Corporate Accounting Report: Share Buy-backs and Impairment Losses

VerifiedAdded on 2023/04/23

|7

|1472

|327

Report

AI Summary

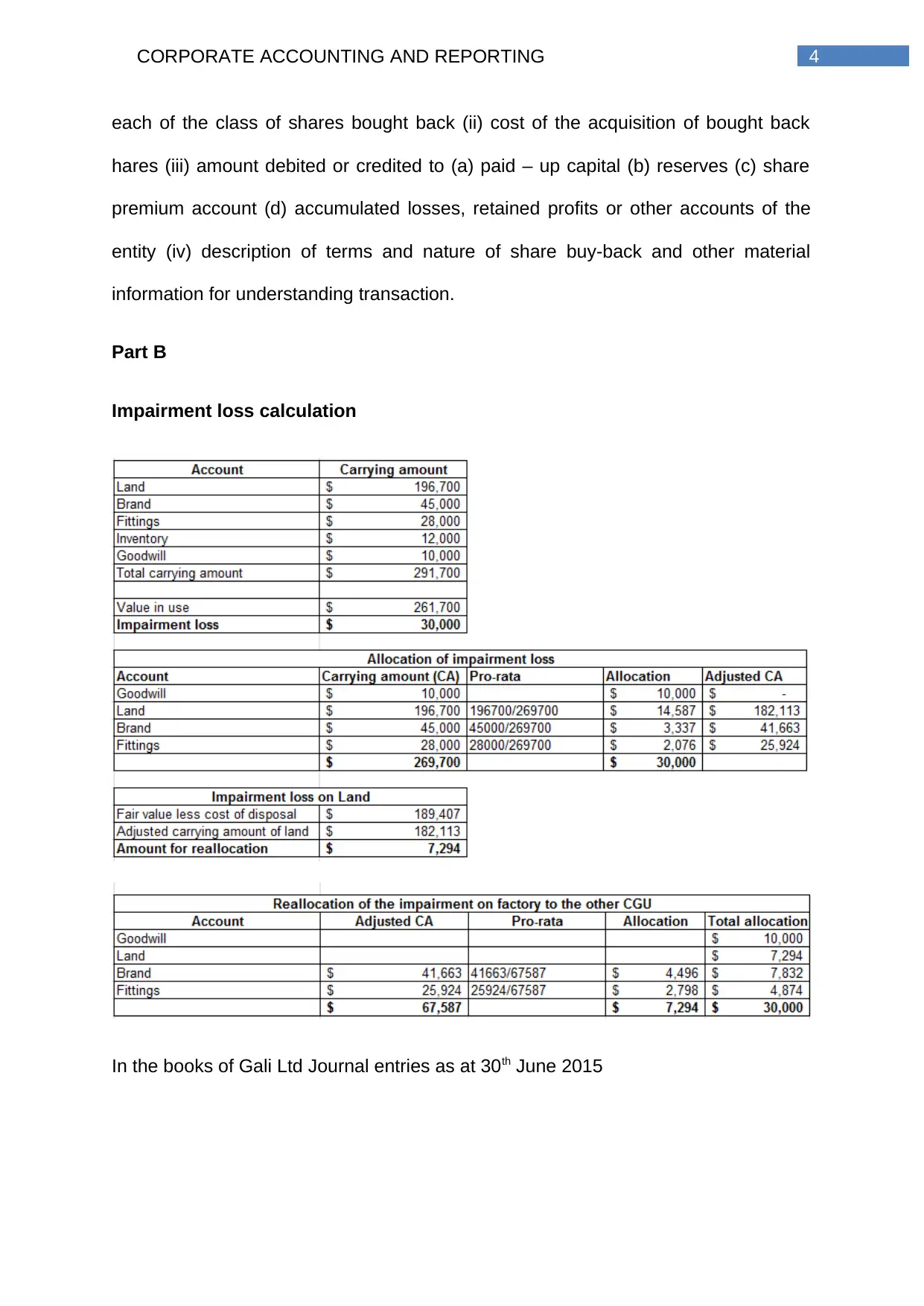

This report focuses on corporate accounting and reporting, specifically addressing share buy-backs and impairment loss calculations. Part A of the report explains share buy-backs, detailing the process, reasons for buy-backs, shareholder implications, and different types of buy-back methods, including equal access, employee share schemes, and on-market buy-backs. The report also covers the relevant provisions in the Corporations Act 2001. Part B provides an impairment loss calculation for Gali Ltd, including journal entries to illustrate the accounting treatment. The report concludes with a list of references to support the information presented.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.