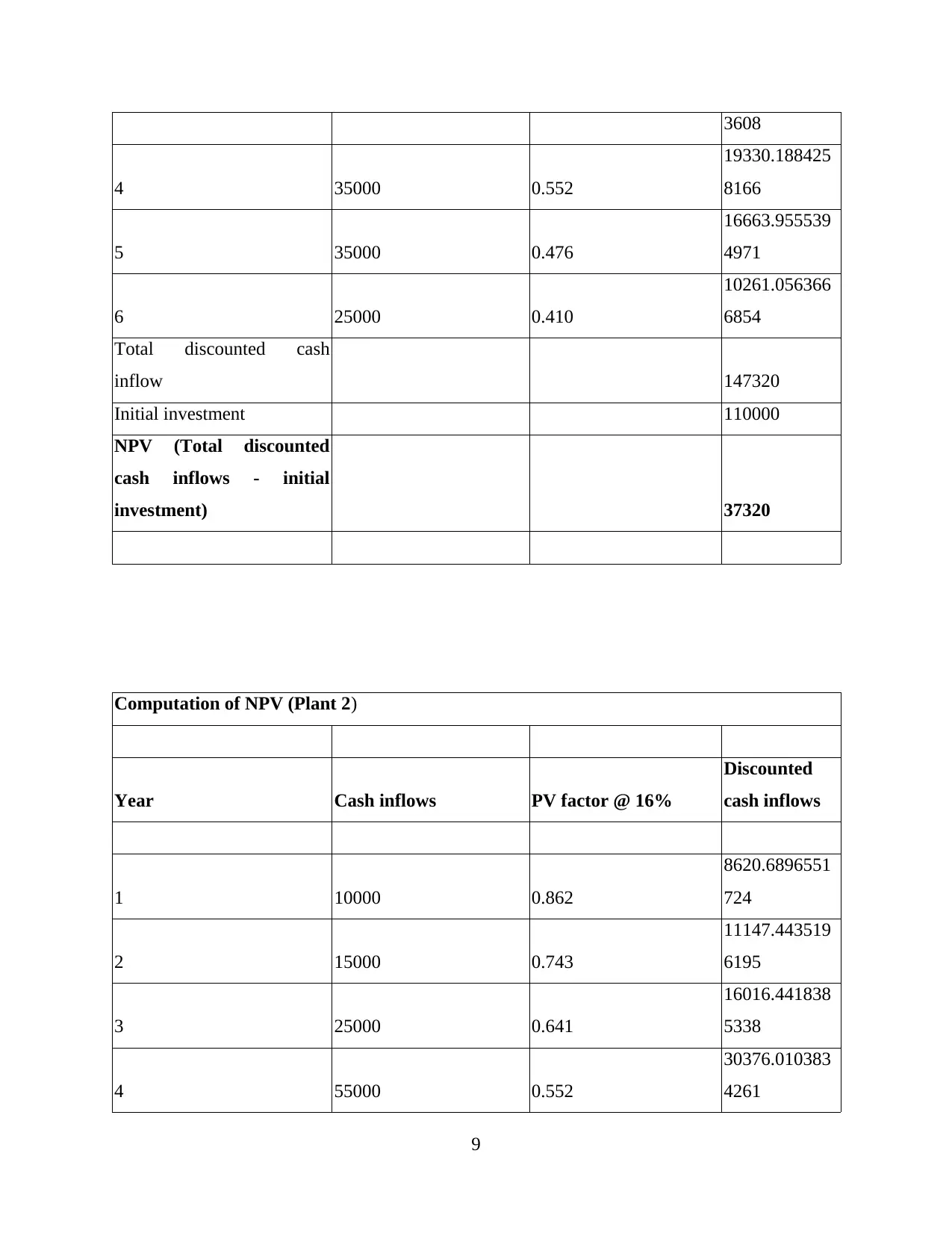

3608

4 35000 0.552

19330.188425

8166

5 35000 0.476

16663.955539

4971

6 25000 0.410

10261.056366

6854

Total discounted cash

inflow 147320

Initial investment 110000

NPV (Total discounted

cash inflows - initial

investment) 37320

Computation of NPV (Plant 2)

Year Cash inflows PV factor @ 16%

Discounted

cash inflows

1 10000 0.862

8620.6896551

724

2 15000 0.743

11147.443519

6195

3 25000 0.641

16016.441838

5338

4 55000 0.552

30376.010383

4261

9

4 35000 0.552

19330.188425

8166

5 35000 0.476

16663.955539

4971

6 25000 0.410

10261.056366

6854

Total discounted cash

inflow 147320

Initial investment 110000

NPV (Total discounted

cash inflows - initial

investment) 37320

Computation of NPV (Plant 2)

Year Cash inflows PV factor @ 16%

Discounted

cash inflows

1 10000 0.862

8620.6896551

724

2 15000 0.743

11147.443519

6195

3 25000 0.641

16016.441838

5338

4 55000 0.552

30376.010383

4261

9

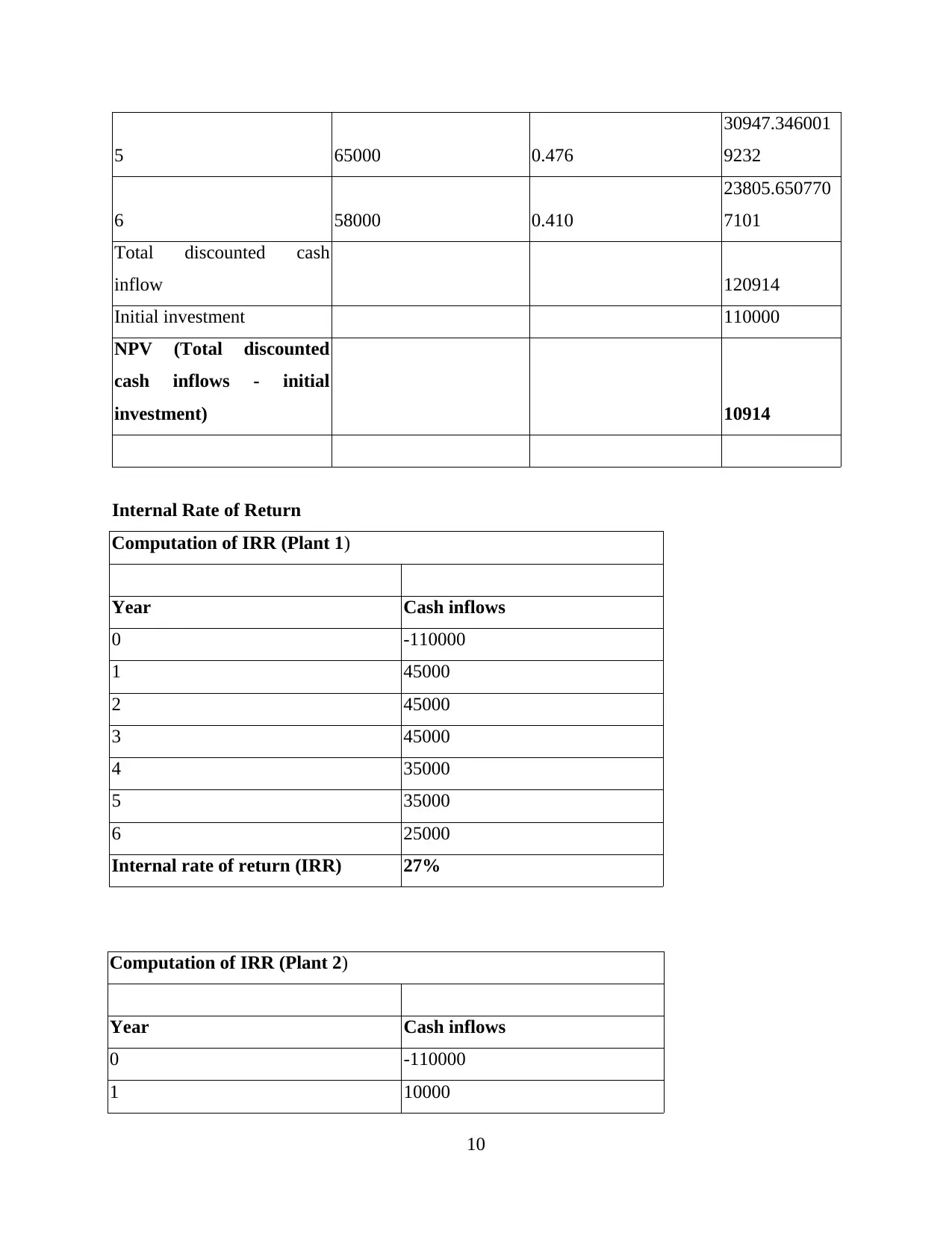

5 65000 0.476

30947.346001

9232

6 58000 0.410

23805.650770

7101

Total discounted cash

inflow 120914

Initial investment 110000

NPV (Total discounted

cash inflows - initial

investment) 10914

Internal Rate of Return

Computation of IRR (Plant 1)

Year Cash inflows

0 -110000

1 45000

2 45000

3 45000

4 35000

5 35000

6 25000

Internal rate of return (IRR) 27%

Computation of IRR (Plant 2)

Year Cash inflows

0 -110000

1 10000

10

30947.346001

9232

6 58000 0.410

23805.650770

7101

Total discounted cash

inflow 120914

Initial investment 110000

NPV (Total discounted

cash inflows - initial

investment) 10914

Internal Rate of Return

Computation of IRR (Plant 1)

Year Cash inflows

0 -110000

1 45000

2 45000

3 45000

4 35000

5 35000

6 25000

Internal rate of return (IRR) 27%

Computation of IRR (Plant 2)

Year Cash inflows

0 -110000

1 10000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.