Audit Report of Madoff Investment Securities LLC: A Detailed Analysis

VerifiedAdded on 2023/06/13

|9

|1770

|56

Report

AI Summary

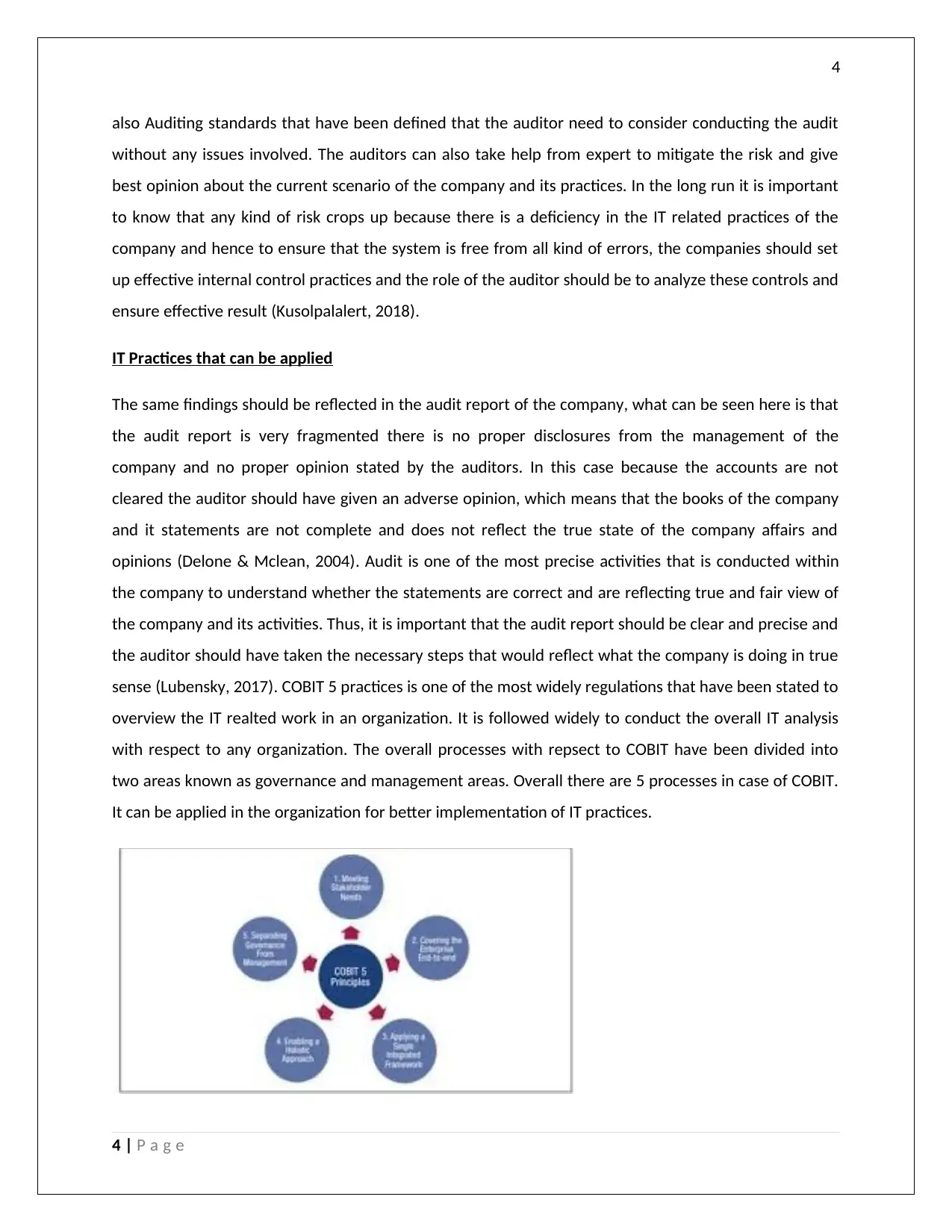

This report provides an analysis of the audit report issued for Bernard L. Madoff Investment Securities LLC, a Wall Street firm involved in a significant financial scandal. The analysis highlights the deficiencies in the original audit, particularly the failure to identify the Ponzi scheme orchestrated by Madoff. It emphasizes the importance of IT audits and the application of frameworks like COBIT 5 to identify and mitigate IT-related risks. The report suggests that the auditor should have issued an adverse opinion due to the misrepresentation of the company's financial state. Recommendations include implementing robust internal controls, seeking expert help for IT audits, and closely monitoring management actions to prevent future fraud. The document underscores the crucial role of auditors in ensuring the accuracy and reliability of financial statements for investors and stakeholders.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.