Econometric Report: Causality and Forecasting in Sales and Advertising

VerifiedAdded on 2021/06/17

|12

|1519

|39

Report

AI Summary

This report replicates and analyzes the study "The long run, causality, and forecasting in the advertising-sales Relationship" by George P Zanias (1994), which examines the relationship between sales and advertising spending using the Lydia Pinkham data set from 1907 to 1960. The analysis involves co-integration, Granger Causality tests to determine the structural relationship, and Vector Error Correction Models (VECM) for forecasting. The study employs logarithmic values of advertising and sales to analyze growth patterns, finding a bi-directional Granger causality between the two variables, and uses impulse response functions to further analyze the relationship. The report also includes unit root tests to assess data stationarity and critical evaluation of the methodologies used, highlighting the study's contribution to improved forecasting through the use of error correction models, although the model fit is weak due to the omission of other variables. The study does take into account Auto-Correlation or serial co-relation among the variables, which makes the study incomplete.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

[Type the document title]

[Type the document subtitle]

[Pick the date]

Geeta

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

[Type the document title]

[Type the document subtitle]

[Pick the date]

Geeta

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Summary.....................................................................................................................................................1

Critical evaluation........................................................................................................................................1

Data and Analysis : Model Replication........................................................................................................2

Unit Root Tests........................................................................................................................................2

Granger Causality Test.............................................................................................................................6

Further Analysis..........................................................................................................................................8

Further Structural Analysis using impulse responses...............................................................................8

Vector Error Correction Model Forecasts................................................................................................9

Bibliography...............................................................................................................................................11

Summary

The paper being replicated is “The long run, causality, and forecasting in the advertising- sales

Relationship” by George P Zanias.(Zanias, 1994) The paper conduct a co-integration analysis of

the Lydia Pinkham Data set. The Co-intergration analysis is used to analyse the long term

relationship between the sales and advertising process. Granger Causality test is used to test this

relationship and model the data, using an error corrected model.

The paper takes the logarithmic values of the advertising and sales spending (in US Dollars) .

Logarithmic values often depict the growth of a variable, implying that spending in advertising

grew, given an increase in sales and vice versa.

The study utilized data from 1907 to 1960 i.e 53 years. The study models data in both the long

run and short run. The author finds that there is a bi-directional Granger causality between the

two variables viz: sales and advertising, in the long run. In simple words, the study concludes

that the greater increases in sales revenue are caused by advertising, the greater is the likelihood

of an increase in spending in advertising. The study also, compared the results with previous

studies using the same data sets and concluded that the forecasts are better of error correction

systems are employed and data is modeled in error corrected models i.e. residuals in an equation

should not be neglected.

Summary.....................................................................................................................................................1

Critical evaluation........................................................................................................................................1

Data and Analysis : Model Replication........................................................................................................2

Unit Root Tests........................................................................................................................................2

Granger Causality Test.............................................................................................................................6

Further Analysis..........................................................................................................................................8

Further Structural Analysis using impulse responses...............................................................................8

Vector Error Correction Model Forecasts................................................................................................9

Bibliography...............................................................................................................................................11

Summary

The paper being replicated is “The long run, causality, and forecasting in the advertising- sales

Relationship” by George P Zanias.(Zanias, 1994) The paper conduct a co-integration analysis of

the Lydia Pinkham Data set. The Co-intergration analysis is used to analyse the long term

relationship between the sales and advertising process. Granger Causality test is used to test this

relationship and model the data, using an error corrected model.

The paper takes the logarithmic values of the advertising and sales spending (in US Dollars) .

Logarithmic values often depict the growth of a variable, implying that spending in advertising

grew, given an increase in sales and vice versa.

The study utilized data from 1907 to 1960 i.e 53 years. The study models data in both the long

run and short run. The author finds that there is a bi-directional Granger causality between the

two variables viz: sales and advertising, in the long run. In simple words, the study concludes

that the greater increases in sales revenue are caused by advertising, the greater is the likelihood

of an increase in spending in advertising. The study also, compared the results with previous

studies using the same data sets and concluded that the forecasts are better of error correction

systems are employed and data is modeled in error corrected models i.e. residuals in an equation

should not be neglected.

Critical evaluation

Granger Causality test is usually, conducted to establish if there is a structural relationship

between two variables. The test is well designed since it utilizes the Granger Causality Test with

the log of variables. Taking the log of variable helps establish the structural relationship even

further since the causality between the logs of variables will help understand how the growth in

one variable affects the growth in another variable and it helps understand “elasticity” between

two variables.(Wooldridge, 2015)

The paper goes into details about the augmentation of the Dickey Fuller (Augmented Dickey

Fuller) test to highlight the importance of lags in the causality. (Sjo, 2008) However, the use of

Dickey Fuller Test and Augmented Dickey Fuller Test seem to be redundant. Co-integration is

further established using the Co-integration Durbin Watson (CRDW) Statistic.

The logarithmic values of both the series seem to be non-stationary and had to be differentiated.

However, the tests conducted in this report provide results to the contrary and establish that the

logarithmic values of both the variables are stationary. The reasons for the differing results

cannot be , understood. However, the author does, further use the Error Corrected Model for

modeling which seems appropriate.(Wooldridge, 2015)

The study does take into account Auto-Correlation or serial co-relation among the variables,

which makes the study incomplete. It is possible that the growth is a result of serial co-relation

and not exclusively caused by a change in the other variable.(Wooldridge, 2015)

Overall, the study has been well designed and implemented with all the appropriate tests being

conducted. The study also, highlights the importance of logarithmic values compared to

arithmetic values. The primary achievement of the study, however, lies in the fact that it has

contributed to literature by improving the quality of forecasts as compared to previous studies by

including a vector-error corrected model.

Data and Analysis : Model Replication

The data taken is sales and advertising data for the period of 1907 to 1960. In this data, the data

taken is for both

Unit Root Tests

The paper first evaluates the stationarity of the data. The stationarity of the data is evaluated

using the Advanced Dickey Fuller Test (separately for both variables). The Null Hypothesis

Granger Causality test is usually, conducted to establish if there is a structural relationship

between two variables. The test is well designed since it utilizes the Granger Causality Test with

the log of variables. Taking the log of variable helps establish the structural relationship even

further since the causality between the logs of variables will help understand how the growth in

one variable affects the growth in another variable and it helps understand “elasticity” between

two variables.(Wooldridge, 2015)

The paper goes into details about the augmentation of the Dickey Fuller (Augmented Dickey

Fuller) test to highlight the importance of lags in the causality. (Sjo, 2008) However, the use of

Dickey Fuller Test and Augmented Dickey Fuller Test seem to be redundant. Co-integration is

further established using the Co-integration Durbin Watson (CRDW) Statistic.

The logarithmic values of both the series seem to be non-stationary and had to be differentiated.

However, the tests conducted in this report provide results to the contrary and establish that the

logarithmic values of both the variables are stationary. The reasons for the differing results

cannot be , understood. However, the author does, further use the Error Corrected Model for

modeling which seems appropriate.(Wooldridge, 2015)

The study does take into account Auto-Correlation or serial co-relation among the variables,

which makes the study incomplete. It is possible that the growth is a result of serial co-relation

and not exclusively caused by a change in the other variable.(Wooldridge, 2015)

Overall, the study has been well designed and implemented with all the appropriate tests being

conducted. The study also, highlights the importance of logarithmic values compared to

arithmetic values. The primary achievement of the study, however, lies in the fact that it has

contributed to literature by improving the quality of forecasts as compared to previous studies by

including a vector-error corrected model.

Data and Analysis : Model Replication

The data taken is sales and advertising data for the period of 1907 to 1960. In this data, the data

taken is for both

Unit Root Tests

The paper first evaluates the stationarity of the data. The stationarity of the data is evaluated

using the Advanced Dickey Fuller Test (separately for both variables). The Null Hypothesis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

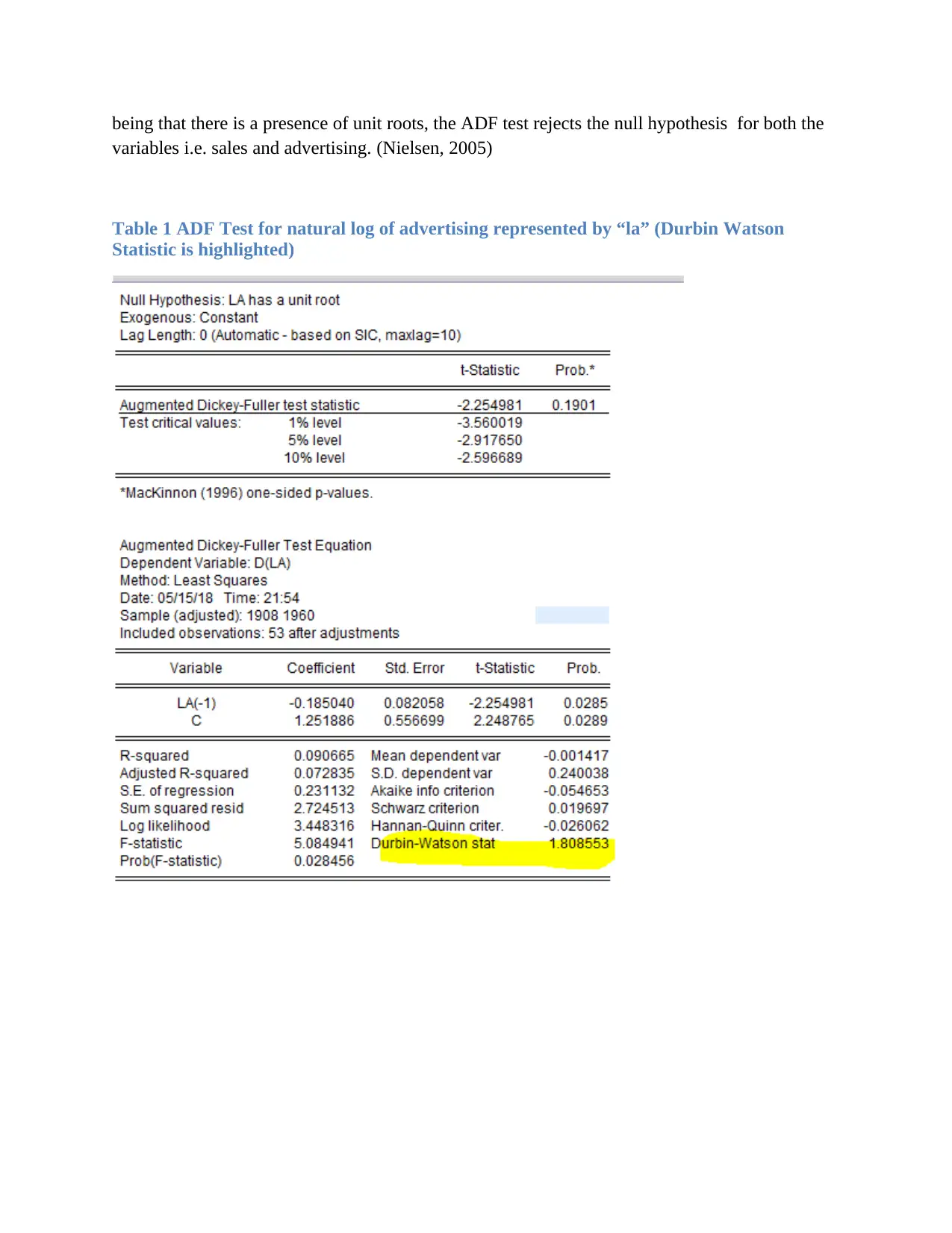

being that there is a presence of unit roots, the ADF test rejects the null hypothesis for both the

variables i.e. sales and advertising. (Nielsen, 2005)

Table 1 ADF Test for natural log of advertising represented by “la” (Durbin Watson

Statistic is highlighted)

variables i.e. sales and advertising. (Nielsen, 2005)

Table 1 ADF Test for natural log of advertising represented by “la” (Durbin Watson

Statistic is highlighted)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

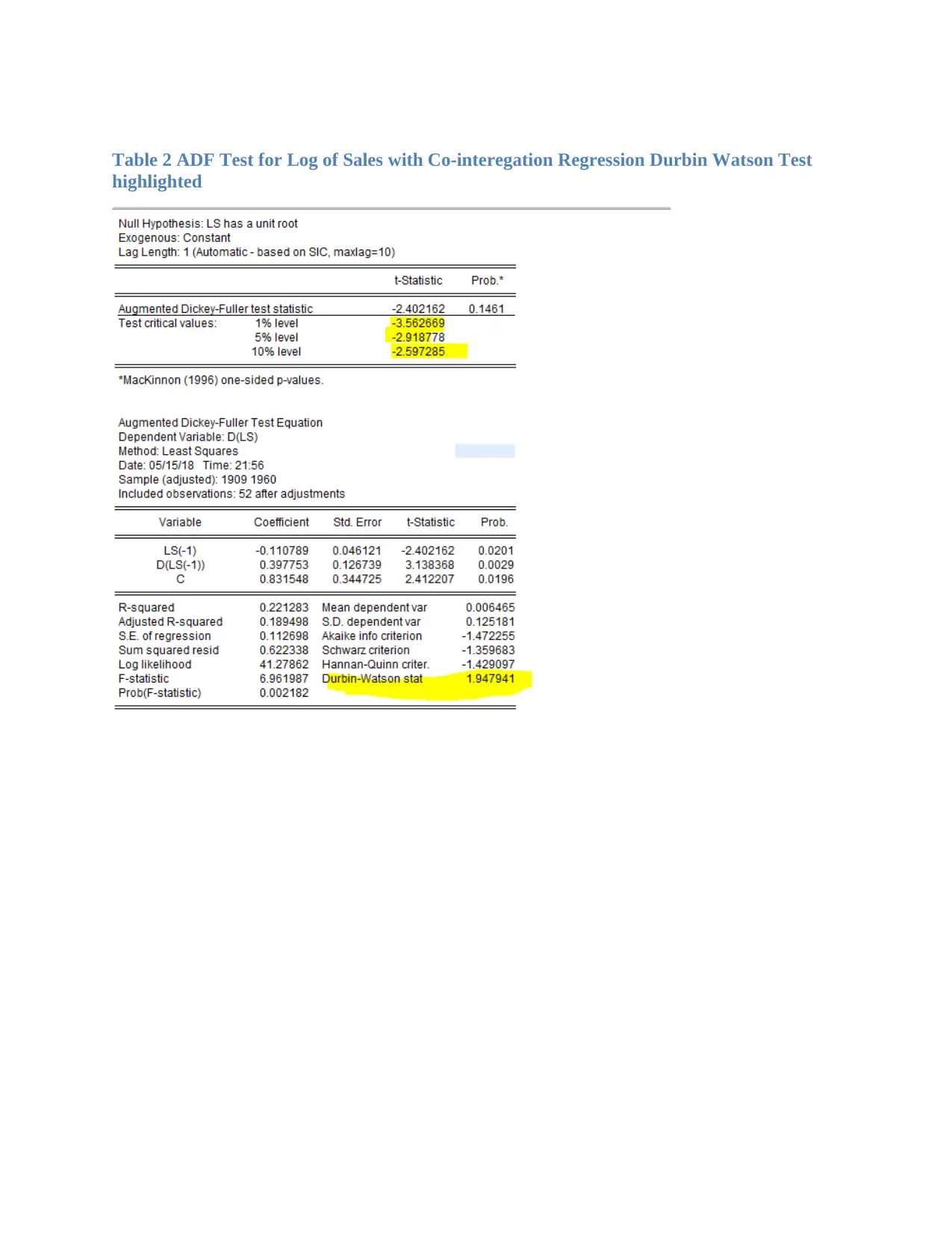

Table 2 ADF Test for Log of Sales with Co-interegation Regression Durbin Watson Test

highlighted

highlighted

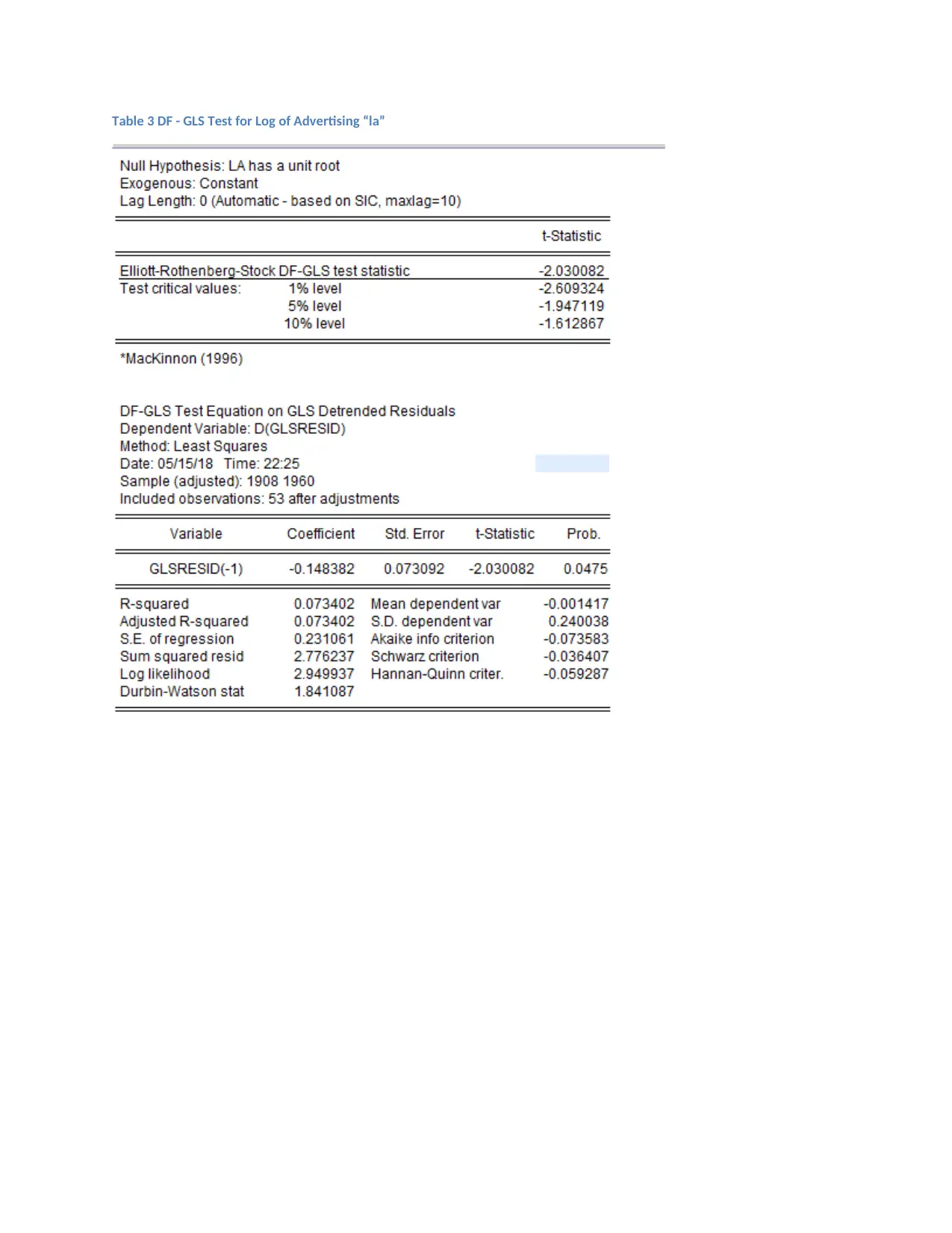

Table 3 DF - GLS Test for Log of Advertising “la”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

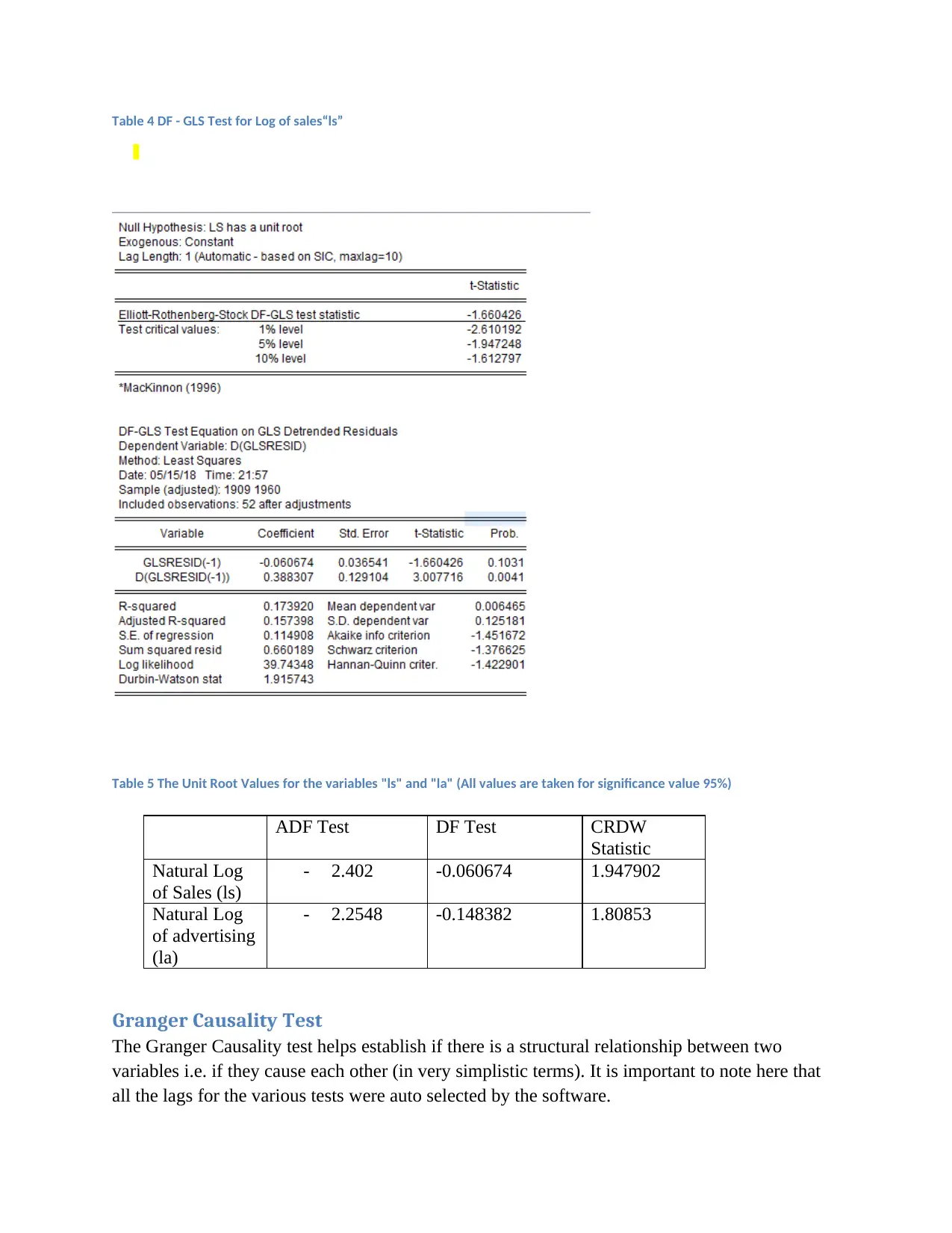

Table 4 DF - GLS Test for Log of sales“ls”

Table 5 The Unit Root Values for the variables "ls" and "la" (All values are taken for significance value 95%)

Granger Causality Test

The Granger Causality test helps establish if there is a structural relationship between two

variables i.e. if they cause each other (in very simplistic terms). It is important to note here that

all the lags for the various tests were auto selected by the software.

ADF Test DF Test CRDW

Statistic

Natural Log

of Sales (ls)

- 2.402 -0.060674 1.947902

Natural Log

of advertising

(la)

- 2.2548 -0.148382 1.80853

Table 5 The Unit Root Values for the variables "ls" and "la" (All values are taken for significance value 95%)

Granger Causality Test

The Granger Causality test helps establish if there is a structural relationship between two

variables i.e. if they cause each other (in very simplistic terms). It is important to note here that

all the lags for the various tests were auto selected by the software.

ADF Test DF Test CRDW

Statistic

Natural Log

of Sales (ls)

- 2.402 -0.060674 1.947902

Natural Log

of advertising

(la)

- 2.2548 -0.148382 1.80853

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The equation for the Granger Causality is:

Lst = α + ∑ β (lst-1) + Residuals --- >

Lsa= α + ∑ β (lat-1) + Residuals --->

If the test is significant , then the null hypothesis that there is no Granger Causality from one

variable to another is not rejected.

The output is as follows:

Table 6 Pair Wise Granger Causality Test

In the above results, the p-value in both cases “LS does not Granger cause La” and “La does not

Granger cause Ls” is below 0.05 i.e the test is not significant for both cases. Hence, the null

hypothesis is rejected in both cases and alternative hypothesis is accepted i.e. “LS Granger

causes La” and ““La Granger causes Ls”

Thus, there is a two way causality between the two variables.

Lst = α + ∑ β (lst-1) + Residuals --- >

Lsa= α + ∑ β (lat-1) + Residuals --->

If the test is significant , then the null hypothesis that there is no Granger Causality from one

variable to another is not rejected.

The output is as follows:

Table 6 Pair Wise Granger Causality Test

In the above results, the p-value in both cases “LS does not Granger cause La” and “La does not

Granger cause Ls” is below 0.05 i.e the test is not significant for both cases. Hence, the null

hypothesis is rejected in both cases and alternative hypothesis is accepted i.e. “LS Granger

causes La” and ““La Granger causes Ls”

Thus, there is a two way causality between the two variables.

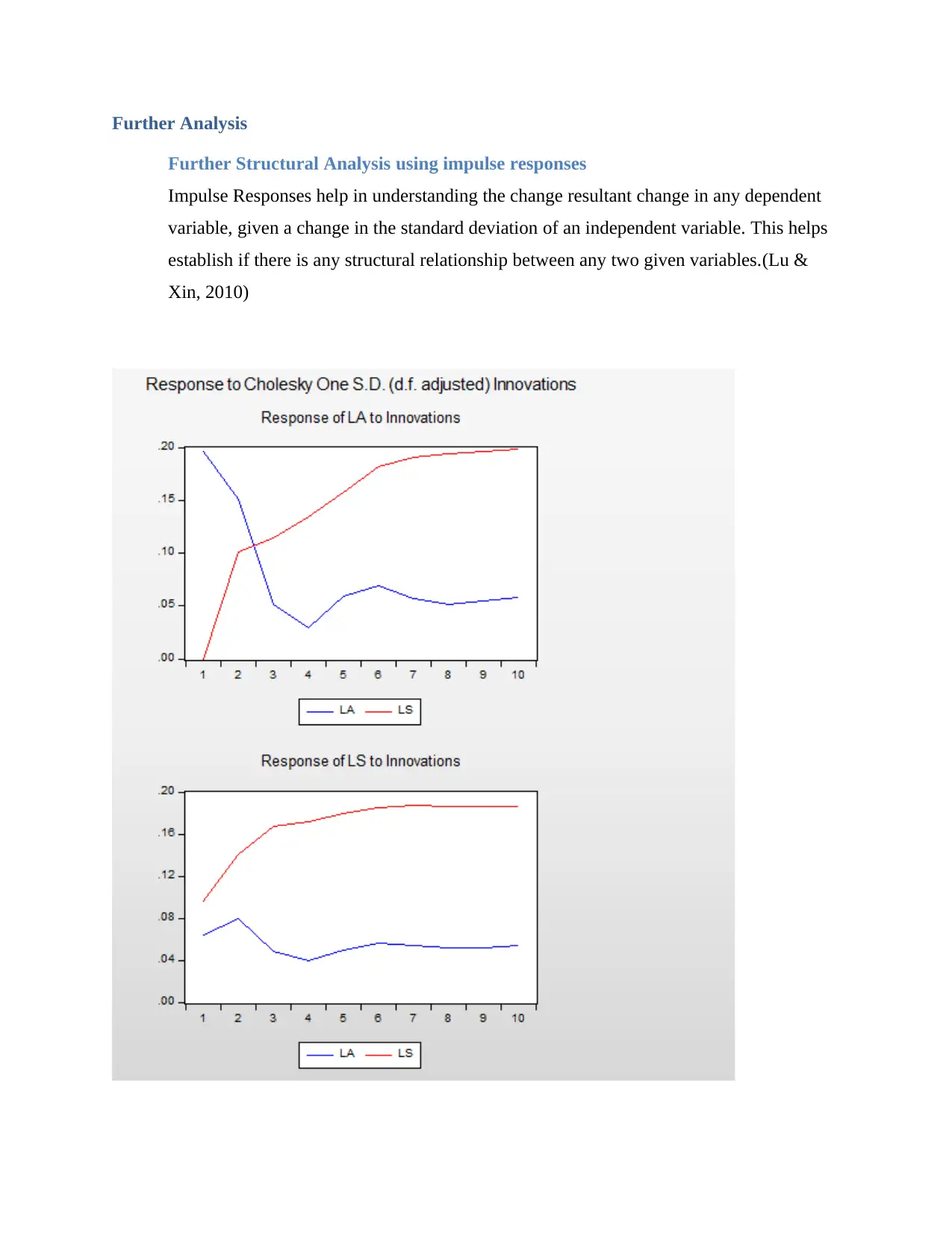

Further Analysis

Further Structural Analysis using impulse responses

Impulse Responses help in understanding the change resultant change in any dependent

variable, given a change in the standard deviation of an independent variable. This helps

establish if there is any structural relationship between any two given variables.(Lu &

Xin, 2010)

Further Structural Analysis using impulse responses

Impulse Responses help in understanding the change resultant change in any dependent

variable, given a change in the standard deviation of an independent variable. This helps

establish if there is any structural relationship between any two given variables.(Lu &

Xin, 2010)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The plotted impulse response graph shows that for every standard deviation change in the

Logarithmic values of sales moves away further . Similarly, for every change in the standard

deviation in the logarithmic values of sales, the logarithmic values move away further. This

implies that there is a structural relationship that works both ways.

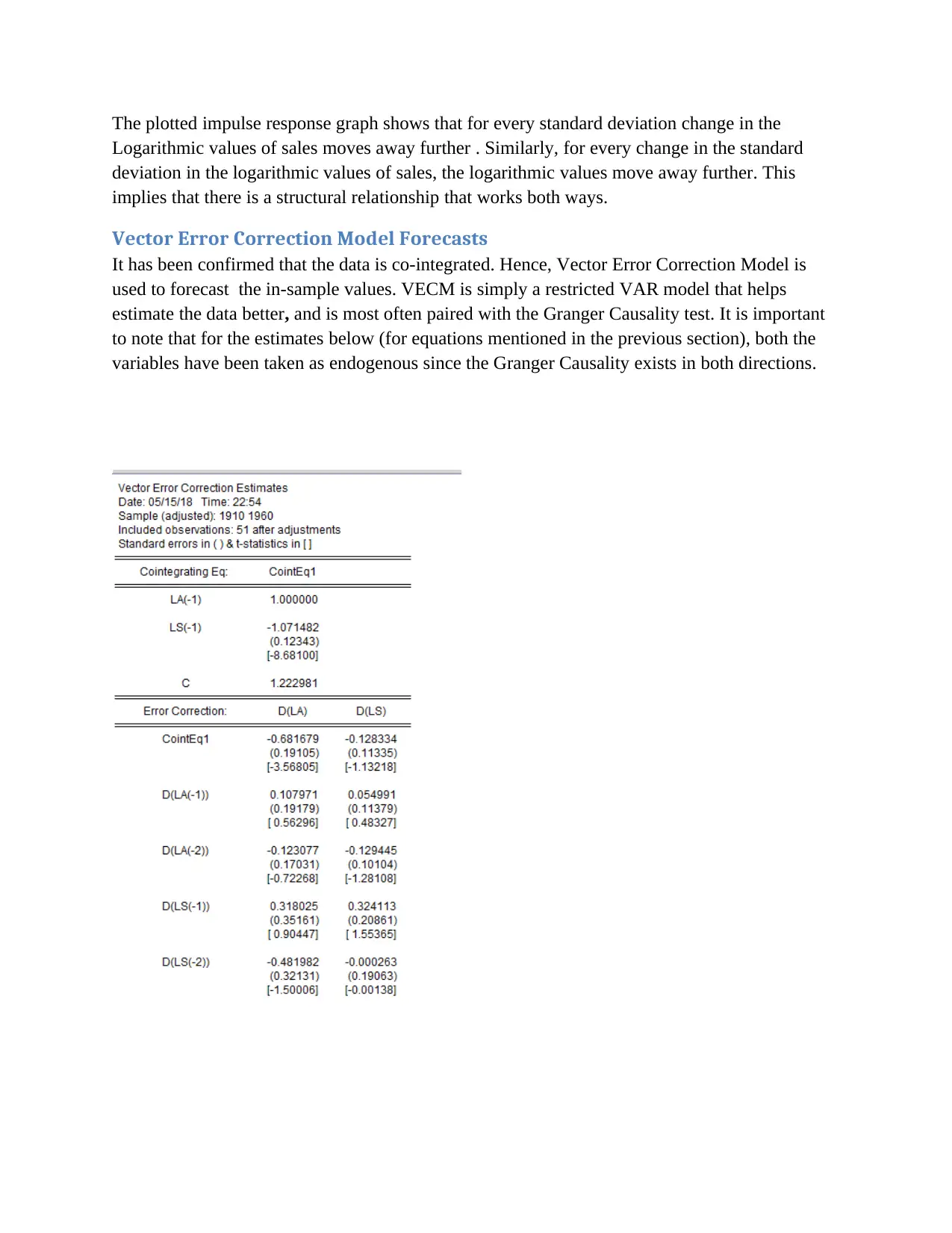

Vector Error Correction Model Forecasts

It has been confirmed that the data is co-integrated. Hence, Vector Error Correction Model is

used to forecast the in-sample values. VECM is simply a restricted VAR model that helps

estimate the data better, and is most often paired with the Granger Causality test. It is important

to note that for the estimates below (for equations mentioned in the previous section), both the

variables have been taken as endogenous since the Granger Causality exists in both directions.

Logarithmic values of sales moves away further . Similarly, for every change in the standard

deviation in the logarithmic values of sales, the logarithmic values move away further. This

implies that there is a structural relationship that works both ways.

Vector Error Correction Model Forecasts

It has been confirmed that the data is co-integrated. Hence, Vector Error Correction Model is

used to forecast the in-sample values. VECM is simply a restricted VAR model that helps

estimate the data better, and is most often paired with the Granger Causality test. It is important

to note that for the estimates below (for equations mentioned in the previous section), both the

variables have been taken as endogenous since the Granger Causality exists in both directions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

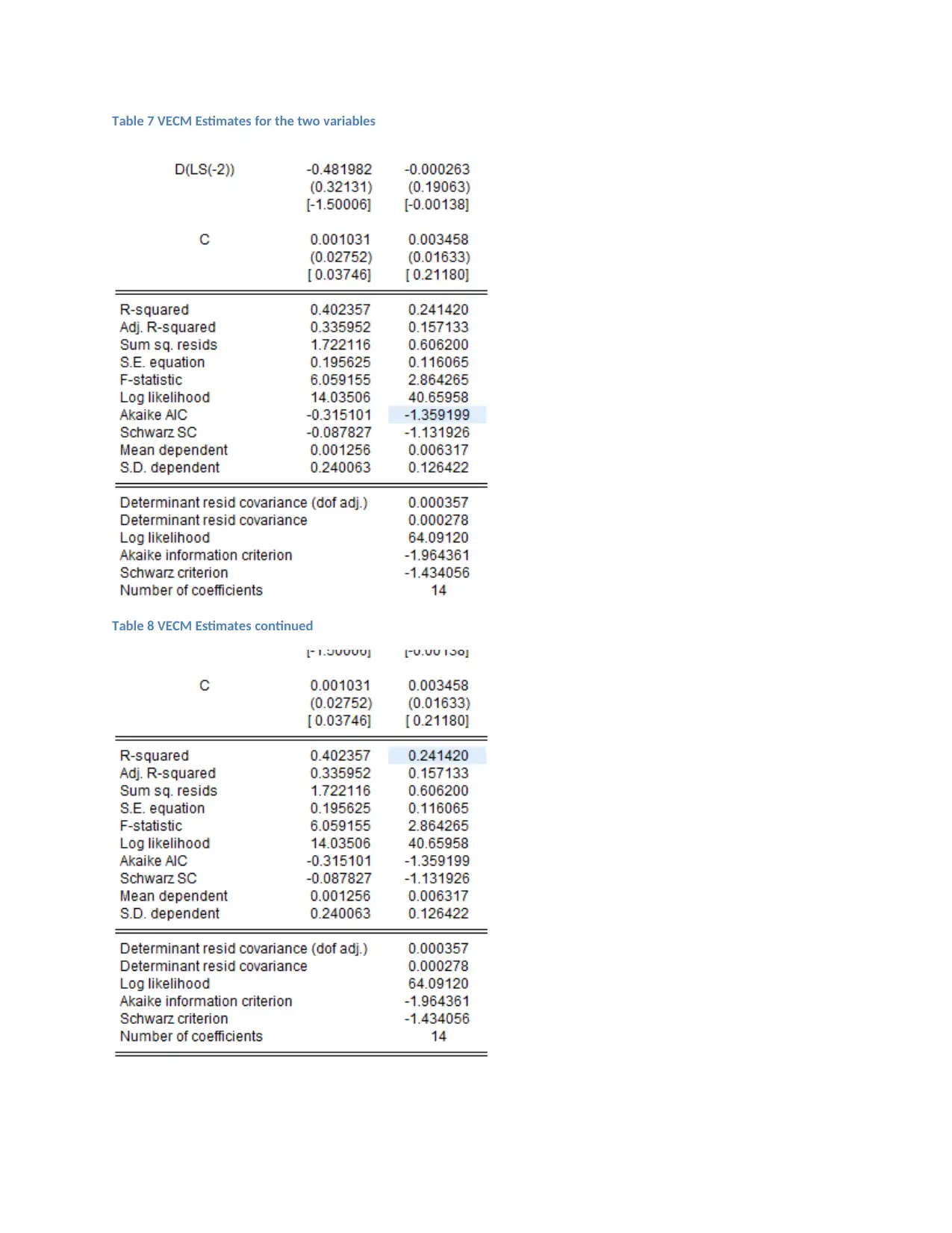

Table 7 VECM Estimates for the two variables

Table 8 VECM Estimates continued

Table 8 VECM Estimates continued

As seen above, the model is not a good fit since the R-Square is less than 0.5 I,e the model is a

weak fit. In order to improve the model , more variables must be accounted for i.e there are other

variables that cause a change in spending in advertising and sales.

Bibliography

Lu, C., & Xin, Z. (2010). Impulse-Response function Analysis: An application to macroeconomy data of

China. Hoskolan Dalarna, Sweden: School of Economics and Social Sciences, Hoskolan Dalarna.

Nielsen, H. B. (2005). Non-Stationary Time Series and Unit Root Tests. Retrieved March 29, 2018, from

http://www.econ.ku.dk/metrics/econometrics2_05_ii/slides/08_unitroottests_2pp.pdf

Sjo, B. (2008, August). Testing for Unit Roots and Cointegration -Guide. Retrieved from Research Gate:

https://www.researchgate.net/publication/265151092_Testing_for_Unit_Roots_and_Cointegra

tion_-Guide

Wooldridge, J. M. (2015). Introductory Econometrics: A Modern Approach : Sixth Edition (pg 75). online:

Cengage Learning.

Zanias, G. P. (1994). The long run, causality, and forecasting in the advertising-sales relationship. Journal

of Forecasting , 13 (7), 601 -610.

weak fit. In order to improve the model , more variables must be accounted for i.e there are other

variables that cause a change in spending in advertising and sales.

Bibliography

Lu, C., & Xin, Z. (2010). Impulse-Response function Analysis: An application to macroeconomy data of

China. Hoskolan Dalarna, Sweden: School of Economics and Social Sciences, Hoskolan Dalarna.

Nielsen, H. B. (2005). Non-Stationary Time Series and Unit Root Tests. Retrieved March 29, 2018, from

http://www.econ.ku.dk/metrics/econometrics2_05_ii/slides/08_unitroottests_2pp.pdf

Sjo, B. (2008, August). Testing for Unit Roots and Cointegration -Guide. Retrieved from Research Gate:

https://www.researchgate.net/publication/265151092_Testing_for_Unit_Roots_and_Cointegra

tion_-Guide

Wooldridge, J. M. (2015). Introductory Econometrics: A Modern Approach : Sixth Edition (pg 75). online:

Cengage Learning.

Zanias, G. P. (1994). The long run, causality, and forecasting in the advertising-sales relationship. Journal

of Forecasting , 13 (7), 601 -610.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.