Finance for Strategic Managers: Samsung PLC Financial Analysis Report

VerifiedAdded on 2023/01/20

|10

|2068

|51

Report

AI Summary

This report provides a comprehensive financial analysis of Samsung PLC, examining its financial statements, including the Statement of Cash Flows, Statement of Profits or Loss, and Statement of Financial Position. It assesses Samsung's current viability by interpreting financial data from 2017 and 2018, and conducting a comparative ratio analysis to evaluate liquidity, profitability, and leverage. The report also provides recommendations based on the financial data, such as reducing the current ratio and increasing revenue while managing costs. Furthermore, it includes a capital expenditure appraisal for evaluating new versus current machinery using the Net Present Value method, recommending the purchase of new machinery based on a higher NPV. The report concludes that finance plays a vital role in strategic planning, enabling managers to align business strategies with the internal and external environment.

FINANCE FOR

STRATEGIC MANAGERS

STRATEGIC MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

[Covered in PPT].........................................................................................................................1

TASK 2............................................................................................................................................1

Interpretation of Samsung PLC Financial Statements to assess its current viability..................1

Comparative analysis of Financial Data related to Samsung PLC.............................................2

Recommendations.......................................................................................................................3

TASK 3............................................................................................................................................4

[Covered in Information Leaflet]................................................................................................4

TASK 4............................................................................................................................................4

Capital Expenditure Appraisal....................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDICES.................................................................................................................................7

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

[Covered in PPT].........................................................................................................................1

TASK 2............................................................................................................................................1

Interpretation of Samsung PLC Financial Statements to assess its current viability..................1

Comparative analysis of Financial Data related to Samsung PLC.............................................2

Recommendations.......................................................................................................................3

TASK 3............................................................................................................................................4

[Covered in Information Leaflet]................................................................................................4

TASK 4............................................................................................................................................4

Capital Expenditure Appraisal....................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDICES.................................................................................................................................7

INTRODUCTION

Finance for Strategic Managers plays an important role as most of the businesses require

formulation of various strategies and decisions on the type of financial data and information

available with the company. Such managers, then, analyse and interpret various data so as to

conduct resource planning and forecasting so as to achieve their overall short-term and long-term

objectives (Alkaraan, 2015). This report aims to provide a detailed account on Samsung PLC in

regards to the types of methodologies undertaken by it for the purpose of strategic planning,

appraisal of capital investment projects as well as financial data required for the same. The entire

report is bifurcated into various tasks which provides supporting evidence for the members of

Chamber of Commerce who want to research and study the success of Samsung PLC. For this

purpose, this report aims to provide a presentation, information leaflet, discussion paper and

practical application of capital expenditure appraisal methods in a comprehensive manner.

TASK 1

[Covered in PPT]

TASK 2

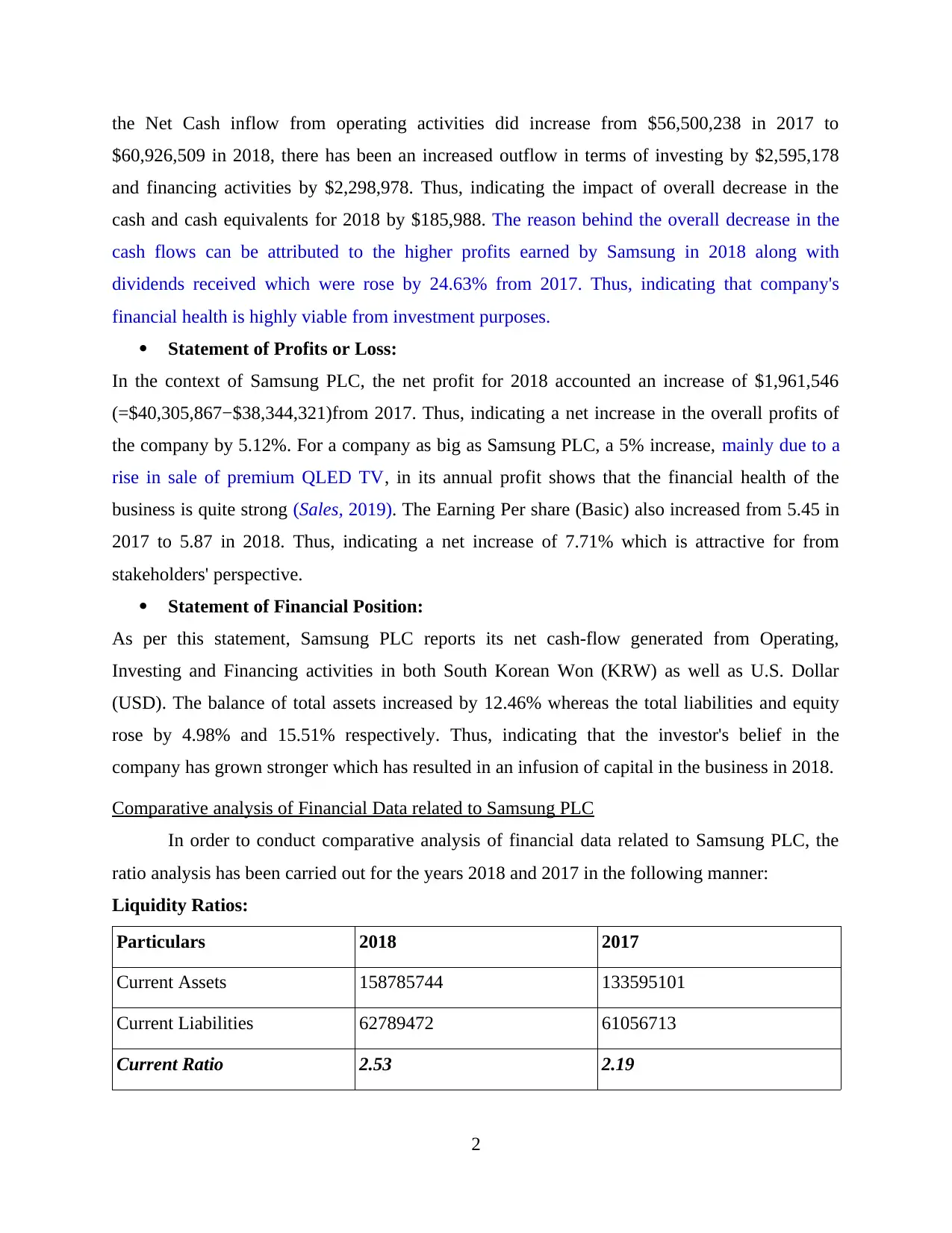

Interpretation of Samsung PLC Financial Statements to assess its current viability

Financial Statements help in providing relevant information to not only the management

of the business but also to other internal as well as external stakeholders. This is due to the fact

that they include all the financial data in a predefined format that facilitates easy identification of

the company's health in terms of corporate performance and profitability.

In the context of Samsung PLC, the company creates quarter-wise reports along with a

full year report so as to brief their stakeholders in a continuous manner (Annual Report, 2018).

For this purpose, however, the following financial statements, related to full year, have been

analysed so as to determine its current viability:

Statement of Cash Flows:

As per this statement, Samsung PLC reports its net cash-flow generated from Operating,

Investing and Financing activities in both South Korean Won (KRW) as well as U.S. Dollar

(USD). The balance of cash and cash equivalents at the beginning of 2018 is reported as

$27,763,038 whereas at the end of the period, this amount reduced to $27,577,050. Even though

1

Finance for Strategic Managers plays an important role as most of the businesses require

formulation of various strategies and decisions on the type of financial data and information

available with the company. Such managers, then, analyse and interpret various data so as to

conduct resource planning and forecasting so as to achieve their overall short-term and long-term

objectives (Alkaraan, 2015). This report aims to provide a detailed account on Samsung PLC in

regards to the types of methodologies undertaken by it for the purpose of strategic planning,

appraisal of capital investment projects as well as financial data required for the same. The entire

report is bifurcated into various tasks which provides supporting evidence for the members of

Chamber of Commerce who want to research and study the success of Samsung PLC. For this

purpose, this report aims to provide a presentation, information leaflet, discussion paper and

practical application of capital expenditure appraisal methods in a comprehensive manner.

TASK 1

[Covered in PPT]

TASK 2

Interpretation of Samsung PLC Financial Statements to assess its current viability

Financial Statements help in providing relevant information to not only the management

of the business but also to other internal as well as external stakeholders. This is due to the fact

that they include all the financial data in a predefined format that facilitates easy identification of

the company's health in terms of corporate performance and profitability.

In the context of Samsung PLC, the company creates quarter-wise reports along with a

full year report so as to brief their stakeholders in a continuous manner (Annual Report, 2018).

For this purpose, however, the following financial statements, related to full year, have been

analysed so as to determine its current viability:

Statement of Cash Flows:

As per this statement, Samsung PLC reports its net cash-flow generated from Operating,

Investing and Financing activities in both South Korean Won (KRW) as well as U.S. Dollar

(USD). The balance of cash and cash equivalents at the beginning of 2018 is reported as

$27,763,038 whereas at the end of the period, this amount reduced to $27,577,050. Even though

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the Net Cash inflow from operating activities did increase from $56,500,238 in 2017 to

$60,926,509 in 2018, there has been an increased outflow in terms of investing by $2,595,178

and financing activities by $2,298,978. Thus, indicating the impact of overall decrease in the

cash and cash equivalents for 2018 by $185,988. The reason behind the overall decrease in the

cash flows can be attributed to the higher profits earned by Samsung in 2018 along with

dividends received which were rose by 24.63% from 2017. Thus, indicating that company's

financial health is highly viable from investment purposes.

Statement of Profits or Loss:

In the context of Samsung PLC, the net profit for 2018 accounted an increase of $1,961,546

(=$40,305,867−$38,344,321)from 2017. Thus, indicating a net increase in the overall profits of

the company by 5.12%. For a company as big as Samsung PLC, a 5% increase, mainly due to a

rise in sale of premium QLED TV, in its annual profit shows that the financial health of the

business is quite strong (Sales, 2019). The Earning Per share (Basic) also increased from 5.45 in

2017 to 5.87 in 2018. Thus, indicating a net increase of 7.71% which is attractive for from

stakeholders' perspective.

Statement of Financial Position:

As per this statement, Samsung PLC reports its net cash-flow generated from Operating,

Investing and Financing activities in both South Korean Won (KRW) as well as U.S. Dollar

(USD). The balance of total assets increased by 12.46% whereas the total liabilities and equity

rose by 4.98% and 15.51% respectively. Thus, indicating that the investor's belief in the

company has grown stronger which has resulted in an infusion of capital in the business in 2018.

Comparative analysis of Financial Data related to Samsung PLC

In order to conduct comparative analysis of financial data related to Samsung PLC, the

ratio analysis has been carried out for the years 2018 and 2017 in the following manner:

Liquidity Ratios:

Particulars 2018 2017

Current Assets 158785744 133595101

Current Liabilities 62789472 61056713

Current Ratio 2.53 2.19

2

$60,926,509 in 2018, there has been an increased outflow in terms of investing by $2,595,178

and financing activities by $2,298,978. Thus, indicating the impact of overall decrease in the

cash and cash equivalents for 2018 by $185,988. The reason behind the overall decrease in the

cash flows can be attributed to the higher profits earned by Samsung in 2018 along with

dividends received which were rose by 24.63% from 2017. Thus, indicating that company's

financial health is highly viable from investment purposes.

Statement of Profits or Loss:

In the context of Samsung PLC, the net profit for 2018 accounted an increase of $1,961,546

(=$40,305,867−$38,344,321)from 2017. Thus, indicating a net increase in the overall profits of

the company by 5.12%. For a company as big as Samsung PLC, a 5% increase, mainly due to a

rise in sale of premium QLED TV, in its annual profit shows that the financial health of the

business is quite strong (Sales, 2019). The Earning Per share (Basic) also increased from 5.45 in

2017 to 5.87 in 2018. Thus, indicating a net increase of 7.71% which is attractive for from

stakeholders' perspective.

Statement of Financial Position:

As per this statement, Samsung PLC reports its net cash-flow generated from Operating,

Investing and Financing activities in both South Korean Won (KRW) as well as U.S. Dollar

(USD). The balance of total assets increased by 12.46% whereas the total liabilities and equity

rose by 4.98% and 15.51% respectively. Thus, indicating that the investor's belief in the

company has grown stronger which has resulted in an infusion of capital in the business in 2018.

Comparative analysis of Financial Data related to Samsung PLC

In order to conduct comparative analysis of financial data related to Samsung PLC, the

ratio analysis has been carried out for the years 2018 and 2017 in the following manner:

Liquidity Ratios:

Particulars 2018 2017

Current Assets 158785744 133595101

Current Liabilities 62789472 61056713

Current Ratio 2.53 2.19

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

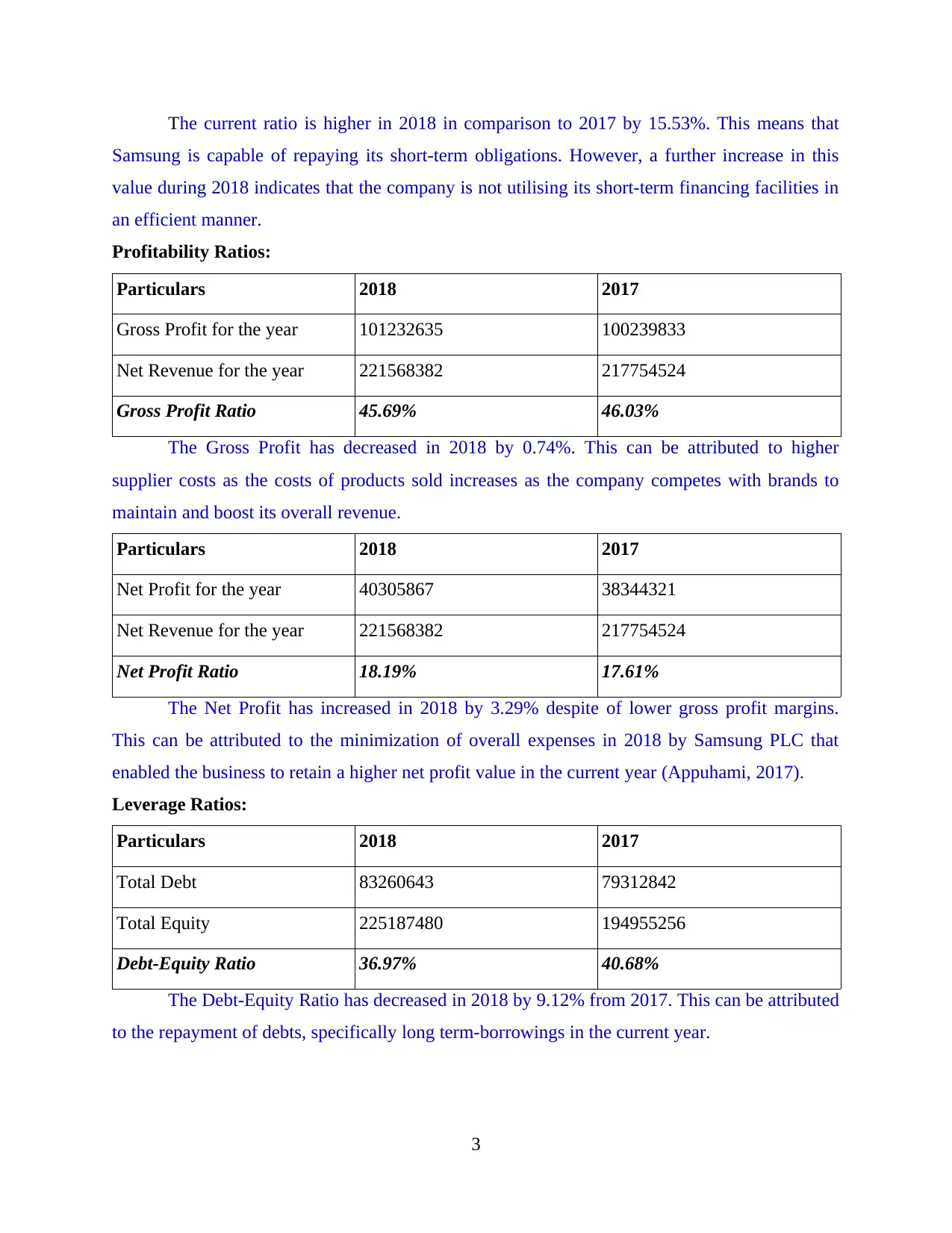

The current ratio is higher in 2018 in comparison to 2017 by 15.53%. This means that

Samsung is capable of repaying its short-term obligations. However, a further increase in this

value during 2018 indicates that the company is not utilising its short-term financing facilities in

an efficient manner.

Profitability Ratios:

Particulars 2018 2017

Gross Profit for the year 101232635 100239833

Net Revenue for the year 221568382 217754524

Gross Profit Ratio 45.69% 46.03%

The Gross Profit has decreased in 2018 by 0.74%. This can be attributed to higher

supplier costs as the costs of products sold increases as the company competes with brands to

maintain and boost its overall revenue.

Particulars 2018 2017

Net Profit for the year 40305867 38344321

Net Revenue for the year 221568382 217754524

Net Profit Ratio 18.19% 17.61%

The Net Profit has increased in 2018 by 3.29% despite of lower gross profit margins.

This can be attributed to the minimization of overall expenses in 2018 by Samsung PLC that

enabled the business to retain a higher net profit value in the current year (Appuhami, 2017).

Leverage Ratios:

Particulars 2018 2017

Total Debt 83260643 79312842

Total Equity 225187480 194955256

Debt-Equity Ratio 36.97% 40.68%

The Debt-Equity Ratio has decreased in 2018 by 9.12% from 2017. This can be attributed

to the repayment of debts, specifically long term-borrowings in the current year.

3

Samsung is capable of repaying its short-term obligations. However, a further increase in this

value during 2018 indicates that the company is not utilising its short-term financing facilities in

an efficient manner.

Profitability Ratios:

Particulars 2018 2017

Gross Profit for the year 101232635 100239833

Net Revenue for the year 221568382 217754524

Gross Profit Ratio 45.69% 46.03%

The Gross Profit has decreased in 2018 by 0.74%. This can be attributed to higher

supplier costs as the costs of products sold increases as the company competes with brands to

maintain and boost its overall revenue.

Particulars 2018 2017

Net Profit for the year 40305867 38344321

Net Revenue for the year 221568382 217754524

Net Profit Ratio 18.19% 17.61%

The Net Profit has increased in 2018 by 3.29% despite of lower gross profit margins.

This can be attributed to the minimization of overall expenses in 2018 by Samsung PLC that

enabled the business to retain a higher net profit value in the current year (Appuhami, 2017).

Leverage Ratios:

Particulars 2018 2017

Total Debt 83260643 79312842

Total Equity 225187480 194955256

Debt-Equity Ratio 36.97% 40.68%

The Debt-Equity Ratio has decreased in 2018 by 9.12% from 2017. This can be attributed

to the repayment of debts, specifically long term-borrowings in the current year.

3

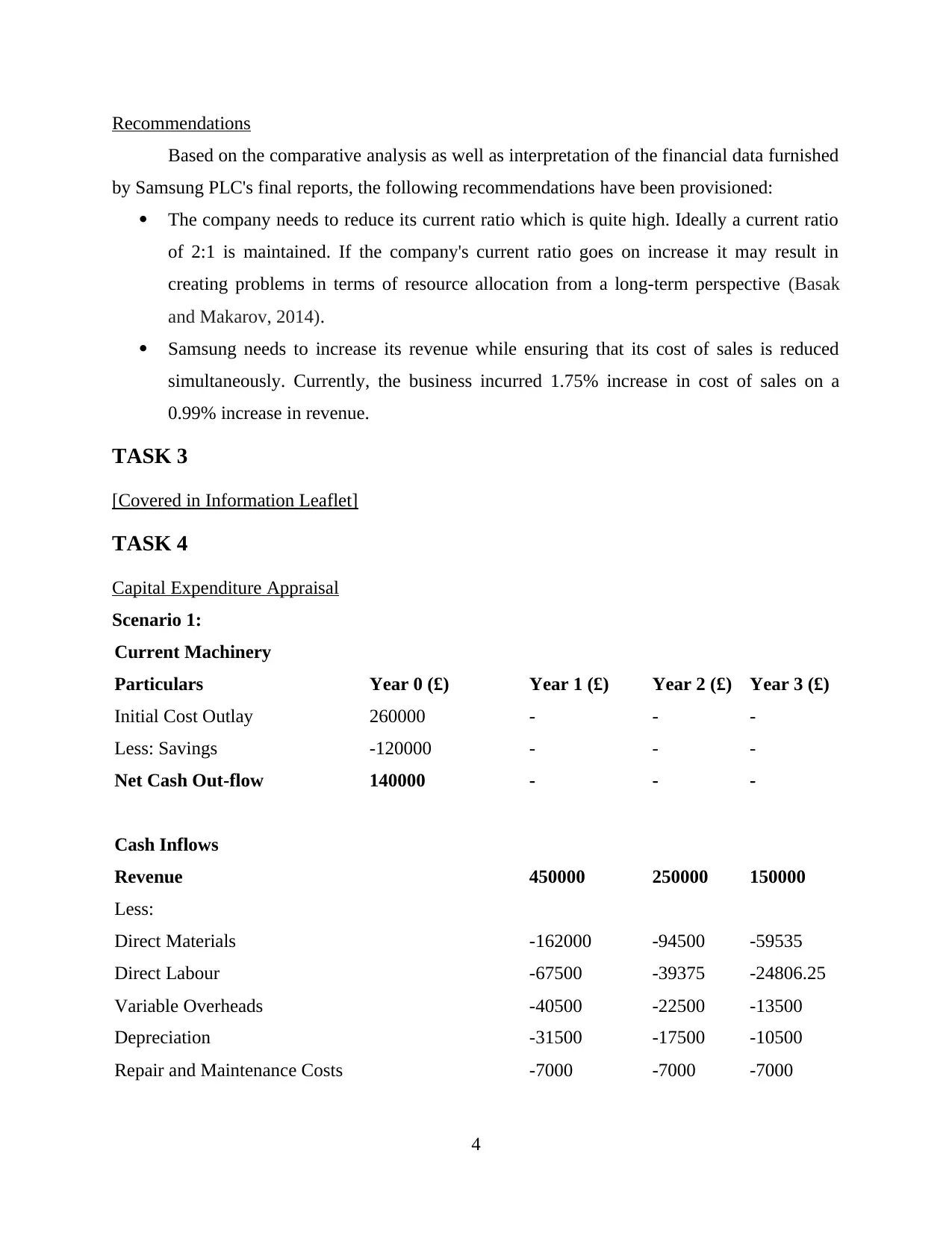

Recommendations

Based on the comparative analysis as well as interpretation of the financial data furnished

by Samsung PLC's final reports, the following recommendations have been provisioned:

The company needs to reduce its current ratio which is quite high. Ideally a current ratio

of 2:1 is maintained. If the company's current ratio goes on increase it may result in

creating problems in terms of resource allocation from a long-term perspective (Basak

and Makarov, 2014).

Samsung needs to increase its revenue while ensuring that its cost of sales is reduced

simultaneously. Currently, the business incurred 1.75% increase in cost of sales on a

0.99% increase in revenue.

TASK 3

[Covered in Information Leaflet]

TASK 4

Capital Expenditure Appraisal

Scenario 1:

Current Machinery

Particulars Year 0 (£) Year 1 (£) Year 2 (£) Year 3 (£)

Initial Cost Outlay 260000 - - -

Less: Savings -120000 - - -

Net Cash Out-flow 140000 - - -

Cash Inflows

Revenue 450000 250000 150000

Less:

Direct Materials -162000 -94500 -59535

Direct Labour -67500 -39375 -24806.25

Variable Overheads -40500 -22500 -13500

Depreciation -31500 -17500 -10500

Repair and Maintenance Costs -7000 -7000 -7000

4

Based on the comparative analysis as well as interpretation of the financial data furnished

by Samsung PLC's final reports, the following recommendations have been provisioned:

The company needs to reduce its current ratio which is quite high. Ideally a current ratio

of 2:1 is maintained. If the company's current ratio goes on increase it may result in

creating problems in terms of resource allocation from a long-term perspective (Basak

and Makarov, 2014).

Samsung needs to increase its revenue while ensuring that its cost of sales is reduced

simultaneously. Currently, the business incurred 1.75% increase in cost of sales on a

0.99% increase in revenue.

TASK 3

[Covered in Information Leaflet]

TASK 4

Capital Expenditure Appraisal

Scenario 1:

Current Machinery

Particulars Year 0 (£) Year 1 (£) Year 2 (£) Year 3 (£)

Initial Cost Outlay 260000 - - -

Less: Savings -120000 - - -

Net Cash Out-flow 140000 - - -

Cash Inflows

Revenue 450000 250000 150000

Less:

Direct Materials -162000 -94500 -59535

Direct Labour -67500 -39375 -24806.25

Variable Overheads -40500 -22500 -13500

Depreciation -31500 -17500 -10500

Repair and Maintenance Costs -7000 -7000 -7000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

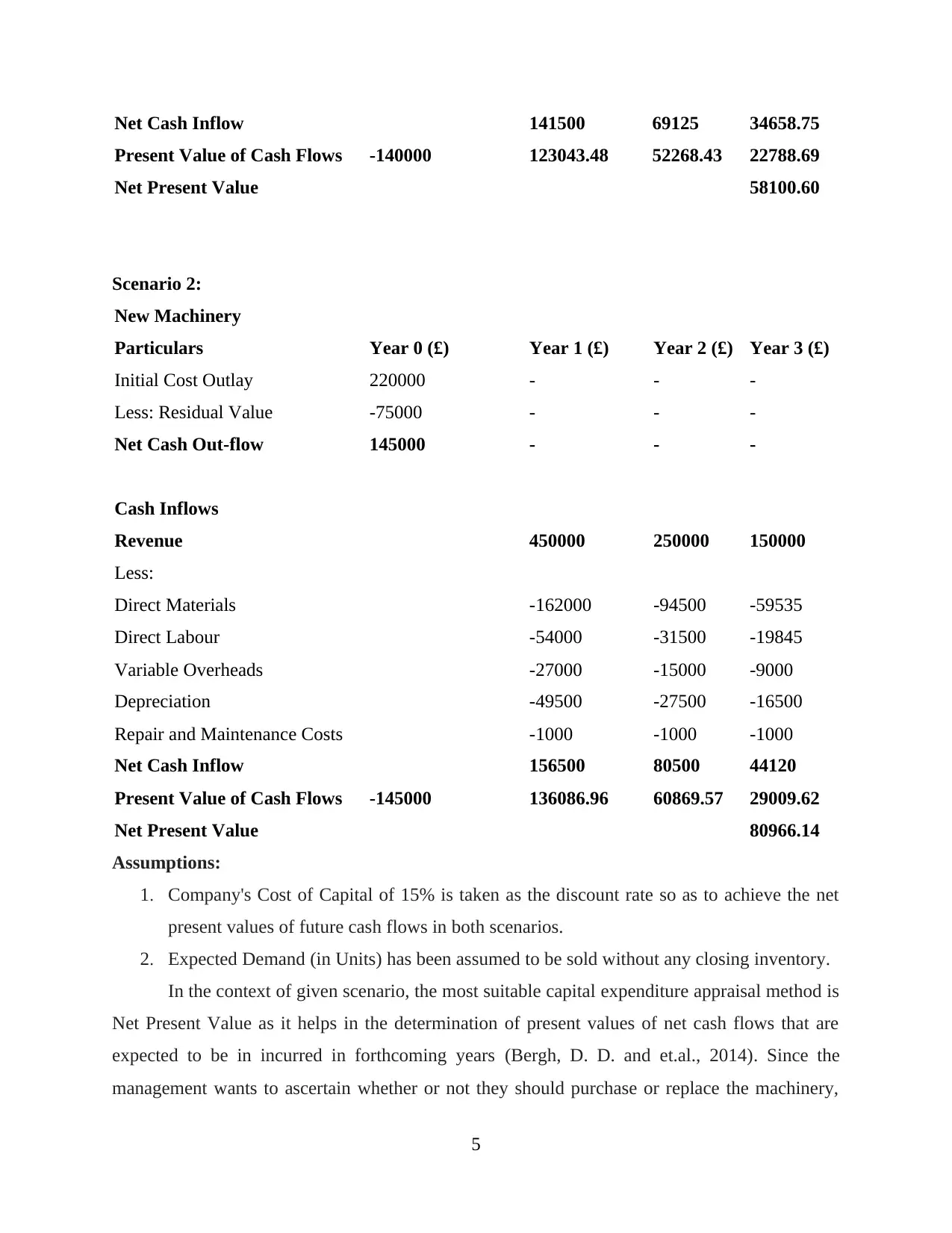

Net Cash Inflow 141500 69125 34658.75

Present Value of Cash Flows -140000 123043.48 52268.43 22788.69

Net Present Value 58100.60

Scenario 2:

New Machinery

Particulars Year 0 (£) Year 1 (£) Year 2 (£) Year 3 (£)

Initial Cost Outlay 220000 - - -

Less: Residual Value -75000 - - -

Net Cash Out-flow 145000 - - -

Cash Inflows

Revenue 450000 250000 150000

Less:

Direct Materials -162000 -94500 -59535

Direct Labour -54000 -31500 -19845

Variable Overheads -27000 -15000 -9000

Depreciation -49500 -27500 -16500

Repair and Maintenance Costs -1000 -1000 -1000

Net Cash Inflow 156500 80500 44120

Present Value of Cash Flows -145000 136086.96 60869.57 29009.62

Net Present Value 80966.14

Assumptions:

1. Company's Cost of Capital of 15% is taken as the discount rate so as to achieve the net

present values of future cash flows in both scenarios.

2. Expected Demand (in Units) has been assumed to be sold without any closing inventory.

In the context of given scenario, the most suitable capital expenditure appraisal method is

Net Present Value as it helps in the determination of present values of net cash flows that are

expected to be in incurred in forthcoming years (Bergh, D. D. and et.al., 2014). Since the

management wants to ascertain whether or not they should purchase or replace the machinery,

5

Present Value of Cash Flows -140000 123043.48 52268.43 22788.69

Net Present Value 58100.60

Scenario 2:

New Machinery

Particulars Year 0 (£) Year 1 (£) Year 2 (£) Year 3 (£)

Initial Cost Outlay 220000 - - -

Less: Residual Value -75000 - - -

Net Cash Out-flow 145000 - - -

Cash Inflows

Revenue 450000 250000 150000

Less:

Direct Materials -162000 -94500 -59535

Direct Labour -54000 -31500 -19845

Variable Overheads -27000 -15000 -9000

Depreciation -49500 -27500 -16500

Repair and Maintenance Costs -1000 -1000 -1000

Net Cash Inflow 156500 80500 44120

Present Value of Cash Flows -145000 136086.96 60869.57 29009.62

Net Present Value 80966.14

Assumptions:

1. Company's Cost of Capital of 15% is taken as the discount rate so as to achieve the net

present values of future cash flows in both scenarios.

2. Expected Demand (in Units) has been assumed to be sold without any closing inventory.

In the context of given scenario, the most suitable capital expenditure appraisal method is

Net Present Value as it helps in the determination of present values of net cash flows that are

expected to be in incurred in forthcoming years (Bergh, D. D. and et.al., 2014). Since the

management wants to ascertain whether or not they should purchase or replace the machinery,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this method would help them in getting a comprehensive breakdown of costs as well as revenue.

Comparing the two scenarios, it is strongly recommended that the management should

immediately purchase the new machinery. The main reason to suggest this solution is that:

Repair and Maintenance costs are substantially minimised;

Savings provide a tax-shield for the company;

NPV for the new machinery worth £80,996.14 is significantly higher than the NPV

ascertained for the current machinery worth £58,100.60 (Chatterji and et.al., 2016).

CONCLUSION

From the given report it can be concluded that finance plays an imperative role in the

process of strategic planning. Thus, enabling strategic managers of various organisations to

ensure that their business is in complete alignment with the internal as well as external

environment. Along with this, it is also observed that financial data and information plays a

crucial role in ascertaining how the business strategy relating to a particular department or

organisation as a whole. This enables the company to ensure that the strategic direction

undertaken by the business is correct or not for its overall success in the forthcoming years.

6

Comparing the two scenarios, it is strongly recommended that the management should

immediately purchase the new machinery. The main reason to suggest this solution is that:

Repair and Maintenance costs are substantially minimised;

Savings provide a tax-shield for the company;

NPV for the new machinery worth £80,996.14 is significantly higher than the NPV

ascertained for the current machinery worth £58,100.60 (Chatterji and et.al., 2016).

CONCLUSION

From the given report it can be concluded that finance plays an imperative role in the

process of strategic planning. Thus, enabling strategic managers of various organisations to

ensure that their business is in complete alignment with the internal as well as external

environment. Along with this, it is also observed that financial data and information plays a

crucial role in ascertaining how the business strategy relating to a particular department or

organisation as a whole. This enables the company to ensure that the strategic direction

undertaken by the business is correct or not for its overall success in the forthcoming years.

6

REFERENCES

Books and Journal

Alkaraan, F., 2015. Strategic Investment Decision-Making Perspectives', Advances in Mergers

and Acquisitions (Advances in Mergers & Acquisitions, Volume 14).

Appuhami, R., 2017. Exploring the relationship between strategic performance measurement

systems and managers' creativity: the mediating role of psychological empowerment

and organisational learning. Accounting & Finance.

Basak, S. and Makarov, D., 2014. Strategic asset allocation in money management. The Journal

of Finance. 69(1). pp.179-217.

Bergh, D. D. and et.al., 2014. Signalling theory and equilibrium in strategic management

research: An assessment and a research agenda. Journal of Management Studies. 51(8).

pp.1334-1360.

Chatterji, A. K. and et.al., 2016. Do ratings of firms converge? Implications for managers,

investors and strategy researchers. Strategic Management Journal. 37(8). pp.1597-1614.

Online

Annual Report. 2018. [Online]. Available Through:

<https://images.samsung.com/is/content/samsung/p5/global/ir/docs/2018_con_quarter0

4_all.pdf>

Sales. 2019. [Online]. Available Through:

<https://news.samsung.com/global/samsung-electronics-announces-fourth-quarter-and-

fy-2018-results>

7

Books and Journal

Alkaraan, F., 2015. Strategic Investment Decision-Making Perspectives', Advances in Mergers

and Acquisitions (Advances in Mergers & Acquisitions, Volume 14).

Appuhami, R., 2017. Exploring the relationship between strategic performance measurement

systems and managers' creativity: the mediating role of psychological empowerment

and organisational learning. Accounting & Finance.

Basak, S. and Makarov, D., 2014. Strategic asset allocation in money management. The Journal

of Finance. 69(1). pp.179-217.

Bergh, D. D. and et.al., 2014. Signalling theory and equilibrium in strategic management

research: An assessment and a research agenda. Journal of Management Studies. 51(8).

pp.1334-1360.

Chatterji, A. K. and et.al., 2016. Do ratings of firms converge? Implications for managers,

investors and strategy researchers. Strategic Management Journal. 37(8). pp.1597-1614.

Online

Annual Report. 2018. [Online]. Available Through:

<https://images.samsung.com/is/content/samsung/p5/global/ir/docs/2018_con_quarter0

4_all.pdf>

Sales. 2019. [Online]. Available Through:

<https://news.samsung.com/global/samsung-electronics-announces-fourth-quarter-and-

fy-2018-results>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

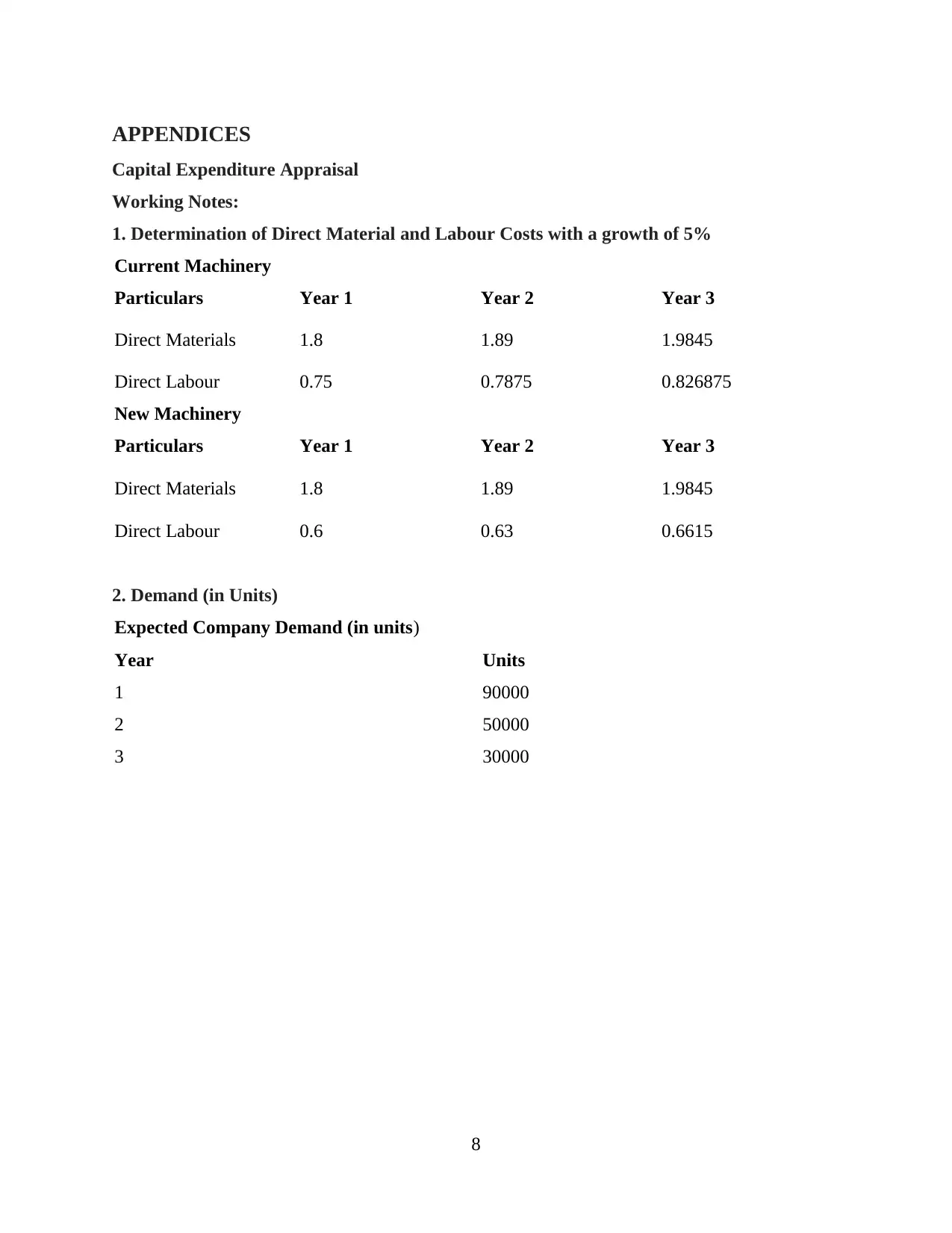

APPENDICES

Capital Expenditure Appraisal

Working Notes:

1. Determination of Direct Material and Labour Costs with a growth of 5%

Current Machinery

Particulars Year 1 Year 2 Year 3

Direct Materials 1.8 1.89 1.9845

Direct Labour 0.75 0.7875 0.826875

New Machinery

Particulars Year 1 Year 2 Year 3

Direct Materials 1.8 1.89 1.9845

Direct Labour 0.6 0.63 0.6615

2. Demand (in Units)

Expected Company Demand (in units)

Year Units

1 90000

2 50000

3 30000

8

Capital Expenditure Appraisal

Working Notes:

1. Determination of Direct Material and Labour Costs with a growth of 5%

Current Machinery

Particulars Year 1 Year 2 Year 3

Direct Materials 1.8 1.89 1.9845

Direct Labour 0.75 0.7875 0.826875

New Machinery

Particulars Year 1 Year 2 Year 3

Direct Materials 1.8 1.89 1.9845

Direct Labour 0.6 0.63 0.6615

2. Demand (in Units)

Expected Company Demand (in units)

Year Units

1 90000

2 50000

3 30000

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.