DFP4 Securities & Managed Investments: Developing Client Solutions

VerifiedAdded on 2024/05/21

|52

|14843

|207

Case Study

AI Summary

This assignment presents a case study involving Arthur and Gwen, a couple seeking investment advice after downsizing. The assignment requires an analysis of their financial situation, risk tolerance, and investment objectives to determine suitable investment strategies. It covers assessing their ability and willingness to take on investment risk, considering factors like income, expenses, existing assets, and retirement plans. The case study also involves addressing ethical considerations and preferences regarding investment types. Furthermore, the assignment includes questions related to presenting and implementing a financial plan, completing necessary documentation, and providing ongoing service, as well as offering a comprehensive approach to financial planning and investment advice.

Assignment

Securities and Managed Investments

(DFP4_AS_v2A1)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Section 1

Case study 1 questions

Not yet demonstrated Not yet demonstrated

Section 1

Case study 2 questions

Not yet demonstrated Not yet demonstrated

Section 1

Case study 3 questions

Not yet demonstrated Not yet demonstrated

Section 1

Case study 4 questions

Not yet demonstrated Not yet demonstrated

Section 2

Short answer questions

Not yet demonstrated Not yet demonstrated

Section 3

Short answer questions

Not yet demonstrated Not yet demonstrated

Section 4

Short answer questions

Not yet demonstrated Not yet demonstrated

DFP4_AS_v2

Securities and Managed Investments

(DFP4_AS_v2A1)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Section 1

Case study 1 questions

Not yet demonstrated Not yet demonstrated

Section 1

Case study 2 questions

Not yet demonstrated Not yet demonstrated

Section 1

Case study 3 questions

Not yet demonstrated Not yet demonstrated

Section 1

Case study 4 questions

Not yet demonstrated Not yet demonstrated

Section 2

Short answer questions

Not yet demonstrated Not yet demonstrated

Section 3

Short answer questions

Not yet demonstrated Not yet demonstrated

Section 4

Short answer questions

Not yet demonstrated Not yet demonstrated

DFP4_AS_v2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Feedback (assessor to complete)

[insert assessor feedback]

Page 2 of 52

[insert assessor feedback]

Page 2 of 52

Before you begin

Read everything in this document before you start your assignment for Securities and Managed

Investments (DFP4_AS_v2A1).

About this document

This document includes the following three (3) parts:

• Part 1: Instructions for completing and submitting this assignment

• Part 2: The assignment

• Section 1: Case Study Questions

– Case study 1: Establish relationship with client and identify client’s objectives, needs and

financial situation

– Case study 2: Analyse client’s objectives, needs, financial situation and risk profile to develop

appropriate strategies and solutions

– Case study 3: Present appropriate strategies and solutions to client and negotiate a financial plan,

policy or transaction

– Case study 4: Agree the plan, policy or transaction and complete documentation

– Appendices

> Risk profiles

> Approved products list

• Section 2: Present appropriate strategies and solutions to client and negotiate a financial plan, policy or

transaction

• Section 3: Agree the plan, policy or transaction and complete documentation

• Section 4: Provide ongoing service where requested by client

Note: Section 2–4 questions relate to Case Study 4.

Completing the assignment

The assignment

Complete Part 2:

Section 1

• Case study 1: Questions 1–4

• Case study 2: Questions 1–4

• Case study 3: Questions 1–4

• Case study 4: Questions 1–4

Section 2

• Parts A–C

Section 3

• Parts A–C

Section 4

• Parts A & B.

Page 3 of 52

Read everything in this document before you start your assignment for Securities and Managed

Investments (DFP4_AS_v2A1).

About this document

This document includes the following three (3) parts:

• Part 1: Instructions for completing and submitting this assignment

• Part 2: The assignment

• Section 1: Case Study Questions

– Case study 1: Establish relationship with client and identify client’s objectives, needs and

financial situation

– Case study 2: Analyse client’s objectives, needs, financial situation and risk profile to develop

appropriate strategies and solutions

– Case study 3: Present appropriate strategies and solutions to client and negotiate a financial plan,

policy or transaction

– Case study 4: Agree the plan, policy or transaction and complete documentation

– Appendices

> Risk profiles

> Approved products list

• Section 2: Present appropriate strategies and solutions to client and negotiate a financial plan, policy or

transaction

• Section 3: Agree the plan, policy or transaction and complete documentation

• Section 4: Provide ongoing service where requested by client

Note: Section 2–4 questions relate to Case Study 4.

Completing the assignment

The assignment

Complete Part 2:

Section 1

• Case study 1: Questions 1–4

• Case study 2: Questions 1–4

• Case study 3: Questions 1–4

• Case study 4: Questions 1–4

Section 2

• Parts A–C

Section 3

• Parts A–C

Section 4

• Parts A & B.

Page 3 of 52

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1: Instructions for completing and submitting this

assignment

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Securities and Managed

Investments (DFP4v2) subject room.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing this assignment, assumptions are permitted, although they must not be in conflict with

the information provided in the case studies.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your clients’ requirements, or to calculate any service fees

that may be applicable.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your

work regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Page 4 of 52

assignment

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Securities and Managed

Investments (DFP4v2) subject room.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing this assignment, assumptions are permitted, although they must not be in conflict with

the information provided in the case studies.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your clients’ requirements, or to calculate any service fees

that may be applicable.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your

work regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Page 4 of 52

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Submitting the assignment

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’, you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Securities and Managed Investments

(DFP4v2) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 52

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’, you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Securities and Managed Investments

(DFP4v2) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 52

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This assignment is your opportunity to demonstrate your competency against these units:

FNSASICW503 Provide advice in securities

FNSASICT503 Provide advice in managed investments

FNSFMK502 Analyse financial market products for client

FNSFMK503 Advise clients on financial risk

FNSCUS505 Determine client requirements and expectations

FNSCUS506 Record and implement client instructions

FNSINC501 Conduct product research to support recommendations

FNSIAD501 Provide appropriate services, advice and products to clients

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 52

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This assignment is your opportunity to demonstrate your competency against these units:

FNSASICW503 Provide advice in securities

FNSASICT503 Provide advice in managed investments

FNSFMK502 Analyse financial market products for client

FNSFMK503 Advise clients on financial risk

FNSCUS505 Determine client requirements and expectations

FNSCUS506 Record and implement client instructions

FNSINC501 Conduct product research to support recommendations

FNSIAD501 Provide appropriate services, advice and products to clients

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 52

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 2: The assignment

Section 1: Case Study Questions

Case study 1 (Arthur and Gwen)

Background information

Arthur (61) and Gwen (62) have recently sold their four-bedroom home of 35 years, downsizing into a new

‘over 55s’ townhouse. This has generated net proceeds of $250,000, and as this is the first time they have a

significant amount of surplus funds, they have decided to seek some investment advice. After some

discussion, you have determined the following facts.

Employment

Arthur is still working, but will look to retire from the workforce in two years time. Arthur earns $120,000

(including super) as a meteorologist. Gwen does not work and has no intention of rejoining the workforce.

Savings and spending

Arthur is not currently making any contributions into super apart from his employer’s 9.5% SGC.

Since paying off their mortgage a few years ago, they have tended to save about $5000 every year from

Arthur’s income, which has been going to their savings account. They have looked at their budget over the

years and they figure that they spend about $1000 per week on bills, food and lifestyle expenses. This level

of spending will likely continue after Arthur is retired.

Page 7 of 52

Section 1: Case Study Questions

Case study 1 (Arthur and Gwen)

Background information

Arthur (61) and Gwen (62) have recently sold their four-bedroom home of 35 years, downsizing into a new

‘over 55s’ townhouse. This has generated net proceeds of $250,000, and as this is the first time they have a

significant amount of surplus funds, they have decided to seek some investment advice. After some

discussion, you have determined the following facts.

Employment

Arthur is still working, but will look to retire from the workforce in two years time. Arthur earns $120,000

(including super) as a meteorologist. Gwen does not work and has no intention of rejoining the workforce.

Savings and spending

Arthur is not currently making any contributions into super apart from his employer’s 9.5% SGC.

Since paying off their mortgage a few years ago, they have tended to save about $5000 every year from

Arthur’s income, which has been going to their savings account. They have looked at their budget over the

years and they figure that they spend about $1000 per week on bills, food and lifestyle expenses. This level

of spending will likely continue after Arthur is retired.

Page 7 of 52

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

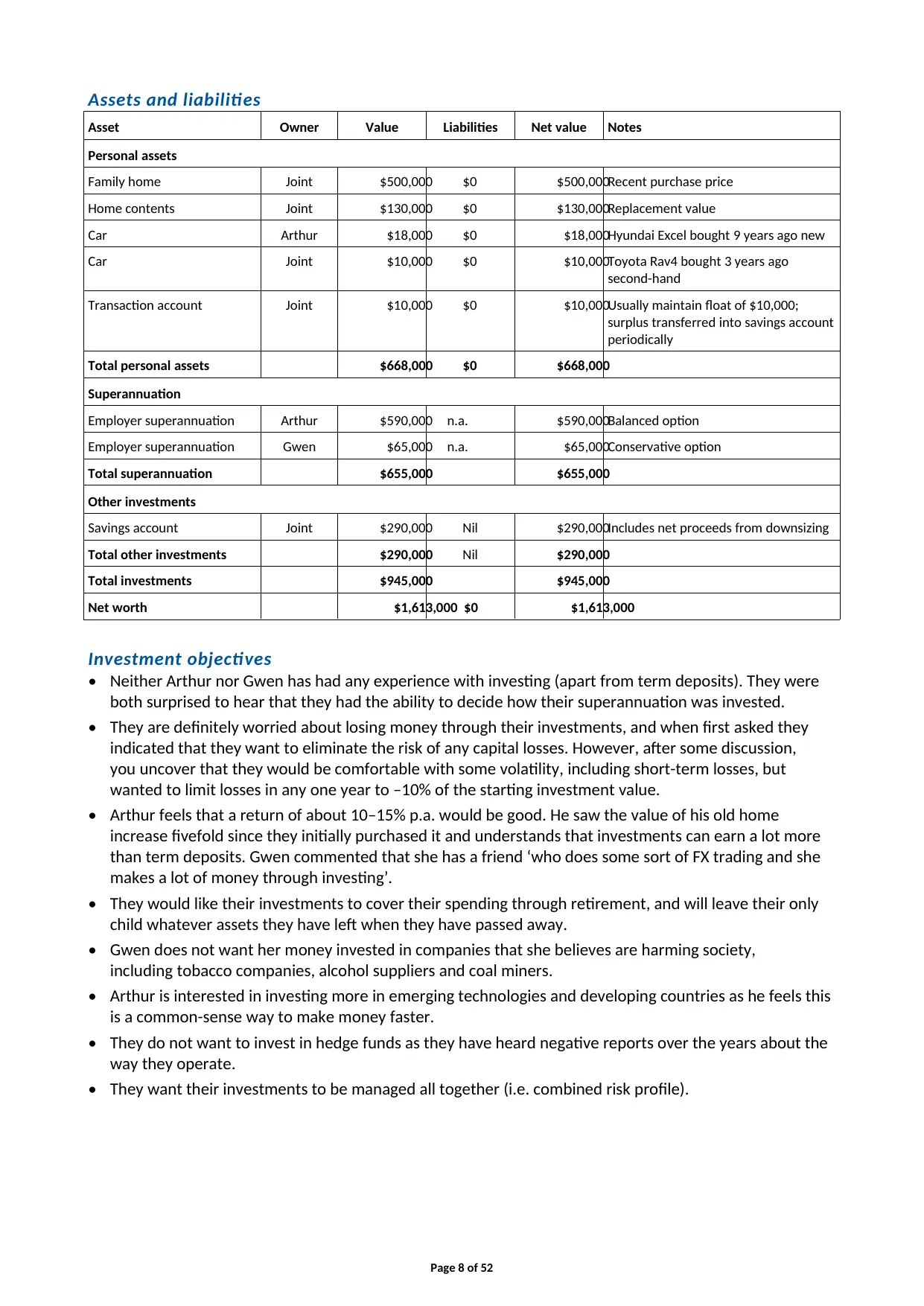

Assets and liabilities

Asset Owner Value Liabilities Net value Notes

Personal assets

Family home Joint $500,000 $0 $500,000Recent purchase price

Home contents Joint $130,000 $0 $130,000Replacement value

Car Arthur $18,000 $0 $18,000Hyundai Excel bought 9 years ago new

Car Joint $10,000 $0 $10,000Toyota Rav4 bought 3 years ago

second-hand

Transaction account Joint $10,000 $0 $10,000Usually maintain float of $10,000;

surplus transferred into savings account

periodically

Total personal assets $668,000 $0 $668,000

Superannuation

Employer superannuation Arthur $590,000 n.a. $590,000Balanced option

Employer superannuation Gwen $65,000 n.a. $65,000Conservative option

Total superannuation $655,000 $655,000

Other investments

Savings account Joint $290,000 Nil $290,000Includes net proceeds from downsizing

Total other investments $290,000 Nil $290,000

Total investments $945,000 $945,000

Net worth $1,613,000 $0 $1,613,000

Investment objectives

• Neither Arthur nor Gwen has had any experience with investing (apart from term deposits). They were

both surprised to hear that they had the ability to decide how their superannuation was invested.

• They are definitely worried about losing money through their investments, and when first asked they

indicated that they want to eliminate the risk of any capital losses. However, after some discussion,

you uncover that they would be comfortable with some volatility, including short-term losses, but

wanted to limit losses in any one year to –10% of the starting investment value.

• Arthur feels that a return of about 10–15% p.a. would be good. He saw the value of his old home

increase fivefold since they initially purchased it and understands that investments can earn a lot more

than term deposits. Gwen commented that she has a friend ‘who does some sort of FX trading and she

makes a lot of money through investing’.

• They would like their investments to cover their spending through retirement, and will leave their only

child whatever assets they have left when they have passed away.

• Gwen does not want her money invested in companies that she believes are harming society,

including tobacco companies, alcohol suppliers and coal miners.

• Arthur is interested in investing more in emerging technologies and developing countries as he feels this

is a common-sense way to make money faster.

• They do not want to invest in hedge funds as they have heard negative reports over the years about the

way they operate.

• They want their investments to be managed all together (i.e. combined risk profile).

Page 8 of 52

Asset Owner Value Liabilities Net value Notes

Personal assets

Family home Joint $500,000 $0 $500,000Recent purchase price

Home contents Joint $130,000 $0 $130,000Replacement value

Car Arthur $18,000 $0 $18,000Hyundai Excel bought 9 years ago new

Car Joint $10,000 $0 $10,000Toyota Rav4 bought 3 years ago

second-hand

Transaction account Joint $10,000 $0 $10,000Usually maintain float of $10,000;

surplus transferred into savings account

periodically

Total personal assets $668,000 $0 $668,000

Superannuation

Employer superannuation Arthur $590,000 n.a. $590,000Balanced option

Employer superannuation Gwen $65,000 n.a. $65,000Conservative option

Total superannuation $655,000 $655,000

Other investments

Savings account Joint $290,000 Nil $290,000Includes net proceeds from downsizing

Total other investments $290,000 Nil $290,000

Total investments $945,000 $945,000

Net worth $1,613,000 $0 $1,613,000

Investment objectives

• Neither Arthur nor Gwen has had any experience with investing (apart from term deposits). They were

both surprised to hear that they had the ability to decide how their superannuation was invested.

• They are definitely worried about losing money through their investments, and when first asked they

indicated that they want to eliminate the risk of any capital losses. However, after some discussion,

you uncover that they would be comfortable with some volatility, including short-term losses, but

wanted to limit losses in any one year to –10% of the starting investment value.

• Arthur feels that a return of about 10–15% p.a. would be good. He saw the value of his old home

increase fivefold since they initially purchased it and understands that investments can earn a lot more

than term deposits. Gwen commented that she has a friend ‘who does some sort of FX trading and she

makes a lot of money through investing’.

• They would like their investments to cover their spending through retirement, and will leave their only

child whatever assets they have left when they have passed away.

• Gwen does not want her money invested in companies that she believes are harming society,

including tobacco companies, alcohol suppliers and coal miners.

• Arthur is interested in investing more in emerging technologies and developing countries as he feels this

is a common-sense way to make money faster.

• They do not want to invest in hedge funds as they have heard negative reports over the years about the

way they operate.

• They want their investments to be managed all together (i.e. combined risk profile).

Page 8 of 52

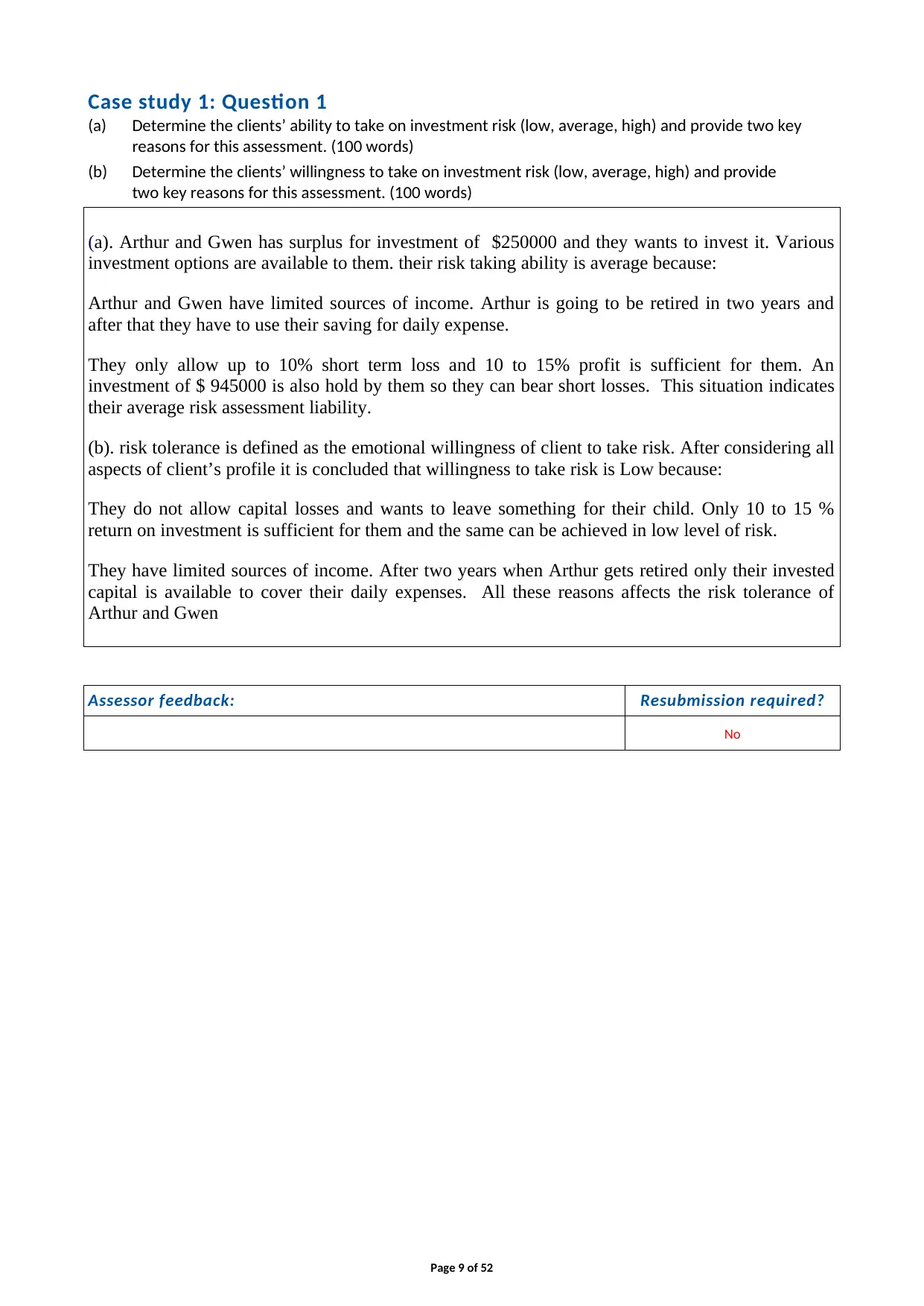

Case study 1: Question 1

(a) Determine the clients’ ability to take on investment risk (low, average, high) and provide two key

reasons for this assessment. (100 words)

(b) Determine the clients’ willingness to take on investment risk (low, average, high) and provide

two key reasons for this assessment. (100 words)

(a). Arthur and Gwen has surplus for investment of $250000 and they wants to invest it. Various

investment options are available to them. their risk taking ability is average because:

Arthur and Gwen have limited sources of income. Arthur is going to be retired in two years and

after that they have to use their saving for daily expense.

They only allow up to 10% short term loss and 10 to 15% profit is sufficient for them. An

investment of $ 945000 is also hold by them so they can bear short losses. This situation indicates

their average risk assessment liability.

(b). risk tolerance is defined as the emotional willingness of client to take risk. After considering all

aspects of client’s profile it is concluded that willingness to take risk is Low because:

They do not allow capital losses and wants to leave something for their child. Only 10 to 15 %

return on investment is sufficient for them and the same can be achieved in low level of risk.

They have limited sources of income. After two years when Arthur gets retired only their invested

capital is available to cover their daily expenses. All these reasons affects the risk tolerance of

Arthur and Gwen

Assessor feedback: Resubmission required?

No

Page 9 of 52

(a) Determine the clients’ ability to take on investment risk (low, average, high) and provide two key

reasons for this assessment. (100 words)

(b) Determine the clients’ willingness to take on investment risk (low, average, high) and provide

two key reasons for this assessment. (100 words)

(a). Arthur and Gwen has surplus for investment of $250000 and they wants to invest it. Various

investment options are available to them. their risk taking ability is average because:

Arthur and Gwen have limited sources of income. Arthur is going to be retired in two years and

after that they have to use their saving for daily expense.

They only allow up to 10% short term loss and 10 to 15% profit is sufficient for them. An

investment of $ 945000 is also hold by them so they can bear short losses. This situation indicates

their average risk assessment liability.

(b). risk tolerance is defined as the emotional willingness of client to take risk. After considering all

aspects of client’s profile it is concluded that willingness to take risk is Low because:

They do not allow capital losses and wants to leave something for their child. Only 10 to 15 %

return on investment is sufficient for them and the same can be achieved in low level of risk.

They have limited sources of income. After two years when Arthur gets retired only their invested

capital is available to cover their daily expenses. All these reasons affects the risk tolerance of

Arthur and Gwen

Assessor feedback: Resubmission required?

No

Page 9 of 52

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Case study 1: Question 2

Is the clients’ return objective appropriate? Why or why not? What further actions should be taken prior to

establishing an investment strategy? (200 words)

Client’s objective is appropriate as per his financial situation. Client is going to be retired in next

two years. Client’s partner Gwen does not work so there is no regular income source to cover

routine expenses. After considering all these factors, a defensive investment strategy is advised for

this client. Following steps should be taken before establishing investment planning:

Financial position: it is necessary to examine own financial position and possible financial needs

before making investment strategy.

Financial objectives: after identifying financial situation it is necessary to determinate financial

aims of client. In this step investment goals are prepared after considering accepted level of risk

and desired return.

Investment allocation: by considering risk and return analysis client can develop a proper

investment allocation strategy.

Identify investment options: with the help of investment allocation plan an appropriate asset mix

can be decided.

Execution, monitor and improvement; after deciding appropriate mix, client can invest in pre-decide

options and monitor the actual return with desired standards. If there is any adverse result he can re-

balance his planning.

Assessor feedback: Resubmission required?

No

Page 10 of 52

Is the clients’ return objective appropriate? Why or why not? What further actions should be taken prior to

establishing an investment strategy? (200 words)

Client’s objective is appropriate as per his financial situation. Client is going to be retired in next

two years. Client’s partner Gwen does not work so there is no regular income source to cover

routine expenses. After considering all these factors, a defensive investment strategy is advised for

this client. Following steps should be taken before establishing investment planning:

Financial position: it is necessary to examine own financial position and possible financial needs

before making investment strategy.

Financial objectives: after identifying financial situation it is necessary to determinate financial

aims of client. In this step investment goals are prepared after considering accepted level of risk

and desired return.

Investment allocation: by considering risk and return analysis client can develop a proper

investment allocation strategy.

Identify investment options: with the help of investment allocation plan an appropriate asset mix

can be decided.

Execution, monitor and improvement; after deciding appropriate mix, client can invest in pre-decide

options and monitor the actual return with desired standards. If there is any adverse result he can re-

balance his planning.

Assessor feedback: Resubmission required?

No

Page 10 of 52

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case study 1: Question 3

Refer to the risk profiles in Appendix 1. Which of these would be most appropriate to meet the clients’

investment needs? (100 words)

According to the need and ability of client moderate investment approach is appropriate. It is 72%

defensive approach. This approach is used when client desires better then basic returns but risk level

must be low. This approach is appropriate for client in following manner:

Client is going to be retired in two years and after this, they do not have any income source so they

want to protect their wealth for future expenses.

In this approach up to 23% return is possible. Client desires only for 10 to 15 percentage return so it

is suitable for client.

In this approach 75% amount is invested in fix interest provider options and the same will solve the

liquidity problem of client after retirement.

Assessor feedback: Resubmission required?

No

Page 11 of 52

Refer to the risk profiles in Appendix 1. Which of these would be most appropriate to meet the clients’

investment needs? (100 words)

According to the need and ability of client moderate investment approach is appropriate. It is 72%

defensive approach. This approach is used when client desires better then basic returns but risk level

must be low. This approach is appropriate for client in following manner:

Client is going to be retired in two years and after this, they do not have any income source so they

want to protect their wealth for future expenses.

In this approach up to 23% return is possible. Client desires only for 10 to 15 percentage return so it

is suitable for client.

In this approach 75% amount is invested in fix interest provider options and the same will solve the

liquidity problem of client after retirement.

Assessor feedback: Resubmission required?

No

Page 11 of 52

Case study 1: Question 4

List and describe four (4) different investment constraints the clients exhibit. (200 words)

Investment decisions are affected by various constraints. Every investment adviser needs to

consider these constraints during decision making. Constraints which affects the investment

decisions are as follows:

Liquidity: As future is uncertain, every person wants to reserve some money for unexpected future

needs and the same will constraints the investment amount. It is necessary for advisor to focus on

liquidity constraints when he is taking decisions about investment portfolio.

Tax rules: this factor rely upon how, when and if investment returns are taxed. In the case of sole

person all profits and incomes created by his portfolio are taxable. It is necessary for an advisor to

analyse the tax policy when he decides investment options.

Time period: various short term and long term investment options are available to the investor.

Smart investment analysis is required to earn the expected returns. Time is also an important factor

in this analysis. For example, client may require funds to pay the higher education fees in future. So

it is very important for client to maintain appropriate balance of short term and long term

investments while making investments.

Internal issues: internal issues are related with the client’s special concerns like culture and

traditions. Some investors do not want to invest in tobacco and alcohol companies. These internal

constraints should be considered at the time of investment decision-making.

Assessor feedback: Resubmission required?

No

Page 12 of 52

List and describe four (4) different investment constraints the clients exhibit. (200 words)

Investment decisions are affected by various constraints. Every investment adviser needs to

consider these constraints during decision making. Constraints which affects the investment

decisions are as follows:

Liquidity: As future is uncertain, every person wants to reserve some money for unexpected future

needs and the same will constraints the investment amount. It is necessary for advisor to focus on

liquidity constraints when he is taking decisions about investment portfolio.

Tax rules: this factor rely upon how, when and if investment returns are taxed. In the case of sole

person all profits and incomes created by his portfolio are taxable. It is necessary for an advisor to

analyse the tax policy when he decides investment options.

Time period: various short term and long term investment options are available to the investor.

Smart investment analysis is required to earn the expected returns. Time is also an important factor

in this analysis. For example, client may require funds to pay the higher education fees in future. So

it is very important for client to maintain appropriate balance of short term and long term

investments while making investments.

Internal issues: internal issues are related with the client’s special concerns like culture and

traditions. Some investors do not want to invest in tobacco and alcohol companies. These internal

constraints should be considered at the time of investment decision-making.

Assessor feedback: Resubmission required?

No

Page 12 of 52

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 52

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.