Corporate Accounting Analysis of Santos Limited: Financial Report

VerifiedAdded on 2021/06/14

|9

|2177

|38

Report

AI Summary

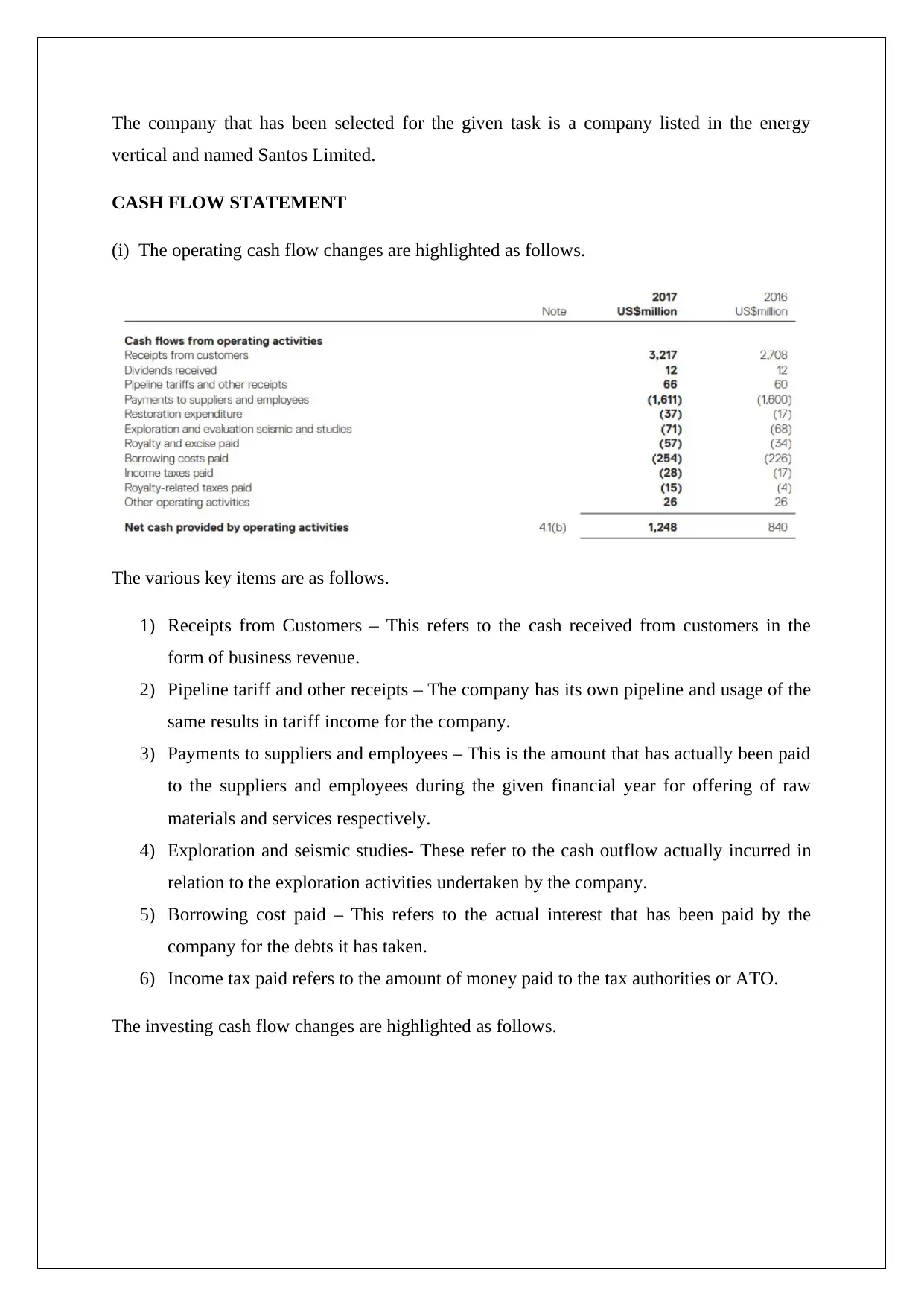

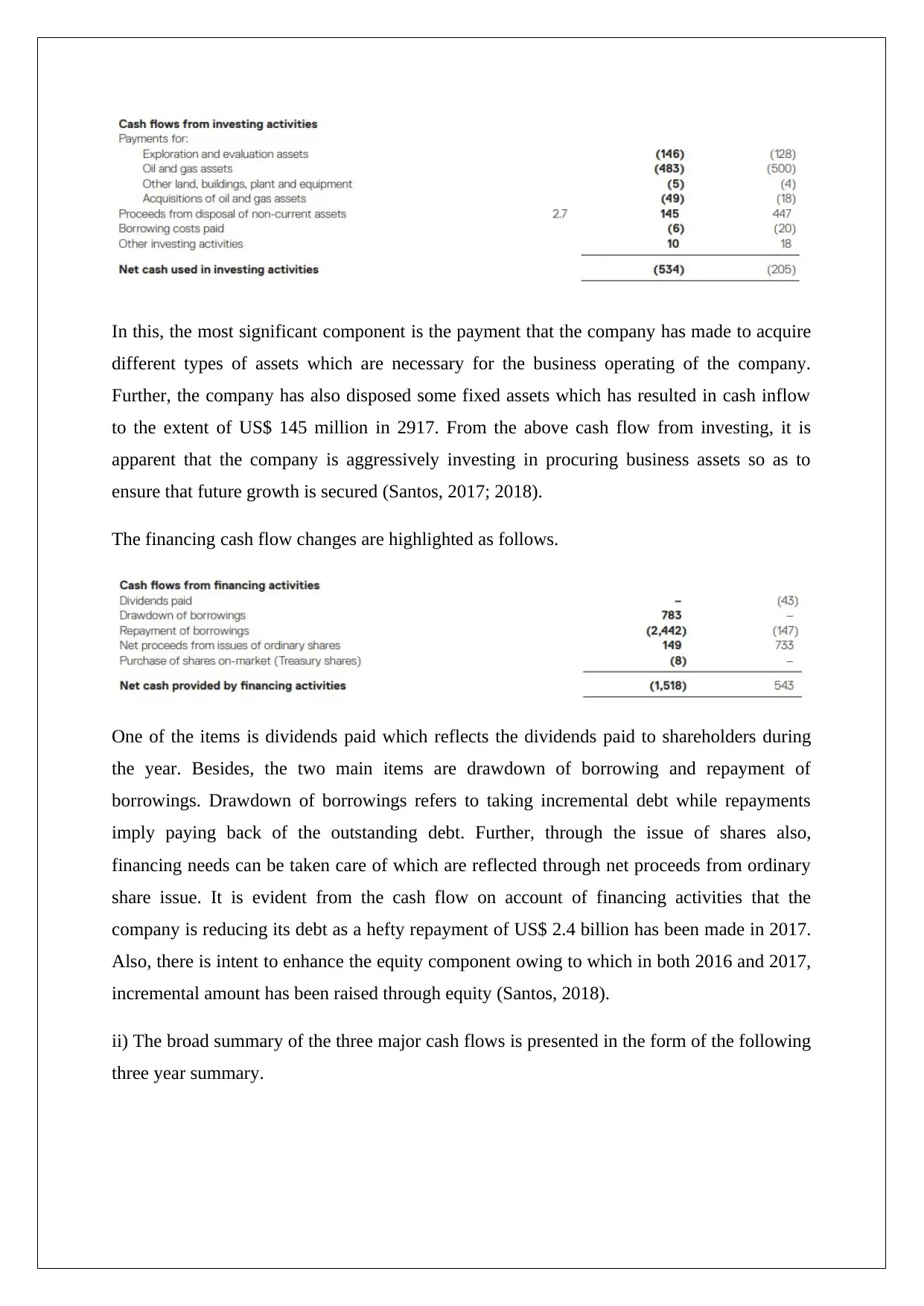

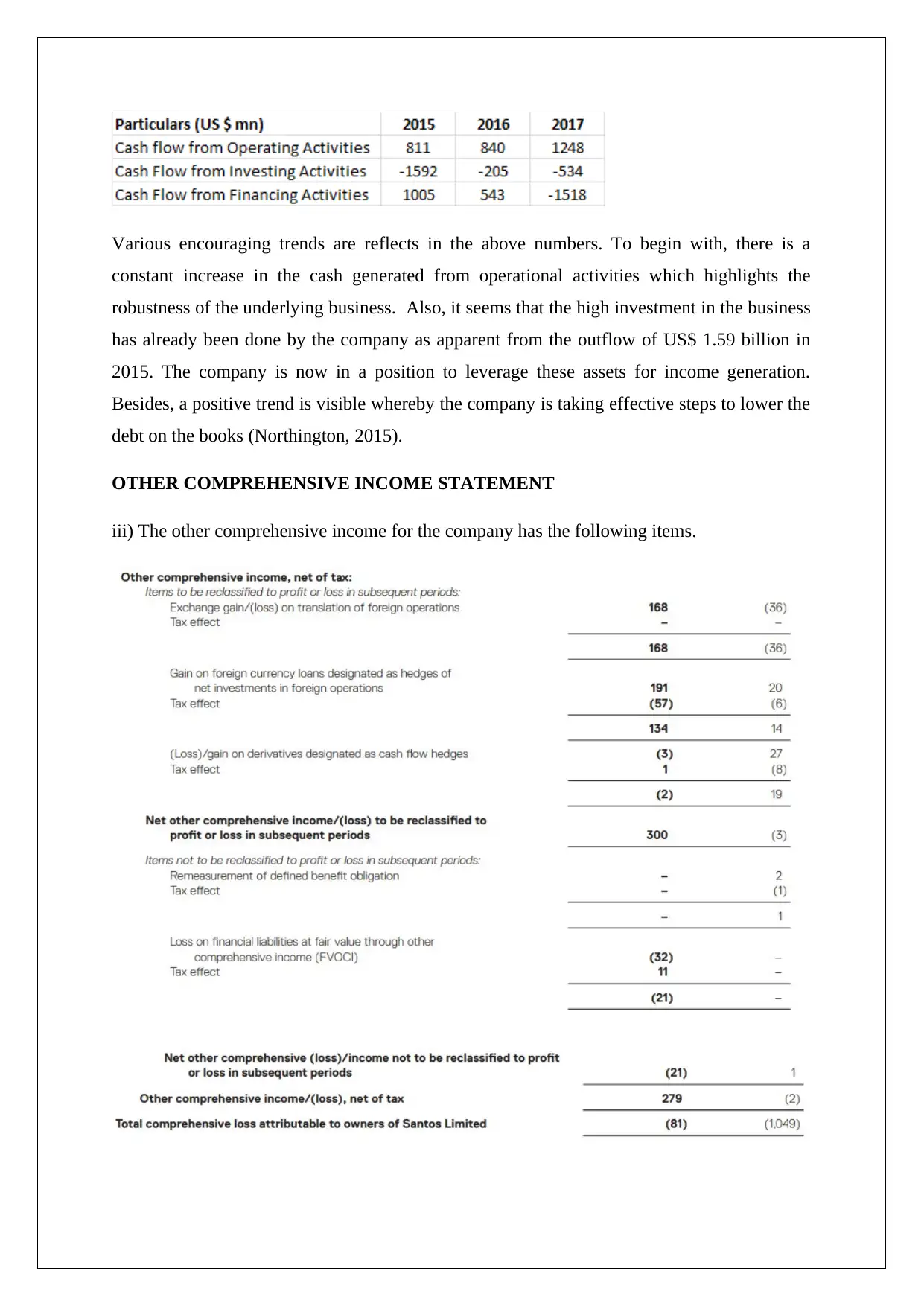

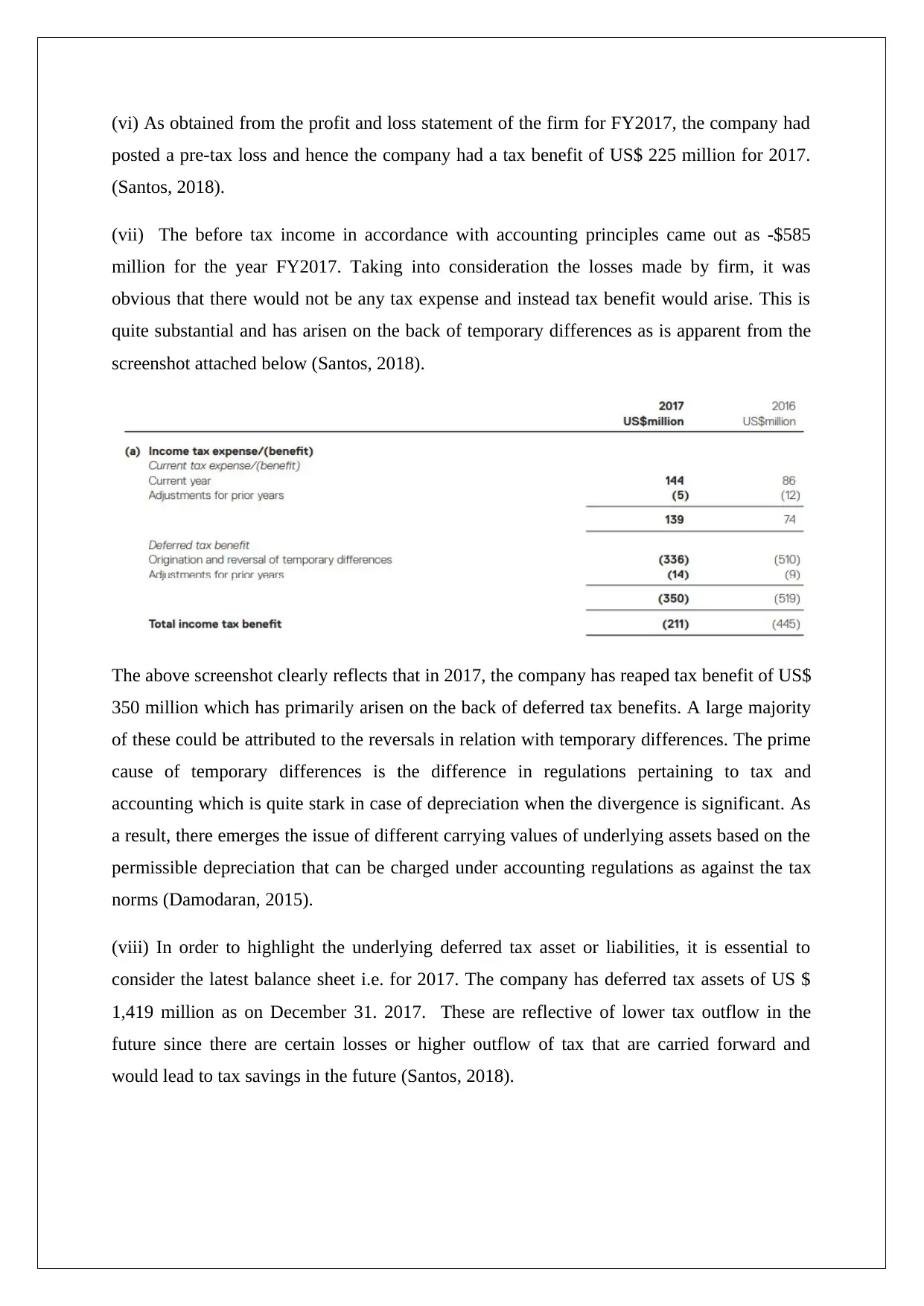

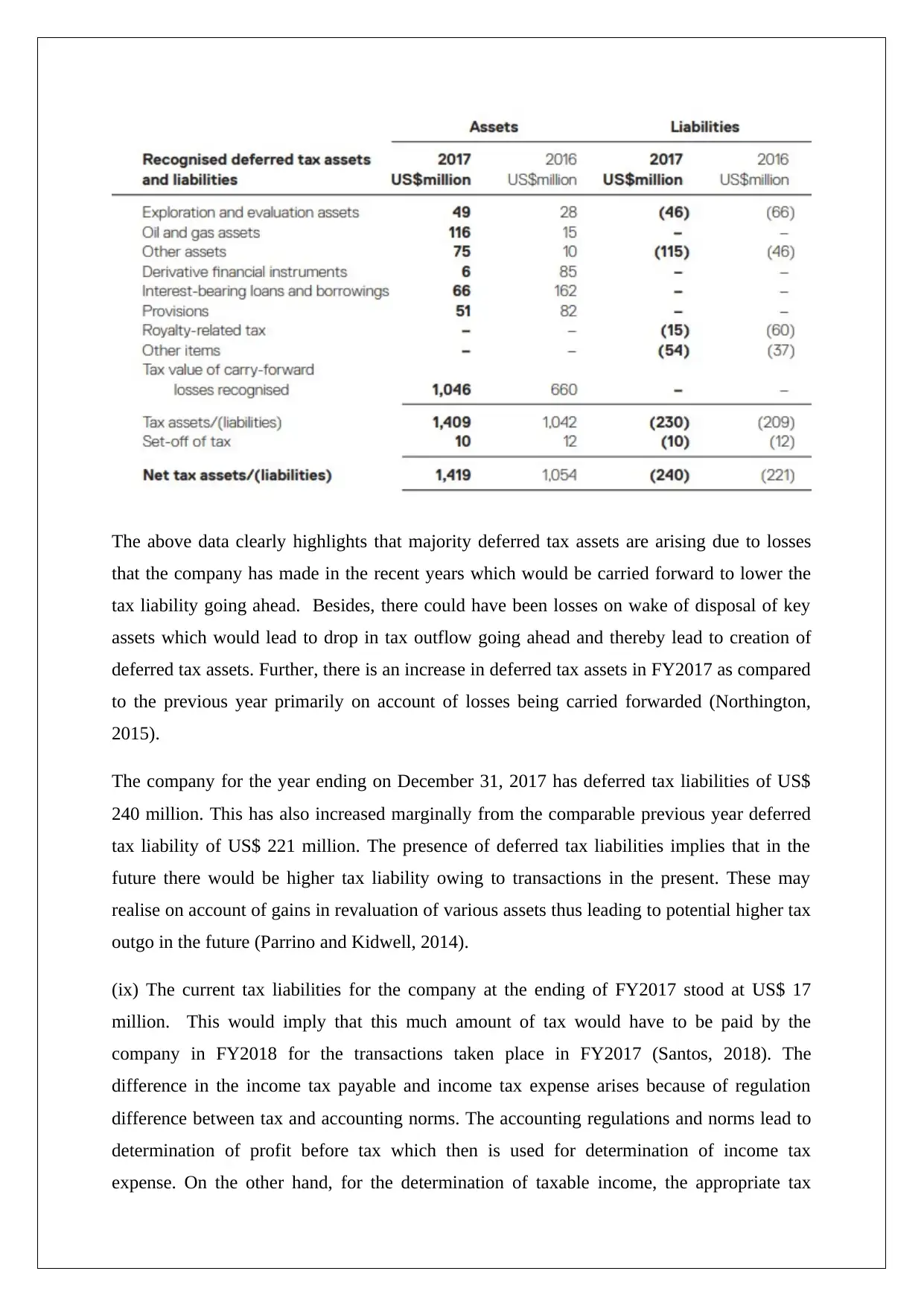

This report provides a detailed analysis of the corporate accounting practices of Santos Limited. It begins with an examination of the cash flow statement, highlighting key items such as receipts from customers, payments to suppliers, and exploration expenses. The report then delves into the investing and financing cash flow activities, noting the company's investment in business assets and its debt reduction strategies. A three-year summary of the major cash flows reveals positive trends in operational cash generation and debt management. The report also explores the other comprehensive income (OCI) statement, detailing items like exchange gains/losses and foreign currency hedges, and explains why these items are presented in OCI rather than the profit and loss statement. Furthermore, the report analyzes the company's corporate income tax, including the tax benefit received, deferred tax assets and liabilities, and the difference between income tax expense and cash paid for taxes. The report concludes by emphasizing the practical complexities of taxation and the importance of understanding the differences between accounting and tax regulations. The report uses Santos Limited's 2016 and 2017 annual reports and relevant financial literature to support its analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.