Samway Baker Fitzgerald (SBF) Audit Report: API, 2019 Audit Findings

VerifiedAdded on 2023/02/01

|13

|3969

|54

Report

AI Summary

This report, prepared by an audit manager at Samway Baker Fitzgerald (SBF), details the findings of the 2019 audit of Always Precise Instruments Pty Limited (API). The report begins with an identification of potential audit risks, determined through ratio analysis, including current ratio, quick ratio, return on equity, return on total assets, gross margin, marketing expense, administrative expense, times interest earned, days in inventory, days in accounts receivable, and debt to equity ratio. Each ratio is analyzed, and the associated level of audit risk is assessed. The report then delves into internal control weaknesses within API, such as purchase order generation, receipt of raw materials, and lack of emergency inventory options, detailing the audit risk and proposed audit procedures to mitigate these risks. The audit highlights several high-risk areas, including declining gross margins, a decrease in times interest earned, and inefficiencies in accounts receivable management, emphasizing the need for careful observation and further examination. The report aims to provide a comprehensive assessment of API's financial health and internal controls.

Audit

1

2019

AUDIT

1

2019

AUDIT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

MEMO TO: Wayne Wiadrowski

FROM: Audit manager at Samway Baker Fitzgerald (SBF)

DATE: May 5, 2019

SUBJECT: Finalizing the audit of Always Precise Instruments Pty Limited

1. Identification of potential audit risk

Identification of potential risk can be ascertained with the help of ratio analysis. When it

comes to the concept of risk, it can be said that each potential risk can be evaluated and an

audit procedure can be undertaken so that the risk can be eliminated. It is imperative that the

business will have a potential audit risk and the risk can be identified through an in-depth

analysis. It is vital to trace the risk and device mechanism that will help to solve the problem.

the following table explains the ratio with an in-depth analysis of the risk followed by the

level of the audit risk.

Ratio Analysis Audit

Risk

Current ratio: Current Ratio is the ratio of current assets to current liabilities. In

other words, it tells us that for every 1 unit of current liability (i.e.,

any outstanding liability that the business might have to pay within 1

year), how many units of current assets (i.e., amount that I may

receive within 1year) do I have.

The current ratio is a very important ratio in terms of determining the

short term liquidity position of the company. Keeping in mind the

fact that Always Precise Instruments Pty Limited (API) could not

meet the industry benchmark last year and that they are looking to

improve the same this year and also keeping in mind that Always

Precise Instruments Pty Limited (API) proposes to generate a larger

volume of sales and reduce the levels of accounts receivable and

inventory it can be said that increasing the current ratio is in the best

interests of Always Precise Instruments Pty Limited (API). If we are

Low Risk

2

MEMO TO: Wayne Wiadrowski

FROM: Audit manager at Samway Baker Fitzgerald (SBF)

DATE: May 5, 2019

SUBJECT: Finalizing the audit of Always Precise Instruments Pty Limited

1. Identification of potential audit risk

Identification of potential risk can be ascertained with the help of ratio analysis. When it

comes to the concept of risk, it can be said that each potential risk can be evaluated and an

audit procedure can be undertaken so that the risk can be eliminated. It is imperative that the

business will have a potential audit risk and the risk can be identified through an in-depth

analysis. It is vital to trace the risk and device mechanism that will help to solve the problem.

the following table explains the ratio with an in-depth analysis of the risk followed by the

level of the audit risk.

Ratio Analysis Audit

Risk

Current ratio: Current Ratio is the ratio of current assets to current liabilities. In

other words, it tells us that for every 1 unit of current liability (i.e.,

any outstanding liability that the business might have to pay within 1

year), how many units of current assets (i.e., amount that I may

receive within 1year) do I have.

The current ratio is a very important ratio in terms of determining the

short term liquidity position of the company. Keeping in mind the

fact that Always Precise Instruments Pty Limited (API) could not

meet the industry benchmark last year and that they are looking to

improve the same this year and also keeping in mind that Always

Precise Instruments Pty Limited (API) proposes to generate a larger

volume of sales and reduce the levels of accounts receivable and

inventory it can be said that increasing the current ratio is in the best

interests of Always Precise Instruments Pty Limited (API). If we are

Low Risk

2

Audit

looking to increase sales while at the same time reduce inventory and

debtors, thereby improving the cash flow position, the current assets

and current liabilities should move in the same direction and current

assets should change at a pace greater than current liabilities (Riddle,

2015). In the year 2018, we have been told that the current ratio has

marginally improved from 1.54 to 1.64. This, while still being less

than the industry average, is a small movement from the past year

even though changes had been budgeted. This, therefore, becomes a

Low-risk area.

Quick asset

ratio:

The quick ratio is the acid test ratio. It is the ratio of liquid assets to

liquid liabilities. The quick ratio should move in the same direction

as the current ratio. In the year 2018, the quick ratio has improved,

just like the current ratio. This indicates that the current assets have

increased while the current liabilities have either not increased or

have increased at a pace less than that of the increase in current

assets. The auditor will have to check that the current ratio and a

quick ratio of Always Precise Instruments Pty Limited (API) are

increasing mainly because of an increase in Cash and Cash

Equivalents and not due to the increase in Debtors. However, this

should be a Low-Risk area.

Low Risk

Return on

equity %

Return on equity % indicates the net profit after tax as a percentage

of the net worth of the company. In the case of Always Precise

Instruments Pty Limited (API), the return on equity during 2017 was

16.6% and the budgeted return on equity was 18.4% but the

unaudited figures are 14.7%. While the industry average for the same

is 17.3%. This doesn’t seem good. This hints that the management

has not been able to achieve the budgeted sales volume. And because

they had lowered the margin %, the plan has resulted in a reduction

in profits (Johnstone, Gramling & Rittenberg, 2014) . This call for

evaluation and study as to why the company has failed to achieve its

budgeted target and has actually fared worse than the previous year.

This will be a Moderate Risk area.

Moderate

Risk

Return on Return on total assets expresses earnings as a percentage of total Moderate

3

looking to increase sales while at the same time reduce inventory and

debtors, thereby improving the cash flow position, the current assets

and current liabilities should move in the same direction and current

assets should change at a pace greater than current liabilities (Riddle,

2015). In the year 2018, we have been told that the current ratio has

marginally improved from 1.54 to 1.64. This, while still being less

than the industry average, is a small movement from the past year

even though changes had been budgeted. This, therefore, becomes a

Low-risk area.

Quick asset

ratio:

The quick ratio is the acid test ratio. It is the ratio of liquid assets to

liquid liabilities. The quick ratio should move in the same direction

as the current ratio. In the year 2018, the quick ratio has improved,

just like the current ratio. This indicates that the current assets have

increased while the current liabilities have either not increased or

have increased at a pace less than that of the increase in current

assets. The auditor will have to check that the current ratio and a

quick ratio of Always Precise Instruments Pty Limited (API) are

increasing mainly because of an increase in Cash and Cash

Equivalents and not due to the increase in Debtors. However, this

should be a Low-Risk area.

Low Risk

Return on

equity %

Return on equity % indicates the net profit after tax as a percentage

of the net worth of the company. In the case of Always Precise

Instruments Pty Limited (API), the return on equity during 2017 was

16.6% and the budgeted return on equity was 18.4% but the

unaudited figures are 14.7%. While the industry average for the same

is 17.3%. This doesn’t seem good. This hints that the management

has not been able to achieve the budgeted sales volume. And because

they had lowered the margin %, the plan has resulted in a reduction

in profits (Johnstone, Gramling & Rittenberg, 2014) . This call for

evaluation and study as to why the company has failed to achieve its

budgeted target and has actually fared worse than the previous year.

This will be a Moderate Risk area.

Moderate

Risk

Return on Return on total assets expresses earnings as a percentage of total Moderate

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

total assets % assets. For Always Precise Instruments Pty Limited (API), the return

on total assets was estimated at 16% while the company could

actually achieve a return on total assets of 12.5%. There is a fall in

this ratio percentage and indicates the fact that the assets could not

be utilized in an effective manner. Last year, its figures for the same

were 14.9%. From the above increment in Current ratio and quick

ratio, it can be estimated that assets have increased. While the above

fall in return on equity can be due to a decrease in profits. Return on

total assets % calls for a study as to why the earnings have decreased

in a situation where the total assets have supposedly increased

(Merchant, 2012). This will also be a Moderate Risk area. When the

overall assets have increased then the company should have provided

a strong percentage in this ratio. However, the fall in the ROA is a

highly critical area that needs to be assessed by the auditor.

Risk

Gross margin

%

Gross margin% or gross profit % is the operating profit % on goods

before accounting for non-trading and non-operating items. Gross

margin% or gross profit % has decreased miserably to 6.5% as

against the budgeted Gross margin% of 10.8% and the previous

years’ Gross margin% of 10.3%. Though Always Precise

Instruments Pty Limited (API) had decided to decrease gross margin

% in an attempt to increases sales volume, they still had a budgeted

gross margin % of 10.8% (higher than that of the last year). In

reality, it seems that they have not been able to achieve the desired

sales volume and at the same time, have lowered the gross margin %

much below the budgeted levels (Kaplan & Williams, 2013). This

calls for a detailed examination on the auditor’s part and should,

therefore, be classified as a High-risk area.

High Risk

Marketing

expense %

Marketing expenses are the expenses incurred on the selling and

distribution of the product. It includes advertisement cost, selling

cost, packing cost and distribution cost. Marketing expenses were

budgeted to be at 3.6% but were actually 4.4% and the expense of

last year was 3.8%. This could be due to increase in costs actually

incurred as compared to costs budgeted for. This will be a low-risk

Low risk

4

total assets % assets. For Always Precise Instruments Pty Limited (API), the return

on total assets was estimated at 16% while the company could

actually achieve a return on total assets of 12.5%. There is a fall in

this ratio percentage and indicates the fact that the assets could not

be utilized in an effective manner. Last year, its figures for the same

were 14.9%. From the above increment in Current ratio and quick

ratio, it can be estimated that assets have increased. While the above

fall in return on equity can be due to a decrease in profits. Return on

total assets % calls for a study as to why the earnings have decreased

in a situation where the total assets have supposedly increased

(Merchant, 2012). This will also be a Moderate Risk area. When the

overall assets have increased then the company should have provided

a strong percentage in this ratio. However, the fall in the ROA is a

highly critical area that needs to be assessed by the auditor.

Risk

Gross margin

%

Gross margin% or gross profit % is the operating profit % on goods

before accounting for non-trading and non-operating items. Gross

margin% or gross profit % has decreased miserably to 6.5% as

against the budgeted Gross margin% of 10.8% and the previous

years’ Gross margin% of 10.3%. Though Always Precise

Instruments Pty Limited (API) had decided to decrease gross margin

% in an attempt to increases sales volume, they still had a budgeted

gross margin % of 10.8% (higher than that of the last year). In

reality, it seems that they have not been able to achieve the desired

sales volume and at the same time, have lowered the gross margin %

much below the budgeted levels (Kaplan & Williams, 2013). This

calls for a detailed examination on the auditor’s part and should,

therefore, be classified as a High-risk area.

High Risk

Marketing

expense %

Marketing expenses are the expenses incurred on the selling and

distribution of the product. It includes advertisement cost, selling

cost, packing cost and distribution cost. Marketing expenses were

budgeted to be at 3.6% but were actually 4.4% and the expense of

last year was 3.8%. This could be due to increase in costs actually

incurred as compared to costs budgeted for. This will be a low-risk

Low risk

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

area.

Admin

expenses/sales

%

Administrative expenses are the expenses incurred on day-to-day

administrative activities like supervisor’s salary, directors’

remuneration, etc. Administrative expenses were 3.4% of sales and

did not differ from the budgeted level of 3.4%. However, during the

last year, the same was 3.6% while the industry benchmark is 3.8%.

This is a low-risk area.

Low Risk

Times interest

earned

The number of interest earned has plummeted to 3.6 times as against

the budgeted level of 6.3 times. The last year’s figures for the same

was 4.6 times and the industry benchmark is 4.2. This is due to an

increase in debt and a corresponding reduction in profits. This will

be a high-risk area.

High risk

Days in

inventory

The number of days for which inventory is held has marginally risen

to 34.9 as against the budgeted level of 32.2 and last year’s figures of

32.9. This will be a low-risk area.

Low risk

Days in

accounts

receivable

The number of days for which an amount remains receivable is 53

days as against the budgeted level of 49.8 days. The industry average

for the same is 46.9. Always Precise Instruments Pty Limited’s (API)

debtor collection policy is clearly ineffective and unable to meet the

budgeted efficiency levels. This calls for a detailed examination and

requires special attention on the auditor’s part (Kaplan, 2011). This,

therefore, becomes a high-risk area.

High risk

Debt to equity

ratio: 1

The debt-equity ratio is the ratio which external liabilities (debt)

bears to shareholders fund. It denotes the extent of debt that is taken

by the company and the extent to which equity is maintained by the

company. In other words, it means that for every 1 unit of equity in

the company, what the debt is held. The debt to equity ratio is 0.61

as against the budgeted level of 0.43. The industry averages for the

same is 0.5. This, combined with the sharp decline in interest

coverage time’s hints that the debt has increased. Increment of debt

is a major issue because it exposes the firm to risk and leads to the

drifting of profit towards the interest payment (Kaplan & Williams,

2013). This again will require special attention on the auditor’s part.

High risk

5

area.

Admin

expenses/sales

%

Administrative expenses are the expenses incurred on day-to-day

administrative activities like supervisor’s salary, directors’

remuneration, etc. Administrative expenses were 3.4% of sales and

did not differ from the budgeted level of 3.4%. However, during the

last year, the same was 3.6% while the industry benchmark is 3.8%.

This is a low-risk area.

Low Risk

Times interest

earned

The number of interest earned has plummeted to 3.6 times as against

the budgeted level of 6.3 times. The last year’s figures for the same

was 4.6 times and the industry benchmark is 4.2. This is due to an

increase in debt and a corresponding reduction in profits. This will

be a high-risk area.

High risk

Days in

inventory

The number of days for which inventory is held has marginally risen

to 34.9 as against the budgeted level of 32.2 and last year’s figures of

32.9. This will be a low-risk area.

Low risk

Days in

accounts

receivable

The number of days for which an amount remains receivable is 53

days as against the budgeted level of 49.8 days. The industry average

for the same is 46.9. Always Precise Instruments Pty Limited’s (API)

debtor collection policy is clearly ineffective and unable to meet the

budgeted efficiency levels. This calls for a detailed examination and

requires special attention on the auditor’s part (Kaplan, 2011). This,

therefore, becomes a high-risk area.

High risk

Debt to equity

ratio: 1

The debt-equity ratio is the ratio which external liabilities (debt)

bears to shareholders fund. It denotes the extent of debt that is taken

by the company and the extent to which equity is maintained by the

company. In other words, it means that for every 1 unit of equity in

the company, what the debt is held. The debt to equity ratio is 0.61

as against the budgeted level of 0.43. The industry averages for the

same is 0.5. This, combined with the sharp decline in interest

coverage time’s hints that the debt has increased. Increment of debt

is a major issue because it exposes the firm to risk and leads to the

drifting of profit towards the interest payment (Kaplan & Williams,

2013). This again will require special attention on the auditor’s part.

High risk

5

Audit

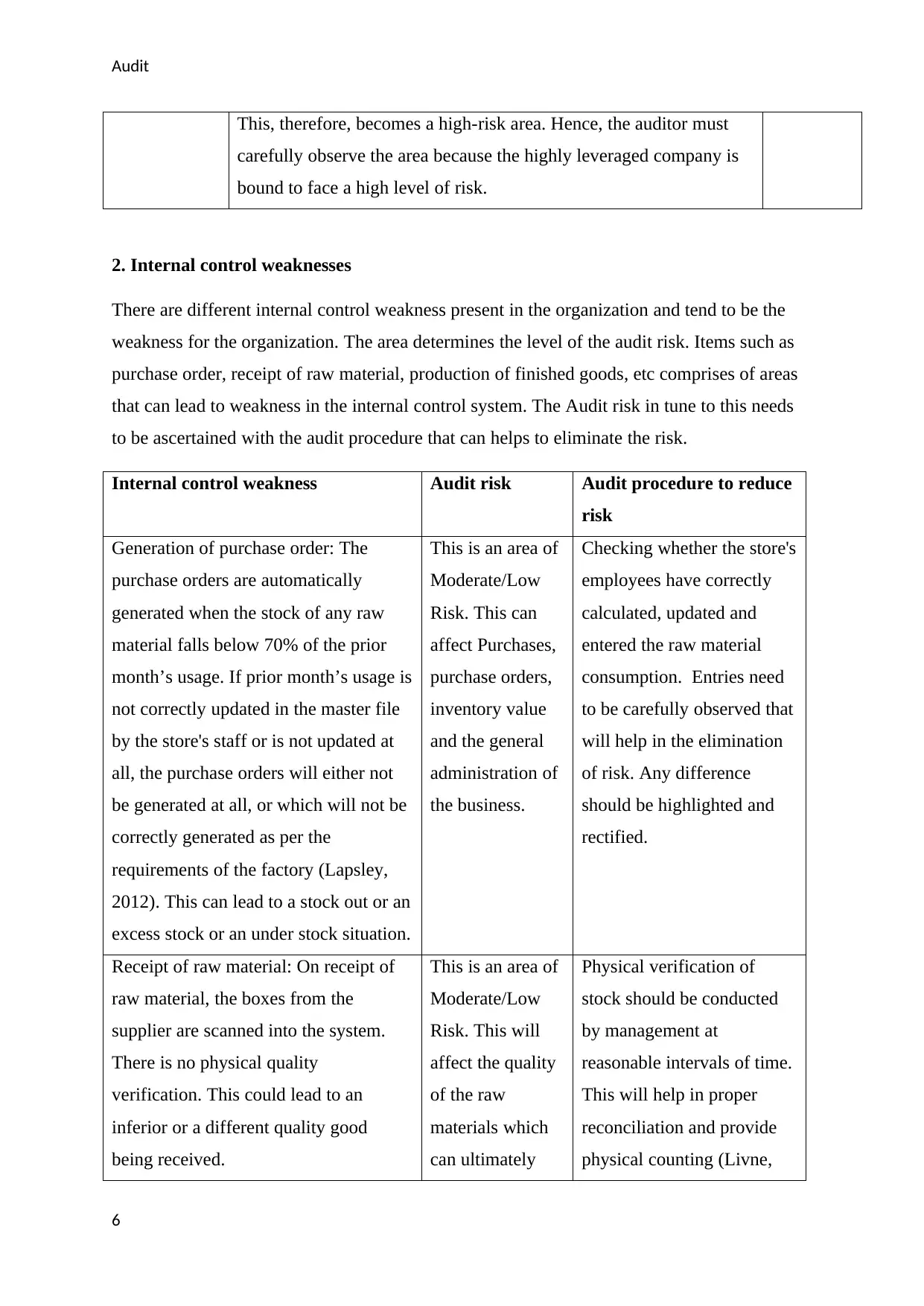

This, therefore, becomes a high-risk area. Hence, the auditor must

carefully observe the area because the highly leveraged company is

bound to face a high level of risk.

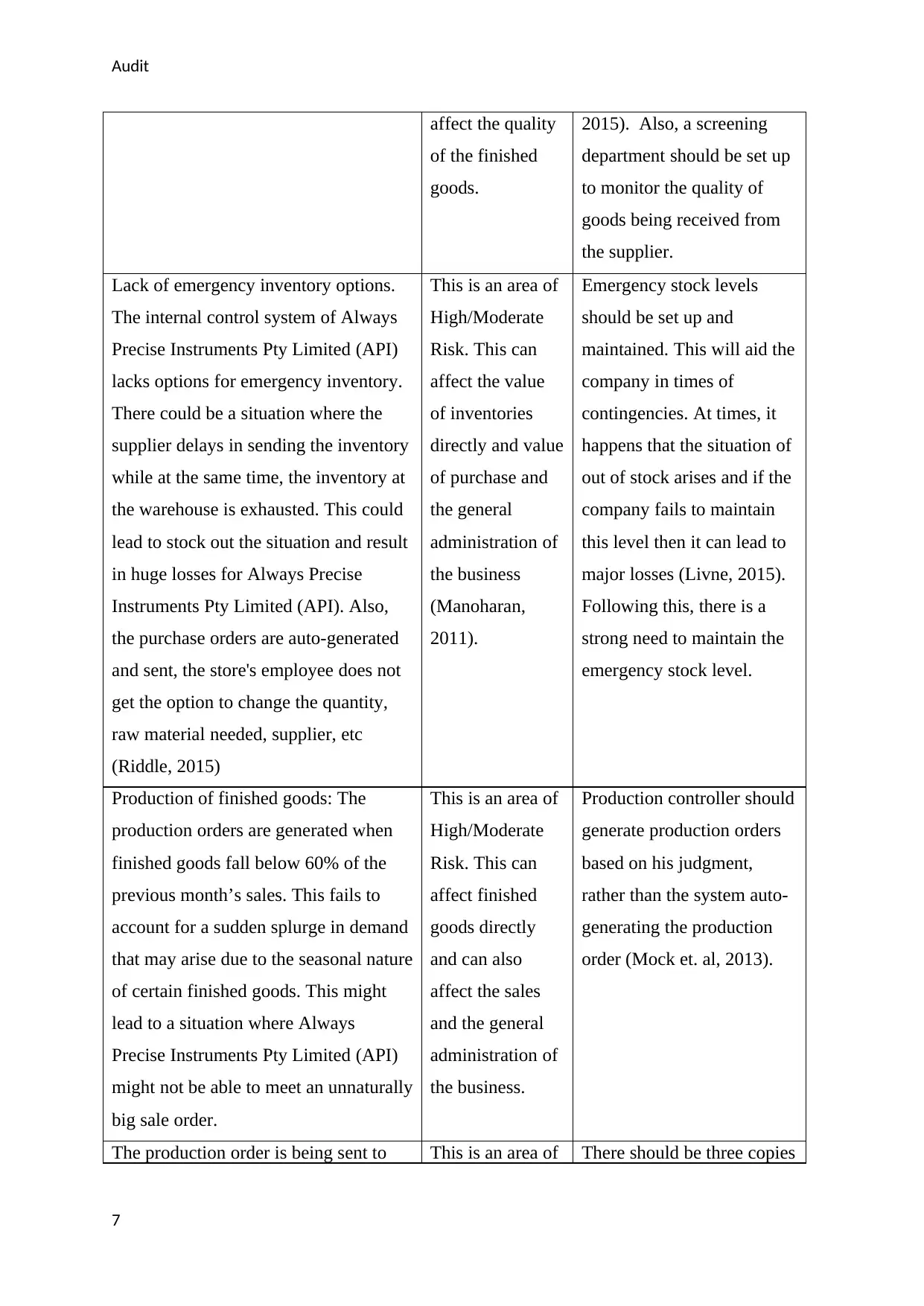

2. Internal control weaknesses

There are different internal control weakness present in the organization and tend to be the

weakness for the organization. The area determines the level of the audit risk. Items such as

purchase order, receipt of raw material, production of finished goods, etc comprises of areas

that can lead to weakness in the internal control system. The Audit risk in tune to this needs

to be ascertained with the audit procedure that can helps to eliminate the risk.

Internal control weakness Audit risk Audit procedure to reduce

risk

Generation of purchase order: The

purchase orders are automatically

generated when the stock of any raw

material falls below 70% of the prior

month’s usage. If prior month’s usage is

not correctly updated in the master file

by the store's staff or is not updated at

all, the purchase orders will either not

be generated at all, or which will not be

correctly generated as per the

requirements of the factory (Lapsley,

2012). This can lead to a stock out or an

excess stock or an under stock situation.

This is an area of

Moderate/Low

Risk. This can

affect Purchases,

purchase orders,

inventory value

and the general

administration of

the business.

Checking whether the store's

employees have correctly

calculated, updated and

entered the raw material

consumption. Entries need

to be carefully observed that

will help in the elimination

of risk. Any difference

should be highlighted and

rectified.

Receipt of raw material: On receipt of

raw material, the boxes from the

supplier are scanned into the system.

There is no physical quality

verification. This could lead to an

inferior or a different quality good

being received.

This is an area of

Moderate/Low

Risk. This will

affect the quality

of the raw

materials which

can ultimately

Physical verification of

stock should be conducted

by management at

reasonable intervals of time.

This will help in proper

reconciliation and provide

physical counting (Livne,

6

This, therefore, becomes a high-risk area. Hence, the auditor must

carefully observe the area because the highly leveraged company is

bound to face a high level of risk.

2. Internal control weaknesses

There are different internal control weakness present in the organization and tend to be the

weakness for the organization. The area determines the level of the audit risk. Items such as

purchase order, receipt of raw material, production of finished goods, etc comprises of areas

that can lead to weakness in the internal control system. The Audit risk in tune to this needs

to be ascertained with the audit procedure that can helps to eliminate the risk.

Internal control weakness Audit risk Audit procedure to reduce

risk

Generation of purchase order: The

purchase orders are automatically

generated when the stock of any raw

material falls below 70% of the prior

month’s usage. If prior month’s usage is

not correctly updated in the master file

by the store's staff or is not updated at

all, the purchase orders will either not

be generated at all, or which will not be

correctly generated as per the

requirements of the factory (Lapsley,

2012). This can lead to a stock out or an

excess stock or an under stock situation.

This is an area of

Moderate/Low

Risk. This can

affect Purchases,

purchase orders,

inventory value

and the general

administration of

the business.

Checking whether the store's

employees have correctly

calculated, updated and

entered the raw material

consumption. Entries need

to be carefully observed that

will help in the elimination

of risk. Any difference

should be highlighted and

rectified.

Receipt of raw material: On receipt of

raw material, the boxes from the

supplier are scanned into the system.

There is no physical quality

verification. This could lead to an

inferior or a different quality good

being received.

This is an area of

Moderate/Low

Risk. This will

affect the quality

of the raw

materials which

can ultimately

Physical verification of

stock should be conducted

by management at

reasonable intervals of time.

This will help in proper

reconciliation and provide

physical counting (Livne,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

affect the quality

of the finished

goods.

2015). Also, a screening

department should be set up

to monitor the quality of

goods being received from

the supplier.

Lack of emergency inventory options.

The internal control system of Always

Precise Instruments Pty Limited (API)

lacks options for emergency inventory.

There could be a situation where the

supplier delays in sending the inventory

while at the same time, the inventory at

the warehouse is exhausted. This could

lead to stock out the situation and result

in huge losses for Always Precise

Instruments Pty Limited (API). Also,

the purchase orders are auto-generated

and sent, the store's employee does not

get the option to change the quantity,

raw material needed, supplier, etc

(Riddle, 2015)

This is an area of

High/Moderate

Risk. This can

affect the value

of inventories

directly and value

of purchase and

the general

administration of

the business

(Manoharan,

2011).

Emergency stock levels

should be set up and

maintained. This will aid the

company in times of

contingencies. At times, it

happens that the situation of

out of stock arises and if the

company fails to maintain

this level then it can lead to

major losses (Livne, 2015).

Following this, there is a

strong need to maintain the

emergency stock level.

Production of finished goods: The

production orders are generated when

finished goods fall below 60% of the

previous month’s sales. This fails to

account for a sudden splurge in demand

that may arise due to the seasonal nature

of certain finished goods. This might

lead to a situation where Always

Precise Instruments Pty Limited (API)

might not be able to meet an unnaturally

big sale order.

This is an area of

High/Moderate

Risk. This can

affect finished

goods directly

and can also

affect the sales

and the general

administration of

the business.

Production controller should

generate production orders

based on his judgment,

rather than the system auto-

generating the production

order (Mock et. al, 2013).

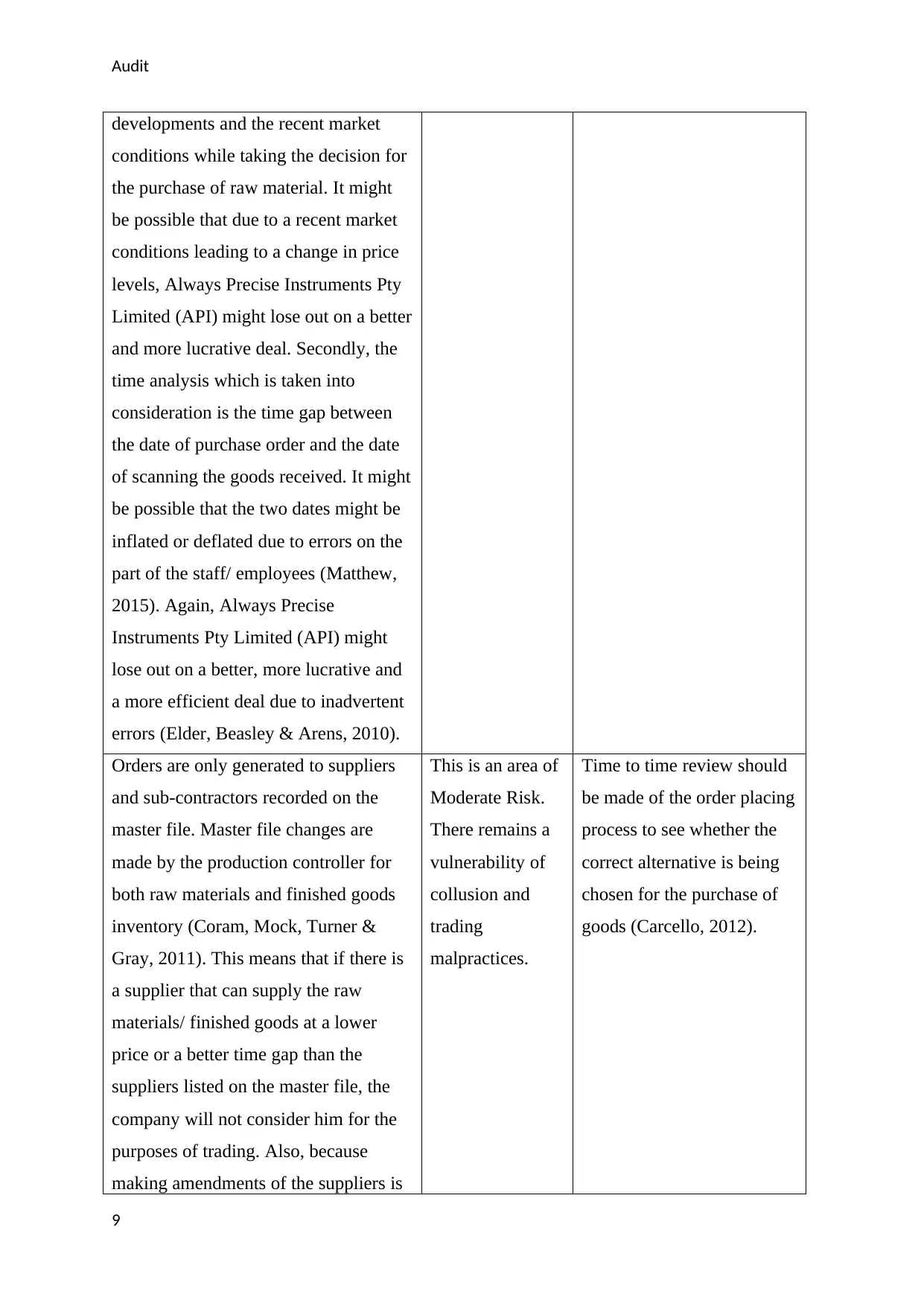

The production order is being sent to This is an area of There should be three copies

7

affect the quality

of the finished

goods.

2015). Also, a screening

department should be set up

to monitor the quality of

goods being received from

the supplier.

Lack of emergency inventory options.

The internal control system of Always

Precise Instruments Pty Limited (API)

lacks options for emergency inventory.

There could be a situation where the

supplier delays in sending the inventory

while at the same time, the inventory at

the warehouse is exhausted. This could

lead to stock out the situation and result

in huge losses for Always Precise

Instruments Pty Limited (API). Also,

the purchase orders are auto-generated

and sent, the store's employee does not

get the option to change the quantity,

raw material needed, supplier, etc

(Riddle, 2015)

This is an area of

High/Moderate

Risk. This can

affect the value

of inventories

directly and value

of purchase and

the general

administration of

the business

(Manoharan,

2011).

Emergency stock levels

should be set up and

maintained. This will aid the

company in times of

contingencies. At times, it

happens that the situation of

out of stock arises and if the

company fails to maintain

this level then it can lead to

major losses (Livne, 2015).

Following this, there is a

strong need to maintain the

emergency stock level.

Production of finished goods: The

production orders are generated when

finished goods fall below 60% of the

previous month’s sales. This fails to

account for a sudden splurge in demand

that may arise due to the seasonal nature

of certain finished goods. This might

lead to a situation where Always

Precise Instruments Pty Limited (API)

might not be able to meet an unnaturally

big sale order.

This is an area of

High/Moderate

Risk. This can

affect finished

goods directly

and can also

affect the sales

and the general

administration of

the business.

Production controller should

generate production orders

based on his judgment,

rather than the system auto-

generating the production

order (Mock et. al, 2013).

The production order is being sent to This is an area of There should be three copies

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

only the raw materials store for use as a

picking slip and filed by production

controller in date order. It would be

better if a third copy would also be

generated and sent to the finished goods

department (stores staff). This way, he

would know when to expect the

delivery of the next lot of finished

goods and would manage his stock

accordingly.

Low Risk. This

affects the

general

administration of

the business.

of a production order. One

for the production controller,

one for the raw materials

store and one more for the

finished goods department

(stores staff). This would

increase transparency and be

better for the general

administration of the

business. The maintenance

of the order will help in

ensuring better performance

and proper compliance

(Niemi & Sundgren, 2012).

Further, the conduct of the

audit is easier in this

manner.

Selection of supplier of raw material

and finished goods. The system selects

the supplier of raw material and

finished goods on the basis of the latest

price as per the last invoice and their

delivery times (based on the number of

days between the date the purchase/

production order is raised and the date

the goods are scanned by the

warehouse). This is vulnerable to

certain errors and fallacies. Firstly,

because the prices which are being

taken as the basis for consideration are

the prices as per the previous invoices,

Always Precise Instruments Pty Limited

(API) fails to account for the recent

This is an area of

Moderate Risk.

This affects the

decision making

with respect to

the purchase of

raw materials and

the finished

goods (Roach,

2010).

Quotations can be invited

from the interested suppliers

and then the applications can

be screened and the best

quotation in terms of price

and time period, be selected.

8

only the raw materials store for use as a

picking slip and filed by production

controller in date order. It would be

better if a third copy would also be

generated and sent to the finished goods

department (stores staff). This way, he

would know when to expect the

delivery of the next lot of finished

goods and would manage his stock

accordingly.

Low Risk. This

affects the

general

administration of

the business.

of a production order. One

for the production controller,

one for the raw materials

store and one more for the

finished goods department

(stores staff). This would

increase transparency and be

better for the general

administration of the

business. The maintenance

of the order will help in

ensuring better performance

and proper compliance

(Niemi & Sundgren, 2012).

Further, the conduct of the

audit is easier in this

manner.

Selection of supplier of raw material

and finished goods. The system selects

the supplier of raw material and

finished goods on the basis of the latest

price as per the last invoice and their

delivery times (based on the number of

days between the date the purchase/

production order is raised and the date

the goods are scanned by the

warehouse). This is vulnerable to

certain errors and fallacies. Firstly,

because the prices which are being

taken as the basis for consideration are

the prices as per the previous invoices,

Always Precise Instruments Pty Limited

(API) fails to account for the recent

This is an area of

Moderate Risk.

This affects the

decision making

with respect to

the purchase of

raw materials and

the finished

goods (Roach,

2010).

Quotations can be invited

from the interested suppliers

and then the applications can

be screened and the best

quotation in terms of price

and time period, be selected.

8

Audit

developments and the recent market

conditions while taking the decision for

the purchase of raw material. It might

be possible that due to a recent market

conditions leading to a change in price

levels, Always Precise Instruments Pty

Limited (API) might lose out on a better

and more lucrative deal. Secondly, the

time analysis which is taken into

consideration is the time gap between

the date of purchase order and the date

of scanning the goods received. It might

be possible that the two dates might be

inflated or deflated due to errors on the

part of the staff/ employees (Matthew,

2015). Again, Always Precise

Instruments Pty Limited (API) might

lose out on a better, more lucrative and

a more efficient deal due to inadvertent

errors (Elder, Beasley & Arens, 2010).

Orders are only generated to suppliers

and sub-contractors recorded on the

master file. Master file changes are

made by the production controller for

both raw materials and finished goods

inventory (Coram, Mock, Turner &

Gray, 2011). This means that if there is

a supplier that can supply the raw

materials/ finished goods at a lower

price or a better time gap than the

suppliers listed on the master file, the

company will not consider him for the

purposes of trading. Also, because

making amendments of the suppliers is

This is an area of

Moderate Risk.

There remains a

vulnerability of

collusion and

trading

malpractices.

Time to time review should

be made of the order placing

process to see whether the

correct alternative is being

chosen for the purchase of

goods (Carcello, 2012).

9

developments and the recent market

conditions while taking the decision for

the purchase of raw material. It might

be possible that due to a recent market

conditions leading to a change in price

levels, Always Precise Instruments Pty

Limited (API) might lose out on a better

and more lucrative deal. Secondly, the

time analysis which is taken into

consideration is the time gap between

the date of purchase order and the date

of scanning the goods received. It might

be possible that the two dates might be

inflated or deflated due to errors on the

part of the staff/ employees (Matthew,

2015). Again, Always Precise

Instruments Pty Limited (API) might

lose out on a better, more lucrative and

a more efficient deal due to inadvertent

errors (Elder, Beasley & Arens, 2010).

Orders are only generated to suppliers

and sub-contractors recorded on the

master file. Master file changes are

made by the production controller for

both raw materials and finished goods

inventory (Coram, Mock, Turner &

Gray, 2011). This means that if there is

a supplier that can supply the raw

materials/ finished goods at a lower

price or a better time gap than the

suppliers listed on the master file, the

company will not consider him for the

purposes of trading. Also, because

making amendments of the suppliers is

This is an area of

Moderate Risk.

There remains a

vulnerability of

collusion and

trading

malpractices.

Time to time review should

be made of the order placing

process to see whether the

correct alternative is being

chosen for the purchase of

goods (Carcello, 2012).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

in the hands of the production

controller, there is always a risk that he

might collide with a particular supplier

and provide certain undue advantages or

uncalled for services to him/her. Thus,

there also comes up the risk of collusion

within the firm between the production

controller and a particular supplier

(Carcello, 2012).

3. API’s year-end stocktakes

Finally, the test count will be done at API yearly end stock takes. The step is vital as the

samples will address the assertion completeness and the population from which the samples

should be collected. Therefore, selection of samples by Wayne should be done in the

following manner that will help to test the existence, as well as completeness assertion at

every stage.

Assertion Which population? Sample

selection

method

Justification for the

sample selection

method

Completeness Finished goods. Finished being actually

produced, they should be checked for

completeness in order to determine

whether the finished goods actually

being produced conform to the

established framework and the required

benchmarks or not. They should be

physically verified to test their degree of

likability with the desired standard

(Blay, Geiger, & North, 2011).

Random Random sampling

from category A, B

and C after applying

ABC analysis and

categorising the

finished goods stock

into category A, B or

C.

Existence Raw material. Raw material stock held

by the store's department should be

Random Random sampling

from category A, B

10

in the hands of the production

controller, there is always a risk that he

might collide with a particular supplier

and provide certain undue advantages or

uncalled for services to him/her. Thus,

there also comes up the risk of collusion

within the firm between the production

controller and a particular supplier

(Carcello, 2012).

3. API’s year-end stocktakes

Finally, the test count will be done at API yearly end stock takes. The step is vital as the

samples will address the assertion completeness and the population from which the samples

should be collected. Therefore, selection of samples by Wayne should be done in the

following manner that will help to test the existence, as well as completeness assertion at

every stage.

Assertion Which population? Sample

selection

method

Justification for the

sample selection

method

Completeness Finished goods. Finished being actually

produced, they should be checked for

completeness in order to determine

whether the finished goods actually

being produced conform to the

established framework and the required

benchmarks or not. They should be

physically verified to test their degree of

likability with the desired standard

(Blay, Geiger, & North, 2011).

Random Random sampling

from category A, B

and C after applying

ABC analysis and

categorising the

finished goods stock

into category A, B or

C.

Existence Raw material. Raw material stock held

by the store's department should be

Random Random sampling

from category A, B

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

physically verified to check for its

existence. Whether the raw material

stock actually exists or not? If it does,

whether or not it matches with the

quantity stated in the master file or the

specification stated in the master file.

and C after applying

ABC analysis and

categorising the raw

material stock into

category A, B or C.

11

physically verified to check for its

existence. Whether the raw material

stock actually exists or not? If it does,

whether or not it matches with the

quantity stated in the master file or the

specification stated in the master file.

and C after applying

ABC analysis and

categorising the raw

material stock into

category A, B or C.

11

Audit

References

Blay, A. D., Geiger, M. A. & North, D. S. (2011). The Auditor's Going-Concern Opinion as a

Communication of Risk. Auditing: A Journal of Practice & Theory, 30 (2): 77- 102.

Doi: https://doi.org/10.2308/ajpt-50002

Carcello, J. (2012). What do investors want from the standard audit report? CPA Journal 82

Retrieved from https://www.questia.com/magazine/1P3-2594765681/what-do-

investors-want-from-the-standard-audit-report

Coram, P., Mock, T. J., Turner, J. & Gray, G. (2011). The communicative value of the

auditor’s report. Australian Accounting Review 21(3): 235-252. Doi:

https://doi.org/10.1111/j.1835-2561.2011.00140.x

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Johnstone, K, Gramling, A & Rittenberg, L.E. (2014). Auditing: A Risk Based-Approach to

Conducting a Quality Audit, 10th ed. Cengage Learning

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Kaplan, S. & Williams, D. (2013). Do going concern audit reports protect auditors from

litigation? A simultaneous equations approach. The Accounting Review, 88 (1), 199-

232. Doi: https://doi.org/10.2308/accr-50279

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015). Threats to Auditor Independence and Possible Remedies. Retrieved from:

http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The George

Washington University.

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management Misconduct?.

The Accounting Review, 90(2), 495-527. Doi: https://doi.org/10.2308/accr-50871

12

References

Blay, A. D., Geiger, M. A. & North, D. S. (2011). The Auditor's Going-Concern Opinion as a

Communication of Risk. Auditing: A Journal of Practice & Theory, 30 (2): 77- 102.

Doi: https://doi.org/10.2308/ajpt-50002

Carcello, J. (2012). What do investors want from the standard audit report? CPA Journal 82

Retrieved from https://www.questia.com/magazine/1P3-2594765681/what-do-

investors-want-from-the-standard-audit-report

Coram, P., Mock, T. J., Turner, J. & Gray, G. (2011). The communicative value of the

auditor’s report. Australian Accounting Review 21(3): 235-252. Doi:

https://doi.org/10.1111/j.1835-2561.2011.00140.x

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Johnstone, K, Gramling, A & Rittenberg, L.E. (2014). Auditing: A Risk Based-Approach to

Conducting a Quality Audit, 10th ed. Cengage Learning

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Kaplan, S. & Williams, D. (2013). Do going concern audit reports protect auditors from

litigation? A simultaneous equations approach. The Accounting Review, 88 (1), 199-

232. Doi: https://doi.org/10.2308/accr-50279

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015). Threats to Auditor Independence and Possible Remedies. Retrieved from:

http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The George

Washington University.

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management Misconduct?.

The Accounting Review, 90(2), 495-527. Doi: https://doi.org/10.2308/accr-50871

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.