Service Management Project: Analyzing ADCB Bank's Service Strategies

VerifiedAdded on 2022/08/19

|15

|2468

|26

Project

AI Summary

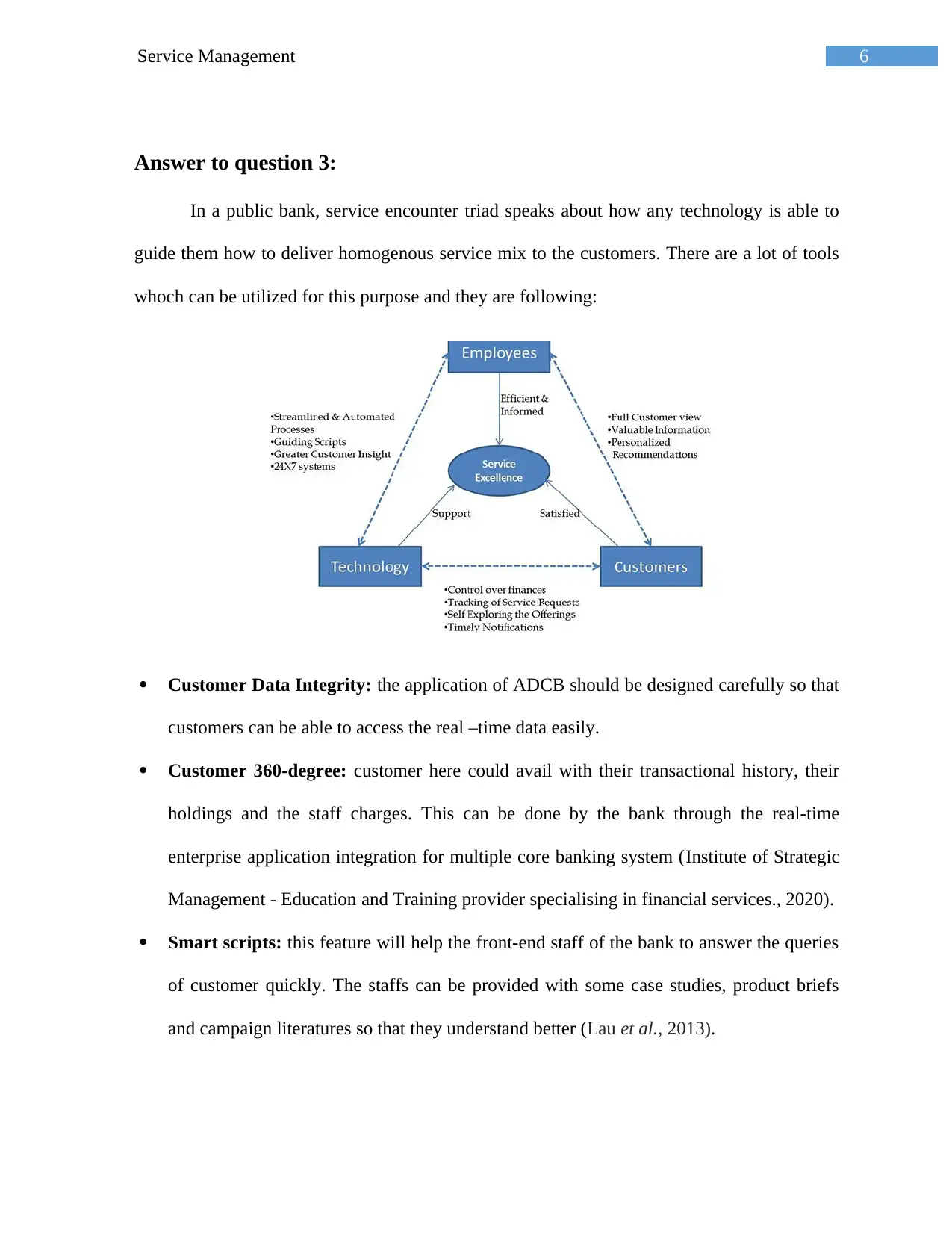

This project is a comprehensive analysis of Abu Dhabi Commercial Bank (ADCB) focusing on various aspects of service management. The project begins with an overview of ADCB, its services, and its position in the UAE banking sector, highlighting its customer-centric approach through digital platforms like ADCB Moneybuddy, and personalized banking options. The project then delves into the features of ADCB Moneybuddy, a money management tool designed to assist customers in managing their finances effectively. The core of the project explores service encounter triads in the context of a public bank, emphasizing the use of technology and strategies for delivering consistent service, including customer data integrity, smart scripts, and high-quality service delivery. Furthermore, the project applies the SERVQUAL model to assess ADCB's service quality and customer satisfaction, examining key dimensions like reliability, responsiveness, and tangibles. Finally, the project identifies and discusses several service management challenges faced by ADCB, such as evolving customer expectations, competition, and regulatory conditions, offering insights into the dynamic nature of service management within the financial industry.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.