BSc Accounting: Service vs. Product Accounting Report, Spring 2020

VerifiedAdded on 2022/09/21

|11

|2013

|22

Report

AI Summary

This report provides a comprehensive analysis of service versus product accounting, comparing and contrasting the characteristics of service, manufacturing, and merchandising industries. It explores the implications of limitation of liability clauses in commercial transactions, detailing their advantages and limitations, and their role in mitigating risks. The report further delves into the financial metric of dividend payout ratio, explaining its calculation, interpretation, and significance in assessing a company's financial health and sustainability. Finally, it examines the use of fixed asset usage and fixed asset life ratios, illustrating how they can be used to determine the appropriate time for fixed asset replacement, aiding in budgetary planning and operational efficiency. The report uses examples to illustrate the concepts discussed, providing a practical understanding of the topics covered.

Running head: SERVICE vs. PRODUCT ACCOUNTING

SERVICE vs. PRODUCT ACCOUNTING

Name of Student

Name of University

Author’s Note

SERVICE vs. PRODUCT ACCOUNTING

Name of Student

Name of University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1SERVICE vs. PRODUCT ACCOUNTING

Table of Contents

QUESTION 1:.....................................................................................................................2

QUESTION 2:.....................................................................................................................5

QUESTION 3:.....................................................................................................................6

QUESTION 4:.....................................................................................................................7

REFERENCES:...................................................................................................................9

Table of Contents

QUESTION 1:.....................................................................................................................2

QUESTION 2:.....................................................................................................................5

QUESTION 3:.....................................................................................................................6

QUESTION 4:.....................................................................................................................7

REFERENCES:...................................................................................................................9

2SERVICE vs. PRODUCT ACCOUNTING

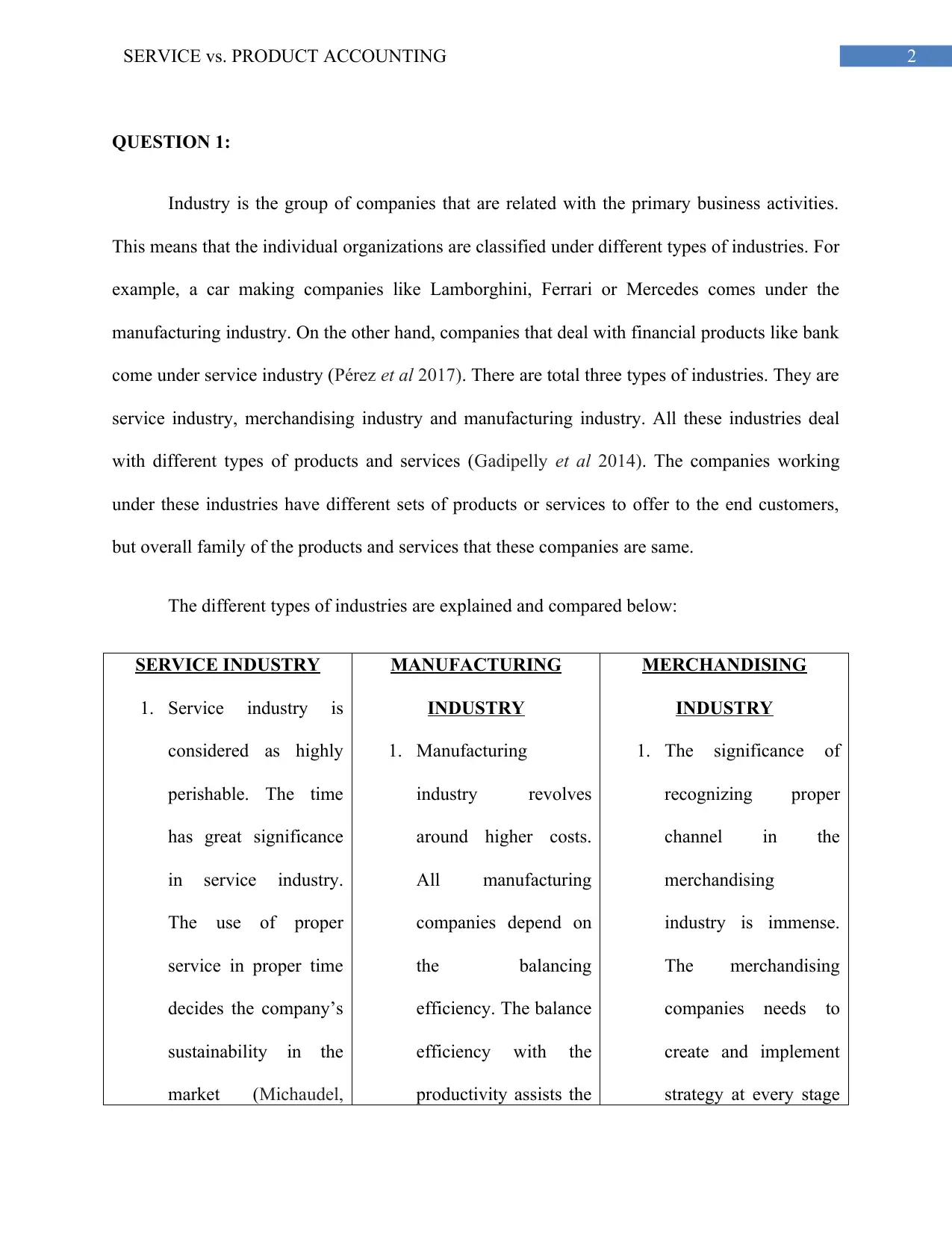

QUESTION 1:

Industry is the group of companies that are related with the primary business activities.

This means that the individual organizations are classified under different types of industries. For

example, a car making companies like Lamborghini, Ferrari or Mercedes comes under the

manufacturing industry. On the other hand, companies that deal with financial products like bank

come under service industry (Pérez et al 2017). There are total three types of industries. They are

service industry, merchandising industry and manufacturing industry. All these industries deal

with different types of products and services (Gadipelly et al 2014). The companies working

under these industries have different sets of products or services to offer to the end customers,

but overall family of the products and services that these companies are same.

The different types of industries are explained and compared below:

SERVICE INDUSTRY

1. Service industry is

considered as highly

perishable. The time

has great significance

in service industry.

The use of proper

service in proper time

decides the company’s

sustainability in the

market (Michaudel,

MANUFACTURING

INDUSTRY

1. Manufacturing

industry revolves

around higher costs.

All manufacturing

companies depend on

the balancing

efficiency. The balance

efficiency with the

productivity assists the

MERCHANDISING

INDUSTRY

1. The significance of

recognizing proper

channel in the

merchandising

industry is immense.

The merchandising

companies needs to

create and implement

strategy at every stage

QUESTION 1:

Industry is the group of companies that are related with the primary business activities.

This means that the individual organizations are classified under different types of industries. For

example, a car making companies like Lamborghini, Ferrari or Mercedes comes under the

manufacturing industry. On the other hand, companies that deal with financial products like bank

come under service industry (Pérez et al 2017). There are total three types of industries. They are

service industry, merchandising industry and manufacturing industry. All these industries deal

with different types of products and services (Gadipelly et al 2014). The companies working

under these industries have different sets of products or services to offer to the end customers,

but overall family of the products and services that these companies are same.

The different types of industries are explained and compared below:

SERVICE INDUSTRY

1. Service industry is

considered as highly

perishable. The time

has great significance

in service industry.

The use of proper

service in proper time

decides the company’s

sustainability in the

market (Michaudel,

MANUFACTURING

INDUSTRY

1. Manufacturing

industry revolves

around higher costs.

All manufacturing

companies depend on

the balancing

efficiency. The balance

efficiency with the

productivity assists the

MERCHANDISING

INDUSTRY

1. The significance of

recognizing proper

channel in the

merchandising

industry is immense.

The merchandising

companies needs to

create and implement

strategy at every stage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3SERVICE vs. PRODUCT ACCOUNTING

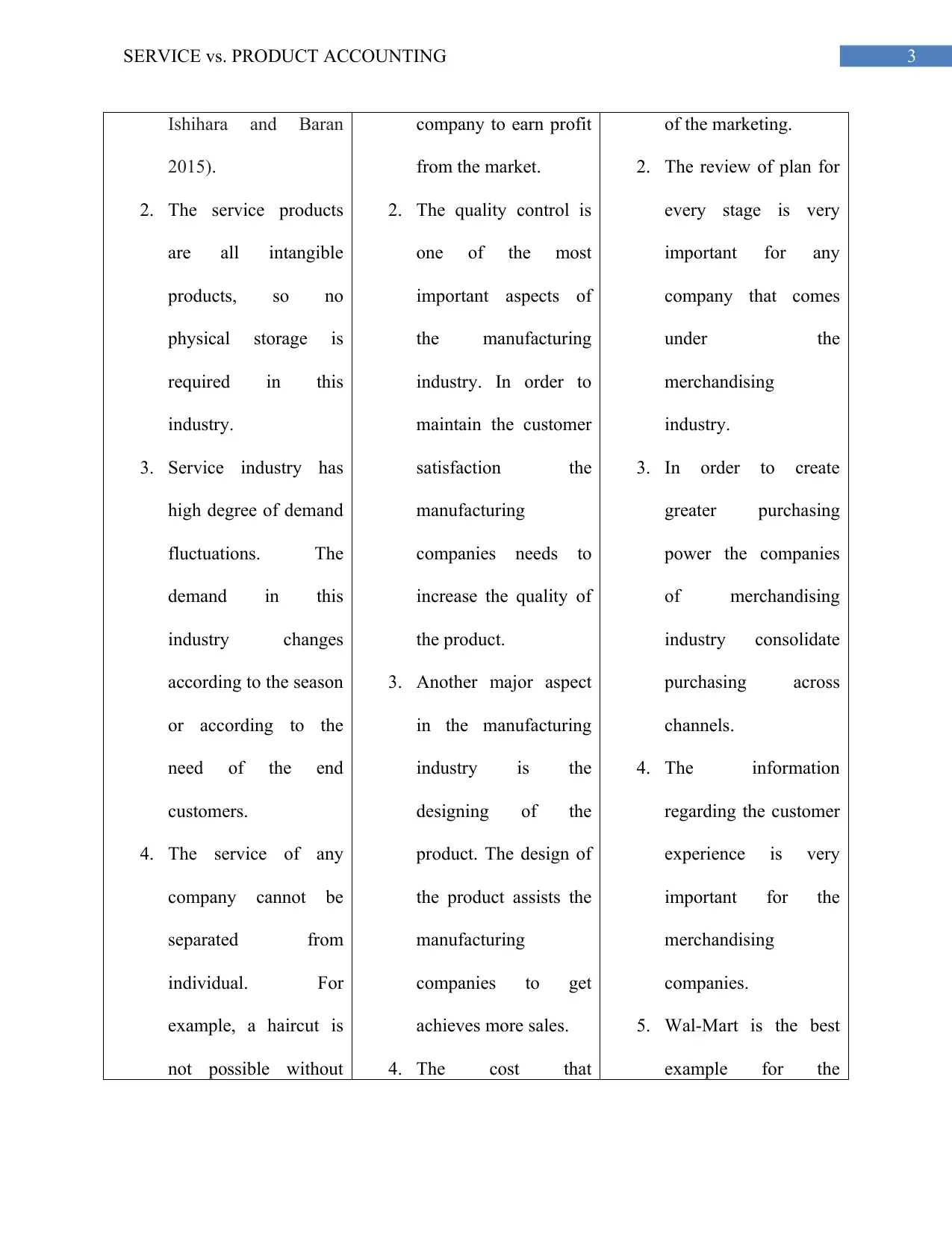

Ishihara and Baran

2015).

2. The service products

are all intangible

products, so no

physical storage is

required in this

industry.

3. Service industry has

high degree of demand

fluctuations. The

demand in this

industry changes

according to the season

or according to the

need of the end

customers.

4. The service of any

company cannot be

separated from

individual. For

example, a haircut is

not possible without

company to earn profit

from the market.

2. The quality control is

one of the most

important aspects of

the manufacturing

industry. In order to

maintain the customer

satisfaction the

manufacturing

companies needs to

increase the quality of

the product.

3. Another major aspect

in the manufacturing

industry is the

designing of the

product. The design of

the product assists the

manufacturing

companies to get

achieves more sales.

4. The cost that

of the marketing.

2. The review of plan for

every stage is very

important for any

company that comes

under the

merchandising

industry.

3. In order to create

greater purchasing

power the companies

of merchandising

industry consolidate

purchasing across

channels.

4. The information

regarding the customer

experience is very

important for the

merchandising

companies.

5. Wal-Mart is the best

example for the

Ishihara and Baran

2015).

2. The service products

are all intangible

products, so no

physical storage is

required in this

industry.

3. Service industry has

high degree of demand

fluctuations. The

demand in this

industry changes

according to the season

or according to the

need of the end

customers.

4. The service of any

company cannot be

separated from

individual. For

example, a haircut is

not possible without

company to earn profit

from the market.

2. The quality control is

one of the most

important aspects of

the manufacturing

industry. In order to

maintain the customer

satisfaction the

manufacturing

companies needs to

increase the quality of

the product.

3. Another major aspect

in the manufacturing

industry is the

designing of the

product. The design of

the product assists the

manufacturing

companies to get

achieves more sales.

4. The cost that

of the marketing.

2. The review of plan for

every stage is very

important for any

company that comes

under the

merchandising

industry.

3. In order to create

greater purchasing

power the companies

of merchandising

industry consolidate

purchasing across

channels.

4. The information

regarding the customer

experience is very

important for the

merchandising

companies.

5. Wal-Mart is the best

example for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4SERVICE vs. PRODUCT ACCOUNTING

the barber.

5. Pricing of services are

mainly influenced by

perishability,

fluctuations in demand

and insuperability.

6. The best example of

service industry is the

service that IT

companies provide to

their clients.

manufacturing industry

spends in creating a

product determines the

price of the product.

Thus, it is necessary

for the manufacturing

industry to implement

cost-effective strategy,

so that they can reduce

the price of the

product, which will

enable them to gather

more customers in the

market.

5. The car companies like

Mercedes or Aston

Martin creates cars for

their customers are

some of the best

example of

manufacturing

industry.

merchandising

industry who sales

products directly to the

customers.

the barber.

5. Pricing of services are

mainly influenced by

perishability,

fluctuations in demand

and insuperability.

6. The best example of

service industry is the

service that IT

companies provide to

their clients.

manufacturing industry

spends in creating a

product determines the

price of the product.

Thus, it is necessary

for the manufacturing

industry to implement

cost-effective strategy,

so that they can reduce

the price of the

product, which will

enable them to gather

more customers in the

market.

5. The car companies like

Mercedes or Aston

Martin creates cars for

their customers are

some of the best

example of

manufacturing

industry.

merchandising

industry who sales

products directly to the

customers.

5SERVICE vs. PRODUCT ACCOUNTING

QUESTION 2:

Commercial transactions carry lots of risks. In order to mitigate the risks the limitation of

liability clause are being created. Limitation of liability is a clause that both parties agree during

any kind of transactions (Aguir et al 2014). As per this clause the amount that one party has to

pay to the other party gets limited if that first party suffers loss. The limitation of liability clause

needs to be created based on the agreement that both the companies have to offer. The limited

liability clause has certain limitations. These limitations are explained below:

1. If one party fails to fulfill the conditions or obligations that are mentioned in the limited

liability clause then the party suffers severe consequences regarding the breach of

contract.

2. The negligence in fulfilling the duty enables the company to make liability, which affects

the profitability of the company (Segerson 2018).

3. If any of the party makes false representation then the contract automatically becomes

null and void.

The main advantage of limitation of liability is as follows:

1. It protects the company from certain liability and claims. The company can safeguard

themselves from unforeseen losses using the limitation of liability.

2. It also protects the company from having any kind of damage by bringing strict rules in

the contract (Elkin-Koren 2014). The rules enable the parties to conduct their business

operations without any kind of problem.

For example an investment company or an individual investor enters into an agreement of

limited liability clause of investment of $1 million, which is also his total liability. This indicates

QUESTION 2:

Commercial transactions carry lots of risks. In order to mitigate the risks the limitation of

liability clause are being created. Limitation of liability is a clause that both parties agree during

any kind of transactions (Aguir et al 2014). As per this clause the amount that one party has to

pay to the other party gets limited if that first party suffers loss. The limitation of liability clause

needs to be created based on the agreement that both the companies have to offer. The limited

liability clause has certain limitations. These limitations are explained below:

1. If one party fails to fulfill the conditions or obligations that are mentioned in the limited

liability clause then the party suffers severe consequences regarding the breach of

contract.

2. The negligence in fulfilling the duty enables the company to make liability, which affects

the profitability of the company (Segerson 2018).

3. If any of the party makes false representation then the contract automatically becomes

null and void.

The main advantage of limitation of liability is as follows:

1. It protects the company from certain liability and claims. The company can safeguard

themselves from unforeseen losses using the limitation of liability.

2. It also protects the company from having any kind of damage by bringing strict rules in

the contract (Elkin-Koren 2014). The rules enable the parties to conduct their business

operations without any kind of problem.

For example an investment company or an individual investor enters into an agreement of

limited liability clause of investment of $1 million, which is also his total liability. This indicates

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6SERVICE vs. PRODUCT ACCOUNTING

that potentially loss of the investor or investing company is secured. It also states that the

investment company or the individual investor is not liable for any kind of liability till $ 1

million.

QUESTION 3:

The payout ratio is the important financial metric that enable the company to determine

the financial position of the company. It actually does so by analysing the sustainability of the

company. The dividend payout ratio analyses the sustainability through company’s dividend

program. The dividend payment program can be explained as the amount that the company needs

to pay to their shareholders from the net income of the company. The sustainability of the

company can be determined through the total earnings of the company (Giné and Karlan 2014).

The higher the total earnings of the company, it is more likely that the company will pay the high

dividend to their shareholders. The dividend payout ratio is also termed as the payout ratio and it

is calculated using by dividing the total dividends with the net income of the company. The most

favourable payout ratio is 100%. The 100% dividend payout ratio states that the company is

paying high amount of dividend to their shareholders. If the dividend payout ratio is less than

100% then it states that the company’s is paying fewer amounts in comparison to their earnings.

On the contrary if the dividend payout ratio is higher than 100% then it indicates that the

company is paying high dividend in comparison to the total earnings of the company. There is

no specific percentage of dividend payout ratios. The percentage totally depends on the industry

in which company operates in (Hasan et al 2015). The companies who fall under the defensive

industries like pipelines, utilities and telecommunication companies can afford to pay high

dividend after a long haul. Companies that falls under the manufacturing industries works under

that potentially loss of the investor or investing company is secured. It also states that the

investment company or the individual investor is not liable for any kind of liability till $ 1

million.

QUESTION 3:

The payout ratio is the important financial metric that enable the company to determine

the financial position of the company. It actually does so by analysing the sustainability of the

company. The dividend payout ratio analyses the sustainability through company’s dividend

program. The dividend payment program can be explained as the amount that the company needs

to pay to their shareholders from the net income of the company. The sustainability of the

company can be determined through the total earnings of the company (Giné and Karlan 2014).

The higher the total earnings of the company, it is more likely that the company will pay the high

dividend to their shareholders. The dividend payout ratio is also termed as the payout ratio and it

is calculated using by dividing the total dividends with the net income of the company. The most

favourable payout ratio is 100%. The 100% dividend payout ratio states that the company is

paying high amount of dividend to their shareholders. If the dividend payout ratio is less than

100% then it states that the company’s is paying fewer amounts in comparison to their earnings.

On the contrary if the dividend payout ratio is higher than 100% then it indicates that the

company is paying high dividend in comparison to the total earnings of the company. There is

no specific percentage of dividend payout ratios. The percentage totally depends on the industry

in which company operates in (Hasan et al 2015). The companies who fall under the defensive

industries like pipelines, utilities and telecommunication companies can afford to pay high

dividend after a long haul. Companies that falls under the manufacturing industries works under

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7SERVICE vs. PRODUCT ACCOUNTING

very vulnerable market, so it is seen that these companies are more likely to have less dividends

payout ratio in comparison to other industries.

For example, if a company’s total earnings for a single financial year is $1 million and

the management of the company decides to pay dividend of $25,000 then the dividend payout

ratio for the company would be 40% for that company. This also indicates that the company’s

retention ratio is 60%, which will be visible in the retained earnings section of the financial

statements of the annual report.

QUESTION 4:

In order to replace the fixed assets the fixed assets usage and fixed assets life can be used.

Both these ratios state the fixed assets life expectancy. Irrespective of the industry, the

management of the company can use these ratios, so that they can determine the time when the

fixed assets needs to replace. In this way the management of the company can predict the

expenses and create a budget for the company for that financial year.

The fixed assets usage determines the usage of the fixed assets. In this way the

management of the company can easily determine the importance of the fixed assets. The

formula for calculating the fixed assets usage is the Accumulated depreciation divided by the

gross depreciation fixed assets. The fixed usage ratio always provides answers in percentage. On

the other hand, fixed assets life states about the remaining life of the fixed assets. In order to

calculate the fixed assets life net depreciable fixed assets needs to divided from depreciable

expense.

For example, a delivery van, which is considered as the fixed asset has the life usage of

70% and the fixed asset life for that van is 3 months. This indicates that the van has the high

very vulnerable market, so it is seen that these companies are more likely to have less dividends

payout ratio in comparison to other industries.

For example, if a company’s total earnings for a single financial year is $1 million and

the management of the company decides to pay dividend of $25,000 then the dividend payout

ratio for the company would be 40% for that company. This also indicates that the company’s

retention ratio is 60%, which will be visible in the retained earnings section of the financial

statements of the annual report.

QUESTION 4:

In order to replace the fixed assets the fixed assets usage and fixed assets life can be used.

Both these ratios state the fixed assets life expectancy. Irrespective of the industry, the

management of the company can use these ratios, so that they can determine the time when the

fixed assets needs to replace. In this way the management of the company can predict the

expenses and create a budget for the company for that financial year.

The fixed assets usage determines the usage of the fixed assets. In this way the

management of the company can easily determine the importance of the fixed assets. The

formula for calculating the fixed assets usage is the Accumulated depreciation divided by the

gross depreciation fixed assets. The fixed usage ratio always provides answers in percentage. On

the other hand, fixed assets life states about the remaining life of the fixed assets. In order to

calculate the fixed assets life net depreciable fixed assets needs to divided from depreciable

expense.

For example, a delivery van, which is considered as the fixed asset has the life usage of

70% and the fixed asset life for that van is 3 months. This indicates that the van has the high

8SERVICE vs. PRODUCT ACCOUNTING

percentage of use and the life expectancy of the van is also less. This states the company needs to

think for changing the van, so that business operation does not get hampered.

percentage of use and the life expectancy of the van is also less. This states the company needs to

think for changing the van, so that business operation does not get hampered.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9SERVICE vs. PRODUCT ACCOUNTING

REFERENCES:

Aguir, I., Burns, N., Mansi, S.A. and Wald, J.K., 2014. Liability protection, director

compensation, and incentives. Journal of Financial Intermediation, 23(4), pp.570-589.

Ahmed, I.E., 2015. Liquidity, profitability and the dividends payout policy. World Review of

Business Research, 5(2), pp.73-85.

Demirgüneş, K., 2015. Determinants of target dividend payout ratio: A panel autoregressive

distributed lag analysis. International Journal of Economics and Financial Issues, 5(2), pp.418-

426.

Elkin-Koren, N., 2014. After twenty years: Copyright liability of online intermediaries. The

Evolution and Equilibrium of Copyright in the Digital Age (Susy Frankel & Daniel J Gervais

eds.)(2014 Forthcoming).

Gadipelly, C., Pérez-González, A., Yadav, G.D., Ortiz, I., Ibáñez, R., Rathod, V.K. and Marathe,

K.V., 2014. Pharmaceutical industry wastewater: review of the technologies for water treatment

and reuse. Industrial & Engineering Chemistry Research, 53(29), pp.11571-11592.

Giné, X. and Karlan, D.S., 2014. Group versus individual liability: Short and long term evidence

from Philippine microcredit lending groups. Journal of development Economics, 107, pp.65-83.

Hasan, M., Ahmad, M.I., Rafiq, M.Y. and Rehman, R.U., 2015. Dividend payout ratio and firm’s

profitability. Evidence from Pakistan. Theoretical Economics Letters, 5(03), p.441.

REFERENCES:

Aguir, I., Burns, N., Mansi, S.A. and Wald, J.K., 2014. Liability protection, director

compensation, and incentives. Journal of Financial Intermediation, 23(4), pp.570-589.

Ahmed, I.E., 2015. Liquidity, profitability and the dividends payout policy. World Review of

Business Research, 5(2), pp.73-85.

Demirgüneş, K., 2015. Determinants of target dividend payout ratio: A panel autoregressive

distributed lag analysis. International Journal of Economics and Financial Issues, 5(2), pp.418-

426.

Elkin-Koren, N., 2014. After twenty years: Copyright liability of online intermediaries. The

Evolution and Equilibrium of Copyright in the Digital Age (Susy Frankel & Daniel J Gervais

eds.)(2014 Forthcoming).

Gadipelly, C., Pérez-González, A., Yadav, G.D., Ortiz, I., Ibáñez, R., Rathod, V.K. and Marathe,

K.V., 2014. Pharmaceutical industry wastewater: review of the technologies for water treatment

and reuse. Industrial & Engineering Chemistry Research, 53(29), pp.11571-11592.

Giné, X. and Karlan, D.S., 2014. Group versus individual liability: Short and long term evidence

from Philippine microcredit lending groups. Journal of development Economics, 107, pp.65-83.

Hasan, M., Ahmad, M.I., Rafiq, M.Y. and Rehman, R.U., 2015. Dividend payout ratio and firm’s

profitability. Evidence from Pakistan. Theoretical Economics Letters, 5(03), p.441.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10SERVICE vs. PRODUCT ACCOUNTING

Michaudel, Q., Ishihara, Y. and Baran, P.S., 2015. Academia–industry symbiosis in organic

chemistry. Accounts of chemical research, 48(3), pp.712-721.

Pérez, J.F., Llanos, J., Sá ez, C., López, C., Cañ izares, P. and Rodrigo, M.A., 2017. Treatment of

real effluents from the pharmaceutical industry: a comparison between Fenton oxidation and

conductive-diamond electro-oxidation. Journal of environmental management, 195, pp.216-223.

Segerson, K., 2018. Liability for groundwater contamination from pesticides. The Economics of

Water Quality.

Michaudel, Q., Ishihara, Y. and Baran, P.S., 2015. Academia–industry symbiosis in organic

chemistry. Accounts of chemical research, 48(3), pp.712-721.

Pérez, J.F., Llanos, J., Sá ez, C., López, C., Cañ izares, P. and Rodrigo, M.A., 2017. Treatment of

real effluents from the pharmaceutical industry: a comparison between Fenton oxidation and

conductive-diamond electro-oxidation. Journal of environmental management, 195, pp.216-223.

Segerson, K., 2018. Liability for groundwater contamination from pesticides. The Economics of

Water Quality.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.