Financial Analysis Report: University Financial Planning for Mr. Simon

VerifiedAdded on 2021/06/14

|16

|3936

|64

Report

AI Summary

This report presents a financial analysis of Mr. Simon and his family, focusing on his financial goals, current position, and risk profile. The analysis covers key areas such as superannuation, money management, insurance, savings, lifestyle changes, and property. The report recommends specific investment strategies, including diversification across short, medium, and long-term funds, debt management, and insurance to mitigate risks. The report also considers Mr. Simon's mother's health issues and the financial implications, providing tailored advice for achieving his goals, including saving for his niece's education and ensuring long-term financial stability. The report also includes an investment risk profile based on different investment strategies.

Financial Analysis

2018

2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: May 12, 2018.

1 | P a g e

By student name

Professor

University

Date: May 12, 2018.

1 | P a g e

2

Executive summary

We are going to do financial analysis of Mr. Simon and bob and their family it contains the goals and current

financial position of Mr Simon. In which we can make analysis of their goals as per the priority of client. After that

we recommend the proper strategy to Mr. Simon to achieve their desire objective and goals. Mr Simone is an

individual who is seeking financial help to manage his funds and in order to provide long term support to his

family. The same can be extracted with the help of experts and analysts and he wants the same in this assignment.

For that we do an analysis of requirement and risk profile and how much risk are involve on such investment

strategy. The client has a lot of problems that they need to deal with and the prospects with respect to overall

investment be a criterion that can be considered based on which the client can make little money which he can use

to satisfy his long-term needs. Financial analysis involves analysis of the overall aspect with respect to accounting

and finance of an individual and the probable benefits that they can use if they can manage their finance

effectively. As a financial planner the overall information with respect to the client has been extracted and

important points have been considered that will play an important role in influencing the overall profit the client

will make. This assignment will also contain illustrations based on the recommended strategies’ and how the client

will benefit from the same, based on their investment decisions and risk-taking capabilities. The market is always

fluctuating sometimes the returns are high and some times it is not that much enough to suffice the needs of the

people. It is very important that smart decisions should be taken else it might lead to heavy losses, thus when it

comes to market analysis decisions should be based on overall research that would help the individual in making

use of the funds that they have. We have seen that there are so many areas in which people can invest and there

are so many ways which they can follow to earn money. There comes the importance of financial planning in

picture. When people are aware that in future they would need money, they should take steps from today based

on which they can make their future return viable and for that they need to invest in various sources of income,

that includes stocks, bonds, and other different financial instruments. The role of a financial planner is to study the

overall current position of the client and get all information about his goals and based on that provide him with

methods that can earn him required returns for the company. So we see that generating income is not a tough task

but planning for the same requires effort and time and that can only be put by when you have experience. In this

case we are studying about Simone and the various ways in which he can earn income, based on the goals that he

needs to achieve.

2 | P a g e

Executive summary

We are going to do financial analysis of Mr. Simon and bob and their family it contains the goals and current

financial position of Mr Simon. In which we can make analysis of their goals as per the priority of client. After that

we recommend the proper strategy to Mr. Simon to achieve their desire objective and goals. Mr Simone is an

individual who is seeking financial help to manage his funds and in order to provide long term support to his

family. The same can be extracted with the help of experts and analysts and he wants the same in this assignment.

For that we do an analysis of requirement and risk profile and how much risk are involve on such investment

strategy. The client has a lot of problems that they need to deal with and the prospects with respect to overall

investment be a criterion that can be considered based on which the client can make little money which he can use

to satisfy his long-term needs. Financial analysis involves analysis of the overall aspect with respect to accounting

and finance of an individual and the probable benefits that they can use if they can manage their finance

effectively. As a financial planner the overall information with respect to the client has been extracted and

important points have been considered that will play an important role in influencing the overall profit the client

will make. This assignment will also contain illustrations based on the recommended strategies’ and how the client

will benefit from the same, based on their investment decisions and risk-taking capabilities. The market is always

fluctuating sometimes the returns are high and some times it is not that much enough to suffice the needs of the

people. It is very important that smart decisions should be taken else it might lead to heavy losses, thus when it

comes to market analysis decisions should be based on overall research that would help the individual in making

use of the funds that they have. We have seen that there are so many areas in which people can invest and there

are so many ways which they can follow to earn money. There comes the importance of financial planning in

picture. When people are aware that in future they would need money, they should take steps from today based

on which they can make their future return viable and for that they need to invest in various sources of income,

that includes stocks, bonds, and other different financial instruments. The role of a financial planner is to study the

overall current position of the client and get all information about his goals and based on that provide him with

methods that can earn him required returns for the company. So we see that generating income is not a tough task

but planning for the same requires effort and time and that can only be put by when you have experience. In this

case we are studying about Simone and the various ways in which he can earn income, based on the goals that he

needs to achieve.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Introduction………..………………………………………………………………….....................................................4

Analysis…..…………………………………………………………………………………………………………………..……….……4

Conclusion…..………………………………………………………………………………………………………………..……….…12

References.....……………………………………………………………..................................................................15

3 | P a g e

Contents

Introduction………..………………………………………………………………….....................................................4

Analysis…..…………………………………………………………………………………………………………………..……….……4

Conclusion…..………………………………………………………………………………………………………………..……….…12

References.....……………………………………………………………..................................................................15

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

GOAL DISCUSSION AND CURRENT FINANCIAL POSITION

In this assignment we are discussing the financial position of Simone and what are the possible options

that he has which will help him in managing his funds that he can use for future reference. Given below

are the possible goals for Simone that he has in his mind, with repsect to long term and short term areas

and what is his current financial position that is affecting his financial needs.So the same has been

applied in case of Simone and his financial position.Later we will suggest the strategy based on that

goals that can help Simone in the future to fulfil all his responsibility and reach to a position where he

can support himself and his life (Anon., 2017).

Analysis

1. Superannuation fund

Simon would like to get his super sorted into just one fund, that’s easy to track and based on how he wants it

invested. Simon does not want to invest in more funds because he is stick on one fund but the Bob does not want

to advice to stick on only 1 fund which Mr. Simon has following some other risk also and other area to manage. As

a financial advisory it is good to invest in all the portfolio rather than to investing in 1 fund. If we invest in some

other fund our risk will reduce and client is able to achieve their objective (Abbott & Kantor, 2017).

2. Money Management

In this Mr. Simon want to manage their money by paying off their debt faster and do a better job” with

their credit card and car loan. Strategy of Mr Simon is good because if we pay our debt than we don’t

have risk, so that we manage our fund very well and we do some another job to manage our fund. If we

want to risk free than we must pay our car loan also along with our debt.

3. Insurance and protection

4 | P a g e

Introduction

GOAL DISCUSSION AND CURRENT FINANCIAL POSITION

In this assignment we are discussing the financial position of Simone and what are the possible options

that he has which will help him in managing his funds that he can use for future reference. Given below

are the possible goals for Simone that he has in his mind, with repsect to long term and short term areas

and what is his current financial position that is affecting his financial needs.So the same has been

applied in case of Simone and his financial position.Later we will suggest the strategy based on that

goals that can help Simone in the future to fulfil all his responsibility and reach to a position where he

can support himself and his life (Anon., 2017).

Analysis

1. Superannuation fund

Simon would like to get his super sorted into just one fund, that’s easy to track and based on how he wants it

invested. Simon does not want to invest in more funds because he is stick on one fund but the Bob does not want

to advice to stick on only 1 fund which Mr. Simon has following some other risk also and other area to manage. As

a financial advisory it is good to invest in all the portfolio rather than to investing in 1 fund. If we invest in some

other fund our risk will reduce and client is able to achieve their objective (Abbott & Kantor, 2017).

2. Money Management

In this Mr. Simon want to manage their money by paying off their debt faster and do a better job” with

their credit card and car loan. Strategy of Mr Simon is good because if we pay our debt than we don’t

have risk, so that we manage our fund very well and we do some another job to manage our fund. If we

want to risk free than we must pay our car loan also along with our debt.

3. Insurance and protection

4 | P a g e

5

Mr. Simon and bob both exercise daily and feel fit and healthy They have had no significant injuries or

health issues in the past and aren’t concerned about insurance. It is advisable to Mr. Simon and bob to take

medical insurance to avoid any kind of medical related risk in future despite they are doing exercise and

they are physically fit they must take medical insurance because health is the most important assets of

any individual. We must protect it (Alexander, 2016).

4. Savings and Investment

Mr. Bob would love to help his niece with his high school cost approx. ($ 50000 in 2027) for that we

need to invest in our portfolio to get the desire return in 2027. But before this aspect we need to thing

about Simon’s mom_ Gloria who is suffering from cancer, she is the most priority than this.

5. Life style Change

Simons’ mum –Gloria is terminally ill that Mr. Simon and Bob need some fund for their mom’s treatment because

She does not have any other assets. Hence Mr. Simon and bob will invest some money for long term so that

they cannot scarifies their life style after retirement (Boghossian, 2017).

6. Home and property

With respect to the house property we see that currently renting a two-bedroom top floor unit. Bob

and Simon both feel renting suits their lifestyle as they don’t want to be ‘tied down’ to a mortgage They

understand that financially this could be a detriment in the long term but feel their lifestyle and the

flexibility that comes with being “mortgage free” is more important. yes, if you don’t want to scarify

their life style than you must be mortgage free for that this strategy is best. i.e. rent out vacate flat

despite mortgaging the same (Chariri, 2017).

Strategy Discussion

1. We have recommended Mr. Simon to invest in all the 3-super shorted fund i.e. on short

term and medium and long-term fund. He needs to invest $ 30000 in short term fund be

short involve higher risk rather than the long term but Mr. Simon needs funds after 2 years

on the death of his mother, so for that he invests more amount in short term despite higher

risk on such fund. Further he need to invest $ 10000 in medium term fund because medium

term has the moderate risk so can invest little more than short term. Further the balance $

5 | P a g e

Mr. Simon and bob both exercise daily and feel fit and healthy They have had no significant injuries or

health issues in the past and aren’t concerned about insurance. It is advisable to Mr. Simon and bob to take

medical insurance to avoid any kind of medical related risk in future despite they are doing exercise and

they are physically fit they must take medical insurance because health is the most important assets of

any individual. We must protect it (Alexander, 2016).

4. Savings and Investment

Mr. Bob would love to help his niece with his high school cost approx. ($ 50000 in 2027) for that we

need to invest in our portfolio to get the desire return in 2027. But before this aspect we need to thing

about Simon’s mom_ Gloria who is suffering from cancer, she is the most priority than this.

5. Life style Change

Simons’ mum –Gloria is terminally ill that Mr. Simon and Bob need some fund for their mom’s treatment because

She does not have any other assets. Hence Mr. Simon and bob will invest some money for long term so that

they cannot scarifies their life style after retirement (Boghossian, 2017).

6. Home and property

With respect to the house property we see that currently renting a two-bedroom top floor unit. Bob

and Simon both feel renting suits their lifestyle as they don’t want to be ‘tied down’ to a mortgage They

understand that financially this could be a detriment in the long term but feel their lifestyle and the

flexibility that comes with being “mortgage free” is more important. yes, if you don’t want to scarify

their life style than you must be mortgage free for that this strategy is best. i.e. rent out vacate flat

despite mortgaging the same (Chariri, 2017).

Strategy Discussion

1. We have recommended Mr. Simon to invest in all the 3-super shorted fund i.e. on short

term and medium and long-term fund. He needs to invest $ 30000 in short term fund be

short involve higher risk rather than the long term but Mr. Simon needs funds after 2 years

on the death of his mother, so for that he invests more amount in short term despite higher

risk on such fund. Further he need to invest $ 10000 in medium term fund because medium

term has the moderate risk so can invest little more than short term. Further the balance $

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

10000 we invest in long term so that we can achieve our long-term goal in future (YUAN,

2018).

2. It is recommended to Mr. Simon to pay off their debt because goal of Simon is they don’t

want to take risk. so, for that they need to pay off their debt $ 30000 (car loan and credit

card)

3. It is advisable to take medical insurance because health is the most important assets of any

individual. Further in the present case Mr. Simon and bob can do the exercise to stay fit,

despite the current position it is advisable to take medical insurance for future. Long term

insurance policies are more recommendable rather than the short term or medium term

because the more you get old the more health issue of individuals are beginning generally

so for that the long-term policies a are recommendable (Coate & Mitschow, 2017).

4. Mr. Bob want to gift of $ 50000 to her niece on her birthday which is on 2027. So, it is

recommendable to invest in long term strategy because he needs fund after 5 years for that

long-term fund is more advisable (Ghofiqi, 2018).

5. Simon’s mum has recently been diagnosing terminally ill and expecting to pass away within

2 years, Mr. Simon needs $ 400000 after 2 years. Mr. Simon is expected to receive his short-

term superannuation fund within 2 years and he is advisable to invest on some more money

in short term fund plan to meet the expenses to death of his mother (Iggers, 2018).

Investment Risk profile

1. Short term investment means Protection of capital or certainty of income is your only

objective. You do not wish to attain higher returns if your capital is at risk. It consists the

100% growth and no score.

2. Conservative investment means You are a defensive investor. You are willing to consider

less risky assets; mainly cash only and some fixed interest investments. You are

6 | P a g e

10000 we invest in long term so that we can achieve our long-term goal in future (YUAN,

2018).

2. It is recommended to Mr. Simon to pay off their debt because goal of Simon is they don’t

want to take risk. so, for that they need to pay off their debt $ 30000 (car loan and credit

card)

3. It is advisable to take medical insurance because health is the most important assets of any

individual. Further in the present case Mr. Simon and bob can do the exercise to stay fit,

despite the current position it is advisable to take medical insurance for future. Long term

insurance policies are more recommendable rather than the short term or medium term

because the more you get old the more health issue of individuals are beginning generally

so for that the long-term policies a are recommendable (Coate & Mitschow, 2017).

4. Mr. Bob want to gift of $ 50000 to her niece on her birthday which is on 2027. So, it is

recommendable to invest in long term strategy because he needs fund after 5 years for that

long-term fund is more advisable (Ghofiqi, 2018).

5. Simon’s mum has recently been diagnosing terminally ill and expecting to pass away within

2 years, Mr. Simon needs $ 400000 after 2 years. Mr. Simon is expected to receive his short-

term superannuation fund within 2 years and he is advisable to invest on some more money

in short term fund plan to meet the expenses to death of his mother (Iggers, 2018).

Investment Risk profile

1. Short term investment means Protection of capital or certainty of income is your only

objective. You do not wish to attain higher returns if your capital is at risk. It consists the

100% growth and no score.

2. Conservative investment means You are a defensive investor. You are willing to consider

less risky assets; mainly cash only and some fixed interest investments. You are

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

prepared to accept lower returns to protect the value of your capital. The

recommended minimum investment term is 3 years. It consists the growth of 25% and

score of 50-110

3. Caution investment means You are a cautious investor seeking a combination of income

and growth, but risk must continue to be low. Therefore, you will maintain a greater

weighting to defensive assets within your portfolio, but will consider including some of

the less aggressive growth investments. Generally, you are willing to chase improved

short-term returns while accepting some, limited short-term volatility. The

recommended minimum investment term is 3 years. It involves the 40 % growth and

score of 111-160 (Norberg, 2018).

4. Moderately conservative investment means You are an investor seeking a combination

of income and growth from your investment portfolio. Generally, you are willing to

chase medium to long-term goals while accepting the risk of short to medium-term

negative returns. Your investment mix is likely to include an equal mix of the defensive

assets and growth assets such as equities and property. The recommended minimum

investment term is 3 years. It consists of growth of 55% and score of 161- 210 (Webster,

2017).

5. Balance investment means You are a growth investor. You are willing to consider assets

with higher volatility in the short-term (such as equities and property) to achieve capital

growth over the medium to longer term. Your investment mix will comprise a greater

share of growth assets. The recommended minimum investment term is 5 years. It

consists of growth of 70 % and score of 211- 260 (Vieira, et al., 2017).

6. The Moderately aggressive investment means You are a growth investor. You are

prepared to accept higher volatility in the short to medium term, your primary concern

is to accumulate growth assets over the long term. Your investment mix will spread

7 | P a g e

prepared to accept lower returns to protect the value of your capital. The

recommended minimum investment term is 3 years. It consists the growth of 25% and

score of 50-110

3. Caution investment means You are a cautious investor seeking a combination of income

and growth, but risk must continue to be low. Therefore, you will maintain a greater

weighting to defensive assets within your portfolio, but will consider including some of

the less aggressive growth investments. Generally, you are willing to chase improved

short-term returns while accepting some, limited short-term volatility. The

recommended minimum investment term is 3 years. It involves the 40 % growth and

score of 111-160 (Norberg, 2018).

4. Moderately conservative investment means You are an investor seeking a combination

of income and growth from your investment portfolio. Generally, you are willing to

chase medium to long-term goals while accepting the risk of short to medium-term

negative returns. Your investment mix is likely to include an equal mix of the defensive

assets and growth assets such as equities and property. The recommended minimum

investment term is 3 years. It consists of growth of 55% and score of 161- 210 (Webster,

2017).

5. Balance investment means You are a growth investor. You are willing to consider assets

with higher volatility in the short-term (such as equities and property) to achieve capital

growth over the medium to longer term. Your investment mix will comprise a greater

share of growth assets. The recommended minimum investment term is 5 years. It

consists of growth of 70 % and score of 211- 260 (Vieira, et al., 2017).

6. The Moderately aggressive investment means You are a growth investor. You are

prepared to accept higher volatility in the short to medium term, your primary concern

is to accumulate growth assets over the long term. Your investment mix will spread

7 | P a g e

8

across all asset sectors but will mainly consist of more aggressive investments minimum

investment term is 6 years it consists 85 % risk and score of 261- 310 (Wellmer, 2018).

7. Aggressive investment means Your primary objective is capital growth. You are an

aggressive growth investor and are prepared to compromise your portfolio balance to

pursue greater long-term returns. You are willing to accept higher levels of risk.

Fluctuation in capital is acceptable in the short-medium term for the greater potential

for wealth accumulation. Except for a minimal level of cash for liquidity purposes, your

investment mix will only consist of growth assets such as international and domestic

equities. The minimum investment term is 7 years. It consists 100% growth and score of

311-350 (Wellmer, 2018).

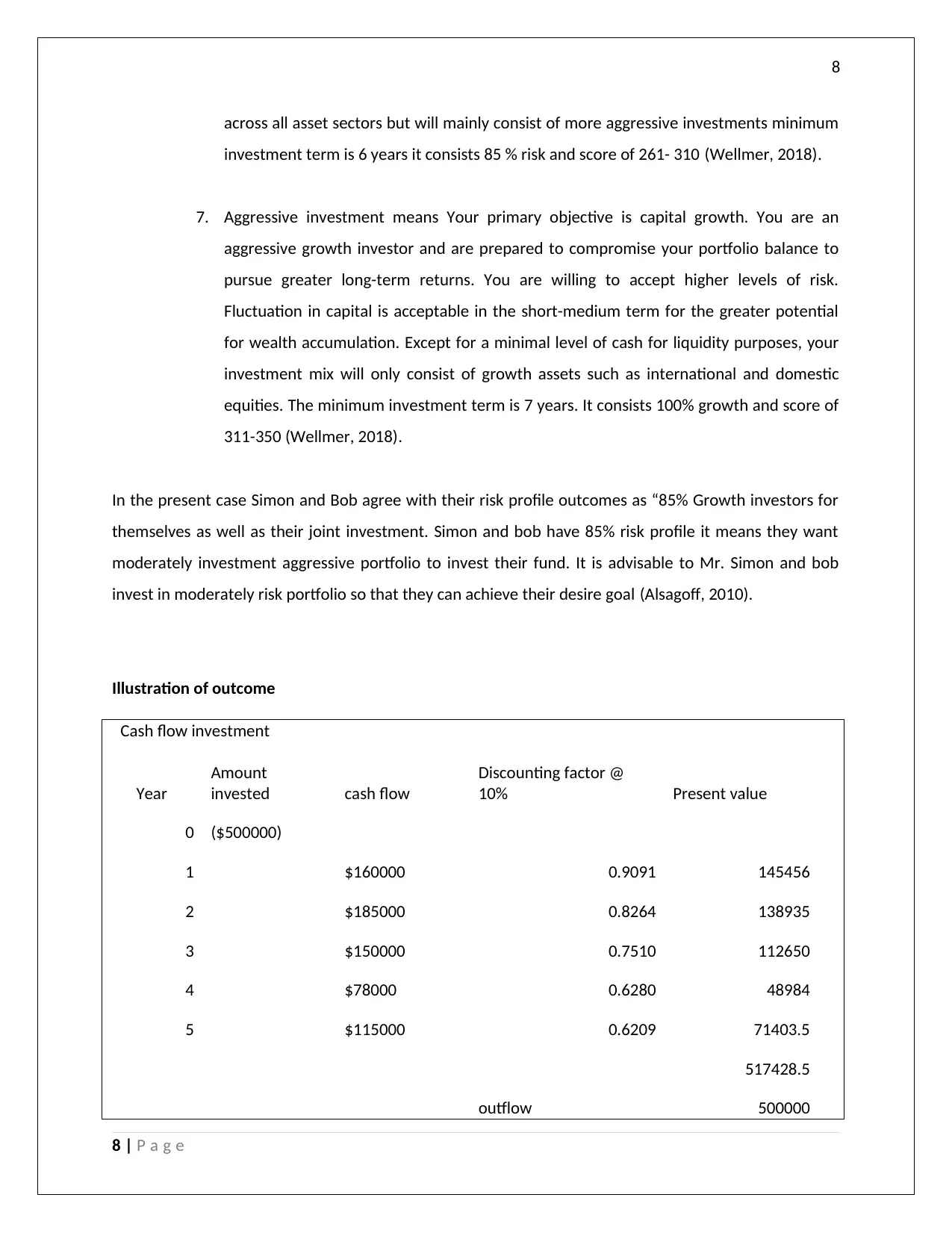

In the present case Simon and Bob agree with their risk profile outcomes as “85% Growth investors for

themselves as well as their joint investment. Simon and bob have 85% risk profile it means they want

moderately investment aggressive portfolio to invest their fund. It is advisable to Mr. Simon and bob

invest in moderately risk portfolio so that they can achieve their desire goal (Alsagoff, 2010).

Illustration of outcome

Cash flow investment

Year

Amount

invested cash flow

Discounting factor @

10% Present value

0 ($500000)

1 $160000 0.9091 145456

2 $185000 0.8264 138935

3 $150000 0.7510 112650

4 $78000 0.6280 48984

5 $115000 0.6209 71403.5

517428.5

outflow 500000

8 | P a g e

across all asset sectors but will mainly consist of more aggressive investments minimum

investment term is 6 years it consists 85 % risk and score of 261- 310 (Wellmer, 2018).

7. Aggressive investment means Your primary objective is capital growth. You are an

aggressive growth investor and are prepared to compromise your portfolio balance to

pursue greater long-term returns. You are willing to accept higher levels of risk.

Fluctuation in capital is acceptable in the short-medium term for the greater potential

for wealth accumulation. Except for a minimal level of cash for liquidity purposes, your

investment mix will only consist of growth assets such as international and domestic

equities. The minimum investment term is 7 years. It consists 100% growth and score of

311-350 (Wellmer, 2018).

In the present case Simon and Bob agree with their risk profile outcomes as “85% Growth investors for

themselves as well as their joint investment. Simon and bob have 85% risk profile it means they want

moderately investment aggressive portfolio to invest their fund. It is advisable to Mr. Simon and bob

invest in moderately risk portfolio so that they can achieve their desire goal (Alsagoff, 2010).

Illustration of outcome

Cash flow investment

Year

Amount

invested cash flow

Discounting factor @

10% Present value

0 ($500000)

1 $160000 0.9091 145456

2 $185000 0.8264 138935

3 $150000 0.7510 112650

4 $78000 0.6280 48984

5 $115000 0.6209 71403.5

517428.5

outflow 500000

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

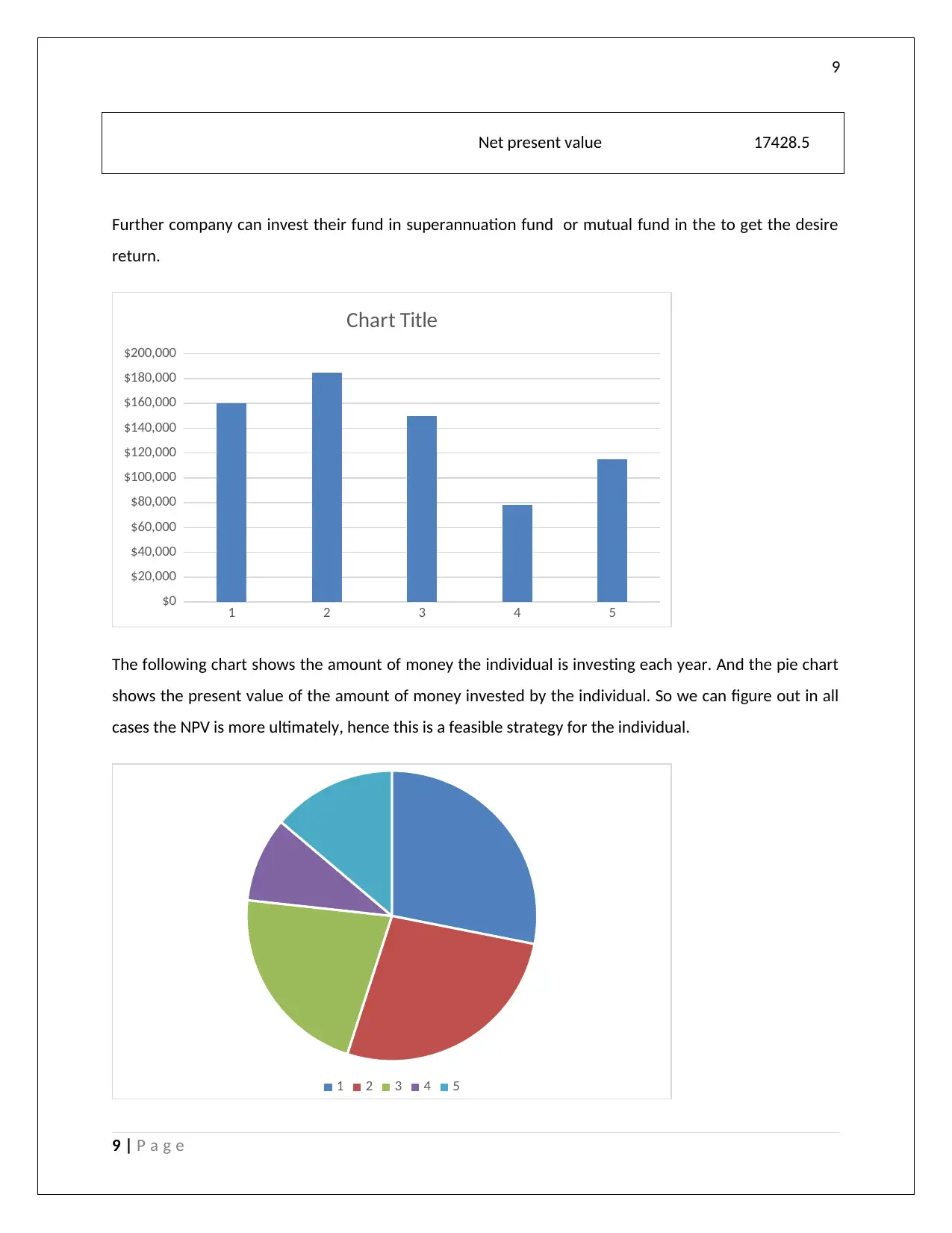

Net present value 17428.5

Further company can invest their fund in superannuation fund or mutual fund in the to get the desire

return.

1 2 3 4 5

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

Chart Title

The following chart shows the amount of money the individual is investing each year. And the pie chart

shows the present value of the amount of money invested by the individual. So we can figure out in all

cases the NPV is more ultimately, hence this is a feasible strategy for the individual.

1 2 3 4 5

9 | P a g e

Net present value 17428.5

Further company can invest their fund in superannuation fund or mutual fund in the to get the desire

return.

1 2 3 4 5

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

Chart Title

The following chart shows the amount of money the individual is investing each year. And the pie chart

shows the present value of the amount of money invested by the individual. So we can figure out in all

cases the NPV is more ultimately, hence this is a feasible strategy for the individual.

1 2 3 4 5

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Superannuation fund;- Superannuation fund are the arrangement of which is organise by the

government to assist the people to accumulated money for income and their desired result It is

compulsory for employers to make superannuation contributions for their employees on top of the

employees' wages and salaries. It is also referred to a company as a pension plan. Fund deposited in

superannuation fund will grow ever year. This fund does not contain any tax implication ever year or an

withdrawal of money.

Mutual fund;- A mutual fund is a professionally managed investment that pools money from many

investors to purchase securities These investors may be retail or institutional in nature.

Mutual funds have advantages and disadvantages compared to direct investing in individual securities.

The primary advantages of mutual funds are that they provide economies of scale, a higher level of

diversification, they provide liquidity, and they are managed by professional investors. Since it is mange

by professional it contain some professional fees (Durtschi, 2004).

There are 2 type of mutual fund exist in the market open ended and closed ended mutual fund. We can

hedge our fund with the help of mutual fund. Because this fund is mange by the professionals.

Risk Return profile;- we can prepare the risk return profile of individuals to through which we can

understand the calculated risk of the individual and base on such risk we can analysis the our portfolio.

We can select our best portfolio based on such above analysis. Any types of fund or stock consist the

following factor to analysis the such stock the factor is volatility, risk and co-relation between two stock,

co-efficient of variance between two stock. Volatility of any stock means how the stock will move into

both side i.e on positive side or on negative side basically we called it as variance. Square root of

variance is called standard deviation of any stock

Example;

1 Consider the following portfolio

P1 P2 P3 P4 P5 P6

Return

(%)

18 20 30 30 34 35

Risk (%) 7 6 10 11 11 11

Based on above portfolio of the stock find the efficient portfolio

10 | P a g e

Superannuation fund;- Superannuation fund are the arrangement of which is organise by the

government to assist the people to accumulated money for income and their desired result It is

compulsory for employers to make superannuation contributions for their employees on top of the

employees' wages and salaries. It is also referred to a company as a pension plan. Fund deposited in

superannuation fund will grow ever year. This fund does not contain any tax implication ever year or an

withdrawal of money.

Mutual fund;- A mutual fund is a professionally managed investment that pools money from many

investors to purchase securities These investors may be retail or institutional in nature.

Mutual funds have advantages and disadvantages compared to direct investing in individual securities.

The primary advantages of mutual funds are that they provide economies of scale, a higher level of

diversification, they provide liquidity, and they are managed by professional investors. Since it is mange

by professional it contain some professional fees (Durtschi, 2004).

There are 2 type of mutual fund exist in the market open ended and closed ended mutual fund. We can

hedge our fund with the help of mutual fund. Because this fund is mange by the professionals.

Risk Return profile;- we can prepare the risk return profile of individuals to through which we can

understand the calculated risk of the individual and base on such risk we can analysis the our portfolio.

We can select our best portfolio based on such above analysis. Any types of fund or stock consist the

following factor to analysis the such stock the factor is volatility, risk and co-relation between two stock,

co-efficient of variance between two stock. Volatility of any stock means how the stock will move into

both side i.e on positive side or on negative side basically we called it as variance. Square root of

variance is called standard deviation of any stock

Example;

1 Consider the following portfolio

P1 P2 P3 P4 P5 P6

Return

(%)

18 20 30 30 34 35

Risk (%) 7 6 10 11 11 11

Based on above portfolio of the stock find the efficient portfolio

10 | P a g e

11

Solution 1. P1 is inefficient because P2 can provide a higher return at

lower risk

2. P4 and P5 are in efficient because P6 can provide higher return at

same risk

3. P5 are in efficient because P6 can provide higher return at

same risk

Hence P2, P3 And P6 are efficient

portfolio

2 Out of efficient portfolio choose the optimum portfolio for an

investor

Solution Since No information are given about the investor level of risk aversion, we will choose

the optimum

portfolio as the one having the lowest co-efficient of

variance

Where co- efficient of variance means

CV= Standard deviation/ Mean*100

P2 CV= 6/20*100 30%

P3 CV= 10/30*100 33.33%

11 | P a g e

Solution 1. P1 is inefficient because P2 can provide a higher return at

lower risk

2. P4 and P5 are in efficient because P6 can provide higher return at

same risk

3. P5 are in efficient because P6 can provide higher return at

same risk

Hence P2, P3 And P6 are efficient

portfolio

2 Out of efficient portfolio choose the optimum portfolio for an

investor

Solution Since No information are given about the investor level of risk aversion, we will choose

the optimum

portfolio as the one having the lowest co-efficient of

variance

Where co- efficient of variance means

CV= Standard deviation/ Mean*100

P2 CV= 6/20*100 30%

P3 CV= 10/30*100 33.33%

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.