Costing Methods Comparison: Traditional vs. ABC for Sewing Easy Ltd

VerifiedAdded on 2021/05/31

|9

|1031

|453

Homework Assignment

AI Summary

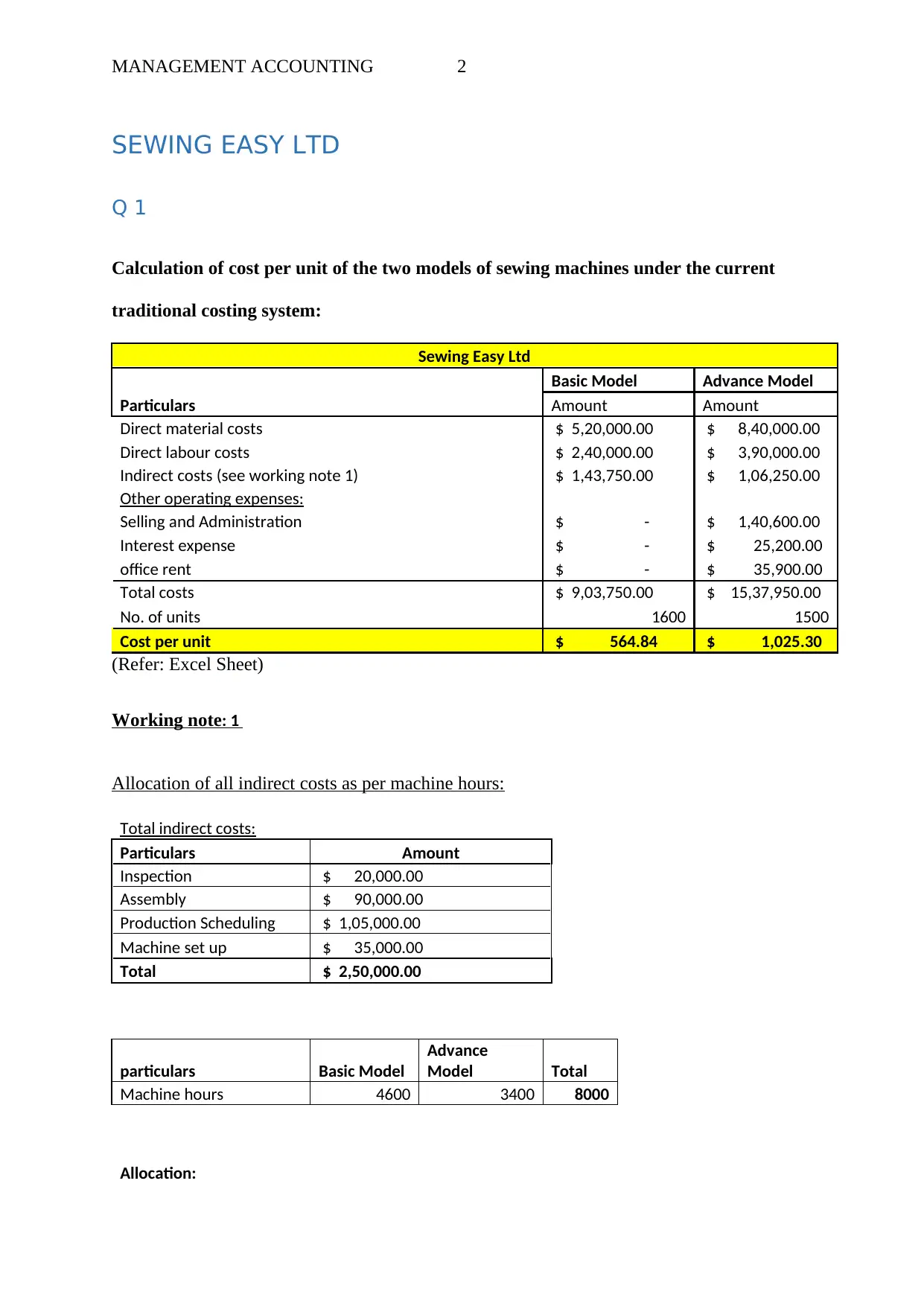

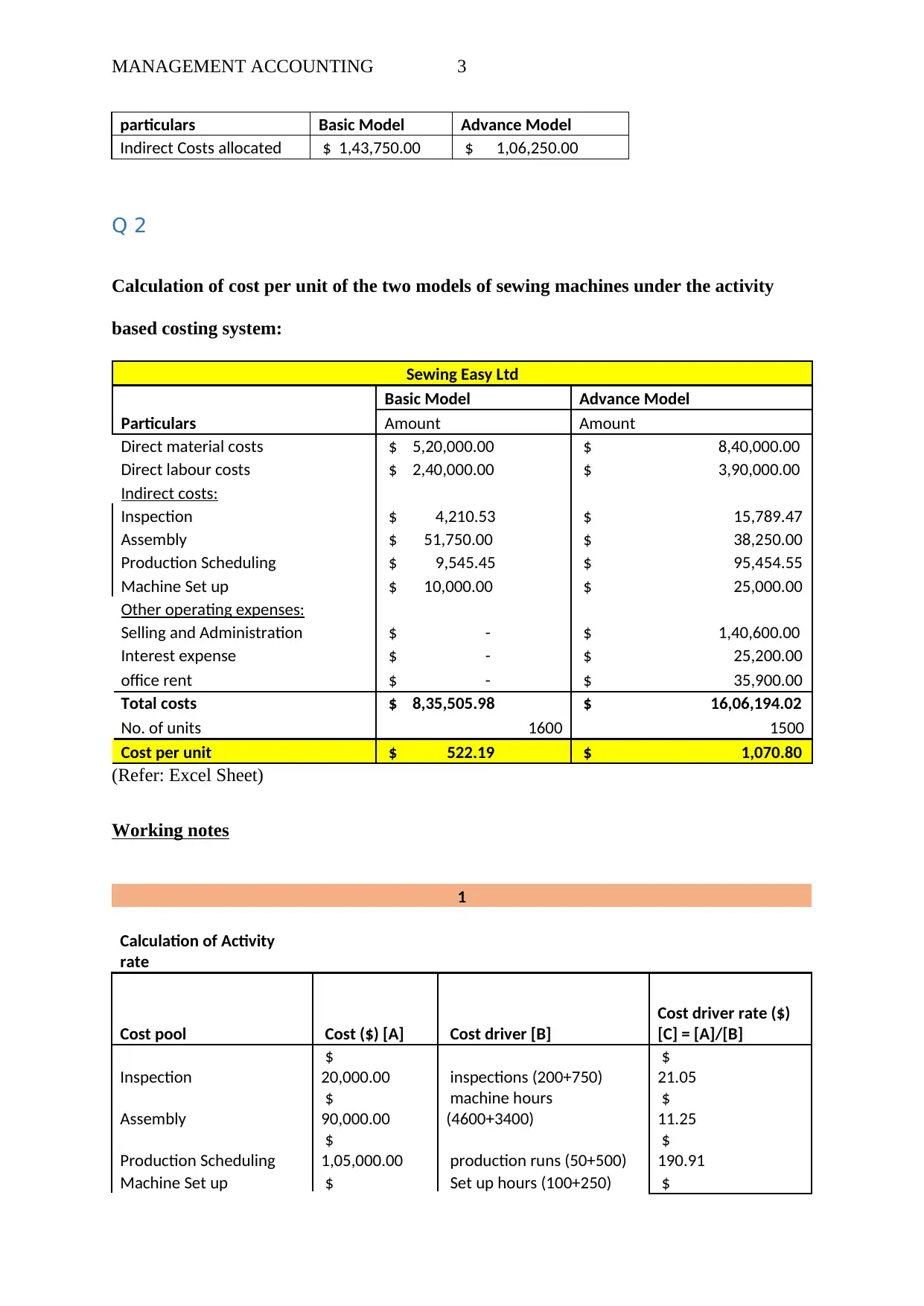

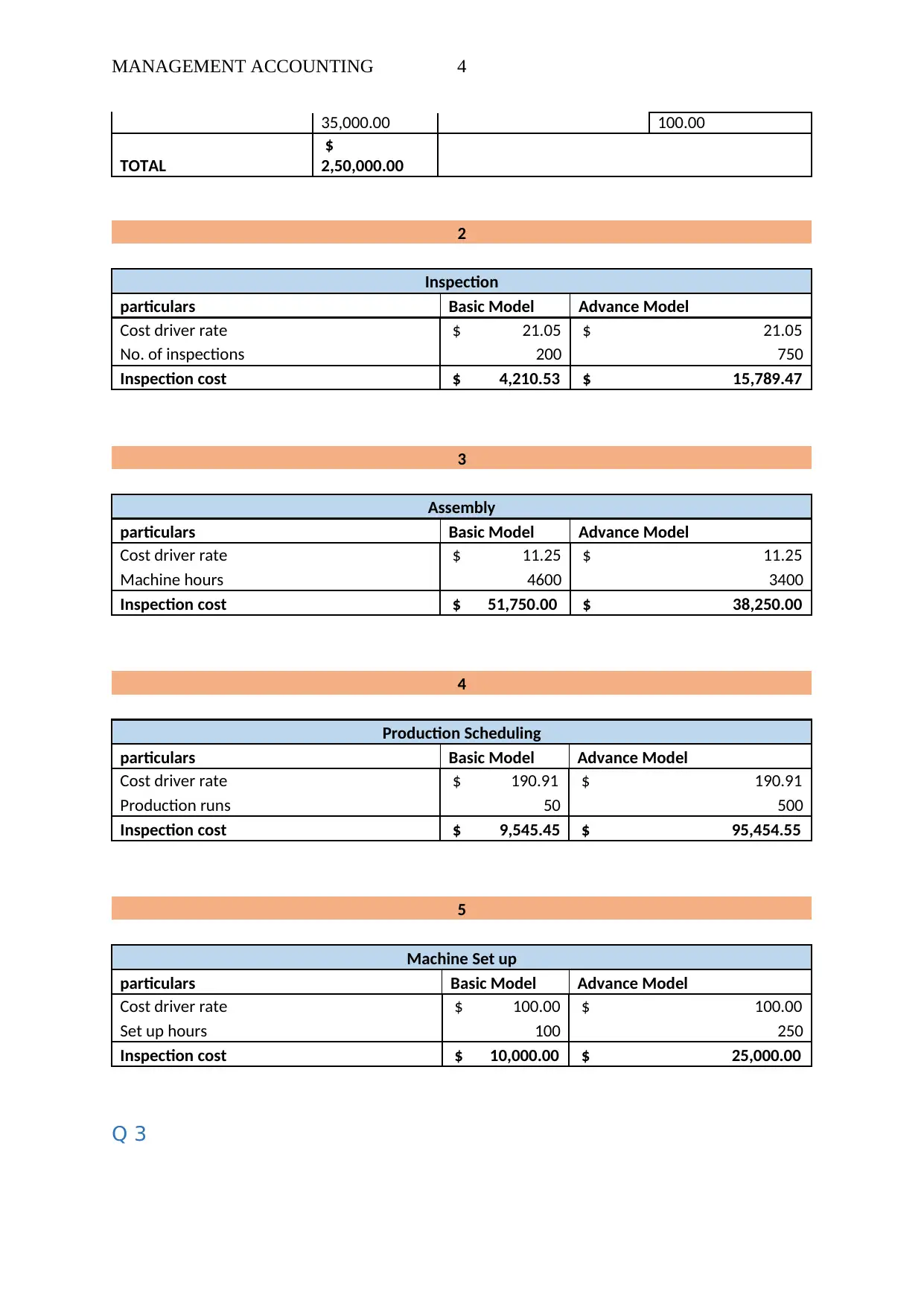

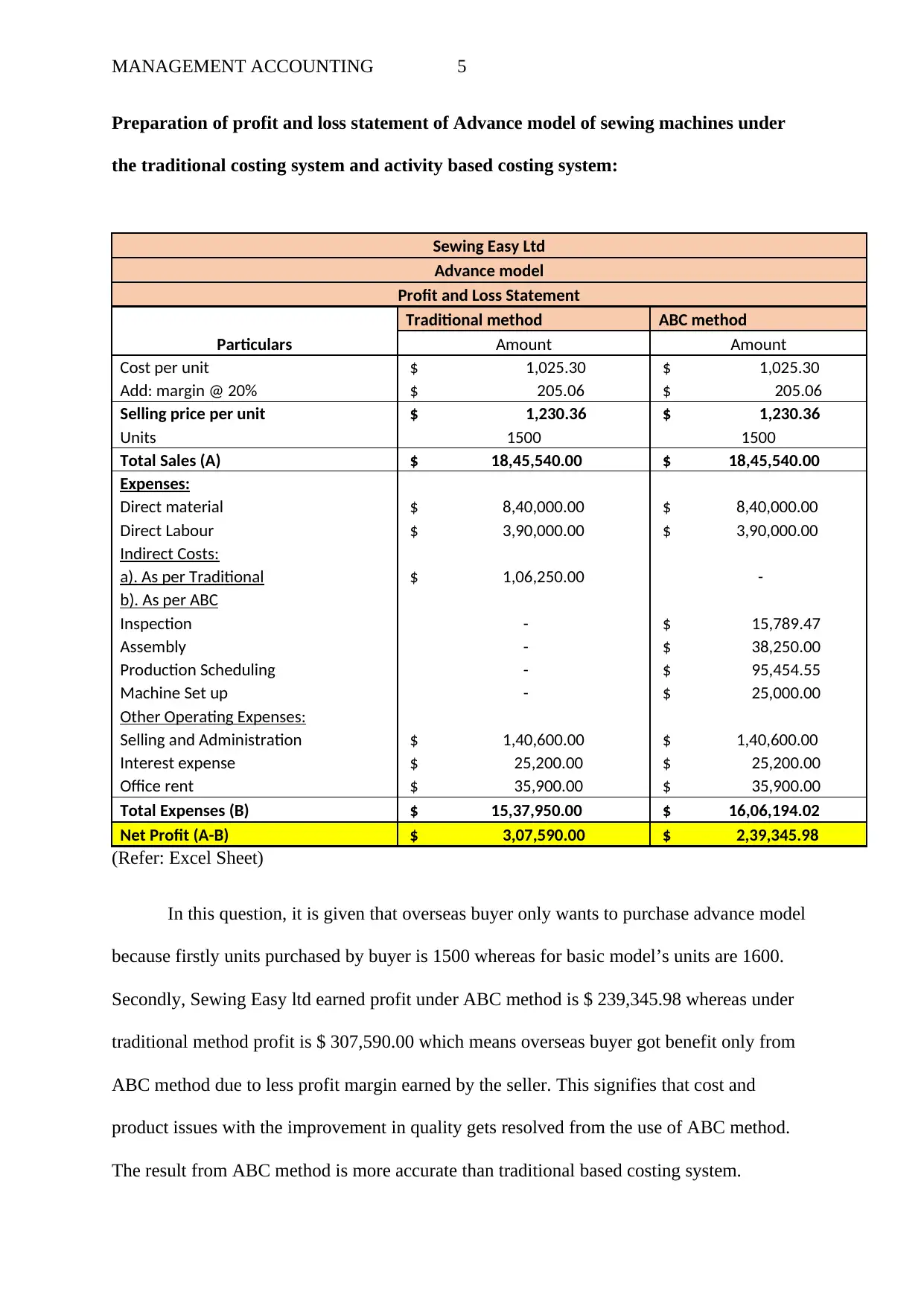

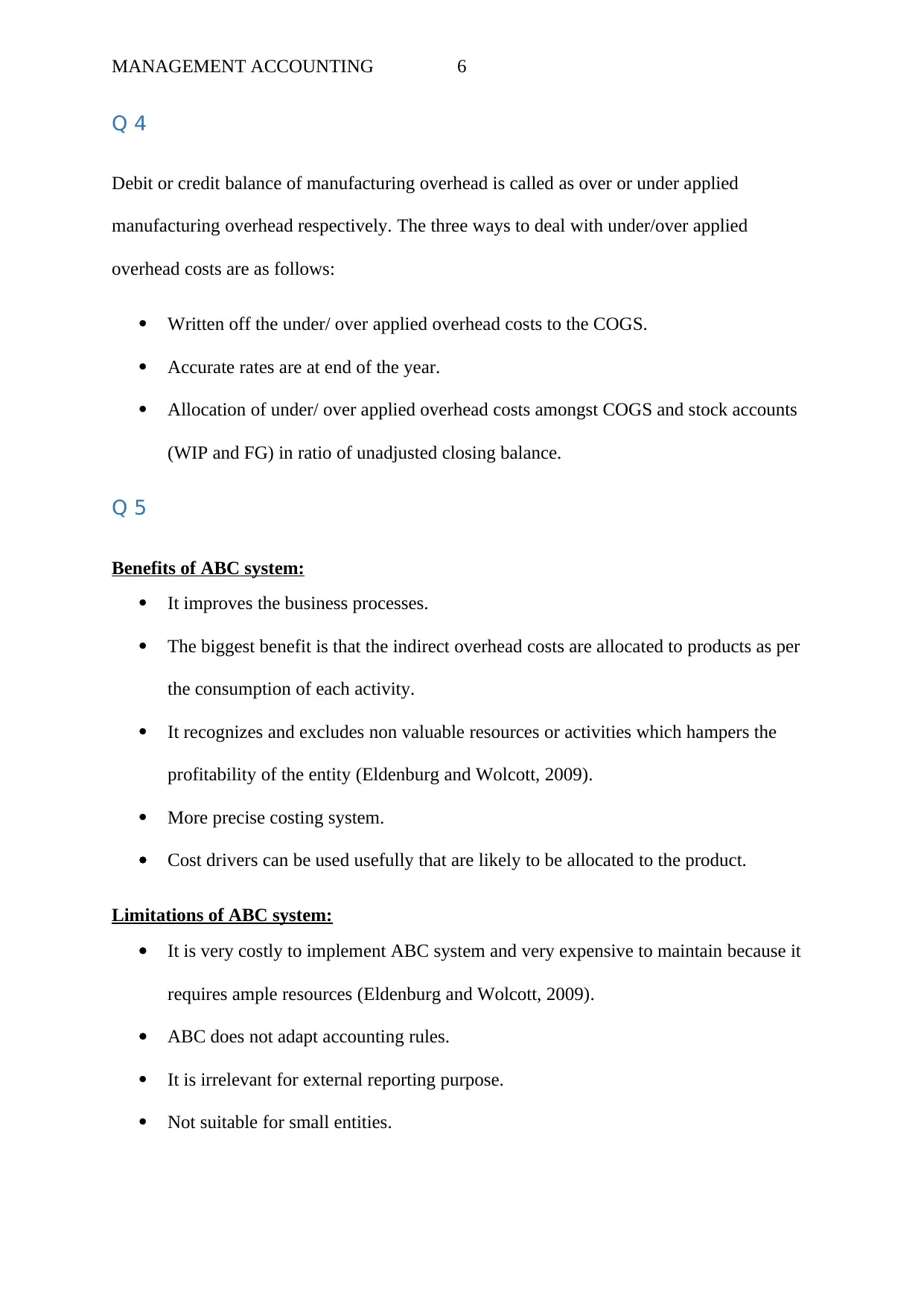

This assignment analyzes the costing methods of Sewing Easy Ltd, comparing traditional and activity-based costing (ABC) systems for two models of sewing machines. The solution begins by calculating the cost per unit for both models under the traditional costing system, followed by a similar calculation using ABC. The assignment then prepares profit and loss statements for the Advance model under both costing methods and discusses the implications of each. It further addresses the treatment of over/under applied manufacturing overhead, providing three methods for its handling. Finally, the assignment outlines the benefits and limitations of the ABC system, offering a comprehensive overview of its application in cost management. The analysis includes detailed calculations, working notes, and a comparison of the two costing approaches to determine the impact on profitability and decision-making.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.