Corporate Accounting Report: Analysis of Santos Limited's Finances

VerifiedAdded on 2021/05/31

|10

|2628

|23

Report

AI Summary

This report provides a comprehensive analysis of Santos Limited's financial performance, focusing on its cash flow statement, other comprehensive income (OCI), and accounting for corporate income tax. The cash flow analysis reveals an increase in customer receipts, minimal rise in supplier and employee payments, and investments in new oil and gas assets. The OCI section explains items like exchange gains/losses, foreign currency loans, and hedges. The corporate income tax section explores the company's tax benefit, temporary differences, deferred tax assets and liabilities, and the difference between income tax expense and payable. The report highlights trends, provides explanations for financial items, and discusses the complexities of tax rules and accounting treatments. The student has used various financial accounting concepts to analyze the financial performance of the company.

CORPORATE ACCOUNTING

SANTOS LIMITED

STUDENT ID:

[Pick the date]

SANTOS LIMITED

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The selected firm for this task is Santos Limited which is primarily an energy company. The

relevant analysis required is carried out below (Demello, 2005).

CASH FLOW STATEMENT

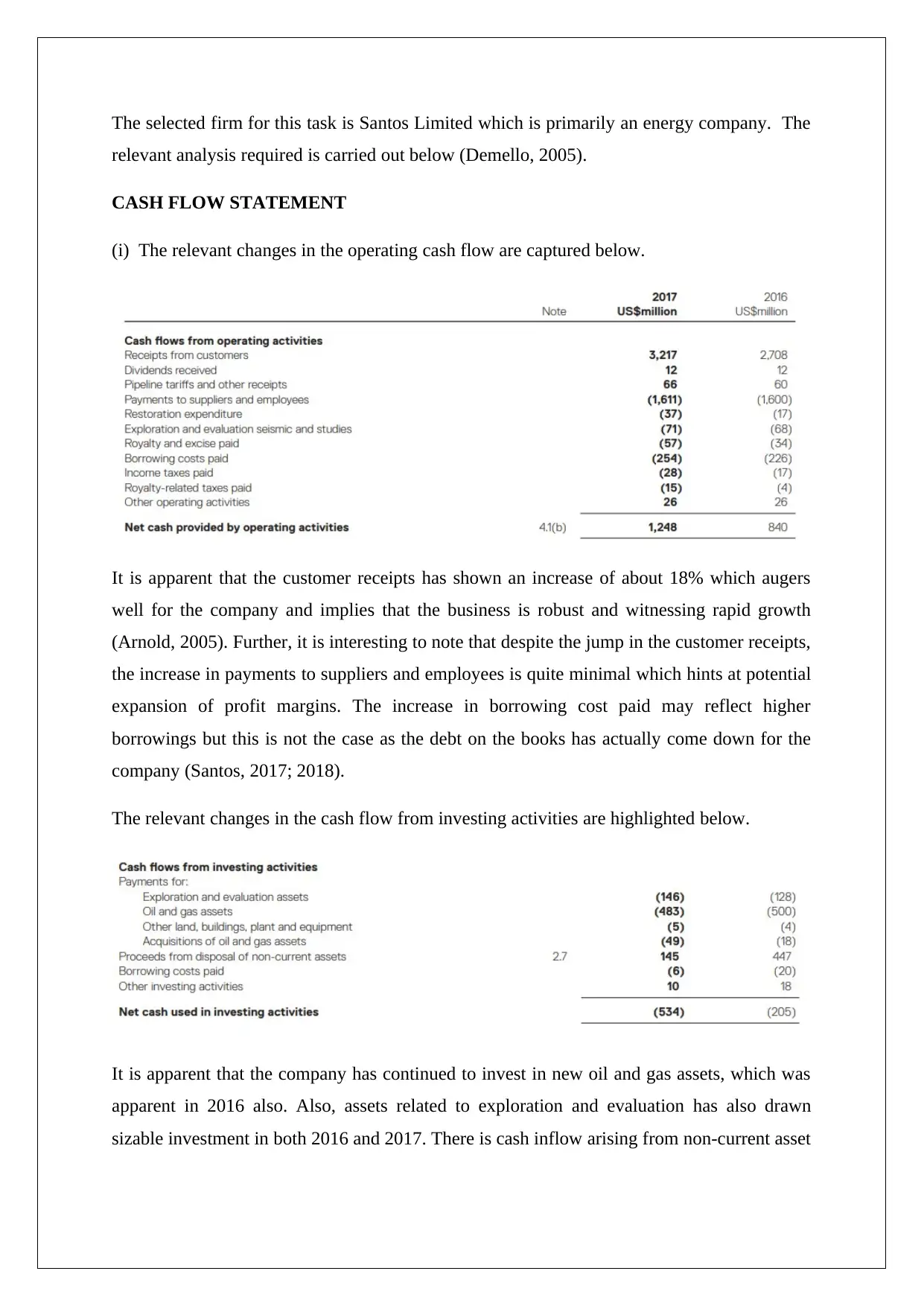

(i) The relevant changes in the operating cash flow are captured below.

It is apparent that the customer receipts has shown an increase of about 18% which augers

well for the company and implies that the business is robust and witnessing rapid growth

(Arnold, 2005). Further, it is interesting to note that despite the jump in the customer receipts,

the increase in payments to suppliers and employees is quite minimal which hints at potential

expansion of profit margins. The increase in borrowing cost paid may reflect higher

borrowings but this is not the case as the debt on the books has actually come down for the

company (Santos, 2017; 2018).

The relevant changes in the cash flow from investing activities are highlighted below.

It is apparent that the company has continued to invest in new oil and gas assets, which was

apparent in 2016 also. Also, assets related to exploration and evaluation has also drawn

sizable investment in both 2016 and 2017. There is cash inflow arising from non-current asset

relevant analysis required is carried out below (Demello, 2005).

CASH FLOW STATEMENT

(i) The relevant changes in the operating cash flow are captured below.

It is apparent that the customer receipts has shown an increase of about 18% which augers

well for the company and implies that the business is robust and witnessing rapid growth

(Arnold, 2005). Further, it is interesting to note that despite the jump in the customer receipts,

the increase in payments to suppliers and employees is quite minimal which hints at potential

expansion of profit margins. The increase in borrowing cost paid may reflect higher

borrowings but this is not the case as the debt on the books has actually come down for the

company (Santos, 2017; 2018).

The relevant changes in the cash flow from investing activities are highlighted below.

It is apparent that the company has continued to invest in new oil and gas assets, which was

apparent in 2016 also. Also, assets related to exploration and evaluation has also drawn

sizable investment in both 2016 and 2017. There is cash inflow arising from non-current asset

disposal but it is significantly lesser in 2017 as compared to the corresponding figure in 2016

(Santos, 2017; 2018).

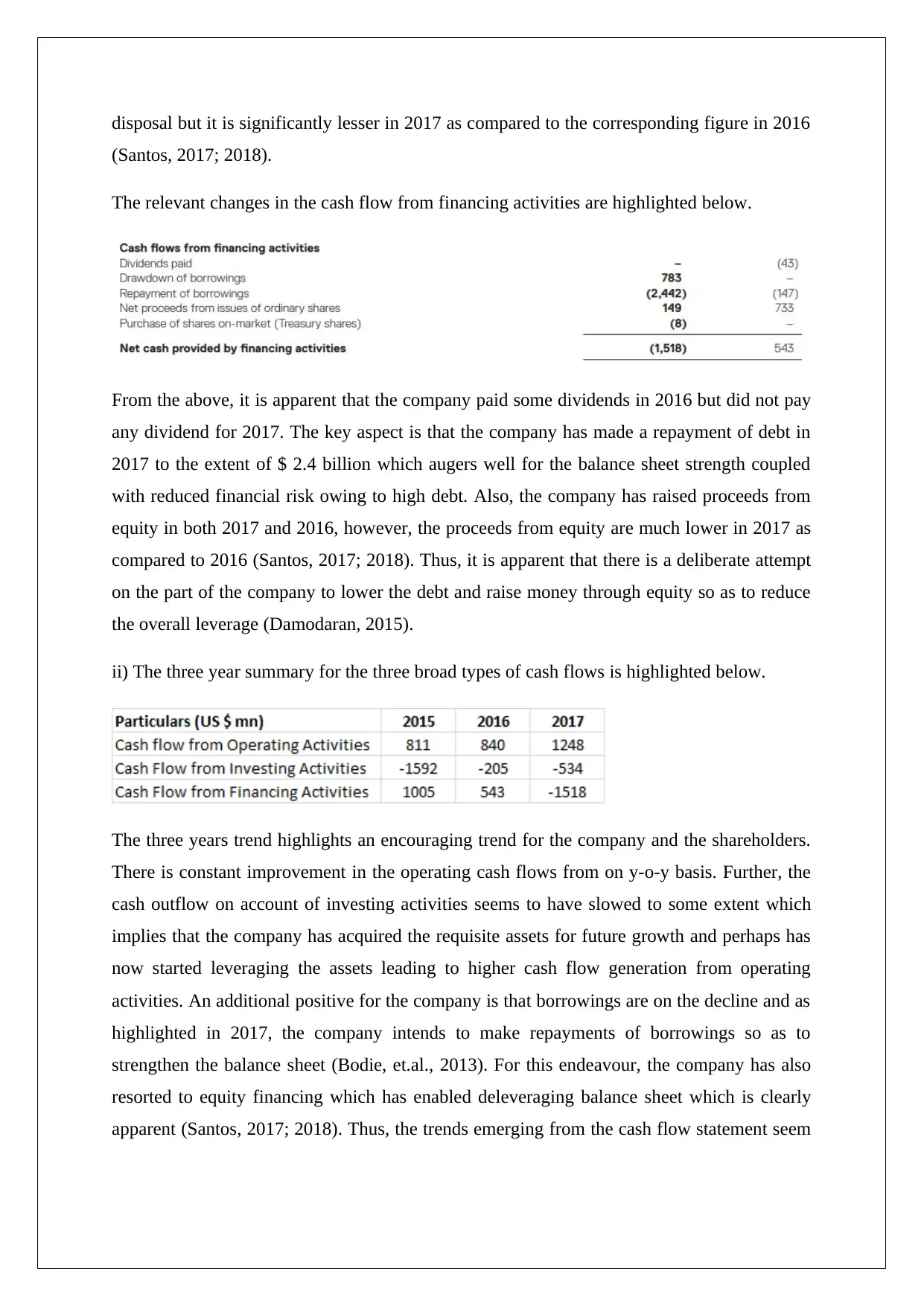

The relevant changes in the cash flow from financing activities are highlighted below.

From the above, it is apparent that the company paid some dividends in 2016 but did not pay

any dividend for 2017. The key aspect is that the company has made a repayment of debt in

2017 to the extent of $ 2.4 billion which augers well for the balance sheet strength coupled

with reduced financial risk owing to high debt. Also, the company has raised proceeds from

equity in both 2017 and 2016, however, the proceeds from equity are much lower in 2017 as

compared to 2016 (Santos, 2017; 2018). Thus, it is apparent that there is a deliberate attempt

on the part of the company to lower the debt and raise money through equity so as to reduce

the overall leverage (Damodaran, 2015).

ii) The three year summary for the three broad types of cash flows is highlighted below.

The three years trend highlights an encouraging trend for the company and the shareholders.

There is constant improvement in the operating cash flows from on y-o-y basis. Further, the

cash outflow on account of investing activities seems to have slowed to some extent which

implies that the company has acquired the requisite assets for future growth and perhaps has

now started leveraging the assets leading to higher cash flow generation from operating

activities. An additional positive for the company is that borrowings are on the decline and as

highlighted in 2017, the company intends to make repayments of borrowings so as to

strengthen the balance sheet (Bodie, et.al., 2013). For this endeavour, the company has also

resorted to equity financing which has enabled deleveraging balance sheet which is clearly

apparent (Santos, 2017; 2018). Thus, the trends emerging from the cash flow statement seem

(Santos, 2017; 2018).

The relevant changes in the cash flow from financing activities are highlighted below.

From the above, it is apparent that the company paid some dividends in 2016 but did not pay

any dividend for 2017. The key aspect is that the company has made a repayment of debt in

2017 to the extent of $ 2.4 billion which augers well for the balance sheet strength coupled

with reduced financial risk owing to high debt. Also, the company has raised proceeds from

equity in both 2017 and 2016, however, the proceeds from equity are much lower in 2017 as

compared to 2016 (Santos, 2017; 2018). Thus, it is apparent that there is a deliberate attempt

on the part of the company to lower the debt and raise money through equity so as to reduce

the overall leverage (Damodaran, 2015).

ii) The three year summary for the three broad types of cash flows is highlighted below.

The three years trend highlights an encouraging trend for the company and the shareholders.

There is constant improvement in the operating cash flows from on y-o-y basis. Further, the

cash outflow on account of investing activities seems to have slowed to some extent which

implies that the company has acquired the requisite assets for future growth and perhaps has

now started leveraging the assets leading to higher cash flow generation from operating

activities. An additional positive for the company is that borrowings are on the decline and as

highlighted in 2017, the company intends to make repayments of borrowings so as to

strengthen the balance sheet (Bodie, et.al., 2013). For this endeavour, the company has also

resorted to equity financing which has enabled deleveraging balance sheet which is clearly

apparent (Santos, 2017; 2018). Thus, the trends emerging from the cash flow statement seem

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to be quite encouraging and indicate better days for the investors in the future (Northington,

2015).

OTHER COMPREHENSIVE INCOME STATEMENT

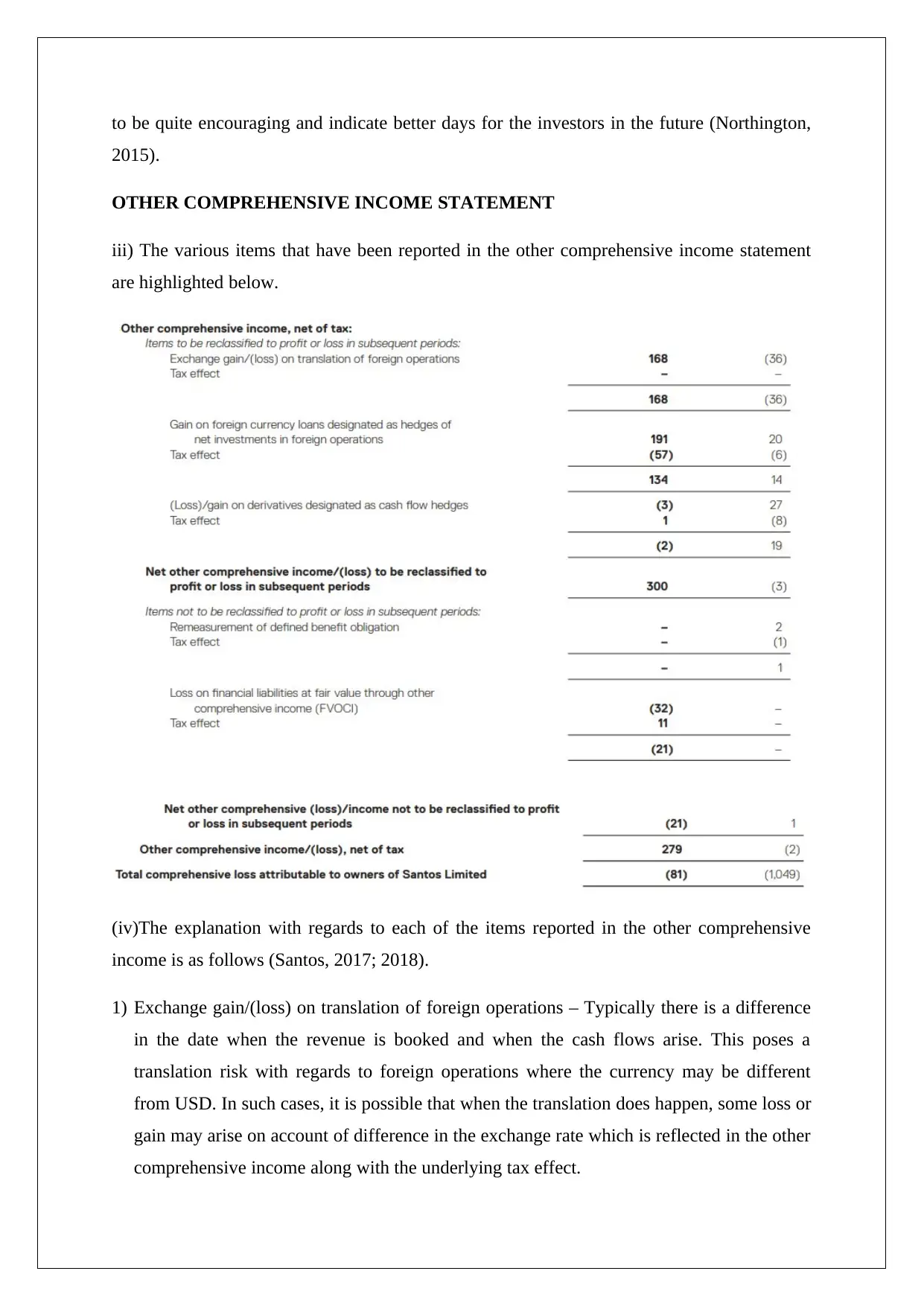

iii) The various items that have been reported in the other comprehensive income statement

are highlighted below.

(iv)The explanation with regards to each of the items reported in the other comprehensive

income is as follows (Santos, 2017; 2018).

1) Exchange gain/(loss) on translation of foreign operations – Typically there is a difference

in the date when the revenue is booked and when the cash flows arise. This poses a

translation risk with regards to foreign operations where the currency may be different

from USD. In such cases, it is possible that when the translation does happen, some loss or

gain may arise on account of difference in the exchange rate which is reflected in the other

comprehensive income along with the underlying tax effect.

2015).

OTHER COMPREHENSIVE INCOME STATEMENT

iii) The various items that have been reported in the other comprehensive income statement

are highlighted below.

(iv)The explanation with regards to each of the items reported in the other comprehensive

income is as follows (Santos, 2017; 2018).

1) Exchange gain/(loss) on translation of foreign operations – Typically there is a difference

in the date when the revenue is booked and when the cash flows arise. This poses a

translation risk with regards to foreign operations where the currency may be different

from USD. In such cases, it is possible that when the translation does happen, some loss or

gain may arise on account of difference in the exchange rate which is reflected in the other

comprehensive income along with the underlying tax effect.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2) Foreign Currency loans related gain/(loss) – Owing to presence of foreign operations, the

company take loans in foreign currency which acts as a hedge against these foreign

operations. This is because the interest and principal repayment need to be done in the

foreign currency and hence part of the cash inflows generated from the foreign operations

could be used for the same. However, owing to favourable or unfavourable movement of

the foreign currency with USD, gain or loss may be realised which is captured along with

the underlying tax effect (Arnold, 2005).

3) (Loss)/gain arising from foreign currency hedges – In order to reduce the foreign currency

related translation risk, the company has put in place, the hedges related to foreign

currency. The value of these hedges keeps on changing and thereby the difference in the

value on the starting date of the year and the ending date of the year needs to be recorded

so that any mark to market profits/(losses) may be booked. Additionally, the tax effect of

this revaluation is also considered (Berk, et.al., 2013).

4) Additionally reclassification of various liabilities which would not be recognised as

profit/loss in subsequent periods is also represented in OCI or other comprehensive

income.

v) The above items are captured in the form of other comprehensive income as these profits

or losses are not related to the core operations of the company and also tend to very volatile.

Consider for instance, the gains or losses made on foreign currency hedges or foreign

currency loans (Berk, et.al., 2013). There is no definite pattern for these and these tend to

highly volatile, thereby making them difficult to predict in advance. Earlier the items under

OCI were recognised in the balance sheet under the equity section. However, changes to

financial accounting norms in the recent years has implied that reporting entities are required

to report the same along with the income statement in the form of comprehensive income

(Petty et. al., 2015). OCI can be extremely helpful in understanding the changes in the market

value of various assets and liabilities especially related to financial assets. Reporting these

items in the profit and loss would not be appropriate as these do not indicate the profit or loss

generated from the operating activities of the company. Also, the intention of these is not to

earn profits but rather to reduce operational risk or these are part of normal business practices

(Parrino and Kidwell, 2014).

ACCOUNTING FOR CORPORATE INCOME TAX

company take loans in foreign currency which acts as a hedge against these foreign

operations. This is because the interest and principal repayment need to be done in the

foreign currency and hence part of the cash inflows generated from the foreign operations

could be used for the same. However, owing to favourable or unfavourable movement of

the foreign currency with USD, gain or loss may be realised which is captured along with

the underlying tax effect (Arnold, 2005).

3) (Loss)/gain arising from foreign currency hedges – In order to reduce the foreign currency

related translation risk, the company has put in place, the hedges related to foreign

currency. The value of these hedges keeps on changing and thereby the difference in the

value on the starting date of the year and the ending date of the year needs to be recorded

so that any mark to market profits/(losses) may be booked. Additionally, the tax effect of

this revaluation is also considered (Berk, et.al., 2013).

4) Additionally reclassification of various liabilities which would not be recognised as

profit/loss in subsequent periods is also represented in OCI or other comprehensive

income.

v) The above items are captured in the form of other comprehensive income as these profits

or losses are not related to the core operations of the company and also tend to very volatile.

Consider for instance, the gains or losses made on foreign currency hedges or foreign

currency loans (Berk, et.al., 2013). There is no definite pattern for these and these tend to

highly volatile, thereby making them difficult to predict in advance. Earlier the items under

OCI were recognised in the balance sheet under the equity section. However, changes to

financial accounting norms in the recent years has implied that reporting entities are required

to report the same along with the income statement in the form of comprehensive income

(Petty et. al., 2015). OCI can be extremely helpful in understanding the changes in the market

value of various assets and liabilities especially related to financial assets. Reporting these

items in the profit and loss would not be appropriate as these do not indicate the profit or loss

generated from the operating activities of the company. Also, the intention of these is not to

earn profits but rather to reduce operational risk or these are part of normal business practices

(Parrino and Kidwell, 2014).

ACCOUNTING FOR CORPORATE INCOME TAX

(vi)The firm tax expense can be extracted from the income statement pertaining to FY2017

ending on December 31, 2017. Considering that the firm had posted an pre-tax loss for the

year FY2017, hence instead of tax expense, the company has obtained tax benefit to the

extent of US$ 225 million (Santos, 2017; 2018).

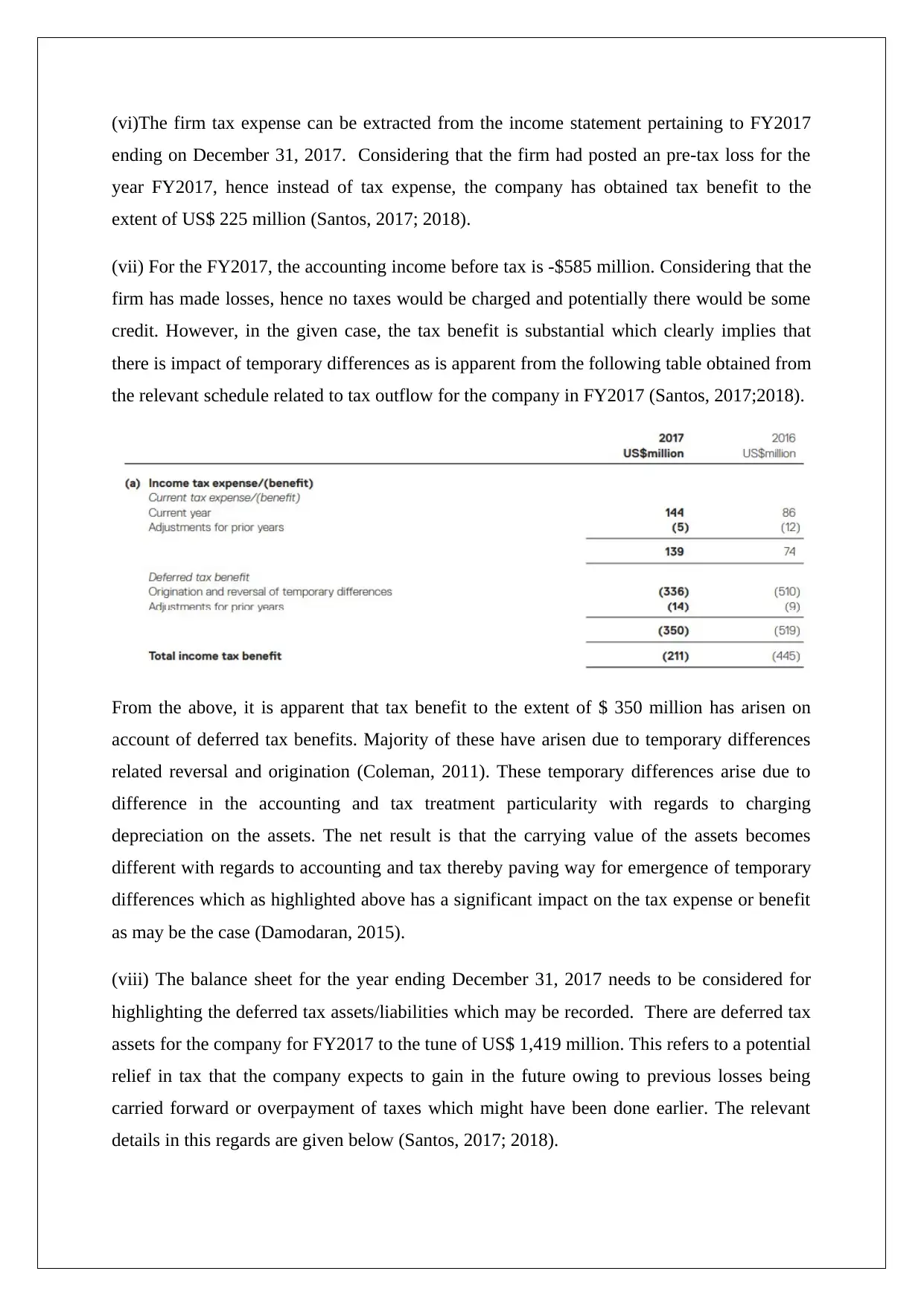

(vii) For the FY2017, the accounting income before tax is -$585 million. Considering that the

firm has made losses, hence no taxes would be charged and potentially there would be some

credit. However, in the given case, the tax benefit is substantial which clearly implies that

there is impact of temporary differences as is apparent from the following table obtained from

the relevant schedule related to tax outflow for the company in FY2017 (Santos, 2017;2018).

From the above, it is apparent that tax benefit to the extent of $ 350 million has arisen on

account of deferred tax benefits. Majority of these have arisen due to temporary differences

related reversal and origination (Coleman, 2011). These temporary differences arise due to

difference in the accounting and tax treatment particularity with regards to charging

depreciation on the assets. The net result is that the carrying value of the assets becomes

different with regards to accounting and tax thereby paving way for emergence of temporary

differences which as highlighted above has a significant impact on the tax expense or benefit

as may be the case (Damodaran, 2015).

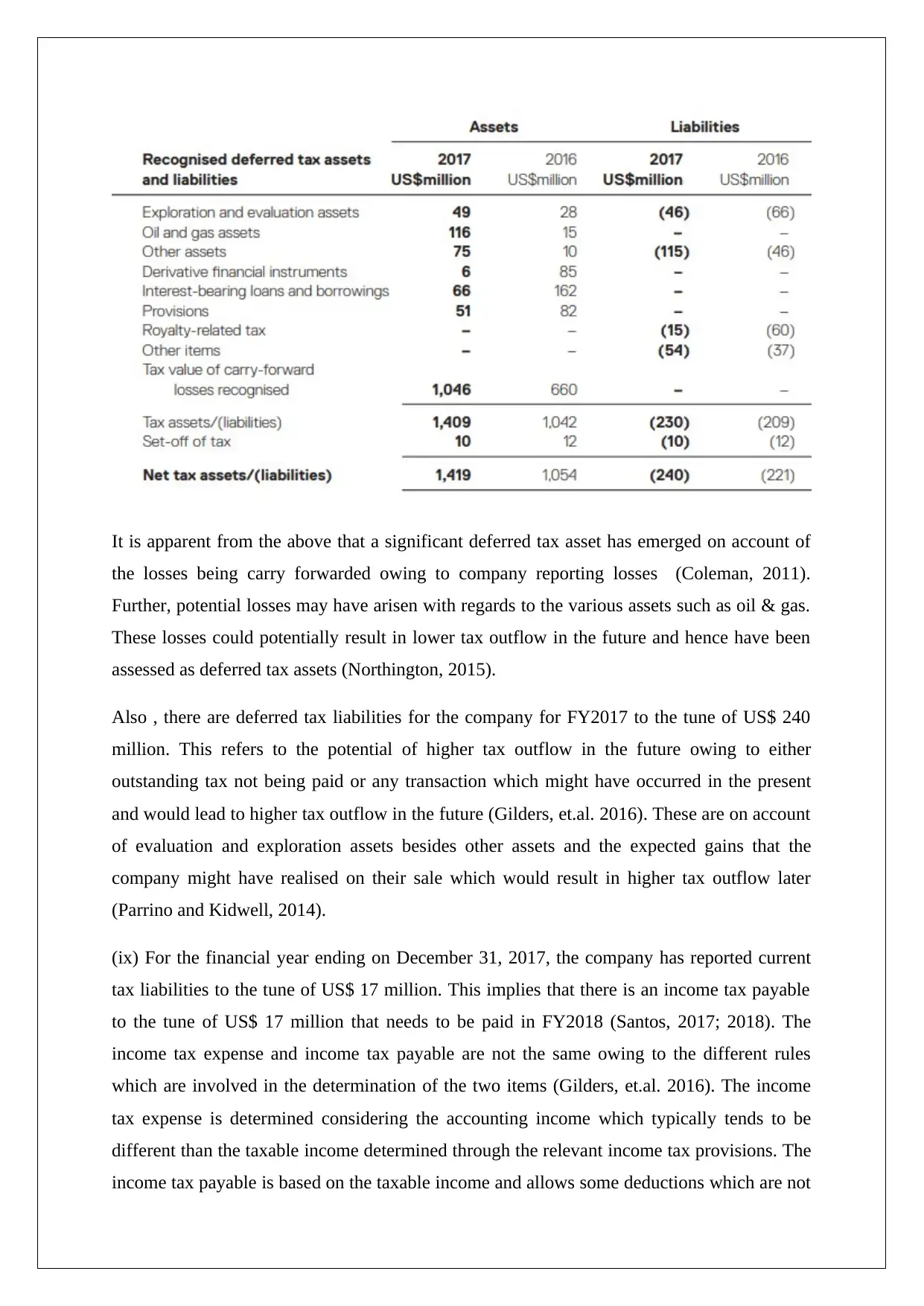

(viii) The balance sheet for the year ending December 31, 2017 needs to be considered for

highlighting the deferred tax assets/liabilities which may be recorded. There are deferred tax

assets for the company for FY2017 to the tune of US$ 1,419 million. This refers to a potential

relief in tax that the company expects to gain in the future owing to previous losses being

carried forward or overpayment of taxes which might have been done earlier. The relevant

details in this regards are given below (Santos, 2017; 2018).

ending on December 31, 2017. Considering that the firm had posted an pre-tax loss for the

year FY2017, hence instead of tax expense, the company has obtained tax benefit to the

extent of US$ 225 million (Santos, 2017; 2018).

(vii) For the FY2017, the accounting income before tax is -$585 million. Considering that the

firm has made losses, hence no taxes would be charged and potentially there would be some

credit. However, in the given case, the tax benefit is substantial which clearly implies that

there is impact of temporary differences as is apparent from the following table obtained from

the relevant schedule related to tax outflow for the company in FY2017 (Santos, 2017;2018).

From the above, it is apparent that tax benefit to the extent of $ 350 million has arisen on

account of deferred tax benefits. Majority of these have arisen due to temporary differences

related reversal and origination (Coleman, 2011). These temporary differences arise due to

difference in the accounting and tax treatment particularity with regards to charging

depreciation on the assets. The net result is that the carrying value of the assets becomes

different with regards to accounting and tax thereby paving way for emergence of temporary

differences which as highlighted above has a significant impact on the tax expense or benefit

as may be the case (Damodaran, 2015).

(viii) The balance sheet for the year ending December 31, 2017 needs to be considered for

highlighting the deferred tax assets/liabilities which may be recorded. There are deferred tax

assets for the company for FY2017 to the tune of US$ 1,419 million. This refers to a potential

relief in tax that the company expects to gain in the future owing to previous losses being

carried forward or overpayment of taxes which might have been done earlier. The relevant

details in this regards are given below (Santos, 2017; 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is apparent from the above that a significant deferred tax asset has emerged on account of

the losses being carry forwarded owing to company reporting losses (Coleman, 2011).

Further, potential losses may have arisen with regards to the various assets such as oil & gas.

These losses could potentially result in lower tax outflow in the future and hence have been

assessed as deferred tax assets (Northington, 2015).

Also , there are deferred tax liabilities for the company for FY2017 to the tune of US$ 240

million. This refers to the potential of higher tax outflow in the future owing to either

outstanding tax not being paid or any transaction which might have occurred in the present

and would lead to higher tax outflow in the future (Gilders, et.al. 2016). These are on account

of evaluation and exploration assets besides other assets and the expected gains that the

company might have realised on their sale which would result in higher tax outflow later

(Parrino and Kidwell, 2014).

(ix) For the financial year ending on December 31, 2017, the company has reported current

tax liabilities to the tune of US$ 17 million. This implies that there is an income tax payable

to the tune of US$ 17 million that needs to be paid in FY2018 (Santos, 2017; 2018). The

income tax expense and income tax payable are not the same owing to the different rules

which are involved in the determination of the two items (Gilders, et.al. 2016). The income

tax expense is determined considering the accounting income which typically tends to be

different than the taxable income determined through the relevant income tax provisions. The

income tax payable is based on the taxable income and allows some deductions which are not

the losses being carry forwarded owing to company reporting losses (Coleman, 2011).

Further, potential losses may have arisen with regards to the various assets such as oil & gas.

These losses could potentially result in lower tax outflow in the future and hence have been

assessed as deferred tax assets (Northington, 2015).

Also , there are deferred tax liabilities for the company for FY2017 to the tune of US$ 240

million. This refers to the potential of higher tax outflow in the future owing to either

outstanding tax not being paid or any transaction which might have occurred in the present

and would lead to higher tax outflow in the future (Gilders, et.al. 2016). These are on account

of evaluation and exploration assets besides other assets and the expected gains that the

company might have realised on their sale which would result in higher tax outflow later

(Parrino and Kidwell, 2014).

(ix) For the financial year ending on December 31, 2017, the company has reported current

tax liabilities to the tune of US$ 17 million. This implies that there is an income tax payable

to the tune of US$ 17 million that needs to be paid in FY2018 (Santos, 2017; 2018). The

income tax expense and income tax payable are not the same owing to the different rules

which are involved in the determination of the two items (Gilders, et.al. 2016). The income

tax expense is determined considering the accounting income which typically tends to be

different than the taxable income determined through the relevant income tax provisions. The

income tax payable is based on the taxable income and allows some deductions which are not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

allowed in computation of profit before tax. The difference between the profit before tax and

taxable income lead to the difference between tax expense and tax payable (Brealey, Myers

and Allen, 2014).

(x) No, the income tax benefit recognised in the income statement is not the same as that

indicated in the cash flow statement. The key reason for this difference is the fact that the

income statement is prepared on accrual basis so the tax expense is realised completed in the

income statement irrespective of it being paid or not. However, the cash flow highlights the

actual income tax related outflow has occurred and thereby records transactions based on the

cash basis. An additional reason for the difference is on account of income tax paid being

linked to tax payable rather than income tax expense (Petty et. al., 2015).

(xi) In theory, tax seems a quite straight forward affair which is applied at a particular rate on

the pre-tax profits. However, in reality, determining the taxable income and hence income tax

payable is quite complex owing to the tax rules that are applicable which are comparatively

more complex (Deutsch, et. al., 2015). Further, the most interesting aspect which I found was

the reconciliation between the accounting and tax treatment which is captured in the financial

statements through the use of various assets and liabilities along with adjustments based on

temporary difference. This was quite fascinating but simultaneously challenging considering

the wide scope of the same (Barkoczy, 2017).

taxable income lead to the difference between tax expense and tax payable (Brealey, Myers

and Allen, 2014).

(x) No, the income tax benefit recognised in the income statement is not the same as that

indicated in the cash flow statement. The key reason for this difference is the fact that the

income statement is prepared on accrual basis so the tax expense is realised completed in the

income statement irrespective of it being paid or not. However, the cash flow highlights the

actual income tax related outflow has occurred and thereby records transactions based on the

cash basis. An additional reason for the difference is on account of income tax paid being

linked to tax payable rather than income tax expense (Petty et. al., 2015).

(xi) In theory, tax seems a quite straight forward affair which is applied at a particular rate on

the pre-tax profits. However, in reality, determining the taxable income and hence income tax

payable is quite complex owing to the tax rules that are applicable which are comparatively

more complex (Deutsch, et. al., 2015). Further, the most interesting aspect which I found was

the reconciliation between the accounting and tax treatment which is captured in the financial

statements through the use of various assets and liabilities along with adjustments based on

temporary difference. This was quite fascinating but simultaneously challenging considering

the wide scope of the same (Barkoczy, 2017).

References

Arnold, G. (2005) Corporate Financial Management. 3rd edn. Sydney: Financial Times

Management.

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd edn. Sydney: Oxford

University Press Australia.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. and Finch, N. (2013) Fundamentals

of corporate finance. London: Pearson Higher Education AU.

Bodie, Z., Merton, R. C., and Cleeton, D. L. (2009). Financial economics (2nd ed.). New

Delhi: Pearson Education India.

Brealey, R. A., Myers, S. C., and Allen, F. (2014) Principles of corporate finance, 2nd ed.

New York: McGraw-Hill Inc.

Coleman, C. (2011) Australian Tax Analysis. 4th edn. Sydney: Thomson Reuters

(Professional) Australia.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Demello, J., (2005) Cases in Finance. 2nd edn. New York City: McGraw-Hill.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax

handbook. 8th edn. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016. 9th edn. Sydney: LexisNexis/Butterworths.

Northington, S. (2015) Finance, 4th ed. New York: Ferguson

Parrino, R. and Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H.

(2015). Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education,

French Forest Australia.

Arnold, G. (2005) Corporate Financial Management. 3rd edn. Sydney: Financial Times

Management.

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd edn. Sydney: Oxford

University Press Australia.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. and Finch, N. (2013) Fundamentals

of corporate finance. London: Pearson Higher Education AU.

Bodie, Z., Merton, R. C., and Cleeton, D. L. (2009). Financial economics (2nd ed.). New

Delhi: Pearson Education India.

Brealey, R. A., Myers, S. C., and Allen, F. (2014) Principles of corporate finance, 2nd ed.

New York: McGraw-Hill Inc.

Coleman, C. (2011) Australian Tax Analysis. 4th edn. Sydney: Thomson Reuters

(Professional) Australia.

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Demello, J., (2005) Cases in Finance. 2nd edn. New York City: McGraw-Hill.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax

handbook. 8th edn. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016. 9th edn. Sydney: LexisNexis/Butterworths.

Northington, S. (2015) Finance, 4th ed. New York: Ferguson

Parrino, R. and Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H.

(2015). Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education,

French Forest Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Santos (2017) Annual Report 2016, [online] Available at

https://www.santos.com/media/3525/san675_annualreport2016_fa3_low-res_.pdf [Accessed

May 16, 2018]

Santos (2018) Annual Report 2017, [online] Available at

https://www.santos.com/media/4319/2017-annual-report.pdf [Accessed May 16, 2018]

https://www.santos.com/media/3525/san675_annualreport2016_fa3_low-res_.pdf [Accessed

May 16, 2018]

Santos (2018) Annual Report 2017, [online] Available at

https://www.santos.com/media/4319/2017-annual-report.pdf [Accessed May 16, 2018]

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.