Schlumberger Advance Taxation Case Study: Regulations and Ethics

VerifiedAdded on 2023/04/07

|5

|771

|120

Case Study

AI Summary

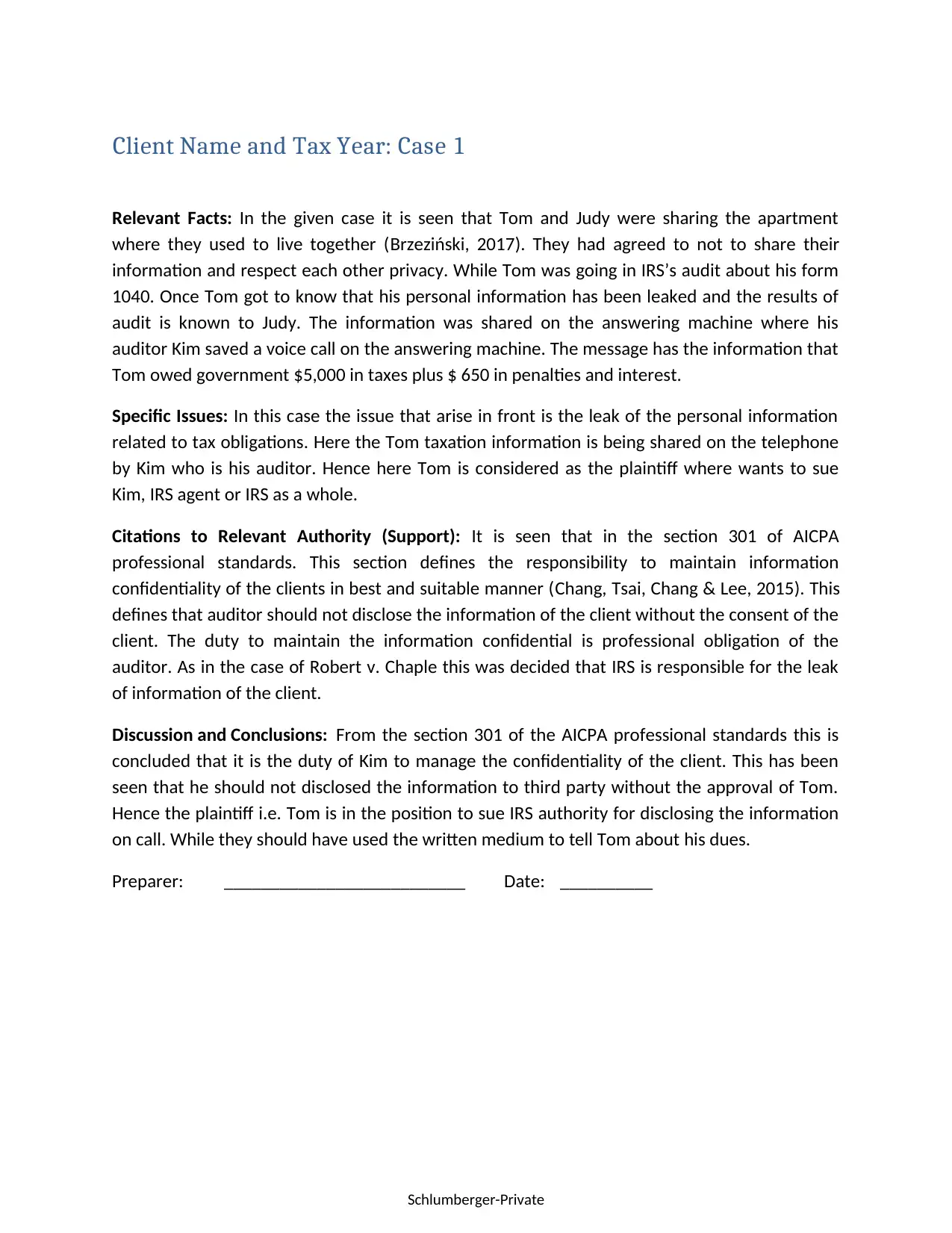

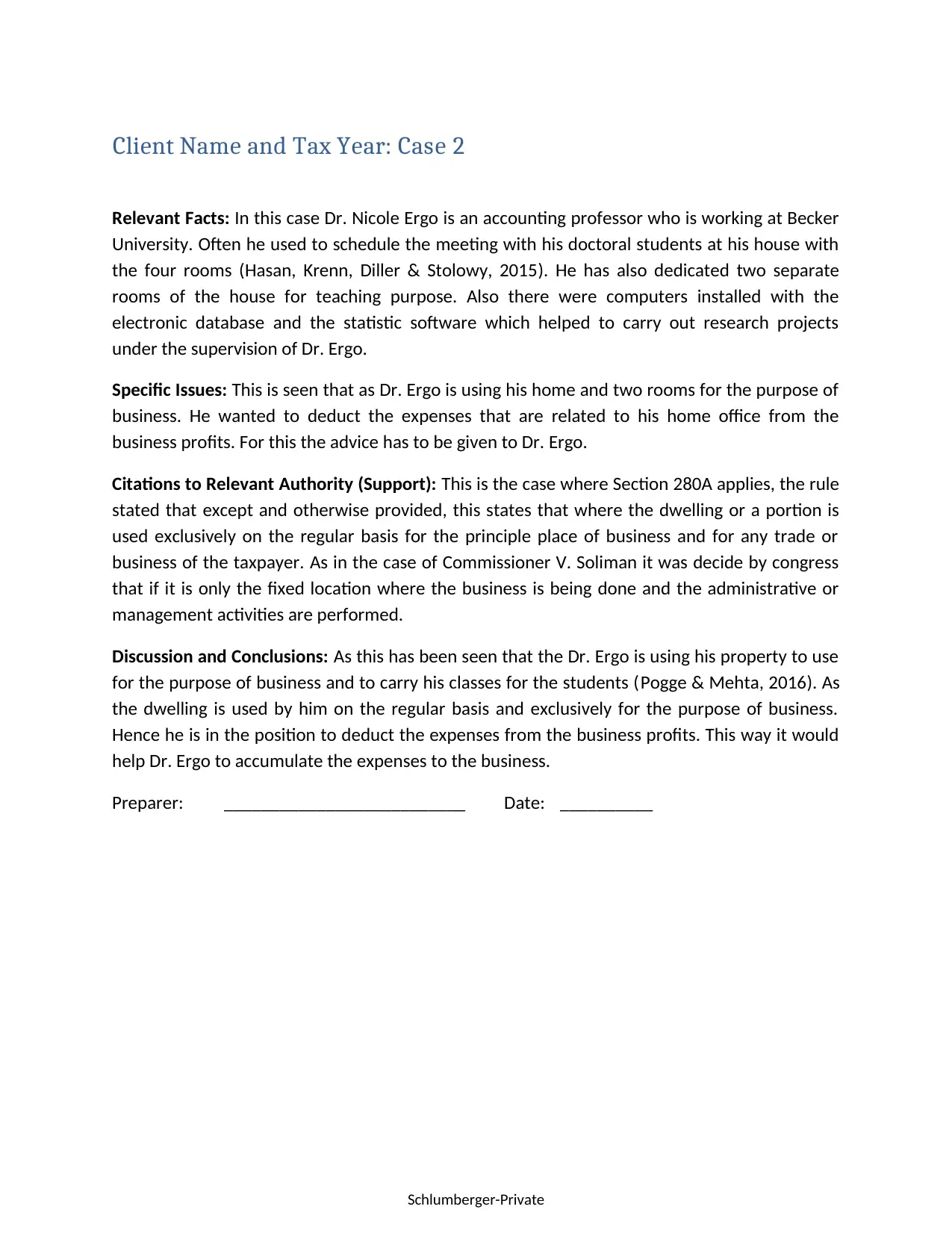

This assignment presents two case studies related to advance taxation. The first case involves Tom, whose tax information was leaked by his auditor, Kim, via an answering machine message, revealing that he owed the government $5,000 in taxes plus penalties and interest. The issue revolves around the violation of client confidentiality, referencing Section 301 of the AICPA professional standards, which mandates auditors to maintain client information confidentially. Tom has grounds to sue the IRS for the disclosure. The second case features Dr. Nicole Ergo, an accounting professor using two rooms in his house for teaching and research with doctoral students, seeking to deduct home office expenses. Applying Section 280A and the precedent set by Commissioner V. Soliman, it's determined that Dr. Ergo can deduct these expenses as the space is used exclusively and regularly for business purposes, aiding in accumulating business-related expenses. Desklib provides a platform for students to access similar solved assignments and past papers.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.