SBM3307 Project Development: Computer Assembly & Economic Analysis

VerifiedAdded on 2023/03/30

|12

|1329

|228

Report

AI Summary

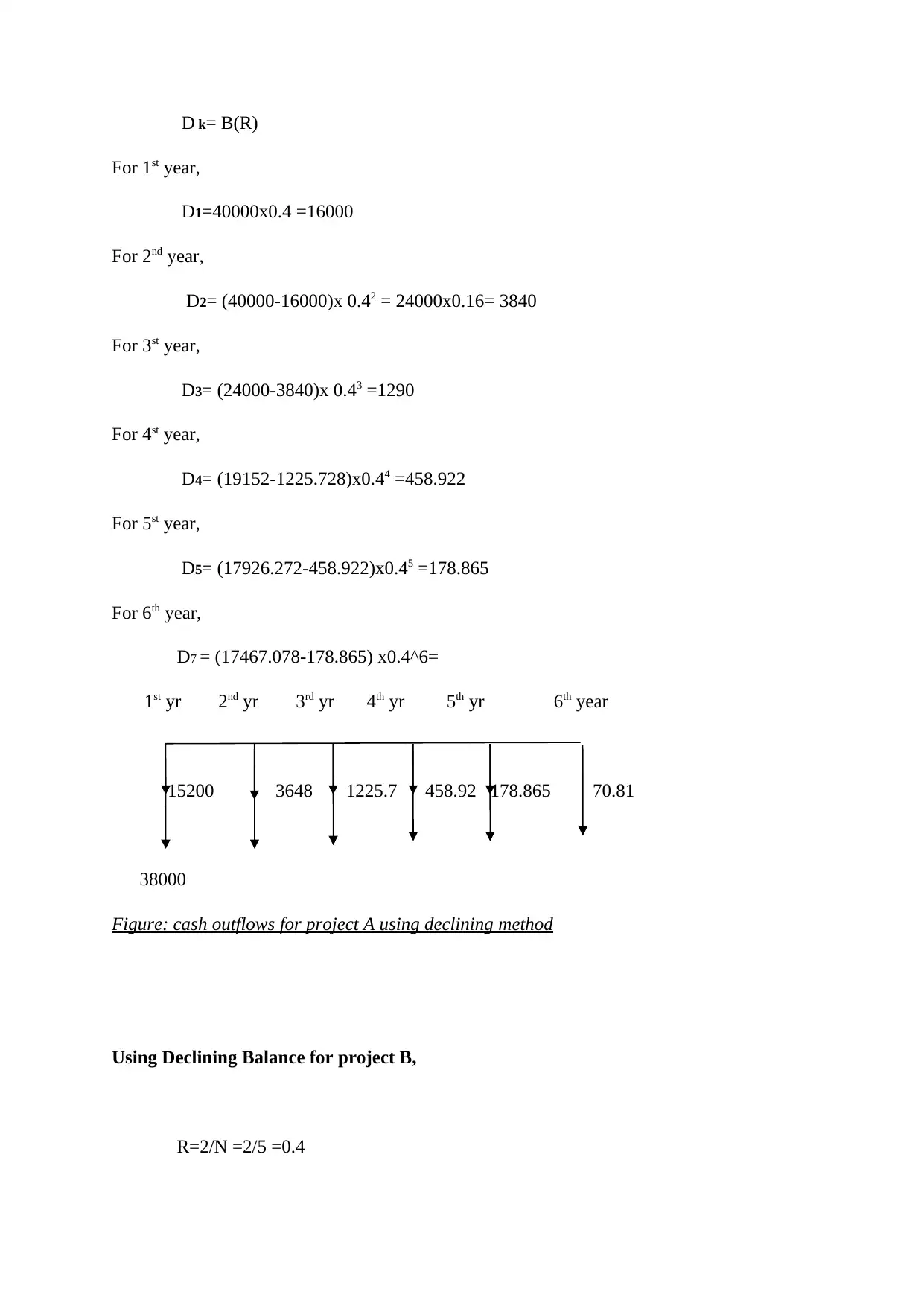

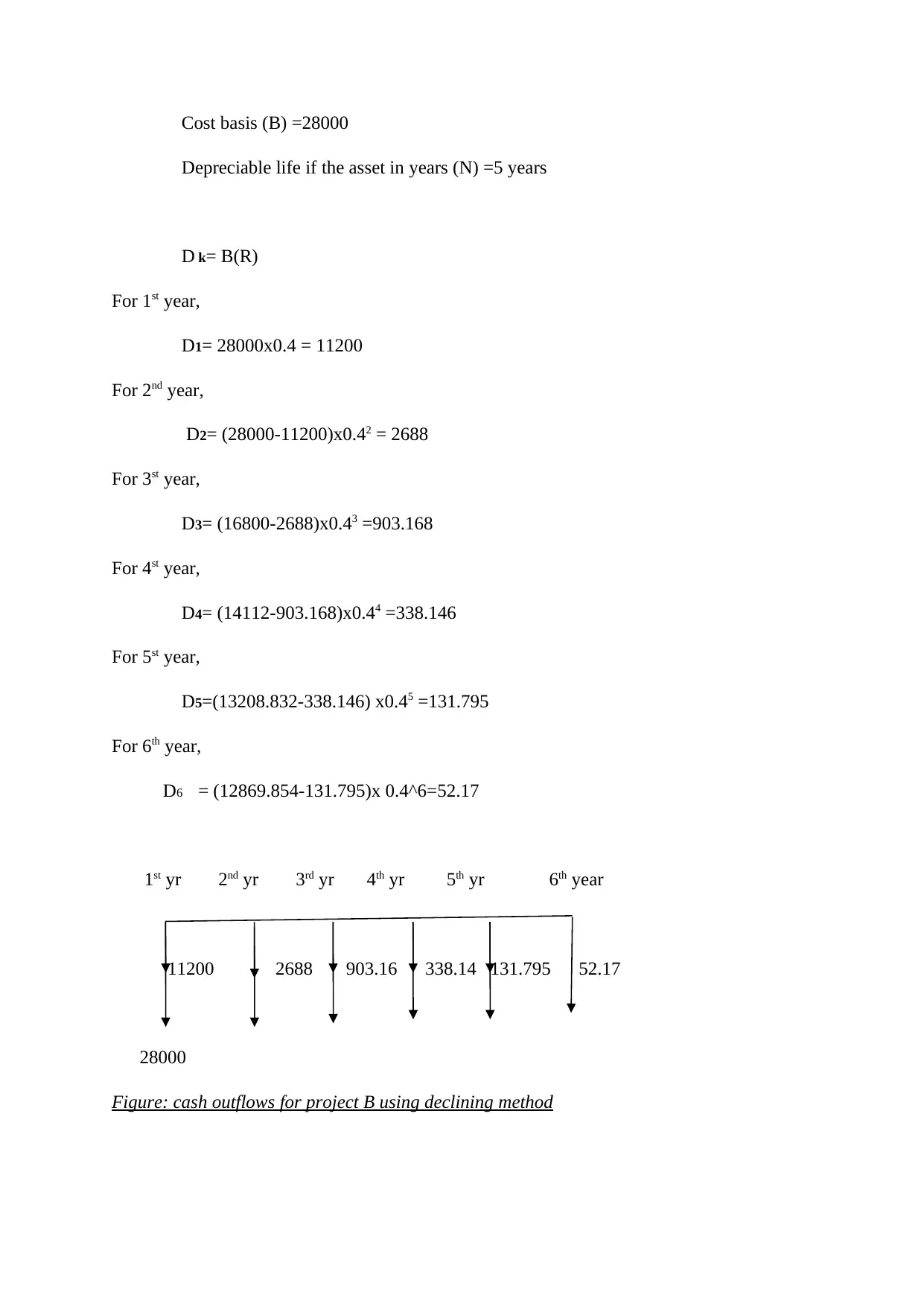

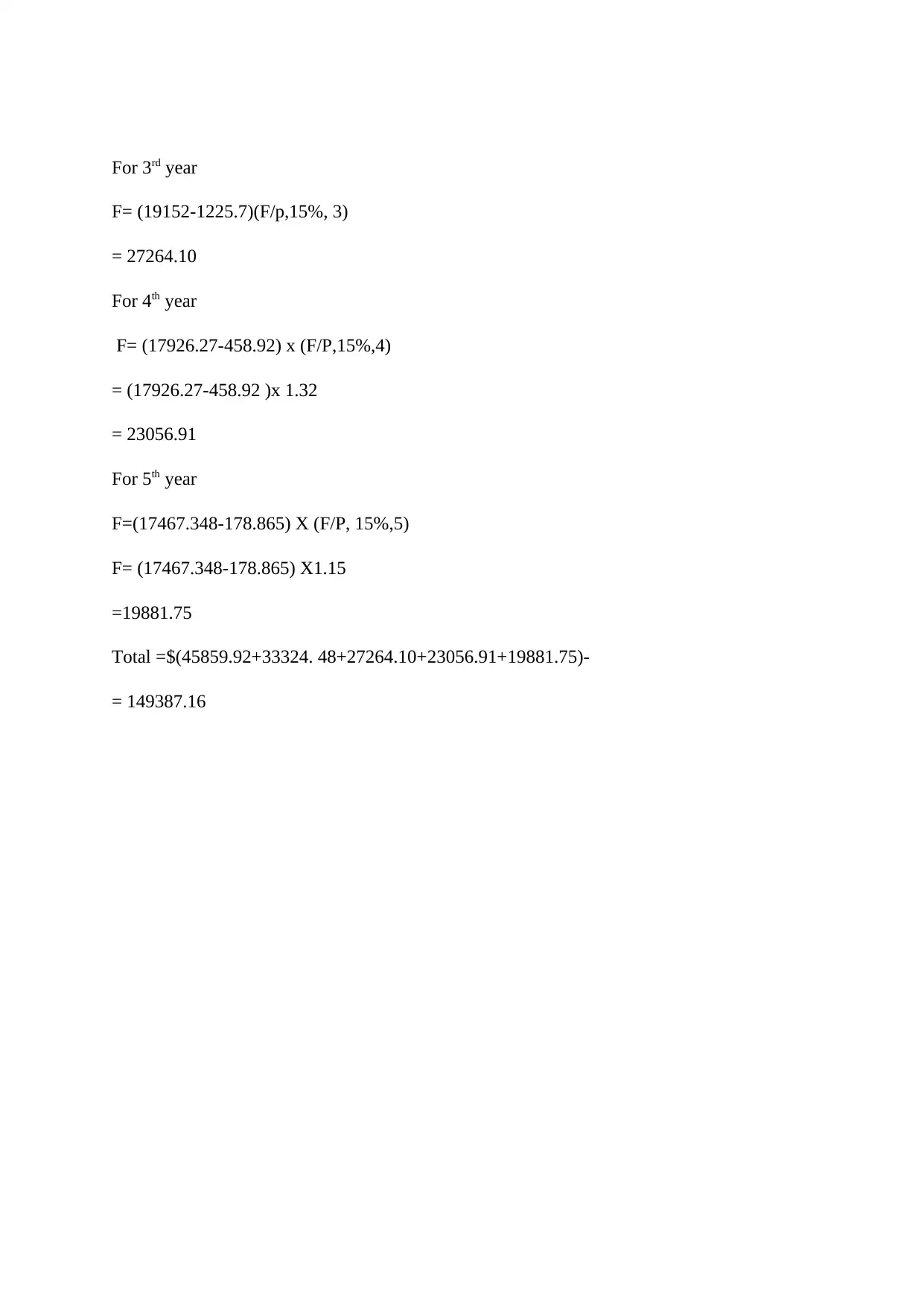

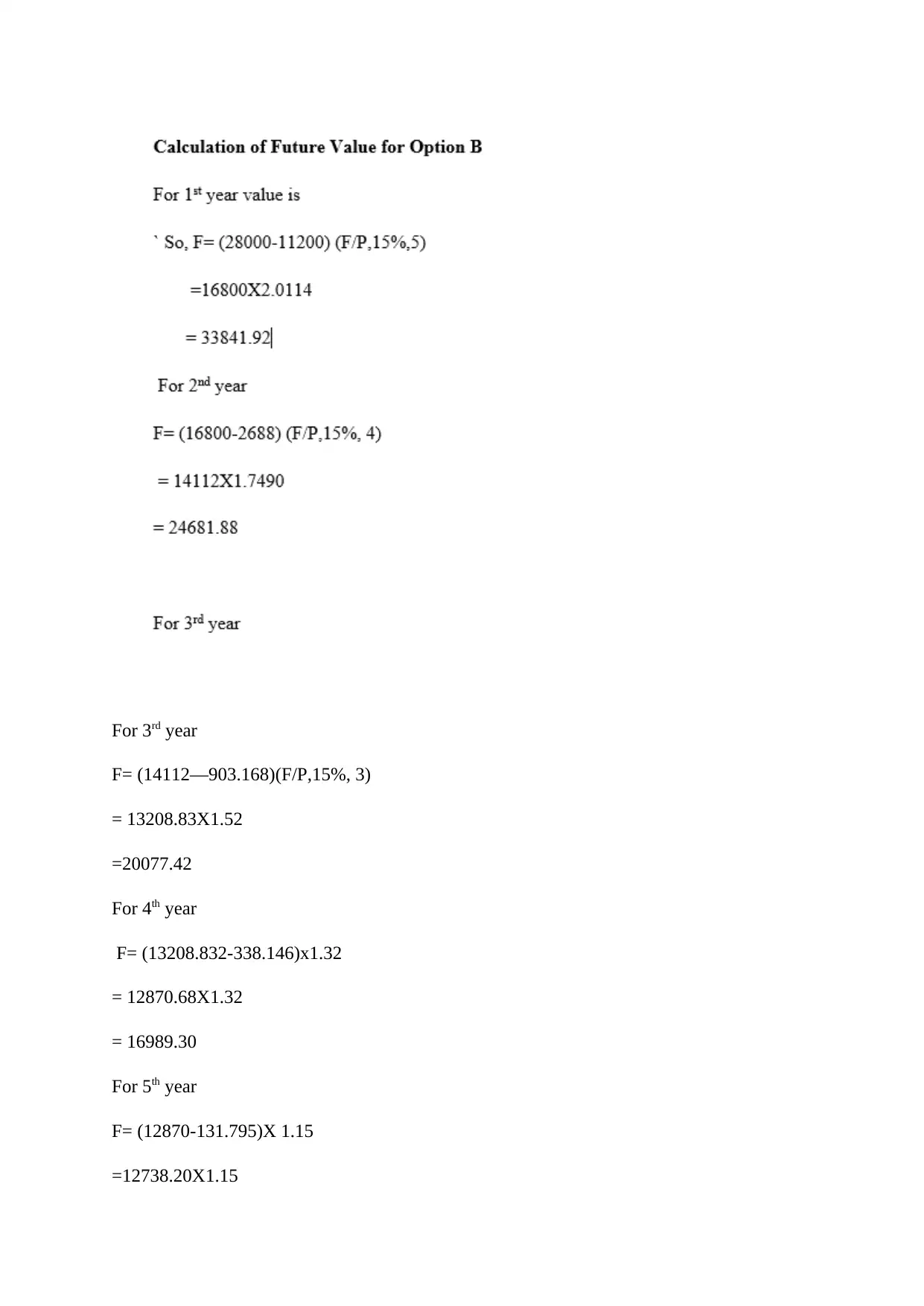

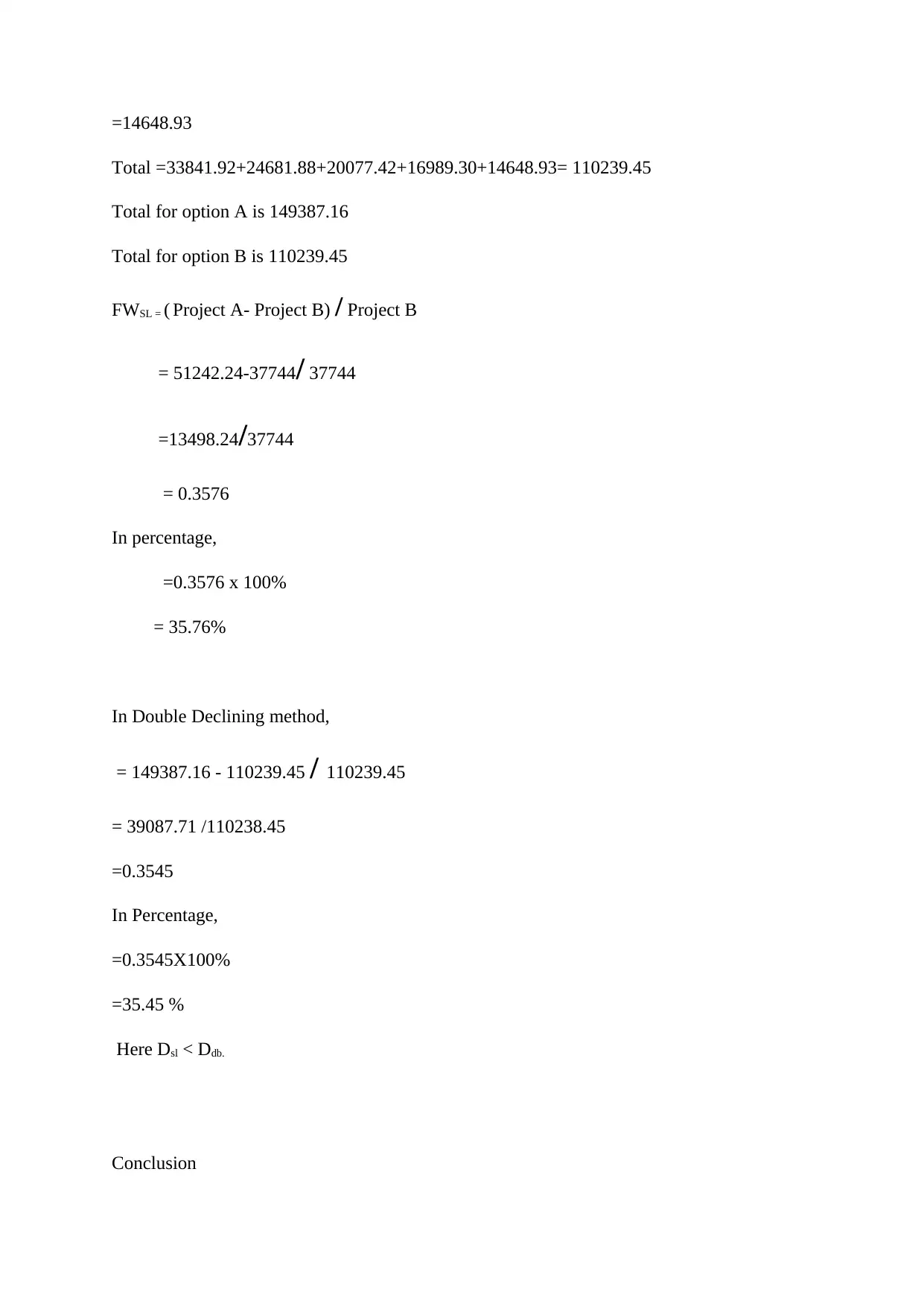

This report provides a detailed analysis of a computer assembly project, focusing on depreciation and sensitivity analysis. It calculates depreciation values for both buying and assembling computers, using both straight-line and declining balance methods over a five-year period. Cash flow diagrams are presented to illustrate the effectiveness of cash flows for each method. The report includes a sensitivity analysis to determine the impact of depreciation on the project's economics, and it calculates future values for both options to compare their profitability. The analysis concludes with a comparison of the two depreciation methods and a determination of the more appropriate alternative for the association.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.