Comprehensive Financial Analysis: Seven Group Holdings Report

VerifiedAdded on 2023/06/04

|21

|4454

|357

Report

AI Summary

This report provides a comprehensive financial analysis of Seven Group Holdings, examining its performance across various key areas. The analysis begins with an introduction to Seven Group Holdings, detailing its business segments and operational scope within Australia and China. The core of the report focuses on a detailed financial ratio analysis, categorized into liquidity, solvency, asset utilization, profitability, and market value ratios. The liquidity ratios, including current and quick ratios, are used to assess the company's short-term solvency. Long-term solvency is evaluated through debt-to-asset, debt-to-equity, and interest coverage ratios. Asset utilization is examined through inventory turnover, asset turnover, and receivable turnover ratios. Profitability is assessed using gross margin, ROA, and ROE. Market value is evaluated through EPS and P/E ratios. The analysis also includes an examination of Seven Group Holdings' share price movements and a share valuation based on a dividend growth rate model. The report concludes with an overall evaluation of the company's financial health and provides recommendations based on the analysis.

Fundamental Analysis of Seven Group Holdings 1

FUNDAMENTAL ANALYSIS OF SEVEN GROUP HOLDINGS

Author

Course

Professor

City

Date

FUNDAMENTAL ANALYSIS OF SEVEN GROUP HOLDINGS

Author

Course

Professor

City

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fundamental Analysis of Seven Group Holdings 2

Table of Contents

Introduction....................................................................................................................3

Performance Ratios Analysis of Seven Group Holdings...............................................3

Short-Run Solvency or the Liquidity Ratios..............................................................4

Current ratio...........................................................................................................4

Quick ratio..............................................................................................................5

Long-Term Solvency or the Financial Leverage Ratios............................................6

Debt to total assets.................................................................................................6

Debt to equity.........................................................................................................7

Interest coverage....................................................................................................8

Asset Utilization or Turnover Ratios.........................................................................8

Inventory turnover..................................................................................................9

Assets turnover.......................................................................................................9

Receivable turnover.............................................................................................10

Profitability Ratios...................................................................................................11

Gross Margin........................................................................................................11

ROA.....................................................................................................................12

ROE......................................................................................................................13

Market Value Ratios................................................................................................14

EPS.......................................................................................................................14

P/E ratio................................................................................................................14

Seven Group Share Price Movements.........................................................................15

Share Valuation............................................................................................................17

Conclusion...................................................................................................................18

Recommendation.........................................................................................................18

REFERENCES.............................................................................................................20

Table of Contents

Introduction....................................................................................................................3

Performance Ratios Analysis of Seven Group Holdings...............................................3

Short-Run Solvency or the Liquidity Ratios..............................................................4

Current ratio...........................................................................................................4

Quick ratio..............................................................................................................5

Long-Term Solvency or the Financial Leverage Ratios............................................6

Debt to total assets.................................................................................................6

Debt to equity.........................................................................................................7

Interest coverage....................................................................................................8

Asset Utilization or Turnover Ratios.........................................................................8

Inventory turnover..................................................................................................9

Assets turnover.......................................................................................................9

Receivable turnover.............................................................................................10

Profitability Ratios...................................................................................................11

Gross Margin........................................................................................................11

ROA.....................................................................................................................12

ROE......................................................................................................................13

Market Value Ratios................................................................................................14

EPS.......................................................................................................................14

P/E ratio................................................................................................................14

Seven Group Share Price Movements.........................................................................15

Share Valuation............................................................................................................17

Conclusion...................................................................................................................18

Recommendation.........................................................................................................18

REFERENCES.............................................................................................................20

Fundamental Analysis of Seven Group Holdings 3

Introduction

Seven Group Holdings is usually a diversified investment and operating firm

operating in construction, mining and media industries (Reuters.com 2018). The

company was established in the year 1991 by the receivers with the aim of bundling

together assets Christopher’s failed business. Its segment comprises of Wes Trac

Australia that is currently the authorized caterpillar seller in the Australian Capital

Territory as well as in New South Wales (Investsmart.com 2018). The second

segment is Wes Trac China that is currently the only authorized caterpillar trader in

North Eastern China. Finally, there is AllightSykes that operates in sales, assembly,

manufacture as well as support of the lighting, dewatering equipment and power

generation as well as in distribution of the Perkins engines. The company operates in

two key countries; that is, China and Australia (Market Index 2018). Seven Group

Holdings has great assets, strong management team as well as engaged personnel that

enable it to capture any opportunity of improving markets where it operates. As such,

the paper present analysis of financial ratio analysis based on five categories; that is,

profitability, market value, liquidity, efficiency and financial leverage in determining

strength and weakness of the firm (Seven Group Holdings 2017). It also presents

historical share trend and value of the company’s stock based on dividend growth rate

model. These would help in the researcher in evaluating Seven Group Holdings and

provide financial advice to the client on whether or not the client should include share

of Seven Group Holding in his investment portfolio.

Performance Ratios Analysis of Seven Group Holdings

Financial ratio analysis is usually the tool developed in performing quantitative

analysis on figures reported on the financial statements (Lewellen 2004). This assists

Introduction

Seven Group Holdings is usually a diversified investment and operating firm

operating in construction, mining and media industries (Reuters.com 2018). The

company was established in the year 1991 by the receivers with the aim of bundling

together assets Christopher’s failed business. Its segment comprises of Wes Trac

Australia that is currently the authorized caterpillar seller in the Australian Capital

Territory as well as in New South Wales (Investsmart.com 2018). The second

segment is Wes Trac China that is currently the only authorized caterpillar trader in

North Eastern China. Finally, there is AllightSykes that operates in sales, assembly,

manufacture as well as support of the lighting, dewatering equipment and power

generation as well as in distribution of the Perkins engines. The company operates in

two key countries; that is, China and Australia (Market Index 2018). Seven Group

Holdings has great assets, strong management team as well as engaged personnel that

enable it to capture any opportunity of improving markets where it operates. As such,

the paper present analysis of financial ratio analysis based on five categories; that is,

profitability, market value, liquidity, efficiency and financial leverage in determining

strength and weakness of the firm (Seven Group Holdings 2017). It also presents

historical share trend and value of the company’s stock based on dividend growth rate

model. These would help in the researcher in evaluating Seven Group Holdings and

provide financial advice to the client on whether or not the client should include share

of Seven Group Holding in his investment portfolio.

Performance Ratios Analysis of Seven Group Holdings

Financial ratio analysis is usually the tool developed in performing quantitative

analysis on figures reported on the financial statements (Lewellen 2004). This assists

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fundamental Analysis of Seven Group Holdings 4

in linking the three forms of the financial statements all together and provides figures

which are comparable between firms and across sectors. Basically, ratio analysis if the

most widely utilized fundamental analysis approaches (Halkos & Salamouris 2004).

Nonetheless, ratios differ across different sectors and comparisons in between

completely different forms of organization are usually not valid (Kumbirai & Webb

2010). Ratios falls into numerous categories and for this purpose, the analysis would

use the five commonly used categories to analyse financial performance and position

of Seven Group Holdings in the past two years. These categories include profitability

ratios, asset utilizations, liquidity ratios, market value as well as financial leverage

ratios.

Short-Run Solvency or the Liquidity Ratios

Liquidity or short-term solvency ratios are the widely used financial ratios. These

ratios are very significant especially to the creditors as they measure an organization’s

capacity of meeting its immediate or short-term debts (Lewellen 2004). In this case,

quick as well as current ratio would be used in evaluating liquidity of Seven Group

Holdings over the past two years.

Current ratio

This form of financial ratio would be useful in measuring Seven Group Holdings

current assets against current liabilities (Halkos & Salamouris 2004). It would indicate

or signals whether Seven Group Holdings could settle its short-term debts obligations

by liquidating all its current assets (Kumbirai & Webb 2010). In this case, a low ratio

would signal that Seven Group Holdings might be experiencing hard times in settling

its current debts and therefore require immediate investigations; nonetheless, high

ratio means that Seven Group Holdings is having easier times in settling its short-term

in linking the three forms of the financial statements all together and provides figures

which are comparable between firms and across sectors. Basically, ratio analysis if the

most widely utilized fundamental analysis approaches (Halkos & Salamouris 2004).

Nonetheless, ratios differ across different sectors and comparisons in between

completely different forms of organization are usually not valid (Kumbirai & Webb

2010). Ratios falls into numerous categories and for this purpose, the analysis would

use the five commonly used categories to analyse financial performance and position

of Seven Group Holdings in the past two years. These categories include profitability

ratios, asset utilizations, liquidity ratios, market value as well as financial leverage

ratios.

Short-Run Solvency or the Liquidity Ratios

Liquidity or short-term solvency ratios are the widely used financial ratios. These

ratios are very significant especially to the creditors as they measure an organization’s

capacity of meeting its immediate or short-term debts (Lewellen 2004). In this case,

quick as well as current ratio would be used in evaluating liquidity of Seven Group

Holdings over the past two years.

Current ratio

This form of financial ratio would be useful in measuring Seven Group Holdings

current assets against current liabilities (Halkos & Salamouris 2004). It would indicate

or signals whether Seven Group Holdings could settle its short-term debts obligations

by liquidating all its current assets (Kumbirai & Webb 2010). In this case, a low ratio

would signal that Seven Group Holdings might be experiencing hard times in settling

its current debts and therefore require immediate investigations; nonetheless, high

ratio means that Seven Group Holdings is having easier times in settling its short-term

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fundamental Analysis of Seven Group Holdings 5

debts. . In this case, Seven Group Holdings current ratio for the past two years was as

follows:

2016 = 1,783.1/907.4 = 1.97

2017 = 1,909.4/686.6= 2.78

Figure 1: trend in current ratio 2016-2017

2016 2017

0

0.5

1

1.5

2

2.5

3

1.97

2.78

Current ratio

Current ratio

Based on the above results, it is evident that Seven Group Holdings current ratio

increased over the last two years moving from 1.97 in 2016 to 2.78 in 2017. The

increase in current ratio is attributable to introduction of assets held for the sales in

2017. Besides, the increase in this ratio implies that for the last two years, Seven

Group Holdings has been having easy time in settling all its short-term debts.

Quick ratio

The ratio is a bit stringent compared to current ratio. It would help in comparing cash,

the short-term marketable stocks as well as the account receivables of Seven Group

debts. . In this case, Seven Group Holdings current ratio for the past two years was as

follows:

2016 = 1,783.1/907.4 = 1.97

2017 = 1,909.4/686.6= 2.78

Figure 1: trend in current ratio 2016-2017

2016 2017

0

0.5

1

1.5

2

2.5

3

1.97

2.78

Current ratio

Current ratio

Based on the above results, it is evident that Seven Group Holdings current ratio

increased over the last two years moving from 1.97 in 2016 to 2.78 in 2017. The

increase in current ratio is attributable to introduction of assets held for the sales in

2017. Besides, the increase in this ratio implies that for the last two years, Seven

Group Holdings has been having easy time in settling all its short-term debts.

Quick ratio

The ratio is a bit stringent compared to current ratio. It would help in comparing cash,

the short-term marketable stocks as well as the account receivables of Seven Group

Fundamental Analysis of Seven Group Holdings 6

Holdings to its current liabilities (Halkos & Salamouris 2004). In this case, Seven

Group Holdings quick ratio for the past two years was as follows:

2016 = 1,783,100- 831,300 /907,400 = 1.05

2017 = 1,909,400- 654,700 / 686,600 = 1.83

From the above outcome, it is evident that Seven Group Holdings quick ratio

increased over the past two years. The increase implies that the company has been

having easy time in turning its most liquid assets to settle its short-term debts.

Long-Term Solvency or the Financial Leverage Ratios

Financial leverage are the financial ratios used in measuring an organization’s

capacity of meeting most of its long-term debts (Kumbirai & Webb 2010). This offers

some insights on an organization’s capital structure and level of the financial leverage

the company is utilizing. In this case, financial leverage ratios such as debt to asset,

interest coverage and the debt/equity ratios would be useful in Seven Group Holdings

case since it would permit Seven Group Holdings’ potential investors to determine

whether SVW has enough cash flows in settling its interest expenses and other

expenses (Halkos & Salamouris 2004).

Debt to total assets

This ratio is one of the most common solvency ratios and would be used in measuring

percentage of Seven Group Holdings total assets which is mostly financed by the

debts. It is usually computed by dividing the total debts by the total assets (Halkos &

Salamouris 2004). Here, higher figure implies that the company is utilizing huge

Holdings to its current liabilities (Halkos & Salamouris 2004). In this case, Seven

Group Holdings quick ratio for the past two years was as follows:

2016 = 1,783,100- 831,300 /907,400 = 1.05

2017 = 1,909,400- 654,700 / 686,600 = 1.83

From the above outcome, it is evident that Seven Group Holdings quick ratio

increased over the past two years. The increase implies that the company has been

having easy time in turning its most liquid assets to settle its short-term debts.

Long-Term Solvency or the Financial Leverage Ratios

Financial leverage are the financial ratios used in measuring an organization’s

capacity of meeting most of its long-term debts (Kumbirai & Webb 2010). This offers

some insights on an organization’s capital structure and level of the financial leverage

the company is utilizing. In this case, financial leverage ratios such as debt to asset,

interest coverage and the debt/equity ratios would be useful in Seven Group Holdings

case since it would permit Seven Group Holdings’ potential investors to determine

whether SVW has enough cash flows in settling its interest expenses and other

expenses (Halkos & Salamouris 2004).

Debt to total assets

This ratio is one of the most common solvency ratios and would be used in measuring

percentage of Seven Group Holdings total assets which is mostly financed by the

debts. It is usually computed by dividing the total debts by the total assets (Halkos &

Salamouris 2004). Here, higher figure implies that the company is utilizing huge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fundamental Analysis of Seven Group Holdings 7

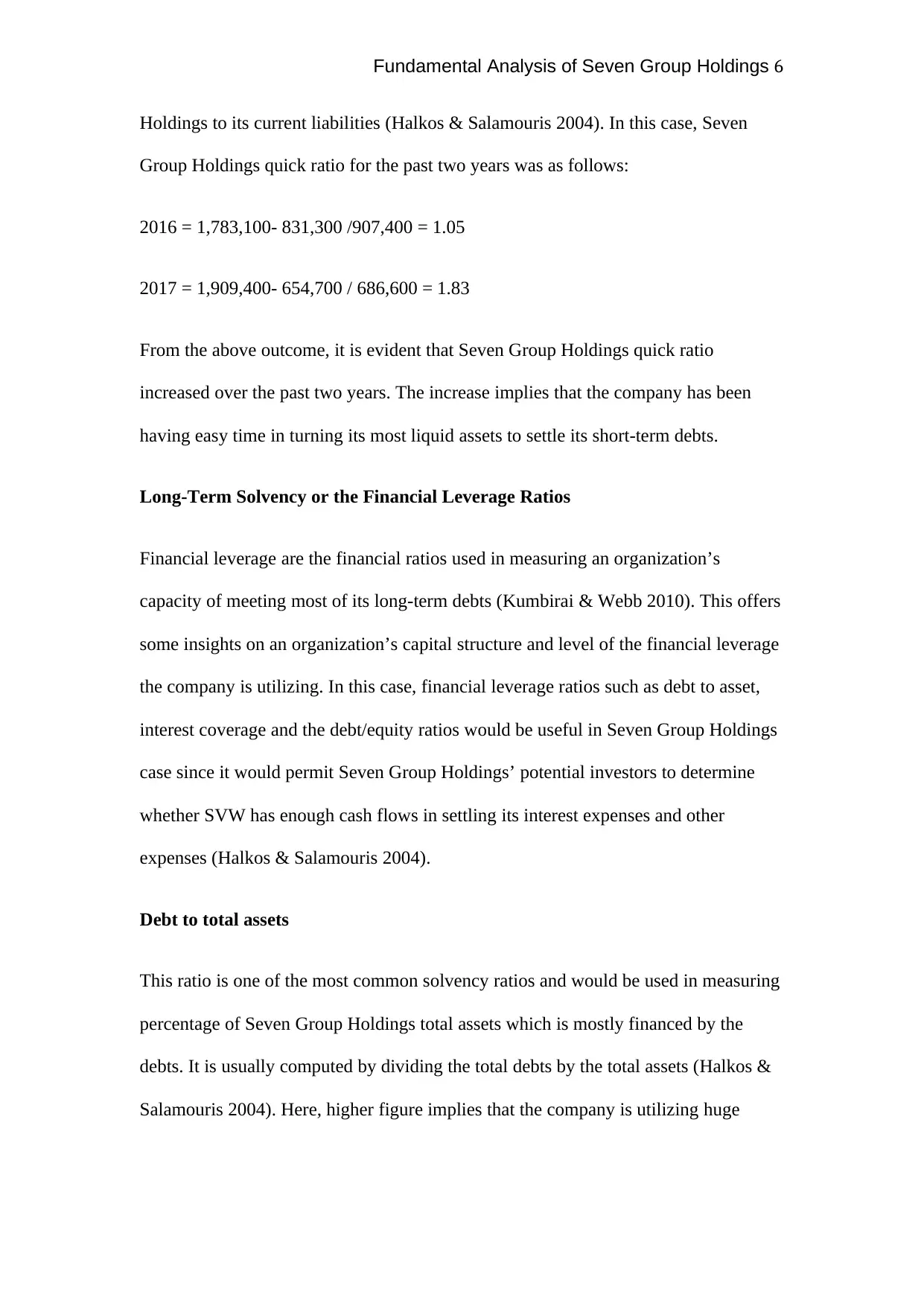

amount of the financial leverage that increases their financial risks. In this case, Seven

Group Holdings debt to assets ratio for the past two years was as follows:

2016 = 2,632,700/ 5,330,900 = 0.49

2017 = 2,410,800 / 4,836,000 = 0.50

Figure 2: trend in debt to assets 2016-2017

2016 2017

0.484

0.486

0.488

0.49

0.492

0.494

0.496

0.498

0.5

0.49

0.5

Detb to assets

Detb to assets

Based on the above results, it is evident that Seven Group Holdings debt to asset was

relatively low below 1. This means that Seven Group Holdings is utilizing

significantly low amount of the financial leverage which in turn lessen its financial

risks.

Debt to equity

The ratio would be used in measuring amount of the debt Seven Group Holdings

utilizes in comparison to amount of the equity used (White, Sondh & Fried 2005). In

this case, Seven Group Holdings debt to equity ratio for the past two years was as

follows:

amount of the financial leverage that increases their financial risks. In this case, Seven

Group Holdings debt to assets ratio for the past two years was as follows:

2016 = 2,632,700/ 5,330,900 = 0.49

2017 = 2,410,800 / 4,836,000 = 0.50

Figure 2: trend in debt to assets 2016-2017

2016 2017

0.484

0.486

0.488

0.49

0.492

0.494

0.496

0.498

0.5

0.49

0.5

Detb to assets

Detb to assets

Based on the above results, it is evident that Seven Group Holdings debt to asset was

relatively low below 1. This means that Seven Group Holdings is utilizing

significantly low amount of the financial leverage which in turn lessen its financial

risks.

Debt to equity

The ratio would be used in measuring amount of the debt Seven Group Holdings

utilizes in comparison to amount of the equity used (White, Sondh & Fried 2005). In

this case, Seven Group Holdings debt to equity ratio for the past two years was as

follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fundamental Analysis of Seven Group Holdings 8

2016 = 2,632,700/ 2,698,200 = 0.98

2017 = 2,410,800 / 2,425,200 = 0.99

As from the above computations, it is evident that Seven Group Holdings debt/equity

ratio decreased in the last two years. Besides, the ratio for the last two years was

below one meaning that Seven Group Holdings was relying on equity financing rather

than the debt financing.

Interest coverage

This ratio would help in measuring Seven Group Holdings cash flow generated in

comparison to the interest paid. It is computed by dividing the EBIT by the interest

expenses (White, Sondh & Fried 2005). In this case, Seven Group Holdings interest

coverage for the past two years was as follows:

2016 = 284,400/ 82,400 = 3.45

2017 = 124,600/ 77,300 = 1.61

Based on the aforementioned calculations, it is evident that Seven Group Holdings

interest coverage for the past two years decreased from 3.45 in 2016 to 1.61 in 2017.

The ratio was also relatively high meaning that the company was not experiencing

hard times in settling its interest expenses over the period.

Asset Utilization or Turnover Ratios

Asset utilization or efficiency ratios are mostly used in measuring how efficiently an

organization employs its assets (Kumbirai & Webb 2010). This offers potential

investors with a rough idea of overall operational performance of the company. In

2016 = 2,632,700/ 2,698,200 = 0.98

2017 = 2,410,800 / 2,425,200 = 0.99

As from the above computations, it is evident that Seven Group Holdings debt/equity

ratio decreased in the last two years. Besides, the ratio for the last two years was

below one meaning that Seven Group Holdings was relying on equity financing rather

than the debt financing.

Interest coverage

This ratio would help in measuring Seven Group Holdings cash flow generated in

comparison to the interest paid. It is computed by dividing the EBIT by the interest

expenses (White, Sondh & Fried 2005). In this case, Seven Group Holdings interest

coverage for the past two years was as follows:

2016 = 284,400/ 82,400 = 3.45

2017 = 124,600/ 77,300 = 1.61

Based on the aforementioned calculations, it is evident that Seven Group Holdings

interest coverage for the past two years decreased from 3.45 in 2016 to 1.61 in 2017.

The ratio was also relatively high meaning that the company was not experiencing

hard times in settling its interest expenses over the period.

Asset Utilization or Turnover Ratios

Asset utilization or efficiency ratios are mostly used in measuring how efficiently an

organization employs its assets (Kumbirai & Webb 2010). This offers potential

investors with a rough idea of overall operational performance of the company. In

Fundamental Analysis of Seven Group Holdings 9

essences, asset utilization or efficiency ratios would be useful in this case since they

will help in measuring rate at which Seven Group Holdings is turning its assets into

sales (White, Sondh & Fried 2005). In this case, inventory turnover, asset turnover

and receivable turnover would be used in measuring efficiency of Seven Group

Holdings over the past two years.

Inventory turnover

This ratio usually computed by dividing COGs by inventories would be useful in

determining how fast Seven Group Holdings turns its inventories or how faster the

company sells its inventories (Gapenski & Reiter 2008). A high turnover could means

that the firm’s inventories are too lean and the company might be unable to

correspond to the high demand (White, Sondh & Fried 2005). In this case, Seven

Group Holdings inventory turnover for the past two years was as follows:

2016 = 2,040,000 / (831,300 + 929,200)/2 = 2,040,000/ 1,760,500 = 1.16

2017 = 2,073, 100 / (654,700 + 831,300)/2 = 2,073,100 / 1,486,000 = 1.40

Based on the above computations, it is evident that Seven Group Holdings inventory

turnover increased over the period. The ratio was relatively low implying that Seven

Group Holdings inventories were less lean and that the firm was able to correspond or

to meet the relatively high demand.

Assets turnover

The ratio helps in measuring how efficiently or quickly Seven Group Holdings turns

its assets into revenue or sales (Gapenski & Reiter 2008). It is usually computed by

dividing sales by the average total assets. Where lesser asset turnover is said to imply

essences, asset utilization or efficiency ratios would be useful in this case since they

will help in measuring rate at which Seven Group Holdings is turning its assets into

sales (White, Sondh & Fried 2005). In this case, inventory turnover, asset turnover

and receivable turnover would be used in measuring efficiency of Seven Group

Holdings over the past two years.

Inventory turnover

This ratio usually computed by dividing COGs by inventories would be useful in

determining how fast Seven Group Holdings turns its inventories or how faster the

company sells its inventories (Gapenski & Reiter 2008). A high turnover could means

that the firm’s inventories are too lean and the company might be unable to

correspond to the high demand (White, Sondh & Fried 2005). In this case, Seven

Group Holdings inventory turnover for the past two years was as follows:

2016 = 2,040,000 / (831,300 + 929,200)/2 = 2,040,000/ 1,760,500 = 1.16

2017 = 2,073, 100 / (654,700 + 831,300)/2 = 2,073,100 / 1,486,000 = 1.40

Based on the above computations, it is evident that Seven Group Holdings inventory

turnover increased over the period. The ratio was relatively low implying that Seven

Group Holdings inventories were less lean and that the firm was able to correspond or

to meet the relatively high demand.

Assets turnover

The ratio helps in measuring how efficiently or quickly Seven Group Holdings turns

its assets into revenue or sales (Gapenski & Reiter 2008). It is usually computed by

dividing sales by the average total assets. Where lesser asset turnover is said to imply

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fundamental Analysis of Seven Group Holdings 10

that the company is inefficient in utilizing its assets. In this case, Seven Group

Holdings assets turnover for the past two years was as follows:

2016 = 2,418,700 / (5,330,900 + 5,372,900)/2 = 2,418,700/5,351,900 =0.45

2017 = 2,286,400 / (4,836,000 + 5,330,900)/2 = 2,286,400/ 5,083,450 = 0.45

The results above show that Seven Group Holdings asset turnover was relatively

constant over the past two years. In essence, given that the ratio was relatively low in

the past two years, this implies that Seven Group Holdings was inefficient in utilizing

its total assets to generate revenue.

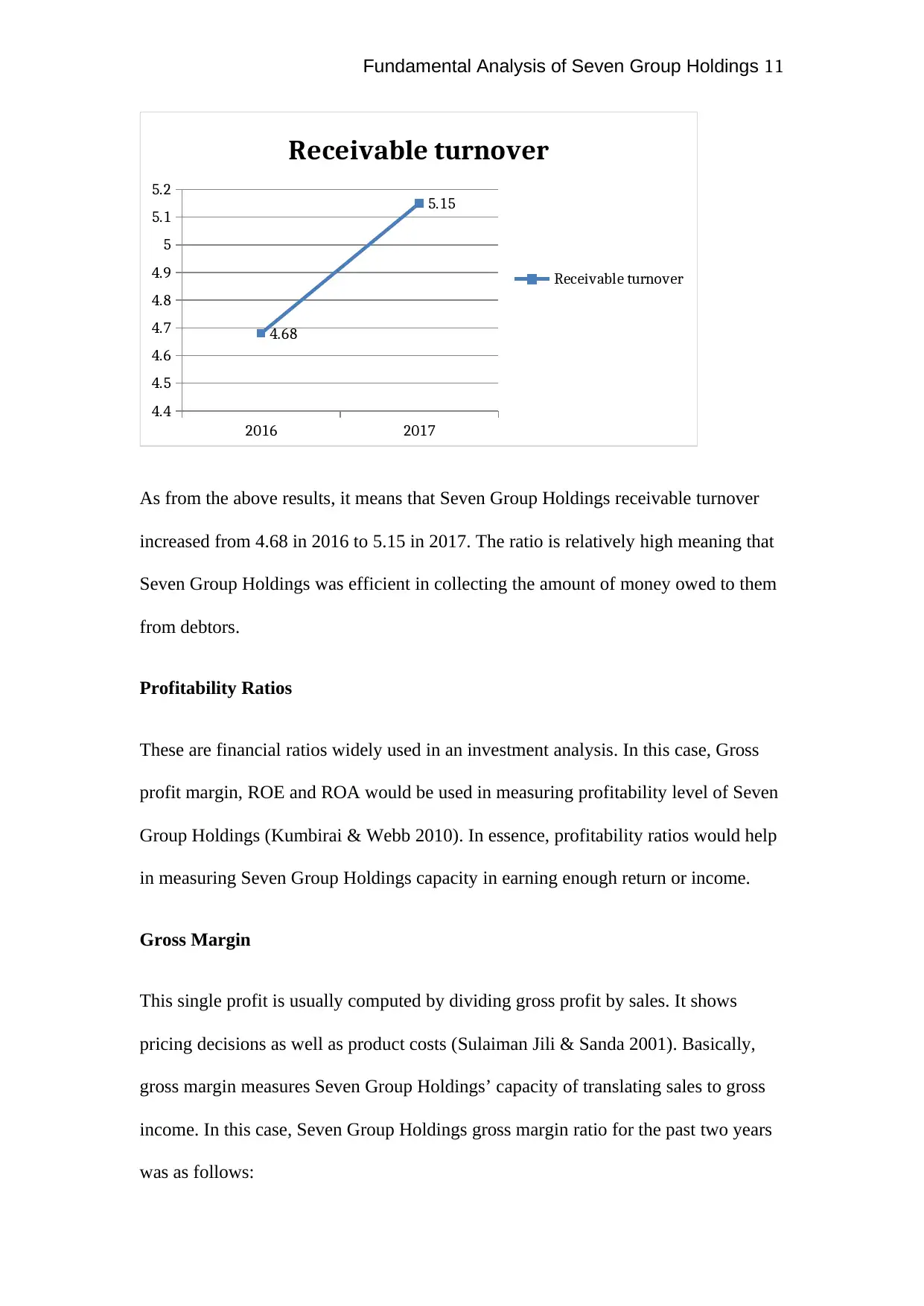

Receivable turnover

The ratio which is usually computed by dividing sales by the average receivables

would be used in measuring how efficiently and quickly Seven Group Holdings

collects most of its outstanding bills from debtors (Gapenski & Reiter 2008). In

essence, it would be used in measuring how many times Seven Group Holdings

collects money owed to them or turns into cash the account receivables (Kumbirai &

Webb 2010). In this case, Seven Group Holdings receivable turnover for the past two

years was as follows:

2016 = 2,418,700 / (551,300 + 482,100)/2 = 2,418,700/516,700 = 4.68 times

2017 = 2,286,400 / (336,500 + 551,300)/2 =2,286,400 /443,900 = 5.15 times

Figure 3: trend in receivable turnover 2016-2017

that the company is inefficient in utilizing its assets. In this case, Seven Group

Holdings assets turnover for the past two years was as follows:

2016 = 2,418,700 / (5,330,900 + 5,372,900)/2 = 2,418,700/5,351,900 =0.45

2017 = 2,286,400 / (4,836,000 + 5,330,900)/2 = 2,286,400/ 5,083,450 = 0.45

The results above show that Seven Group Holdings asset turnover was relatively

constant over the past two years. In essence, given that the ratio was relatively low in

the past two years, this implies that Seven Group Holdings was inefficient in utilizing

its total assets to generate revenue.

Receivable turnover

The ratio which is usually computed by dividing sales by the average receivables

would be used in measuring how efficiently and quickly Seven Group Holdings

collects most of its outstanding bills from debtors (Gapenski & Reiter 2008). In

essence, it would be used in measuring how many times Seven Group Holdings

collects money owed to them or turns into cash the account receivables (Kumbirai &

Webb 2010). In this case, Seven Group Holdings receivable turnover for the past two

years was as follows:

2016 = 2,418,700 / (551,300 + 482,100)/2 = 2,418,700/516,700 = 4.68 times

2017 = 2,286,400 / (336,500 + 551,300)/2 =2,286,400 /443,900 = 5.15 times

Figure 3: trend in receivable turnover 2016-2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fundamental Analysis of Seven Group Holdings 11

2016 2017

4.4

4.5

4.6

4.7

4.8

4.9

5

5.1

5.2

4.68

5.15

Receivable turnover

Receivable turnover

As from the above results, it means that Seven Group Holdings receivable turnover

increased from 4.68 in 2016 to 5.15 in 2017. The ratio is relatively high meaning that

Seven Group Holdings was efficient in collecting the amount of money owed to them

from debtors.

Profitability Ratios

These are financial ratios widely used in an investment analysis. In this case, Gross

profit margin, ROE and ROA would be used in measuring profitability level of Seven

Group Holdings (Kumbirai & Webb 2010). In essence, profitability ratios would help

in measuring Seven Group Holdings capacity in earning enough return or income.

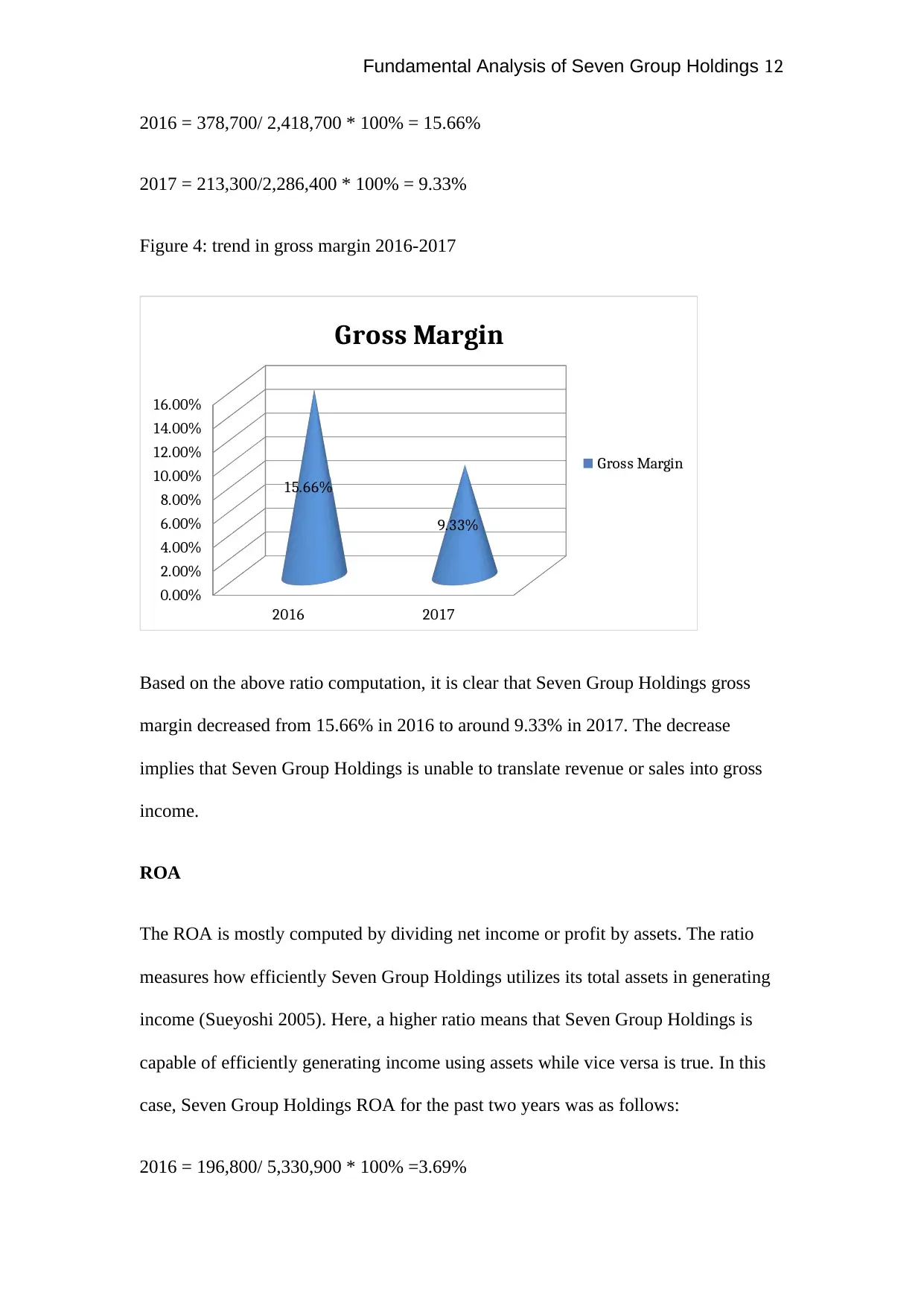

Gross Margin

This single profit is usually computed by dividing gross profit by sales. It shows

pricing decisions as well as product costs (Sulaiman Jili & Sanda 2001). Basically,

gross margin measures Seven Group Holdings’ capacity of translating sales to gross

income. In this case, Seven Group Holdings gross margin ratio for the past two years

was as follows:

2016 2017

4.4

4.5

4.6

4.7

4.8

4.9

5

5.1

5.2

4.68

5.15

Receivable turnover

Receivable turnover

As from the above results, it means that Seven Group Holdings receivable turnover

increased from 4.68 in 2016 to 5.15 in 2017. The ratio is relatively high meaning that

Seven Group Holdings was efficient in collecting the amount of money owed to them

from debtors.

Profitability Ratios

These are financial ratios widely used in an investment analysis. In this case, Gross

profit margin, ROE and ROA would be used in measuring profitability level of Seven

Group Holdings (Kumbirai & Webb 2010). In essence, profitability ratios would help

in measuring Seven Group Holdings capacity in earning enough return or income.

Gross Margin

This single profit is usually computed by dividing gross profit by sales. It shows

pricing decisions as well as product costs (Sulaiman Jili & Sanda 2001). Basically,

gross margin measures Seven Group Holdings’ capacity of translating sales to gross

income. In this case, Seven Group Holdings gross margin ratio for the past two years

was as follows:

Fundamental Analysis of Seven Group Holdings 12

2016 = 378,700/ 2,418,700 * 100% = 15.66%

2017 = 213,300/2,286,400 * 100% = 9.33%

Figure 4: trend in gross margin 2016-2017

2016 2017

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

15.66%

9.33%

Gross Margin

Gross Margin

Based on the above ratio computation, it is clear that Seven Group Holdings gross

margin decreased from 15.66% in 2016 to around 9.33% in 2017. The decrease

implies that Seven Group Holdings is unable to translate revenue or sales into gross

income.

ROA

The ROA is mostly computed by dividing net income or profit by assets. The ratio

measures how efficiently Seven Group Holdings utilizes its total assets in generating

income (Sueyoshi 2005). Here, a higher ratio means that Seven Group Holdings is

capable of efficiently generating income using assets while vice versa is true. In this

case, Seven Group Holdings ROA for the past two years was as follows:

2016 = 196,800/ 5,330,900 * 100% =3.69%

2016 = 378,700/ 2,418,700 * 100% = 15.66%

2017 = 213,300/2,286,400 * 100% = 9.33%

Figure 4: trend in gross margin 2016-2017

2016 2017

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

15.66%

9.33%

Gross Margin

Gross Margin

Based on the above ratio computation, it is clear that Seven Group Holdings gross

margin decreased from 15.66% in 2016 to around 9.33% in 2017. The decrease

implies that Seven Group Holdings is unable to translate revenue or sales into gross

income.

ROA

The ROA is mostly computed by dividing net income or profit by assets. The ratio

measures how efficiently Seven Group Holdings utilizes its total assets in generating

income (Sueyoshi 2005). Here, a higher ratio means that Seven Group Holdings is

capable of efficiently generating income using assets while vice versa is true. In this

case, Seven Group Holdings ROA for the past two years was as follows:

2016 = 196,800/ 5,330,900 * 100% =3.69%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.