Analysis of Segment Reporting and Consolidated Financial Results

VerifiedAdded on 2020/03/16

|8

|1077

|59

Report

AI Summary

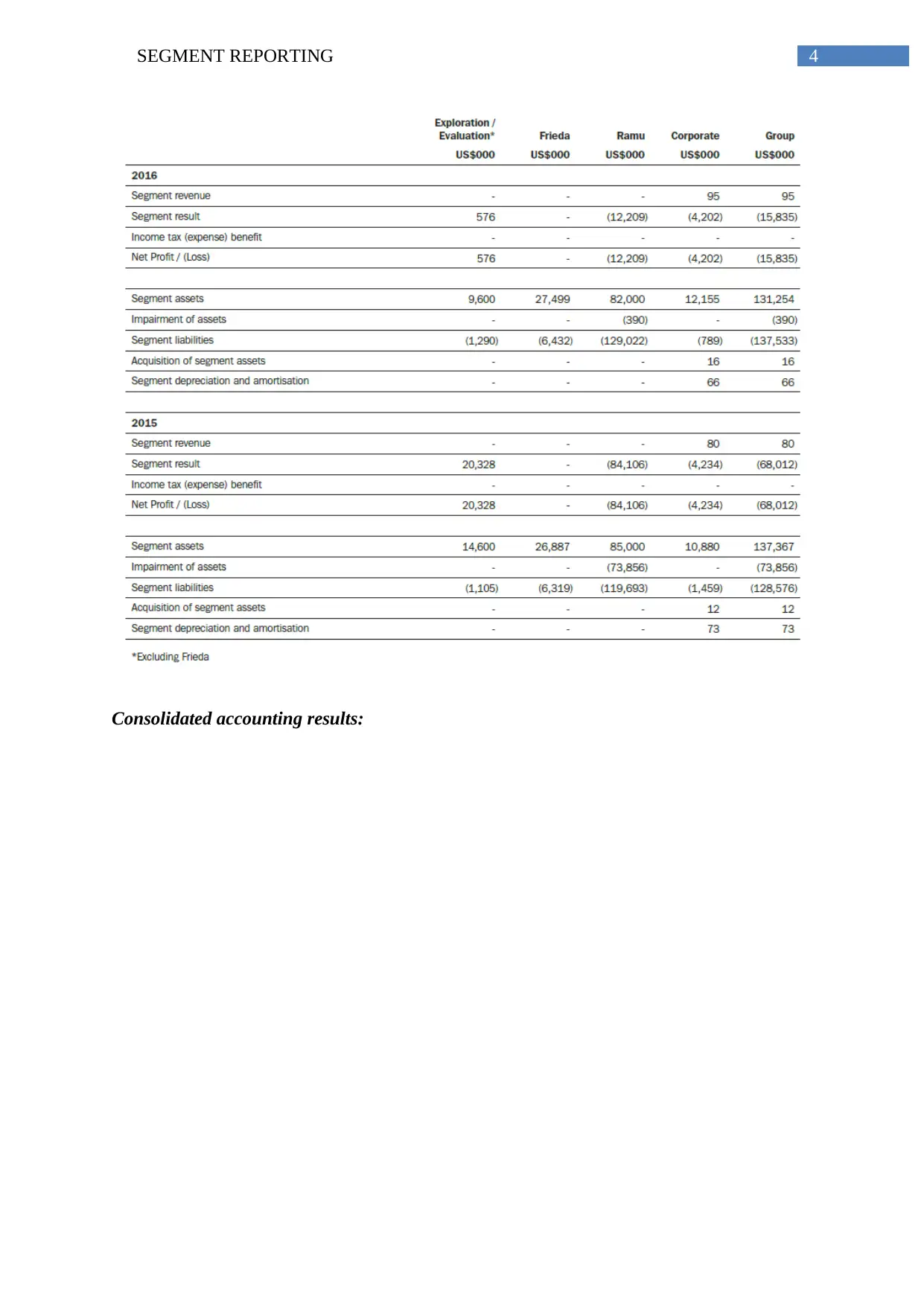

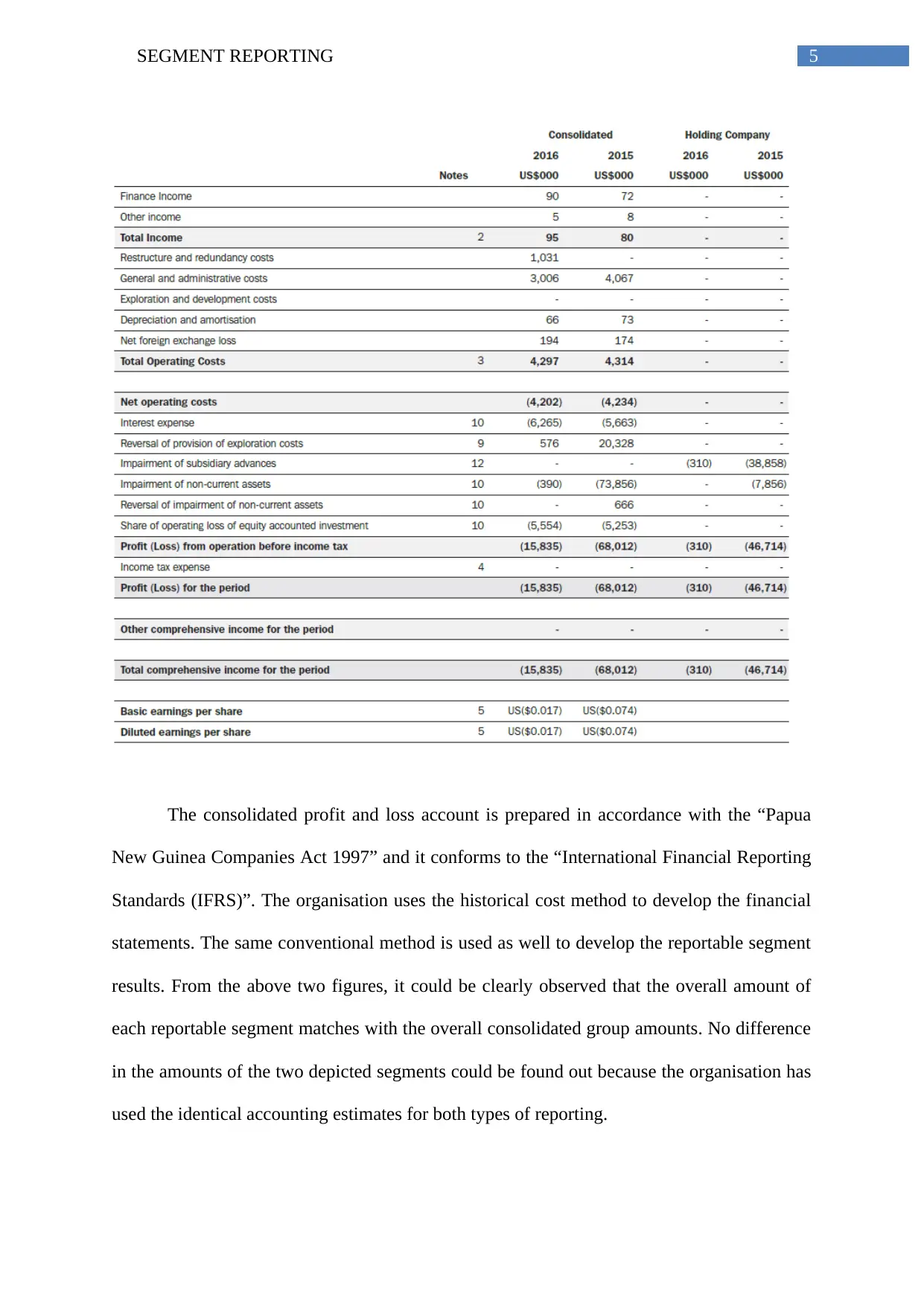

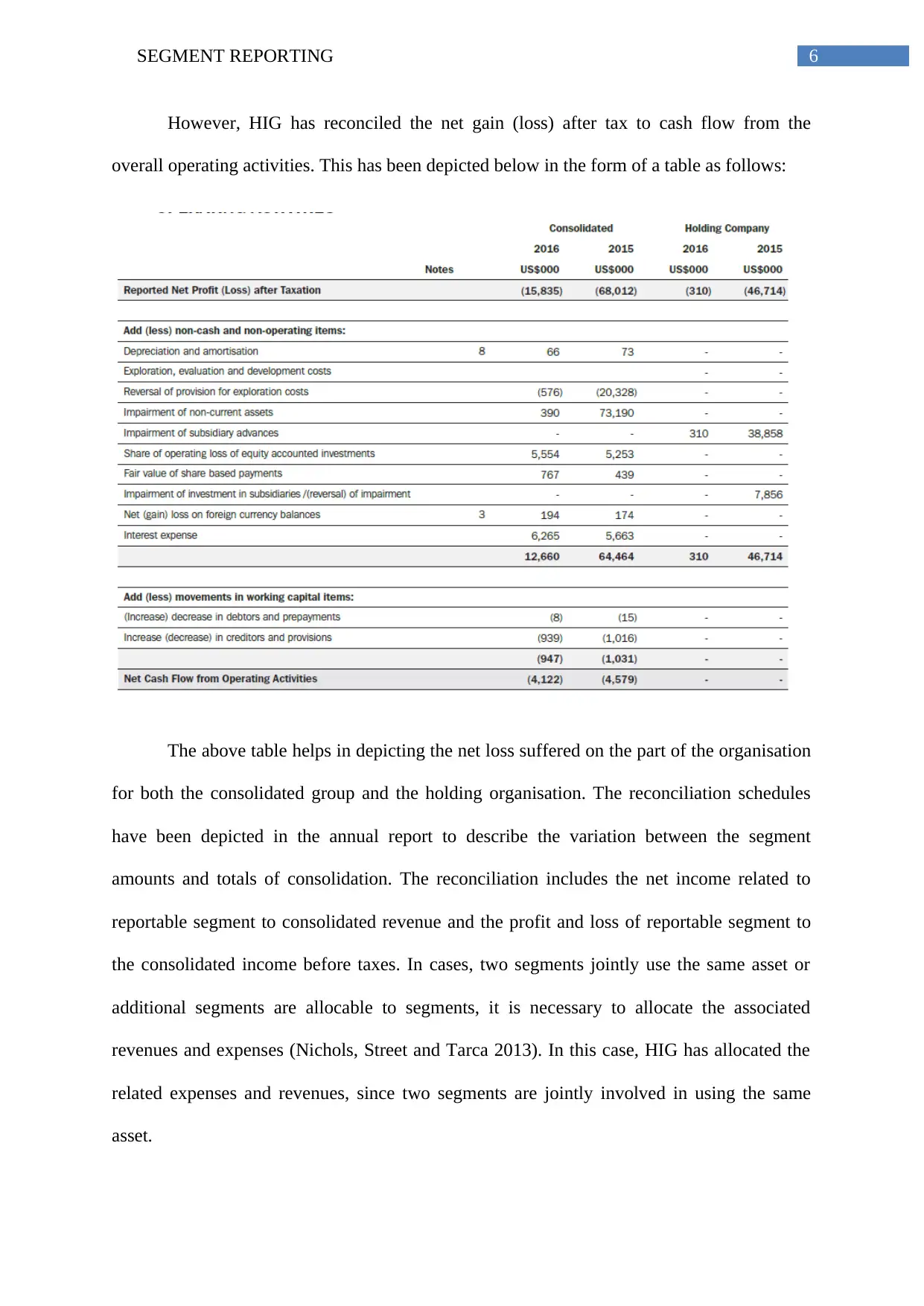

This report provides a comprehensive analysis of segment reporting, focusing on its application in financial statements and consolidated accounting. It examines the core components of segment reporting, including geographically-based external reporting and industry or product-line based internal reporting. The report delves into the criteria for identifying reportable segments as defined by AASB 8, such as business activities, chief decision-maker review, and discrete financial information. It explores the accounting policies related to segment reporting, emphasizing the importance of reconciliation schedules to describe the variations between segment amounts and consolidation totals. The report uses the annual report of HIG to illustrate the practical application of segment reporting, including the identification of reportable segments, the use of consolidated accounting results, and the reconciliation of net gain/loss after tax to cash flow from operating activities. It highlights the allocation of expenses and revenues when two segments jointly use the same asset, demonstrating the practical considerations in segment reporting. The report references key literature and standards, including AASB 8 and AASB 10, to support its analysis and provide a robust understanding of segment reporting.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.