Business, Society, and Planet: Shell and BP Sustainability Analysis

VerifiedAdded on 2020/02/24

|14

|2913

|87

Report

AI Summary

This report provides a detailed comparison of Shell and British Petroleum's sustainability reports, focusing on their core business activities, social, environmental, and economic impacts. It examines differences in their reporting practices, including climate change initiatives, community engagement, and transparency. The report evaluates both companies based on Zadek et al.'s (1997) criteria for social accounting, such as inclusivity, comparability, completeness, and external verification. It also analyzes the companies' values and reflects on a group discussion regarding their sustainability approaches, ultimately concluding that Royal Dutch Shell demonstrates a more comprehensive and transparent approach to sustainability compared to British Petroleum, despite both companies facing similar ethical considerations regarding environmental incidents. The report underscores the importance of sustainability in the oil and gas industry and the ongoing efforts of these companies to address climate change and societal impacts. The report can be found on Desklib, a platform for students to access past papers and solved assignments.

Running head: BUSINESS, SOCIETY AND PLANET

Business, Society and Planet

Name of the Student

Name of the University

Author Note

Business, Society and Planet

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS, SOCIETY AND PLANET

Table of Contents

1.0 Introduction................................................................................................................................2

2.0 Discussion..................................................................................................................................2

2.1 Core business activities in the industry.................................................................................2

2.2 Difference of the two companies based on range of social, environmental and economic

issues............................................................................................................................................4

2.3 Differences between reports of Shell and British Petroleum.................................................5

2.4 Evaluation of social accounting approach according to Zadek et al.’s (1997) criteria..........6

2.4.1 Inclusivity.......................................................................................................................6

2.4.2 Comparability.................................................................................................................7

2.4.3 Completeness..................................................................................................................7

2.4.4 Evolution.........................................................................................................................8

2.4.5 Management policies and system...................................................................................8

2.4.6 Disclosure.......................................................................................................................8

2.4.7 External verification.......................................................................................................9

2.4.8 Continuous improvement................................................................................................9

2.5 Company’s values- Shell and British Petroleum...................................................................9

2.6 Reflection of the group discussion......................................................................................10

3.0 Conclusion...............................................................................................................................10

4.0 Reference List..........................................................................................................................12

Table of Contents

1.0 Introduction................................................................................................................................2

2.0 Discussion..................................................................................................................................2

2.1 Core business activities in the industry.................................................................................2

2.2 Difference of the two companies based on range of social, environmental and economic

issues............................................................................................................................................4

2.3 Differences between reports of Shell and British Petroleum.................................................5

2.4 Evaluation of social accounting approach according to Zadek et al.’s (1997) criteria..........6

2.4.1 Inclusivity.......................................................................................................................6

2.4.2 Comparability.................................................................................................................7

2.4.3 Completeness..................................................................................................................7

2.4.4 Evolution.........................................................................................................................8

2.4.5 Management policies and system...................................................................................8

2.4.6 Disclosure.......................................................................................................................8

2.4.7 External verification.......................................................................................................9

2.4.8 Continuous improvement................................................................................................9

2.5 Company’s values- Shell and British Petroleum...................................................................9

2.6 Reflection of the group discussion......................................................................................10

3.0 Conclusion...............................................................................................................................10

4.0 Reference List..........................................................................................................................12

2BUSINESS, SOCIETY AND PLANET

1.0 Introduction

The United Kingdom’s two leading oil and gas companies Shell and British Petroleum

are taken into consideration for this assessment. Every organization publishes their sustainability

report so that stakeholders of those companies can view their reflection on past performance and

future initiatives in terms of social and governance (ESG), environmental aspects and corporate

social responsibility to some extent. This assessment highlights the comparison of the two

companies based on their sustainability report. The difference between these two companies

based on the range of social, environmental and economic issues is also illustrated in the

business report. Moreover, a difference between the reports that furthermore describes the

differences of culture, attitudes, regulations and technology is also represented. The discussions

of the differences in this sustainability report based on the Zadek et al.’s (1997) criteria. Lastly, a

group dissection based on the preferences of one of the two considered organization will also be

discussed.

2.0 Discussion

2.1 Core business activities in the industry

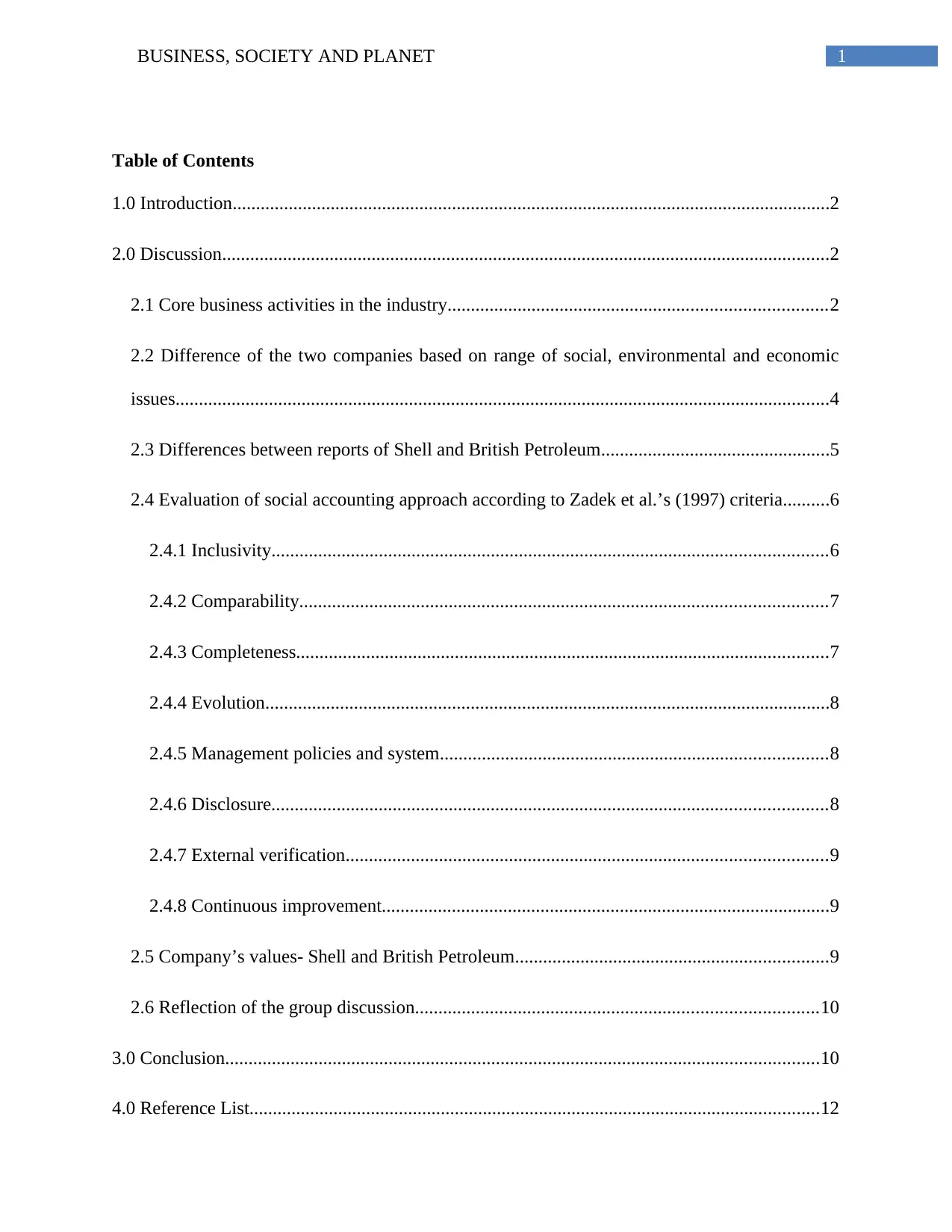

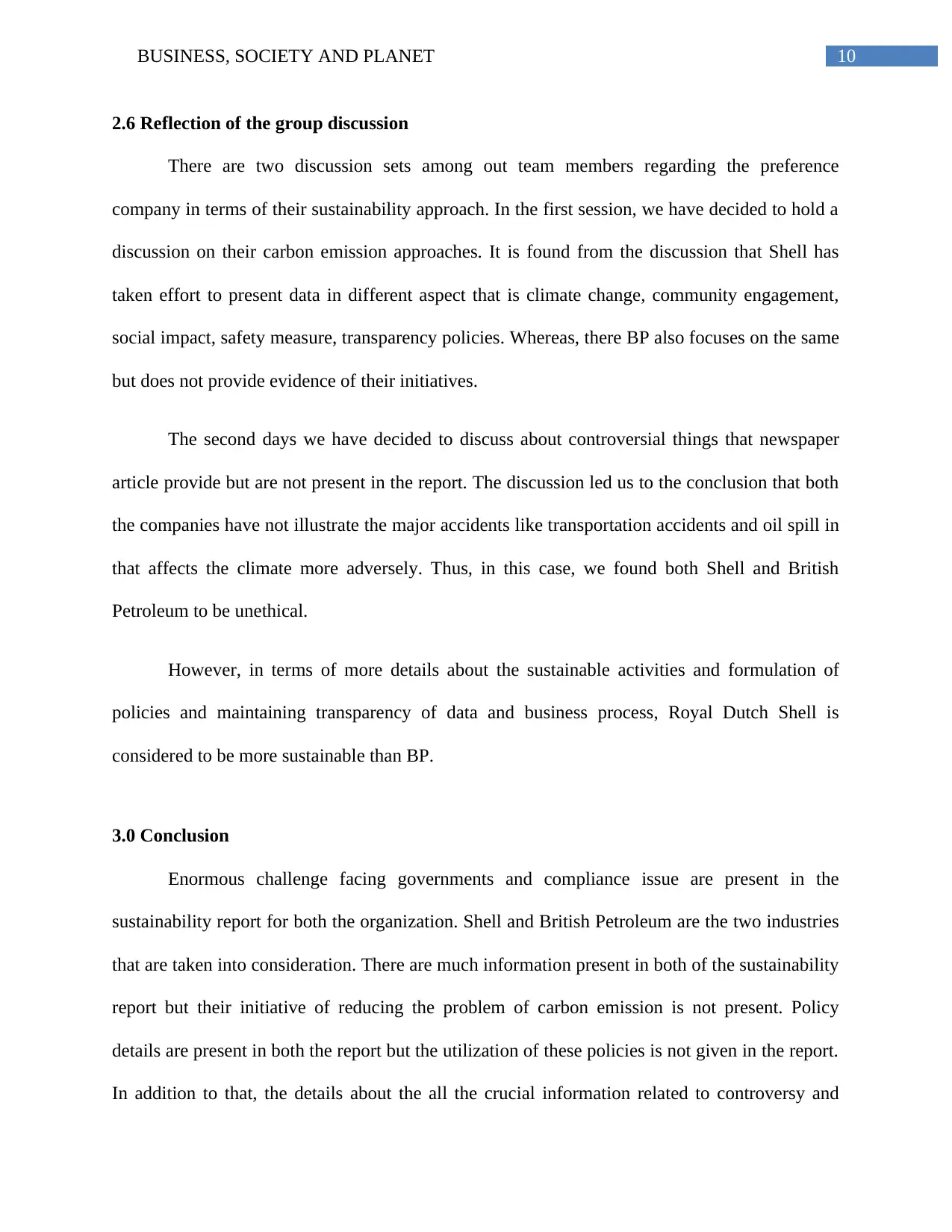

Shell in the year 2016 had attained the annual revenue of $183,008 million which was

$222,894 million in the previous year (Statista, 2017)

1.0 Introduction

The United Kingdom’s two leading oil and gas companies Shell and British Petroleum

are taken into consideration for this assessment. Every organization publishes their sustainability

report so that stakeholders of those companies can view their reflection on past performance and

future initiatives in terms of social and governance (ESG), environmental aspects and corporate

social responsibility to some extent. This assessment highlights the comparison of the two

companies based on their sustainability report. The difference between these two companies

based on the range of social, environmental and economic issues is also illustrated in the

business report. Moreover, a difference between the reports that furthermore describes the

differences of culture, attitudes, regulations and technology is also represented. The discussions

of the differences in this sustainability report based on the Zadek et al.’s (1997) criteria. Lastly, a

group dissection based on the preferences of one of the two considered organization will also be

discussed.

2.0 Discussion

2.1 Core business activities in the industry

Shell in the year 2016 had attained the annual revenue of $183,008 million which was

$222,894 million in the previous year (Statista, 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS, SOCIETY AND PLANET

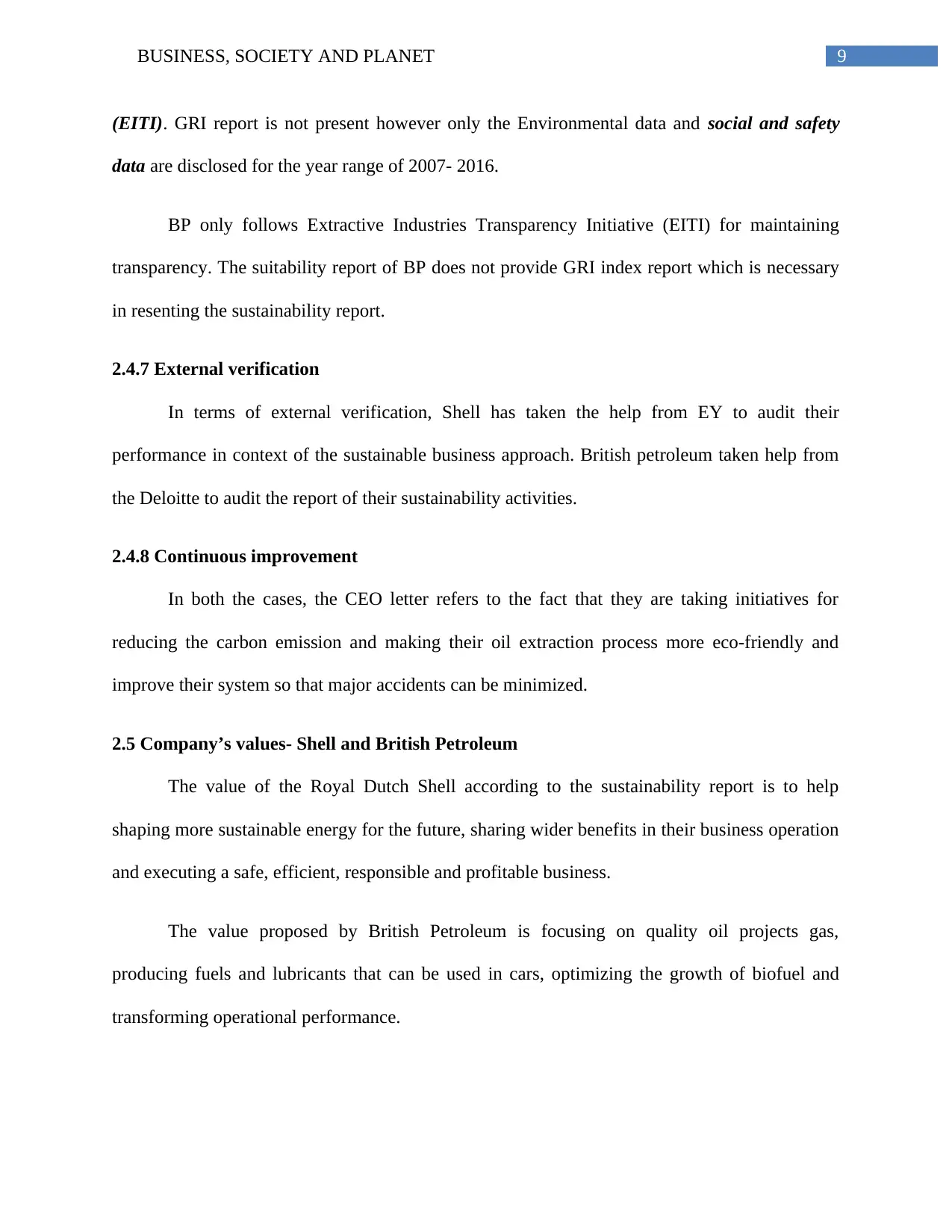

Image 1: Annual revenue of British Petroleum

(Source: Statista, 2017)

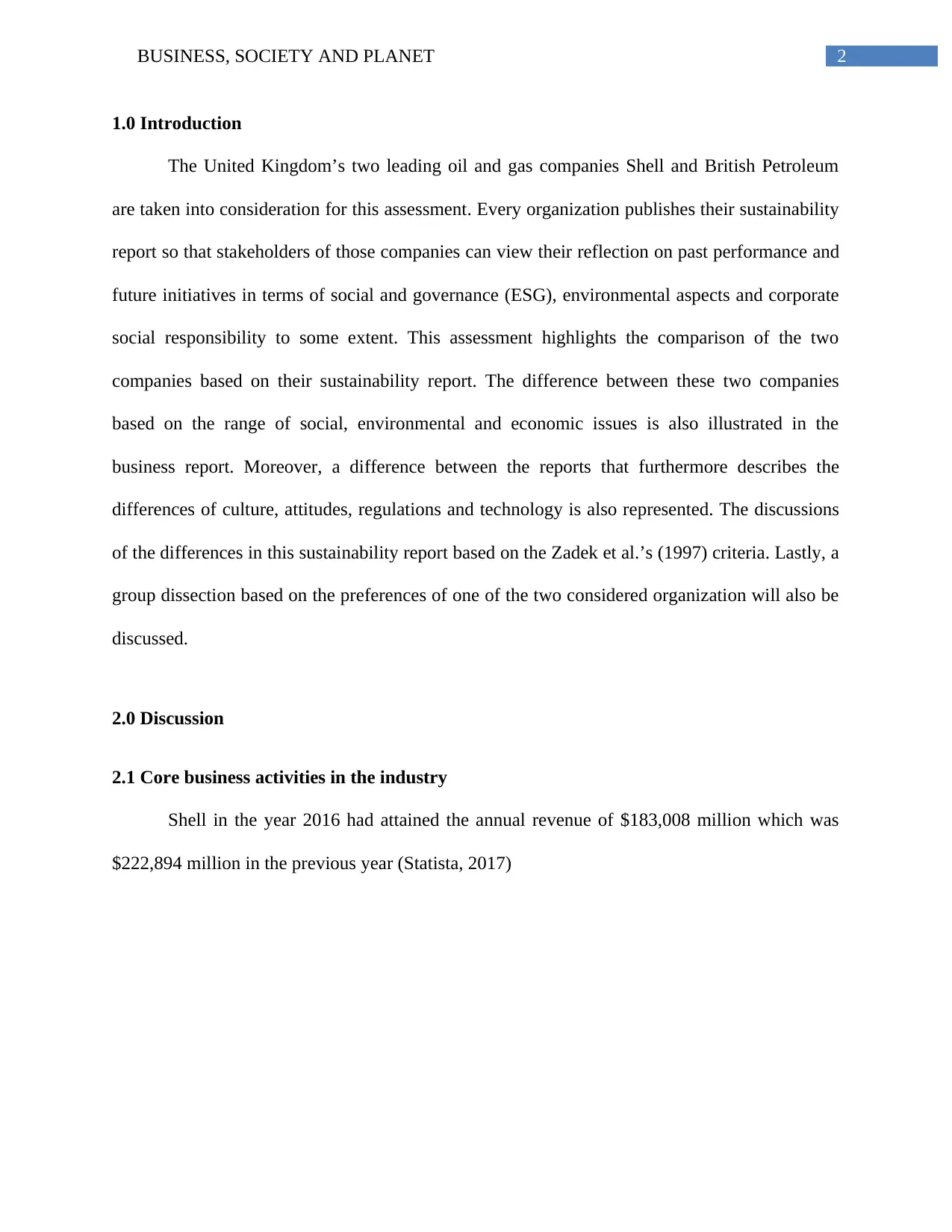

The annual revenue incurred in the year 2016 by Royal Dutch Shell $233.59 billion;

whereas, in the previous year the concerned organization have earned $ 264.96 billion (Statista,

2017).

Image 2: Annual revenue of Royal Dutch Shell

Image 1: Annual revenue of British Petroleum

(Source: Statista, 2017)

The annual revenue incurred in the year 2016 by Royal Dutch Shell $233.59 billion;

whereas, in the previous year the concerned organization have earned $ 264.96 billion (Statista,

2017).

Image 2: Annual revenue of Royal Dutch Shell

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS, SOCIETY AND PLANET

(Source: Statista, 2017)

However, in terms of oil and gas sustainability ranking British Petroleum leads the Royal

Dutch Shell. In this business report, the difference among the two companies is effective as both

serve same performance and thus carrying a comparison between the two companies present a

greater overview regarding the activities towards sustainability.

Shell is associated with the business activity of oil exploration, development and

extraction, manufacturing and energy production, transport and trading and sales and

marketing. This information is present in the starting pages of the sustainability report of Shell.

BP on the other hand is also liable for performing the similar job roles. Another fact that is

necessary to address that is both the companies publishes their sustainability report from decades

and thus it can be said that both these companies are aware of their responsibility towards the

planet earth.

2.2 Difference of the two companies based on range of social, environmental and economic

issues

Shell has mentioned the issue on climate change and energy transition, Business ethics,

transparency and governance, environmental impacts, GHG and energy and Community

engagement and societal impact. According to the CEO’s letter, they are taking continuous effort

to ensure safety so that they can work without causing harm to people and the environment.

British Petroleum reported their social issues that are they have to play a crucial role in

business for lower carbon future to take action on climate change, focusing on safe operations,

maximizing value to society, respecting human rights and managing the local environmental

impacts. The letter written by CEO of the concerned organization written that $1 billion of

(Source: Statista, 2017)

However, in terms of oil and gas sustainability ranking British Petroleum leads the Royal

Dutch Shell. In this business report, the difference among the two companies is effective as both

serve same performance and thus carrying a comparison between the two companies present a

greater overview regarding the activities towards sustainability.

Shell is associated with the business activity of oil exploration, development and

extraction, manufacturing and energy production, transport and trading and sales and

marketing. This information is present in the starting pages of the sustainability report of Shell.

BP on the other hand is also liable for performing the similar job roles. Another fact that is

necessary to address that is both the companies publishes their sustainability report from decades

and thus it can be said that both these companies are aware of their responsibility towards the

planet earth.

2.2 Difference of the two companies based on range of social, environmental and economic

issues

Shell has mentioned the issue on climate change and energy transition, Business ethics,

transparency and governance, environmental impacts, GHG and energy and Community

engagement and societal impact. According to the CEO’s letter, they are taking continuous effort

to ensure safety so that they can work without causing harm to people and the environment.

British Petroleum reported their social issues that are they have to play a crucial role in

business for lower carbon future to take action on climate change, focusing on safe operations,

maximizing value to society, respecting human rights and managing the local environmental

impacts. The letter written by CEO of the concerned organization written that $1 billion of

5BUSINESS, SOCIETY AND PLANET

investment was made for formulating and implementing low carbon technologies to build a

sustainable future. Thus, it can be said that both the companies are taking initiative for

sustainable business procedure.

2.3 Differences between reports of Shell and British Petroleum

Shell started their discussion of sustainability by representing their aim for running a safe,

efficient, responsible and profitable business. The positive and unique attribute of this report is

that they have presented their goals for the year 2016 and highlight the priorities for the year

2017. This approach shows that they have focused both on their current business strategies and

future business plans.

Shell also presented their work for addressing the climate change that is utilizing only the

natural gas into different products that is liquid fuels, hydraulic fluids and lubricants for final

use. The concerned organization also collaborated with government to create carbon pricing

mechanisms. Moreover, they also have taken steps for demonstrating CCS technology with their

global partners.

British Petroleum highlighted their key issues prior to any other information. However,

the report consists of the details of the business functions, their business trading throughout the

world and segmentation of their employees based on region and segments, which is not required

to be reported in sustainability report. In addition to that, there positive aspect of this report is

that they have presented their green house gas emission and their breakdown along with their

details for the year 2012 to 2016.

British Petroleum also presented their timeline of two decades that illustrates their

initiatives of tackling climate change. They have also represented a statistical representation of

investment was made for formulating and implementing low carbon technologies to build a

sustainable future. Thus, it can be said that both the companies are taking initiative for

sustainable business procedure.

2.3 Differences between reports of Shell and British Petroleum

Shell started their discussion of sustainability by representing their aim for running a safe,

efficient, responsible and profitable business. The positive and unique attribute of this report is

that they have presented their goals for the year 2016 and highlight the priorities for the year

2017. This approach shows that they have focused both on their current business strategies and

future business plans.

Shell also presented their work for addressing the climate change that is utilizing only the

natural gas into different products that is liquid fuels, hydraulic fluids and lubricants for final

use. The concerned organization also collaborated with government to create carbon pricing

mechanisms. Moreover, they also have taken steps for demonstrating CCS technology with their

global partners.

British Petroleum highlighted their key issues prior to any other information. However,

the report consists of the details of the business functions, their business trading throughout the

world and segmentation of their employees based on region and segments, which is not required

to be reported in sustainability report. In addition to that, there positive aspect of this report is

that they have presented their green house gas emission and their breakdown along with their

details for the year 2012 to 2016.

British Petroleum also presented their timeline of two decades that illustrates their

initiatives of tackling climate change. They have also represented a statistical representation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS, SOCIETY AND PLANET

GHG movements from 2015 to 2016 along with their performance for reducing the climate

change impact.

2.4 Evaluation of social accounting approach according to Zadek et al.’s (1997) criteria

Lee and Vachon (2016) stated that there are total of eight principles under the Zadek et

al.’s (1997) criteria- inclusivity, comparability, completeness, evolution, management policies

and system, disclosure, external verification and continuous improvement. Iannuzzi (2017)

furthermore explains that these criteria assess whether or not an organization is auditing their

sustainable report appropriately. In this aspect both the companies- British Petroleum and Royal

Dutch Shell reported their issues, controversies and transparency in their business.

2.4.1 Inclusivity

Shell has successfully identified their Board of Directors (BOD) who is liable to assess

the governance of tax. These members also assess system of risk management and internal

control. However, the key members and their role in maintaining the sustainability are not

present. The committee about which the details are given is for the corporate social

responsibility. This committee is also responsible for measuring sustainability performance and

audit results.

Alike Royal Dutch Shell, British Petroleum also stated that their Board of Directors

evaluate the carbon emission and carbon footprint research. However in this case also, the

stakeholder’s details are not discussed.

GHG movements from 2015 to 2016 along with their performance for reducing the climate

change impact.

2.4 Evaluation of social accounting approach according to Zadek et al.’s (1997) criteria

Lee and Vachon (2016) stated that there are total of eight principles under the Zadek et

al.’s (1997) criteria- inclusivity, comparability, completeness, evolution, management policies

and system, disclosure, external verification and continuous improvement. Iannuzzi (2017)

furthermore explains that these criteria assess whether or not an organization is auditing their

sustainable report appropriately. In this aspect both the companies- British Petroleum and Royal

Dutch Shell reported their issues, controversies and transparency in their business.

2.4.1 Inclusivity

Shell has successfully identified their Board of Directors (BOD) who is liable to assess

the governance of tax. These members also assess system of risk management and internal

control. However, the key members and their role in maintaining the sustainability are not

present. The committee about which the details are given is for the corporate social

responsibility. This committee is also responsible for measuring sustainability performance and

audit results.

Alike Royal Dutch Shell, British Petroleum also stated that their Board of Directors

evaluate the carbon emission and carbon footprint research. However in this case also, the

stakeholder’s details are not discussed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS, SOCIETY AND PLANET

2.4.2 Comparability

Shell has information about their corporate social responsibility along with their

sustainable approaches. The details of the code of conduct is not discussed however a link is

provided in which the values and business principles of shell is defined properly.

British Petroleum does not include their CSR activities in their business sustainability

report. On the other hand, details about governance of sustainability issues are given in the

report. This committee is known as safety, ethics and environment assurance committee

(SEEAC) but the details about code of ethics is absent in the report.

2.4.3 Completeness

In both the cases, the pictorial representation is not present for all the aspects. Descriptive

detail is present that need much time to read and getting the information. In the sustainability

report for Royal Dutch Shell, the information only focused on energy transition that is addressing

climate change, utilization of natural gas, research and development for lower carbon

alternatives.

In comparison, British Petroleum’s sustainability report illustrates the sustainability in

every aspect that is climate change, energy transformation, supply chain and inventory

management. Details about freshwater consumption, water consumption intensity, air

emissions and environmental expenditures are discussed properly that on the other hand is not

present in Shell’s report. In both the cases the major accidents done by oil spillage is not

highlighted in the sustainability report. Thus, it can be said that some important controversy is

hidden in the report in both the case.

2.4.2 Comparability

Shell has information about their corporate social responsibility along with their

sustainable approaches. The details of the code of conduct is not discussed however a link is

provided in which the values and business principles of shell is defined properly.

British Petroleum does not include their CSR activities in their business sustainability

report. On the other hand, details about governance of sustainability issues are given in the

report. This committee is known as safety, ethics and environment assurance committee

(SEEAC) but the details about code of ethics is absent in the report.

2.4.3 Completeness

In both the cases, the pictorial representation is not present for all the aspects. Descriptive

detail is present that need much time to read and getting the information. In the sustainability

report for Royal Dutch Shell, the information only focused on energy transition that is addressing

climate change, utilization of natural gas, research and development for lower carbon

alternatives.

In comparison, British Petroleum’s sustainability report illustrates the sustainability in

every aspect that is climate change, energy transformation, supply chain and inventory

management. Details about freshwater consumption, water consumption intensity, air

emissions and environmental expenditures are discussed properly that on the other hand is not

present in Shell’s report. In both the cases the major accidents done by oil spillage is not

highlighted in the sustainability report. Thus, it can be said that some important controversy is

hidden in the report in both the case.

8BUSINESS, SOCIETY AND PLANET

2.4.4 Evolution

Identification of the target line is not given in the report but the planning for reducing the

carbon emission is present. However, the measures for reducing the number of accidents are

discussed. Shell provides the details of their safety target in terms of road safety and oil spills

only. British Petroleum in terms of major accidents consider vehicle accidents and traffic

accidents is discussed. One positive aspect in this case is BP’s report; the graphical interpretation

of the vehicle accidents is given for the year 2012 to 2016.

2.4.5 Management policies and system

Shell have formulated energy and climate policy, retaliation policy, Health, Safety,

Security and Environment and Social Performance (HSSE&SP) policy, child labor policy,

employment policy, fair-work policy, policies for equal opportunities and supply chain policy.

Policies in British Petroleum are formulated for risk management systems, greenhouse

gas policy, consumer behavior policy, human rights policy and corruption policy. In both the

reports there are definition of these policies are only present and the details of the

implementation of these policies on breaching of the business approaches is not present. Thus,

here also the sustainability report lacks some crucial details.

2.4.6 Disclosure

In the report, Shell mentioned that they have disclosed their every details from their form

20-F, File No 1-32575 but the data is not present for public use or preview. The company also

adhere Governments Regulations 2014 for disclosure related to payments. They have adhered to

the transparency aspect under the initiative of Extractive Industries Transparency Initiative

2.4.4 Evolution

Identification of the target line is not given in the report but the planning for reducing the

carbon emission is present. However, the measures for reducing the number of accidents are

discussed. Shell provides the details of their safety target in terms of road safety and oil spills

only. British Petroleum in terms of major accidents consider vehicle accidents and traffic

accidents is discussed. One positive aspect in this case is BP’s report; the graphical interpretation

of the vehicle accidents is given for the year 2012 to 2016.

2.4.5 Management policies and system

Shell have formulated energy and climate policy, retaliation policy, Health, Safety,

Security and Environment and Social Performance (HSSE&SP) policy, child labor policy,

employment policy, fair-work policy, policies for equal opportunities and supply chain policy.

Policies in British Petroleum are formulated for risk management systems, greenhouse

gas policy, consumer behavior policy, human rights policy and corruption policy. In both the

reports there are definition of these policies are only present and the details of the

implementation of these policies on breaching of the business approaches is not present. Thus,

here also the sustainability report lacks some crucial details.

2.4.6 Disclosure

In the report, Shell mentioned that they have disclosed their every details from their form

20-F, File No 1-32575 but the data is not present for public use or preview. The company also

adhere Governments Regulations 2014 for disclosure related to payments. They have adhered to

the transparency aspect under the initiative of Extractive Industries Transparency Initiative

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS, SOCIETY AND PLANET

(EITI). GRI report is not present however only the Environmental data and social and safety

data are disclosed for the year range of 2007- 2016.

BP only follows Extractive Industries Transparency Initiative (EITI) for maintaining

transparency. The suitability report of BP does not provide GRI index report which is necessary

in resenting the sustainability report.

2.4.7 External verification

In terms of external verification, Shell has taken the help from EY to audit their

performance in context of the sustainable business approach. British petroleum taken help from

the Deloitte to audit the report of their sustainability activities.

2.4.8 Continuous improvement

In both the cases, the CEO letter refers to the fact that they are taking initiatives for

reducing the carbon emission and making their oil extraction process more eco-friendly and

improve their system so that major accidents can be minimized.

2.5 Company’s values- Shell and British Petroleum

The value of the Royal Dutch Shell according to the sustainability report is to help

shaping more sustainable energy for the future, sharing wider benefits in their business operation

and executing a safe, efficient, responsible and profitable business.

The value proposed by British Petroleum is focusing on quality oil projects gas,

producing fuels and lubricants that can be used in cars, optimizing the growth of biofuel and

transforming operational performance.

(EITI). GRI report is not present however only the Environmental data and social and safety

data are disclosed for the year range of 2007- 2016.

BP only follows Extractive Industries Transparency Initiative (EITI) for maintaining

transparency. The suitability report of BP does not provide GRI index report which is necessary

in resenting the sustainability report.

2.4.7 External verification

In terms of external verification, Shell has taken the help from EY to audit their

performance in context of the sustainable business approach. British petroleum taken help from

the Deloitte to audit the report of their sustainability activities.

2.4.8 Continuous improvement

In both the cases, the CEO letter refers to the fact that they are taking initiatives for

reducing the carbon emission and making their oil extraction process more eco-friendly and

improve their system so that major accidents can be minimized.

2.5 Company’s values- Shell and British Petroleum

The value of the Royal Dutch Shell according to the sustainability report is to help

shaping more sustainable energy for the future, sharing wider benefits in their business operation

and executing a safe, efficient, responsible and profitable business.

The value proposed by British Petroleum is focusing on quality oil projects gas,

producing fuels and lubricants that can be used in cars, optimizing the growth of biofuel and

transforming operational performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS, SOCIETY AND PLANET

2.6 Reflection of the group discussion

There are two discussion sets among out team members regarding the preference

company in terms of their sustainability approach. In the first session, we have decided to hold a

discussion on their carbon emission approaches. It is found from the discussion that Shell has

taken effort to present data in different aspect that is climate change, community engagement,

social impact, safety measure, transparency policies. Whereas, there BP also focuses on the same

but does not provide evidence of their initiatives.

The second days we have decided to discuss about controversial things that newspaper

article provide but are not present in the report. The discussion led us to the conclusion that both

the companies have not illustrate the major accidents like transportation accidents and oil spill in

that affects the climate more adversely. Thus, in this case, we found both Shell and British

Petroleum to be unethical.

However, in terms of more details about the sustainable activities and formulation of

policies and maintaining transparency of data and business process, Royal Dutch Shell is

considered to be more sustainable than BP.

3.0 Conclusion

Enormous challenge facing governments and compliance issue are present in the

sustainability report for both the organization. Shell and British Petroleum are the two industries

that are taken into consideration. There are much information present in both of the sustainability

report but their initiative of reducing the problem of carbon emission is not present. Policy

details are present in both the report but the utilization of these policies is not given in the report.

In addition to that, the details about the all the crucial information related to controversy and

2.6 Reflection of the group discussion

There are two discussion sets among out team members regarding the preference

company in terms of their sustainability approach. In the first session, we have decided to hold a

discussion on their carbon emission approaches. It is found from the discussion that Shell has

taken effort to present data in different aspect that is climate change, community engagement,

social impact, safety measure, transparency policies. Whereas, there BP also focuses on the same

but does not provide evidence of their initiatives.

The second days we have decided to discuss about controversial things that newspaper

article provide but are not present in the report. The discussion led us to the conclusion that both

the companies have not illustrate the major accidents like transportation accidents and oil spill in

that affects the climate more adversely. Thus, in this case, we found both Shell and British

Petroleum to be unethical.

However, in terms of more details about the sustainable activities and formulation of

policies and maintaining transparency of data and business process, Royal Dutch Shell is

considered to be more sustainable than BP.

3.0 Conclusion

Enormous challenge facing governments and compliance issue are present in the

sustainability report for both the organization. Shell and British Petroleum are the two industries

that are taken into consideration. There are much information present in both of the sustainability

report but their initiative of reducing the problem of carbon emission is not present. Policy

details are present in both the report but the utilization of these policies is not given in the report.

In addition to that, the details about the all the crucial information related to controversy and

11BUSINESS, SOCIETY AND PLANET

adversity is not mentioned in the report. Thus, it is difficult to state whether their policy is

effective to maintain the sustainability of the earth. Lastly, another important aspect that is absent

from the report is the information about the code of conduct and data sheet of GRI index.

adversity is not mentioned in the report. Thus, it is difficult to state whether their policy is

effective to maintain the sustainability of the earth. Lastly, another important aspect that is absent

from the report is the information about the code of conduct and data sheet of GRI index.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.