SOE11144 - Scylace plc: Business Economics and Finance Report

VerifiedAdded on 2023/01/19

|12

|3381

|81

Report

AI Summary

This report provides a comprehensive analysis of Scylace plc's potential business expansion strategies, focusing on building new superstores and acquiring Helibeb plc. It evaluates two superstore locations (A and B) based on cost, sales, and profitability, using metrics like annual profit and accounting rate of return. The report also examines different financing options, including issuing bonds with varying redemption periods and issuing new shares, assessing their impact on the cost of capital. Furthermore, it analyzes Helibeb plc's financial statements, calculating key ratios like return on shareholders' equity and turnover of capital employed to determine the viability of a takeover bid. The report concludes with recommendations on whether Scylace should invest in building superstores, acquire Helibeb, or pursue a combination of both strategies, considering profitability, market share, and capital adequacy.

BUSINESS ECONOMICS

AND FINANCE IN A

GLOBAL ENVIRONMENT

AND FINANCE IN A

GLOBAL ENVIRONMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Business economics and business finance provides an overall overview of economic theory

and the aspects of real business problems. This report extract the financial information of

Scylace plc which is a grocery retail industry. Company has a two alternatives as building a new

superstore and a proposal to make a takeover bid for Helibeb plc. These are the two options

available with organisation to build the superstore at one of the location. Scylace plc appointed a

management consultant in order to determine which option is most favourable for company and

helpful to attain future objectives and goals of organisation. Financial decision will be based

upon critical evaluation of using financial statements of Helibeb plc and the assessment of

financial ratios of Scylace plc.

This report is suggestive report for managers in order to recommend sustainable and

effective business option that may lead organisation towards consistent growth. In the report both

the options are evaluated on profitability, market hold and capital adequacy. The methodology in

the given study the following methods are used as business investment appraisal in resource

allocation and business goals, Cost of capital as business finance, financial statement ratio

calculation in financial reporting. Apart from it, the cause and impact of opting one option on

another also presented in such a manner so that managers be able to bifurcate the option as per

their organisational needs. In recommendation, two points are primary subject as whether both

the superstores should be build and second is at least one superstore should be built while

Scylace acquire Helibeb. The management consultant is required to suggest, either Scylace

should invest in first option of building the superstores or invest in second one which is building

one superstore with acquiring Helibeb plc.

Business economics and business finance provides an overall overview of economic theory

and the aspects of real business problems. This report extract the financial information of

Scylace plc which is a grocery retail industry. Company has a two alternatives as building a new

superstore and a proposal to make a takeover bid for Helibeb plc. These are the two options

available with organisation to build the superstore at one of the location. Scylace plc appointed a

management consultant in order to determine which option is most favourable for company and

helpful to attain future objectives and goals of organisation. Financial decision will be based

upon critical evaluation of using financial statements of Helibeb plc and the assessment of

financial ratios of Scylace plc.

This report is suggestive report for managers in order to recommend sustainable and

effective business option that may lead organisation towards consistent growth. In the report both

the options are evaluated on profitability, market hold and capital adequacy. The methodology in

the given study the following methods are used as business investment appraisal in resource

allocation and business goals, Cost of capital as business finance, financial statement ratio

calculation in financial reporting. Apart from it, the cause and impact of opting one option on

another also presented in such a manner so that managers be able to bifurcate the option as per

their organisational needs. In recommendation, two points are primary subject as whether both

the superstores should be build and second is at least one superstore should be built while

Scylace acquire Helibeb. The management consultant is required to suggest, either Scylace

should invest in first option of building the superstores or invest in second one which is building

one superstore with acquiring Helibeb plc.

Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

METHODOLOGY..........................................................................................................................1

Evaluation of the proposed new superstore location and prospective acquisition.................2

Recommendations..................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

METHODOLOGY..........................................................................................................................1

Evaluation of the proposed new superstore location and prospective acquisition.................2

Recommendations..................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Business finance and finance is a branch of financial management and control in numerous

sectors. It is recognised as an internal part of traditional economical trend which helps in

conducting the planning in decision making process. An in-depth study of accounting and

economic aspects of business finance helps in conducting the value positioning and connecting

the world to global financial market (Rugman and Verbeke, 2017). Management theory reflects

on corporation, leadership, and strategy-related problems. Problems and concerns involve: an

answer of why multinational companies take shape as well as arise; why they broaden: vertically,

laterally as well as spatially; the position of innovators and business people; the importance of

structure; the relationship between firms and employees, capital providers, clients and

administration; and relationships among industries or the economic climate. In this report the

managers of Scylace plc advised that which option will bring profitability in near future for

Scylace plc. Ratio analysis, capital investment appraisal and cost of capital techniques are used

for succeeding the business projects in long term duration (Isik and Bolat, 2016). The

recommendation regarding the relevant project is provided to managers to forecast business

probability in various streams. These are considered as a qualitative technique of calculating the

probability of proposed projects options.

METHODOLOGY

There are key methodologies used in the proposed business options which are defined as

follows:

Resource allocation and business goals

Business investment appraisal technique is mainly used in this section in order to

determine the probability and possibility of future profitability by choosing better options among

available alternatives (McNay, 2015). Investment assessment is mainly centralized on the initial

stages of a venture and system therefore, it is conducted in connection to earlier work on staff

schemes and distribution proposals (Raziq and Maulabakhsh, 2015). the presence of separate

scheduling or induction phases depends completely on the magnitude of both the project.

A portfolio to create coherent evaluation in all element projects as well as programs. This

method will be implemented in the resource allocation section as there are two options are

available to Scylace plc as option A and option B.

1

Business finance and finance is a branch of financial management and control in numerous

sectors. It is recognised as an internal part of traditional economical trend which helps in

conducting the planning in decision making process. An in-depth study of accounting and

economic aspects of business finance helps in conducting the value positioning and connecting

the world to global financial market (Rugman and Verbeke, 2017). Management theory reflects

on corporation, leadership, and strategy-related problems. Problems and concerns involve: an

answer of why multinational companies take shape as well as arise; why they broaden: vertically,

laterally as well as spatially; the position of innovators and business people; the importance of

structure; the relationship between firms and employees, capital providers, clients and

administration; and relationships among industries or the economic climate. In this report the

managers of Scylace plc advised that which option will bring profitability in near future for

Scylace plc. Ratio analysis, capital investment appraisal and cost of capital techniques are used

for succeeding the business projects in long term duration (Isik and Bolat, 2016). The

recommendation regarding the relevant project is provided to managers to forecast business

probability in various streams. These are considered as a qualitative technique of calculating the

probability of proposed projects options.

METHODOLOGY

There are key methodologies used in the proposed business options which are defined as

follows:

Resource allocation and business goals

Business investment appraisal technique is mainly used in this section in order to

determine the probability and possibility of future profitability by choosing better options among

available alternatives (McNay, 2015). Investment assessment is mainly centralized on the initial

stages of a venture and system therefore, it is conducted in connection to earlier work on staff

schemes and distribution proposals (Raziq and Maulabakhsh, 2015). the presence of separate

scheduling or induction phases depends completely on the magnitude of both the project.

A portfolio to create coherent evaluation in all element projects as well as programs. This

method will be implemented in the resource allocation section as there are two options are

available to Scylace plc as option A and option B.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

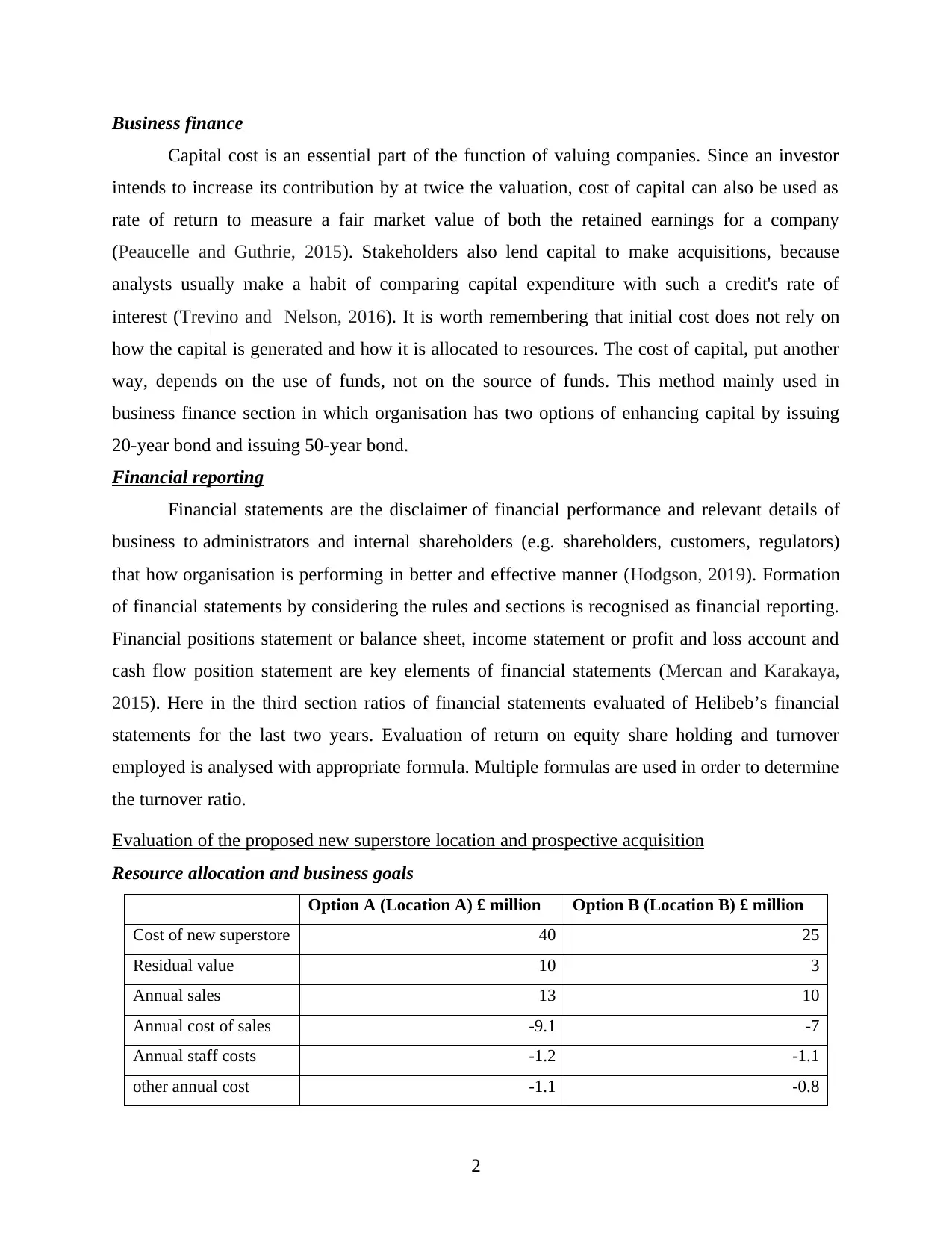

Business finance

Capital cost is an essential part of the function of valuing companies. Since an investor

intends to increase its contribution by at twice the valuation, cost of capital can also be used as

rate of return to measure a fair market value of both the retained earnings for a company

(Peaucelle and Guthrie, 2015). Stakeholders also lend capital to make acquisitions, because

analysts usually make a habit of comparing capital expenditure with such a credit's rate of

interest (Trevino and Nelson, 2016). It is worth remembering that initial cost does not rely on

how the capital is generated and how it is allocated to resources. The cost of capital, put another

way, depends on the use of funds, not on the source of funds. This method mainly used in

business finance section in which organisation has two options of enhancing capital by issuing

20-year bond and issuing 50-year bond.

Financial reporting

Financial statements are the disclaimer of financial performance and relevant details of

business to administrators and internal shareholders (e.g. shareholders, customers, regulators)

that how organisation is performing in better and effective manner (Hodgson, 2019). Formation

of financial statements by considering the rules and sections is recognised as financial reporting.

Financial positions statement or balance sheet, income statement or profit and loss account and

cash flow position statement are key elements of financial statements (Mercan and Karakaya,

2015). Here in the third section ratios of financial statements evaluated of Helibeb’s financial

statements for the last two years. Evaluation of return on equity share holding and turnover

employed is analysed with appropriate formula. Multiple formulas are used in order to determine

the turnover ratio.

Evaluation of the proposed new superstore location and prospective acquisition

Resource allocation and business goals

Option A (Location A) £ million Option B (Location B) £ million

Cost of new superstore 40 25

Residual value 10 3

Annual sales 13 10

Annual cost of sales -9.1 -7

Annual staff costs -1.2 -1.1

other annual cost -1.1 -0.8

2

Capital cost is an essential part of the function of valuing companies. Since an investor

intends to increase its contribution by at twice the valuation, cost of capital can also be used as

rate of return to measure a fair market value of both the retained earnings for a company

(Peaucelle and Guthrie, 2015). Stakeholders also lend capital to make acquisitions, because

analysts usually make a habit of comparing capital expenditure with such a credit's rate of

interest (Trevino and Nelson, 2016). It is worth remembering that initial cost does not rely on

how the capital is generated and how it is allocated to resources. The cost of capital, put another

way, depends on the use of funds, not on the source of funds. This method mainly used in

business finance section in which organisation has two options of enhancing capital by issuing

20-year bond and issuing 50-year bond.

Financial reporting

Financial statements are the disclaimer of financial performance and relevant details of

business to administrators and internal shareholders (e.g. shareholders, customers, regulators)

that how organisation is performing in better and effective manner (Hodgson, 2019). Formation

of financial statements by considering the rules and sections is recognised as financial reporting.

Financial positions statement or balance sheet, income statement or profit and loss account and

cash flow position statement are key elements of financial statements (Mercan and Karakaya,

2015). Here in the third section ratios of financial statements evaluated of Helibeb’s financial

statements for the last two years. Evaluation of return on equity share holding and turnover

employed is analysed with appropriate formula. Multiple formulas are used in order to determine

the turnover ratio.

Evaluation of the proposed new superstore location and prospective acquisition

Resource allocation and business goals

Option A (Location A) £ million Option B (Location B) £ million

Cost of new superstore 40 25

Residual value 10 3

Annual sales 13 10

Annual cost of sales -9.1 -7

Annual staff costs -1.2 -1.1

other annual cost -1.1 -0.8

2

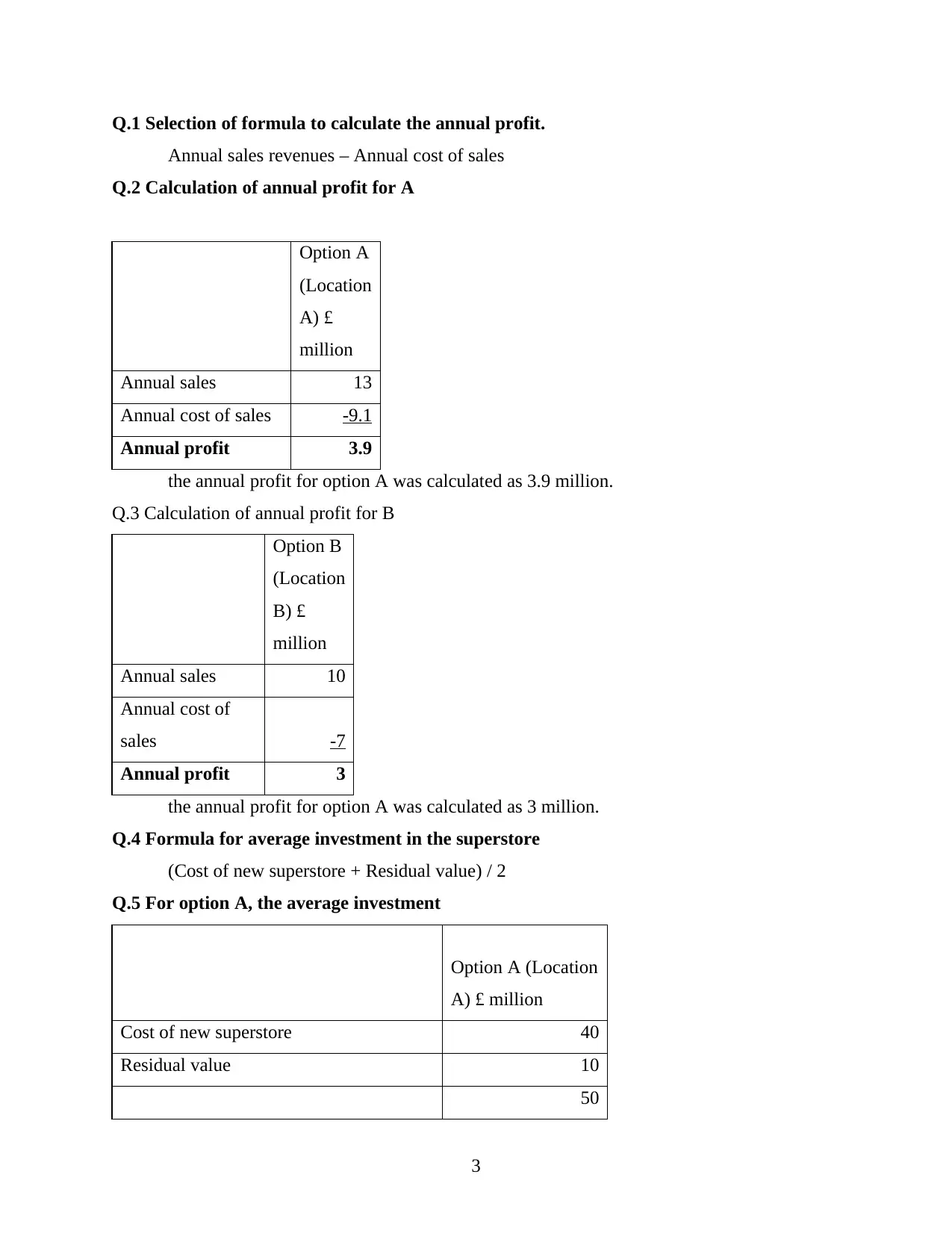

Q.1 Selection of formula to calculate the annual profit.

Annual sales revenues – Annual cost of sales

Q.2 Calculation of annual profit for A

Option A

(Location

A) £

million

Annual sales 13

Annual cost of sales -9.1

Annual profit 3.9

the annual profit for option A was calculated as 3.9 million.

Q.3 Calculation of annual profit for B

Option B

(Location

B) £

million

Annual sales 10

Annual cost of

sales -7

Annual profit 3

the annual profit for option A was calculated as 3 million.

Q.4 Formula for average investment in the superstore

(Cost of new superstore + Residual value) / 2

Q.5 For option A, the average investment

Option A (Location

A) £ million

Cost of new superstore 40

Residual value 10

50

3

Annual sales revenues – Annual cost of sales

Q.2 Calculation of annual profit for A

Option A

(Location

A) £

million

Annual sales 13

Annual cost of sales -9.1

Annual profit 3.9

the annual profit for option A was calculated as 3.9 million.

Q.3 Calculation of annual profit for B

Option B

(Location

B) £

million

Annual sales 10

Annual cost of

sales -7

Annual profit 3

the annual profit for option A was calculated as 3 million.

Q.4 Formula for average investment in the superstore

(Cost of new superstore + Residual value) / 2

Q.5 For option A, the average investment

Option A (Location

A) £ million

Cost of new superstore 40

Residual value 10

50

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Average investment 50/2=25

The average investment for option A is calculated as £ 25 million.

Q.6 For option B, the average investment

Option B (Location

B) £ million

Cost of new superstore 25

Residual value 3

28

Average investment 28/2 = 14

The average investment for option B is calculated as £ 14 million.

Q.7 Formula for the accounting rate of return

Annual profit / average investment

Q.8 Accounting rate of return for Option A

Average rate of return is calculated as 4% in option A

Q.9 Accounting rate of return for Option B

Average rate of return is calculated as 4.71% in option A

From the above computations it is resulted that both the locations are profitable for

Scylace plc. However, annual profit is higher at location A compared to location B but the

accounting rate of return is higher in option B comparatively to option A. after evaluating the

reason behind the difference, it is ensued that the investment made at location A is £22 million

higher that location b and return on investment rate is lower even after incurring heavy

investment. After all, both the projects are favourable for company. If Scylace plc would have to

choose among one option than option B will be beneficial in longer run.

Business finance

Scylace plc have an additional three alternative proposals in terms of financial expansion

as

a) To issue a bond redeemable in 20 years

b) To issue a bond redeemable in 50 years

c) To issue new shares

4

The average investment for option A is calculated as £ 25 million.

Q.6 For option B, the average investment

Option B (Location

B) £ million

Cost of new superstore 25

Residual value 3

28

Average investment 28/2 = 14

The average investment for option B is calculated as £ 14 million.

Q.7 Formula for the accounting rate of return

Annual profit / average investment

Q.8 Accounting rate of return for Option A

Average rate of return is calculated as 4% in option A

Q.9 Accounting rate of return for Option B

Average rate of return is calculated as 4.71% in option A

From the above computations it is resulted that both the locations are profitable for

Scylace plc. However, annual profit is higher at location A compared to location B but the

accounting rate of return is higher in option B comparatively to option A. after evaluating the

reason behind the difference, it is ensued that the investment made at location A is £22 million

higher that location b and return on investment rate is lower even after incurring heavy

investment. After all, both the projects are favourable for company. If Scylace plc would have to

choose among one option than option B will be beneficial in longer run.

Business finance

Scylace plc have an additional three alternative proposals in terms of financial expansion

as

a) To issue a bond redeemable in 20 years

b) To issue a bond redeemable in 50 years

c) To issue new shares

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

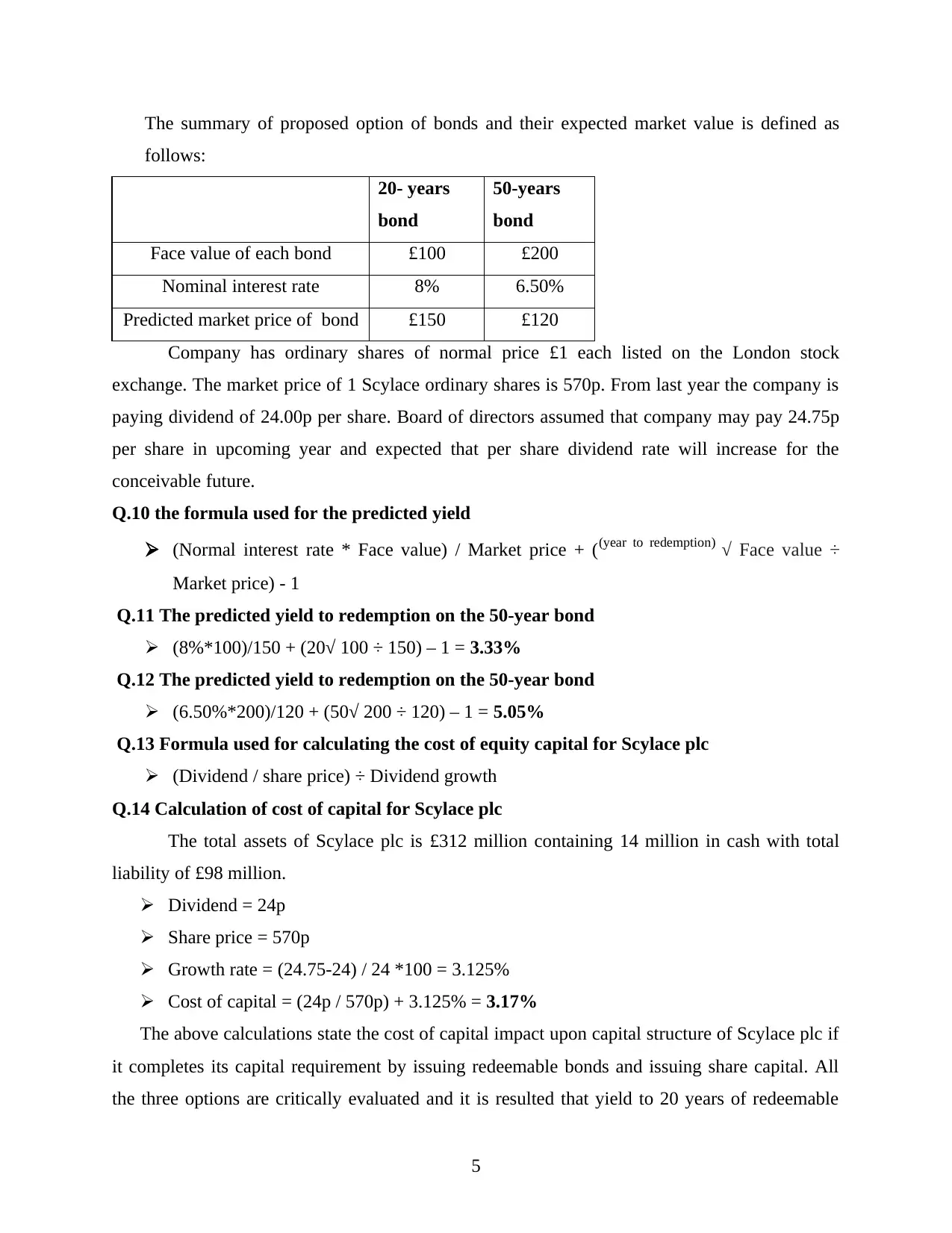

The summary of proposed option of bonds and their expected market value is defined as

follows:

20- years

bond

50-years

bond

Face value of each bond £100 £200

Nominal interest rate 8% 6.50%

Predicted market price of bond £150 £120

Company has ordinary shares of normal price £1 each listed on the London stock

exchange. The market price of 1 Scylace ordinary shares is 570p. From last year the company is

paying dividend of 24.00p per share. Board of directors assumed that company may pay 24.75p

per share in upcoming year and expected that per share dividend rate will increase for the

conceivable future.

Q.10 the formula used for the predicted yield

(Normal interest rate * Face value) / Market price + ((year to redemption) √ Face value ÷

Market price) - 1

Q.11 The predicted yield to redemption on the 50-year bond

(8%*100)/150 + (20√ 100 ÷ 150) – 1 = 3.33%

Q.12 The predicted yield to redemption on the 50-year bond

(6.50%*200)/120 + (50√ 200 ÷ 120) – 1 = 5.05%

Q.13 Formula used for calculating the cost of equity capital for Scylace plc

(Dividend / share price) ÷ Dividend growth

Q.14 Calculation of cost of capital for Scylace plc

The total assets of Scylace plc is £312 million containing 14 million in cash with total

liability of £98 million.

Dividend = 24p

Share price = 570p

Growth rate = (24.75-24) / 24 *100 = 3.125%

Cost of capital = (24p / 570p) + 3.125% = 3.17%

The above calculations state the cost of capital impact upon capital structure of Scylace plc if

it completes its capital requirement by issuing redeemable bonds and issuing share capital. All

the three options are critically evaluated and it is resulted that yield to 20 years of redeemable

5

follows:

20- years

bond

50-years

bond

Face value of each bond £100 £200

Nominal interest rate 8% 6.50%

Predicted market price of bond £150 £120

Company has ordinary shares of normal price £1 each listed on the London stock

exchange. The market price of 1 Scylace ordinary shares is 570p. From last year the company is

paying dividend of 24.00p per share. Board of directors assumed that company may pay 24.75p

per share in upcoming year and expected that per share dividend rate will increase for the

conceivable future.

Q.10 the formula used for the predicted yield

(Normal interest rate * Face value) / Market price + ((year to redemption) √ Face value ÷

Market price) - 1

Q.11 The predicted yield to redemption on the 50-year bond

(8%*100)/150 + (20√ 100 ÷ 150) – 1 = 3.33%

Q.12 The predicted yield to redemption on the 50-year bond

(6.50%*200)/120 + (50√ 200 ÷ 120) – 1 = 5.05%

Q.13 Formula used for calculating the cost of equity capital for Scylace plc

(Dividend / share price) ÷ Dividend growth

Q.14 Calculation of cost of capital for Scylace plc

The total assets of Scylace plc is £312 million containing 14 million in cash with total

liability of £98 million.

Dividend = 24p

Share price = 570p

Growth rate = (24.75-24) / 24 *100 = 3.125%

Cost of capital = (24p / 570p) + 3.125% = 3.17%

The above calculations state the cost of capital impact upon capital structure of Scylace plc if

it completes its capital requirement by issuing redeemable bonds and issuing share capital. All

the three options are critically evaluated and it is resulted that yield to 20 years of redeemable

5

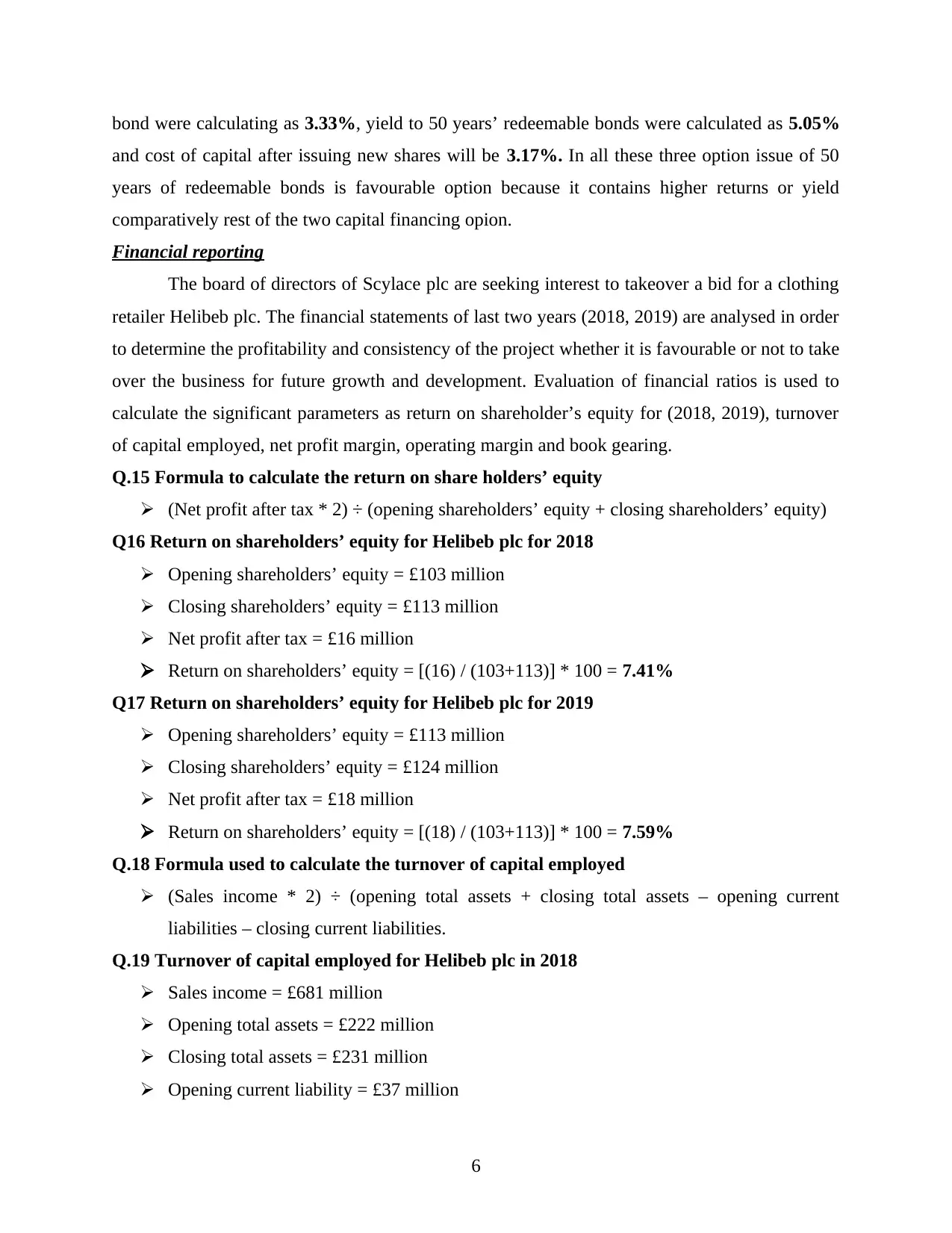

bond were calculating as 3.33%, yield to 50 years’ redeemable bonds were calculated as 5.05%

and cost of capital after issuing new shares will be 3.17%. In all these three option issue of 50

years of redeemable bonds is favourable option because it contains higher returns or yield

comparatively rest of the two capital financing opion.

Financial reporting

The board of directors of Scylace plc are seeking interest to takeover a bid for a clothing

retailer Helibeb plc. The financial statements of last two years (2018, 2019) are analysed in order

to determine the profitability and consistency of the project whether it is favourable or not to take

over the business for future growth and development. Evaluation of financial ratios is used to

calculate the significant parameters as return on shareholder’s equity for (2018, 2019), turnover

of capital employed, net profit margin, operating margin and book gearing.

Q.15 Formula to calculate the return on share holders’ equity

(Net profit after tax * 2) ÷ (opening shareholders’ equity + closing shareholders’ equity)

Q16 Return on shareholders’ equity for Helibeb plc for 2018

Opening shareholders’ equity = £103 million

Closing shareholders’ equity = £113 million

Net profit after tax = £16 million

Return on shareholders’ equity = [(16) / (103+113)] * 100 = 7.41%

Q17 Return on shareholders’ equity for Helibeb plc for 2019

Opening shareholders’ equity = £113 million

Closing shareholders’ equity = £124 million

Net profit after tax = £18 million

Return on shareholders’ equity = [(18) / (103+113)] * 100 = 7.59%

Q.18 Formula used to calculate the turnover of capital employed

(Sales income * 2) ÷ (opening total assets + closing total assets – opening current

liabilities – closing current liabilities.

Q.19 Turnover of capital employed for Helibeb plc in 2018

Sales income = £681 million

Opening total assets = £222 million

Closing total assets = £231 million

Opening current liability = £37 million

6

and cost of capital after issuing new shares will be 3.17%. In all these three option issue of 50

years of redeemable bonds is favourable option because it contains higher returns or yield

comparatively rest of the two capital financing opion.

Financial reporting

The board of directors of Scylace plc are seeking interest to takeover a bid for a clothing

retailer Helibeb plc. The financial statements of last two years (2018, 2019) are analysed in order

to determine the profitability and consistency of the project whether it is favourable or not to take

over the business for future growth and development. Evaluation of financial ratios is used to

calculate the significant parameters as return on shareholder’s equity for (2018, 2019), turnover

of capital employed, net profit margin, operating margin and book gearing.

Q.15 Formula to calculate the return on share holders’ equity

(Net profit after tax * 2) ÷ (opening shareholders’ equity + closing shareholders’ equity)

Q16 Return on shareholders’ equity for Helibeb plc for 2018

Opening shareholders’ equity = £103 million

Closing shareholders’ equity = £113 million

Net profit after tax = £16 million

Return on shareholders’ equity = [(16) / (103+113)] * 100 = 7.41%

Q17 Return on shareholders’ equity for Helibeb plc for 2019

Opening shareholders’ equity = £113 million

Closing shareholders’ equity = £124 million

Net profit after tax = £18 million

Return on shareholders’ equity = [(18) / (103+113)] * 100 = 7.59%

Q.18 Formula used to calculate the turnover of capital employed

(Sales income * 2) ÷ (opening total assets + closing total assets – opening current

liabilities – closing current liabilities.

Q.19 Turnover of capital employed for Helibeb plc in 2018

Sales income = £681 million

Opening total assets = £222 million

Closing total assets = £231 million

Opening current liability = £37 million

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Closing current liability = £38 million

Capital employed = (681*2) / (222+231-37-38) = 3.53%

Q. 20 Turnover of capital employed for Helibeb plc in 2019

Sales income = £697 million

Opening total assets = £231 million

Closing total assets = £240 million

Opening current liability = £38 million

Closing current liability = £40 million

Capital employed = (697*2) / (231+240-38-40) = 2.90%

Q.21 Formula to calculate the net profit margin

Net profit after tax / sales income

Q.22 Net profit margin for Helibeb plc in 2018

Net profit after tax = £16 million

Sales income for 2018 = £681 million

Net profit margin = 16 / 681 = 2.35%

Q.23 Net profit margin for Helibeb plc in 2019

Net profit after tax = £18 million

Sales income for 2018 = £697 million

Net profit margin = 18 / 697 = 2.58%

Q.24 Formula for operating margin

Operating profit / sales income

Q.25 Operating margin for Helibeb plc in 2018

Net profit after tax = £19 million

Sales income for 2018 = £681 million

Operating margin = 29 / 681 = 2.35%

Q.26 Operating margin for Helibeb plc in 2019

Net profit after tax = £22 million

Sales income for 2018 = £697 million

Operating margin = 22 / 697 = 3.16%

Q.28 to 30 the book gearing ratios

7

Capital employed = (681*2) / (222+231-37-38) = 3.53%

Q. 20 Turnover of capital employed for Helibeb plc in 2019

Sales income = £697 million

Opening total assets = £231 million

Closing total assets = £240 million

Opening current liability = £38 million

Closing current liability = £40 million

Capital employed = (697*2) / (231+240-38-40) = 2.90%

Q.21 Formula to calculate the net profit margin

Net profit after tax / sales income

Q.22 Net profit margin for Helibeb plc in 2018

Net profit after tax = £16 million

Sales income for 2018 = £681 million

Net profit margin = 16 / 681 = 2.35%

Q.23 Net profit margin for Helibeb plc in 2019

Net profit after tax = £18 million

Sales income for 2018 = £697 million

Net profit margin = 18 / 697 = 2.58%

Q.24 Formula for operating margin

Operating profit / sales income

Q.25 Operating margin for Helibeb plc in 2018

Net profit after tax = £19 million

Sales income for 2018 = £681 million

Operating margin = 29 / 681 = 2.35%

Q.26 Operating margin for Helibeb plc in 2019

Net profit after tax = £22 million

Sales income for 2018 = £697 million

Operating margin = 22 / 697 = 3.16%

Q.28 to 30 the book gearing ratios

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The book gearing ratios for 2017, 2018, 2019 for subsequently as 53.6%, 51.8% and

48.33%.

Recommendations

The assessment of financial performance and capital financing options for Scylace plc is

evaluated above which states that if company must be choosing option b to build a new super

store at location B and acquire helibeb plc. It is evaluated that for long term perspective the

option b will provide long term feasibility. Financial evaluation of Helibeb plc presents that the

financial perforce of company is increasing year by year. net profitability, operating margin and

return on capital employed. It is observed that gearing ratio also get decreased in terms which

present that even after having profitability the debts are increasing. This sign provides a

favourable sign to take over the company.

CONCLUSION

The above report presents the economic study for business finance in order to determine the

efficient financial aspects. In the report the organisation is suggested a better option for better

capital and financing growth and development of business. It is resulted that financial

measurement tools as cost of capital, financial ratios evaluation and investment appraisal are

essential elements that provides a brief overview for further investment and growth

opportunities.

8

48.33%.

Recommendations

The assessment of financial performance and capital financing options for Scylace plc is

evaluated above which states that if company must be choosing option b to build a new super

store at location B and acquire helibeb plc. It is evaluated that for long term perspective the

option b will provide long term feasibility. Financial evaluation of Helibeb plc presents that the

financial perforce of company is increasing year by year. net profitability, operating margin and

return on capital employed. It is observed that gearing ratio also get decreased in terms which

present that even after having profitability the debts are increasing. This sign provides a

favourable sign to take over the company.

CONCLUSION

The above report presents the economic study for business finance in order to determine the

efficient financial aspects. In the report the organisation is suggested a better option for better

capital and financing growth and development of business. It is resulted that financial

measurement tools as cost of capital, financial ratios evaluation and investment appraisal are

essential elements that provides a brief overview for further investment and growth

opportunities.

8

REFERENCES

Books and Journals:

Rugman, A. M., & Verbeke, A. (2017). Global corporate strategy and trade policy. Routledge.

Raziq, A. & Maulabakhsh, R., (2015). Impact of working environment on job

satisfaction. Procedia Economics and Finance. 23. pp.717-725.

Peaucelle, J. L., & Guthrie, C. (2015). Henri Fayol. In The Oxford Handbook of Management

Theorists.

Mercan, M., & Karakaya, E. (2015). Energy consumption, economic growth and carbon

emission: Dynamic panel cointegration analysis for selected OECD countries. Procedia

Economics and Finance. 23. 587-592.

Isik, O., & Bolat, S. (2016). Determinants of non-performing loans of deposit banks in

Turkey. Journal of Business, Economics and Finance. 5(4). 341-350.

McNay, L. (2015). Agency. In The Oxford handbook of feminist theory.

Trevino, L. K., & Nelson, K. A. (2016). Managing business ethics: Straight talk about how to do

it right. John Wiley & Sons.

Hodgson, G. M. (2019). The great crash of 2008 and the reform of economics. In The Handbook

of Globalisation, Third Edition. Edward Elgar Publishing.

Lew, A. A., & Cheer, J. M. (Eds.). (2017). Tourism resilience and adaptation to environmental

change: Definitions and frameworks. Routledge.

Belabes, A., Belouafi, A., & Daoudi, M. (2015). Designing Islamic Finance Programmes in a

Competitive Educational Space: The Islamic Economics Institute Experiment. Procedia-

Social and Behavioral Sciences. 191. 639-643.

Sumedrea, S. (2015). How the companies did structure their capital to surpass crises?. Procedia

Economics and Finance, 27, 22-28.

Taghian, M., D’Souza, C., & Polonsky, M. (2015). A stakeholder approach to corporate social

responsibility, reputation and business performance. Social Responsibility Journal. 11(2).

340-363.

Terjesen, S., Bosma, N., & Stam, E. (2016). Advancing public policy for high‐growth, female,

and social entrepreneurs. Public Administration Review. 76(2). 230-239.

Caliendo, M., Fossen, F. & Kritikos, A. S. (2014). Personality characteristics and the decisions to

become and stay self-employed. Small Business Economics. 42(4). pp.787-814.

Aronczyk, M. (2013). Branding the nation: The global business of national identity. Oxford

University Press.

Kula, E. (2012). Economics of natural resources, the environment and policies. Springer Science

& Business Media.

Murray, A., Skene, K. & Haynes, K. (2017). The circular economy: an interdisciplinary

exploration of the concept and application in a global context. Journal of Business Ethics.

140(3). pp.369-380.

Cogo, B. (2018). The impact of high-tech startups' ecosystems on economic systems'

development: the case of Israel (Bachelor's thesis, Università Ca'Foscari Venezia).

Renko, M., Kroeck, K. G., & Bullough, A. (2012). Expectancy theory and nascent

entrepreneurship. Small Business Economics. 39(3). 667-684.

Polus, J. (2019). Succesfactoren om kruisbestuiving tussen bedrijven te creëren in een incubator

context (Master's thesis, UHasselt).

9

Books and Journals:

Rugman, A. M., & Verbeke, A. (2017). Global corporate strategy and trade policy. Routledge.

Raziq, A. & Maulabakhsh, R., (2015). Impact of working environment on job

satisfaction. Procedia Economics and Finance. 23. pp.717-725.

Peaucelle, J. L., & Guthrie, C. (2015). Henri Fayol. In The Oxford Handbook of Management

Theorists.

Mercan, M., & Karakaya, E. (2015). Energy consumption, economic growth and carbon

emission: Dynamic panel cointegration analysis for selected OECD countries. Procedia

Economics and Finance. 23. 587-592.

Isik, O., & Bolat, S. (2016). Determinants of non-performing loans of deposit banks in

Turkey. Journal of Business, Economics and Finance. 5(4). 341-350.

McNay, L. (2015). Agency. In The Oxford handbook of feminist theory.

Trevino, L. K., & Nelson, K. A. (2016). Managing business ethics: Straight talk about how to do

it right. John Wiley & Sons.

Hodgson, G. M. (2019). The great crash of 2008 and the reform of economics. In The Handbook

of Globalisation, Third Edition. Edward Elgar Publishing.

Lew, A. A., & Cheer, J. M. (Eds.). (2017). Tourism resilience and adaptation to environmental

change: Definitions and frameworks. Routledge.

Belabes, A., Belouafi, A., & Daoudi, M. (2015). Designing Islamic Finance Programmes in a

Competitive Educational Space: The Islamic Economics Institute Experiment. Procedia-

Social and Behavioral Sciences. 191. 639-643.

Sumedrea, S. (2015). How the companies did structure their capital to surpass crises?. Procedia

Economics and Finance, 27, 22-28.

Taghian, M., D’Souza, C., & Polonsky, M. (2015). A stakeholder approach to corporate social

responsibility, reputation and business performance. Social Responsibility Journal. 11(2).

340-363.

Terjesen, S., Bosma, N., & Stam, E. (2016). Advancing public policy for high‐growth, female,

and social entrepreneurs. Public Administration Review. 76(2). 230-239.

Caliendo, M., Fossen, F. & Kritikos, A. S. (2014). Personality characteristics and the decisions to

become and stay self-employed. Small Business Economics. 42(4). pp.787-814.

Aronczyk, M. (2013). Branding the nation: The global business of national identity. Oxford

University Press.

Kula, E. (2012). Economics of natural resources, the environment and policies. Springer Science

& Business Media.

Murray, A., Skene, K. & Haynes, K. (2017). The circular economy: an interdisciplinary

exploration of the concept and application in a global context. Journal of Business Ethics.

140(3). pp.369-380.

Cogo, B. (2018). The impact of high-tech startups' ecosystems on economic systems'

development: the case of Israel (Bachelor's thesis, Università Ca'Foscari Venezia).

Renko, M., Kroeck, K. G., & Bullough, A. (2012). Expectancy theory and nascent

entrepreneurship. Small Business Economics. 39(3). 667-684.

Polus, J. (2019). Succesfactoren om kruisbestuiving tussen bedrijven te creëren in een incubator

context (Master's thesis, UHasselt).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.