Comprehensive Review: Sony Financial Holdings 2020 Report

VerifiedAdded on 2023/06/28

|100

|52138

|366

Report

AI Summary

This is Sony Financial Holdings Inc.'s 2020 Annual Report, covering the period from April 1, 2019, to March 31, 2020. The report includes a corporate overview with the mission, vision, and values, a company profile detailing its history, and profiles of group companies. It highlights the value creation story, financial and non-financial performance, and stock information. A message from the President & CEO sets the stage for a review of operations, including segments like Sony Financial Group, Sony Life, Sony Assurance, Sony Bank, and the Nursing Care Business. The report also delves into sustainability, corporate governance, human resources, and risk management. Detailed financial statements, segment information, and other financial data are provided, along with a glossary and editorial policy. The document emphasizes Sony Financial Group's commitment to innovation, customer satisfaction, and adapting to significant social and environmental changes.

2020Annual Report

April 1, 2019March 31, 2020

April 1, 2019March 31, 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

Mission, Vision & Values 1

History 2

Value Creation Story 4

Financial and Non-financial Highlights 8

Message from the President & CEO 10

Strategy and Review

Sony Financial Group 14

Sony Life 18

Sony Assurance 20

Sony Bank 22

Nursing Care Business 24

SFG’s Value Creation

Sustainability, Value Creation and Our

Foundation for Creating Value 26

Initiatives to Strengthen Our Foundation

for Creating Value 28

Corporate Section

Corporate Profile 50

Profiles of Group Companies

(Main subsidiaries) 51

Stock Information 52

Reference Materials

Review of Operations / Organizational Chart

of Business Operations 54

Financial Highlights 55

SFH Consolidated Financial Statements56

Significant Basic Items for the Preparation

of the Consolidated Financial Statements64

Notes to the Consolidated Financial

Statements 68

Segment Information 88

Other Financial Data 90

Relationship with Parent Company, Sony

Corp. 92

Glossary 93

Financial Data Book Contents 96

● The SFG refers to the financial group that comprises SFH, Sony Life,

Sony Assurance, Sony Bank, Sony Lifecare, Sony Financial Ventures, as

well as their subsidiaries and affiliates.

● Unless otherwise indicated, figures less than the indicated unit in this

material have been truncated, while ratios and percentage changes have

been rounded off.

● “Lifeplanner,” “LiPSS” and “Karte” are registered trademarks of Sony Life,

“GOOD DRIVE” is a registered trademark of Sony Assurance. Company

names and product names that appear in this report, other than those

mentioned above, are trademarks or registered trademarks of the

respective company.

● Fiscal 1996–fiscal 2020 represent the fiscal years ended / ending March

31, 1997–2021.

Company Name Abbreviations

The following abbreviations for company names are used in this report.

Sony Financial Group…………………………… SFG

Sony Financial Holdings Inc.…………………… SFH

Sony Life Insurance Co., Ltd. …………………… Sony Life

AEGON Sony Life Insurance Co., Ltd.………… AEGON Sony Life Insurance

SA Reinsurance Ltd. ……………………………… SA Reinsurance

Sony Life With Insurance Co.,Ltd. ……………… Sony Life With Insurance

Sony Life Business Partners Co., Ltd.………… Sony Life Business Partners

Sony Assurance Inc. ……………………………… Sony Assurance

Sony Bank Inc. …………………………………… Sony Bank

Sony Payment Services Inc.……………………… Sony Payment Services

SmartLink Network Hong Kong Limited ………… SmartLink Network Hong Kong

SmartLink Network Europe B.V. ………………… SmartLink Network Europe

Sony Lifecare Inc. ………………………………… Sony Lifecare

Lifecare Design Inc. ……………………………… Lifecare Design

Proud Life Inc.…………………………………… Proud Life

Sony Financial Ventures Inc.…………………… Sony Financial Ventures

Sony Corporation ………………………………… Sony Corp.

Disclaimer

This annual report contains statements concerning the current plans, expecta-

tions, strategies and beliefs of the SFG. Any statements contained herein that

are not historical facts are forward-looking statements or pro forma informa-

tion. Forward-looking statements may include—but are not limited to—words

such as “believe,” “anticipate,” “plan,” “strategy,” “expect,” “assume,” “fore-

cast,” “predict,” “propose,” “intend” and “possibility” that describe future

operating activities, business performance, events or conditions. For-

ward-looking statements, whether spoken or written, may also be included in

other materials released to the public. These forward-looking statements and

pro forma information are based on assumptions, decisions and judgments

made by the management of SFG companies, and are based on information

that is currently available to them. As such, they are subject to various risks

and uncertainties, and actual business results may vary substantially from the

forecasts expressed or implied in forward-looking statements. Consequently,

investors are cautioned not to place undue reliance on forward-looking

statements. SFG companies are under no obligation to revise forward-looking

statements or pro forma information in light of new information, future events

or other findings. The information contained in this annual report does not

constitute or form part of any offer for sale or subscription of or solicitation or

invitation of any offer to buy or subscribe to any securities, nor shall it or any

part of it form the basis of or be relied on in connection with any contract or

commitment whatsoever in Japan or abroad.

SFH refers to “Guidance for Collaborative Value

Creation” published by the Ministry of Economy,

Trade and Industry when organizing and examin-

ing matters to be listed in this report, in order to

make this report a starting point for dialogue with

shareholders and investors.

Editorial Policy

Mission, Vision & Values 1

History 2

Value Creation Story 4

Financial and Non-financial Highlights 8

Message from the President & CEO 10

Strategy and Review

Sony Financial Group 14

Sony Life 18

Sony Assurance 20

Sony Bank 22

Nursing Care Business 24

SFG’s Value Creation

Sustainability, Value Creation and Our

Foundation for Creating Value 26

Initiatives to Strengthen Our Foundation

for Creating Value 28

Corporate Section

Corporate Profile 50

Profiles of Group Companies

(Main subsidiaries) 51

Stock Information 52

Reference Materials

Review of Operations / Organizational Chart

of Business Operations 54

Financial Highlights 55

SFH Consolidated Financial Statements56

Significant Basic Items for the Preparation

of the Consolidated Financial Statements64

Notes to the Consolidated Financial

Statements 68

Segment Information 88

Other Financial Data 90

Relationship with Parent Company, Sony

Corp. 92

Glossary 93

Financial Data Book Contents 96

● The SFG refers to the financial group that comprises SFH, Sony Life,

Sony Assurance, Sony Bank, Sony Lifecare, Sony Financial Ventures, as

well as their subsidiaries and affiliates.

● Unless otherwise indicated, figures less than the indicated unit in this

material have been truncated, while ratios and percentage changes have

been rounded off.

● “Lifeplanner,” “LiPSS” and “Karte” are registered trademarks of Sony Life,

“GOOD DRIVE” is a registered trademark of Sony Assurance. Company

names and product names that appear in this report, other than those

mentioned above, are trademarks or registered trademarks of the

respective company.

● Fiscal 1996–fiscal 2020 represent the fiscal years ended / ending March

31, 1997–2021.

Company Name Abbreviations

The following abbreviations for company names are used in this report.

Sony Financial Group…………………………… SFG

Sony Financial Holdings Inc.…………………… SFH

Sony Life Insurance Co., Ltd. …………………… Sony Life

AEGON Sony Life Insurance Co., Ltd.………… AEGON Sony Life Insurance

SA Reinsurance Ltd. ……………………………… SA Reinsurance

Sony Life With Insurance Co.,Ltd. ……………… Sony Life With Insurance

Sony Life Business Partners Co., Ltd.………… Sony Life Business Partners

Sony Assurance Inc. ……………………………… Sony Assurance

Sony Bank Inc. …………………………………… Sony Bank

Sony Payment Services Inc.……………………… Sony Payment Services

SmartLink Network Hong Kong Limited ………… SmartLink Network Hong Kong

SmartLink Network Europe B.V. ………………… SmartLink Network Europe

Sony Lifecare Inc. ………………………………… Sony Lifecare

Lifecare Design Inc. ……………………………… Lifecare Design

Proud Life Inc.…………………………………… Proud Life

Sony Financial Ventures Inc.…………………… Sony Financial Ventures

Sony Corporation ………………………………… Sony Corp.

Disclaimer

This annual report contains statements concerning the current plans, expecta-

tions, strategies and beliefs of the SFG. Any statements contained herein that

are not historical facts are forward-looking statements or pro forma informa-

tion. Forward-looking statements may include—but are not limited to—words

such as “believe,” “anticipate,” “plan,” “strategy,” “expect,” “assume,” “fore-

cast,” “predict,” “propose,” “intend” and “possibility” that describe future

operating activities, business performance, events or conditions. For-

ward-looking statements, whether spoken or written, may also be included in

other materials released to the public. These forward-looking statements and

pro forma information are based on assumptions, decisions and judgments

made by the management of SFG companies, and are based on information

that is currently available to them. As such, they are subject to various risks

and uncertainties, and actual business results may vary substantially from the

forecasts expressed or implied in forward-looking statements. Consequently,

investors are cautioned not to place undue reliance on forward-looking

statements. SFG companies are under no obligation to revise forward-looking

statements or pro forma information in light of new information, future events

or other findings. The information contained in this annual report does not

constitute or form part of any offer for sale or subscription of or solicitation or

invitation of any offer to buy or subscribe to any securities, nor shall it or any

part of it form the basis of or be relied on in connection with any contract or

commitment whatsoever in Japan or abroad.

SFH refers to “Guidance for Collaborative Value

Creation” published by the Ministry of Economy,

Trade and Industry when organizing and examin-

ing matters to be listed in this report, in order to

make this report a starting point for dialogue with

shareholders and investors.

Editorial Policy

Sony Financial Holdings Inc.Annual Report2020 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

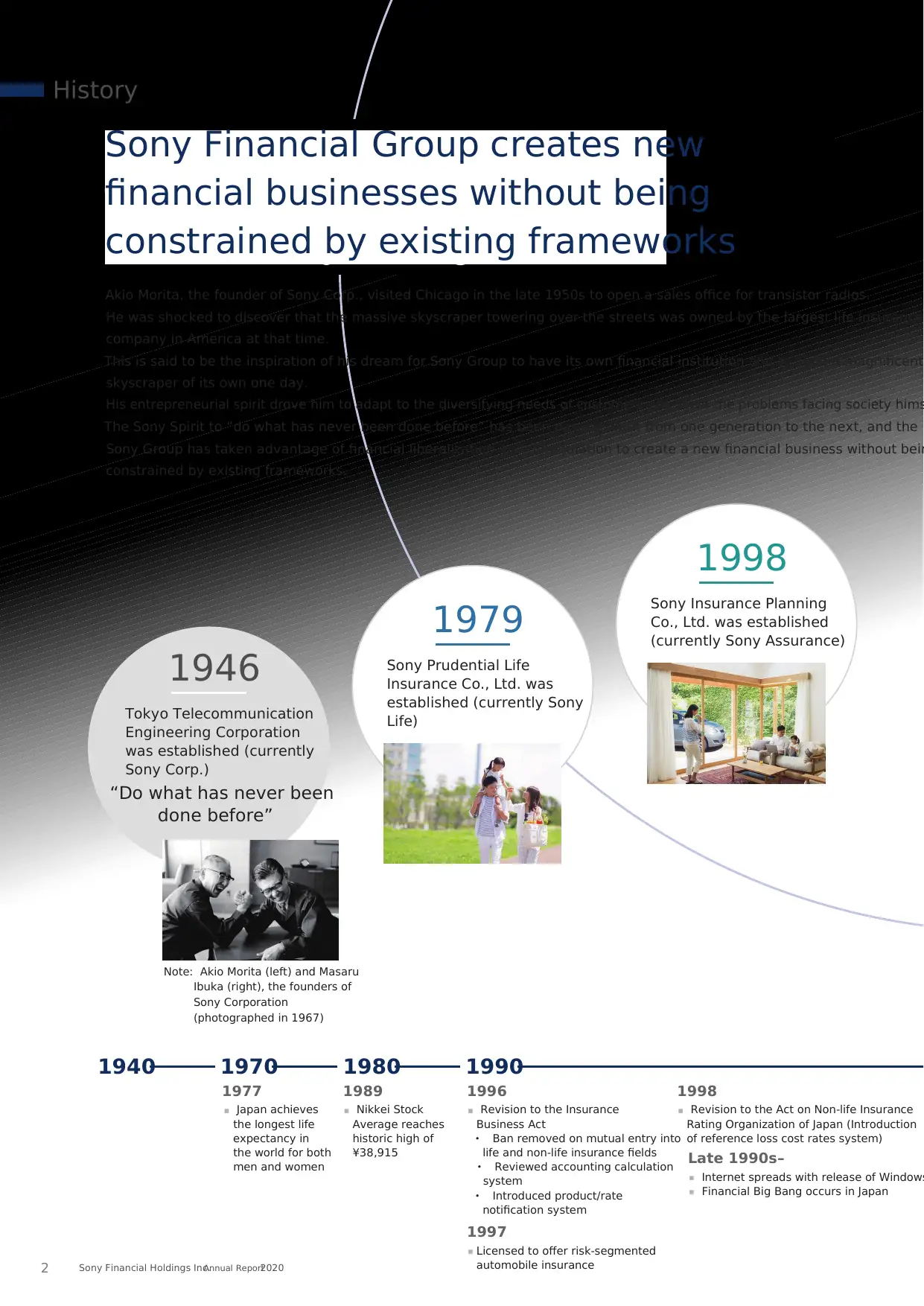

1946

Tokyo Telecommunication

Engineering Corporation

was established (currently

Sony Corp.)

1979

Sony Prudential Life

Insurance Co., Ltd. was

established (currently Sony

Life)

1998

Sony Insurance Planning

Co., Ltd. was established

(currently Sony Assurance)

“Do what has never been

done before”

Note: Akio Morita (left) and Masaru

Ibuka (right), the founders of

Sony Corporation

(photographed in 1967)

1989

■ Nikkei Stock

Average reaches

historic high of

¥38,915

1997

■ Licensed to offer risk-segmented

automobile insurance

Late 1990s–

■ Internet spreads with release of Windows

■ Financial Big Bang occurs in Japan

1998

■ Revision to the Act on Non-life Insurance

Rating Organization of Japan (Introduction

of reference loss cost rates system)

1977

■ Japan achieves

the longest life

expectancy in

the world for both

men and women

Akio Morita, the founder of Sony Corp., visited Chicago in the late 1950s to open a sales office for transistor radios.

He was shocked to discover that the massive skyscraper towering over the streets was owned by the largest life insurance

company in America at that time.

This is said to be the inspiration of his dream for Sony Group to have its own financial institution and to build a magnificent

skyscraper of its own one day.

His entrepreneurial spirit drove him to adapt to the diversifying needs of customers and solve the problems facing society hims

The Sony Spirit to “do what has never been done before” has been passed down from one generation to the next, and the

Sony Group has taken advantage of financial liberalization and deregulation to create a new financial business without bein

constrained by existing frameworks.

Sony Financial Group creates new

financial businesses without being

constrained by existing frameworks

1940 1970 1980

1996

■ Revision to the Insurance

Business Act

・ Ban removed on mutual entry into

life and non-life insurance fields

・ Reviewed accounting calculation

system

・ Introduced product/rate

notification system

1990

History

Sony Financial Holdings Inc.Annual Report20202

Tokyo Telecommunication

Engineering Corporation

was established (currently

Sony Corp.)

1979

Sony Prudential Life

Insurance Co., Ltd. was

established (currently Sony

Life)

1998

Sony Insurance Planning

Co., Ltd. was established

(currently Sony Assurance)

“Do what has never been

done before”

Note: Akio Morita (left) and Masaru

Ibuka (right), the founders of

Sony Corporation

(photographed in 1967)

1989

■ Nikkei Stock

Average reaches

historic high of

¥38,915

1997

■ Licensed to offer risk-segmented

automobile insurance

Late 1990s–

■ Internet spreads with release of Windows

■ Financial Big Bang occurs in Japan

1998

■ Revision to the Act on Non-life Insurance

Rating Organization of Japan (Introduction

of reference loss cost rates system)

1977

■ Japan achieves

the longest life

expectancy in

the world for both

men and women

Akio Morita, the founder of Sony Corp., visited Chicago in the late 1950s to open a sales office for transistor radios.

He was shocked to discover that the massive skyscraper towering over the streets was owned by the largest life insurance

company in America at that time.

This is said to be the inspiration of his dream for Sony Group to have its own financial institution and to build a magnificent

skyscraper of its own one day.

His entrepreneurial spirit drove him to adapt to the diversifying needs of customers and solve the problems facing society hims

The Sony Spirit to “do what has never been done before” has been passed down from one generation to the next, and the

Sony Group has taken advantage of financial liberalization and deregulation to create a new financial business without bein

constrained by existing frameworks.

Sony Financial Group creates new

financial businesses without being

constrained by existing frameworks

1940 1970 1980

1996

■ Revision to the Insurance

Business Act

・ Ban removed on mutual entry into

life and non-life insurance fields

・ Reviewed accounting calculation

system

・ Introduced product/rate

notification system

1990

History

Sony Financial Holdings Inc.Annual Report20202

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018

Sony Financial Ventures

was established

2014

Sony Lifecare was established

2001

Sony Bank was established

Become the most trusted financial

services group by invoking emotion

through the power of technology

and high-value-added products

and services that meet every

customer’s needs

2004

SFH was established

(2007 SFH was listed on the First Section of

Tokyo Stock Exchange)

2001

■ Removal of ban on sales of insurance

products at banks

■ Revision to the Banking Act (removal of

ban on companies from other industries

entering the banking industry)

2000

■ Enactment of the nursing care

insurance system

■ Removal of ban on companies

from other industries entering

the banking industry

2007

■ Enactment of the Financial

Instruments and Exchange Act

2008

■ Collapse of Lehman Brothers

2010

■ Enactment of the

Insurance Act

2016

■ Introduction of negative interest

rates

■ Full enactment of revisions to

the Insurance Business Act

・ Comparative recommendation

regulations

・ Fulfillment of obligation to

grasp intentions

2011

■ Occurrence of the Great

East Japan Earthquake

2012

■ Economic policies enacted

by the second Abe

administration (Abenomics)

2000 2010

The logo used by the Sony Financial Group, uses the “S” in “Sony” as a motif.

Combining Sony blue 90, the corporate color of Sony Corporation, to represent

our origin, with green, which invokes the image of “safety” required of finance

businesses, the logo expresses:

1. “Innovation” that overturns the image of existing finance businesses;

2. “Intelligence” that invokes new business models; and

3. “Speed” to respond to the digital network society.

The Origin of Our Corporate Logo

Corporate

Logo

Sony Financial Holdings Inc.Annual Report2020 3

Sony Financial Ventures

was established

2014

Sony Lifecare was established

2001

Sony Bank was established

Become the most trusted financial

services group by invoking emotion

through the power of technology

and high-value-added products

and services that meet every

customer’s needs

2004

SFH was established

(2007 SFH was listed on the First Section of

Tokyo Stock Exchange)

2001

■ Removal of ban on sales of insurance

products at banks

■ Revision to the Banking Act (removal of

ban on companies from other industries

entering the banking industry)

2000

■ Enactment of the nursing care

insurance system

■ Removal of ban on companies

from other industries entering

the banking industry

2007

■ Enactment of the Financial

Instruments and Exchange Act

2008

■ Collapse of Lehman Brothers

2010

■ Enactment of the

Insurance Act

2016

■ Introduction of negative interest

rates

■ Full enactment of revisions to

the Insurance Business Act

・ Comparative recommendation

regulations

・ Fulfillment of obligation to

grasp intentions

2011

■ Occurrence of the Great

East Japan Earthquake

2012

■ Economic policies enacted

by the second Abe

administration (Abenomics)

2000 2010

The logo used by the Sony Financial Group, uses the “S” in “Sony” as a motif.

Combining Sony blue 90, the corporate color of Sony Corporation, to represent

our origin, with green, which invokes the image of “safety” required of finance

businesses, the logo expresses:

1. “Innovation” that overturns the image of existing finance businesses;

2. “Intelligence” that invokes new business models; and

3. “Speed” to respond to the digital network society.

The Origin of Our Corporate Logo

Corporate

Logo

Sony Financial Holdings Inc.Annual Report2020 3

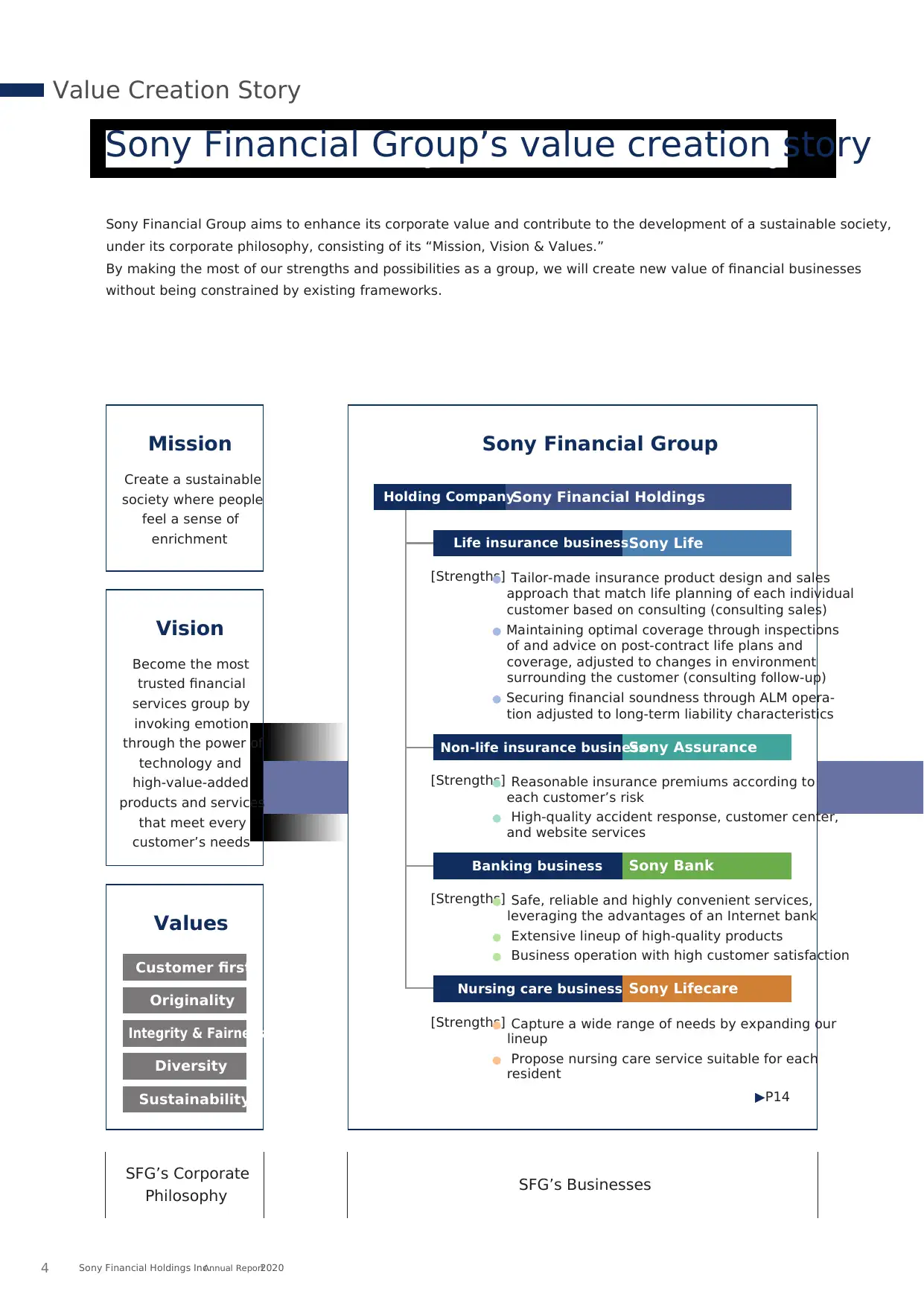

SFG’s Corporate

Philosophy SFG’s Businesses

Sony Financial Group aims to enhance its corporate value and contribute to the development of a sustainable society,

under its corporate philosophy, consisting of its “Mission, Vision & Values.”

By making the most of our strengths and possibilities as a group, we will create new value of financial businesses

without being constrained by existing frameworks.

Sony Financial Group’s value creation story

Vision

Become the most

trusted financial

services group by

invoking emotion

through the power of

technology and

high-value-added

products and services

that meet every

customer’s needs

Mission

Create a sustainable

society where people

feel a sense of

enrichment

Values

Customer first

Originality

Integrity & Fairness

Diversity

Sustainability

Sony Financial Group

Sony Financial HoldingsHolding Company

▶P14

Sony LifecareNursing care business

[Strengths]● Capture a wide range of needs by expanding our

lineup

● Propose nursing care service suitable for each

resident

Sony LifeLife insurance business

[Strengths]● Tailor-made insurance product design and sales

approach that match life planning of each individual

customer based on consulting (consulting sales)

● Maintaining optimal coverage through inspections

of and advice on post-contract life plans and

coverage, adjusted to changes in environment

surrounding the customer (consulting follow-up)

● Securing financial soundness through ALM opera-

tion adjusted to long-term liability characteristics

[Strengths]● Reasonable insurance premiums according to

each customer’s risk

● High-quality accident response, customer center,

and website services

Sony AssuranceNon-life insurance business

[Strengths]● Safe, reliable and highly convenient services,

leveraging the advantages of an Internet bank

● Extensive lineup of high-quality products

● Business operation with high customer satisfaction

Sony BankBanking business

Value Creation Story

Sony Financial Holdings Inc.Annual Report20204

Philosophy SFG’s Businesses

Sony Financial Group aims to enhance its corporate value and contribute to the development of a sustainable society,

under its corporate philosophy, consisting of its “Mission, Vision & Values.”

By making the most of our strengths and possibilities as a group, we will create new value of financial businesses

without being constrained by existing frameworks.

Sony Financial Group’s value creation story

Vision

Become the most

trusted financial

services group by

invoking emotion

through the power of

technology and

high-value-added

products and services

that meet every

customer’s needs

Mission

Create a sustainable

society where people

feel a sense of

enrichment

Values

Customer first

Originality

Integrity & Fairness

Diversity

Sustainability

Sony Financial Group

Sony Financial HoldingsHolding Company

▶P14

Sony LifecareNursing care business

[Strengths]● Capture a wide range of needs by expanding our

lineup

● Propose nursing care service suitable for each

resident

Sony LifeLife insurance business

[Strengths]● Tailor-made insurance product design and sales

approach that match life planning of each individual

customer based on consulting (consulting sales)

● Maintaining optimal coverage through inspections

of and advice on post-contract life plans and

coverage, adjusted to changes in environment

surrounding the customer (consulting follow-up)

● Securing financial soundness through ALM opera-

tion adjusted to long-term liability characteristics

[Strengths]● Reasonable insurance premiums according to

each customer’s risk

● High-quality accident response, customer center,

and website services

Sony AssuranceNon-life insurance business

[Strengths]● Safe, reliable and highly convenient services,

leveraging the advantages of an Internet bank

● Extensive lineup of high-quality products

● Business operation with high customer satisfaction

Sony BankBanking business

Value Creation Story

Sony Financial Holdings Inc.Annual Report20204

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

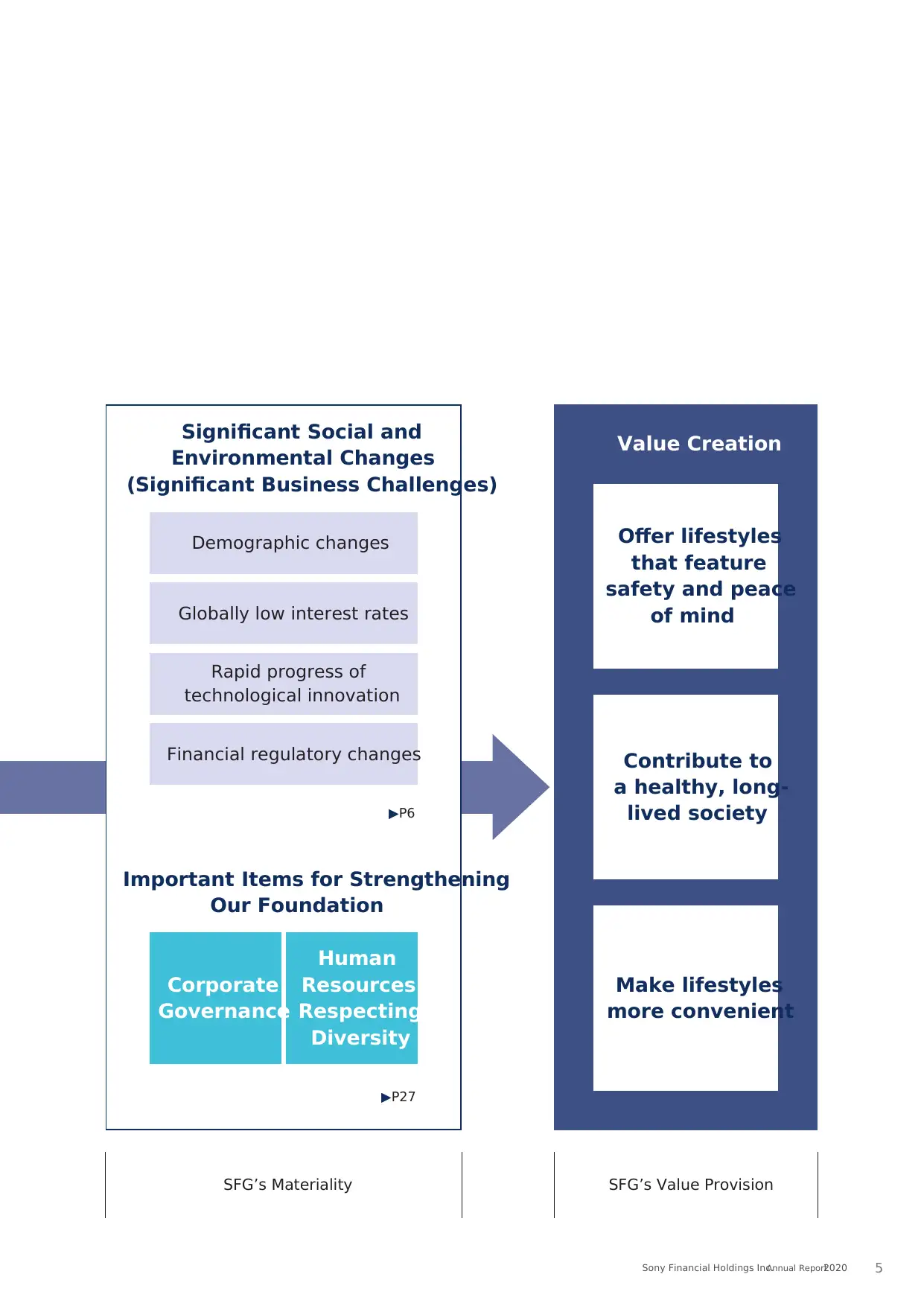

SFG’s Materiality SFG’s Value Provision

Significant Social and

Environmental Changes

(Significant Business Challenges)

Value Creation

Make lifestyles

more convenient

Offer lifestyles

that feature

safety and peace

of mind

Contribute to

a healthy, long-

lived society

▶P27

Corporate

Governance

Human

Resources

Respecting

Diversity

Important Items for Strengthening

Our Foundation

▶P6

Demographic changes

Globally low interest rates

Rapid progress of

technological innovation

Financial regulatory changes

Sony Financial Holdings Inc.Annual Report2020 5

Significant Social and

Environmental Changes

(Significant Business Challenges)

Value Creation

Make lifestyles

more convenient

Offer lifestyles

that feature

safety and peace

of mind

Contribute to

a healthy, long-

lived society

▶P27

Corporate

Governance

Human

Resources

Respecting

Diversity

Important Items for Strengthening

Our Foundation

▶P6

Demographic changes

Globally low interest rates

Rapid progress of

technological innovation

Financial regulatory changes

Sony Financial Holdings Inc.Annual Report2020 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

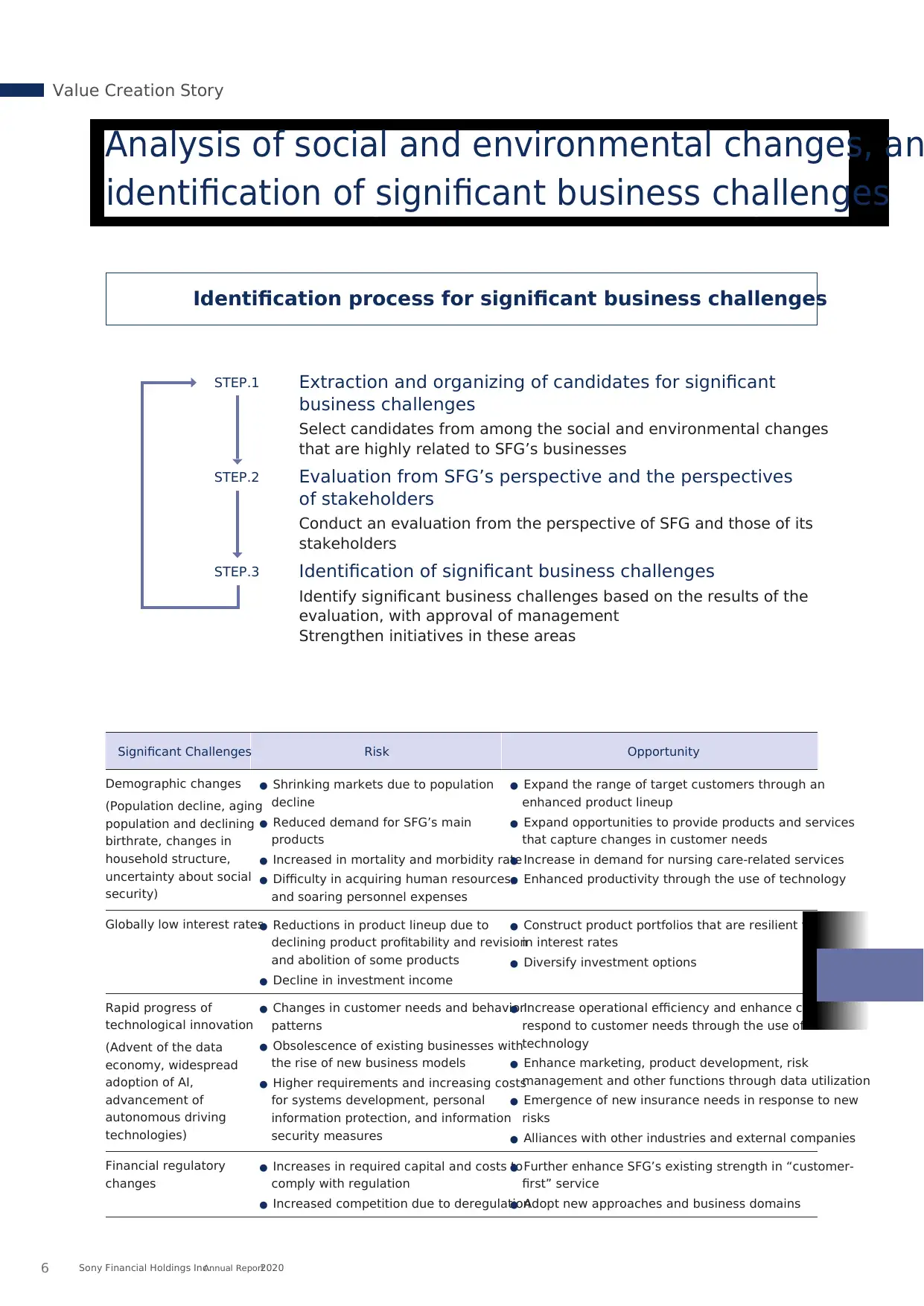

Significant Challenges Risk Opportunity

Demographic changes

(Population decline, aging

population and declining

birthrate, changes in

household structure,

uncertainty about social

security)

● Shrinking markets due to population

decline

● Reduced demand for SFG’s main

products

● Increased in mortality and morbidity rate

● Difficulty in acquiring human resources,

and soaring personnel expenses

● Expand the range of target customers through an

enhanced product lineup

● Expand opportunities to provide products and services

that capture changes in customer needs

● Increase in demand for nursing care-related services

● Enhanced productivity through the use of technology

Globally low interest rates● Reductions in product lineup due to

declining product profitability and revision

and abolition of some products

● Decline in investment income

● Construct product portfolios that are resilient to changes

in interest rates

● Diversify investment options

Rapid progress of

technological innovation

(Advent of the data

economy, widespread

adoption of AI,

advancement of

autonomous driving

technologies)

● Changes in customer needs and behavior

patterns

● Obsolescence of existing businesses with

the rise of new business models

● Higher requirements and increasing costs

for systems development, personal

information protection, and information

security measures

● Increase operational efficiency and enhance capacity to

respond to customer needs through the use of

technology

● Enhance marketing, product development, risk

management and other functions through data utilization

● Emergence of new insurance needs in response to new

risks

● Alliances with other industries and external companies

Financial regulatory

changes

● Increases in required capital and costs to

comply with regulation

● Increased competition due to deregulation

● Further enhance SFG’s existing strength in “customer-

first” service

● Adopt new approaches and business domains

Analysis of social and environmental changes, an

identification of significant business challenges

STEP.2

STEP.3

STEP.1

Evaluation from SFG’s perspective and the perspectives

of stakeholders

Conduct an evaluation from the perspective of SFG and those of its

stakeholders

Identification of significant business challenges

Identify significant business challenges based on the results of the

evaluation, with approval of management

Strengthen initiatives in these areas

Extraction and organizing of candidates for significant

business challenges

Select candidates from among the social and environmental changes

that are highly related to SFG’s businesses

Identification process for significant business challenges

Value Creation Story

Sony Financial Holdings Inc.Annual Report20206

Demographic changes

(Population decline, aging

population and declining

birthrate, changes in

household structure,

uncertainty about social

security)

● Shrinking markets due to population

decline

● Reduced demand for SFG’s main

products

● Increased in mortality and morbidity rate

● Difficulty in acquiring human resources,

and soaring personnel expenses

● Expand the range of target customers through an

enhanced product lineup

● Expand opportunities to provide products and services

that capture changes in customer needs

● Increase in demand for nursing care-related services

● Enhanced productivity through the use of technology

Globally low interest rates● Reductions in product lineup due to

declining product profitability and revision

and abolition of some products

● Decline in investment income

● Construct product portfolios that are resilient to changes

in interest rates

● Diversify investment options

Rapid progress of

technological innovation

(Advent of the data

economy, widespread

adoption of AI,

advancement of

autonomous driving

technologies)

● Changes in customer needs and behavior

patterns

● Obsolescence of existing businesses with

the rise of new business models

● Higher requirements and increasing costs

for systems development, personal

information protection, and information

security measures

● Increase operational efficiency and enhance capacity to

respond to customer needs through the use of

technology

● Enhance marketing, product development, risk

management and other functions through data utilization

● Emergence of new insurance needs in response to new

risks

● Alliances with other industries and external companies

Financial regulatory

changes

● Increases in required capital and costs to

comply with regulation

● Increased competition due to deregulation

● Further enhance SFG’s existing strength in “customer-

first” service

● Adopt new approaches and business domains

Analysis of social and environmental changes, an

identification of significant business challenges

STEP.2

STEP.3

STEP.1

Evaluation from SFG’s perspective and the perspectives

of stakeholders

Conduct an evaluation from the perspective of SFG and those of its

stakeholders

Identification of significant business challenges

Identify significant business challenges based on the results of the

evaluation, with approval of management

Strengthen initiatives in these areas

Extraction and organizing of candidates for significant

business challenges

Select candidates from among the social and environmental changes

that are highly related to SFG’s businesses

Identification process for significant business challenges

Value Creation Story

Sony Financial Holdings Inc.Annual Report20206

Value Creation Main Initiatives

Make lifestyles

more

convenient

Offer lifestyles

that feature

safety and

peace of mind

● We utilize a wide range of information to support the

life of each customer by offering appropriate advice,

products and services.

● We aim to contribute to a safe and secure society

featuring next-generation mobility by providing new

technology-enabled insurance products and services.

● We will provide products and services that anticipate

a long-lived society, providing economic security and

promoting wealth-building.

● We will make life more convenient by improving

access to financial services and promoting

innovation.

Contribute to

a healthy,

long-lived

society

Requests from stakeholders

Significant Social and Environmental

Changes

(Significant Business Challenges)

Demographic changes

● Populationdecline ● Aging populationand decliningbirthrate

● Changesin householdstructure● Uncertaintyaboutsocial security

Globally low interest rates

Rapid progress of technological innovation

● Advent of the data economy● Widespread adoption of AI

● Advancement of autonomous driving technologies

Financial regulatory changes

Impact on SFG

Sony Financial Holdings Inc.Annual Report2020 7

Make lifestyles

more

convenient

Offer lifestyles

that feature

safety and

peace of mind

● We utilize a wide range of information to support the

life of each customer by offering appropriate advice,

products and services.

● We aim to contribute to a safe and secure society

featuring next-generation mobility by providing new

technology-enabled insurance products and services.

● We will provide products and services that anticipate

a long-lived society, providing economic security and

promoting wealth-building.

● We will make life more convenient by improving

access to financial services and promoting

innovation.

Contribute to

a healthy,

long-lived

society

Requests from stakeholders

Significant Social and Environmental

Changes

(Significant Business Challenges)

Demographic changes

● Populationdecline ● Aging populationand decliningbirthrate

● Changesin householdstructure● Uncertaintyaboutsocial security

Globally low interest rates

Rapid progress of technological innovation

● Advent of the data economy● Widespread adoption of AI

● Advancement of autonomous driving technologies

Financial regulatory changes

Impact on SFG

Sony Financial Holdings Inc.Annual Report2020 7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

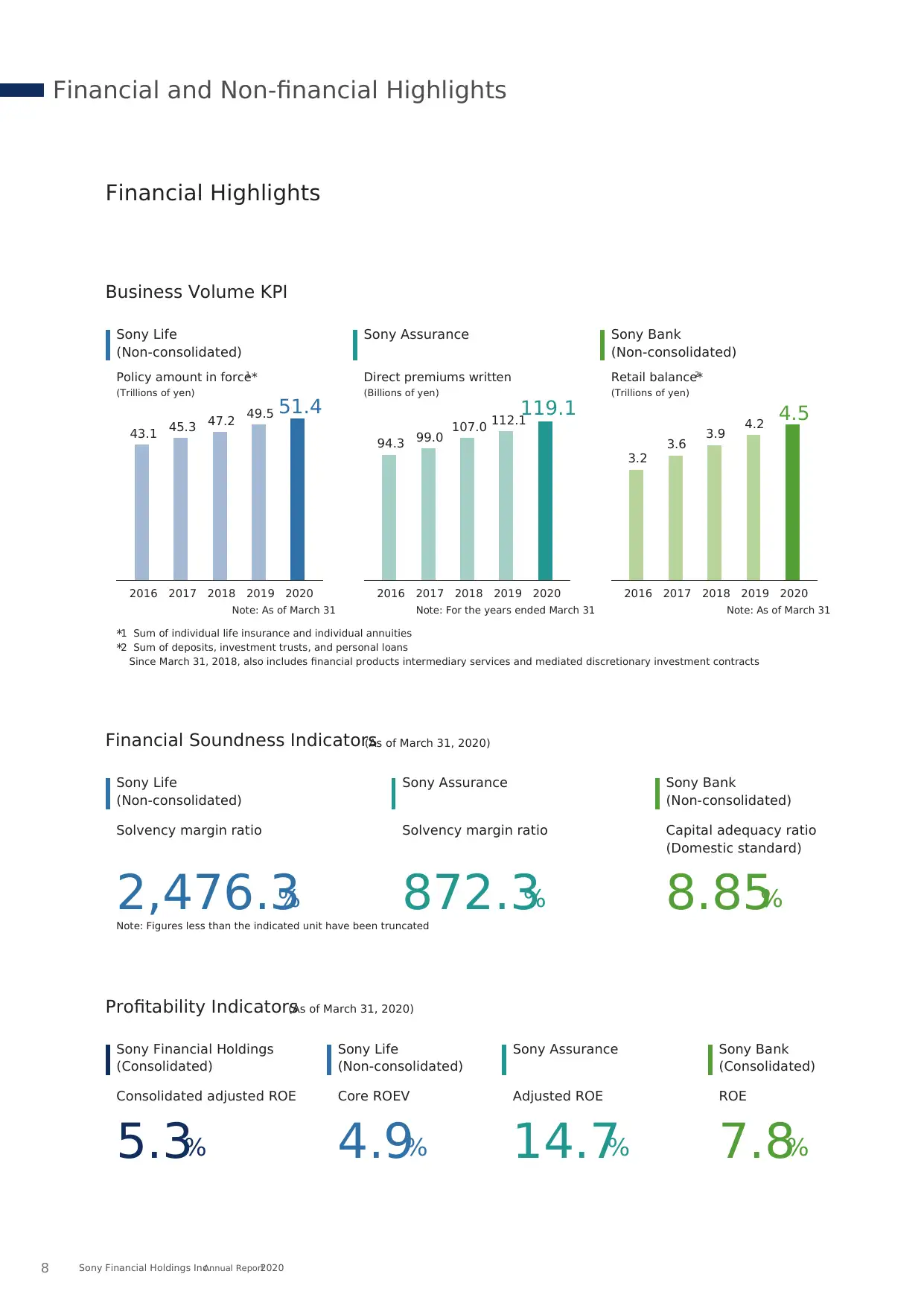

Solvency margin ratio

2,476.3%

Solvency margin ratio

872.3%

Capital adequacy ratio

(Domestic standard)

8.85%

Financial Soundness Indicators(As of March 31, 2020)

Sony Life

(Non-consolidated)

Sony Assurance Sony Bank

(Non-consolidated)

Profitability Indicators(As of March 31, 2020)

Consolidated adjusted ROE

5.3%

Sony Financial Holdings

(Consolidated)

Adjusted ROE

14.7%

Sony Assurance

ROE

7.8%

Sony Bank

(Consolidated)

Core ROEV

4.9%

Sony Life

(Non-consolidated)

Business Volume KPI

*1 Sum of individual life insurance and individual annuities

*2 Sum of deposits, investment trusts, and personal loans

Since March 31, 2018, also includes financial products intermediary services and mediated discretionary investment contracts

Note: Figures less than the indicated unit have been truncated

Financial Highlights

Sony Life

(Non-consolidated)

Sony Assurance Sony Bank

(Non-consolidated)

2016 2017 2018 2020

43.1 45.3 47.2

51.4

2019

49.5

2016 2017 2018 2020

94.3 99.0 107.0

119.1

2019

112.1

2016 2017 2018 2020

3.2

3.6 3.9

4.5

2019

4.2

Note: As of March 31 Note: As of March 31Note: For the years ended March 31

Policy amount in force*1

(Trillions of yen)

Direct premiums written

(Billions of yen)

Retail balance*2

(Trillions of yen)

Financial and Non-financial Highlights

Sony Financial Holdings Inc.Annual Report20208

2,476.3%

Solvency margin ratio

872.3%

Capital adequacy ratio

(Domestic standard)

8.85%

Financial Soundness Indicators(As of March 31, 2020)

Sony Life

(Non-consolidated)

Sony Assurance Sony Bank

(Non-consolidated)

Profitability Indicators(As of March 31, 2020)

Consolidated adjusted ROE

5.3%

Sony Financial Holdings

(Consolidated)

Adjusted ROE

14.7%

Sony Assurance

ROE

7.8%

Sony Bank

(Consolidated)

Core ROEV

4.9%

Sony Life

(Non-consolidated)

Business Volume KPI

*1 Sum of individual life insurance and individual annuities

*2 Sum of deposits, investment trusts, and personal loans

Since March 31, 2018, also includes financial products intermediary services and mediated discretionary investment contracts

Note: Figures less than the indicated unit have been truncated

Financial Highlights

Sony Life

(Non-consolidated)

Sony Assurance Sony Bank

(Non-consolidated)

2016 2017 2018 2020

43.1 45.3 47.2

51.4

2019

49.5

2016 2017 2018 2020

94.3 99.0 107.0

119.1

2019

112.1

2016 2017 2018 2020

3.2

3.6 3.9

4.5

2019

4.2

Note: As of March 31 Note: As of March 31Note: For the years ended March 31

Policy amount in force*1

(Trillions of yen)

Direct premiums written

(Billions of yen)

Retail balance*2

(Trillions of yen)

Financial and Non-financial Highlights

Sony Financial Holdings Inc.Annual Report20208

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

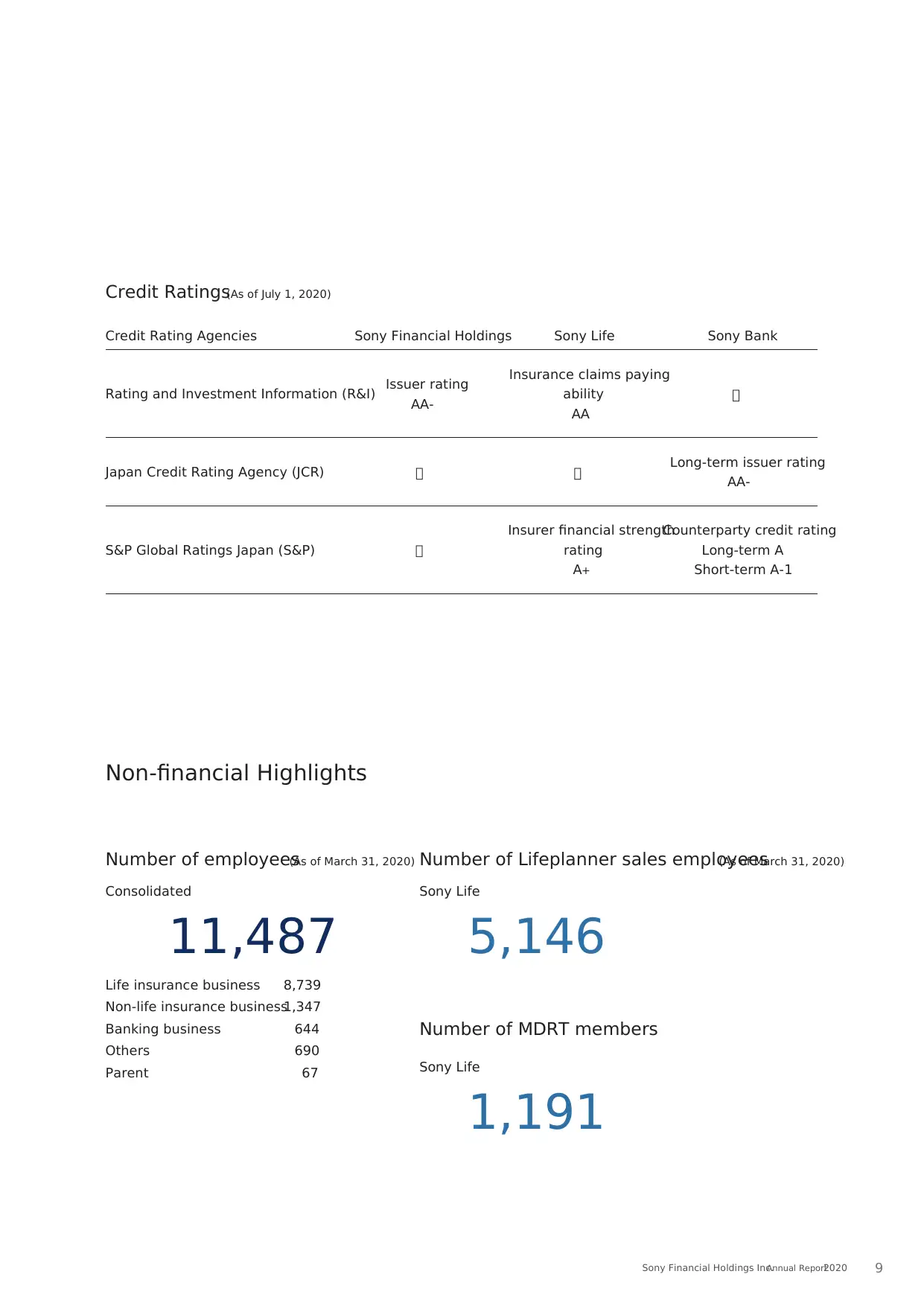

Credit Ratings(As of July 1, 2020)

Credit Rating Agencies Sony Financial Holdings Sony Life Sony Bank

Rating and Investment Information (R&I) Issuer rating

AA-

Insurance claims paying

ability

AA

ー

Japan Credit Rating Agency (JCR) ー ー Long-term issuer rating

AA-

S&P Global Ratings Japan (S&P) ー

Insurer financial strength

rating

A+

Counterparty credit rating

Long-term A

Short-term A-1

Number of employees(As of March 31, 2020)

Non-financial Highlights

Consolidated

11,487

Sony Life

5,146

Number of Lifeplanner sales employees(As of March 31, 2020)

Number of MDRT members

Sony Life

1,191

Life insurance business 8,739

Non-life insurance business1,347

Banking business 644

Others 690

Parent 67

Sony Financial Holdings Inc.Annual Report2020 9

Credit Rating Agencies Sony Financial Holdings Sony Life Sony Bank

Rating and Investment Information (R&I) Issuer rating

AA-

Insurance claims paying

ability

AA

ー

Japan Credit Rating Agency (JCR) ー ー Long-term issuer rating

AA-

S&P Global Ratings Japan (S&P) ー

Insurer financial strength

rating

A+

Counterparty credit rating

Long-term A

Short-term A-1

Number of employees(As of March 31, 2020)

Non-financial Highlights

Consolidated

11,487

Sony Life

5,146

Number of Lifeplanner sales employees(As of March 31, 2020)

Number of MDRT members

Sony Life

1,191

Life insurance business 8,739

Non-life insurance business1,347

Banking business 644

Others 690

Parent 67

Sony Financial Holdings Inc.Annual Report2020 9

Contribute to a sustainable society where

people feel a sense of enrichment

President & CEO, Representative Director

Message from the President & CEO

Sony Financial Holdings Inc.Annual Report202010

people feel a sense of enrichment

President & CEO, Representative Director

Message from the President & CEO

Sony Financial Holdings Inc.Annual Report202010

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 100

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.