Managerial Accounting: Analyzing SAS Company's Financial Statements

VerifiedAdded on 2023/06/11

|45

|6379

|358

Report

AI Summary

This assignment provides a comprehensive analysis of SAS Company's financial statements using managerial accounting principles and the PwC framework. It examines various elements reported in the annual reports, assessing their appropriateness and consistency with the framework. The analysis covers key areas such as strategies and objectives, business model, governance, risk management, remuneration, financial assets, physical assets, customers, people & culture, innovation, brands and intellectual assets, processes and supply chain, operational performance, economic performance, social impact, environmental considerations, and segmental reporting. Each element is evaluated based on report extracts, reporting critique, extensiveness and accessibility, comprehensiveness, and overall strength. The report aims to provide a thorough assessment of SAS Company's financial reporting practices and their alignment with the PwC Value Framework.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGERIAL ACCOUNTING

Executive Summary

The main purpose of the assignment is to analyze the different aspects of financial statements of

SAS company which is engaged in business of d. The different analysis will be graded on the

basis of good, bad and ugly policy. The reporting framework of PwC will be followed for the

purpose of establishing whether the financial reports which are prepared by SAS ltd is consistent

with the framework. In addition to this, the various elements which are reported in the annual

reports will be considered if the same are appropriately reported or not.

Table of Contents

MANAGERIAL ACCOUNTING

Executive Summary

The main purpose of the assignment is to analyze the different aspects of financial statements of

SAS company which is engaged in business of d. The different analysis will be graded on the

basis of good, bad and ugly policy. The reporting framework of PwC will be followed for the

purpose of establishing whether the financial reports which are prepared by SAS ltd is consistent

with the framework. In addition to this, the various elements which are reported in the annual

reports will be considered if the same are appropriately reported or not.

Table of Contents

2

MANAGERIAL ACCOUNTING

PwC Value Framework Elements....................................................................................................8

1. Value Framework Element: Strategies and Objectives............................................................8

Report Extracts:...........................................................................................................................8

Reporting Critique.......................................................................................................................8

Extensiveness and Accessibility..................................................................................................9

Comprehensiveness.....................................................................................................................9

Conclusion and Strength..............................................................................................................9

2. Value Framework Element: Business Model.........................................................................10

Report Extracts:.........................................................................................................................10

Reporting Critique.....................................................................................................................10

Extensiveness and Accessibility................................................................................................11

Comprehensiveness...................................................................................................................11

Conclusion and Strength............................................................................................................11

3. Value Framework Element: Governance...............................................................................11

Report Extracts:.........................................................................................................................11

Reporting Critique.....................................................................................................................12

Extensiveness and Accessibility................................................................................................13

Comprehensiveness...................................................................................................................13

Conclusion and Strength............................................................................................................13

4. Value Framework Element: Risk Management.....................................................................14

MANAGERIAL ACCOUNTING

PwC Value Framework Elements....................................................................................................8

1. Value Framework Element: Strategies and Objectives............................................................8

Report Extracts:...........................................................................................................................8

Reporting Critique.......................................................................................................................8

Extensiveness and Accessibility..................................................................................................9

Comprehensiveness.....................................................................................................................9

Conclusion and Strength..............................................................................................................9

2. Value Framework Element: Business Model.........................................................................10

Report Extracts:.........................................................................................................................10

Reporting Critique.....................................................................................................................10

Extensiveness and Accessibility................................................................................................11

Comprehensiveness...................................................................................................................11

Conclusion and Strength............................................................................................................11

3. Value Framework Element: Governance...............................................................................11

Report Extracts:.........................................................................................................................11

Reporting Critique.....................................................................................................................12

Extensiveness and Accessibility................................................................................................13

Comprehensiveness...................................................................................................................13

Conclusion and Strength............................................................................................................13

4. Value Framework Element: Risk Management.....................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGERIAL ACCOUNTING

Report Extracts:.........................................................................................................................14

Reporting Critique.....................................................................................................................15

Extensiveness and Accessibility................................................................................................15

Comprehensiveness...................................................................................................................15

Conclusion and Strength............................................................................................................16

5. Value Framework Element: Remuneration............................................................................16

Report Extracts:.........................................................................................................................16

Reporting Critique.....................................................................................................................17

Extensiveness and Accessibility................................................................................................18

Comprehensiveness...................................................................................................................18

Conclusion and Strength............................................................................................................19

6. Value Framework Element: Financial Assets........................................................................19

Report Extracts:.........................................................................................................................19

Reporting Critique.....................................................................................................................20

Extensiveness and Accessibility................................................................................................20

Comprehensiveness...................................................................................................................20

Conclusion and Strength............................................................................................................20

7. Value Framework Element: Physical Assets..........................................................................21

Report Extracts:.........................................................................................................................21

Reporting Critique.....................................................................................................................22

MANAGERIAL ACCOUNTING

Report Extracts:.........................................................................................................................14

Reporting Critique.....................................................................................................................15

Extensiveness and Accessibility................................................................................................15

Comprehensiveness...................................................................................................................15

Conclusion and Strength............................................................................................................16

5. Value Framework Element: Remuneration............................................................................16

Report Extracts:.........................................................................................................................16

Reporting Critique.....................................................................................................................17

Extensiveness and Accessibility................................................................................................18

Comprehensiveness...................................................................................................................18

Conclusion and Strength............................................................................................................19

6. Value Framework Element: Financial Assets........................................................................19

Report Extracts:.........................................................................................................................19

Reporting Critique.....................................................................................................................20

Extensiveness and Accessibility................................................................................................20

Comprehensiveness...................................................................................................................20

Conclusion and Strength............................................................................................................20

7. Value Framework Element: Physical Assets..........................................................................21

Report Extracts:.........................................................................................................................21

Reporting Critique.....................................................................................................................22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGERIAL ACCOUNTING

Extensiveness and Accessibility................................................................................................23

Comprehensiveness...................................................................................................................23

Conclusion and Strength............................................................................................................23

8. Value Framework Element: Customers.................................................................................24

Report Extracts:.........................................................................................................................24

Reporting Critique.....................................................................................................................25

Extensiveness and Accessibility................................................................................................25

Comprehensiveness...................................................................................................................25

Conclusion and Strength............................................................................................................25

9. Value Framework Element: People & Culture.......................................................................26

Report Extracts:.........................................................................................................................26

Reporting Critique.....................................................................................................................26

Extensiveness and Accessibility................................................................................................26

Comprehensiveness...................................................................................................................27

Conclusion and Strength............................................................................................................27

10. Value Framework Element: Innovation G&S....................................................................28

Report Extracts:.........................................................................................................................28

Reporting Critique.....................................................................................................................28

Extensiveness and Accessibility................................................................................................28

Comprehensiveness...................................................................................................................28

MANAGERIAL ACCOUNTING

Extensiveness and Accessibility................................................................................................23

Comprehensiveness...................................................................................................................23

Conclusion and Strength............................................................................................................23

8. Value Framework Element: Customers.................................................................................24

Report Extracts:.........................................................................................................................24

Reporting Critique.....................................................................................................................25

Extensiveness and Accessibility................................................................................................25

Comprehensiveness...................................................................................................................25

Conclusion and Strength............................................................................................................25

9. Value Framework Element: People & Culture.......................................................................26

Report Extracts:.........................................................................................................................26

Reporting Critique.....................................................................................................................26

Extensiveness and Accessibility................................................................................................26

Comprehensiveness...................................................................................................................27

Conclusion and Strength............................................................................................................27

10. Value Framework Element: Innovation G&S....................................................................28

Report Extracts:.........................................................................................................................28

Reporting Critique.....................................................................................................................28

Extensiveness and Accessibility................................................................................................28

Comprehensiveness...................................................................................................................28

5

MANAGERIAL ACCOUNTING

Conclusion and Strength............................................................................................................29

11. Value Framework Element: Brands and Intellectual Assets..............................................29

Report Extracts:.........................................................................................................................29

Reporting Critique.....................................................................................................................29

Extensiveness and Accessibility................................................................................................29

Comprehensiveness...................................................................................................................30

Conclusion and Strength............................................................................................................30

12. Value Framework Element: Processes and Supply Chain..................................................30

Report Extracts:.........................................................................................................................30

Reporting Critique.....................................................................................................................31

Extensiveness and Accessibility................................................................................................31

Comprehensiveness...................................................................................................................32

Conclusion and Strength............................................................................................................32

13. Value Framework Element: Operational Performance.......................................................32

Report Extracts:.........................................................................................................................32

Reporting Critique.....................................................................................................................33

Extensiveness and Accessibility................................................................................................33

Comprehensiveness...................................................................................................................34

Conclusion and Strength............................................................................................................34

14. Value Framework Element: Economic Performance.........................................................34

MANAGERIAL ACCOUNTING

Conclusion and Strength............................................................................................................29

11. Value Framework Element: Brands and Intellectual Assets..............................................29

Report Extracts:.........................................................................................................................29

Reporting Critique.....................................................................................................................29

Extensiveness and Accessibility................................................................................................29

Comprehensiveness...................................................................................................................30

Conclusion and Strength............................................................................................................30

12. Value Framework Element: Processes and Supply Chain..................................................30

Report Extracts:.........................................................................................................................30

Reporting Critique.....................................................................................................................31

Extensiveness and Accessibility................................................................................................31

Comprehensiveness...................................................................................................................32

Conclusion and Strength............................................................................................................32

13. Value Framework Element: Operational Performance.......................................................32

Report Extracts:.........................................................................................................................32

Reporting Critique.....................................................................................................................33

Extensiveness and Accessibility................................................................................................33

Comprehensiveness...................................................................................................................34

Conclusion and Strength............................................................................................................34

14. Value Framework Element: Economic Performance.........................................................34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGERIAL ACCOUNTING

Report Extracts:.........................................................................................................................34

Reporting Critique.....................................................................................................................35

Extensiveness and Accessibility................................................................................................35

Comprehensiveness...................................................................................................................36

Conclusion and Strength............................................................................................................36

15. Value Framework Element: Social.....................................................................................36

Report Extracts:.........................................................................................................................36

Reporting Critique.....................................................................................................................37

Extensiveness and Accessibility................................................................................................37

Comprehensiveness...................................................................................................................37

Conclusion and Strength............................................................................................................37

16. Value Framework Element: Environmental.......................................................................38

Report Extracts:.........................................................................................................................38

Reporting Critique.....................................................................................................................38

Extensiveness and Accessibility................................................................................................38

Comprehensiveness...................................................................................................................38

Conclusion and Strength............................................................................................................39

17. Value Framework Element: Segmental..............................................................................39

Report Extracts:.........................................................................................................................39

Reporting Critique.....................................................................................................................40

MANAGERIAL ACCOUNTING

Report Extracts:.........................................................................................................................34

Reporting Critique.....................................................................................................................35

Extensiveness and Accessibility................................................................................................35

Comprehensiveness...................................................................................................................36

Conclusion and Strength............................................................................................................36

15. Value Framework Element: Social.....................................................................................36

Report Extracts:.........................................................................................................................36

Reporting Critique.....................................................................................................................37

Extensiveness and Accessibility................................................................................................37

Comprehensiveness...................................................................................................................37

Conclusion and Strength............................................................................................................37

16. Value Framework Element: Environmental.......................................................................38

Report Extracts:.........................................................................................................................38

Reporting Critique.....................................................................................................................38

Extensiveness and Accessibility................................................................................................38

Comprehensiveness...................................................................................................................38

Conclusion and Strength............................................................................................................39

17. Value Framework Element: Segmental..............................................................................39

Report Extracts:.........................................................................................................................39

Reporting Critique.....................................................................................................................40

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL ACCOUNTING

Extensiveness and Accessibility................................................................................................40

Comprehensiveness...................................................................................................................40

Conclusion and Strength............................................................................................................41

Reference.......................................................................................................................................42

MANAGERIAL ACCOUNTING

Extensiveness and Accessibility................................................................................................40

Comprehensiveness...................................................................................................................40

Conclusion and Strength............................................................................................................41

Reference.......................................................................................................................................42

8

MANAGERIAL ACCOUNTING

PwC Value Framework Elements

1. Value Framework Element: Strategies and Objectives

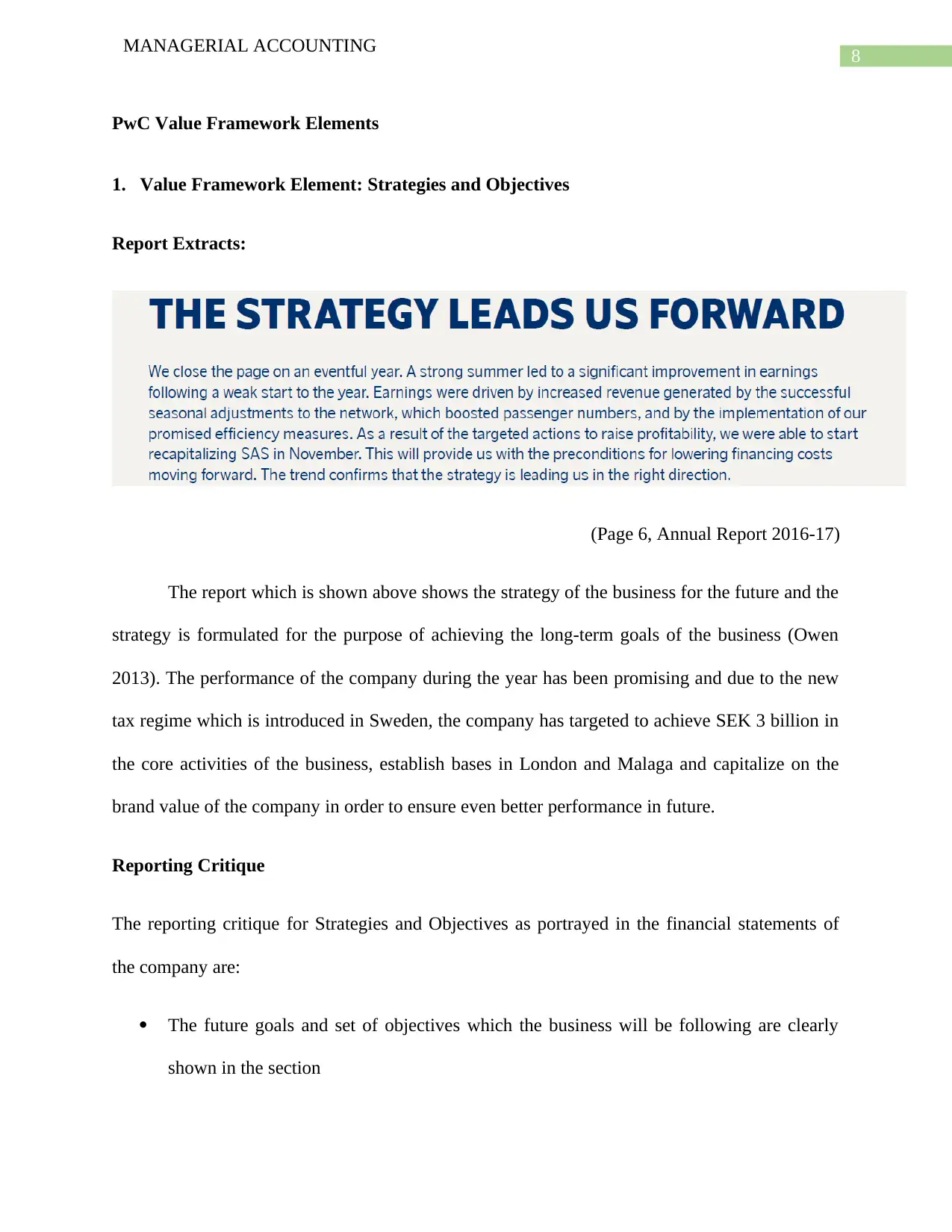

Report Extracts:

(Page 6, Annual Report 2016-17)

The report which is shown above shows the strategy of the business for the future and the

strategy is formulated for the purpose of achieving the long-term goals of the business (Owen

2013). The performance of the company during the year has been promising and due to the new

tax regime which is introduced in Sweden, the company has targeted to achieve SEK 3 billion in

the core activities of the business, establish bases in London and Malaga and capitalize on the

brand value of the company in order to ensure even better performance in future.

Reporting Critique

The reporting critique for Strategies and Objectives as portrayed in the financial statements of

the company are:

The future goals and set of objectives which the business will be following are clearly

shown in the section

MANAGERIAL ACCOUNTING

PwC Value Framework Elements

1. Value Framework Element: Strategies and Objectives

Report Extracts:

(Page 6, Annual Report 2016-17)

The report which is shown above shows the strategy of the business for the future and the

strategy is formulated for the purpose of achieving the long-term goals of the business (Owen

2013). The performance of the company during the year has been promising and due to the new

tax regime which is introduced in Sweden, the company has targeted to achieve SEK 3 billion in

the core activities of the business, establish bases in London and Malaga and capitalize on the

brand value of the company in order to ensure even better performance in future.

Reporting Critique

The reporting critique for Strategies and Objectives as portrayed in the financial statements of

the company are:

The future goals and set of objectives which the business will be following are clearly

shown in the section

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGERIAL ACCOUNTING

In addition to this, the goals are also segregated on the basis of how much it is anticipated

that the business will be achieving such goals that is by 2019 or 2020.

Extensiveness and Accessibility

The strategy which is followed by SAS Ltd are easily made available from the financial

reports as the same is provided ion the initial pages of the report that is om page 6. The strategies

are extensively explained in the President’s letter informing the stakeholders about the

performance of the business. Further on Page 12 of the annual report strategies which makes the

business successful are provided. The strategies also include the future expectations of the

business which is provided in page 6.

Comprehensiveness

The president’s letter which is shown in page 6, the over all performance of the business

and also the future perspective of the business are set out effectively on the basis of Improved

Customers Offerings by the company, Enhancing the Efficiency program, Sustainable Aviation

and building up a strong financial position for the business in the market.

Conclusion and Strength

As per the strategies set by SAS ltd and the effective pursuance of the same resulted in

enhanced efficiency of the business. In addition to this, the strategies focus mainly on medium

term and long terms plans as shown the target time period is 2020 in most cases. Therefore, it

can be said that the quality of strategies and objective of the business is ‘good’

.

MANAGERIAL ACCOUNTING

In addition to this, the goals are also segregated on the basis of how much it is anticipated

that the business will be achieving such goals that is by 2019 or 2020.

Extensiveness and Accessibility

The strategy which is followed by SAS Ltd are easily made available from the financial

reports as the same is provided ion the initial pages of the report that is om page 6. The strategies

are extensively explained in the President’s letter informing the stakeholders about the

performance of the business. Further on Page 12 of the annual report strategies which makes the

business successful are provided. The strategies also include the future expectations of the

business which is provided in page 6.

Comprehensiveness

The president’s letter which is shown in page 6, the over all performance of the business

and also the future perspective of the business are set out effectively on the basis of Improved

Customers Offerings by the company, Enhancing the Efficiency program, Sustainable Aviation

and building up a strong financial position for the business in the market.

Conclusion and Strength

As per the strategies set by SAS ltd and the effective pursuance of the same resulted in

enhanced efficiency of the business. In addition to this, the strategies focus mainly on medium

term and long terms plans as shown the target time period is 2020 in most cases. Therefore, it

can be said that the quality of strategies and objective of the business is ‘good’

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGERIAL ACCOUNTING

2. Value Framework Element: Business Model

Report Extracts:

(Page 8, Annual Report 2016-17)

Reporting Critique

The report critique of the business model of business model of the company are:

The extract provides a clear view as to how SAS creates value and what are the activities

which the business engages in for the purpose of creating value.

MANAGERIAL ACCOUNTING

2. Value Framework Element: Business Model

Report Extracts:

(Page 8, Annual Report 2016-17)

Reporting Critique

The report critique of the business model of business model of the company are:

The extract provides a clear view as to how SAS creates value and what are the activities

which the business engages in for the purpose of creating value.

11

MANAGERIAL ACCOUNTING

Extensiveness and Accessibility

The presentation of the business model of the company is effectively shown in Table

form which is quite easy to understand and the accessibility is also effective as the it is presented

in the initial pages of the annual report specifically page 8 which deals with the value creation

model of the business. In addition to this, the annual report also looks promising to provide

further information of the value creation activities of the business in later pages of the report.

Comprehensiveness

The business model of SAS ltd is based on a broad network for effective departure to,

from and within the country in which the business operates. The company offers a variety of

choices in terms of products which are related to business travels, leisure travel. The business

rewards the customers of the business through the EuroBonus programs. The performance

elements of the business are effectively depicted in the business model and the page also shows

different types of capital which is utilized by the business.

Conclusion and Strength

As per the analysis of the Business model of SAS ltd, it is clearly seen that the

management of the company is crystal clear on the activities which the business needs to engage

in for the purpose of attaining the business goals. The quality of the reporting of business model

is ‘good’.

MANAGERIAL ACCOUNTING

Extensiveness and Accessibility

The presentation of the business model of the company is effectively shown in Table

form which is quite easy to understand and the accessibility is also effective as the it is presented

in the initial pages of the annual report specifically page 8 which deals with the value creation

model of the business. In addition to this, the annual report also looks promising to provide

further information of the value creation activities of the business in later pages of the report.

Comprehensiveness

The business model of SAS ltd is based on a broad network for effective departure to,

from and within the country in which the business operates. The company offers a variety of

choices in terms of products which are related to business travels, leisure travel. The business

rewards the customers of the business through the EuroBonus programs. The performance

elements of the business are effectively depicted in the business model and the page also shows

different types of capital which is utilized by the business.

Conclusion and Strength

As per the analysis of the Business model of SAS ltd, it is clearly seen that the

management of the company is crystal clear on the activities which the business needs to engage

in for the purpose of attaining the business goals. The quality of the reporting of business model

is ‘good’.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 45

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.