Comprehensive Report on Accounting for Share Buy Back Practices

VerifiedAdded on 2023/06/04

|8

|1579

|388

Report

AI Summary

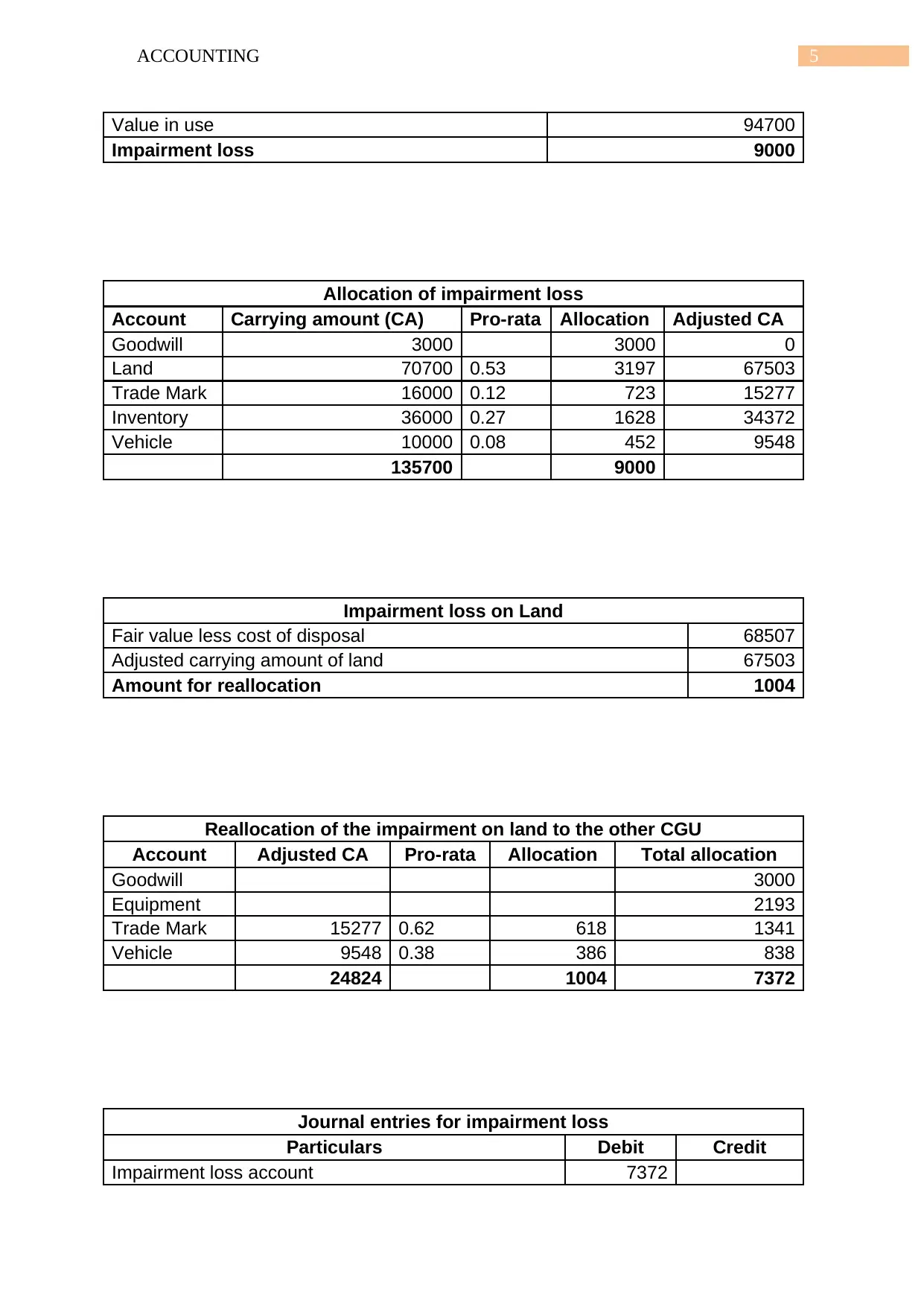

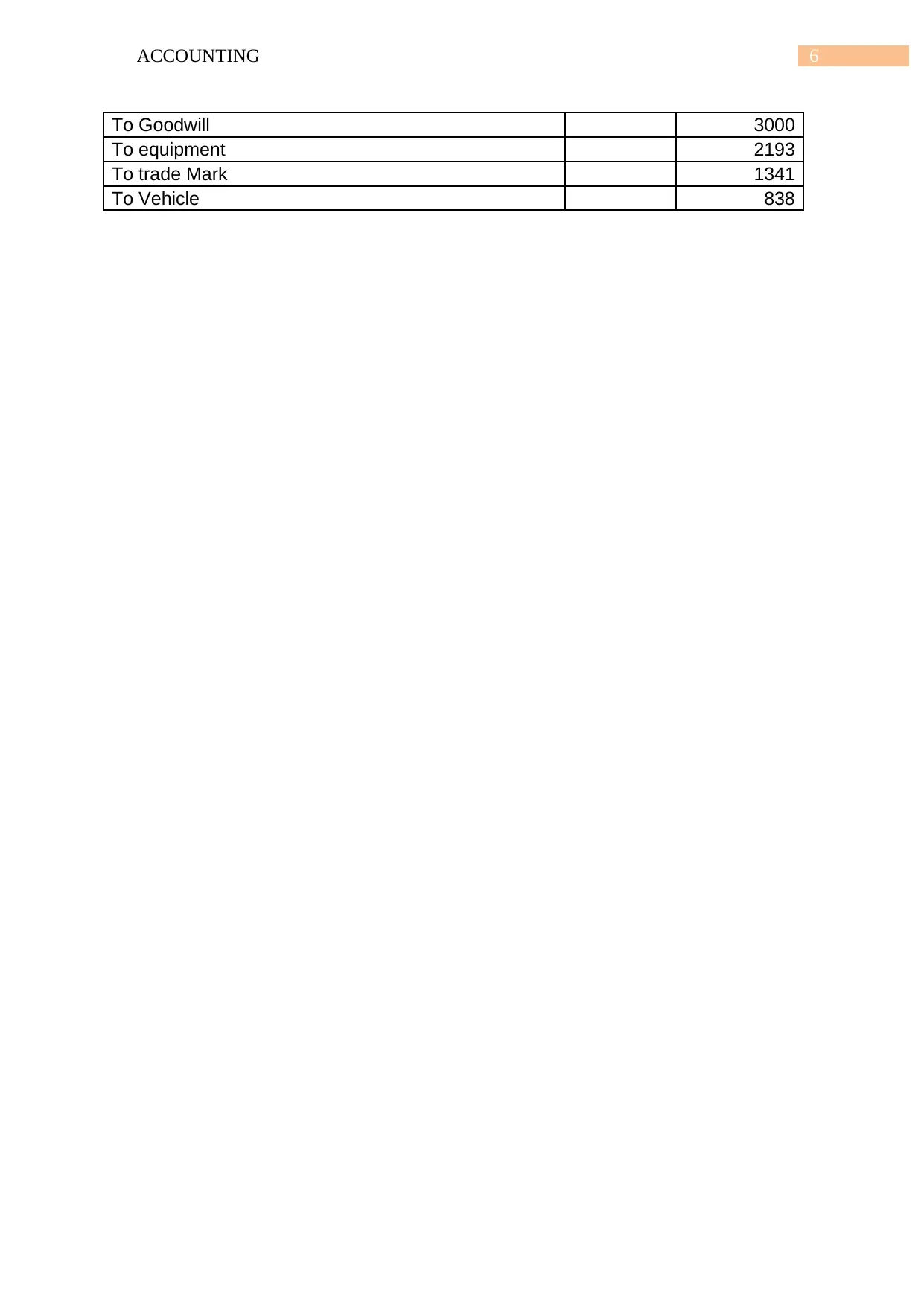

This report provides a detailed analysis of accounting for share buybacks, focusing on the cost method and its implications for financial reporting. It explains how companies repurchase their own shares, the accounting treatment of treasury stock as a contra-equity account, and the impact on key financial metrics such as return on capital and return on equity. The report also covers the journal entries required for share buybacks, including the debit and credit entries for treasury stock, cash, and paid-in capital. Furthermore, it addresses the accounting for impairment loss, including the allocation of impairment to different assets and the necessary journal entries. The report concludes with recommendations for companies regarding the use of surplus funds for share repurchases and the importance of proper accounting practices. Desklib offers this and many other solved assignments for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.