Accounting Analysis: Share Buybacks and Asset Impairment - Gali Ltd

VerifiedAdded on 2023/04/03

|5

|1557

|264

Report

AI Summary

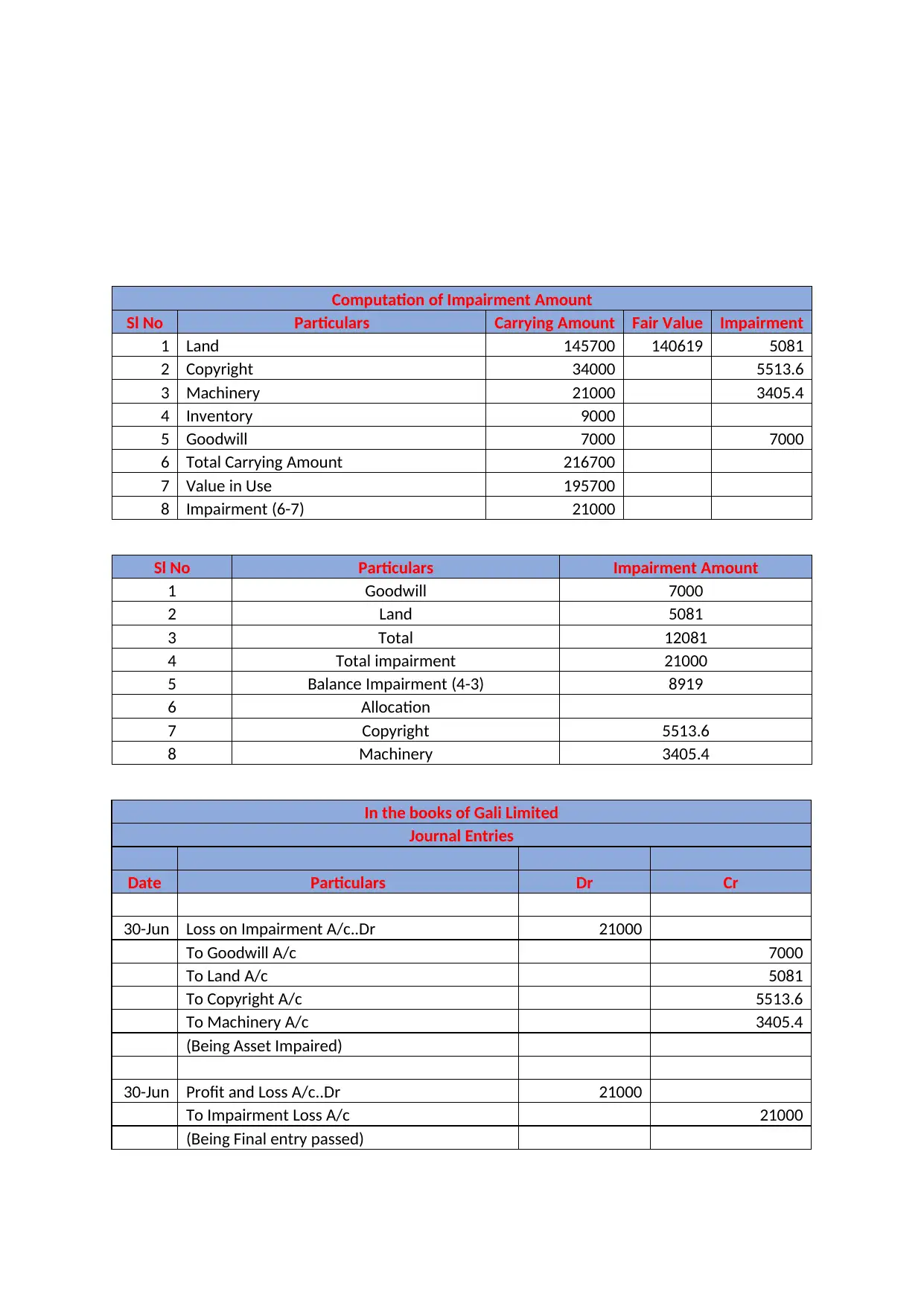

This report provides a detailed overview of accounting for share buybacks, including the cost method and constructive retirement method, along with the accounting treatment for related transaction costs. It further explains the Australian Accounting Standard AASB 136 on Impairment of Assets, outlining its objectives, scope, and key definitions such as carrying amount, cash-generating unit, and recoverable amount. The report includes a practical analysis of Gali Ltd, demonstrating the calculation of impairment loss and the corresponding journal entries for goodwill, land, copyright, and machinery. The analysis adheres to AASB 136 guidelines, ensuring assets are not carried at amounts exceeding their recoverable value.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.