Security Audit: Vulnerabilities, Controls, Safeguards for Assets

VerifiedAdded on 2022/09/01

|12

|2717

|30

Report

AI Summary

This document presents an audit report focusing on the security of six assets, identifying common vulnerabilities and exposures related to cash, prepaid expenses, marketable securities, inventory, accounts receivable, accounts payable, and tangible assets. The report discusses the importance of information security risk management, highlighting the need for continuous monitoring and adaptation due to evolving threats and functional changes. It reviews controls and policies, emphasizing the role of protective measures and countermeasures in mitigating risks. The audit simulation includes discussions on approaching asset simulation, threat characteristics, and valid safeguards that could be implemented to address the findings. The report concludes with an independent auditor's assessment of the security controls and safeguards of the company's assets, underlining management's responsibility in maintaining a secure environment.

Running head: AUDITING

Auditing

Name:

Institution:

Date:

Auditing

Name:

Institution:

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT

Group Discussion #1:

a) Identification of the four vulnerabilities for the various assets

Vulnerability is the threat that can exploit a weak asset. The component itself does not

cause damage because a threat without vulnerability is not dangerous to the organization. It is

however necessary to monitor the vulnerabilities so as to identify the ones that are able to use

new threats in instances where there are functional changes for the assets. In this paper, on

the basis of a common vulnerability assessment system that allows us to determine a

qualitative indicator of vulnerability of information systems taking into account

environmental factors, a risk assessment technique for various types of cloud deployment is

presented. Information risk management, determining the applicability of cloud services to an

organization is impossible without understanding the context in which the organization

operates and the consequences of the possible types of threats that it may encounter as a

result of its activities (Alles, Brennan, Kogan, & Vasarhelyi, 2018).. The article proposes an

approach to risk assessment, used when choosing the most appropriate option for configuring

the cloud computing environment from the point of view of security requirements. The

application of a risk assessment methodology for various types of cloud deployment will help

to identify the coefficient of resistance to possible attacks and to correlate the amount of

damage with the total cost of the entire IT infrastructure of the organization.

b) List of the vulnerabilities

Computer Operations Actual amount Simulated Amount

Computer Application

System

Auditors Simulations

Program

Group Discussion #1:

a) Identification of the four vulnerabilities for the various assets

Vulnerability is the threat that can exploit a weak asset. The component itself does not

cause damage because a threat without vulnerability is not dangerous to the organization. It is

however necessary to monitor the vulnerabilities so as to identify the ones that are able to use

new threats in instances where there are functional changes for the assets. In this paper, on

the basis of a common vulnerability assessment system that allows us to determine a

qualitative indicator of vulnerability of information systems taking into account

environmental factors, a risk assessment technique for various types of cloud deployment is

presented. Information risk management, determining the applicability of cloud services to an

organization is impossible without understanding the context in which the organization

operates and the consequences of the possible types of threats that it may encounter as a

result of its activities (Alles, Brennan, Kogan, & Vasarhelyi, 2018).. The article proposes an

approach to risk assessment, used when choosing the most appropriate option for configuring

the cloud computing environment from the point of view of security requirements. The

application of a risk assessment methodology for various types of cloud deployment will help

to identify the coefficient of resistance to possible attacks and to correlate the amount of

damage with the total cost of the entire IT infrastructure of the organization.

b) List of the vulnerabilities

Computer Operations Actual amount Simulated Amount

Computer Application

System

Auditors Simulations

Program

AUDIT

Auditors Simulation Report

1. Cash and cash

equivalent

1. Prepaid expenses

2. Marketable securities

3. Inventory

4. Accounts receivable

5. Accounts payable

6. Tangible assets

The proposed approach to risk analysis and management allows us to assess the

security of the cloud environment, operating under the influence of a different class of

threats, as well as the effectiveness of a set of measures and means to counter these threats.

The activities of any organization are associated with risk. This means that it is impossible to

pinpoint which undesirable events will necessarily occur in the future and which are not.

Since information is an important asset, information security issues come to the fore. The

organization may suffer damage, including unforeseen expenses and possible loss of

customers, in the event of an information security incident. For critical facilities, the

consequences can be far more serious. Thus, to ensure the security of the organization from

information threats, it is necessary to manage information security risks.

c) Four main types of vulnerabilities and ranking

Type of Assets Common Vulnerabilities and exposures

2. Cash and cash Theft

Auditors Simulation Report

1. Cash and cash

equivalent

1. Prepaid expenses

2. Marketable securities

3. Inventory

4. Accounts receivable

5. Accounts payable

6. Tangible assets

The proposed approach to risk analysis and management allows us to assess the

security of the cloud environment, operating under the influence of a different class of

threats, as well as the effectiveness of a set of measures and means to counter these threats.

The activities of any organization are associated with risk. This means that it is impossible to

pinpoint which undesirable events will necessarily occur in the future and which are not.

Since information is an important asset, information security issues come to the fore. The

organization may suffer damage, including unforeseen expenses and possible loss of

customers, in the event of an information security incident. For critical facilities, the

consequences can be far more serious. Thus, to ensure the security of the organization from

information threats, it is necessary to manage information security risks.

c) Four main types of vulnerabilities and ranking

Type of Assets Common Vulnerabilities and exposures

2. Cash and cash Theft

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT

equivalent

7. Prepaid expenses Data destruction

8. Marketable securities Data exposure

9. Inventory Data modification

10. Accounts receivable

11. Accounts payable

12. Tangible assets

Group Discussion #2:

a) Review the 3 controls/policies

A protective measure can be effective in mitigating the risks associated with a threat

that uses an asset vulnerability group. The risk is considered acceptable, and no measures are

implemented even in the presence of a threat and if the asset is vulnerable. A safeguard group

can be effective in reducing the risks associated with a group of threats that exploit the

vulnerability of an asset.. Security model Information security risk management process The

information security risk management process can be applied both to the entire organization

and to any part of it (division or information system). This process should be continuous,

since over time the security of the object weakens due to changes in the functionality of the

components and the emergence of new threats. Therefore, at all stages of the risk

management process, it is necessary to document the results obtained. In general, risk

management refers to a process that includes a context, assessment, processing and

monitoring of risks

b) Simulation report against controls of the group

equivalent

7. Prepaid expenses Data destruction

8. Marketable securities Data exposure

9. Inventory Data modification

10. Accounts receivable

11. Accounts payable

12. Tangible assets

Group Discussion #2:

a) Review the 3 controls/policies

A protective measure can be effective in mitigating the risks associated with a threat

that uses an asset vulnerability group. The risk is considered acceptable, and no measures are

implemented even in the presence of a threat and if the asset is vulnerable. A safeguard group

can be effective in reducing the risks associated with a group of threats that exploit the

vulnerability of an asset.. Security model Information security risk management process The

information security risk management process can be applied both to the entire organization

and to any part of it (division or information system). This process should be continuous,

since over time the security of the object weakens due to changes in the functionality of the

components and the emergence of new threats. Therefore, at all stages of the risk

management process, it is necessary to document the results obtained. In general, risk

management refers to a process that includes a context, assessment, processing and

monitoring of risks

b) Simulation report against controls of the group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT

This component harms the organization by exploiting the vulnerabilities of its assets.

There are a large number of different classifications of threats, however, it is important to

understand that they can be not only targeted, but also random. The last security component

under consideration is countermeasures, that is, actions that can ensure security against the

threat. The choice of necessary countermeasures determines the effectiveness of measures to

ensure information security. The interconnection of security components shows how assets

can be exposed to threats (Chan, & Vasarhelyi, 2018).. These relationships are the five most

common scenarios: There is an asset vulnerability, but no threats are known that can exploit

it. A protective measure can be effective in reducing the risks associated with a threat that

could exploit the vulnerability of an asset.

The last security component under consideration is countermeasures, that is, actions

that can ensure security against the threat. The choice of necessary countermeasures

determines the effectiveness of measures to ensure information security. The interconnection

of security components shows how assets can be exposed to threats. These relationships are

the five most common scenarios: There is an asset vulnerability, but no threats are known that

can exploit it. A protective measure can be effective in reducing the risks associated with a

threat that could exploit the vulnerability of an asset.

Group Discussion #3:

a) Valid safeguards that could be implemented to address the findings from

audit

This component harms the organization by exploiting the vulnerabilities of its assets.

There are a large number of different classifications of threats, however, it is important to

understand that they can be not only targeted, but also random. The last security component

under consideration is countermeasures, that is, actions that can ensure security against the

threat. The choice of necessary countermeasures determines the effectiveness of measures to

ensure information security. The interconnection of security components shows how assets

can be exposed to threats (Chan, & Vasarhelyi, 2018).. These relationships are the five most

common scenarios: There is an asset vulnerability, but no threats are known that can exploit

it. A protective measure can be effective in reducing the risks associated with a threat that

could exploit the vulnerability of an asset.

The last security component under consideration is countermeasures, that is, actions

that can ensure security against the threat. The choice of necessary countermeasures

determines the effectiveness of measures to ensure information security. The interconnection

of security components shows how assets can be exposed to threats. These relationships are

the five most common scenarios: There is an asset vulnerability, but no threats are known that

can exploit it. A protective measure can be effective in reducing the risks associated with a

threat that could exploit the vulnerability of an asset.

Group Discussion #3:

a) Valid safeguards that could be implemented to address the findings from

audit

AUDIT

A safeguard group can be effective in reducing the risks associated with a group of

threats that exploit the vulnerability of an asset. A protective measure can be effective in

mitigating the risks associated with a threat that uses an asset vulnerability group. The risk is

considered acceptable, and no measures are implemented even in the presence of a threat and

if the asset is vulnerable.For each threat, a decision must be made: accept the risk, reduce the

risk or transfer the risk. Accepting risk means realizing it, accepting its ability and continuing

to act as before. Applicable for threats with low damage and low probability of occurrence.

To reduce risk means to introduce additional measures and means of protection,

conduct staff training, etc. That is, carry out deliberate work to reduce risk. In this case, it is

necessary to quantify the effectiveness of additional measures and remedies. All costs

incurred by the organization, from the purchase of protective equipment to commissioning

(including installation, configuration, training, maintenance, etc.), must not exceed the

amount of damage from the implementation of the threat.

To transfer risk means to transfer the consequences of the risk to a third party, for example,

through insurance.

As a result of a quantitative risk assessment, the following should be determined:

value of assets in monetary terms; A complete list of all IS threats with damage from a single

incident for each threat; frequency of implementation of each threat; potential damage from

each threat;

Recommended security measures, countermeasures and actions for each threat.

Now it is necessary to evaluate expertly how often such a situation may arise (taking into

account the intensity of operation, the quality of power supply, etc.)

A safeguard group can be effective in reducing the risks associated with a group of

threats that exploit the vulnerability of an asset. A protective measure can be effective in

mitigating the risks associated with a threat that uses an asset vulnerability group. The risk is

considered acceptable, and no measures are implemented even in the presence of a threat and

if the asset is vulnerable.For each threat, a decision must be made: accept the risk, reduce the

risk or transfer the risk. Accepting risk means realizing it, accepting its ability and continuing

to act as before. Applicable for threats with low damage and low probability of occurrence.

To reduce risk means to introduce additional measures and means of protection,

conduct staff training, etc. That is, carry out deliberate work to reduce risk. In this case, it is

necessary to quantify the effectiveness of additional measures and remedies. All costs

incurred by the organization, from the purchase of protective equipment to commissioning

(including installation, configuration, training, maintenance, etc.), must not exceed the

amount of damage from the implementation of the threat.

To transfer risk means to transfer the consequences of the risk to a third party, for example,

through insurance.

As a result of a quantitative risk assessment, the following should be determined:

value of assets in monetary terms; A complete list of all IS threats with damage from a single

incident for each threat; frequency of implementation of each threat; potential damage from

each threat;

Recommended security measures, countermeasures and actions for each threat.

Now it is necessary to evaluate expertly how often such a situation may arise (taking into

account the intensity of operation, the quality of power supply, etc.)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT

An analysis of information security risks by a qualitative method should be carried out with

the involvement of employees with experience and competencies in the area in which threats

are considered.

How to conduct a qualitative risk assessment:

1. Determine the value of information assets.

The asset value can be determined by the level of criticality (consequences) in case of

violation of the security characteristics (confidentiality, integrity, availability) of the

information asset.

2. Determine the likelihood of the threat in relation to the information asset.

To assess the likelihood of a threat, a three-level quality scale can be used (low, medium,

high).

3. Determine the level of possibility of successful implementation of the threat, taking into

account the current state of information security, implemented measures and means of

protection (Hall, (2015)..

A three-level quality scale (low, medium, high) can also be used to assess the level of

possibility of implementing a threat. The importance of the possibility of implementing a

threat shows how feasible the successful implementation of the threat is.

4. To draw a conclusion about the level of risk on the basis of the value of the information

asset, the probability of the threat, the possibility of the threat.

To determine the level of risk, you can use a five-point or ten-point scale. (Lins, Schneider, &

Sunyaev, 2016)..

An analysis of information security risks by a qualitative method should be carried out with

the involvement of employees with experience and competencies in the area in which threats

are considered.

How to conduct a qualitative risk assessment:

1. Determine the value of information assets.

The asset value can be determined by the level of criticality (consequences) in case of

violation of the security characteristics (confidentiality, integrity, availability) of the

information asset.

2. Determine the likelihood of the threat in relation to the information asset.

To assess the likelihood of a threat, a three-level quality scale can be used (low, medium,

high).

3. Determine the level of possibility of successful implementation of the threat, taking into

account the current state of information security, implemented measures and means of

protection (Hall, (2015)..

A three-level quality scale (low, medium, high) can also be used to assess the level of

possibility of implementing a threat. The importance of the possibility of implementing a

threat shows how feasible the successful implementation of the threat is.

4. To draw a conclusion about the level of risk on the basis of the value of the information

asset, the probability of the threat, the possibility of the threat.

To determine the level of risk, you can use a five-point or ten-point scale. (Lins, Schneider, &

Sunyaev, 2016)..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT

The next step is to identify existing controls. An understanding is formed of what is

already in the organization and how effective it is. Then, threats and vulnerabilities are

identified. The results are issued in the form of two documents: a list of threats and a list of

vulnerabilities. The last element of this stage is the identification of consequences, which

consists in compiling a list of scenarios of information security incidents with their

consequences for the organization. Often, when conducting a high-level risk assessment

based on the results of a meeting with the parties involved, this list of scenarios is formed,

based on which a detailed risk assessment is carried out. Risk analysis - the process of

studying the nature of the risk and determining the level of risk. This stage includes an

assessment of the severity of the consequences and their corresponding probabilities. In turn,

the probability value includes both the probability of the threat occurring and the probability

that the threat uses the vulnerability of the asset to cause damage. The methods used in risk

analysis can be quantitative, qualitative, or mixed (Groomer, & Murthy, 2018). Depending on

the needs of the organization and the availability of reliable data, the degree of detail of the

analysis is determined. In practice, a qualitative assessment is often used first to obtain

general information about the level of risk. Later, it may be necessary to carry out a more in-

depth analysis, as a result of which a quantitative risk assessment will be applied. When

assessing the severity of the consequences, data on the asset value table are taken into

account, as well as damage assessment results.

Group Submission

Simulate an audit of the information system : Description of how the group

would approach the simulation of the Assets

The next step is to identify existing controls. An understanding is formed of what is

already in the organization and how effective it is. Then, threats and vulnerabilities are

identified. The results are issued in the form of two documents: a list of threats and a list of

vulnerabilities. The last element of this stage is the identification of consequences, which

consists in compiling a list of scenarios of information security incidents with their

consequences for the organization. Often, when conducting a high-level risk assessment

based on the results of a meeting with the parties involved, this list of scenarios is formed,

based on which a detailed risk assessment is carried out. Risk analysis - the process of

studying the nature of the risk and determining the level of risk. This stage includes an

assessment of the severity of the consequences and their corresponding probabilities. In turn,

the probability value includes both the probability of the threat occurring and the probability

that the threat uses the vulnerability of the asset to cause damage. The methods used in risk

analysis can be quantitative, qualitative, or mixed (Groomer, & Murthy, 2018). Depending on

the needs of the organization and the availability of reliable data, the degree of detail of the

analysis is determined. In practice, a qualitative assessment is often used first to obtain

general information about the level of risk. Later, it may be necessary to carry out a more in-

depth analysis, as a result of which a quantitative risk assessment will be applied. When

assessing the severity of the consequences, data on the asset value table are taken into

account, as well as damage assessment results.

Group Submission

Simulate an audit of the information system : Description of how the group

would approach the simulation of the Assets

AUDIT

The main features that characterize the threat: source, frequency of occurrence,

harmful effect. As a component of security, risk is the ability of a threat to exploit the

vulnerability of an asset to harm an organization. Risk is characterized by a combination of

the probability of an information security incident and the consequences of such an incident.

It is important to understand that risk is never completely eliminated. Acceptance of residual

risk is part of the conclusion that the security level meets the organization's needs. The

system can develop and implement an effective security program, but lose sight of any asset,

as a result of which the actual protection of the organization from information security threats

will differ from the established one. The degree of detail for this phase is based on safety

objectives. The next security component under consideration is the threat.

Individual portion

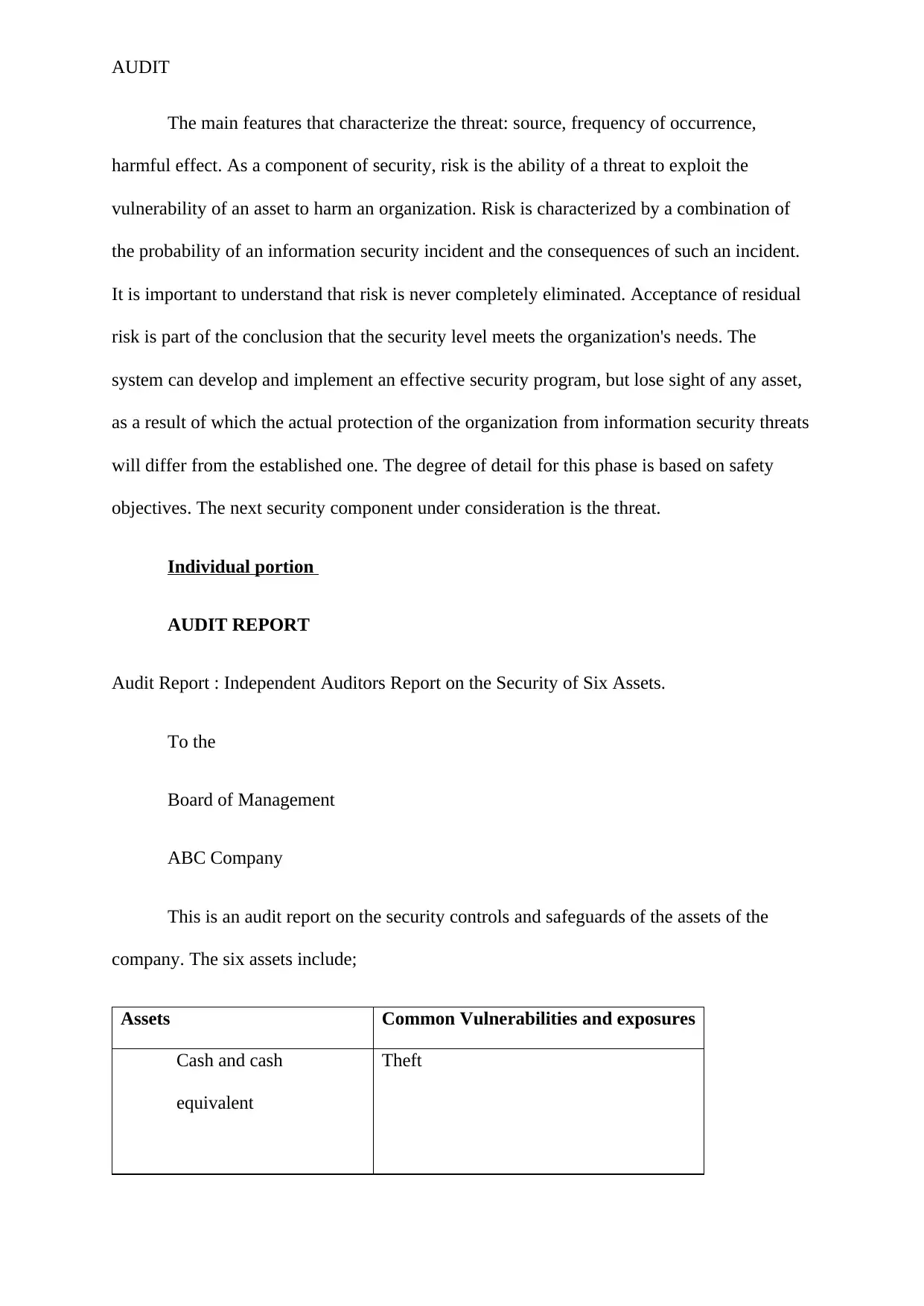

AUDIT REPORT

Audit Report : Independent Auditors Report on the Security of Six Assets.

To the

Board of Management

ABC Company

This is an audit report on the security controls and safeguards of the assets of the

company. The six assets include;

Assets Common Vulnerabilities and exposures

Cash and cash

equivalent

Theft

The main features that characterize the threat: source, frequency of occurrence,

harmful effect. As a component of security, risk is the ability of a threat to exploit the

vulnerability of an asset to harm an organization. Risk is characterized by a combination of

the probability of an information security incident and the consequences of such an incident.

It is important to understand that risk is never completely eliminated. Acceptance of residual

risk is part of the conclusion that the security level meets the organization's needs. The

system can develop and implement an effective security program, but lose sight of any asset,

as a result of which the actual protection of the organization from information security threats

will differ from the established one. The degree of detail for this phase is based on safety

objectives. The next security component under consideration is the threat.

Individual portion

AUDIT REPORT

Audit Report : Independent Auditors Report on the Security of Six Assets.

To the

Board of Management

ABC Company

This is an audit report on the security controls and safeguards of the assets of the

company. The six assets include;

Assets Common Vulnerabilities and exposures

Cash and cash

equivalent

Theft

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT

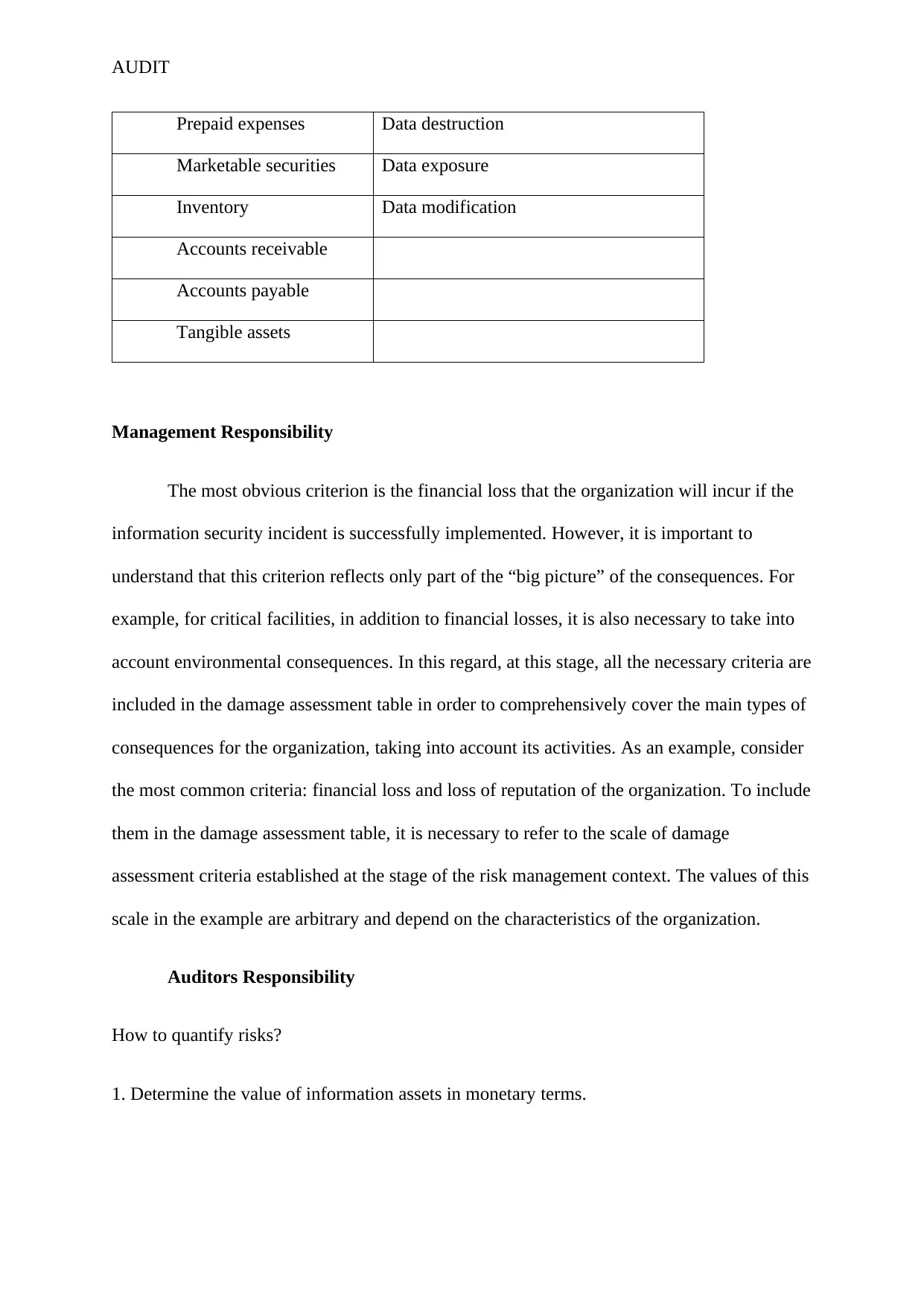

Prepaid expenses Data destruction

Marketable securities Data exposure

Inventory Data modification

Accounts receivable

Accounts payable

Tangible assets

Management Responsibility

The most obvious criterion is the financial loss that the organization will incur if the

information security incident is successfully implemented. However, it is important to

understand that this criterion reflects only part of the “big picture” of the consequences. For

example, for critical facilities, in addition to financial losses, it is also necessary to take into

account environmental consequences. In this regard, at this stage, all the necessary criteria are

included in the damage assessment table in order to comprehensively cover the main types of

consequences for the organization, taking into account its activities. As an example, consider

the most common criteria: financial loss and loss of reputation of the organization. To include

them in the damage assessment table, it is necessary to refer to the scale of damage

assessment criteria established at the stage of the risk management context. The values of this

scale in the example are arbitrary and depend on the characteristics of the organization.

Auditors Responsibility

How to quantify risks?

1. Determine the value of information assets in monetary terms.

Prepaid expenses Data destruction

Marketable securities Data exposure

Inventory Data modification

Accounts receivable

Accounts payable

Tangible assets

Management Responsibility

The most obvious criterion is the financial loss that the organization will incur if the

information security incident is successfully implemented. However, it is important to

understand that this criterion reflects only part of the “big picture” of the consequences. For

example, for critical facilities, in addition to financial losses, it is also necessary to take into

account environmental consequences. In this regard, at this stage, all the necessary criteria are

included in the damage assessment table in order to comprehensively cover the main types of

consequences for the organization, taking into account its activities. As an example, consider

the most common criteria: financial loss and loss of reputation of the organization. To include

them in the damage assessment table, it is necessary to refer to the scale of damage

assessment criteria established at the stage of the risk management context. The values of this

scale in the example are arbitrary and depend on the characteristics of the organization.

Auditors Responsibility

How to quantify risks?

1. Determine the value of information assets in monetary terms.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT

2. To quantify the potential damage from the implementation of each threat in relation to each

information asset.

Answers to the questions “What part of the value of the asset will be the damage from the

realization of each threat?”, “What is the cost of damage in monetary terms from a single

incident when this threat is realized to this asset?”

3. Determine the likelihood of each of the threats of information security.

To do this, you can use statistics, surveys of employees and stakeholders. In the process of

determining the probability, calculate the frequency of incidents related to the

implementation of the IS threat under consideration for the control period (for example, for

one year).

4. Determine the total potential damage from each threat in relation to each asset for the

control period (for one year).

Opinion

The opinion on assets security can either be qualified, unqualified or an adverse opinion. This

is based on the security levels and the transparency of the financials from the assets. The

value is calculated by multiplying the one-time damage from the threat realization by the

frequency of the threat realization.

Yours Faithfully

HHM Auditors

2. To quantify the potential damage from the implementation of each threat in relation to each

information asset.

Answers to the questions “What part of the value of the asset will be the damage from the

realization of each threat?”, “What is the cost of damage in monetary terms from a single

incident when this threat is realized to this asset?”

3. Determine the likelihood of each of the threats of information security.

To do this, you can use statistics, surveys of employees and stakeholders. In the process of

determining the probability, calculate the frequency of incidents related to the

implementation of the IS threat under consideration for the control period (for example, for

one year).

4. Determine the total potential damage from each threat in relation to each asset for the

control period (for one year).

Opinion

The opinion on assets security can either be qualified, unqualified or an adverse opinion. This

is based on the security levels and the transparency of the financials from the assets. The

value is calculated by multiplying the one-time damage from the threat realization by the

frequency of the threat realization.

Yours Faithfully

HHM Auditors

AUDIT

References

Alles, M., Brennan, G., Kogan, A., & Vasarhelyi, M. A. (2018). Continuous monitoring of

business process controls: A pilot implementation of a continuous auditing system at

Siemens. In Continuous Auditing: Theory and Application (pp. 219-246). Emerald

Publishing Limited.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and

Application (pp. 105-124). Emerald Publishing Limited.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

Lins, S., Schneider, S., & Sunyaev, A. (2016). Trust is good, control is better: Creating secure

clouds by continuous auditing. IEEE Transactions on Cloud Computing, 6(3), 890-

903.

References

Alles, M., Brennan, G., Kogan, A., & Vasarhelyi, M. A. (2018). Continuous monitoring of

business process controls: A pilot implementation of a continuous auditing system at

Siemens. In Continuous Auditing: Theory and Application (pp. 219-246). Emerald

Publishing Limited.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and

Application (pp. 105-124). Emerald Publishing Limited.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

Lins, S., Schneider, S., & Sunyaev, A. (2016). Trust is good, control is better: Creating secure

clouds by continuous auditing. IEEE Transactions on Cloud Computing, 6(3), 890-

903.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.