Finance Report: Saturn Group Global Investment Analysis

VerifiedAdded on 2020/10/22

|14

|2921

|214

Report

AI Summary

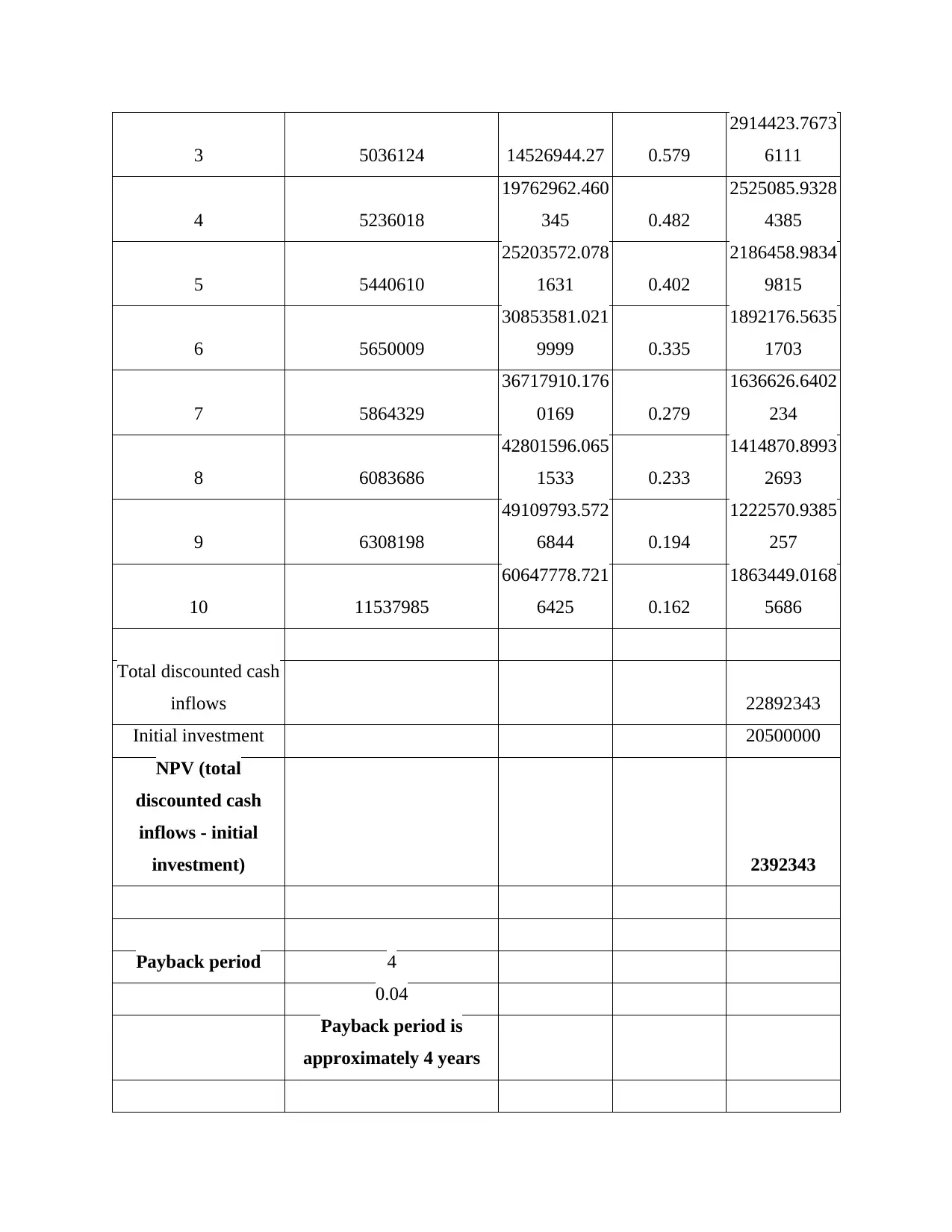

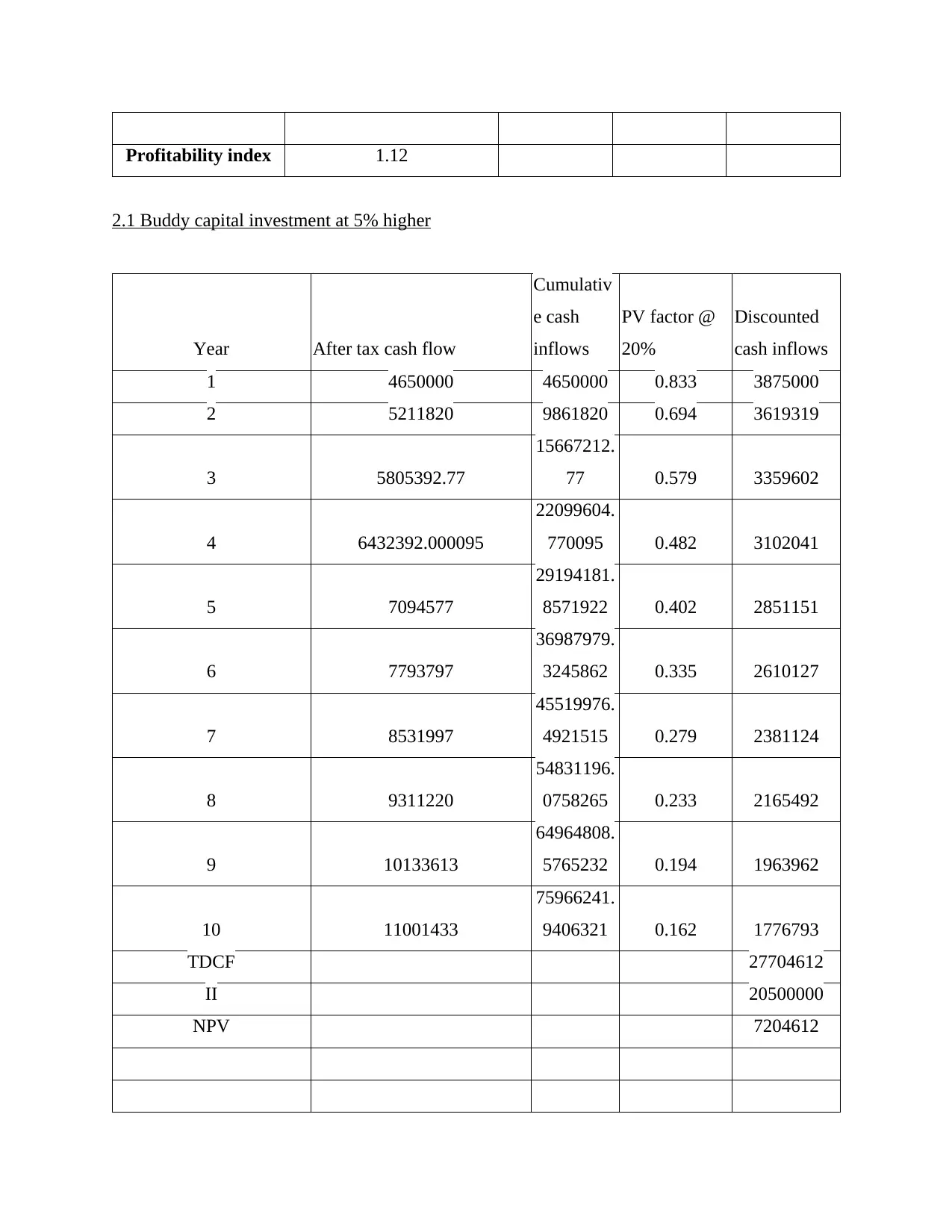

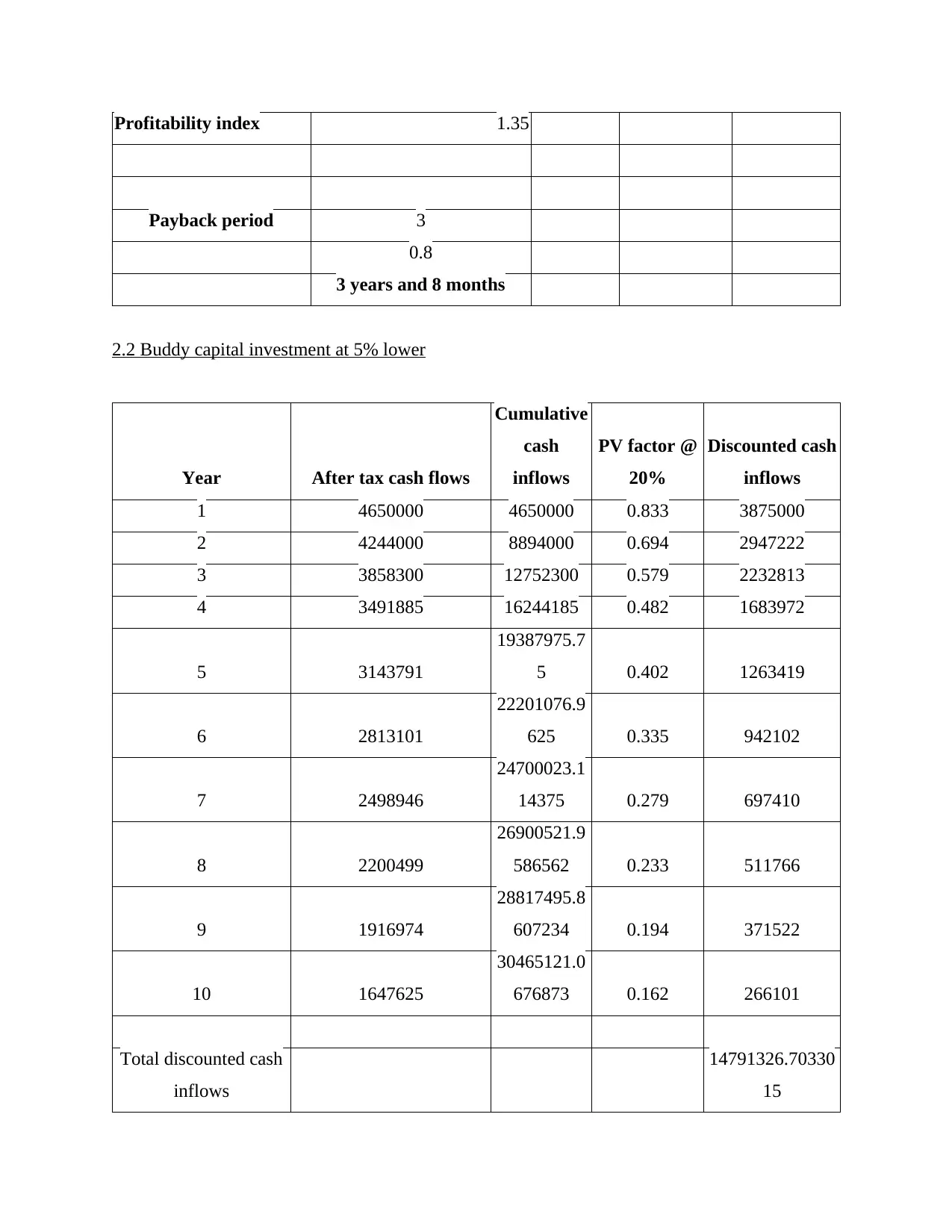

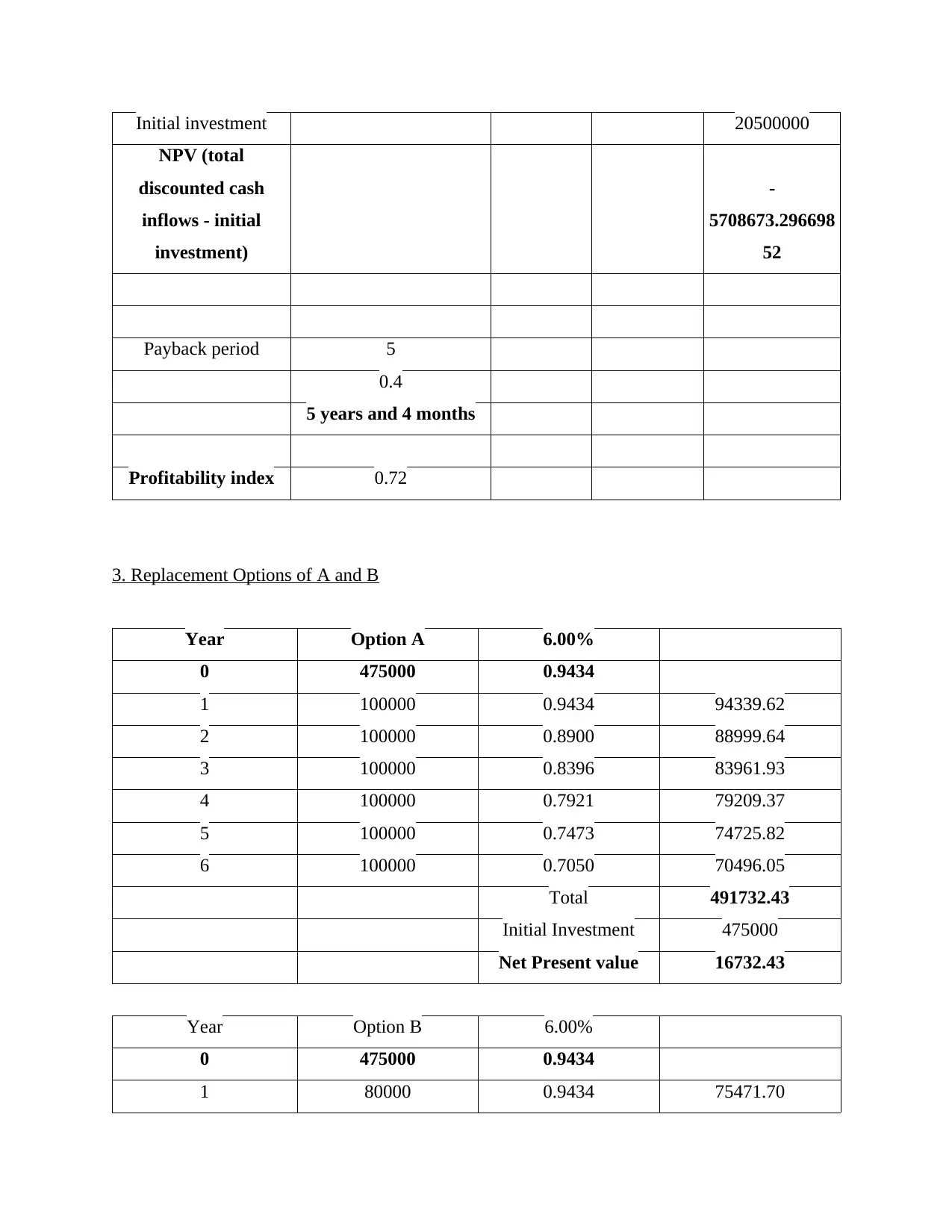

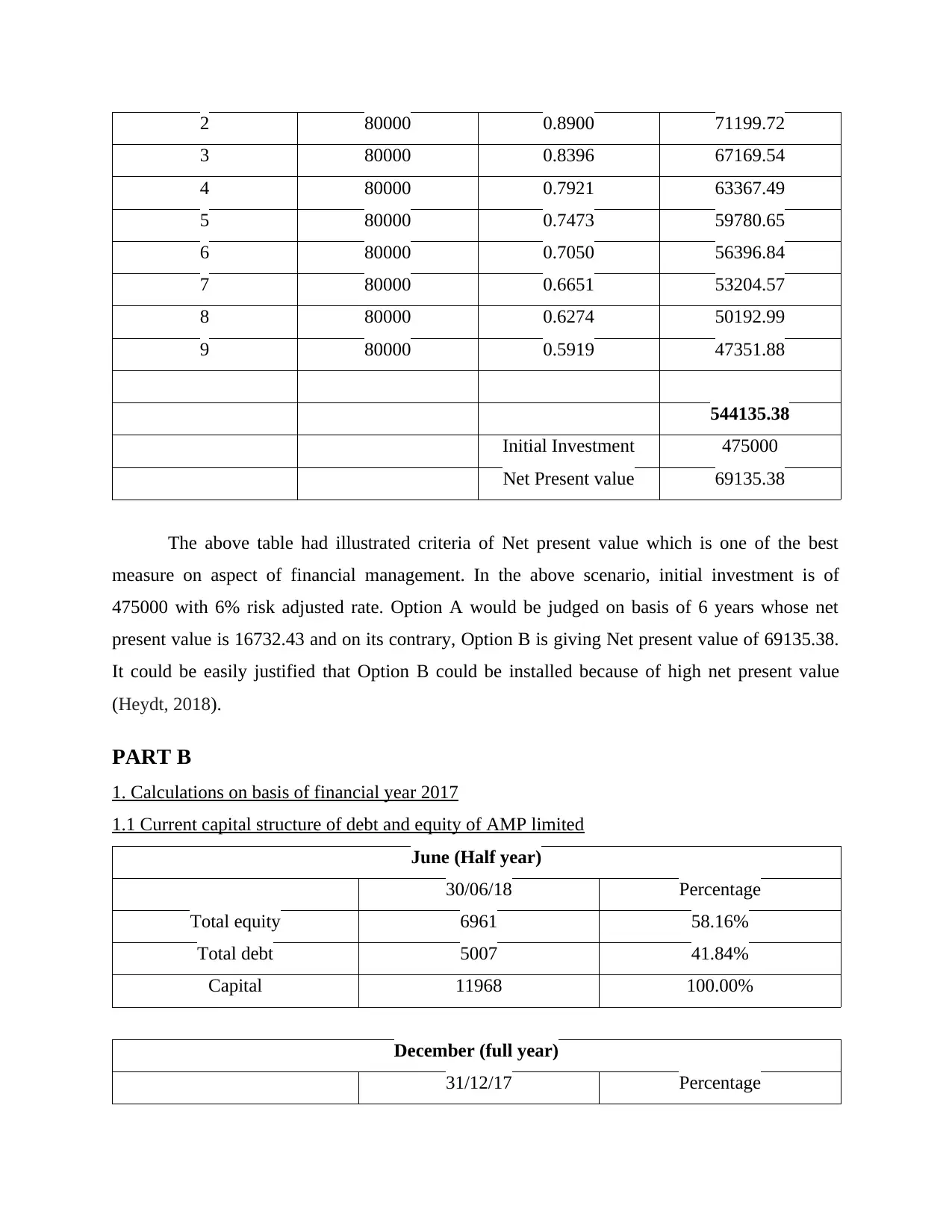

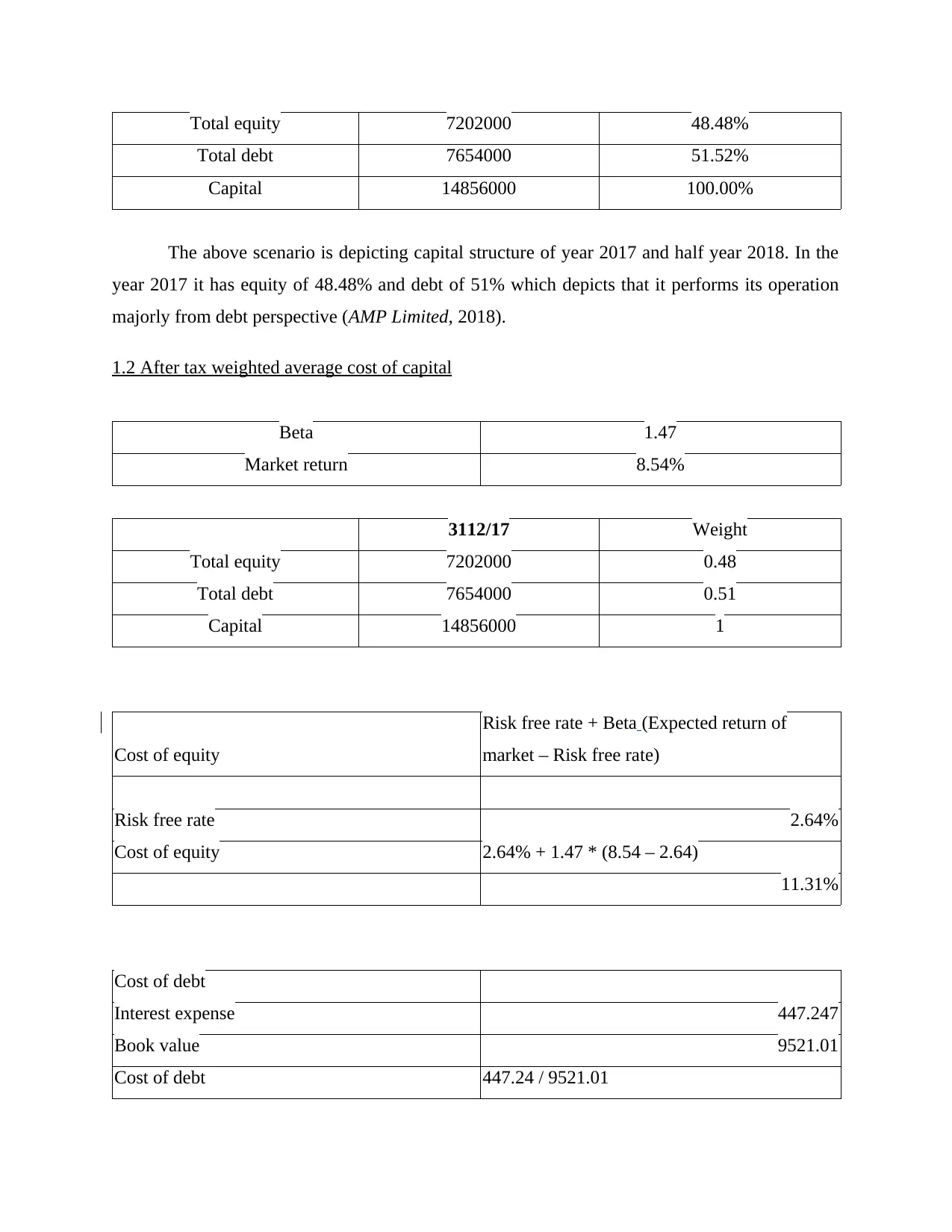

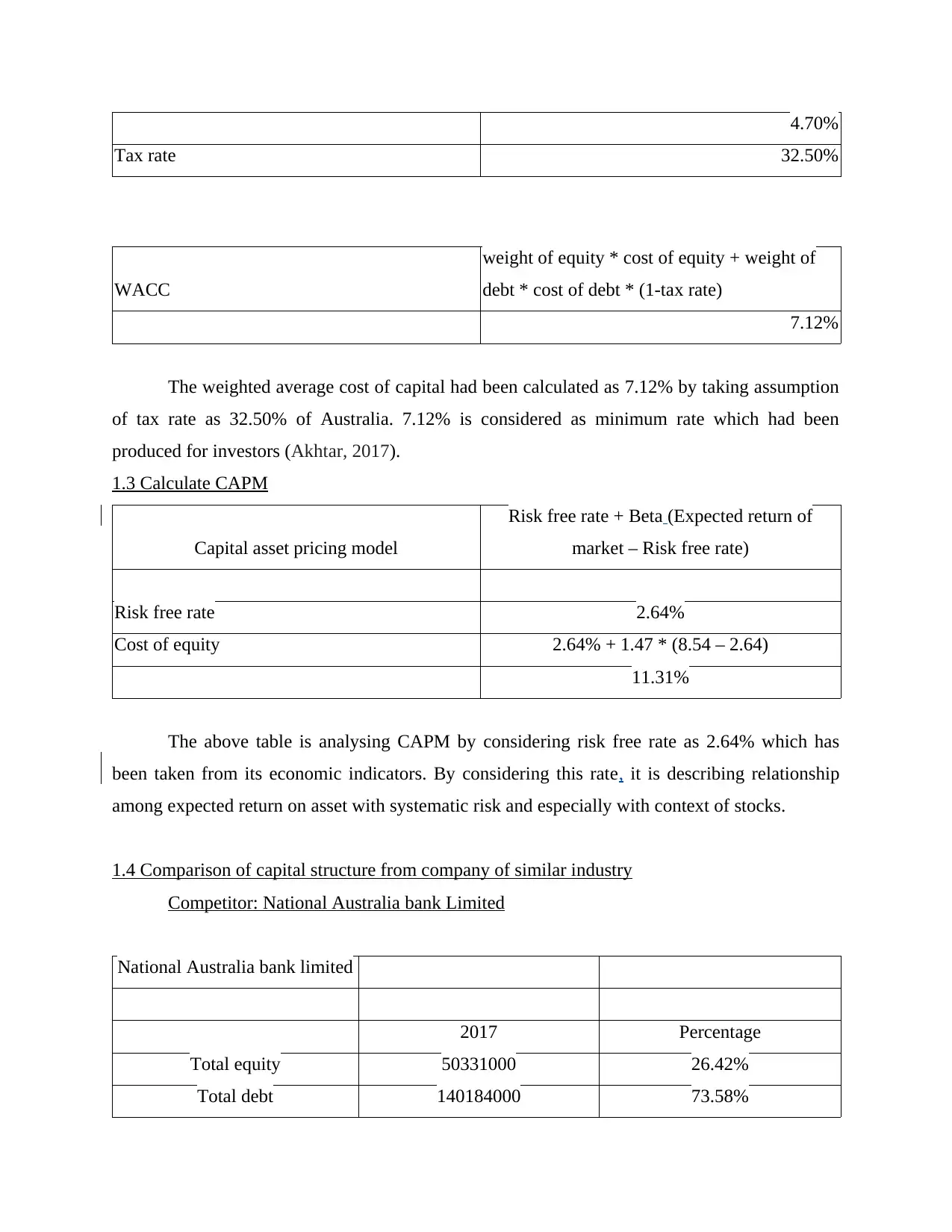

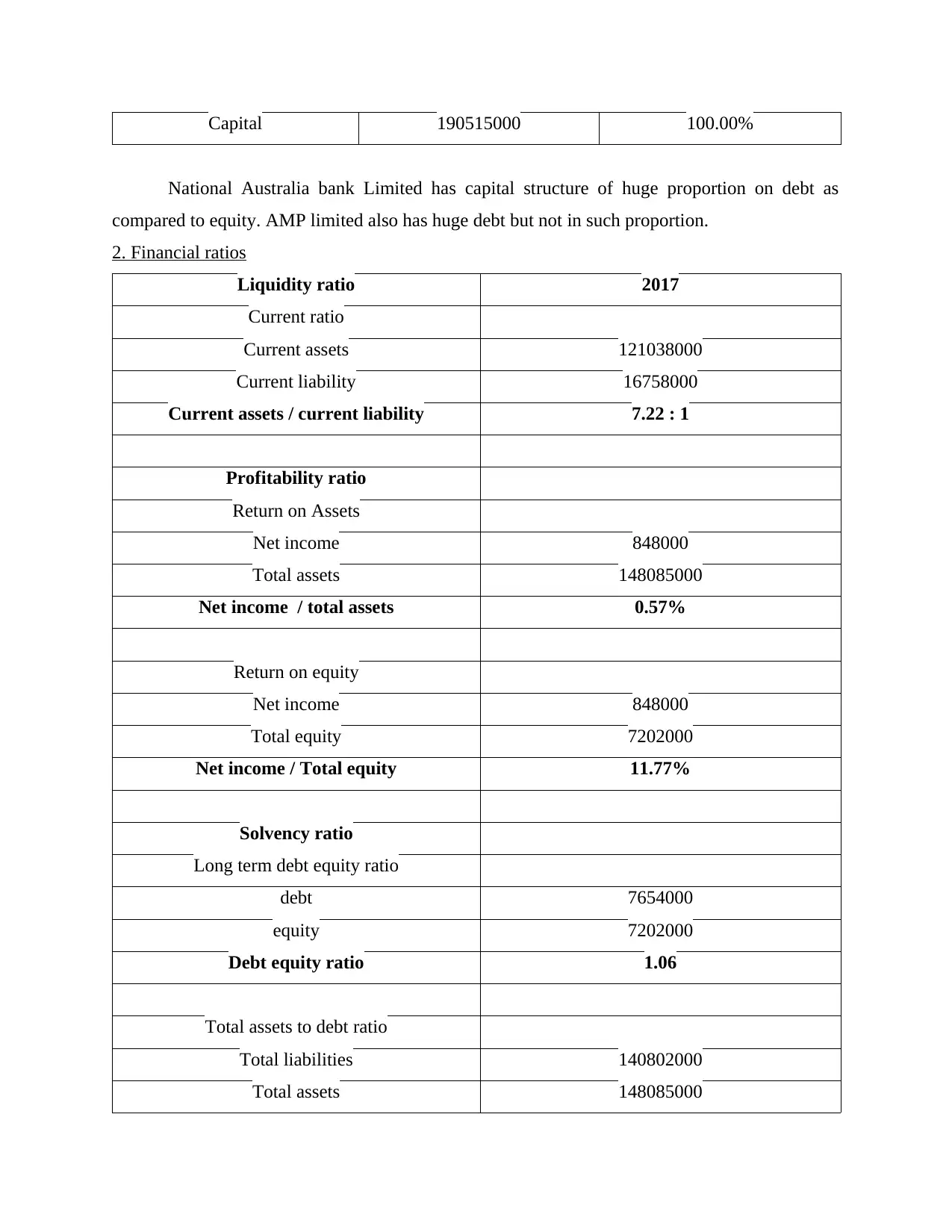

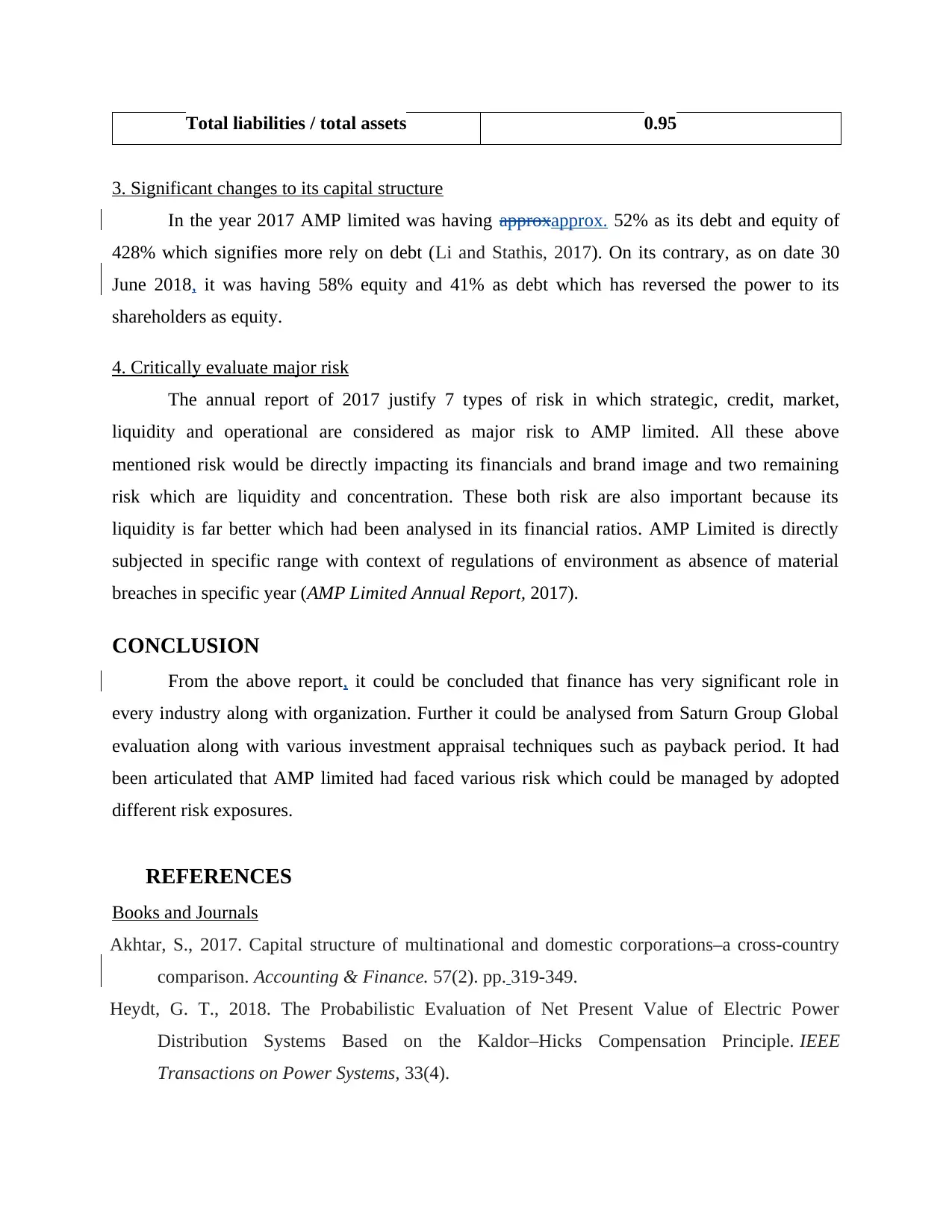

This report presents a detailed financial analysis of Saturn Group Global, examining various investment parameters such as after-tax cash flows, net present value, profitability index, and payback period to assess investment viability. The report delves into the capital structure of AMP Limited, calculating the after-tax weighted average cost of capital (WACC) and CAPM, and comparing it to industry peers. Financial ratios are computed and analyzed, along with a discussion of significant capital structure changes and major risks faced by AMP Limited. The analysis includes calculations for investment options with varying cash flows, incorporating depreciation and illustrating the impact of different investment scenarios. The report concludes with an evaluation of investment options and the importance of financial management principles. It provides insights into financial decision-making, risk management, and the impact of financial metrics on investment choices.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.