Financial Statement Analysis Report: Saracen Mineral Holdings Limited

VerifiedAdded on 2022/10/11

|12

|5037

|26

Report

AI Summary

This report provides a comprehensive financial analysis of Saracen Mineral Holdings Limited (SAR), a gold mining company. It begins with an industry overview and a company profile, detailing Saracen's operations, including the Carosue Dam Operations and Thunderbox operations. The report then presents and analyzes the company's financial statements, including the income statement, balance sheet, and cash flow statement, spanning five years. Business analysis covers revenue, costs, and capital expenditures, while the financial risk section explores market, commodity, and credit risks. Ratio analysis and financial performance are examined, including liquidity and profitability ratios. The report discusses Saracen's financial position, growth, and return on equity, and offers recommendations based on its analysis of the financial data, ultimately aiming to provide an investment recommendation (Buy or Not). The report utilizes financial data from the company's annual reports and other public sources, evaluating the company's performance, and assessing its strengths and weaknesses.

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Industry Overview........................................................................................................................................................................................3

Company Overview......................................................................................................................................................................................3

Financial Statements and Analysis...........................................................................................................................................................4

BUSINESS ANALYSIS AND RECOMMENDATIONS.........................................................................................................................................6

FINANCIAL RISK........................................................................................................................................................................................7

Ratio analysis...............................................................................................................................................................................................8

Financial Analysis.........................................................................................................................................................................................9

Analysis of Income Statement...................................................................................................................................................................11

Valuation....................................................................................................................................................................................................12

Assumptions.......................................................................................................................................................................................12

Conclusion..................................................................................................................................................................................................13

References.................................................................................................................................................................................................13

2

Industry Overview........................................................................................................................................................................................3

Company Overview......................................................................................................................................................................................3

Financial Statements and Analysis...........................................................................................................................................................4

BUSINESS ANALYSIS AND RECOMMENDATIONS.........................................................................................................................................6

FINANCIAL RISK........................................................................................................................................................................................7

Ratio analysis...............................................................................................................................................................................................8

Financial Analysis.........................................................................................................................................................................................9

Analysis of Income Statement...................................................................................................................................................................11

Valuation....................................................................................................................................................................................................12

Assumptions.......................................................................................................................................................................................12

Conclusion..................................................................................................................................................................................................13

References.................................................................................................................................................................................................13

2

Industry Overview

The process of digging out of the ores of gold or gold from the land is known as gold mining. There are a number of methods or

techniques which are used for taking out the gold including, dredging, sluicing, hard rock mining, gold panning, placer mining, rocker

box, and the by-product mining. This industry is a very major industry from since last thousand years. As these gold mining are

conducted by the corporations which are large in size. There are a number of companies which are indulged in this business. These

companies are billion dollar corporations. There is number of research reports and the analysis of this industry can be done by the

industries worldwide.

This industry today finds itself at a point of inflection. This company is on the process of complete growth and the reserves of the gold

are depleting day by day. There are a number of approaches that are both inorganic and organic if they wish to come back in a

sustainable and economical way. (Anon., 2015)

Company Overview

The company SAR owns complete of the Carouse dam workings from the subsidiaries which they own completely named Saracen

Gold Mines Ltd. the assets of the CDO were completely owned by the company in the year 2006 and the beginning of the production

for commercialized activities started in the year 2010. Nearly about 70,000 ounces have been taken out from the pits.

Saracen’s tenement of the CDO holding deposits is located at the world’s most prime locations of the gold provinces including the

places of Keith Kilkenny Tectonic Zones and the Laverton in the part of Western Australia. This is the place which is considered to be

as the most rime province of the gold in the whole world. There is nearly about 23 million ounces of the gold reserves have been

found in this particular area reserves. The company Saracen is planning to build an infrastructure which is long term plan.

This plant at CDO comprises a modern accommodation of nearly about 238 people and provides all the necessities and is located at

the 120 km east to the Kalgoorlie.

Saracen Mineral Holdings Limited is a gold mining company. It explores and develops mineral properties in Australia. It mines for

gold and nickel deposits. The Company was incorporated in the year 1987. The headquarters of the company is located in Perth,

Australia.

The Annual Production of the company is over 300000ozpa with a forecast of growth in the cash flows. One of the unique features of

the company is that it has zero debt as it has the policy of providing funds for the development of the project from cash flows

generated internally. (Anon., 2015)

Raleigh Finlayson is the Managing Director of the Company. He is a Mining Engineer having technical and operational experience of

over 20 years. Morgan Ball is the Chief Financial Officer of the Company, a Chartered Accountant having experience of 25 years in

the field of logistics, finance and resource industries. (Anon., 2019)

The company owns a 100% interest in:

Carosue Dam Operations located in the north eastern side of Kalgoorile in Western Australia

Thunderbox operations situated in Yandal

Agnew Wiluna belts situated in Northeastern Goldfields of Western Australia

3

The process of digging out of the ores of gold or gold from the land is known as gold mining. There are a number of methods or

techniques which are used for taking out the gold including, dredging, sluicing, hard rock mining, gold panning, placer mining, rocker

box, and the by-product mining. This industry is a very major industry from since last thousand years. As these gold mining are

conducted by the corporations which are large in size. There are a number of companies which are indulged in this business. These

companies are billion dollar corporations. There is number of research reports and the analysis of this industry can be done by the

industries worldwide.

This industry today finds itself at a point of inflection. This company is on the process of complete growth and the reserves of the gold

are depleting day by day. There are a number of approaches that are both inorganic and organic if they wish to come back in a

sustainable and economical way. (Anon., 2015)

Company Overview

The company SAR owns complete of the Carouse dam workings from the subsidiaries which they own completely named Saracen

Gold Mines Ltd. the assets of the CDO were completely owned by the company in the year 2006 and the beginning of the production

for commercialized activities started in the year 2010. Nearly about 70,000 ounces have been taken out from the pits.

Saracen’s tenement of the CDO holding deposits is located at the world’s most prime locations of the gold provinces including the

places of Keith Kilkenny Tectonic Zones and the Laverton in the part of Western Australia. This is the place which is considered to be

as the most rime province of the gold in the whole world. There is nearly about 23 million ounces of the gold reserves have been

found in this particular area reserves. The company Saracen is planning to build an infrastructure which is long term plan.

This plant at CDO comprises a modern accommodation of nearly about 238 people and provides all the necessities and is located at

the 120 km east to the Kalgoorlie.

Saracen Mineral Holdings Limited is a gold mining company. It explores and develops mineral properties in Australia. It mines for

gold and nickel deposits. The Company was incorporated in the year 1987. The headquarters of the company is located in Perth,

Australia.

The Annual Production of the company is over 300000ozpa with a forecast of growth in the cash flows. One of the unique features of

the company is that it has zero debt as it has the policy of providing funds for the development of the project from cash flows

generated internally. (Anon., 2015)

Raleigh Finlayson is the Managing Director of the Company. He is a Mining Engineer having technical and operational experience of

over 20 years. Morgan Ball is the Chief Financial Officer of the Company, a Chartered Accountant having experience of 25 years in

the field of logistics, finance and resource industries. (Anon., 2019)

The company owns a 100% interest in:

Carosue Dam Operations located in the north eastern side of Kalgoorile in Western Australia

Thunderbox operations situated in Yandal

Agnew Wiluna belts situated in Northeastern Goldfields of Western Australia

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

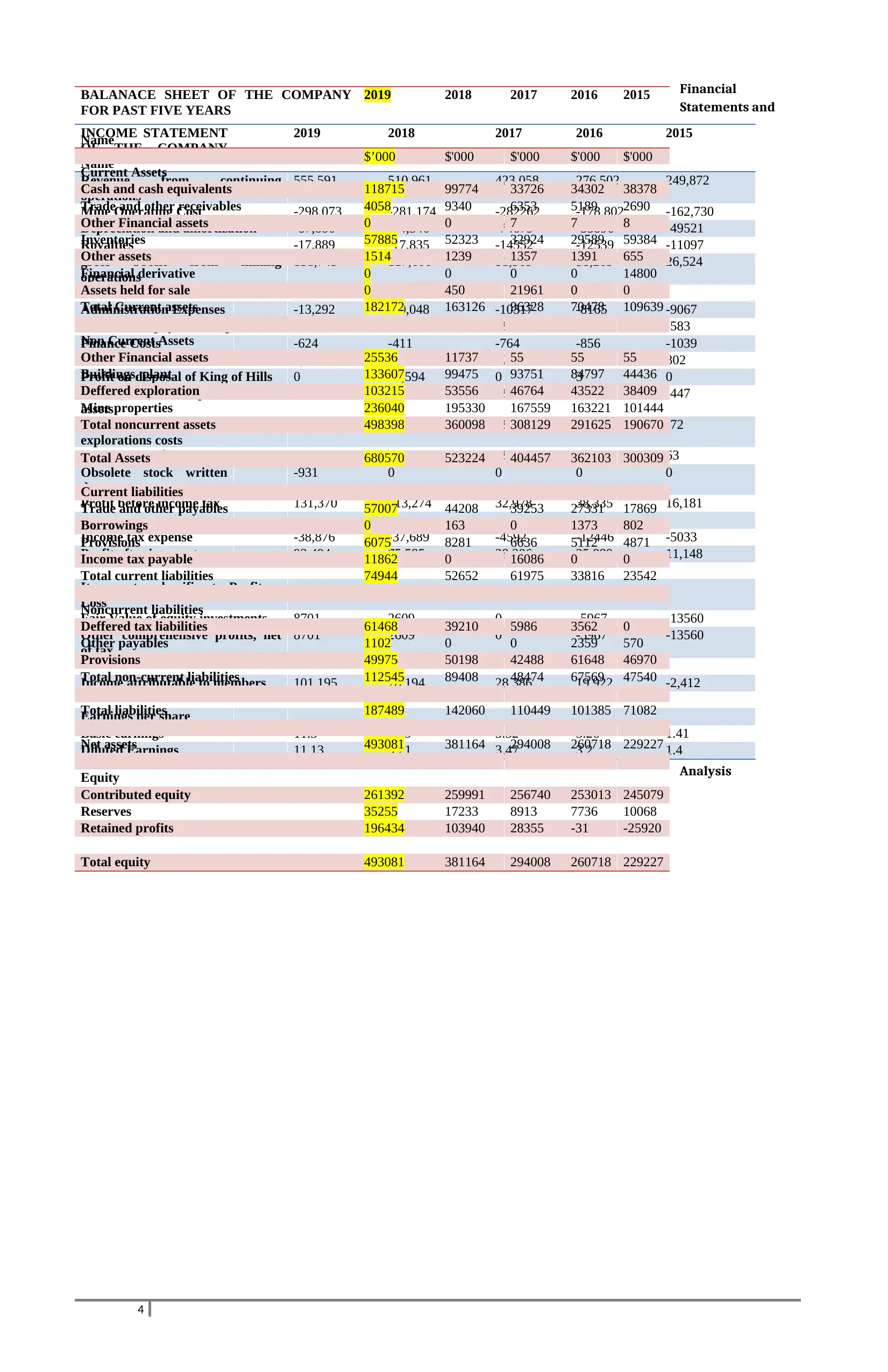

Financial

Statements and

Analysis

4

INCOME STATEMENT

OF THE COMPANY

Name

2019 2018 2017 2016 2015

Revenue from continuing

operations

555,591 510,961 423,058 276,502 249,872

Mine Operating Cost -298,073 -281,174 -282262 -178,802 -162,730

Depreciation and amortization -87,886 -94,346 -74679 -33896 -49521

Royalties -17,889 -17,835 -14552 -12539 -11097

gross Profit from mining

operations

151,743 117,606 51,565 51,265 26,524

Administration Expenses -13,292 -10,048 -10317 -8165 -9067

Share based payments expense -6,969 -3,379 -2736 -3635 -583

Finance Costs -624 -411 -764 -856 -1039

Other Revenue 2,188 1,213 522 729 802

Profit on disposal of King of Hills 0 10,594 0 3 0

Profit/(Loss) on disposal of fixed

assets

-354 0 -39 -1005 -447

Expensing of deferred

explorations costs

-391 1,405 -2477 0 -72

Impairment of assets 0 -896 -2776 -1 63

Obsolete stock written

down

-931 0 0 0 0

Profit before income tax 131,370 113,274 32,978 38,335 16,181

Income tax expense -38,876 -37,689 -4592 -12446 -5033

Profit after income tax 92,494 75,585 28,386 25,889 11,148

Items not reclassifies to Profit or

Loss

Fair Value of equity investments 8701 2609 0 -5967 -13560

Other comprehensive profits, net

of tax

8701 2609 0 -5967 -13560

Income attributable to members 101,195 78,194 28,386 19,922 -2,412

Earnings per share

Basic earnings 11.3 9.29 3.52 3.26 1.41

Diluted Earnings 11.13 9.21 3.47 3.2 1.4

BALANACE SHEET OF THE COMPANY

FOR PAST FIVE YEARS

Name

2019 2018 2017 2016 2015

$’000 $'000 $'000 $'000 $'000

Current Assets

Cash and cash equivalents 118715 99774 33726 34302 38378

Trade and other receivables 4058 9340 6353 5189 2690

Other Financial assets 0 0 7 7 8

Inventories 57885 52323 32924 29589 59384

Other assets 1514 1239 1357 1391 655

Financial derivative 0 0 0 0 14800

Assets held for sale 0 450 21961 0 0

Total Current assets 182172 163126 96328 70478 109639

Non Current Assets

Other Financial assets 25536 11737 55 55 55

Buildings, plant 133607 99475 93751 84797 44436

Deffered exploration 103215 53556 46764 43522 38409

Mine properties 236040 195330 167559 163221 101444

Total noncurrent assets 498398 360098 308129 291625 190670

Total Assets 680570 523224 404457 362103 300309

Current liabilities

Trade and other payables 57007 44208 39253 27331 17869

Borrowings 0 163 0 1373 802

Provisions 6075 8281 6636 5112 4871

Income tax payable 11862 0 16086 0 0

Total current liabilities 74944 52652 61975 33816 23542

Noncurrent liabilities

Deffered tax liabilities 61468 39210 5986 3562 0

Other payables 1102 0 0 2359 570

Provisions 49975 50198 42488 61648 46970

Total non-current liabilities 112545 89408 48474 67569 47540

Total liabilities 187489 142060 110449 101385 71082

Net assets 493081 381164 294008 260718 229227

Equity

Contributed equity 261392 259991 256740 253013 245079

Reserves 35255 17233 8913 7736 10068

Retained profits 196434 103940 28355 -31 -25920

Total equity 493081 381164 294008 260718 229227

Statements and

Analysis

4

INCOME STATEMENT

OF THE COMPANY

Name

2019 2018 2017 2016 2015

Revenue from continuing

operations

555,591 510,961 423,058 276,502 249,872

Mine Operating Cost -298,073 -281,174 -282262 -178,802 -162,730

Depreciation and amortization -87,886 -94,346 -74679 -33896 -49521

Royalties -17,889 -17,835 -14552 -12539 -11097

gross Profit from mining

operations

151,743 117,606 51,565 51,265 26,524

Administration Expenses -13,292 -10,048 -10317 -8165 -9067

Share based payments expense -6,969 -3,379 -2736 -3635 -583

Finance Costs -624 -411 -764 -856 -1039

Other Revenue 2,188 1,213 522 729 802

Profit on disposal of King of Hills 0 10,594 0 3 0

Profit/(Loss) on disposal of fixed

assets

-354 0 -39 -1005 -447

Expensing of deferred

explorations costs

-391 1,405 -2477 0 -72

Impairment of assets 0 -896 -2776 -1 63

Obsolete stock written

down

-931 0 0 0 0

Profit before income tax 131,370 113,274 32,978 38,335 16,181

Income tax expense -38,876 -37,689 -4592 -12446 -5033

Profit after income tax 92,494 75,585 28,386 25,889 11,148

Items not reclassifies to Profit or

Loss

Fair Value of equity investments 8701 2609 0 -5967 -13560

Other comprehensive profits, net

of tax

8701 2609 0 -5967 -13560

Income attributable to members 101,195 78,194 28,386 19,922 -2,412

Earnings per share

Basic earnings 11.3 9.29 3.52 3.26 1.41

Diluted Earnings 11.13 9.21 3.47 3.2 1.4

BALANACE SHEET OF THE COMPANY

FOR PAST FIVE YEARS

Name

2019 2018 2017 2016 2015

$’000 $'000 $'000 $'000 $'000

Current Assets

Cash and cash equivalents 118715 99774 33726 34302 38378

Trade and other receivables 4058 9340 6353 5189 2690

Other Financial assets 0 0 7 7 8

Inventories 57885 52323 32924 29589 59384

Other assets 1514 1239 1357 1391 655

Financial derivative 0 0 0 0 14800

Assets held for sale 0 450 21961 0 0

Total Current assets 182172 163126 96328 70478 109639

Non Current Assets

Other Financial assets 25536 11737 55 55 55

Buildings, plant 133607 99475 93751 84797 44436

Deffered exploration 103215 53556 46764 43522 38409

Mine properties 236040 195330 167559 163221 101444

Total noncurrent assets 498398 360098 308129 291625 190670

Total Assets 680570 523224 404457 362103 300309

Current liabilities

Trade and other payables 57007 44208 39253 27331 17869

Borrowings 0 163 0 1373 802

Provisions 6075 8281 6636 5112 4871

Income tax payable 11862 0 16086 0 0

Total current liabilities 74944 52652 61975 33816 23542

Noncurrent liabilities

Deffered tax liabilities 61468 39210 5986 3562 0

Other payables 1102 0 0 2359 570

Provisions 49975 50198 42488 61648 46970

Total non-current liabilities 112545 89408 48474 67569 47540

Total liabilities 187489 142060 110449 101385 71082

Net assets 493081 381164 294008 260718 229227

Equity

Contributed equity 261392 259991 256740 253013 245079

Reserves 35255 17233 8913 7736 10068

Retained profits 196434 103940 28355 -31 -25920

Total equity 493081 381164 294008 260718 229227

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

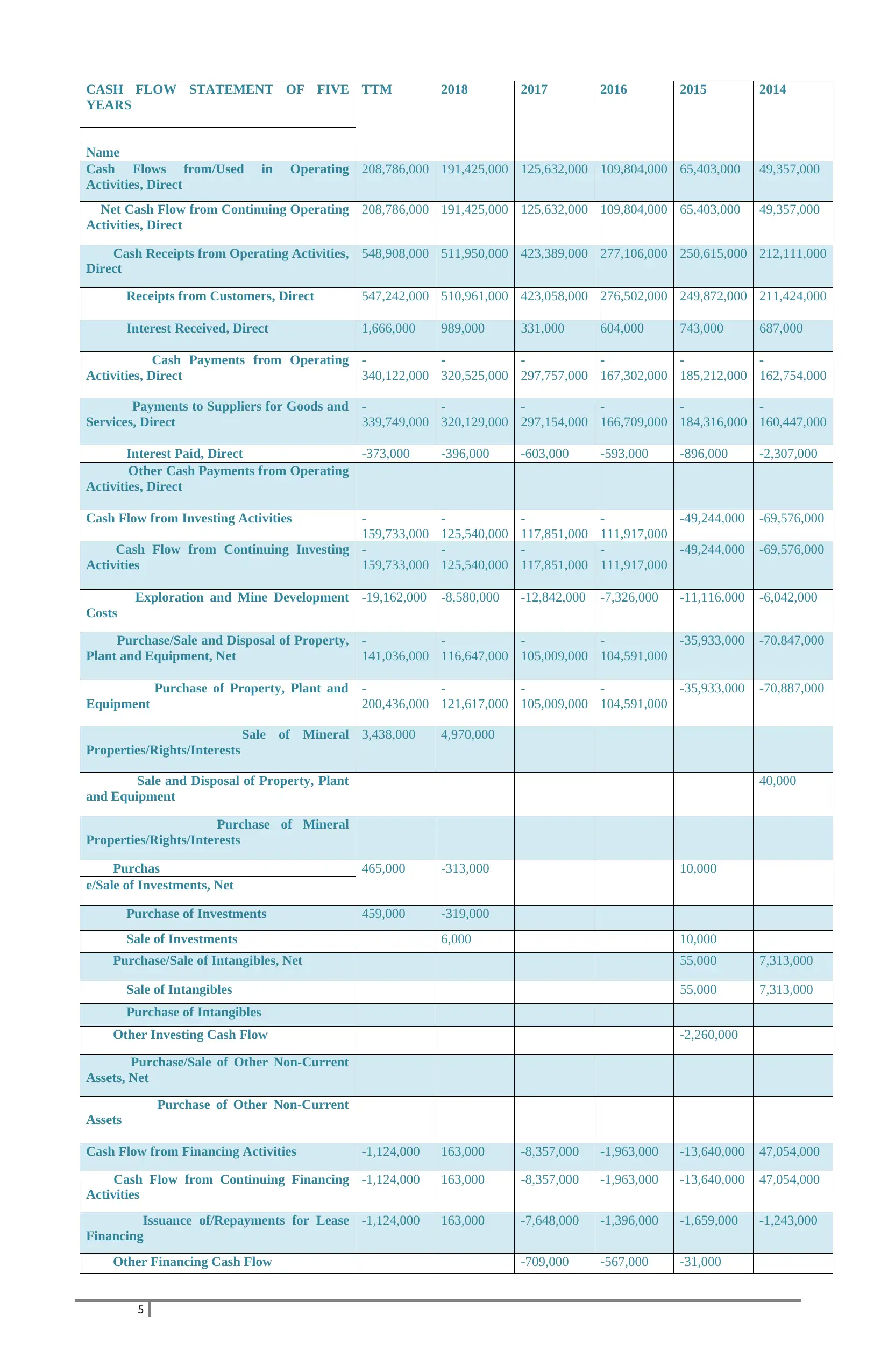

CASH FLOW STATEMENT OF FIVE

YEARS

TTM 2018 2017 2016 2015 2014

Name

Cash Flows from/Used in Operating

Activities, Direct

208,786,000 191,425,000 125,632,000 109,804,000 65,403,000 49,357,000

Net Cash Flow from Continuing Operating

Activities, Direct

208,786,000 191,425,000 125,632,000 109,804,000 65,403,000 49,357,000

Cash Receipts from Operating Activities,

Direct

548,908,000 511,950,000 423,389,000 277,106,000 250,615,000 212,111,000

Receipts from Customers, Direct 547,242,000 510,961,000 423,058,000 276,502,000 249,872,000 211,424,000

Interest Received, Direct 1,666,000 989,000 331,000 604,000 743,000 687,000

Cash Payments from Operating

Activities, Direct

-

340,122,000

-

320,525,000

-

297,757,000

-

167,302,000

-

185,212,000

-

162,754,000

Payments to Suppliers for Goods and

Services, Direct

-

339,749,000

-

320,129,000

-

297,154,000

-

166,709,000

-

184,316,000

-

160,447,000

Interest Paid, Direct -373,000 -396,000 -603,000 -593,000 -896,000 -2,307,000

Other Cash Payments from Operating

Activities, Direct

Cash Flow from Investing Activities -

159,733,000

-

125,540,000

-

117,851,000

-

111,917,000

-49,244,000 -69,576,000

Cash Flow from Continuing Investing

Activities

-

159,733,000

-

125,540,000

-

117,851,000

-

111,917,000

-49,244,000 -69,576,000

Exploration and Mine Development

Costs

-19,162,000 -8,580,000 -12,842,000 -7,326,000 -11,116,000 -6,042,000

Purchase/Sale and Disposal of Property,

Plant and Equipment, Net

-

141,036,000

-

116,647,000

-

105,009,000

-

104,591,000

-35,933,000 -70,847,000

Purchase of Property, Plant and

Equipment

-

200,436,000

-

121,617,000

-

105,009,000

-

104,591,000

-35,933,000 -70,887,000

Sale of Mineral

Properties/Rights/Interests

3,438,000 4,970,000

Sale and Disposal of Property, Plant

and Equipment

40,000

Purchase of Mineral

Properties/Rights/Interests

Purchas 465,000 -313,000 10,000

e/Sale of Investments, Net

Purchase of Investments 459,000 -319,000

Sale of Investments 6,000 10,000

Purchase/Sale of Intangibles, Net 55,000 7,313,000

Sale of Intangibles 55,000 7,313,000

Purchase of Intangibles

Other Investing Cash Flow -2,260,000

Purchase/Sale of Other Non-Current

Assets, Net

Purchase of Other Non-Current

Assets

Cash Flow from Financing Activities -1,124,000 163,000 -8,357,000 -1,963,000 -13,640,000 47,054,000

Cash Flow from Continuing Financing

Activities

-1,124,000 163,000 -8,357,000 -1,963,000 -13,640,000 47,054,000

Issuance of/Repayments for Lease

Financing

-1,124,000 163,000 -7,648,000 -1,396,000 -1,659,000 -1,243,000

Other Financing Cash Flow -709,000 -567,000 -31,000

5

YEARS

TTM 2018 2017 2016 2015 2014

Name

Cash Flows from/Used in Operating

Activities, Direct

208,786,000 191,425,000 125,632,000 109,804,000 65,403,000 49,357,000

Net Cash Flow from Continuing Operating

Activities, Direct

208,786,000 191,425,000 125,632,000 109,804,000 65,403,000 49,357,000

Cash Receipts from Operating Activities,

Direct

548,908,000 511,950,000 423,389,000 277,106,000 250,615,000 212,111,000

Receipts from Customers, Direct 547,242,000 510,961,000 423,058,000 276,502,000 249,872,000 211,424,000

Interest Received, Direct 1,666,000 989,000 331,000 604,000 743,000 687,000

Cash Payments from Operating

Activities, Direct

-

340,122,000

-

320,525,000

-

297,757,000

-

167,302,000

-

185,212,000

-

162,754,000

Payments to Suppliers for Goods and

Services, Direct

-

339,749,000

-

320,129,000

-

297,154,000

-

166,709,000

-

184,316,000

-

160,447,000

Interest Paid, Direct -373,000 -396,000 -603,000 -593,000 -896,000 -2,307,000

Other Cash Payments from Operating

Activities, Direct

Cash Flow from Investing Activities -

159,733,000

-

125,540,000

-

117,851,000

-

111,917,000

-49,244,000 -69,576,000

Cash Flow from Continuing Investing

Activities

-

159,733,000

-

125,540,000

-

117,851,000

-

111,917,000

-49,244,000 -69,576,000

Exploration and Mine Development

Costs

-19,162,000 -8,580,000 -12,842,000 -7,326,000 -11,116,000 -6,042,000

Purchase/Sale and Disposal of Property,

Plant and Equipment, Net

-

141,036,000

-

116,647,000

-

105,009,000

-

104,591,000

-35,933,000 -70,847,000

Purchase of Property, Plant and

Equipment

-

200,436,000

-

121,617,000

-

105,009,000

-

104,591,000

-35,933,000 -70,887,000

Sale of Mineral

Properties/Rights/Interests

3,438,000 4,970,000

Sale and Disposal of Property, Plant

and Equipment

40,000

Purchase of Mineral

Properties/Rights/Interests

Purchas 465,000 -313,000 10,000

e/Sale of Investments, Net

Purchase of Investments 459,000 -319,000

Sale of Investments 6,000 10,000

Purchase/Sale of Intangibles, Net 55,000 7,313,000

Sale of Intangibles 55,000 7,313,000

Purchase of Intangibles

Other Investing Cash Flow -2,260,000

Purchase/Sale of Other Non-Current

Assets, Net

Purchase of Other Non-Current

Assets

Cash Flow from Financing Activities -1,124,000 163,000 -8,357,000 -1,963,000 -13,640,000 47,054,000

Cash Flow from Continuing Financing

Activities

-1,124,000 163,000 -8,357,000 -1,963,000 -13,640,000 47,054,000

Issuance of/Repayments for Lease

Financing

-1,124,000 163,000 -7,648,000 -1,396,000 -1,659,000 -1,243,000

Other Financing Cash Flow -709,000 -567,000 -31,000

5

Issuance of/Repayments for Debt, Net -11,950,000 -10,000,000

Issuance of/Repayments for Long

Term Debt, Net

-11,950,000 -10,000,000

Repayments for Long Term Debt -11,950,000 -10,000,000

Proceeds from Issuance of Long

Term Debt

Issuance of/Payments for Common

Stock, Net

61,232,000

Proceeds from Issuance of Common

Stock

61,232,000

Issue and Financing Costs -2,935,000

Share Issuance Costs -2,935,000

Cash and Cash Equivalents, End of Period 113,221,000 99,774,000 33,726,000 34,302,000 38,378,000 35,859,000

Change in Cash 47,929,000 66,048,000 -576,000 -4,076,000 2,519,000 26,835,000

Cash and Cash Equivalents, Beginning of

Period

65,292,000 33,726,000 34,302,000 38,378,000 35,859,000 9,024,000

The above given are the Financial Statements of the company Saracen Mineral Holdings Ltd. These are the financials of last five years

of this company. In the next section of the report, a comparative study of the company on the basis of its financials is done.

BUSINESS ANALYSIS AND RECOMMENDATIONS

The Company reported a net profit after tax of $92.5 million which is an increase of 22% on the previous year. The Revenue from

sales for the year was $ 555.6 million which has increased by 9% from the previous year.

Capital expenditure on purchase of plant and equipment was $ 198.8 million which has increased from $ 130.2 million. The reason

was due to the development of Kailis open pit and the Thunderbox underground mine at TBO and the Karari and Dervish underground

mines. The increase in activities across Karari – Dervish, and Thunderbox in Carosue Dam corridor also contributed to the increase in

expenditure.

In 2019, Saracen’s total cash position stood at $ 154.5 million. The Company also maintains a long term senior corporate financing

facility. It has an initial $ 45 million loan facility with $ 5 million bank guarantee. During the year, the facility was extended by one

year to November 2020.

DIVIDEND –

No dividend has been declared by the Group since the end of the financial year and no dividend was recommended in respect of FY

2019.

On June 14, 2019 Saracen has announced an off-market takeover offer to Bligh Resources. The 100 % scrip consideration was valued

at a $38 million at the time of announcement.

FINANCIAL RISK

The Company’s financial instruments mainly include cash and short term deposits. In addition to this, the group has financial assets

measured at fair value through debtors and creditors. The Board has established Risk Management and Audit Committees which

control various aspects of financial risks. (Anon., 2015)

Market Risks

The Group is not involved in any hedging or derivative transactions to manage interest rate risk. The interest rate risk primarily

pertains to assets and liabilities having variable interest rates.

Commodity risk

The exposure of the group to commodity risk is due to the up and down movement in the gold price. This is hedged by booking

the delivery contracts at the specific dates and rates.

Credit Risk

The group deals only with recognized third parties. There is no significant concentration of credit risk in the group.

Liquidity Risk

Liquidity of the group is managed as they have sufficient cash reserves and marketable securities and hence monitor cash flows.

6

Issuance of/Repayments for Long

Term Debt, Net

-11,950,000 -10,000,000

Repayments for Long Term Debt -11,950,000 -10,000,000

Proceeds from Issuance of Long

Term Debt

Issuance of/Payments for Common

Stock, Net

61,232,000

Proceeds from Issuance of Common

Stock

61,232,000

Issue and Financing Costs -2,935,000

Share Issuance Costs -2,935,000

Cash and Cash Equivalents, End of Period 113,221,000 99,774,000 33,726,000 34,302,000 38,378,000 35,859,000

Change in Cash 47,929,000 66,048,000 -576,000 -4,076,000 2,519,000 26,835,000

Cash and Cash Equivalents, Beginning of

Period

65,292,000 33,726,000 34,302,000 38,378,000 35,859,000 9,024,000

The above given are the Financial Statements of the company Saracen Mineral Holdings Ltd. These are the financials of last five years

of this company. In the next section of the report, a comparative study of the company on the basis of its financials is done.

BUSINESS ANALYSIS AND RECOMMENDATIONS

The Company reported a net profit after tax of $92.5 million which is an increase of 22% on the previous year. The Revenue from

sales for the year was $ 555.6 million which has increased by 9% from the previous year.

Capital expenditure on purchase of plant and equipment was $ 198.8 million which has increased from $ 130.2 million. The reason

was due to the development of Kailis open pit and the Thunderbox underground mine at TBO and the Karari and Dervish underground

mines. The increase in activities across Karari – Dervish, and Thunderbox in Carosue Dam corridor also contributed to the increase in

expenditure.

In 2019, Saracen’s total cash position stood at $ 154.5 million. The Company also maintains a long term senior corporate financing

facility. It has an initial $ 45 million loan facility with $ 5 million bank guarantee. During the year, the facility was extended by one

year to November 2020.

DIVIDEND –

No dividend has been declared by the Group since the end of the financial year and no dividend was recommended in respect of FY

2019.

On June 14, 2019 Saracen has announced an off-market takeover offer to Bligh Resources. The 100 % scrip consideration was valued

at a $38 million at the time of announcement.

FINANCIAL RISK

The Company’s financial instruments mainly include cash and short term deposits. In addition to this, the group has financial assets

measured at fair value through debtors and creditors. The Board has established Risk Management and Audit Committees which

control various aspects of financial risks. (Anon., 2015)

Market Risks

The Group is not involved in any hedging or derivative transactions to manage interest rate risk. The interest rate risk primarily

pertains to assets and liabilities having variable interest rates.

Commodity risk

The exposure of the group to commodity risk is due to the up and down movement in the gold price. This is hedged by booking

the delivery contracts at the specific dates and rates.

Credit Risk

The group deals only with recognized third parties. There is no significant concentration of credit risk in the group.

Liquidity Risk

Liquidity of the group is managed as they have sufficient cash reserves and marketable securities and hence monitor cash flows.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With zero debt in the balance sheet, Saracen is not constrained to debt obligations and covenants which can be a burden during

financial depression. With no lenders need to tend to, Saracen enjoy financial flexibility and independence.

The cash and short term investment are sufficient to cover upcoming liabilities. The profit growth of the company has been positive

with an average annual growth rate of 58% which is way higher than the industry growth rate of 33%. Return on equity of the

company is 17% which is above the return of industry which is 14%. This strong and consistent market performance shows that track

record of company is robust which focuses on delivering strong return over a large number of years. (Anon., 2019)

7

financial depression. With no lenders need to tend to, Saracen enjoy financial flexibility and independence.

The cash and short term investment are sufficient to cover upcoming liabilities. The profit growth of the company has been positive

with an average annual growth rate of 58% which is way higher than the industry growth rate of 33%. Return on equity of the

company is 17% which is above the return of industry which is 14%. This strong and consistent market performance shows that track

record of company is robust which focuses on delivering strong return over a large number of years. (Anon., 2019)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

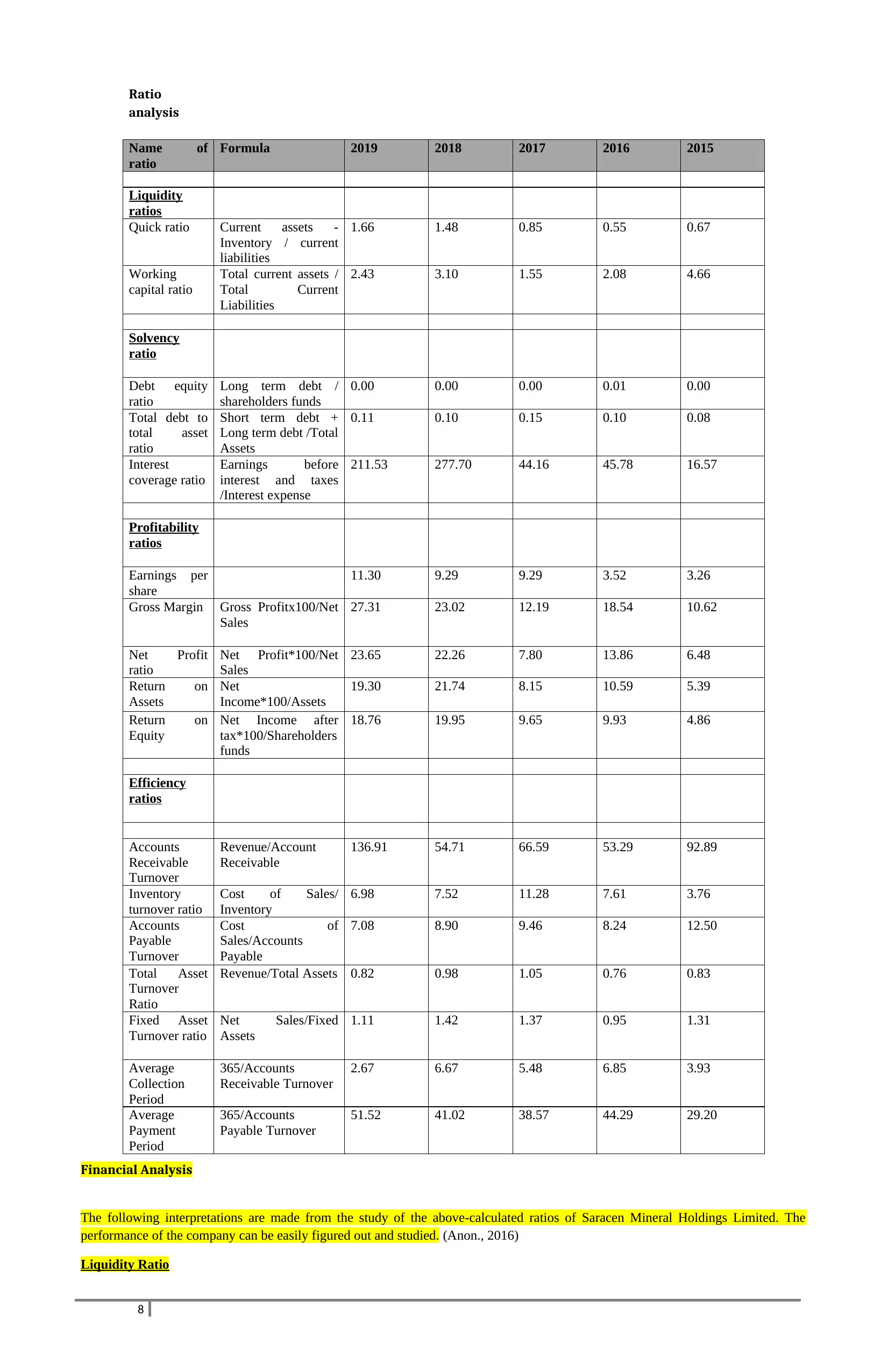

Financial Analysis

The following interpretations are made from the study of the above-calculated ratios of Saracen Mineral Holdings Limited. The

performance of the company can be easily figured out and studied. (Anon., 2016)

Liquidity Ratio

8

Ratio

analysis

Name of

ratio

Formula 2019 2018 2017 2016 2015

Liquidity

ratios

Quick ratio Current assets -

Inventory / current

liabilities

1.66 1.48 0.85 0.55 0.67

Working

capital ratio

Total current assets /

Total Current

Liabilities

2.43 3.10 1.55 2.08 4.66

Solvency

ratio

Debt equity

ratio

Long term debt /

shareholders funds

0.00 0.00 0.00 0.01 0.00

Total debt to

total asset

ratio

Short term debt +

Long term debt /Total

Assets

0.11 0.10 0.15 0.10 0.08

Interest

coverage ratio

Earnings before

interest and taxes

/Interest expense

211.53 277.70 44.16 45.78 16.57

Profitability

ratios

Earnings per

share

11.30 9.29 9.29 3.52 3.26

Gross Margin Gross Profitx100/Net

Sales

27.31 23.02 12.19 18.54 10.62

Net Profit

ratio

Net Profit*100/Net

Sales

23.65 22.26 7.80 13.86 6.48

Return on

Assets

Net

Income*100/Assets

19.30 21.74 8.15 10.59 5.39

Return on

Equity

Net Income after

tax*100/Shareholders

funds

18.76 19.95 9.65 9.93 4.86

Efficiency

ratios

Accounts

Receivable

Turnover

Revenue/Account

Receivable

136.91 54.71 66.59 53.29 92.89

Inventory

turnover ratio

Cost of Sales/

Inventory

6.98 7.52 11.28 7.61 3.76

Accounts

Payable

Turnover

Cost of

Sales/Accounts

Payable

7.08 8.90 9.46 8.24 12.50

Total Asset

Turnover

Ratio

Revenue/Total Assets 0.82 0.98 1.05 0.76 0.83

Fixed Asset

Turnover ratio

Net Sales/Fixed

Assets

1.11 1.42 1.37 0.95 1.31

Average

Collection

Period

365/Accounts

Receivable Turnover

2.67 6.67 5.48 6.85 3.93

Average

Payment

Period

365/Accounts

Payable Turnover

51.52 41.02 38.57 44.29 29.20

The following interpretations are made from the study of the above-calculated ratios of Saracen Mineral Holdings Limited. The

performance of the company can be easily figured out and studied. (Anon., 2016)

Liquidity Ratio

8

Ratio

analysis

Name of

ratio

Formula 2019 2018 2017 2016 2015

Liquidity

ratios

Quick ratio Current assets -

Inventory / current

liabilities

1.66 1.48 0.85 0.55 0.67

Working

capital ratio

Total current assets /

Total Current

Liabilities

2.43 3.10 1.55 2.08 4.66

Solvency

ratio

Debt equity

ratio

Long term debt /

shareholders funds

0.00 0.00 0.00 0.01 0.00

Total debt to

total asset

ratio

Short term debt +

Long term debt /Total

Assets

0.11 0.10 0.15 0.10 0.08

Interest

coverage ratio

Earnings before

interest and taxes

/Interest expense

211.53 277.70 44.16 45.78 16.57

Profitability

ratios

Earnings per

share

11.30 9.29 9.29 3.52 3.26

Gross Margin Gross Profitx100/Net

Sales

27.31 23.02 12.19 18.54 10.62

Net Profit

ratio

Net Profit*100/Net

Sales

23.65 22.26 7.80 13.86 6.48

Return on

Assets

Net

Income*100/Assets

19.30 21.74 8.15 10.59 5.39

Return on

Equity

Net Income after

tax*100/Shareholders

funds

18.76 19.95 9.65 9.93 4.86

Efficiency

ratios

Accounts

Receivable

Turnover

Revenue/Account

Receivable

136.91 54.71 66.59 53.29 92.89

Inventory

turnover ratio

Cost of Sales/

Inventory

6.98 7.52 11.28 7.61 3.76

Accounts

Payable

Turnover

Cost of

Sales/Accounts

Payable

7.08 8.90 9.46 8.24 12.50

Total Asset

Turnover

Ratio

Revenue/Total Assets 0.82 0.98 1.05 0.76 0.83

Fixed Asset

Turnover ratio

Net Sales/Fixed

Assets

1.11 1.42 1.37 0.95 1.31

Average

Collection

Period

365/Accounts

Receivable Turnover

2.67 6.67 5.48 6.85 3.93

Average

Payment

Period

365/Accounts

Payable Turnover

51.52 41.02 38.57 44.29 29.20

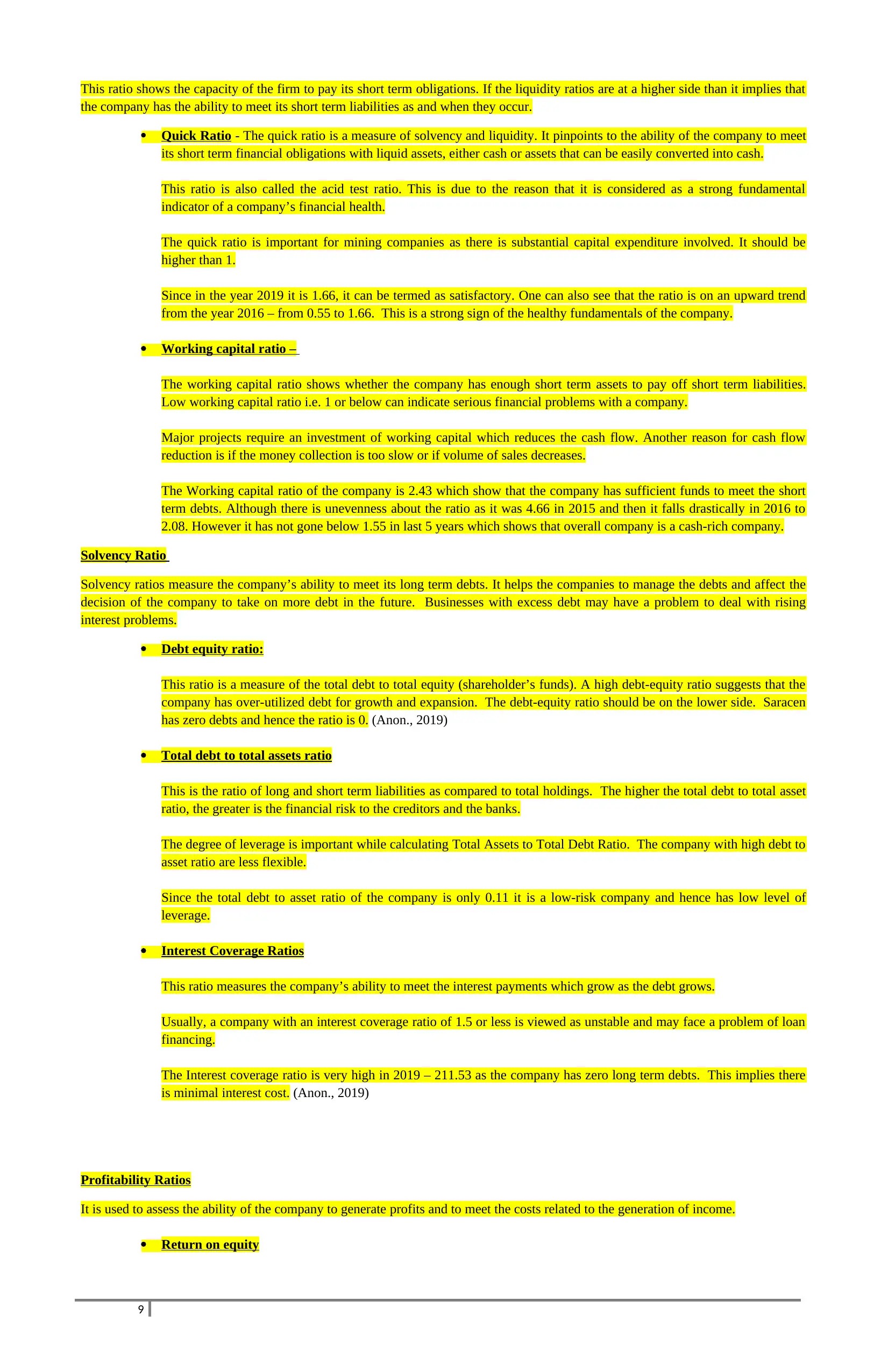

This ratio shows the capacity of the firm to pay its short term obligations. If the liquidity ratios are at a higher side than it implies that

the company has the ability to meet its short term liabilities as and when they occur.

Quick Ratio - The quick ratio is a measure of solvency and liquidity. It pinpoints to the ability of the company to meet

its short term financial obligations with liquid assets, either cash or assets that can be easily converted into cash.

This ratio is also called the acid test ratio. This is due to the reason that it is considered as a strong fundamental

indicator of a company’s financial health.

The quick ratio is important for mining companies as there is substantial capital expenditure involved. It should be

higher than 1.

Since in the year 2019 it is 1.66, it can be termed as satisfactory. One can also see that the ratio is on an upward trend

from the year 2016 – from 0.55 to 1.66. This is a strong sign of the healthy fundamentals of the company.

Working capital ratio –

The working capital ratio shows whether the company has enough short term assets to pay off short term liabilities.

Low working capital ratio i.e. 1 or below can indicate serious financial problems with a company.

Major projects require an investment of working capital which reduces the cash flow. Another reason for cash flow

reduction is if the money collection is too slow or if volume of sales decreases.

The Working capital ratio of the company is 2.43 which show that the company has sufficient funds to meet the short

term debts. Although there is unevenness about the ratio as it was 4.66 in 2015 and then it falls drastically in 2016 to

2.08. However it has not gone below 1.55 in last 5 years which shows that overall company is a cash-rich company.

Solvency Ratio

Solvency ratios measure the company’s ability to meet its long term debts. It helps the companies to manage the debts and affect the

decision of the company to take on more debt in the future. Businesses with excess debt may have a problem to deal with rising

interest problems.

Debt equity ratio:

This ratio is a measure of the total debt to total equity (shareholder’s funds). A high debt-equity ratio suggests that the

company has over-utilized debt for growth and expansion. The debt-equity ratio should be on the lower side. Saracen

has zero debts and hence the ratio is 0. (Anon., 2019)

Total debt to total assets ratio

This is the ratio of long and short term liabilities as compared to total holdings. The higher the total debt to total asset

ratio, the greater is the financial risk to the creditors and the banks.

The degree of leverage is important while calculating Total Assets to Total Debt Ratio. The company with high debt to

asset ratio are less flexible.

Since the total debt to asset ratio of the company is only 0.11 it is a low-risk company and hence has low level of

leverage.

Interest Coverage Ratios

This ratio measures the company’s ability to meet the interest payments which grow as the debt grows.

Usually, a company with an interest coverage ratio of 1.5 or less is viewed as unstable and may face a problem of loan

financing.

The Interest coverage ratio is very high in 2019 – 211.53 as the company has zero long term debts. This implies there

is minimal interest cost. (Anon., 2019)

Profitability Ratios

It is used to assess the ability of the company to generate profits and to meet the costs related to the generation of income.

Return on equity

9

the company has the ability to meet its short term liabilities as and when they occur.

Quick Ratio - The quick ratio is a measure of solvency and liquidity. It pinpoints to the ability of the company to meet

its short term financial obligations with liquid assets, either cash or assets that can be easily converted into cash.

This ratio is also called the acid test ratio. This is due to the reason that it is considered as a strong fundamental

indicator of a company’s financial health.

The quick ratio is important for mining companies as there is substantial capital expenditure involved. It should be

higher than 1.

Since in the year 2019 it is 1.66, it can be termed as satisfactory. One can also see that the ratio is on an upward trend

from the year 2016 – from 0.55 to 1.66. This is a strong sign of the healthy fundamentals of the company.

Working capital ratio –

The working capital ratio shows whether the company has enough short term assets to pay off short term liabilities.

Low working capital ratio i.e. 1 or below can indicate serious financial problems with a company.

Major projects require an investment of working capital which reduces the cash flow. Another reason for cash flow

reduction is if the money collection is too slow or if volume of sales decreases.

The Working capital ratio of the company is 2.43 which show that the company has sufficient funds to meet the short

term debts. Although there is unevenness about the ratio as it was 4.66 in 2015 and then it falls drastically in 2016 to

2.08. However it has not gone below 1.55 in last 5 years which shows that overall company is a cash-rich company.

Solvency Ratio

Solvency ratios measure the company’s ability to meet its long term debts. It helps the companies to manage the debts and affect the

decision of the company to take on more debt in the future. Businesses with excess debt may have a problem to deal with rising

interest problems.

Debt equity ratio:

This ratio is a measure of the total debt to total equity (shareholder’s funds). A high debt-equity ratio suggests that the

company has over-utilized debt for growth and expansion. The debt-equity ratio should be on the lower side. Saracen

has zero debts and hence the ratio is 0. (Anon., 2019)

Total debt to total assets ratio

This is the ratio of long and short term liabilities as compared to total holdings. The higher the total debt to total asset

ratio, the greater is the financial risk to the creditors and the banks.

The degree of leverage is important while calculating Total Assets to Total Debt Ratio. The company with high debt to

asset ratio are less flexible.

Since the total debt to asset ratio of the company is only 0.11 it is a low-risk company and hence has low level of

leverage.

Interest Coverage Ratios

This ratio measures the company’s ability to meet the interest payments which grow as the debt grows.

Usually, a company with an interest coverage ratio of 1.5 or less is viewed as unstable and may face a problem of loan

financing.

The Interest coverage ratio is very high in 2019 – 211.53 as the company has zero long term debts. This implies there

is minimal interest cost. (Anon., 2019)

Profitability Ratios

It is used to assess the ability of the company to generate profits and to meet the costs related to the generation of income.

Return on equity

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The formula for ROE is Net Profit after tax /Shareholders equity. Shareholders equity is capital paid by shareholders

plus retained earnings. Another formula is total liabilities – total assets.

ROE measures a company’s profitability against the profit it has kept for business. Hence a higher profit will lead to

higher ROE.

We can assess a company’s return on equity and compare it with the average of the industry. Saracen Mineral has

higher return on equity as compared to the industry (14%). Since the Return on equity is 18.76%, the company is able

to generate profits to the shareholders. Further the trend shows that the company’s Return on Equity has grown

significantly in last five years. It has touched 18 % from 4.86% in the year 2015. (Anon., 2015)

Earnings per Share

This ratio measures the amount earned by shareholders on the equity shares held by them. EPS of the company has

risen significantly from 3.26 in 2015 to 11.30 per share in 2019. (Anon., 2016)

Gross Margin Ratio

Gross margin ratio shows the mark up of the company above the cost of goods sold to sales. The company’s Gross

Margin ratio stands at 27.31 % in the year 2019. There has been a consistent increase in the gross margin ratio over the

years. In the year 2015 it was 10.62% and now it is above 27. This depicts company has increased sales and decreased

costs.

Net Profit ratio

The net profit ratio measures the ability of the company to generate profit after taxes. The company’s net profit ratio

for the years 2019 is 23.65% which shows an increase of over a percent from last year. There has been a consistent

increase in the net profit ratio over the years. In the year 2015 it was 6.48% and now it is above 23. This depicts

company has increased sales and other revenue and has cut down on inefficient costs. (Anon., 2019)

Return on Assets

The profitability of a company is assessed in relation to cost and expenses and is analyzed as compared to assets to see

whether the assets of the company are deployed effectively to generate sales and profits.

The more asset a company has amassed, the more sales and potentially more profit a company can generate. As at

higher levels, economies of scale set in, it helps to lower the costs and generate returns at higher rate than assets.

The Return on assets has declined in 2019 from 2018 to 19.30% (Anon., 2015)

Efficiency ratios

Efficiency ratios reveal to the investors about the ability of company to generate wealth for the stakeholders. It

primarily analyses how well the assets and liabilities of a company are managed. Efficiency ratios can measure the

general use of inventory and machinery, usage of equity, the repayment of liabilities and turnover of receivables and

payables.

Accounts Receivable Turnover

This ratio shows how effectively a company is collecting debts and extending. Generally, if the Accounts receivable

turnover ratio is high it shows that the business is efficient in collecting debts.

Saracen’s Accounts Receivable Turnover ratio is 136.91 which are on a higher side. Hence it is efficient and it can also

mean that the sales are more on a cash basis.

These are the assets which are current assets and current liabilities.

Inventory turnover ratio

This ratio measures how many times a company sold through its average inventory during a particular period. A higher

ratio shows that the company has high sales and is good at managing inventory. However, a low ratio indicates issues

such as overproduction, poor advertisement, and obsolete products.

Inventories are of three distinct type’s raw material, work in progress and the finished goods. The inventory ratio

includes all the three in the calculation of this.

The inventory turnover ratio of our company is 6.98 which have declined from 2018. However, in the last 5 years it has

grown from 3.76 in 2015 to 6.98 in 2019. (Anon., 2019)

Accounts Payable Turnover

10

plus retained earnings. Another formula is total liabilities – total assets.

ROE measures a company’s profitability against the profit it has kept for business. Hence a higher profit will lead to

higher ROE.

We can assess a company’s return on equity and compare it with the average of the industry. Saracen Mineral has

higher return on equity as compared to the industry (14%). Since the Return on equity is 18.76%, the company is able

to generate profits to the shareholders. Further the trend shows that the company’s Return on Equity has grown

significantly in last five years. It has touched 18 % from 4.86% in the year 2015. (Anon., 2015)

Earnings per Share

This ratio measures the amount earned by shareholders on the equity shares held by them. EPS of the company has

risen significantly from 3.26 in 2015 to 11.30 per share in 2019. (Anon., 2016)

Gross Margin Ratio

Gross margin ratio shows the mark up of the company above the cost of goods sold to sales. The company’s Gross

Margin ratio stands at 27.31 % in the year 2019. There has been a consistent increase in the gross margin ratio over the

years. In the year 2015 it was 10.62% and now it is above 27. This depicts company has increased sales and decreased

costs.

Net Profit ratio

The net profit ratio measures the ability of the company to generate profit after taxes. The company’s net profit ratio

for the years 2019 is 23.65% which shows an increase of over a percent from last year. There has been a consistent

increase in the net profit ratio over the years. In the year 2015 it was 6.48% and now it is above 23. This depicts

company has increased sales and other revenue and has cut down on inefficient costs. (Anon., 2019)

Return on Assets

The profitability of a company is assessed in relation to cost and expenses and is analyzed as compared to assets to see

whether the assets of the company are deployed effectively to generate sales and profits.

The more asset a company has amassed, the more sales and potentially more profit a company can generate. As at

higher levels, economies of scale set in, it helps to lower the costs and generate returns at higher rate than assets.

The Return on assets has declined in 2019 from 2018 to 19.30% (Anon., 2015)

Efficiency ratios

Efficiency ratios reveal to the investors about the ability of company to generate wealth for the stakeholders. It

primarily analyses how well the assets and liabilities of a company are managed. Efficiency ratios can measure the

general use of inventory and machinery, usage of equity, the repayment of liabilities and turnover of receivables and

payables.

Accounts Receivable Turnover

This ratio shows how effectively a company is collecting debts and extending. Generally, if the Accounts receivable

turnover ratio is high it shows that the business is efficient in collecting debts.

Saracen’s Accounts Receivable Turnover ratio is 136.91 which are on a higher side. Hence it is efficient and it can also

mean that the sales are more on a cash basis.

These are the assets which are current assets and current liabilities.

Inventory turnover ratio

This ratio measures how many times a company sold through its average inventory during a particular period. A higher

ratio shows that the company has high sales and is good at managing inventory. However, a low ratio indicates issues

such as overproduction, poor advertisement, and obsolete products.

Inventories are of three distinct type’s raw material, work in progress and the finished goods. The inventory ratio

includes all the three in the calculation of this.

The inventory turnover ratio of our company is 6.98 which have declined from 2018. However, in the last 5 years it has

grown from 3.76 in 2015 to 6.98 in 2019. (Anon., 2019)

Accounts Payable Turnover

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It evaluates how many times in a particular period a company pays off its trade creditors. It helps to assess the cash

situation.

A high ratio means the time gap is less between purchase and payment and lower ratio signifies that the company lags

in payment to the creditors.

The ratio of Saracen is 7.08 in 2019 and 8.90 in 2018. It has declined in the last two years which shows that the

company is lagging in payment and can also be a reason for high liquidity.

Total Asset Turnover Ratio

It measures the value of company’s sales in relation to the value of assets. It shows use of the company’s assets to

generate revenue. (Anon., 2015)

Higher Asset turnover ratio implies that the company is efficient. In our case, the ratio has declined from .98 to .82.

This means that assets are not used efficiently.

Fixed Asset Turnover ratio

This ratio compares the company’s fixed assets to its sales. Fixed assets are assets which provide benefit in operations

to the company for a long period of time. These are the assets which are of capital nature and they are used for earning

the regular incomes of the business.

It reflects the ability of company to put the long term resources in use.

This ratio has also declined to 1.11 from 2019 to 1.42 in 2018.

It was 1.31 in the year 2016. This means that the company is on a downward slope in utilizing the fixed assets.

Average collection and average payment period

The average collection period measures average no. of days between the credit sale and collection of such sale. It

shows the effectiveness of accounts and trade receivables management

A lower average collection period shows that the company is efficient in payment collection. However, a flip to this

side is that it may show that the credit terms are strict.

Saracen has average collection period 2.67 which has decreased drastically from 6.67. This shows that the company is

becoming more efficient in collecting debts. (Anon., 2019)

Average payment period shows a number of days a business takes to pay its suppliers.

As long as the payment period is in line with the peers, it should not affect the company. Payment period is a sensor

that tells us how well credit options utilized to pay short term debts.

The company has a very high payment period. It is 51.52 which show it is slow in paying off creditors. (Anon., 2019)

Analysis of Income Statement

figures in thousands 2019 2018 2017 2016 2015

Net Sales 555,59

1

510,96

1

423,05

8

276,50

2

249,87

2

Cost of sales 403,84

8

393,35

5

371,49

3

225,23

7

223,34

8

Gross profit 151,74

3

117,60

6

51,56

5

51,26

5

26,52

4

Other revenue

Selling, general and administrative expenses 15,35

8

12,11

8

12,01

0

11,41

5

8,03

1

Other expenses 63,61

3

10,36

0

9,53

2

10,36

3

6,82

7

Remuneration of directors 3,66

9

EBIT 131,99

4

114,13

5

33,74

2

39,19

1

17,22

0

Net Interest expense 62

4

41

1

76

4

85

6

1,03

9

11

situation.

A high ratio means the time gap is less between purchase and payment and lower ratio signifies that the company lags

in payment to the creditors.

The ratio of Saracen is 7.08 in 2019 and 8.90 in 2018. It has declined in the last two years which shows that the

company is lagging in payment and can also be a reason for high liquidity.

Total Asset Turnover Ratio

It measures the value of company’s sales in relation to the value of assets. It shows use of the company’s assets to

generate revenue. (Anon., 2015)

Higher Asset turnover ratio implies that the company is efficient. In our case, the ratio has declined from .98 to .82.

This means that assets are not used efficiently.

Fixed Asset Turnover ratio

This ratio compares the company’s fixed assets to its sales. Fixed assets are assets which provide benefit in operations

to the company for a long period of time. These are the assets which are of capital nature and they are used for earning

the regular incomes of the business.

It reflects the ability of company to put the long term resources in use.

This ratio has also declined to 1.11 from 2019 to 1.42 in 2018.

It was 1.31 in the year 2016. This means that the company is on a downward slope in utilizing the fixed assets.

Average collection and average payment period

The average collection period measures average no. of days between the credit sale and collection of such sale. It

shows the effectiveness of accounts and trade receivables management

A lower average collection period shows that the company is efficient in payment collection. However, a flip to this

side is that it may show that the credit terms are strict.

Saracen has average collection period 2.67 which has decreased drastically from 6.67. This shows that the company is

becoming more efficient in collecting debts. (Anon., 2019)

Average payment period shows a number of days a business takes to pay its suppliers.

As long as the payment period is in line with the peers, it should not affect the company. Payment period is a sensor

that tells us how well credit options utilized to pay short term debts.

The company has a very high payment period. It is 51.52 which show it is slow in paying off creditors. (Anon., 2019)

Analysis of Income Statement

figures in thousands 2019 2018 2017 2016 2015

Net Sales 555,59

1

510,96

1

423,05

8

276,50

2

249,87

2

Cost of sales 403,84

8

393,35

5

371,49

3

225,23

7

223,34

8

Gross profit 151,74

3

117,60

6

51,56

5

51,26

5

26,52

4

Other revenue

Selling, general and administrative expenses 15,35

8

12,11

8

12,01

0

11,41

5

8,03

1

Other expenses 63,61

3

10,36

0

9,53

2

10,36

3

6,82

7

Remuneration of directors 3,66

9

EBIT 131,99

4

114,13

5

33,74

2

39,19

1

17,22

0

Net Interest expense 62

4

41

1

76

4

85

6

1,03

9

11

EBT 131,37

0

113,72

4

32,97

8

38,33

5

16,18

1

Income tax paid 38,87

6

37,68

9

4,59

2

12,44

6

5,03

3

Earnings After-tax 92,49

4

76,03

5

28,38

6

25,88

9

11,14

8

The above-given statements are the actual data from the annual reports of the past five years of the Saracen Minerals Holding Ltd. The

income statement is calculated from the data given by the financials of the company.

The above given are the recommendations and comments over the businesses financial position and the financial statements of the

business and the activities of the business in the past five years and the reason behind the increased profits or losses that have occurred

in these last five years. Whenever the company’s position is to be discussed then the initial thing that is required is to discuss its

financial position and have a proper understanding of the financial statements. (Anon., 2019)

Valuation

The valuation is done to know the actual position of the business. (Jan, n.d.)

Using the free cash flow the valuation could be done of two distinct approaches-

1. The weighted average cost of capital

2. Cost of equity

The approach adopted here is related to the valuation of the cost of equity. The formula for this is-

Equity value = Total Business value – Market Value of debt

OR

Equity value= FCFE/ ke- g

Note the numbers here are in millions apart from the per-share values.

An estimate of the next two years: (Jan, n.d.)

2020 2021

$132.00 $153.12

Analyst

x2 Extrapolated @ (16%, capped from 18.43%)

$74.92 $75.43

The present value of next 5 years cash flows: $364

The terminal value would be calculated using the estimated figures of the coming years. The rate of government bond taken by us is at

the assumption of 2.6%. The growth rate is also taken at a discounted rate.

Value of the terminal

Value of terminal = FCF2021 × (1 + g) ÷ (Discount Rate – g)

= $153 × (1 + 2.6%) ÷ (15.2% – 2.6%)

The value of the terminal is based on the Perpetuity Method where the growth (g) = 2.6%: $1,246

Present value of terminal value: $614

Value of equity

Value of equity (Total value) = Present value 5 years cash flows + terminal value = $364 + $614 = $978

Value = Total value totally divided by the Shares Outstanding ($977.50 / 812.94)

Value per share: $1.2

Assumptions

The discount rate chosen is the cost of the equity of the Saracen Company. 15.2% is the figure used and the beta of the market is

assumed to be as 1.704.

12

0

113,72

4

32,97

8

38,33

5

16,18

1

Income tax paid 38,87

6

37,68

9

4,59

2

12,44

6

5,03

3

Earnings After-tax 92,49

4

76,03

5

28,38

6

25,88

9

11,14

8

The above-given statements are the actual data from the annual reports of the past five years of the Saracen Minerals Holding Ltd. The

income statement is calculated from the data given by the financials of the company.

The above given are the recommendations and comments over the businesses financial position and the financial statements of the

business and the activities of the business in the past five years and the reason behind the increased profits or losses that have occurred

in these last five years. Whenever the company’s position is to be discussed then the initial thing that is required is to discuss its

financial position and have a proper understanding of the financial statements. (Anon., 2019)

Valuation

The valuation is done to know the actual position of the business. (Jan, n.d.)

Using the free cash flow the valuation could be done of two distinct approaches-

1. The weighted average cost of capital

2. Cost of equity

The approach adopted here is related to the valuation of the cost of equity. The formula for this is-

Equity value = Total Business value – Market Value of debt

OR

Equity value= FCFE/ ke- g

Note the numbers here are in millions apart from the per-share values.

An estimate of the next two years: (Jan, n.d.)

2020 2021

$132.00 $153.12

Analyst

x2 Extrapolated @ (16%, capped from 18.43%)

$74.92 $75.43

The present value of next 5 years cash flows: $364

The terminal value would be calculated using the estimated figures of the coming years. The rate of government bond taken by us is at

the assumption of 2.6%. The growth rate is also taken at a discounted rate.

Value of the terminal

Value of terminal = FCF2021 × (1 + g) ÷ (Discount Rate – g)

= $153 × (1 + 2.6%) ÷ (15.2% – 2.6%)

The value of the terminal is based on the Perpetuity Method where the growth (g) = 2.6%: $1,246

Present value of terminal value: $614

Value of equity

Value of equity (Total value) = Present value 5 years cash flows + terminal value = $364 + $614 = $978

Value = Total value totally divided by the Shares Outstanding ($977.50 / 812.94)

Value per share: $1.2

Assumptions

The discount rate chosen is the cost of the equity of the Saracen Company. 15.2% is the figure used and the beta of the market is

assumed to be as 1.704.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.