Financial Analysis: Sales, Production Budgets, and Costing Methods

VerifiedAdded on 2019/09/13

|5

|940

|54

Homework Assignment

AI Summary

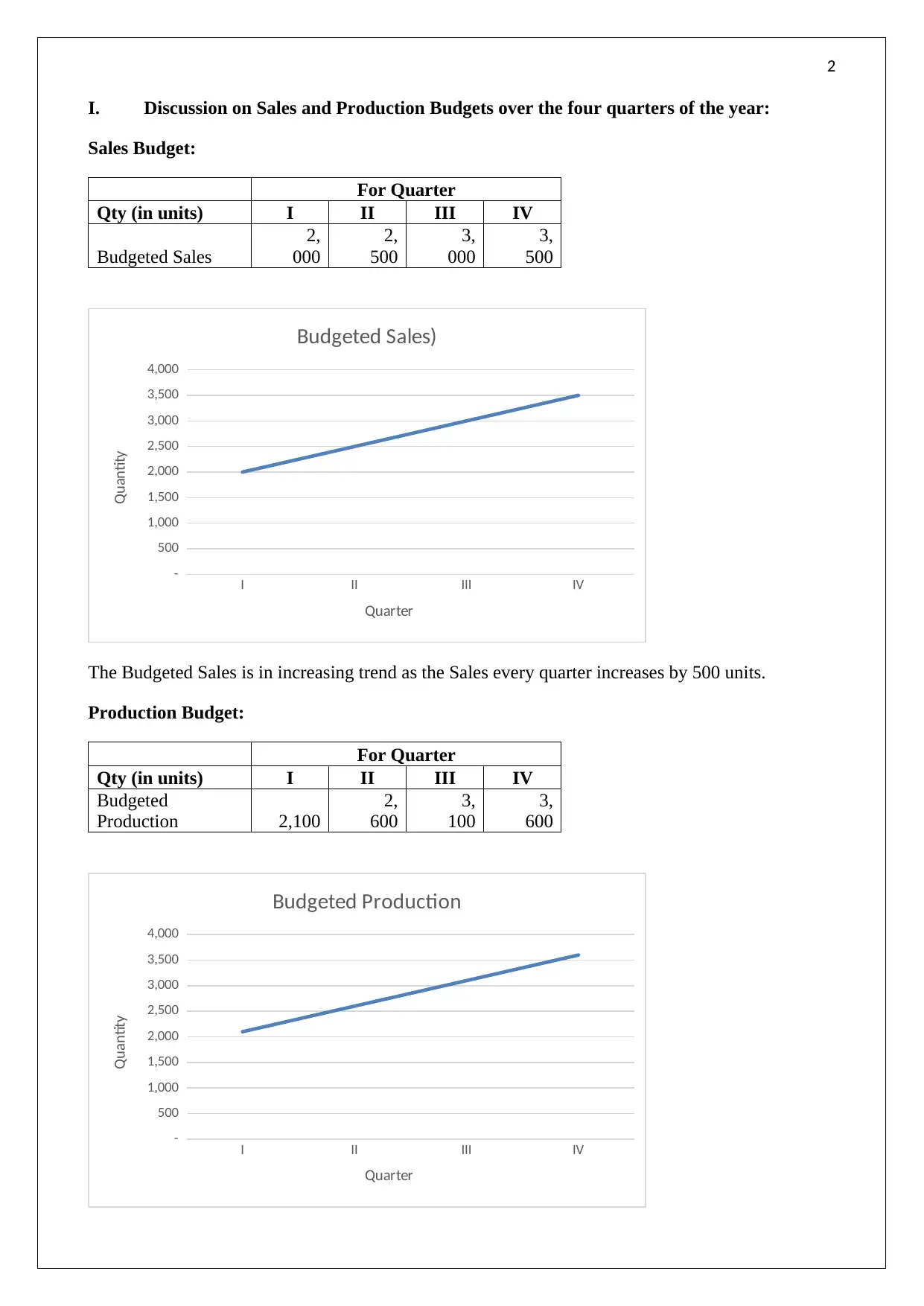

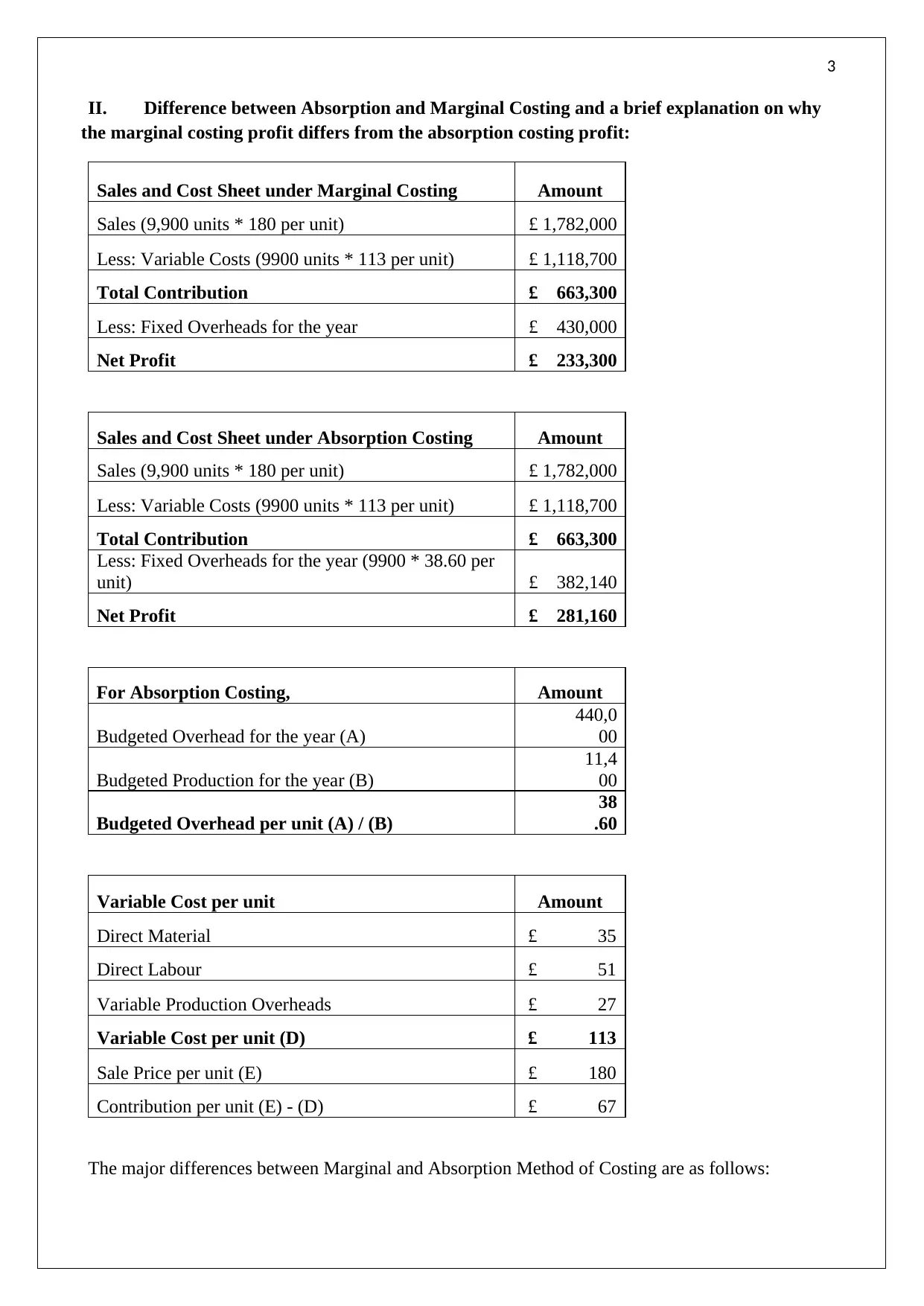

This assignment provides a comprehensive analysis of sales and production budgets across four quarters, detailing budgeted sales and production quantities. It explores the differences between absorption and marginal costing methods, highlighting how they impact profit calculations due to the treatment of fixed overheads. The solution includes detailed sales and cost sheets under both costing methods, explaining the classification of costs and the impact on net profit. Furthermore, it identifies circumstances under which both methods would yield the same profit. The assignment also calculates the break-even point and determines the new selling price required to break even at a different sales volume. Finally, it presents best, worst, and most-likely scenarios, analyzing sales revenue, absorption costing profit, and break-even points under each scenario, with references to relevant accounting resources.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.