Sayaji Hotels Ltd. Financial Performance Analysis Report (2018-2019)

VerifiedAdded on 2021/08/03

|12

|2759

|181

Report

AI Summary

This report presents a financial analysis of Sayaji Hotels Ltd., a prominent India-based hospitality company, using the 2019 annual report for comparison with 2018 data. The methodology employs ratio analysis, including liquidity (current, quick, cash), profitability (gross profit, net profit, return on asset), investor (return on investment, return on capital employed, return on equity), solvency (debt-asset, debt-equity), and activity ratios (working capital turnover, asset turnover). The analysis reveals a mixed performance: while some ratios show improvement, the company's overall financial health remains a concern, particularly regarding liquidity and profitability. The report concludes that Sayaji Hotels Ltd. has shown some financial improvement from the previous year, but has not shown drastic changes in profit or revenue. The findings highlight areas for potential improvement and strategic considerations for the company's financial management.

I. Introduction

Coming out as one of the top India-based hospitality company, Sayaji Hotels Ltd. was

assimilated in April 1982 and commenced in the year 1987 under the direction of Mr Sajid R.

Dhanani. Starting off with the first hotel in Vadodara, followed by properties in other cities

such as Indore, Pune, Bhopal, Kolhapur, Raipur and Gurugram. With more upcoming

properties in Bhopal and Zirakpur, Sayaji Hotel Ltd has four sub-brands under its name,

namely, Enrise by Sayaji, which is a full service, mid- scale and upscale resorts. Their target

market is Leisure travellers who want comfort luxury at an affordable price. Effotel by Sayaji

on the other hand is a four star and upscale business hotel. Sayaji Hotels provide full service

five star luxury experience and services. Lastly, Barbeque Nations restaurant became of the

leading casual dining chain in India is under Sayaji Hotel Ltd. With 10 hotels, 28 restaurants

and 8000+ employees, Sayaji Hotel Ltd. is emerging as a pioneer in Indian Hospitality

Brands. Sayaji Hotel Ltd. has also been awarded with The Economic Times ‘India’s Best

Companies to Work For’ in 2018 and 2019.

II. Methodology

To understand and analyse the financial feasibility of the company taken, the annual report of

Sayaji Hotel Ltd. for 2019 was taken from the official website of the company. The report

was for year ending March 2019 and year ending March 2018 that were used for horizontal

comparison analysis. The financial statements used were as follows:

1) Balance Sheet

2) Statement of Profit & Loss for the year

3) Cash Flow Statement for the year

III. Discussion and Analysis

The tool which is used for the comparison is Ratio Analysis, under which five ratios were

used, namely:

Liquidity Ratio

Profitability Ratio

Investors Ratio

Solvency Ratio

Coming out as one of the top India-based hospitality company, Sayaji Hotels Ltd. was

assimilated in April 1982 and commenced in the year 1987 under the direction of Mr Sajid R.

Dhanani. Starting off with the first hotel in Vadodara, followed by properties in other cities

such as Indore, Pune, Bhopal, Kolhapur, Raipur and Gurugram. With more upcoming

properties in Bhopal and Zirakpur, Sayaji Hotel Ltd has four sub-brands under its name,

namely, Enrise by Sayaji, which is a full service, mid- scale and upscale resorts. Their target

market is Leisure travellers who want comfort luxury at an affordable price. Effotel by Sayaji

on the other hand is a four star and upscale business hotel. Sayaji Hotels provide full service

five star luxury experience and services. Lastly, Barbeque Nations restaurant became of the

leading casual dining chain in India is under Sayaji Hotel Ltd. With 10 hotels, 28 restaurants

and 8000+ employees, Sayaji Hotel Ltd. is emerging as a pioneer in Indian Hospitality

Brands. Sayaji Hotel Ltd. has also been awarded with The Economic Times ‘India’s Best

Companies to Work For’ in 2018 and 2019.

II. Methodology

To understand and analyse the financial feasibility of the company taken, the annual report of

Sayaji Hotel Ltd. for 2019 was taken from the official website of the company. The report

was for year ending March 2019 and year ending March 2018 that were used for horizontal

comparison analysis. The financial statements used were as follows:

1) Balance Sheet

2) Statement of Profit & Loss for the year

3) Cash Flow Statement for the year

III. Discussion and Analysis

The tool which is used for the comparison is Ratio Analysis, under which five ratios were

used, namely:

Liquidity Ratio

Profitability Ratio

Investors Ratio

Solvency Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Ratio

1. Liquidity

When a company is falling short to pay off their short term liabilities, they convert the

already available assets into cash quickly and cheaply. This comprises of companies

capability to quickly sell their assets to raise cash. To analyse and calculate the liquidity ratio,

the following ratios were used: Current Ratio, Quick Ratio and Cash Ratio.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Current Ratio

Current Assets

Current Liabilities

5,116.50 4,783.67

6,876.40 5,155.84

0.74:1 0.92:1

Interpretation: Current Ratio, also referred as Working Capital Ratio, helps in analysis and

comparison of current assets with current liabilities which infers us to understand if the

available current assets (which can be converted into cash within a year) are adequate to

settle the current liabilities (Which needs to be paid off within a year). In the above work

note, a decrease 0.18 in the current ratio is seen. For hospitality companies ratio of 1.5 is

considered good and safe i.e. the available current assets are enough to settle the liabilities. In

case of Sayaji Hotels Ltd., the ratio shows that in 2019 the ratio decreased drastically.

1. Liquidity

When a company is falling short to pay off their short term liabilities, they convert the

already available assets into cash quickly and cheaply. This comprises of companies

capability to quickly sell their assets to raise cash. To analyse and calculate the liquidity ratio,

the following ratios were used: Current Ratio, Quick Ratio and Cash Ratio.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Current Ratio

Current Assets

Current Liabilities

5,116.50 4,783.67

6,876.40 5,155.84

0.74:1 0.92:1

Interpretation: Current Ratio, also referred as Working Capital Ratio, helps in analysis and

comparison of current assets with current liabilities which infers us to understand if the

available current assets (which can be converted into cash within a year) are adequate to

settle the current liabilities (Which needs to be paid off within a year). In the above work

note, a decrease 0.18 in the current ratio is seen. For hospitality companies ratio of 1.5 is

considered good and safe i.e. the available current assets are enough to settle the liabilities. In

case of Sayaji Hotels Ltd., the ratio shows that in 2019 the ratio decreased drastically.

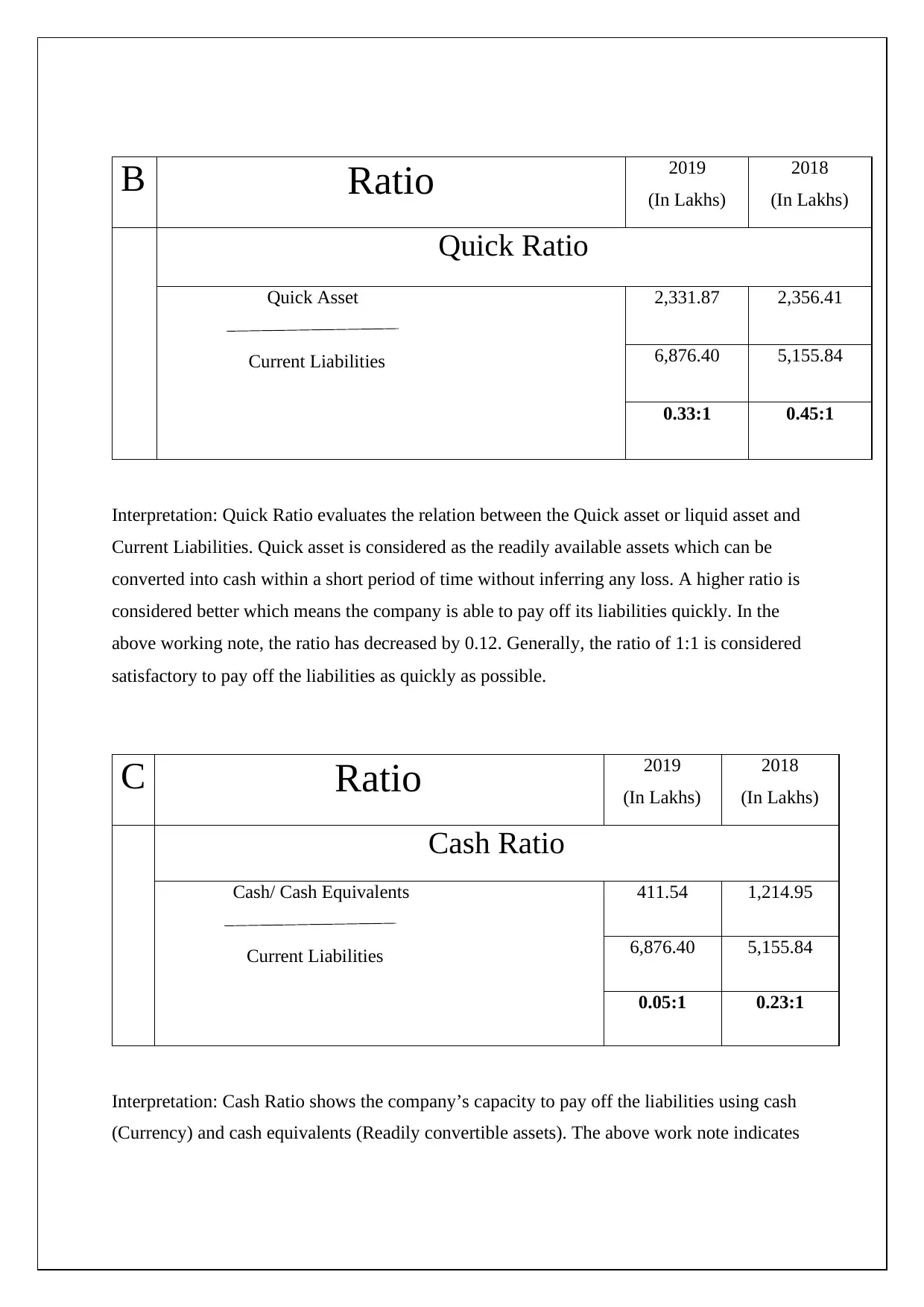

B Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Quick Ratio

Quick Asset

Current Liabilities

2,331.87 2,356.41

6,876.40 5,155.84

0.33:1 0.45:1

Interpretation: Quick Ratio evaluates the relation between the Quick asset or liquid asset and

Current Liabilities. Quick asset is considered as the readily available assets which can be

converted into cash within a short period of time without inferring any loss. A higher ratio is

considered better which means the company is able to pay off its liabilities quickly. In the

above working note, the ratio has decreased by 0.12. Generally, the ratio of 1:1 is considered

satisfactory to pay off the liabilities as quickly as possible.

C Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Cash Ratio

Cash/ Cash Equivalents

Current Liabilities

411.54 1,214.95

6,876.40 5,155.84

0.05:1 0.23:1

Interpretation: Cash Ratio shows the company’s capacity to pay off the liabilities using cash

(Currency) and cash equivalents (Readily convertible assets). The above work note indicates

(In Lakhs)

2018

(In Lakhs)

Quick Ratio

Quick Asset

Current Liabilities

2,331.87 2,356.41

6,876.40 5,155.84

0.33:1 0.45:1

Interpretation: Quick Ratio evaluates the relation between the Quick asset or liquid asset and

Current Liabilities. Quick asset is considered as the readily available assets which can be

converted into cash within a short period of time without inferring any loss. A higher ratio is

considered better which means the company is able to pay off its liabilities quickly. In the

above working note, the ratio has decreased by 0.12. Generally, the ratio of 1:1 is considered

satisfactory to pay off the liabilities as quickly as possible.

C Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Cash Ratio

Cash/ Cash Equivalents

Current Liabilities

411.54 1,214.95

6,876.40 5,155.84

0.05:1 0.23:1

Interpretation: Cash Ratio shows the company’s capacity to pay off the liabilities using cash

(Currency) and cash equivalents (Readily convertible assets). The above work note indicates

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that the company doesn’t have enough cash or cash equivalents to pay off their liabilities.

Since the acceptable ratio is considered to be 1:1.

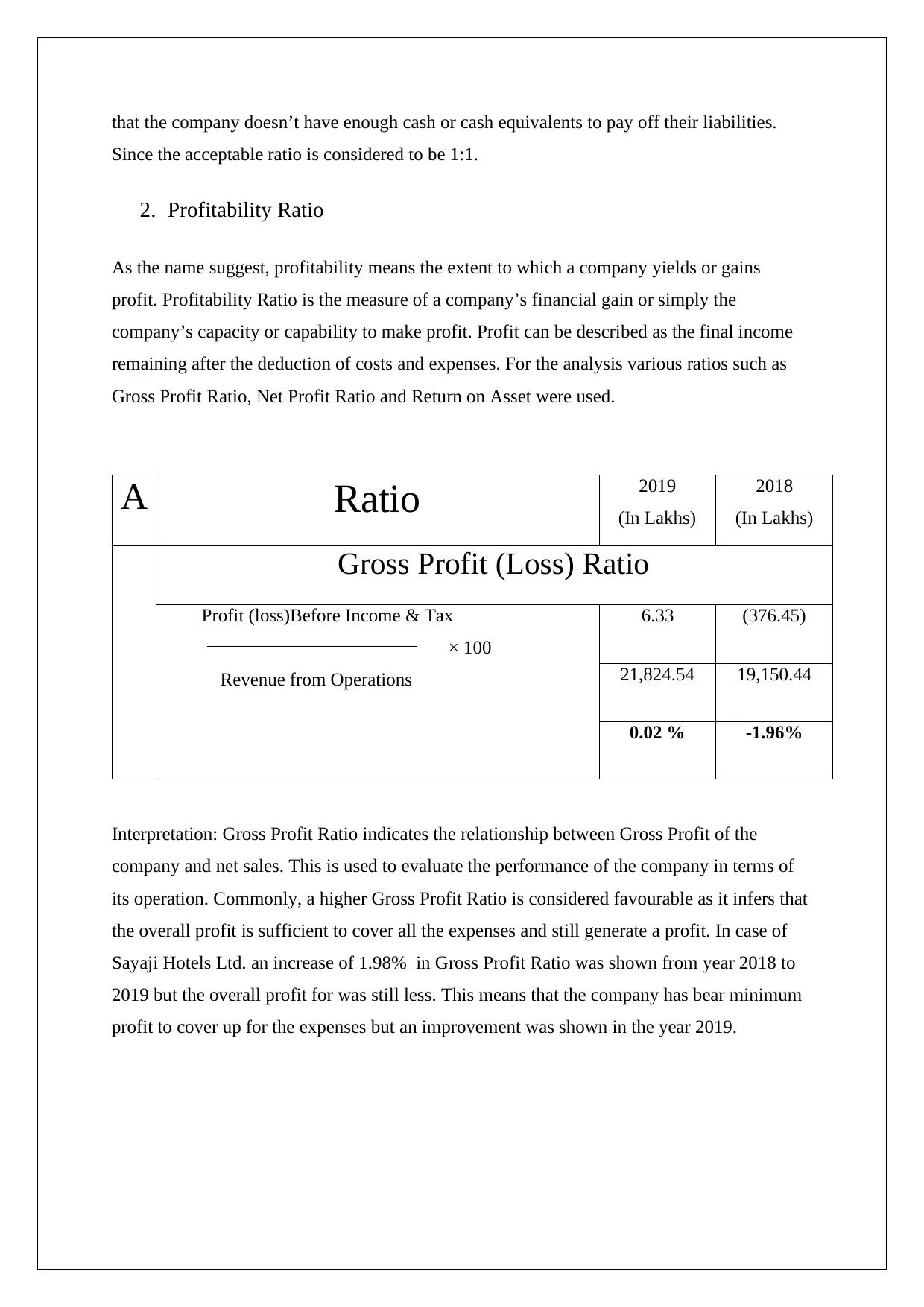

2. Profitability Ratio

As the name suggest, profitability means the extent to which a company yields or gains

profit. Profitability Ratio is the measure of a company’s financial gain or simply the

company’s capacity or capability to make profit. Profit can be described as the final income

remaining after the deduction of costs and expenses. For the analysis various ratios such as

Gross Profit Ratio, Net Profit Ratio and Return on Asset were used.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Gross Profit (Loss) Ratio

Profit (loss)Before Income & Tax

× 100

Revenue from Operations

6.33 (376.45)

21,824.54 19,150.44

0.02 % -1.96%

Interpretation: Gross Profit Ratio indicates the relationship between Gross Profit of the

company and net sales. This is used to evaluate the performance of the company in terms of

its operation. Commonly, a higher Gross Profit Ratio is considered favourable as it infers that

the overall profit is sufficient to cover all the expenses and still generate a profit. In case of

Sayaji Hotels Ltd. an increase of 1.98% in Gross Profit Ratio was shown from year 2018 to

2019 but the overall profit for was still less. This means that the company has bear minimum

profit to cover up for the expenses but an improvement was shown in the year 2019.

Since the acceptable ratio is considered to be 1:1.

2. Profitability Ratio

As the name suggest, profitability means the extent to which a company yields or gains

profit. Profitability Ratio is the measure of a company’s financial gain or simply the

company’s capacity or capability to make profit. Profit can be described as the final income

remaining after the deduction of costs and expenses. For the analysis various ratios such as

Gross Profit Ratio, Net Profit Ratio and Return on Asset were used.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Gross Profit (Loss) Ratio

Profit (loss)Before Income & Tax

× 100

Revenue from Operations

6.33 (376.45)

21,824.54 19,150.44

0.02 % -1.96%

Interpretation: Gross Profit Ratio indicates the relationship between Gross Profit of the

company and net sales. This is used to evaluate the performance of the company in terms of

its operation. Commonly, a higher Gross Profit Ratio is considered favourable as it infers that

the overall profit is sufficient to cover all the expenses and still generate a profit. In case of

Sayaji Hotels Ltd. an increase of 1.98% in Gross Profit Ratio was shown from year 2018 to

2019 but the overall profit for was still less. This means that the company has bear minimum

profit to cover up for the expenses but an improvement was shown in the year 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

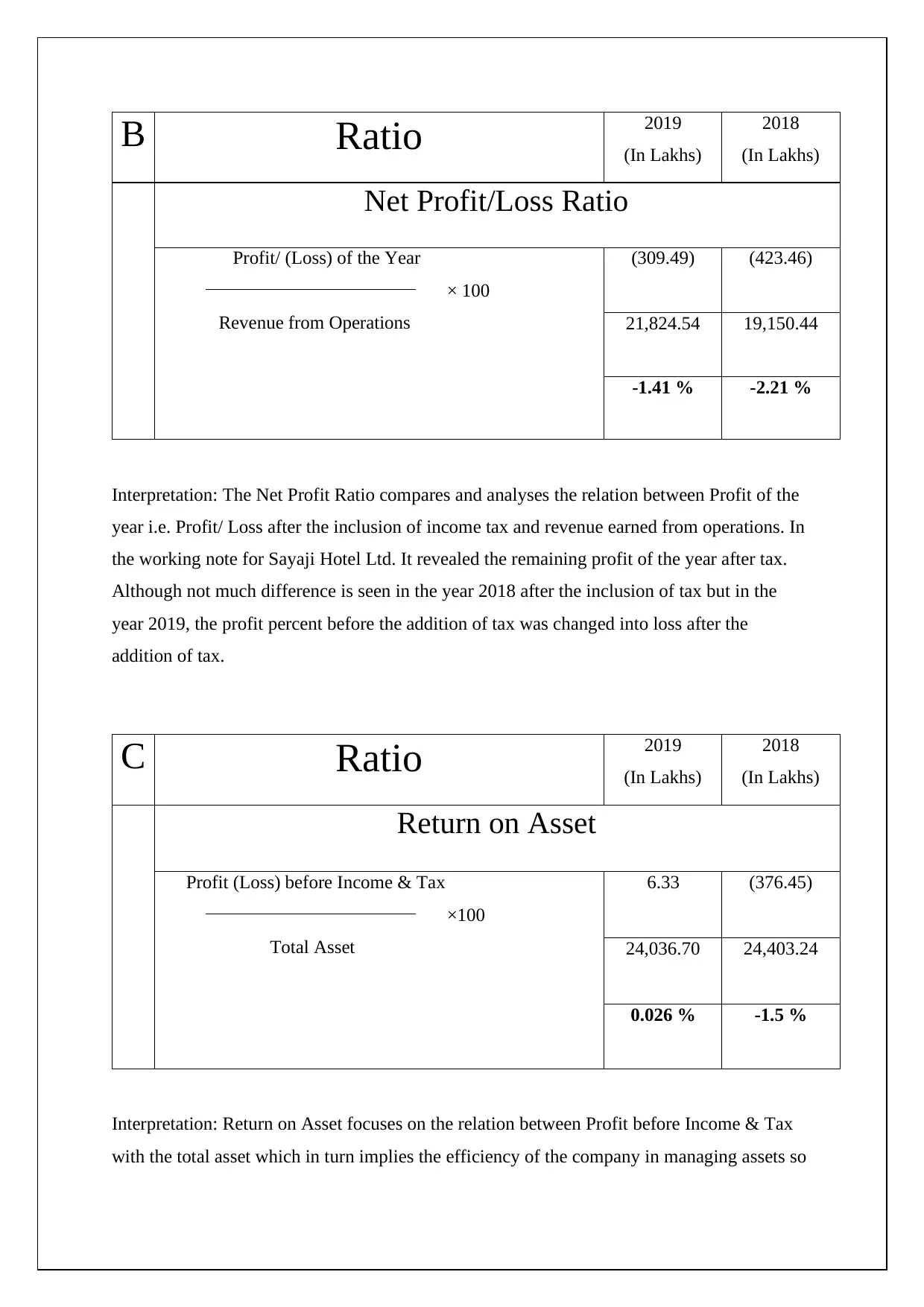

B Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Net Profit/Loss Ratio

Profit/ (Loss) of the Year

× 100

Revenue from Operations

(309.49) (423.46)

21,824.54 19,150.44

-1.41 % -2.21 %

Interpretation: The Net Profit Ratio compares and analyses the relation between Profit of the

year i.e. Profit/ Loss after the inclusion of income tax and revenue earned from operations. In

the working note for Sayaji Hotel Ltd. It revealed the remaining profit of the year after tax.

Although not much difference is seen in the year 2018 after the inclusion of tax but in the

year 2019, the profit percent before the addition of tax was changed into loss after the

addition of tax.

C Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Return on Asset

Profit (Loss) before Income & Tax

×100

Total Asset

6.33 (376.45)

24,036.70 24,403.24

0.026 % -1.5 %

Interpretation: Return on Asset focuses on the relation between Profit before Income & Tax

with the total asset which in turn implies the efficiency of the company in managing assets so

(In Lakhs)

2018

(In Lakhs)

Net Profit/Loss Ratio

Profit/ (Loss) of the Year

× 100

Revenue from Operations

(309.49) (423.46)

21,824.54 19,150.44

-1.41 % -2.21 %

Interpretation: The Net Profit Ratio compares and analyses the relation between Profit of the

year i.e. Profit/ Loss after the inclusion of income tax and revenue earned from operations. In

the working note for Sayaji Hotel Ltd. It revealed the remaining profit of the year after tax.

Although not much difference is seen in the year 2018 after the inclusion of tax but in the

year 2019, the profit percent before the addition of tax was changed into loss after the

addition of tax.

C Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Return on Asset

Profit (Loss) before Income & Tax

×100

Total Asset

6.33 (376.45)

24,036.70 24,403.24

0.026 % -1.5 %

Interpretation: Return on Asset focuses on the relation between Profit before Income & Tax

with the total asset which in turn implies the efficiency of the company in managing assets so

that the company can produce profit. This tells us how well a company can turn the

investment in assets into their financial gain. Higher the percent, effective the asset

management. Unfortunately for Sayaji Hotel Ltd., the Return on Asset was not very

profitable in both years but in 2018 especially it went into loss.

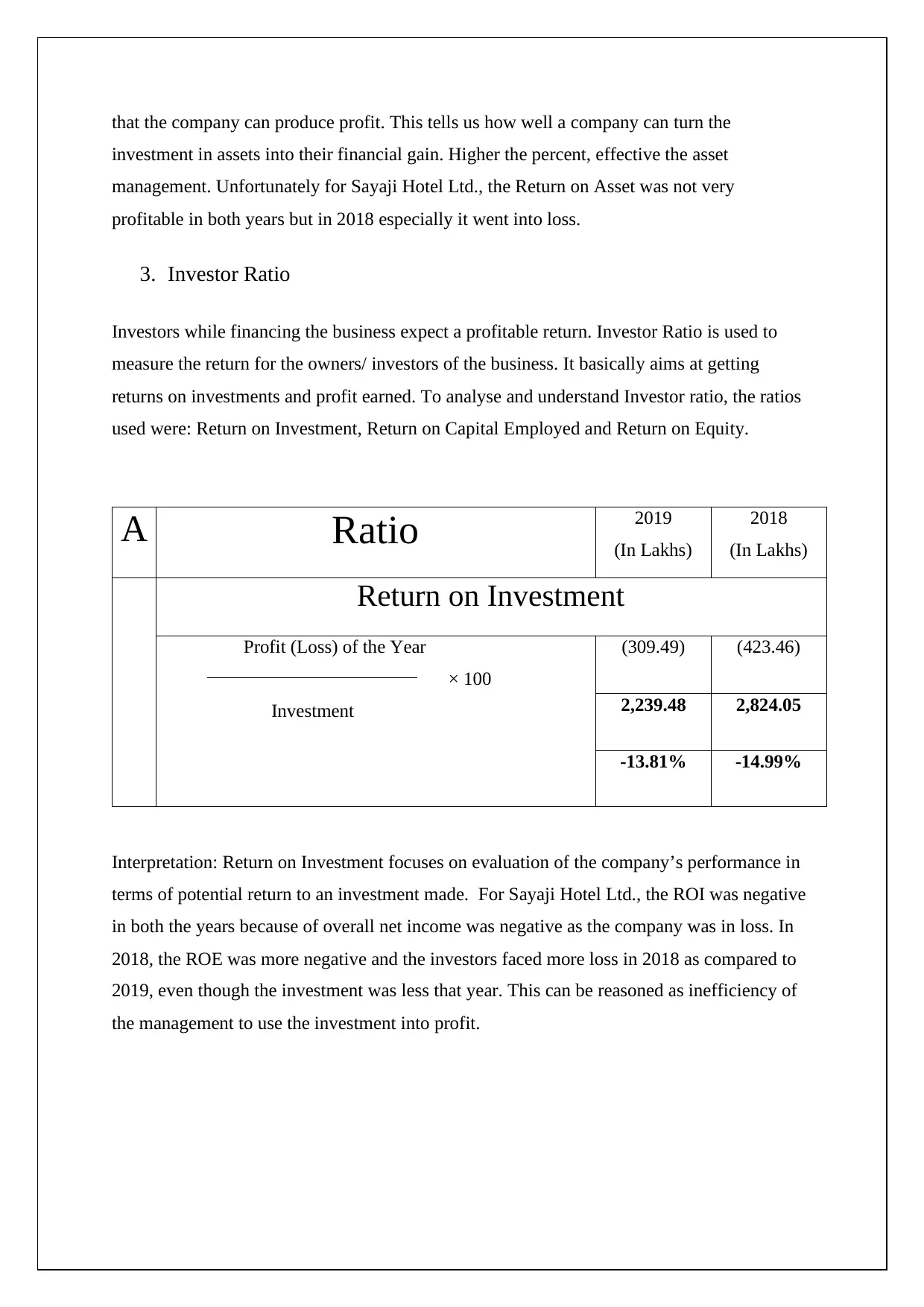

3. Investor Ratio

Investors while financing the business expect a profitable return. Investor Ratio is used to

measure the return for the owners/ investors of the business. It basically aims at getting

returns on investments and profit earned. To analyse and understand Investor ratio, the ratios

used were: Return on Investment, Return on Capital Employed and Return on Equity.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Return on Investment

Profit (Loss) of the Year

× 100

Investment

(309.49) (423.46)

2,239.48 2,824.05

-13.81% -14.99%

Interpretation: Return on Investment focuses on evaluation of the company’s performance in

terms of potential return to an investment made. For Sayaji Hotel Ltd., the ROI was negative

in both the years because of overall net income was negative as the company was in loss. In

2018, the ROE was more negative and the investors faced more loss in 2018 as compared to

2019, even though the investment was less that year. This can be reasoned as inefficiency of

the management to use the investment into profit.

investment in assets into their financial gain. Higher the percent, effective the asset

management. Unfortunately for Sayaji Hotel Ltd., the Return on Asset was not very

profitable in both years but in 2018 especially it went into loss.

3. Investor Ratio

Investors while financing the business expect a profitable return. Investor Ratio is used to

measure the return for the owners/ investors of the business. It basically aims at getting

returns on investments and profit earned. To analyse and understand Investor ratio, the ratios

used were: Return on Investment, Return on Capital Employed and Return on Equity.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Return on Investment

Profit (Loss) of the Year

× 100

Investment

(309.49) (423.46)

2,239.48 2,824.05

-13.81% -14.99%

Interpretation: Return on Investment focuses on evaluation of the company’s performance in

terms of potential return to an investment made. For Sayaji Hotel Ltd., the ROI was negative

in both the years because of overall net income was negative as the company was in loss. In

2018, the ROE was more negative and the investors faced more loss in 2018 as compared to

2019, even though the investment was less that year. This can be reasoned as inefficiency of

the management to use the investment into profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

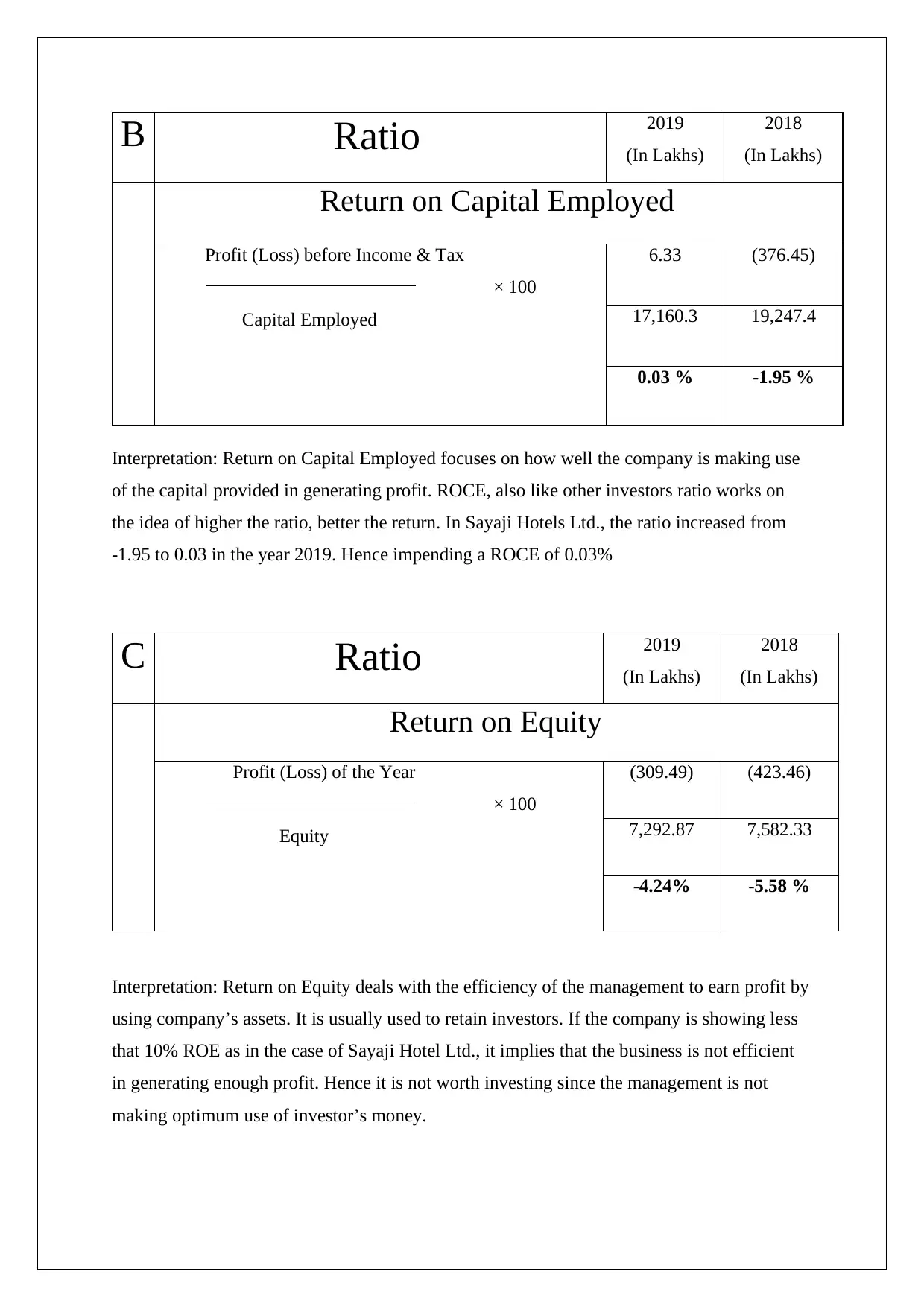

B Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Return on Capital Employed

Profit (Loss) before Income & Tax

× 100

Capital Employed

6.33 (376.45)

17,160.3 19,247.4

0.03 % -1.95 %

Interpretation: Return on Capital Employed focuses on how well the company is making use

of the capital provided in generating profit. ROCE, also like other investors ratio works on

the idea of higher the ratio, better the return. In Sayaji Hotels Ltd., the ratio increased from

-1.95 to 0.03 in the year 2019. Hence impending a ROCE of 0.03%

C Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Return on Equity

Profit (Loss) of the Year

× 100

Equity

(309.49) (423.46)

7,292.87 7,582.33

-4.24% -5.58 %

Interpretation: Return on Equity deals with the efficiency of the management to earn profit by

using company’s assets. It is usually used to retain investors. If the company is showing less

that 10% ROE as in the case of Sayaji Hotel Ltd., it implies that the business is not efficient

in generating enough profit. Hence it is not worth investing since the management is not

making optimum use of investor’s money.

(In Lakhs)

2018

(In Lakhs)

Return on Capital Employed

Profit (Loss) before Income & Tax

× 100

Capital Employed

6.33 (376.45)

17,160.3 19,247.4

0.03 % -1.95 %

Interpretation: Return on Capital Employed focuses on how well the company is making use

of the capital provided in generating profit. ROCE, also like other investors ratio works on

the idea of higher the ratio, better the return. In Sayaji Hotels Ltd., the ratio increased from

-1.95 to 0.03 in the year 2019. Hence impending a ROCE of 0.03%

C Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Return on Equity

Profit (Loss) of the Year

× 100

Equity

(309.49) (423.46)

7,292.87 7,582.33

-4.24% -5.58 %

Interpretation: Return on Equity deals with the efficiency of the management to earn profit by

using company’s assets. It is usually used to retain investors. If the company is showing less

that 10% ROE as in the case of Sayaji Hotel Ltd., it implies that the business is not efficient

in generating enough profit. Hence it is not worth investing since the management is not

making optimum use of investor’s money.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

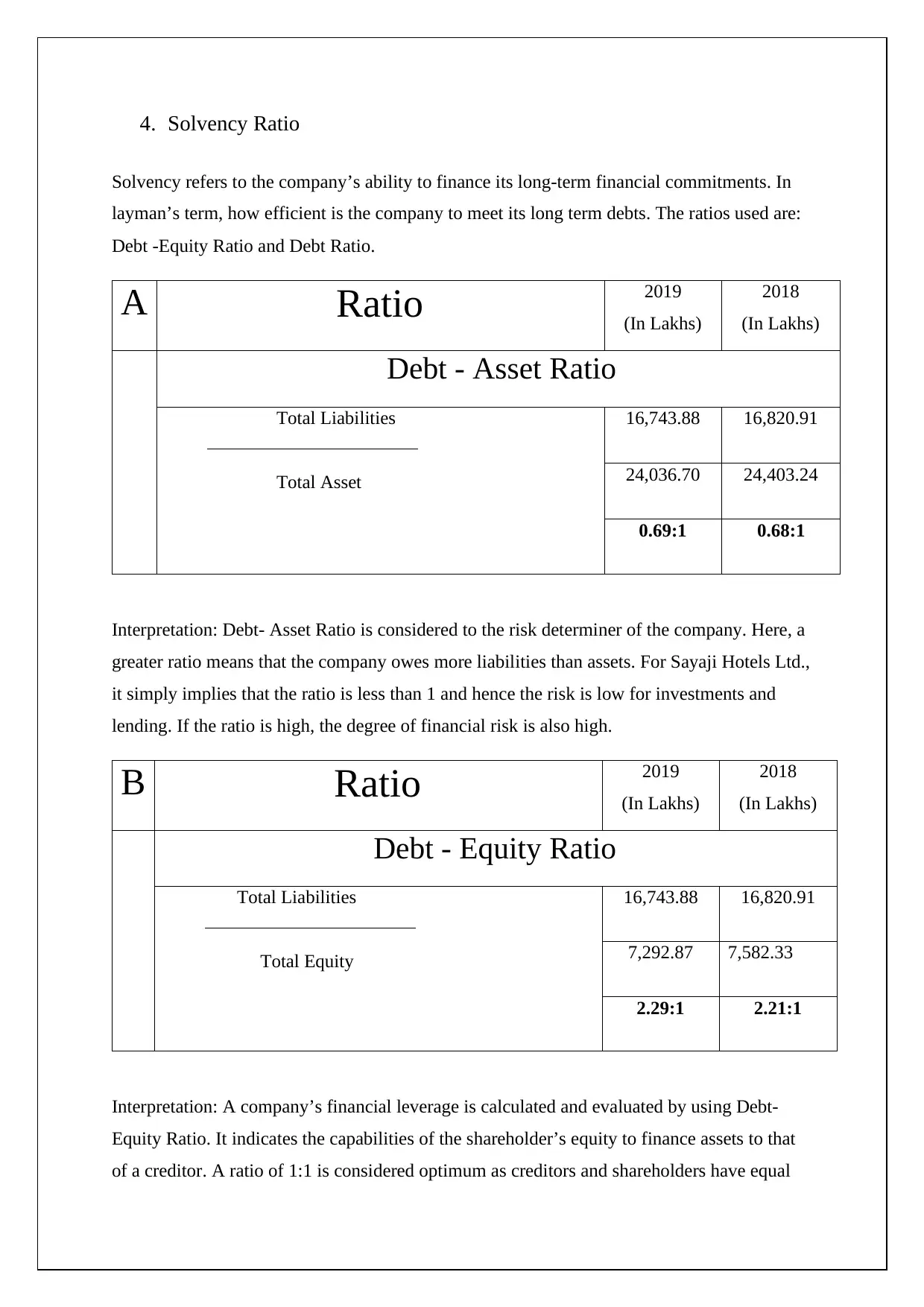

4. Solvency Ratio

Solvency refers to the company’s ability to finance its long-term financial commitments. In

layman’s term, how efficient is the company to meet its long term debts. The ratios used are:

Debt -Equity Ratio and Debt Ratio.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Debt - Asset Ratio

Total Liabilities

Total Asset

16,743.88 16,820.91

24,036.70 24,403.24

0.69:1 0.68:1

Interpretation: Debt- Asset Ratio is considered to the risk determiner of the company. Here, a

greater ratio means that the company owes more liabilities than assets. For Sayaji Hotels Ltd.,

it simply implies that the ratio is less than 1 and hence the risk is low for investments and

lending. If the ratio is high, the degree of financial risk is also high.

B Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Debt - Equity Ratio

Total Liabilities

Total Equity

16,743.88 16,820.91

7,292.87 7,582.33

2.29:1 2.21:1

Interpretation: A company’s financial leverage is calculated and evaluated by using Debt-

Equity Ratio. It indicates the capabilities of the shareholder’s equity to finance assets to that

of a creditor. A ratio of 1:1 is considered optimum as creditors and shareholders have equal

Solvency refers to the company’s ability to finance its long-term financial commitments. In

layman’s term, how efficient is the company to meet its long term debts. The ratios used are:

Debt -Equity Ratio and Debt Ratio.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Debt - Asset Ratio

Total Liabilities

Total Asset

16,743.88 16,820.91

24,036.70 24,403.24

0.69:1 0.68:1

Interpretation: Debt- Asset Ratio is considered to the risk determiner of the company. Here, a

greater ratio means that the company owes more liabilities than assets. For Sayaji Hotels Ltd.,

it simply implies that the ratio is less than 1 and hence the risk is low for investments and

lending. If the ratio is high, the degree of financial risk is also high.

B Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Debt - Equity Ratio

Total Liabilities

Total Equity

16,743.88 16,820.91

7,292.87 7,582.33

2.29:1 2.21:1

Interpretation: A company’s financial leverage is calculated and evaluated by using Debt-

Equity Ratio. It indicates the capabilities of the shareholder’s equity to finance assets to that

of a creditor. A ratio of 1:1 is considered optimum as creditors and shareholders have equal

contribution. If the ratio is more than one that infers that the company is financed by creditors

more and that could be risky. In Sayaji Hotels Ltd. the ratio is high and hence this in turn will

not attract lending capital and shareholders.

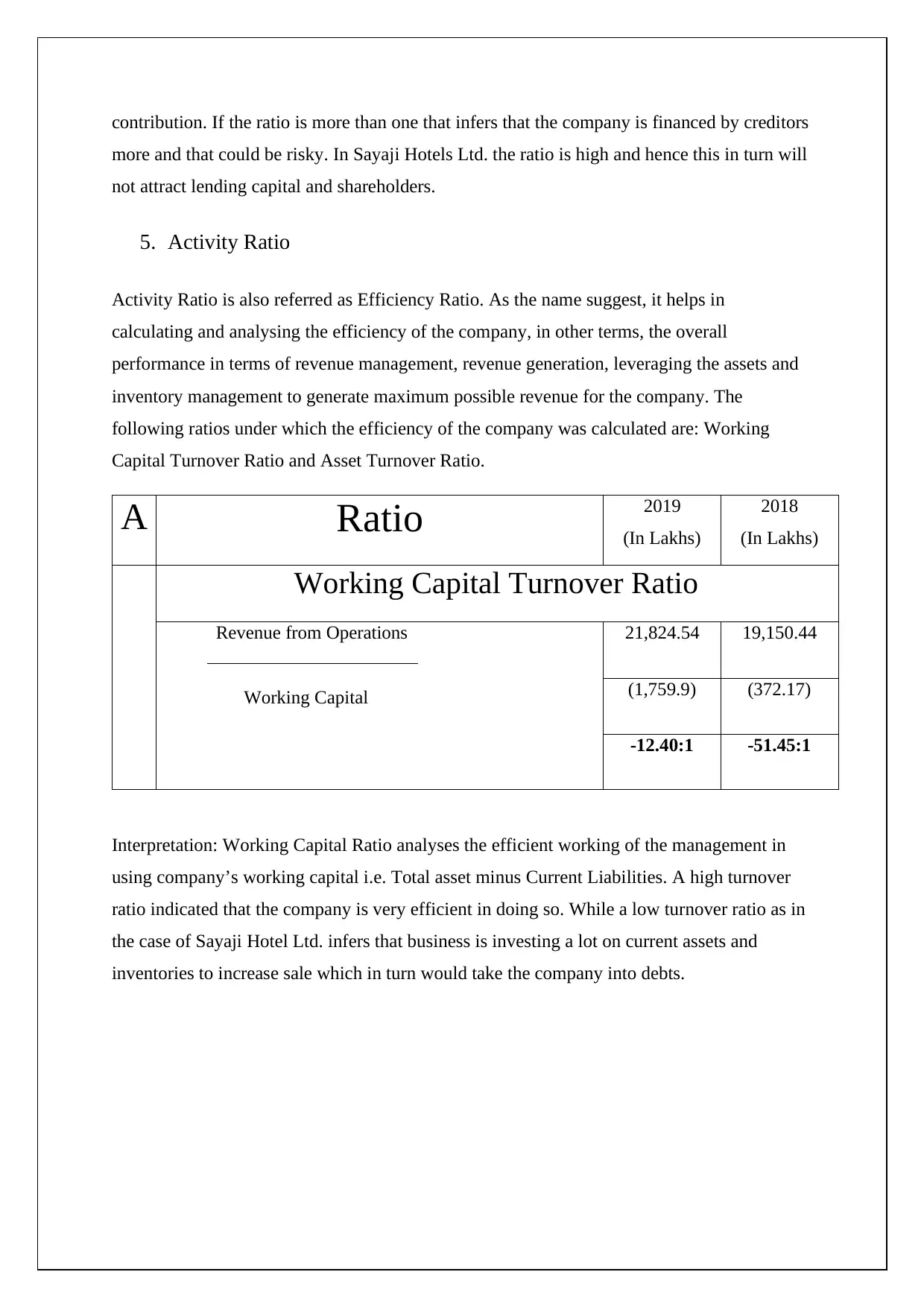

5. Activity Ratio

Activity Ratio is also referred as Efficiency Ratio. As the name suggest, it helps in

calculating and analysing the efficiency of the company, in other terms, the overall

performance in terms of revenue management, revenue generation, leveraging the assets and

inventory management to generate maximum possible revenue for the company. The

following ratios under which the efficiency of the company was calculated are: Working

Capital Turnover Ratio and Asset Turnover Ratio.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Working Capital Turnover Ratio

Revenue from Operations

Working Capital

21,824.54 19,150.44

(1,759.9) (372.17)

-12.40:1 -51.45:1

Interpretation: Working Capital Ratio analyses the efficient working of the management in

using company’s working capital i.e. Total asset minus Current Liabilities. A high turnover

ratio indicated that the company is very efficient in doing so. While a low turnover ratio as in

the case of Sayaji Hotel Ltd. infers that business is investing a lot on current assets and

inventories to increase sale which in turn would take the company into debts.

more and that could be risky. In Sayaji Hotels Ltd. the ratio is high and hence this in turn will

not attract lending capital and shareholders.

5. Activity Ratio

Activity Ratio is also referred as Efficiency Ratio. As the name suggest, it helps in

calculating and analysing the efficiency of the company, in other terms, the overall

performance in terms of revenue management, revenue generation, leveraging the assets and

inventory management to generate maximum possible revenue for the company. The

following ratios under which the efficiency of the company was calculated are: Working

Capital Turnover Ratio and Asset Turnover Ratio.

A Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Working Capital Turnover Ratio

Revenue from Operations

Working Capital

21,824.54 19,150.44

(1,759.9) (372.17)

-12.40:1 -51.45:1

Interpretation: Working Capital Ratio analyses the efficient working of the management in

using company’s working capital i.e. Total asset minus Current Liabilities. A high turnover

ratio indicated that the company is very efficient in doing so. While a low turnover ratio as in

the case of Sayaji Hotel Ltd. infers that business is investing a lot on current assets and

inventories to increase sale which in turn would take the company into debts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

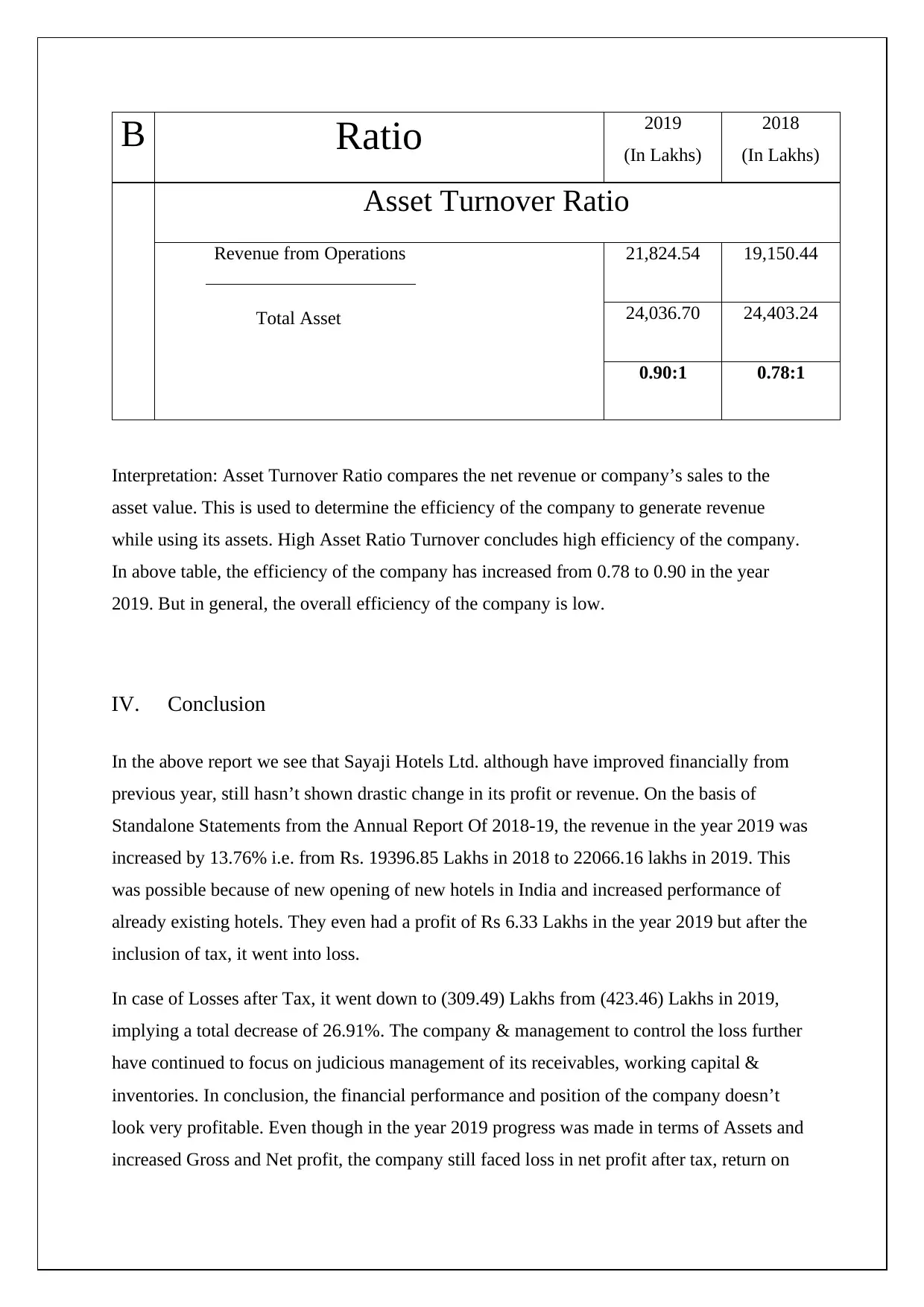

B Ratio 2019

(In Lakhs)

2018

(In Lakhs)

Asset Turnover Ratio

Revenue from Operations

Total Asset

21,824.54 19,150.44

24,036.70 24,403.24

0.90:1 0.78:1

Interpretation: Asset Turnover Ratio compares the net revenue or company’s sales to the

asset value. This is used to determine the efficiency of the company to generate revenue

while using its assets. High Asset Ratio Turnover concludes high efficiency of the company.

In above table, the efficiency of the company has increased from 0.78 to 0.90 in the year

2019. But in general, the overall efficiency of the company is low.

IV. Conclusion

In the above report we see that Sayaji Hotels Ltd. although have improved financially from

previous year, still hasn’t shown drastic change in its profit or revenue. On the basis of

Standalone Statements from the Annual Report Of 2018-19, the revenue in the year 2019 was

increased by 13.76% i.e. from Rs. 19396.85 Lakhs in 2018 to 22066.16 lakhs in 2019. This

was possible because of new opening of new hotels in India and increased performance of

already existing hotels. They even had a profit of Rs 6.33 Lakhs in the year 2019 but after the

inclusion of tax, it went into loss.

In case of Losses after Tax, it went down to (309.49) Lakhs from (423.46) Lakhs in 2019,

implying a total decrease of 26.91%. The company & management to control the loss further

have continued to focus on judicious management of its receivables, working capital &

inventories. In conclusion, the financial performance and position of the company doesn’t

look very profitable. Even though in the year 2019 progress was made in terms of Assets and

increased Gross and Net profit, the company still faced loss in net profit after tax, return on

(In Lakhs)

2018

(In Lakhs)

Asset Turnover Ratio

Revenue from Operations

Total Asset

21,824.54 19,150.44

24,036.70 24,403.24

0.90:1 0.78:1

Interpretation: Asset Turnover Ratio compares the net revenue or company’s sales to the

asset value. This is used to determine the efficiency of the company to generate revenue

while using its assets. High Asset Ratio Turnover concludes high efficiency of the company.

In above table, the efficiency of the company has increased from 0.78 to 0.90 in the year

2019. But in general, the overall efficiency of the company is low.

IV. Conclusion

In the above report we see that Sayaji Hotels Ltd. although have improved financially from

previous year, still hasn’t shown drastic change in its profit or revenue. On the basis of

Standalone Statements from the Annual Report Of 2018-19, the revenue in the year 2019 was

increased by 13.76% i.e. from Rs. 19396.85 Lakhs in 2018 to 22066.16 lakhs in 2019. This

was possible because of new opening of new hotels in India and increased performance of

already existing hotels. They even had a profit of Rs 6.33 Lakhs in the year 2019 but after the

inclusion of tax, it went into loss.

In case of Losses after Tax, it went down to (309.49) Lakhs from (423.46) Lakhs in 2019,

implying a total decrease of 26.91%. The company & management to control the loss further

have continued to focus on judicious management of its receivables, working capital &

inventories. In conclusion, the financial performance and position of the company doesn’t

look very profitable. Even though in the year 2019 progress was made in terms of Assets and

increased Gross and Net profit, the company still faced loss in net profit after tax, return on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital employed and equity. Also the company didn’t have enough assets to cover up for

their debt. As an investor, financing or investing in Sayaji Hotels Ltd. would be risky

granting that they have shown improvement in the feasibility. Even after showing progress,

the company still lacks efficient managerial responsibility in terms of converting investment

into profitable revenue and which in turn does not give feasible return to the investors.

their debt. As an investor, financing or investing in Sayaji Hotels Ltd. would be risky

granting that they have shown improvement in the feasibility. Even after showing progress,

the company still lacks efficient managerial responsibility in terms of converting investment

into profitable revenue and which in turn does not give feasible return to the investors.

V. Bibliography

Jagels, M. G., & Coltman, M. M. (2004). HOSPITALITY MANAGEMENT ACCOUNTING

(8th ed.). New Jersey: John Wiley & Sons.

Schmidgall, R. (1990). Hospitality Industry Managerial Accounting. Michigan: American

Hotel & Motel Association.

Hales, J.A. (2011). Accounting and Financial Analysis in the Hospitality Industry. New

Delhi: Pearson Education, Inc.

Peavler, R. (2009, July 29). Profitability Ratio Analysis. Retrieved from The Balance Small

Business website: https://www.thebalancesmb.com/profitability-ratio-analysis393185

Atkinson, A. A. (2007). Management accounting. Upper Saddle River, N.J.: Pearson/Prentice

Hall.

DeFranco, A., & Lattin, T. (2009). Hospitality financial management. Hoboken, N.J.: Wiley.

Brown, J. (2001). Management Accounting for Hospitality and Tourism. International

Journal Of Hospitality Management, 20(1), 101-102. doi: 10.1016/s0278-4319(00)00029-3

Sharan, V. (2009). Fundamentals of Financial Management. 2nd ed. New Delhi: Pearson

Education, Inc

Jagels, M. G., & Coltman, M. M. (2004). HOSPITALITY MANAGEMENT ACCOUNTING

(8th ed.). New Jersey: John Wiley & Sons.

Schmidgall, R. (1990). Hospitality Industry Managerial Accounting. Michigan: American

Hotel & Motel Association.

Hales, J.A. (2011). Accounting and Financial Analysis in the Hospitality Industry. New

Delhi: Pearson Education, Inc.

Peavler, R. (2009, July 29). Profitability Ratio Analysis. Retrieved from The Balance Small

Business website: https://www.thebalancesmb.com/profitability-ratio-analysis393185

Atkinson, A. A. (2007). Management accounting. Upper Saddle River, N.J.: Pearson/Prentice

Hall.

DeFranco, A., & Lattin, T. (2009). Hospitality financial management. Hoboken, N.J.: Wiley.

Brown, J. (2001). Management Accounting for Hospitality and Tourism. International

Journal Of Hospitality Management, 20(1), 101-102. doi: 10.1016/s0278-4319(00)00029-3

Sharan, V. (2009). Fundamentals of Financial Management. 2nd ed. New Delhi: Pearson

Education, Inc

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.