Financial Ratio Analysis of Singapore Airlines - MBA Finance Report

VerifiedAdded on 2023/04/06

|18

|4085

|283

Report

AI Summary

This report presents a comprehensive financial analysis of Singapore Airlines, comparing its performance against Air Asia using various financial ratios. The analysis covers the period of 2014-2018, examining profitability, liquidity, and cash flow. Key ratios such as current ratio, quick ratio, and cash conversion cycle are calculated and compared for both airlines. The report identifies the strengths and weaknesses of Singapore Airlines, particularly in terms of liquidity and operational efficiency, and provides recommendations for improvement. The study utilizes financial statements, including profit and loss accounts, balance sheets, and cash flow statements, to assess the financial health and stability of Singapore Airlines within the competitive Asian airline industry. Findings suggest that while Singapore Airlines maintains a strong brand image and revenue streams, it faces challenges in managing expenditures and improving its cash conversion cycle compared to Air Asia. This detailed analysis offers valuable insights for investors and stakeholders seeking to understand the financial dynamics of Singapore Airlines.

Running Head: Financial Ratios

0

Financial Ratios

Report

Student Name

3/15/2019

0

Financial Ratios

Report

Student Name

3/15/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Ratios

1

Executive Summary

Financial analysis is a key to know more about company financial position and to take necessary

decision of investment. In this assignment a company is to be selected which is listed on main

board of any stock exchange within Asian region hence Singapore Airlines has been selected

which is listed in Singapore stock exchange. Singapore Airlines is amongst the well performed

companies in airline industry with strong financial position along with that company has good

brand image and investment strategies. In this report Singapore Airlines financial analysis is

been carried on with its competitor Air Asia and comparison is done on different aspects to better

know the position of Singapore Airlines in the market whether firm gives higher return on

investment to the shareholders or not. The study is based on comparison of Singapore Airlines

position in the industry with its competitor. All this is done using the various financial ratios

such as liquidity ratio, leverage ratio and cash flow statement of the company. On the basis of

study some major findings and recommendations are given followed by a brief conclusion.

1

Executive Summary

Financial analysis is a key to know more about company financial position and to take necessary

decision of investment. In this assignment a company is to be selected which is listed on main

board of any stock exchange within Asian region hence Singapore Airlines has been selected

which is listed in Singapore stock exchange. Singapore Airlines is amongst the well performed

companies in airline industry with strong financial position along with that company has good

brand image and investment strategies. In this report Singapore Airlines financial analysis is

been carried on with its competitor Air Asia and comparison is done on different aspects to better

know the position of Singapore Airlines in the market whether firm gives higher return on

investment to the shareholders or not. The study is based on comparison of Singapore Airlines

position in the industry with its competitor. All this is done using the various financial ratios

such as liquidity ratio, leverage ratio and cash flow statement of the company. On the basis of

study some major findings and recommendations are given followed by a brief conclusion.

Financial Ratios

2

Table of Contents

Executive Summary.........................................................................................................................1

Introduction......................................................................................................................................3

Financial Analysis...........................................................................................................................4

Financial Performance.................................................................................................................4

Liquidity analysis and cash conversion cycle..............................................................................8

Debt and Capital Structure Analysis............................................................................................9

Customer Profitability Analysis.................................................................................................10

Level of working capital............................................................................................................11

Findings.........................................................................................................................................12

Recommendations..........................................................................................................................12

Limitations.....................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

2

Table of Contents

Executive Summary.........................................................................................................................1

Introduction......................................................................................................................................3

Financial Analysis...........................................................................................................................4

Financial Performance.................................................................................................................4

Liquidity analysis and cash conversion cycle..............................................................................8

Debt and Capital Structure Analysis............................................................................................9

Customer Profitability Analysis.................................................................................................10

Level of working capital............................................................................................................11

Findings.........................................................................................................................................12

Recommendations..........................................................................................................................12

Limitations.....................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Ratios

3

Introduction

Singapore Airlines Limited is founded in 1972 and owned by the government of Singapore with

its hub at Singapore Changi Airport. The airline showed revenue of $ 14869 million in 2017

from its major operations. Singapore Airlines have some subsidiaries related to repair and

overhaul and in 2017 these group includes 25 subsidiaries, 35 associates and two ventures by

Singapore Airlines. Operations of all these subsidiaries cover 40 countries at 135 destinations

(SingaporeAir, 2019).

Singapore Airlines is listed in Stock Exchange of Singapore as SGX: C6L. Singapore Airlines is

doing very well in the airline industry and ranked 4th amongst its top 10 competitors in term of

revenue. On an average the airline industry in Singapore earns 18.6 billion but from last three

quarters the revenue of Singapore Airlines is declining or decreased by 30%, in Q1 revenue was

$4.2B, in Q2 it was $3.8B and in Q3 it declined to $3B (Bloomberg, 2018). The company has

achieved sustainable competitive advantage and has consistently given high performance against

its competitors throughout its three and half decade history because of its incompatible

investment strategies and organization model (Heracleous & Wirtz, 2012).

The airlines sector in Asian region is growing rapidly, passengers traffic is increased by 10% in

last year. However, competition in this industry became high due to attractive market for the

investors. Singapore Airlines operates in high scale in Asia region due to that it has to face tough

competition mainly from Air Asia as they have market share of USD 8,229 as compare to USD

9,223 of Singapore Airlines (Raynes & Tsui, 2019). Other competitors for the Singapore Airlines

are Virgin America and Malaysian airlines.

The objectives of this study are to compare the performance of Singapore Airlines with its

biggest competitor Air Asia to set the benchmark for company. Other one is to know the area of

improvement that offer the most promising future potential and to analyze the stability and

profitability of airline for the long run for investors.

3

Introduction

Singapore Airlines Limited is founded in 1972 and owned by the government of Singapore with

its hub at Singapore Changi Airport. The airline showed revenue of $ 14869 million in 2017

from its major operations. Singapore Airlines have some subsidiaries related to repair and

overhaul and in 2017 these group includes 25 subsidiaries, 35 associates and two ventures by

Singapore Airlines. Operations of all these subsidiaries cover 40 countries at 135 destinations

(SingaporeAir, 2019).

Singapore Airlines is listed in Stock Exchange of Singapore as SGX: C6L. Singapore Airlines is

doing very well in the airline industry and ranked 4th amongst its top 10 competitors in term of

revenue. On an average the airline industry in Singapore earns 18.6 billion but from last three

quarters the revenue of Singapore Airlines is declining or decreased by 30%, in Q1 revenue was

$4.2B, in Q2 it was $3.8B and in Q3 it declined to $3B (Bloomberg, 2018). The company has

achieved sustainable competitive advantage and has consistently given high performance against

its competitors throughout its three and half decade history because of its incompatible

investment strategies and organization model (Heracleous & Wirtz, 2012).

The airlines sector in Asian region is growing rapidly, passengers traffic is increased by 10% in

last year. However, competition in this industry became high due to attractive market for the

investors. Singapore Airlines operates in high scale in Asia region due to that it has to face tough

competition mainly from Air Asia as they have market share of USD 8,229 as compare to USD

9,223 of Singapore Airlines (Raynes & Tsui, 2019). Other competitors for the Singapore Airlines

are Virgin America and Malaysian airlines.

The objectives of this study are to compare the performance of Singapore Airlines with its

biggest competitor Air Asia to set the benchmark for company. Other one is to know the area of

improvement that offer the most promising future potential and to analyze the stability and

profitability of airline for the long run for investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Ratios

4

4

Financial Ratios

5

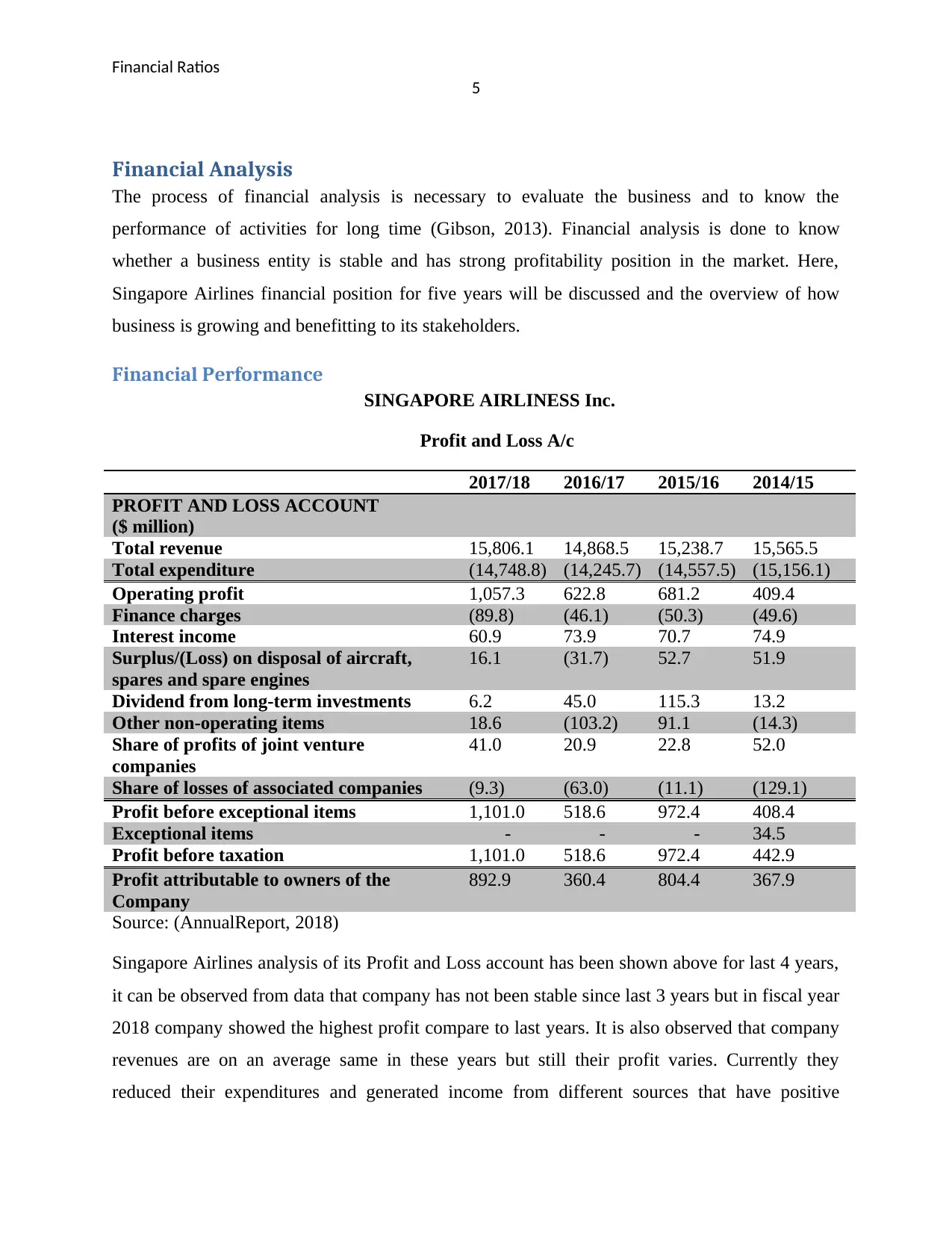

Financial Analysis

The process of financial analysis is necessary to evaluate the business and to know the

performance of activities for long time (Gibson, 2013). Financial analysis is done to know

whether a business entity is stable and has strong profitability position in the market. Here,

Singapore Airlines financial position for five years will be discussed and the overview of how

business is growing and benefitting to its stakeholders.

Financial Performance

SINGAPORE AIRLINESS Inc.

Profit and Loss A/c

2017/18 2016/17 2015/16 2014/15

PROFIT AND LOSS ACCOUNT

($ million)

Total revenue 15,806.1 14,868.5 15,238.7 15,565.5

Total expenditure (14,748.8) (14,245.7) (14,557.5) (15,156.1)

Operating profit 1,057.3 622.8 681.2 409.4

Finance charges (89.8) (46.1) (50.3) (49.6)

Interest income 60.9 73.9 70.7 74.9

Surplus/(Loss) on disposal of aircraft,

spares and spare engines

16.1 (31.7) 52.7 51.9

Dividend from long-term investments 6.2 45.0 115.3 13.2

Other non-operating items 18.6 (103.2) 91.1 (14.3)

Share of profits of joint venture

companies

41.0 20.9 22.8 52.0

Share of losses of associated companies (9.3) (63.0) (11.1) (129.1)

Profit before exceptional items 1,101.0 518.6 972.4 408.4

Exceptional items - - - 34.5

Profit before taxation 1,101.0 518.6 972.4 442.9

Profit attributable to owners of the

Company

892.9 360.4 804.4 367.9

Source: (AnnualReport, 2018)

Singapore Airlines analysis of its Profit and Loss account has been shown above for last 4 years,

it can be observed from data that company has not been stable since last 3 years but in fiscal year

2018 company showed the highest profit compare to last years. It is also observed that company

revenues are on an average same in these years but still their profit varies. Currently they

reduced their expenditures and generated income from different sources that have positive

5

Financial Analysis

The process of financial analysis is necessary to evaluate the business and to know the

performance of activities for long time (Gibson, 2013). Financial analysis is done to know

whether a business entity is stable and has strong profitability position in the market. Here,

Singapore Airlines financial position for five years will be discussed and the overview of how

business is growing and benefitting to its stakeholders.

Financial Performance

SINGAPORE AIRLINESS Inc.

Profit and Loss A/c

2017/18 2016/17 2015/16 2014/15

PROFIT AND LOSS ACCOUNT

($ million)

Total revenue 15,806.1 14,868.5 15,238.7 15,565.5

Total expenditure (14,748.8) (14,245.7) (14,557.5) (15,156.1)

Operating profit 1,057.3 622.8 681.2 409.4

Finance charges (89.8) (46.1) (50.3) (49.6)

Interest income 60.9 73.9 70.7 74.9

Surplus/(Loss) on disposal of aircraft,

spares and spare engines

16.1 (31.7) 52.7 51.9

Dividend from long-term investments 6.2 45.0 115.3 13.2

Other non-operating items 18.6 (103.2) 91.1 (14.3)

Share of profits of joint venture

companies

41.0 20.9 22.8 52.0

Share of losses of associated companies (9.3) (63.0) (11.1) (129.1)

Profit before exceptional items 1,101.0 518.6 972.4 408.4

Exceptional items - - - 34.5

Profit before taxation 1,101.0 518.6 972.4 442.9

Profit attributable to owners of the

Company

892.9 360.4 804.4 367.9

Source: (AnnualReport, 2018)

Singapore Airlines analysis of its Profit and Loss account has been shown above for last 4 years,

it can be observed from data that company has not been stable since last 3 years but in fiscal year

2018 company showed the highest profit compare to last years. It is also observed that company

revenues are on an average same in these years but still their profit varies. Currently they

reduced their expenditures and generated income from different sources that have positive

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Ratios

6

impact in profits. Profit before taxation is doubled during this year from last year profit that was

$518.6 million. Operating profit of the company shown an improvement but expenditures of

Singapore airlines are more which leads to decline in the operating profit as company has

earning good revenue its means its sales and operations are in larger scale if they cut their cost it

can improve their operating profit or overall profits (Singaporeair, 2018).

SINGAPORE AIRLINESS Inc.

Balance Sheet

2017/18 2016/17 2015/16 2014/15

STATEMENT OF FINANCIAL POSITION ($

million)

Share capital 1,856.1 1,856.1 1,856.1 1,856.1

Treasury shares (183.5) (194.7) (381.5) (326.3)

Capital reserve (139.4) (147.6) (129.2) 215.9

Foreign currency translation reserve (175.4) (123.7) (151.3) (135.7)

Share-based compensation reserve 79.5 88.5 123.7 113.2

Fair value reserve 313.5 (234.4) (498.6) (706.2)

General reserve 12,500.4 11,838.8 11,935.5 11,446.6

Equity attributable to owners of the Company 14,251.2 13,083.0 12,754.7 12,463.6

Non-controlling interests 368.1 387.2 378.2 466.5

Total equity 14,619.3 13,470.2 13,132.9 12,930.1

Property, plant and equipment 19,824.6 16,433.3 14,143.5 13,523.2

Intangible assets 435.3 423.5 515.8 497.6

Associated companies 1,048.8 1,056.9 901.9 922.2

Joint venture companies 150.6 160.2 156.3 167.9

Long-term investments 346.0 405.7 773.1 927.6

Other non-current assets 775.6 540.4 562.0 630.2

Current assets 4,968.3 5,700.0 6,794.0 7,252.9

Total assets 27,549.2 24,720.0 23,846.6 23,921.6

Deferred account 123.3 234.5 255.0 141.7

Deferred taxation 2,122.7 1,890.5 1,681.7 1,599.6

Other non-current liabilities 4,134.5 2,836.2 2,289.8 2,609.8

Current liabilities 6,549.4 6,288.6 6,487.2 6,640.4

Total liabilities 12,929.9 11,249.8 10,713.7 10,991.5

Net assets 14,619.3 13,470.2 13,132.9 12,930.1

Source: (AnnualReport, 2018)

On the basis of above information from balance sheet of the company it is analyzed that assets

and liabilities of the company has been increasing from last 4 years but their current assets are

6

impact in profits. Profit before taxation is doubled during this year from last year profit that was

$518.6 million. Operating profit of the company shown an improvement but expenditures of

Singapore airlines are more which leads to decline in the operating profit as company has

earning good revenue its means its sales and operations are in larger scale if they cut their cost it

can improve their operating profit or overall profits (Singaporeair, 2018).

SINGAPORE AIRLINESS Inc.

Balance Sheet

2017/18 2016/17 2015/16 2014/15

STATEMENT OF FINANCIAL POSITION ($

million)

Share capital 1,856.1 1,856.1 1,856.1 1,856.1

Treasury shares (183.5) (194.7) (381.5) (326.3)

Capital reserve (139.4) (147.6) (129.2) 215.9

Foreign currency translation reserve (175.4) (123.7) (151.3) (135.7)

Share-based compensation reserve 79.5 88.5 123.7 113.2

Fair value reserve 313.5 (234.4) (498.6) (706.2)

General reserve 12,500.4 11,838.8 11,935.5 11,446.6

Equity attributable to owners of the Company 14,251.2 13,083.0 12,754.7 12,463.6

Non-controlling interests 368.1 387.2 378.2 466.5

Total equity 14,619.3 13,470.2 13,132.9 12,930.1

Property, plant and equipment 19,824.6 16,433.3 14,143.5 13,523.2

Intangible assets 435.3 423.5 515.8 497.6

Associated companies 1,048.8 1,056.9 901.9 922.2

Joint venture companies 150.6 160.2 156.3 167.9

Long-term investments 346.0 405.7 773.1 927.6

Other non-current assets 775.6 540.4 562.0 630.2

Current assets 4,968.3 5,700.0 6,794.0 7,252.9

Total assets 27,549.2 24,720.0 23,846.6 23,921.6

Deferred account 123.3 234.5 255.0 141.7

Deferred taxation 2,122.7 1,890.5 1,681.7 1,599.6

Other non-current liabilities 4,134.5 2,836.2 2,289.8 2,609.8

Current liabilities 6,549.4 6,288.6 6,487.2 6,640.4

Total liabilities 12,929.9 11,249.8 10,713.7 10,991.5

Net assets 14,619.3 13,470.2 13,132.9 12,930.1

Source: (AnnualReport, 2018)

On the basis of above information from balance sheet of the company it is analyzed that assets

and liabilities of the company has been increasing from last 4 years but their current assets are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Ratios

7

less than current liabilities which somehow affect the liquidity position of the company and

indicate that company will face some trouble in meeting its immediate short term liabilities. It is

also monitored from data that Singapore Airlines has been able to increase the equity of the

company, assets of the company are also increased which clearly showed that company has

strong financial position in the industry compare to its competitor Air Asia whereas its

competitor showed an operating loss of $50 million in FY18 due to their increasing expenses in

high fuel cost (Hashim, 2019).

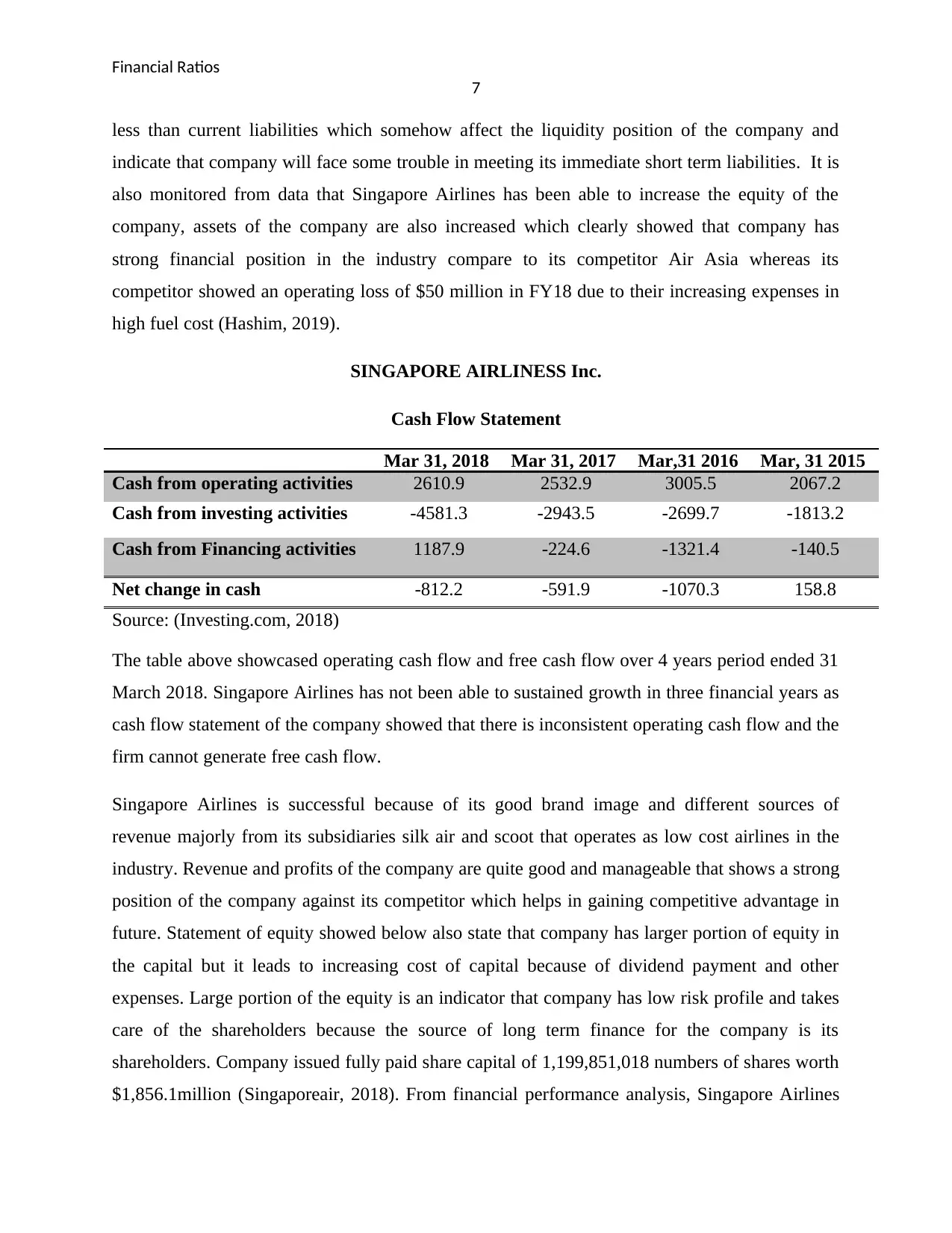

SINGAPORE AIRLINESS Inc.

Cash Flow Statement

Mar 31, 2018 Mar 31, 2017 Mar,31 2016 Mar, 31 2015

Cash from operating activities 2610.9 2532.9 3005.5 2067.2

Cash from investing activities -4581.3 -2943.5 -2699.7 -1813.2

Cash from Financing activities 1187.9 -224.6 -1321.4 -140.5

Net change in cash -812.2 -591.9 -1070.3 158.8

Source: (Investing.com, 2018)

The table above showcased operating cash flow and free cash flow over 4 years period ended 31

March 2018. Singapore Airlines has not been able to sustained growth in three financial years as

cash flow statement of the company showed that there is inconsistent operating cash flow and the

firm cannot generate free cash flow.

Singapore Airlines is successful because of its good brand image and different sources of

revenue majorly from its subsidiaries silk air and scoot that operates as low cost airlines in the

industry. Revenue and profits of the company are quite good and manageable that shows a strong

position of the company against its competitor which helps in gaining competitive advantage in

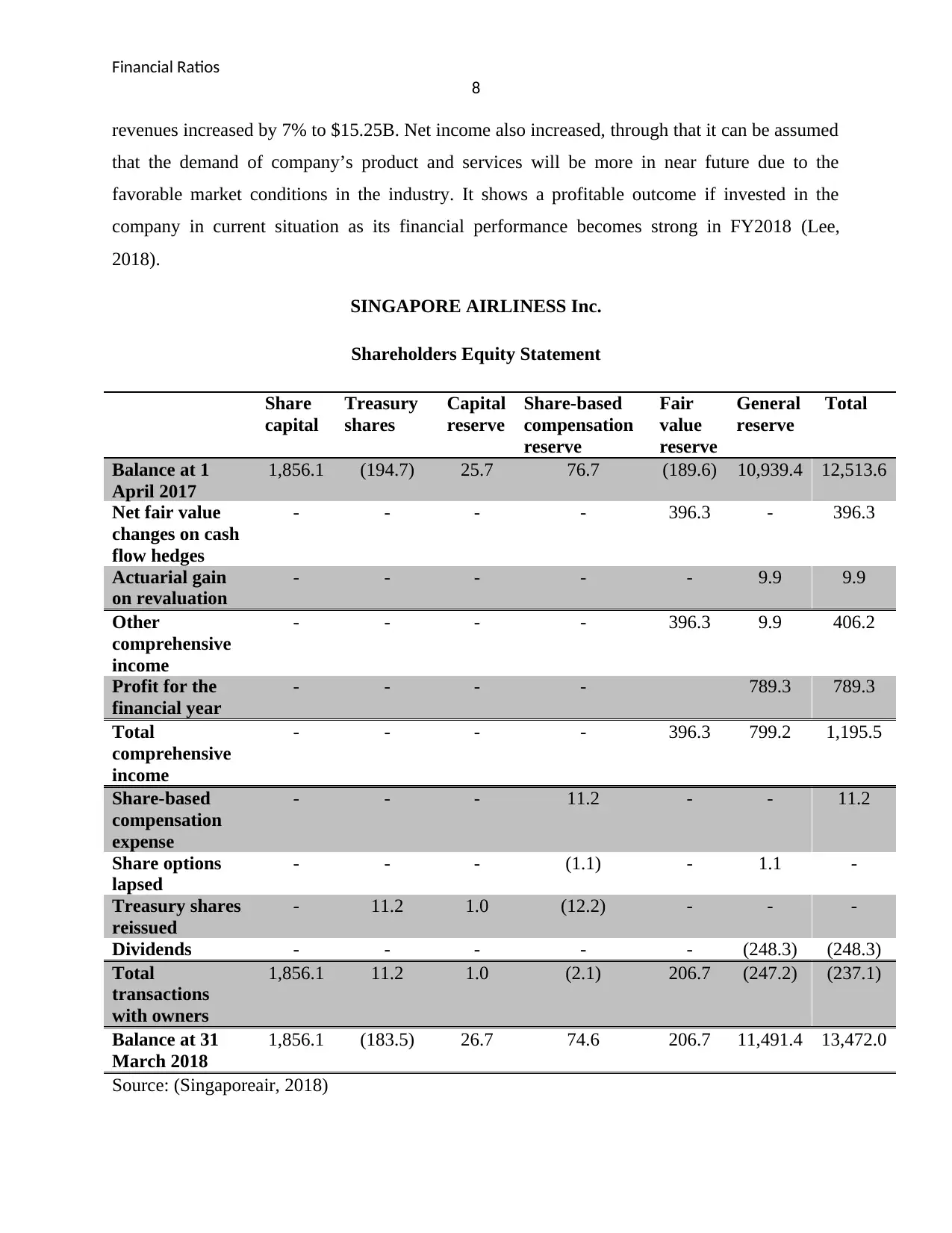

future. Statement of equity showed below also state that company has larger portion of equity in

the capital but it leads to increasing cost of capital because of dividend payment and other

expenses. Large portion of the equity is an indicator that company has low risk profile and takes

care of the shareholders because the source of long term finance for the company is its

shareholders. Company issued fully paid share capital of 1,199,851,018 numbers of shares worth

$1,856.1million (Singaporeair, 2018). From financial performance analysis, Singapore Airlines

7

less than current liabilities which somehow affect the liquidity position of the company and

indicate that company will face some trouble in meeting its immediate short term liabilities. It is

also monitored from data that Singapore Airlines has been able to increase the equity of the

company, assets of the company are also increased which clearly showed that company has

strong financial position in the industry compare to its competitor Air Asia whereas its

competitor showed an operating loss of $50 million in FY18 due to their increasing expenses in

high fuel cost (Hashim, 2019).

SINGAPORE AIRLINESS Inc.

Cash Flow Statement

Mar 31, 2018 Mar 31, 2017 Mar,31 2016 Mar, 31 2015

Cash from operating activities 2610.9 2532.9 3005.5 2067.2

Cash from investing activities -4581.3 -2943.5 -2699.7 -1813.2

Cash from Financing activities 1187.9 -224.6 -1321.4 -140.5

Net change in cash -812.2 -591.9 -1070.3 158.8

Source: (Investing.com, 2018)

The table above showcased operating cash flow and free cash flow over 4 years period ended 31

March 2018. Singapore Airlines has not been able to sustained growth in three financial years as

cash flow statement of the company showed that there is inconsistent operating cash flow and the

firm cannot generate free cash flow.

Singapore Airlines is successful because of its good brand image and different sources of

revenue majorly from its subsidiaries silk air and scoot that operates as low cost airlines in the

industry. Revenue and profits of the company are quite good and manageable that shows a strong

position of the company against its competitor which helps in gaining competitive advantage in

future. Statement of equity showed below also state that company has larger portion of equity in

the capital but it leads to increasing cost of capital because of dividend payment and other

expenses. Large portion of the equity is an indicator that company has low risk profile and takes

care of the shareholders because the source of long term finance for the company is its

shareholders. Company issued fully paid share capital of 1,199,851,018 numbers of shares worth

$1,856.1million (Singaporeair, 2018). From financial performance analysis, Singapore Airlines

Financial Ratios

8

revenues increased by 7% to $15.25B. Net income also increased, through that it can be assumed

that the demand of company’s product and services will be more in near future due to the

favorable market conditions in the industry. It shows a profitable outcome if invested in the

company in current situation as its financial performance becomes strong in FY2018 (Lee,

2018).

SINGAPORE AIRLINESS Inc.

Shareholders Equity Statement

Share

capital

Treasury

shares

Capital

reserve

Share-based

compensation

reserve

Fair

value

reserve

General

reserve

Total

Balance at 1

April 2017

1,856.1 (194.7) 25.7 76.7 (189.6) 10,939.4 12,513.6

Net fair value

changes on cash

flow hedges

- - - - 396.3 - 396.3

Actuarial gain

on revaluation

- - - - - 9.9 9.9

Other

comprehensive

income

- - - - 396.3 9.9 406.2

Profit for the

financial year

- - - - 789.3 789.3

Total

comprehensive

income

- - - - 396.3 799.2 1,195.5

Share-based

compensation

expense

- - - 11.2 - - 11.2

Share options

lapsed

- - - (1.1) - 1.1 -

Treasury shares

reissued

- 11.2 1.0 (12.2) - - -

Dividends - - - - - (248.3) (248.3)

Total

transactions

with owners

1,856.1 11.2 1.0 (2.1) 206.7 (247.2) (237.1)

Balance at 31

March 2018

1,856.1 (183.5) 26.7 74.6 206.7 11,491.4 13,472.0

Source: (Singaporeair, 2018)

8

revenues increased by 7% to $15.25B. Net income also increased, through that it can be assumed

that the demand of company’s product and services will be more in near future due to the

favorable market conditions in the industry. It shows a profitable outcome if invested in the

company in current situation as its financial performance becomes strong in FY2018 (Lee,

2018).

SINGAPORE AIRLINESS Inc.

Shareholders Equity Statement

Share

capital

Treasury

shares

Capital

reserve

Share-based

compensation

reserve

Fair

value

reserve

General

reserve

Total

Balance at 1

April 2017

1,856.1 (194.7) 25.7 76.7 (189.6) 10,939.4 12,513.6

Net fair value

changes on cash

flow hedges

- - - - 396.3 - 396.3

Actuarial gain

on revaluation

- - - - - 9.9 9.9

Other

comprehensive

income

- - - - 396.3 9.9 406.2

Profit for the

financial year

- - - - 789.3 789.3

Total

comprehensive

income

- - - - 396.3 799.2 1,195.5

Share-based

compensation

expense

- - - 11.2 - - 11.2

Share options

lapsed

- - - (1.1) - 1.1 -

Treasury shares

reissued

- 11.2 1.0 (12.2) - - -

Dividends - - - - - (248.3) (248.3)

Total

transactions

with owners

1,856.1 11.2 1.0 (2.1) 206.7 (247.2) (237.1)

Balance at 31

March 2018

1,856.1 (183.5) 26.7 74.6 206.7 11,491.4 13,472.0

Source: (Singaporeair, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Ratios

9

Liquidity analysis and cash conversion cycle

Singapore Airlines liquidity ratio analysis has been performed in comparison with its competitor

Air Asia. All these liquidity ratios are used to check the efficiency of a company and to know the

liquidity position that is how easily assets can be converted into cash in short run (Lee, et al.,

2009).

Singapore Airlines

Ratios Formulas 2017 2016 2015 2014

Current Ratio Current Assets/Current liabilities 0.76 0.90 1.04 1.09

Quick Ratio Total current assets – Total

Inventories/ Total current liabilities

0.73 0.88 1.02 1.06

Cash conversion cycle Days sales outstanding + Days

Inventory – Days Payable

-42.81 -61.34 -46.49 -38.69

(Reuters, 2018)

Air Asia

Ratios Formulas 2017 2016 2015 2014

Current Ratio Current Assets/Current liabilities 0.81 0.97 0.81 0.62

Quick Ratio Total current assets – Total Inventories/

Total current liabilities

0.80 0.96 0.81 0.61

Cash conversion

cycle

Days sales outstanding + Days

Inventory – Days Payable

-2.97 -19.95 -12.78 2.40

Source: (AirAsia, 2017)

The current ratio of Singapore Airlines is 0.76 which shows that the company would be unable to

pay off its obligations if due immediately and this is an indication that company is not in good

liquidity financial health. Mainly higher current ratio that is 2:1 proves better that means a

company can meet its liabilities in a year. In comparing the Singapore Airlines liquidity position

with its competitor Air Asia it is observed that in FY14 and FY15 Singapore Airlines showed a

good liquidity position but currently Air Asia has better position and would be liable to pay its

liabilities quickly.

Cash conversion cycle is calculated to know how fast a company converts its inventory into cash

receivables and the time it takes to pay its bills and its helps in measuring management

effectiveness of a company (Robinson, et al., 2015). The cash conversion cycle of the Singapore

Airlines shows a negative amount for four consecutive years which means the company is

generating revenue from customers on time and paying to its suppliers later. The negative cash

9

Liquidity analysis and cash conversion cycle

Singapore Airlines liquidity ratio analysis has been performed in comparison with its competitor

Air Asia. All these liquidity ratios are used to check the efficiency of a company and to know the

liquidity position that is how easily assets can be converted into cash in short run (Lee, et al.,

2009).

Singapore Airlines

Ratios Formulas 2017 2016 2015 2014

Current Ratio Current Assets/Current liabilities 0.76 0.90 1.04 1.09

Quick Ratio Total current assets – Total

Inventories/ Total current liabilities

0.73 0.88 1.02 1.06

Cash conversion cycle Days sales outstanding + Days

Inventory – Days Payable

-42.81 -61.34 -46.49 -38.69

(Reuters, 2018)

Air Asia

Ratios Formulas 2017 2016 2015 2014

Current Ratio Current Assets/Current liabilities 0.81 0.97 0.81 0.62

Quick Ratio Total current assets – Total Inventories/

Total current liabilities

0.80 0.96 0.81 0.61

Cash conversion

cycle

Days sales outstanding + Days

Inventory – Days Payable

-2.97 -19.95 -12.78 2.40

Source: (AirAsia, 2017)

The current ratio of Singapore Airlines is 0.76 which shows that the company would be unable to

pay off its obligations if due immediately and this is an indication that company is not in good

liquidity financial health. Mainly higher current ratio that is 2:1 proves better that means a

company can meet its liabilities in a year. In comparing the Singapore Airlines liquidity position

with its competitor Air Asia it is observed that in FY14 and FY15 Singapore Airlines showed a

good liquidity position but currently Air Asia has better position and would be liable to pay its

liabilities quickly.

Cash conversion cycle is calculated to know how fast a company converts its inventory into cash

receivables and the time it takes to pay its bills and its helps in measuring management

effectiveness of a company (Robinson, et al., 2015). The cash conversion cycle of the Singapore

Airlines shows a negative amount for four consecutive years which means the company is

generating revenue from customers on time and paying to its suppliers later. The negative cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Ratios

10

conversion cycle is an indicator of effective management team and efficient use of working

capital by the company. Air Asia also has low conversion cycle which is also a good indicator

but Singapore Airlines showed an excellent management of working capital and cash conversion

period.

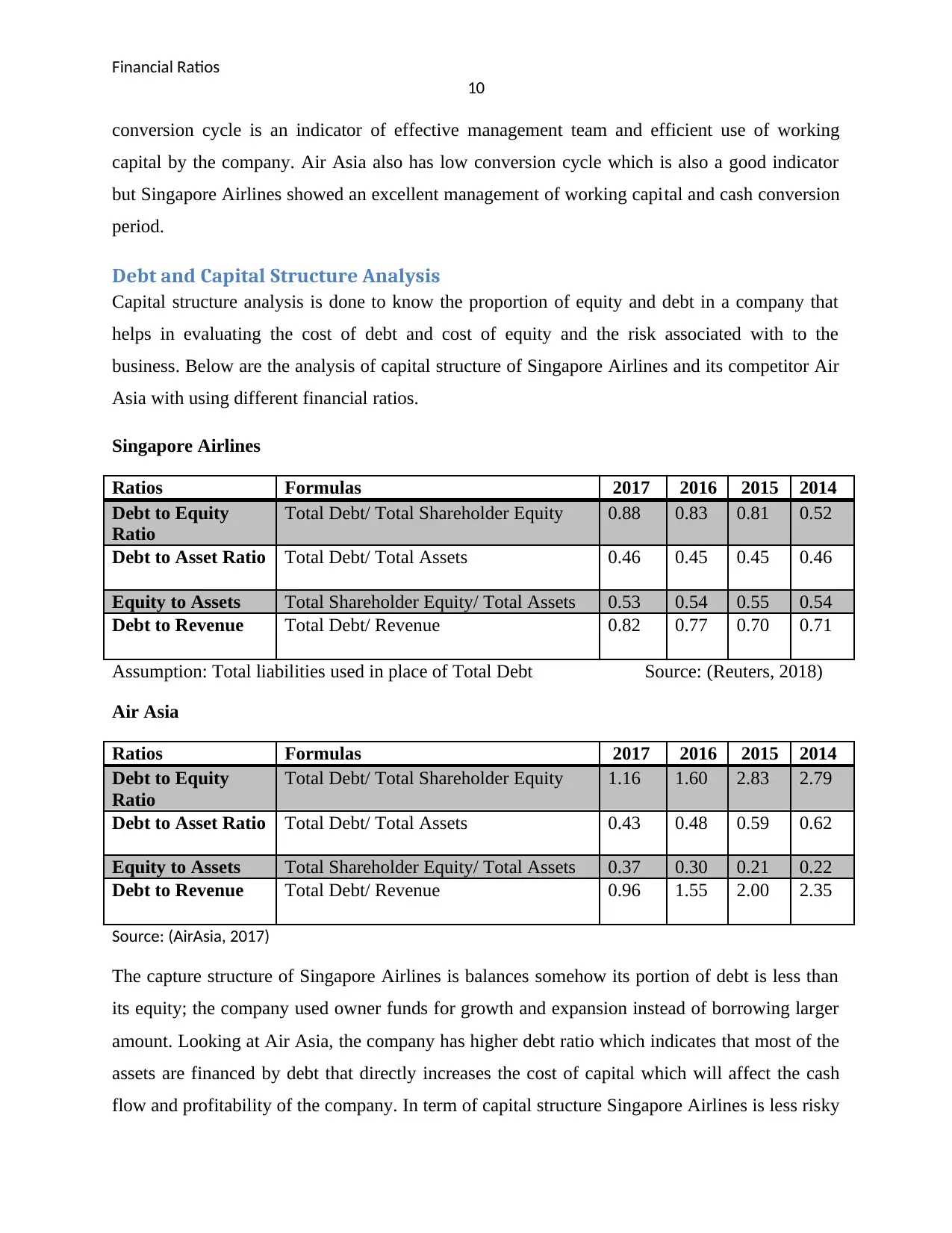

Debt and Capital Structure Analysis

Capital structure analysis is done to know the proportion of equity and debt in a company that

helps in evaluating the cost of debt and cost of equity and the risk associated with to the

business. Below are the analysis of capital structure of Singapore Airlines and its competitor Air

Asia with using different financial ratios.

Singapore Airlines

Ratios Formulas 2017 2016 2015 2014

Debt to Equity

Ratio

Total Debt/ Total Shareholder Equity 0.88 0.83 0.81 0.52

Debt to Asset Ratio Total Debt/ Total Assets 0.46 0.45 0.45 0.46

Equity to Assets Total Shareholder Equity/ Total Assets 0.53 0.54 0.55 0.54

Debt to Revenue Total Debt/ Revenue 0.82 0.77 0.70 0.71

Assumption: Total liabilities used in place of Total Debt Source: (Reuters, 2018)

Air Asia

Ratios Formulas 2017 2016 2015 2014

Debt to Equity

Ratio

Total Debt/ Total Shareholder Equity 1.16 1.60 2.83 2.79

Debt to Asset Ratio Total Debt/ Total Assets 0.43 0.48 0.59 0.62

Equity to Assets Total Shareholder Equity/ Total Assets 0.37 0.30 0.21 0.22

Debt to Revenue Total Debt/ Revenue 0.96 1.55 2.00 2.35

Source: (AirAsia, 2017)

The capture structure of Singapore Airlines is balances somehow its portion of debt is less than

its equity; the company used owner funds for growth and expansion instead of borrowing larger

amount. Looking at Air Asia, the company has higher debt ratio which indicates that most of the

assets are financed by debt that directly increases the cost of capital which will affect the cash

flow and profitability of the company. In term of capital structure Singapore Airlines is less risky

10

conversion cycle is an indicator of effective management team and efficient use of working

capital by the company. Air Asia also has low conversion cycle which is also a good indicator

but Singapore Airlines showed an excellent management of working capital and cash conversion

period.

Debt and Capital Structure Analysis

Capital structure analysis is done to know the proportion of equity and debt in a company that

helps in evaluating the cost of debt and cost of equity and the risk associated with to the

business. Below are the analysis of capital structure of Singapore Airlines and its competitor Air

Asia with using different financial ratios.

Singapore Airlines

Ratios Formulas 2017 2016 2015 2014

Debt to Equity

Ratio

Total Debt/ Total Shareholder Equity 0.88 0.83 0.81 0.52

Debt to Asset Ratio Total Debt/ Total Assets 0.46 0.45 0.45 0.46

Equity to Assets Total Shareholder Equity/ Total Assets 0.53 0.54 0.55 0.54

Debt to Revenue Total Debt/ Revenue 0.82 0.77 0.70 0.71

Assumption: Total liabilities used in place of Total Debt Source: (Reuters, 2018)

Air Asia

Ratios Formulas 2017 2016 2015 2014

Debt to Equity

Ratio

Total Debt/ Total Shareholder Equity 1.16 1.60 2.83 2.79

Debt to Asset Ratio Total Debt/ Total Assets 0.43 0.48 0.59 0.62

Equity to Assets Total Shareholder Equity/ Total Assets 0.37 0.30 0.21 0.22

Debt to Revenue Total Debt/ Revenue 0.96 1.55 2.00 2.35

Source: (AirAsia, 2017)

The capture structure of Singapore Airlines is balances somehow its portion of debt is less than

its equity; the company used owner funds for growth and expansion instead of borrowing larger

amount. Looking at Air Asia, the company has higher debt ratio which indicates that most of the

assets are financed by debt that directly increases the cost of capital which will affect the cash

flow and profitability of the company. In term of capital structure Singapore Airlines is less risky

Financial Ratios

11

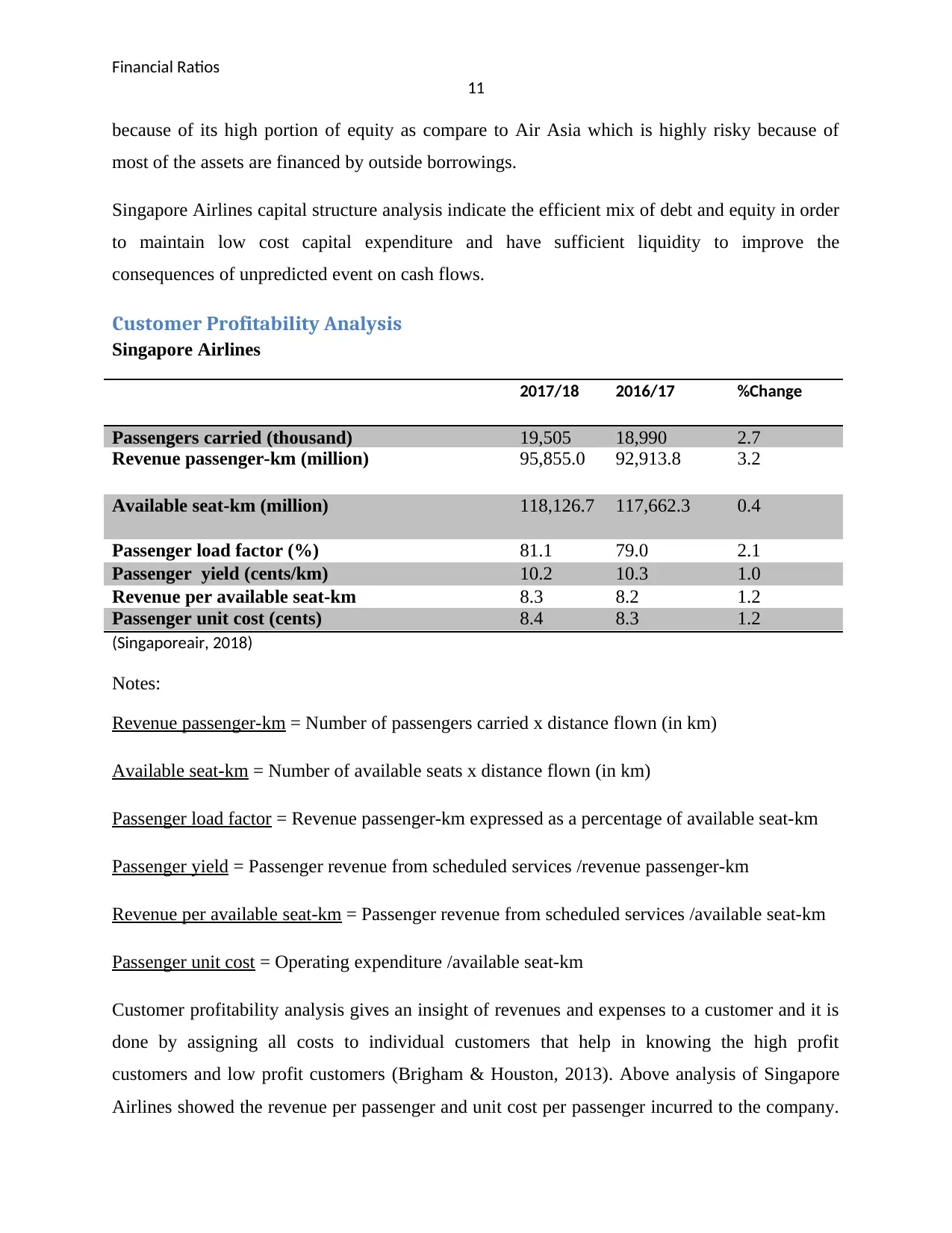

because of its high portion of equity as compare to Air Asia which is highly risky because of

most of the assets are financed by outside borrowings.

Singapore Airlines capital structure analysis indicate the efficient mix of debt and equity in order

to maintain low cost capital expenditure and have sufficient liquidity to improve the

consequences of unpredicted event on cash flows.

Customer Profitability Analysis

Singapore Airlines

2017/18 2016/17 %Change

Passengers carried (thousand) 19,505 18,990 2.7

Revenue passenger-km (million) 95,855.0 92,913.8 3.2

Available seat-km (million) 118,126.7 117,662.3 0.4

Passenger load factor (%) 81.1 79.0 2.1

Passenger yield (cents/km) 10.2 10.3 1.0

Revenue per available seat-km 8.3 8.2 1.2

Passenger unit cost (cents) 8.4 8.3 1.2

(Singaporeair, 2018)

Notes:

Revenue passenger-km = Number of passengers carried x distance flown (in km)

Available seat-km = Number of available seats x distance flown (in km)

Passenger load factor = Revenue passenger-km expressed as a percentage of available seat-km

Passenger yield = Passenger revenue from scheduled services /revenue passenger-km

Revenue per available seat-km = Passenger revenue from scheduled services /available seat-km

Passenger unit cost = Operating expenditure /available seat-km

Customer profitability analysis gives an insight of revenues and expenses to a customer and it is

done by assigning all costs to individual customers that help in knowing the high profit

customers and low profit customers (Brigham & Houston, 2013). Above analysis of Singapore

Airlines showed the revenue per passenger and unit cost per passenger incurred to the company.

11

because of its high portion of equity as compare to Air Asia which is highly risky because of

most of the assets are financed by outside borrowings.

Singapore Airlines capital structure analysis indicate the efficient mix of debt and equity in order

to maintain low cost capital expenditure and have sufficient liquidity to improve the

consequences of unpredicted event on cash flows.

Customer Profitability Analysis

Singapore Airlines

2017/18 2016/17 %Change

Passengers carried (thousand) 19,505 18,990 2.7

Revenue passenger-km (million) 95,855.0 92,913.8 3.2

Available seat-km (million) 118,126.7 117,662.3 0.4

Passenger load factor (%) 81.1 79.0 2.1

Passenger yield (cents/km) 10.2 10.3 1.0

Revenue per available seat-km 8.3 8.2 1.2

Passenger unit cost (cents) 8.4 8.3 1.2

(Singaporeair, 2018)

Notes:

Revenue passenger-km = Number of passengers carried x distance flown (in km)

Available seat-km = Number of available seats x distance flown (in km)

Passenger load factor = Revenue passenger-km expressed as a percentage of available seat-km

Passenger yield = Passenger revenue from scheduled services /revenue passenger-km

Revenue per available seat-km = Passenger revenue from scheduled services /available seat-km

Passenger unit cost = Operating expenditure /available seat-km

Customer profitability analysis gives an insight of revenues and expenses to a customer and it is

done by assigning all costs to individual customers that help in knowing the high profit

customers and low profit customers (Brigham & Houston, 2013). Above analysis of Singapore

Airlines showed the revenue per passenger and unit cost per passenger incurred to the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.