Singapore Income Tax Act and Withholding Tax: A Comprehensive Report

VerifiedAdded on 2022/12/29

|11

|2169

|66

Report

AI Summary

This report provides an overview of Singapore's taxation policies, focusing on the Singapore Income Tax Act (SITA) and specifically Section 45 concerning withholding tax. It explains how the government uses taxation for national development and covers the tax treatment of various items like interest, commission, and royalty payments. The report details the consequences of non-compliance, including penalties for failing to withhold or remit taxes, and highlights exemptions. A key element is a case study of Delta Ltd, analyzing whether the company should deduct withholding tax from payments to a non-resident chef. The report concludes by summarizing the key aspects of Singapore's tax system, emphasizing the importance of understanding and adhering to the regulations outlined in the SITA.

Running head: Taxation

Taxation

Name of the Student

Name of the University

Author Note

Taxation

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Taxation

Executive Summary

The report shows about the taxation policy as how it help the government in regards of the

development of the country as tax is been charged upon the income which is been generated

by the individual and the corporate. It shows about the Section 45 of Singapore Income Tax

Act. Section 45 takes into consideration the withholding tax limit as it say that the individual

should deduct an amount as withholding tax whenever it make payment of royalty or any

other similar nature to an non- resident individual. Lastly it show about the Case of Delta Ltd

as whether it should deduct the amount from the Chef payment or not.

Taxation

Executive Summary

The report shows about the taxation policy as how it help the government in regards of the

development of the country as tax is been charged upon the income which is been generated

by the individual and the corporate. It shows about the Section 45 of Singapore Income Tax

Act. Section 45 takes into consideration the withholding tax limit as it say that the individual

should deduct an amount as withholding tax whenever it make payment of royalty or any

other similar nature to an non- resident individual. Lastly it show about the Case of Delta Ltd

as whether it should deduct the amount from the Chef payment or not.

2

Taxation

Table of Contents

Introduction................................................................................................................................3

S45 as per Singapore Income Tax Act.......................................................................................3

Tax treatment in regards of different items................................................................................4

Consequence of Defaulting withholding Tax Payment.............................................................5

Exemptions for withholding tax.................................................................................................5

Case study of Delta Ltd..............................................................................................................6

Conclusion..................................................................................................................................6

Reference....................................................................................................................................8

Taxation

Table of Contents

Introduction................................................................................................................................3

S45 as per Singapore Income Tax Act.......................................................................................3

Tax treatment in regards of different items................................................................................4

Consequence of Defaulting withholding Tax Payment.............................................................5

Exemptions for withholding tax.................................................................................................5

Case study of Delta Ltd..............................................................................................................6

Conclusion..................................................................................................................................6

Reference....................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Taxation

Introduction

Taxation is been charged by the government upon the individual and the corporate tax

on the proportion of their income. This amount is been charged by the government so that it

can able to make proper development in the country. The report is been based upon the SITA

as Singapore Income Tax Act (Agarwal & Qian 2014). It shows the various aspects of the

taxation and also shows tax treatment in regards of the different payment which is made as

per Singapore Income Tax Act. It also show the consequences of non payment or late

payment and also show a case which is been related to a situation and how it should be

treated as per the Singapore Income Tax Act. So it helps to know how to deal with the norms

of the Singapore taxation and also gave the details of the same (Araki & Claus 2014). It also

about the payment which the individual have to make to the government and also about the

different section which are there in regards of the withholding limit. It also show about the

penalty which can be imposed upon the individual if it does not able to follow the norms

properly and also it show about the case study of delta ltd and suggest whether it should

deduct the amount or not.

S45 as per Singapore Income Tax Act

This section S45 give detail in regards of the Withholding tax payment to Non-

Residents and Partnership. It contains the details of the amount which should be charged

from them as different payment (Brauner & Baez Moreno 2015). As per the section it state

that when any sort of the payment is been made by the individual which is related to the

nature of royalty or interest to an non-resident than it have to deduct a part of payment as

withholding tax and should submit the deducted amount to Inland Revenue Authority of

Singapore (Saad 2014).

Taxation

Introduction

Taxation is been charged by the government upon the individual and the corporate tax

on the proportion of their income. This amount is been charged by the government so that it

can able to make proper development in the country. The report is been based upon the SITA

as Singapore Income Tax Act (Agarwal & Qian 2014). It shows the various aspects of the

taxation and also shows tax treatment in regards of the different payment which is made as

per Singapore Income Tax Act. It also show the consequences of non payment or late

payment and also show a case which is been related to a situation and how it should be

treated as per the Singapore Income Tax Act. So it helps to know how to deal with the norms

of the Singapore taxation and also gave the details of the same (Araki & Claus 2014). It also

about the payment which the individual have to make to the government and also about the

different section which are there in regards of the withholding limit. It also show about the

penalty which can be imposed upon the individual if it does not able to follow the norms

properly and also it show about the case study of delta ltd and suggest whether it should

deduct the amount or not.

S45 as per Singapore Income Tax Act

This section S45 give detail in regards of the Withholding tax payment to Non-

Residents and Partnership. It contains the details of the amount which should be charged

from them as different payment (Brauner & Baez Moreno 2015). As per the section it state

that when any sort of the payment is been made by the individual which is related to the

nature of royalty or interest to an non-resident than it have to deduct a part of payment as

withholding tax and should submit the deducted amount to Inland Revenue Authority of

Singapore (Saad 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Taxation

It also state that if an individual do a payment to the partnership and if any partner of

the partnership is a non-resident than the individual should deduct the withholding tax from

the amount of the payment and the same should be submitted to Inland Revenue Authority of

Singapore (Caruana-Galizia & Caruana-Galizia 2016).

It can be said that the taxation has become very harsh so to give flexibility to the

partnership firm it has given the exemption as if the company have one resident partner than

it does not have to apply with regard of S45 withholding tax limit (Fleming et al., 2014).

It also state that it is necessary for the partnership firm that if there is any kind of the

change in the partner than it should directly notify the same to the Comptroller so that proper

amount of the changes can be done in regards of the partnership (Wiedemann & Finke 2015).

Tax treatment in regards of different items

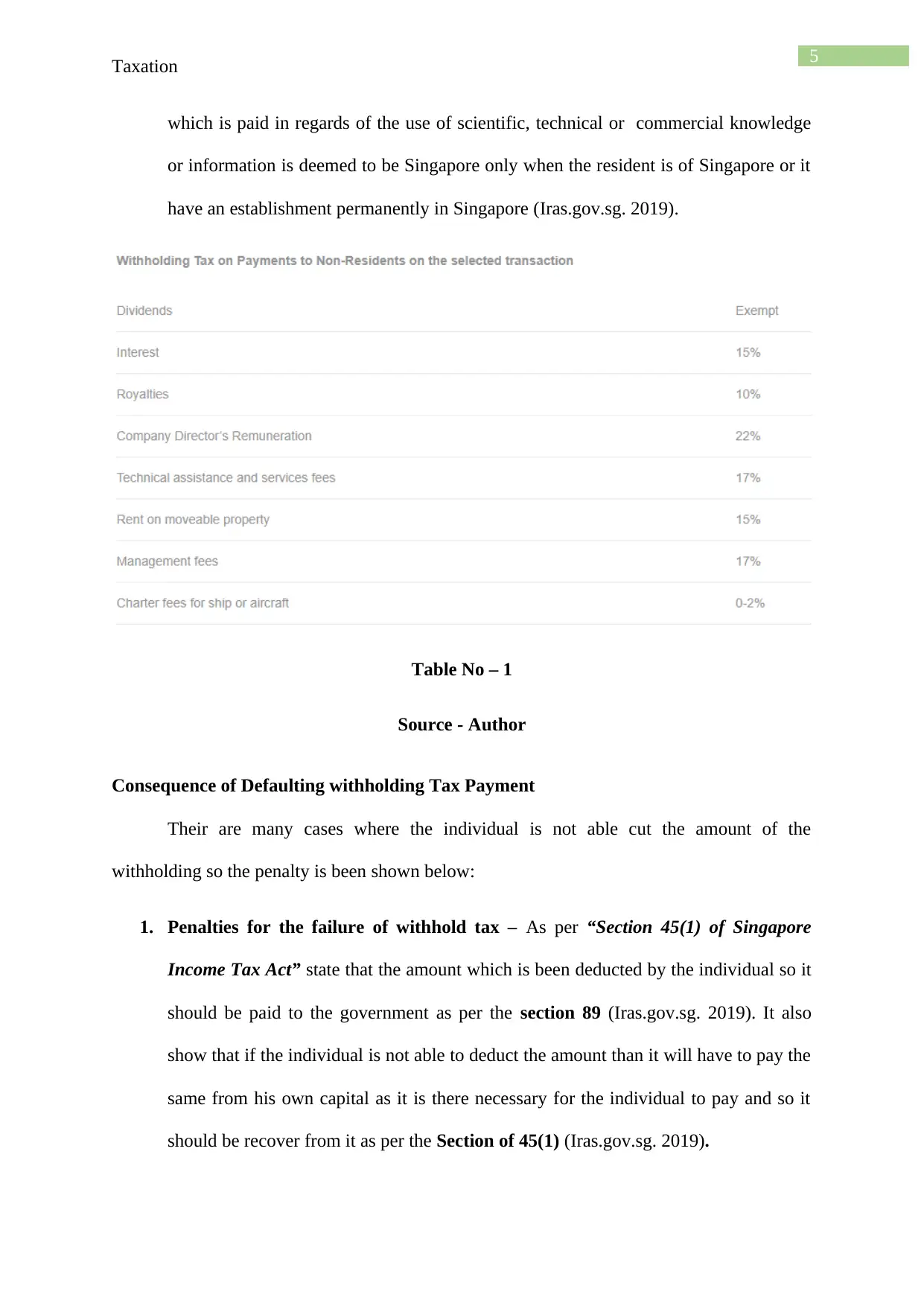

The tax treatment of different nature in Singapore Income Tax Act is shown below:

1. Interest , Commission – As per “Section 12(6) in Singapore Income Tax Act” it

state that any payment of the interest or commission in regards of the loan is to be

considered as part of the Singapore only if it is directly or indirectly related to resident

in Singapore or the individual which have permanent establishment in Singapore

(Iras.gov.sg. 2019). It also takes into consideration the income which is generated by

loan and it is been utilize in Singapore.

2. Royalty – As per “Section 12(7)(a) in Singapore Income Tax Act” say that any

amount paid as royalty or any other payment in regards of the use of the movable

property is deemed to be in Singapore only when the individual is the resident of

Singapore or having some permanent establishment in Singapore (Iras.gov.sg. 2019).

3. Payment for the use of scientific or commercial knowledge or Information - As

per “Section 12(7)(b) in Singapore Income Tax Act” state that any amount of money

Taxation

It also state that if an individual do a payment to the partnership and if any partner of

the partnership is a non-resident than the individual should deduct the withholding tax from

the amount of the payment and the same should be submitted to Inland Revenue Authority of

Singapore (Caruana-Galizia & Caruana-Galizia 2016).

It can be said that the taxation has become very harsh so to give flexibility to the

partnership firm it has given the exemption as if the company have one resident partner than

it does not have to apply with regard of S45 withholding tax limit (Fleming et al., 2014).

It also state that it is necessary for the partnership firm that if there is any kind of the

change in the partner than it should directly notify the same to the Comptroller so that proper

amount of the changes can be done in regards of the partnership (Wiedemann & Finke 2015).

Tax treatment in regards of different items

The tax treatment of different nature in Singapore Income Tax Act is shown below:

1. Interest , Commission – As per “Section 12(6) in Singapore Income Tax Act” it

state that any payment of the interest or commission in regards of the loan is to be

considered as part of the Singapore only if it is directly or indirectly related to resident

in Singapore or the individual which have permanent establishment in Singapore

(Iras.gov.sg. 2019). It also takes into consideration the income which is generated by

loan and it is been utilize in Singapore.

2. Royalty – As per “Section 12(7)(a) in Singapore Income Tax Act” say that any

amount paid as royalty or any other payment in regards of the use of the movable

property is deemed to be in Singapore only when the individual is the resident of

Singapore or having some permanent establishment in Singapore (Iras.gov.sg. 2019).

3. Payment for the use of scientific or commercial knowledge or Information - As

per “Section 12(7)(b) in Singapore Income Tax Act” state that any amount of money

5

Taxation

which is paid in regards of the use of scientific, technical or commercial knowledge

or information is deemed to be Singapore only when the resident is of Singapore or it

have an establishment permanently in Singapore (Iras.gov.sg. 2019).

Table No – 1

Source - Author

Consequence of Defaulting withholding Tax Payment

Their are many cases where the individual is not able cut the amount of the

withholding so the penalty is been shown below:

1. Penalties for the failure of withhold tax – As per “Section 45(1) of Singapore

Income Tax Act” state that the amount which is been deducted by the individual so it

should be paid to the government as per the section 89 (Iras.gov.sg. 2019). It also

show that if the individual is not able to deduct the amount than it will have to pay the

same from his own capital as it is there necessary for the individual to pay and so it

should be recover from it as per the Section of 45(1) (Iras.gov.sg. 2019).

Taxation

which is paid in regards of the use of scientific, technical or commercial knowledge

or information is deemed to be Singapore only when the resident is of Singapore or it

have an establishment permanently in Singapore (Iras.gov.sg. 2019).

Table No – 1

Source - Author

Consequence of Defaulting withholding Tax Payment

Their are many cases where the individual is not able cut the amount of the

withholding so the penalty is been shown below:

1. Penalties for the failure of withhold tax – As per “Section 45(1) of Singapore

Income Tax Act” state that the amount which is been deducted by the individual so it

should be paid to the government as per the section 89 (Iras.gov.sg. 2019). It also

show that if the individual is not able to deduct the amount than it will have to pay the

same from his own capital as it is there necessary for the individual to pay and so it

should be recover from it as per the Section of 45(1) (Iras.gov.sg. 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Taxation

2. Penalties for failure to notify IRAS of tax withheld – If the individual have

deducted the amount of tax withholding from the non-resident but the individual have

not submitted the IR37 so it will be consider as offence so it will be charged penalty

as 3 times of the amount deducted but it should not exceed $10000 or 3 years of

imprisonment or both (Iras.gov.sg. 2019).

3. Penalties for late payment of tax withheld – This penalty is been imposed when the

individual is not able to pay the tax amount on time so it have to pay some penalty

amount so the amount of penalty will be 20% of the tax holding limit. So first 5% of

the withhold tax and additional of 1% tax for every month till to the maximum of

15%. So this is the penalty which the individual have to pay in regards of the late

payment (Iras.gov.sg. 2019).

Exemptions for withholding tax

There are some items which are exempted from the limit of withholding tax and the

exemption are been shown below:

1. Specified Software Payments – This is been consider as withholding tax only after it

able to satisfy the definition which is given as it take into consider downloadable

software, shirnk-wrap software, site licence and also computer hardware with

software bundled (Iras.gov.sg. 2019).

2. Payment for Satellite Capacity – The payment which the individual make in regards

to the non resident for the leasing capacity on the space of satellite so it will be

exempted for 15% final from the withhold tax limit (Iras.gov.sg. 2019).

3. Payment for use International Submarine Capacity – Any amount of payment

which is been done in regards of international submarine capacity so it will be

exempted for 15% from the withhold tax limit (Iras.gov.sg. 2019).

Taxation

2. Penalties for failure to notify IRAS of tax withheld – If the individual have

deducted the amount of tax withholding from the non-resident but the individual have

not submitted the IR37 so it will be consider as offence so it will be charged penalty

as 3 times of the amount deducted but it should not exceed $10000 or 3 years of

imprisonment or both (Iras.gov.sg. 2019).

3. Penalties for late payment of tax withheld – This penalty is been imposed when the

individual is not able to pay the tax amount on time so it have to pay some penalty

amount so the amount of penalty will be 20% of the tax holding limit. So first 5% of

the withhold tax and additional of 1% tax for every month till to the maximum of

15%. So this is the penalty which the individual have to pay in regards of the late

payment (Iras.gov.sg. 2019).

Exemptions for withholding tax

There are some items which are exempted from the limit of withholding tax and the

exemption are been shown below:

1. Specified Software Payments – This is been consider as withholding tax only after it

able to satisfy the definition which is given as it take into consider downloadable

software, shirnk-wrap software, site licence and also computer hardware with

software bundled (Iras.gov.sg. 2019).

2. Payment for Satellite Capacity – The payment which the individual make in regards

to the non resident for the leasing capacity on the space of satellite so it will be

exempted for 15% final from the withhold tax limit (Iras.gov.sg. 2019).

3. Payment for use International Submarine Capacity – Any amount of payment

which is been done in regards of international submarine capacity so it will be

exempted for 15% from the withhold tax limit (Iras.gov.sg. 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Taxation

Case study of Delta Ltd

As per Section 45 of Singapore Income Tax Act it said that if the individual made

payment to an non-resident than it should deduct an withholding tax amount form the same

and should deposit the same to the government (Johannesen & Zucman 2014).

So as per the case given it can be seen that Delta Enterprise have appoint an chef who

is non-resident and as the company was doing payment to Chef so it should deduct the

amount from the payment it was making as per the “Section 89 of Singapore Income Tax

Act” so it should deduct the same for the payment amount (Markle 2016).

Conclusion

The report concludes about the taxation policy, as the taxation policy is been charged

by the government form the individual and corporate. The tax is been charged by the

government so that it can able to make development in the country and able to maintain the

economy as the money which is been invested in the government company so that it can able

to run the economy more successfully. It conclude about the Singapore Income Tax Act and

explain the Section 45 which is related to the withholding tax as it said that if any individual

make payment to an non-resident than it should deduct an amount form the payment as

withholding tax and should deposit the same in the government account.

It show various types of the withholding amount as what should be deducted by the

company and also show the exemption in regards of the same as it does not take into

consideration. Lastly it conclude about the different penalty which is to be imposed by the

Government upon the individual and how much amount it have to pay in regards of the

penalty and also show about the case of Delta Ltd as whether it should deduct the amount of

payment which is been made to the Chef as the Chef is an non-resident so the company

Taxation

Case study of Delta Ltd

As per Section 45 of Singapore Income Tax Act it said that if the individual made

payment to an non-resident than it should deduct an withholding tax amount form the same

and should deposit the same to the government (Johannesen & Zucman 2014).

So as per the case given it can be seen that Delta Enterprise have appoint an chef who

is non-resident and as the company was doing payment to Chef so it should deduct the

amount from the payment it was making as per the “Section 89 of Singapore Income Tax

Act” so it should deduct the same for the payment amount (Markle 2016).

Conclusion

The report concludes about the taxation policy, as the taxation policy is been charged

by the government form the individual and corporate. The tax is been charged by the

government so that it can able to make development in the country and able to maintain the

economy as the money which is been invested in the government company so that it can able

to run the economy more successfully. It conclude about the Singapore Income Tax Act and

explain the Section 45 which is related to the withholding tax as it said that if any individual

make payment to an non-resident than it should deduct an amount form the payment as

withholding tax and should deposit the same in the government account.

It show various types of the withholding amount as what should be deducted by the

company and also show the exemption in regards of the same as it does not take into

consideration. Lastly it conclude about the different penalty which is to be imposed by the

Government upon the individual and how much amount it have to pay in regards of the

penalty and also show about the case of Delta Ltd as whether it should deduct the amount of

payment which is been made to the Chef as the Chef is an non-resident so the company

8

Taxation

should deduct the amount as withholding tax and should deposit the same in the government

account.

Taxation

should deduct the amount as withholding tax and should deposit the same in the government

account.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Taxation

Reference

Agarwal, S., & Qian, W. (2014). Consumption and debt response to unanticipated income

shocks: Evidence from a natural experiment in singapore. American Economic

Review, 104(12), 4205-30.

Araki, S., & Claus, I. (2014). A comparative analysis on tax administration in Asia and the

Pacific. Asian Development Bank.

Brauner, Y., & Baez Moreno, A. (2015). Withholding taxes in the service of BEPS action 1:

address the tax challenges of the digital economy. WU International Taxation

Research Paper Series, (2015-14).

Caruana-Galizia, P., & Caruana-Galizia, M. (2016). Offshore financial activity and tax

policy: evidence from a leaked data set. Journal of Public Policy, 36(3), 457-488.

Fleming Jr, J. C., Peroni, R. J., & Shay, S. E. (2014). Formulary Apportionment in the US

International Income Tax System: Putting Lipstick on a Pig. Mich. J. Int'l L., 36, 1.

Iras.gov.sg. (2019). S45 Withholding Tax and Partnerships - IRAS. Retrieved from

https://www.iras.gov.sg/irashome/Businesses/Self-Employed/Working-out-your-

taxes/S45-Withholding-Tax-and-Partnerships/

Iras.gov.sg. (2019). S45 Withholding Tax and Partnerships - IRAS. Retrieved from

https://www.iras.gov.sg/irashome/Businesses/Self-Employed/Working-out-your-

taxes/S45-Withholding-Tax-and-Partnerships/

Iras.gov.sg. (2019). Withholding Tax - IRAS. Retrieved from

https://www.iras.gov.sg/irashome/e-Services/Other-Taxes/Withholding-Tax/

Johannesen, N., & Zucman, G. (2014). The end of bank secrecy? An evaluation of the G20

tax haven crackdown. American Economic Journal: Economic Policy, 6(1), 65-91.

Taxation

Reference

Agarwal, S., & Qian, W. (2014). Consumption and debt response to unanticipated income

shocks: Evidence from a natural experiment in singapore. American Economic

Review, 104(12), 4205-30.

Araki, S., & Claus, I. (2014). A comparative analysis on tax administration in Asia and the

Pacific. Asian Development Bank.

Brauner, Y., & Baez Moreno, A. (2015). Withholding taxes in the service of BEPS action 1:

address the tax challenges of the digital economy. WU International Taxation

Research Paper Series, (2015-14).

Caruana-Galizia, P., & Caruana-Galizia, M. (2016). Offshore financial activity and tax

policy: evidence from a leaked data set. Journal of Public Policy, 36(3), 457-488.

Fleming Jr, J. C., Peroni, R. J., & Shay, S. E. (2014). Formulary Apportionment in the US

International Income Tax System: Putting Lipstick on a Pig. Mich. J. Int'l L., 36, 1.

Iras.gov.sg. (2019). S45 Withholding Tax and Partnerships - IRAS. Retrieved from

https://www.iras.gov.sg/irashome/Businesses/Self-Employed/Working-out-your-

taxes/S45-Withholding-Tax-and-Partnerships/

Iras.gov.sg. (2019). S45 Withholding Tax and Partnerships - IRAS. Retrieved from

https://www.iras.gov.sg/irashome/Businesses/Self-Employed/Working-out-your-

taxes/S45-Withholding-Tax-and-Partnerships/

Iras.gov.sg. (2019). Withholding Tax - IRAS. Retrieved from

https://www.iras.gov.sg/irashome/e-Services/Other-Taxes/Withholding-Tax/

Johannesen, N., & Zucman, G. (2014). The end of bank secrecy? An evaluation of the G20

tax haven crackdown. American Economic Journal: Economic Policy, 6(1), 65-91.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Taxation

Markle, K. (2016). A comparison of the tax‐motivated income shifting of multinationals in

territorial and worldwide countries. Contemporary Accounting Research, 33(1), 7-43.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Wiedemann, V., & Finke, K. (2015). Taxing investments in the Asia-Pacific region: The

importance of cross-border taxation and tax incentives (No. 15-014). ZEW

Discussion Papers.

Taxation

Markle, K. (2016). A comparison of the tax‐motivated income shifting of multinationals in

territorial and worldwide countries. Contemporary Accounting Research, 33(1), 7-43.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Wiedemann, V., & Finke, K. (2015). Taxing investments in the Asia-Pacific region: The

importance of cross-border taxation and tax incentives (No. 15-014). ZEW

Discussion Papers.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.