ACC702: Seek Group Executive Performance, Remuneration & Motivation

VerifiedAdded on 2023/06/07

|15

|4152

|252

Report

AI Summary

This report delves into the methodologies employed by public companies to assess executive performance, focusing on Seek Group and its competitor, Ambition Group. It explores various evaluation techniques such as the balanced scorecard, management by objectives, human asset accounting, and graphic rating scales. The analysis reveals that Seek Group's balanced scorecard approach has fostered sustainable growth, while Ambition Group's management by objective method has struggled to yield positive outcomes. The report scrutinizes corporate goals, executive remuneration allocation, and performance from a shareholder's perspective, comparing the remuneration policies of both companies to determine the most effective approach in enhancing business success. It concludes that aligning executive performance with organizational goals, as demonstrated by Seek Group, leads to improved profitability and shareholder value. Desklib provides access to similar solved assignments for students.

Seek Company

T218 Group assignment task

Specification: ACC702 PG – Managerial Accounting

Name of the Author-

University Name-

T218 Group assignment task

Specification: ACC702 PG – Managerial Accounting

Name of the Author-

University Name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY........................................................................................................3

INTRODUCTION......................................................................................................................3

REVIEW OF TOPIC AND REVIEW OF LITERATURE........................................................3

Company review........................................................................................................................5

CORPORATE GOALS..............................................................................................................6

ASSESMENT OF PERFORMANCCE OF SENIOR EXECUTIVE........................................6

ALLOCATION OF EXECUTIVE REMUNERATION...........................................................8

PERFORMANCE FROM A SHAREHOLDER’S PERSPECTIVE:........................................9

COMPANY EPRFORMANCE VERSUS EXECUTIVE PAY................................................9

SUMMARY OF FINDINGS...................................................................................................10

ANALYSIS AND COMPARISON OF REMUNERATION METHODS USED..................10

CONCLUSION........................................................................................................................11

REFERNCES...........................................................................................................................11

1

EXECUTIVE SUMMARY........................................................................................................3

INTRODUCTION......................................................................................................................3

REVIEW OF TOPIC AND REVIEW OF LITERATURE........................................................3

Company review........................................................................................................................5

CORPORATE GOALS..............................................................................................................6

ASSESMENT OF PERFORMANCCE OF SENIOR EXECUTIVE........................................6

ALLOCATION OF EXECUTIVE REMUNERATION...........................................................8

PERFORMANCE FROM A SHAREHOLDER’S PERSPECTIVE:........................................9

COMPANY EPRFORMANCE VERSUS EXECUTIVE PAY................................................9

SUMMARY OF FINDINGS...................................................................................................10

ANALYSIS AND COMPARISON OF REMUNERATION METHODS USED..................10

CONCLUSION........................................................................................................................11

REFERNCES...........................................................................................................................11

1

EXECUTIVE SUMMARY

The report focuses on the dealing with the different methods which public company

uses to evaluate the executive performance. There areVarious methods like the balanced

scorecard, management by objectives, human asset accounting, and the graphic rating are

discussed. An analysis is made of the methods used by the two companies in the line of

commercial and professional services, namely the Seek Group and the Ambition Group. The

analysis have shown that the balanced score card method used by the Seek Group had

provided long lasting and sustainable company growth. Whereas the management by

objective method used by the Ambition group has failed to achieve good results and is unable

to revive the company from declining growth.

2

The report focuses on the dealing with the different methods which public company

uses to evaluate the executive performance. There areVarious methods like the balanced

scorecard, management by objectives, human asset accounting, and the graphic rating are

discussed. An analysis is made of the methods used by the two companies in the line of

commercial and professional services, namely the Seek Group and the Ambition Group. The

analysis have shown that the balanced score card method used by the Seek Group had

provided long lasting and sustainable company growth. Whereas the management by

objective method used by the Ambition group has failed to achieve good results and is unable

to revive the company from declining growth.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The current report studies the different methods available to the company to evaluate

the performance of the executives. The success provided by these different methods in terms

of shareholder return and management motivation perspective is also studied. The corporate

goals of the company under discussion i.e. Seek Group are researched with the help of the

statements of chairman and CEO. The same is done for the competitive company named

Ambition Group. Both the companies are in the industry of commercial and professional

services. The initial section details the various options available to the company to evaluate

the managerial performance and set remunerations. After this, the review of company is

made, that includes the details of remuneration committee, membership, executive

remuneration allocation, etc. are analysed. A conclusion is made as to whether the company’s

performance is being improved because of the remuneration programme. A comparison

relating to the remuneration policies of both the companies and the success attained is made.

The best method among the both is mentioned thereafter. The conclusion is placed at the end

of the report. It mentions the company that has undertaken the best policy and how it has

helped the business to achieve success. This report has been prepared on the basis of the

financial details, annual report and remuneration report of Company.

REVIEW OF TOPIC AND REVIEW OF LITERATURE

All the organisations of Australia that are publically listed need to form a

remuneration committee. The role of this committee is to formulate strategies to evaluate the

performance of the executives of the company and at the same time set the basis for

remuneration. The various methods are being used by these remuneration committees to

measure the performance of the executives. These are mentioned as follows:

THE BALANCED SCORECARD: This method tried to evaluate the performance by

bringing a balance in different components. The company’s performance is analysed on the

basis of four different components. If there seems any improvement in the overall

performance based on these components, the managers are appraised with better incentives.

Else, any declining performance sets the executives’ bonus at stake. The different

perspectives among which a balance is strived to be achieved include:

o Financial perspective: The main growth area as assumed here is that of profit made and the

market share captured. The performance is assumed to have improved, if both these

3

The current report studies the different methods available to the company to evaluate

the performance of the executives. The success provided by these different methods in terms

of shareholder return and management motivation perspective is also studied. The corporate

goals of the company under discussion i.e. Seek Group are researched with the help of the

statements of chairman and CEO. The same is done for the competitive company named

Ambition Group. Both the companies are in the industry of commercial and professional

services. The initial section details the various options available to the company to evaluate

the managerial performance and set remunerations. After this, the review of company is

made, that includes the details of remuneration committee, membership, executive

remuneration allocation, etc. are analysed. A conclusion is made as to whether the company’s

performance is being improved because of the remuneration programme. A comparison

relating to the remuneration policies of both the companies and the success attained is made.

The best method among the both is mentioned thereafter. The conclusion is placed at the end

of the report. It mentions the company that has undertaken the best policy and how it has

helped the business to achieve success. This report has been prepared on the basis of the

financial details, annual report and remuneration report of Company.

REVIEW OF TOPIC AND REVIEW OF LITERATURE

All the organisations of Australia that are publically listed need to form a

remuneration committee. The role of this committee is to formulate strategies to evaluate the

performance of the executives of the company and at the same time set the basis for

remuneration. The various methods are being used by these remuneration committees to

measure the performance of the executives. These are mentioned as follows:

THE BALANCED SCORECARD: This method tried to evaluate the performance by

bringing a balance in different components. The company’s performance is analysed on the

basis of four different components. If there seems any improvement in the overall

performance based on these components, the managers are appraised with better incentives.

Else, any declining performance sets the executives’ bonus at stake. The different

perspectives among which a balance is strived to be achieved include:

o Financial perspective: The main growth area as assumed here is that of profit made and the

market share captured. The performance is assumed to have improved, if both these

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

components show an improvement. It is analyzed that company has improved its business

performance by increasing its overall turnover and profitability at large. However, company

o Learning and innovation perspective: this perspective emphasises the need of the organisation

to add value by adding innovation and improvement. It has increased its profit by average

12% since last three years.

o Customer perspective: Herein, the measurement of the level of satisfaction among customers

is observed. It is used to analysis the value, social structure and belief of the clients with the

offered goods and services in market.

o Internal business perspective: this is all about the focus on those internal operations through

which the customers’ needs coud be satiated (Zizlavsky, 2014).

This method proves to be successful because of its ability to measure an employee’s

performance from an overall perspective and not from a single area. Herein, the best part is

the alignment of the achievement of organisational goals with the executive performance.

This stands as a motivation for the management. At the same time it helps in increasing the

profit level that stands as an improvement in the shareholder value (Cooper, Ezzamel, and

Qu, 2017).

HUMAN ASSET ACCOUNTING METHOD: this method is 90% related to profitability of

the company. The termination or promotion of the employee directly depends on the factors

related to that individual performance itself. These performance criteria include the revenue

contribution by that executive, or the number of customers satisfied by him, or the sales lead

generated by him. A complete track of the employee performance is required to be

maintained (Stanko, Zeller, and Melina, 2014).

This method tends to be successful in motivating the executive because his performance is

directly linked to the incentives that he will be getting. However, the shareholder value is also

improved as the increased revenue means increased profits and hence increased returns

(Pucci, Simoni, and Zanni, 2015).

MANAGEMENT BY OBJECTIVE: in this method, goals are already set up for every

executive and a track is made as to what is eventually achieved by him. The goals are set in

accordance with the organisational goals (Uduji, 2013).

This proves to be successful in motivating employees because the executive is already aware

of the returns expected from him. So he will be motivated to perform as best as he can.

4

performance by increasing its overall turnover and profitability at large. However, company

o Learning and innovation perspective: this perspective emphasises the need of the organisation

to add value by adding innovation and improvement. It has increased its profit by average

12% since last three years.

o Customer perspective: Herein, the measurement of the level of satisfaction among customers

is observed. It is used to analysis the value, social structure and belief of the clients with the

offered goods and services in market.

o Internal business perspective: this is all about the focus on those internal operations through

which the customers’ needs coud be satiated (Zizlavsky, 2014).

This method proves to be successful because of its ability to measure an employee’s

performance from an overall perspective and not from a single area. Herein, the best part is

the alignment of the achievement of organisational goals with the executive performance.

This stands as a motivation for the management. At the same time it helps in increasing the

profit level that stands as an improvement in the shareholder value (Cooper, Ezzamel, and

Qu, 2017).

HUMAN ASSET ACCOUNTING METHOD: this method is 90% related to profitability of

the company. The termination or promotion of the employee directly depends on the factors

related to that individual performance itself. These performance criteria include the revenue

contribution by that executive, or the number of customers satisfied by him, or the sales lead

generated by him. A complete track of the employee performance is required to be

maintained (Stanko, Zeller, and Melina, 2014).

This method tends to be successful in motivating the executive because his performance is

directly linked to the incentives that he will be getting. However, the shareholder value is also

improved as the increased revenue means increased profits and hence increased returns

(Pucci, Simoni, and Zanni, 2015).

MANAGEMENT BY OBJECTIVE: in this method, goals are already set up for every

executive and a track is made as to what is eventually achieved by him. The goals are set in

accordance with the organisational goals (Uduji, 2013).

This proves to be successful in motivating employees because the executive is already aware

of the returns expected from him. So he will be motivated to perform as best as he can.

4

Further due to his improved performance the profitability shall increase and that shall lead to

a raise in the shareholder return.

GRAPHIC RATING SCALES: this method involves rating of the customers by using a scale

from 1 to 5. The rating is to done on different grounds including the job duties of the

executive and the related performance standards. This method is relatively judgemental and

depends on the judgement of the work’s supervisor (Aggarwal, and Thakur, 2013).

The executives get employed to perform better by this method as they are always intended to

improve their ratings and gain an edge ahead than the rest executives. And this competition to

get a better rating helps in increasing the ultimate wealth and return for shareholders

(Mwema, and Gachunga, 2014).

Company review

The table presented below is all about the review of remuneration report made for the

company assigned i.e. Seek Group. Further, the details for the same grounds are also laid for

the chosen competitor company, Ambition Group. This is used to analysis the amount of

compensation given to employees and how company has been aligning the interest of the

employees with the organization development.

5

a raise in the shareholder return.

GRAPHIC RATING SCALES: this method involves rating of the customers by using a scale

from 1 to 5. The rating is to done on different grounds including the job duties of the

executive and the related performance standards. This method is relatively judgemental and

depends on the judgement of the work’s supervisor (Aggarwal, and Thakur, 2013).

The executives get employed to perform better by this method as they are always intended to

improve their ratings and gain an edge ahead than the rest executives. And this competition to

get a better rating helps in increasing the ultimate wealth and return for shareholders

(Mwema, and Gachunga, 2014).

Company review

The table presented below is all about the review of remuneration report made for the

company assigned i.e. Seek Group. Further, the details for the same grounds are also laid for

the chosen competitor company, Ambition Group. This is used to analysis the amount of

compensation given to employees and how company has been aligning the interest of the

employees with the organization development.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

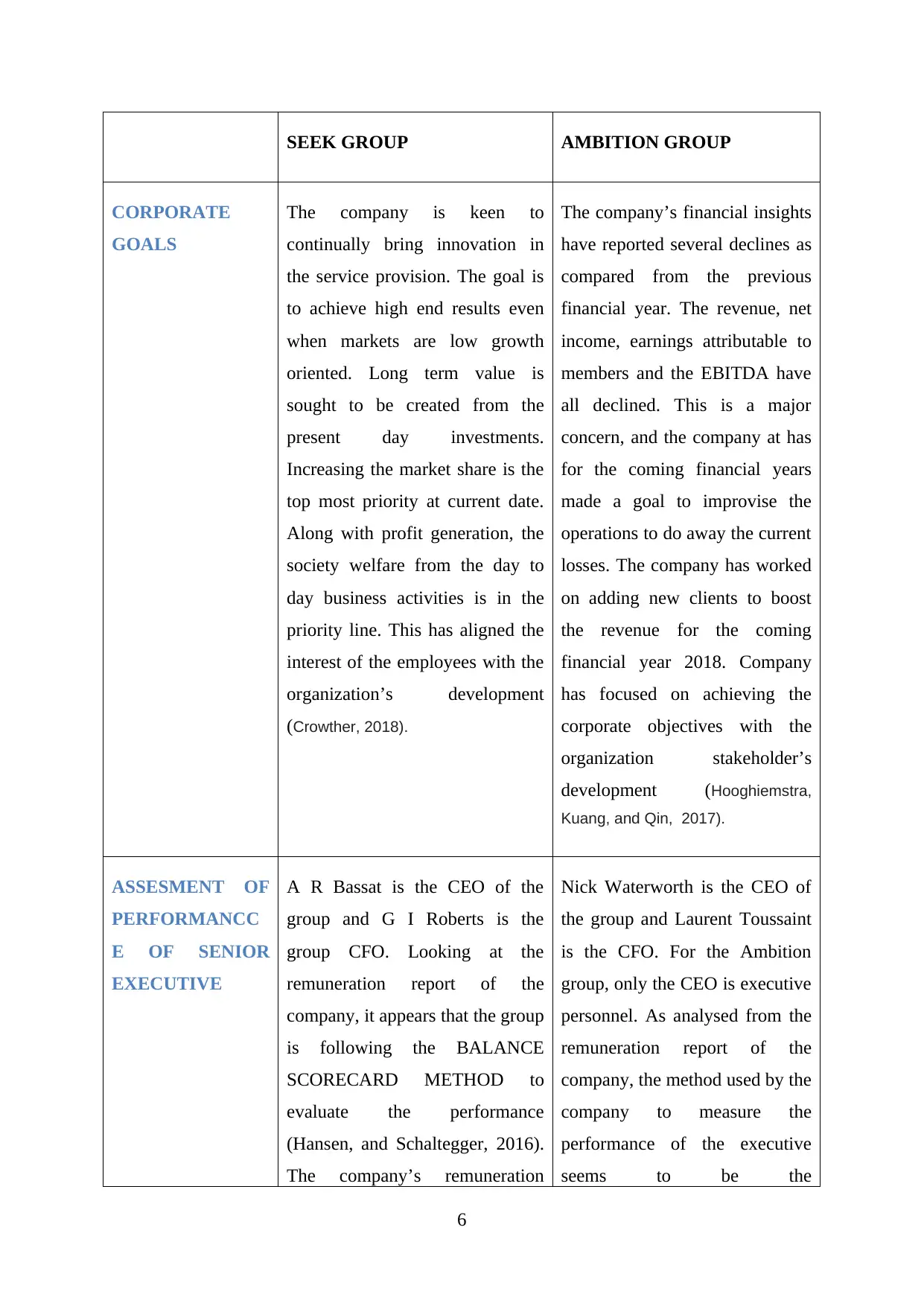

SEEK GROUP AMBITION GROUP

CORPORATE

GOALS

The company is keen to

continually bring innovation in

the service provision. The goal is

to achieve high end results even

when markets are low growth

oriented. Long term value is

sought to be created from the

present day investments.

Increasing the market share is the

top most priority at current date.

Along with profit generation, the

society welfare from the day to

day business activities is in the

priority line. This has aligned the

interest of the employees with the

organization’s development

(Crowther, 2018).

The company’s financial insights

have reported several declines as

compared from the previous

financial year. The revenue, net

income, earnings attributable to

members and the EBITDA have

all declined. This is a major

concern, and the company at has

for the coming financial years

made a goal to improvise the

operations to do away the current

losses. The company has worked

on adding new clients to boost

the revenue for the coming

financial year 2018. Company

has focused on achieving the

corporate objectives with the

organization stakeholder’s

development (Hooghiemstra,

Kuang, and Qin, 2017).

ASSESMENT OF

PERFORMANCC

E OF SENIOR

EXECUTIVE

A R Bassat is the CEO of the

group and G I Roberts is the

group CFO. Looking at the

remuneration report of the

company, it appears that the group

is following the BALANCE

SCORECARD METHOD to

evaluate the performance

(Hansen, and Schaltegger, 2016).

The company’s remuneration

Nick Waterworth is the CEO of

the group and Laurent Toussaint

is the CFO. For the Ambition

group, only the CEO is executive

personnel. As analysed from the

remuneration report of the

company, the method used by the

company to measure the

performance of the executive

seems to be the

6

CORPORATE

GOALS

The company is keen to

continually bring innovation in

the service provision. The goal is

to achieve high end results even

when markets are low growth

oriented. Long term value is

sought to be created from the

present day investments.

Increasing the market share is the

top most priority at current date.

Along with profit generation, the

society welfare from the day to

day business activities is in the

priority line. This has aligned the

interest of the employees with the

organization’s development

(Crowther, 2018).

The company’s financial insights

have reported several declines as

compared from the previous

financial year. The revenue, net

income, earnings attributable to

members and the EBITDA have

all declined. This is a major

concern, and the company at has

for the coming financial years

made a goal to improvise the

operations to do away the current

losses. The company has worked

on adding new clients to boost

the revenue for the coming

financial year 2018. Company

has focused on achieving the

corporate objectives with the

organization stakeholder’s

development (Hooghiemstra,

Kuang, and Qin, 2017).

ASSESMENT OF

PERFORMANCC

E OF SENIOR

EXECUTIVE

A R Bassat is the CEO of the

group and G I Roberts is the

group CFO. Looking at the

remuneration report of the

company, it appears that the group

is following the BALANCE

SCORECARD METHOD to

evaluate the performance

(Hansen, and Schaltegger, 2016).

The company’s remuneration

Nick Waterworth is the CEO of

the group and Laurent Toussaint

is the CFO. For the Ambition

group, only the CEO is executive

personnel. As analysed from the

remuneration report of the

company, the method used by the

company to measure the

performance of the executive

seems to be the

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

structure is based on the company

performance. The challenges that

the executives face in the day to

day business activities are

measured by the effort they take

to achieve the desired results. The

performance is to be measured for

long term basis. The company has

integrated the executive

performance with the overall

return to the shareholders. Every

increase in the return that the

shareholders get shall raise the

remuneration bar for the

executives. A performance hurdle

is set in the remuneration report

which is must to be met if the

executive want to avail the long

term incentive criteria. The

performance is evaluated in terms

of the change in share price. The

bonus and incentives plans are

given to employees on the basis of

performance and outcomes given

to organization.

MANAGEMENT BY

EXECUTIVE METHOD. On an

annual basis, a criteria is laid in

agreement with the executive.

This criterion is based on the

performance of the relevant

operational division, for which

the executive is accountable and

it align the interest of the

executives and their rewards with

the accomplishment of the set

targets and goals.

7

performance. The challenges that

the executives face in the day to

day business activities are

measured by the effort they take

to achieve the desired results. The

performance is to be measured for

long term basis. The company has

integrated the executive

performance with the overall

return to the shareholders. Every

increase in the return that the

shareholders get shall raise the

remuneration bar for the

executives. A performance hurdle

is set in the remuneration report

which is must to be met if the

executive want to avail the long

term incentive criteria. The

performance is evaluated in terms

of the change in share price. The

bonus and incentives plans are

given to employees on the basis of

performance and outcomes given

to organization.

MANAGEMENT BY

EXECUTIVE METHOD. On an

annual basis, a criteria is laid in

agreement with the executive.

This criterion is based on the

performance of the relevant

operational division, for which

the executive is accountable and

it align the interest of the

executives and their rewards with

the accomplishment of the set

targets and goals.

7

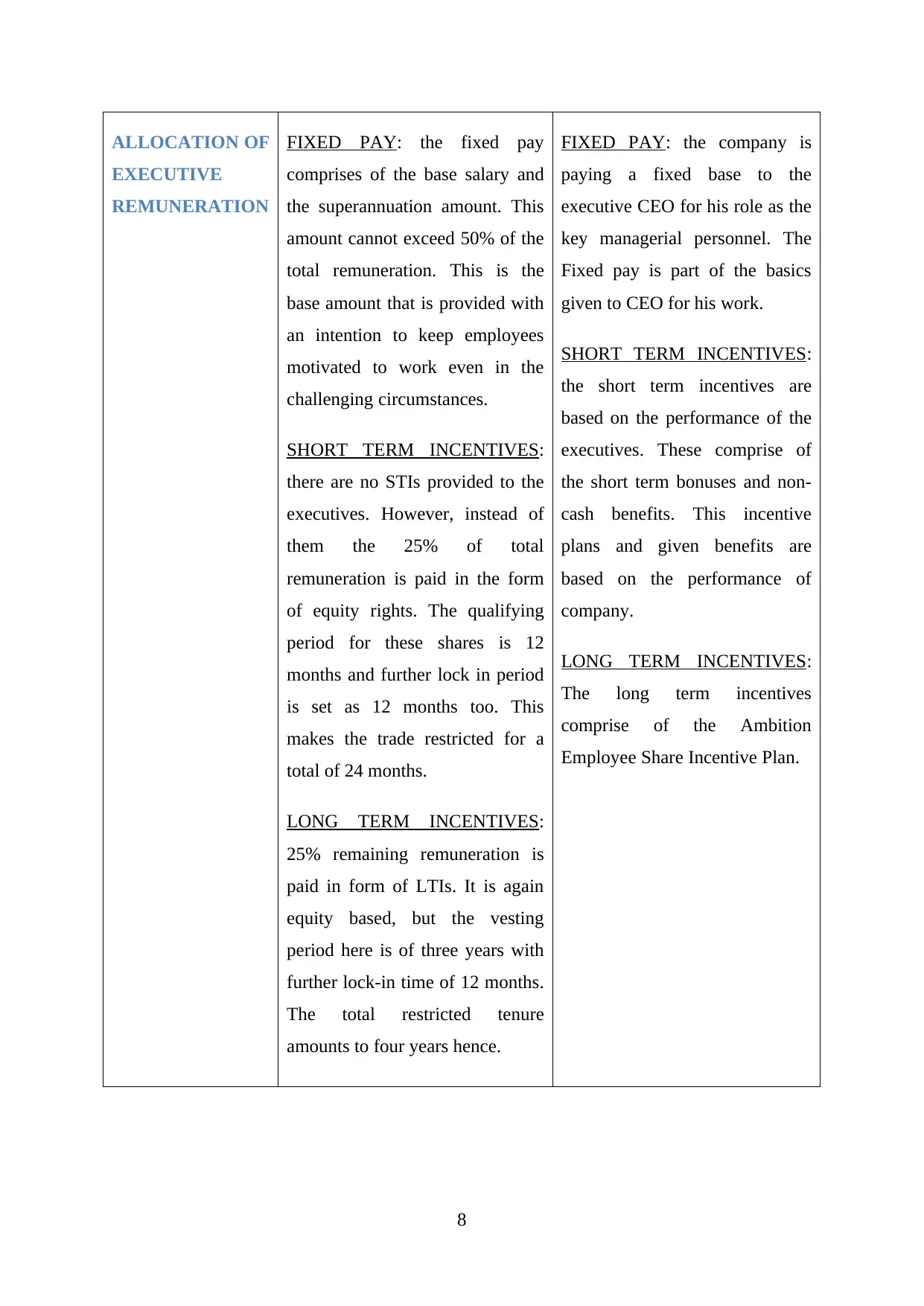

ALLOCATION OF

EXECUTIVE

REMUNERATION

FIXED PAY: the fixed pay

comprises of the base salary and

the superannuation amount. This

amount cannot exceed 50% of the

total remuneration. This is the

base amount that is provided with

an intention to keep employees

motivated to work even in the

challenging circumstances.

SHORT TERM INCENTIVES:

there are no STIs provided to the

executives. However, instead of

them the 25% of total

remuneration is paid in the form

of equity rights. The qualifying

period for these shares is 12

months and further lock in period

is set as 12 months too. This

makes the trade restricted for a

total of 24 months.

LONG TERM INCENTIVES:

25% remaining remuneration is

paid in form of LTIs. It is again

equity based, but the vesting

period here is of three years with

further lock-in time of 12 months.

The total restricted tenure

amounts to four years hence.

FIXED PAY: the company is

paying a fixed base to the

executive CEO for his role as the

key managerial personnel. The

Fixed pay is part of the basics

given to CEO for his work.

SHORT TERM INCENTIVES:

the short term incentives are

based on the performance of the

executives. These comprise of

the short term bonuses and non-

cash benefits. This incentive

plans and given benefits are

based on the performance of

company.

LONG TERM INCENTIVES:

The long term incentives

comprise of the Ambition

Employee Share Incentive Plan.

8

EXECUTIVE

REMUNERATION

FIXED PAY: the fixed pay

comprises of the base salary and

the superannuation amount. This

amount cannot exceed 50% of the

total remuneration. This is the

base amount that is provided with

an intention to keep employees

motivated to work even in the

challenging circumstances.

SHORT TERM INCENTIVES:

there are no STIs provided to the

executives. However, instead of

them the 25% of total

remuneration is paid in the form

of equity rights. The qualifying

period for these shares is 12

months and further lock in period

is set as 12 months too. This

makes the trade restricted for a

total of 24 months.

LONG TERM INCENTIVES:

25% remaining remuneration is

paid in form of LTIs. It is again

equity based, but the vesting

period here is of three years with

further lock-in time of 12 months.

The total restricted tenure

amounts to four years hence.

FIXED PAY: the company is

paying a fixed base to the

executive CEO for his role as the

key managerial personnel. The

Fixed pay is part of the basics

given to CEO for his work.

SHORT TERM INCENTIVES:

the short term incentives are

based on the performance of the

executives. These comprise of

the short term bonuses and non-

cash benefits. This incentive

plans and given benefits are

based on the performance of

company.

LONG TERM INCENTIVES:

The long term incentives

comprise of the Ambition

Employee Share Incentive Plan.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PERFORMANCE

FROM A

SHAREHOLDER’

S PERSPECTIVE:

The analysis for the

growth or decline

that company as

witnessed from the

point of view of the

shareholders is

presented by the use

of the share price

chart for the past

three financial years.

The dividend paid by the

company has increased from $140

million (approx.) to $189 million

(approx.). This dividend payment

includes the bonus and employee

stock option given to executive

(Pelger, 2016).

The dividend paid by the

company has remained almost

same for these financials years.

The amount reported is

$672,000. It reflects that with the

increase in the benefit company

has also increased the overall

benefits for its stakeholders (Rao,

and Tilt, 2016).

COMPANY

EPRFORMANCE

VERSUS

EXECUTIVE PAY

The share price of the company

has risen from $14.06 in for

financial year 2015 to $ 16.91 for

financial year 2017. Growth is

reported in the basic earnings per

share from $56.3 in financial year

2015 to $ 63.5 in financial year

2017. This growth has

significantly led to a rise in the

pay of the executives as all the

payments are somehow linked to

the company performance. The

The company performance over

the three financial years ending

with financial year 2017 has

declined. The share price has

come down from $18 to $16.

This has resulted in a decline in

the basic earnings per share from

$1.71 to $0.52. The remuneration

or executive pay has followed the

same declining trend. The reason

is obvious that the performance

bonuses are eliminated or

9

FROM A

SHAREHOLDER’

S PERSPECTIVE:

The analysis for the

growth or decline

that company as

witnessed from the

point of view of the

shareholders is

presented by the use

of the share price

chart for the past

three financial years.

The dividend paid by the

company has increased from $140

million (approx.) to $189 million

(approx.). This dividend payment

includes the bonus and employee

stock option given to executive

(Pelger, 2016).

The dividend paid by the

company has remained almost

same for these financials years.

The amount reported is

$672,000. It reflects that with the

increase in the benefit company

has also increased the overall

benefits for its stakeholders (Rao,

and Tilt, 2016).

COMPANY

EPRFORMANCE

VERSUS

EXECUTIVE PAY

The share price of the company

has risen from $14.06 in for

financial year 2015 to $ 16.91 for

financial year 2017. Growth is

reported in the basic earnings per

share from $56.3 in financial year

2015 to $ 63.5 in financial year

2017. This growth has

significantly led to a rise in the

pay of the executives as all the

payments are somehow linked to

the company performance. The

The company performance over

the three financial years ending

with financial year 2017 has

declined. The share price has

come down from $18 to $16.

This has resulted in a decline in

the basic earnings per share from

$1.71 to $0.52. The remuneration

or executive pay has followed the

same declining trend. The reason

is obvious that the performance

bonuses are eliminated or

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

growth in the incentive scheme

and increased business payment

has reflected that it has focused on

increasing the overall outcomes

and efficiency in long run (Kent,

Kercher, and Routledge, 2018).

declined with the decreased

returns. Further the eligibility

criteria for the Ambition

Employee Share Incentive Plan

are also not fulfilled. These

incentive plans and undertaken

strategic approach provide the

increased motivation to its

executives.

SUMMARY OF FINDINGS

The Seek Group has adopted an effective measure to evaluate the executive

performance and the basis of remuneration. The way remuneration is allocated highlights the

high end approach followed by the management to achieve results in terms of higher

company performance. The approach of the company’s remuneration programme is very

simple to understand both by the executives and the shareholders. It is a short and

summarised structure. The Seek group has adopted employee oriented remuneration pay

which motivates employees to push themselves for the best outcomes of the organization

(Hyndman, and McConville, 2016).

The basic components as discussed above include the basic pay, the superannuation

payment and the equity rights. The time the holder of the equity right has to wait in terms of

vesting period and the lock in period is also mentioned without any doubts. The approach

adopted had been highly effective in helping the company to attract the talented

professionals. This is also helpful in retaining and motivating them to perform better than

before. The base figure offered to the executives has been set at a level to encourage them to

work effectively and remain motivated in the challenging scenarios. It is the lead given to

keep them active throughout. The equity rights and superannuation payment is provided as

long term benefit plan for its employees which will increase the overall outcomes and

efficiency of company in long run (Doni, Gasperini, and Pavone., 2016).

10

and increased business payment

has reflected that it has focused on

increasing the overall outcomes

and efficiency in long run (Kent,

Kercher, and Routledge, 2018).

declined with the decreased

returns. Further the eligibility

criteria for the Ambition

Employee Share Incentive Plan

are also not fulfilled. These

incentive plans and undertaken

strategic approach provide the

increased motivation to its

executives.

SUMMARY OF FINDINGS

The Seek Group has adopted an effective measure to evaluate the executive

performance and the basis of remuneration. The way remuneration is allocated highlights the

high end approach followed by the management to achieve results in terms of higher

company performance. The approach of the company’s remuneration programme is very

simple to understand both by the executives and the shareholders. It is a short and

summarised structure. The Seek group has adopted employee oriented remuneration pay

which motivates employees to push themselves for the best outcomes of the organization

(Hyndman, and McConville, 2016).

The basic components as discussed above include the basic pay, the superannuation

payment and the equity rights. The time the holder of the equity right has to wait in terms of

vesting period and the lock in period is also mentioned without any doubts. The approach

adopted had been highly effective in helping the company to attract the talented

professionals. This is also helpful in retaining and motivating them to perform better than

before. The base figure offered to the executives has been set at a level to encourage them to

work effectively and remain motivated in the challenging scenarios. It is the lead given to

keep them active throughout. The equity rights and superannuation payment is provided as

long term benefit plan for its employees which will increase the overall outcomes and

efficiency of company in long run (Doni, Gasperini, and Pavone., 2016).

10

The long term incentives offered to the executives relate to the rewards that are

offered in the form of equity. The equity is the same as what is offered to the shareholders.

As a result, the executives in order to attain highest possible return need to perform in a

manner that adds wealth for the shareholders. The same wealth is created for them as they

also own that equity. The lock in period is long which promotes performance that yields

sustainable results. This stands as a motivator to continually improve the average share prices

(Dankova, Valeva, and Štrukelj, 2015).

There are no short term incentives; because the company feels the long term

organisational goals need a consistent approach. The short term incentives rest on the short

term performance based on short term goals. These goals are not consistent and hence

sometimes divert the executives from the main goals (Peng, and Röell, 2014).

ANALYSIS AND COMPARISON OF REMUNERATION METHODS USED

From the table presented above, the policies framed by both the Seek Group and the

Ambition Group have been analysed. The table itself is showing that the policies of Seek

Group have led the executives to perform in a manner that has encouraged an improvement in

company performance. The share price had shown a continual rise over the years. The

eventual rise is also observed in the earning per share of the company. The 50% portion of

total remuneration gets value from the way the company is performing. There is no

alternative available with the executives rather than the improvement of their respective

departments. This shall add to the value that company attains in the market and adds to the

overall wealth of the shareholders (Hoque, 2014). The table has shown that company has

improved its business performance by aligning the interest of the stakeholders with the

organization development.

However, the ambition group has adopted a target based remuneration plan. The

performance bonuses rest on the eligibility of attaining those targets. The share incentive

plans offered are based on the criteria of achievement of a certain level of earning per share.

The whole share incentive plan is already framed which highlights the vesting provisions

(Kerzner, and Kerzner, 2017). This will also result to increasing the overall outcomes and

increased business efficiency in long run.

11

offered in the form of equity. The equity is the same as what is offered to the shareholders.

As a result, the executives in order to attain highest possible return need to perform in a

manner that adds wealth for the shareholders. The same wealth is created for them as they

also own that equity. The lock in period is long which promotes performance that yields

sustainable results. This stands as a motivator to continually improve the average share prices

(Dankova, Valeva, and Štrukelj, 2015).

There are no short term incentives; because the company feels the long term

organisational goals need a consistent approach. The short term incentives rest on the short

term performance based on short term goals. These goals are not consistent and hence

sometimes divert the executives from the main goals (Peng, and Röell, 2014).

ANALYSIS AND COMPARISON OF REMUNERATION METHODS USED

From the table presented above, the policies framed by both the Seek Group and the

Ambition Group have been analysed. The table itself is showing that the policies of Seek

Group have led the executives to perform in a manner that has encouraged an improvement in

company performance. The share price had shown a continual rise over the years. The

eventual rise is also observed in the earning per share of the company. The 50% portion of

total remuneration gets value from the way the company is performing. There is no

alternative available with the executives rather than the improvement of their respective

departments. This shall add to the value that company attains in the market and adds to the

overall wealth of the shareholders (Hoque, 2014). The table has shown that company has

improved its business performance by aligning the interest of the stakeholders with the

organization development.

However, the ambition group has adopted a target based remuneration plan. The

performance bonuses rest on the eligibility of attaining those targets. The share incentive

plans offered are based on the criteria of achievement of a certain level of earning per share.

The whole share incentive plan is already framed which highlights the vesting provisions

(Kerzner, and Kerzner, 2017). This will also result to increasing the overall outcomes and

increased business efficiency in long run.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.