SingTel Optus Pty Ltd: Audit, Assurance, and Compliance Report 2016

VerifiedAdded on 2023/06/05

|14

|3373

|211

Report

AI Summary

This report provides an analysis of the audit process conducted by SingTel Optus Pty. Limited, focusing on assurance and compliance with Australian financial regulations. It examines the auditor's independence, non-audit services provided, and key audit matters such as revenue recognition, acquisition of Trustwave, taxation, and goodwill impairment. The report also reviews the role of the audit committee and the audit opinion, emphasizing the directors' responsibilities in ensuring the company's best interests and compliance with accounting principles. The analysis concludes that the audit processes align with Australian regulations and provide stakeholders with a fair representation of the company's financial position.

Audit, Assurance and Compliance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The main purpose of executing this report is to analyze the process of an audit conducted by

SingTel Optus Pty. Limited which is operating in Australia. This report has successfully

concluded that a process of the audit can have a direct and substantial impact on the decision-

making process of a stakeholder. After the analysis of this report, it can be said that all the

processes are within the perspective of rules and regulation implemented in Australia with

regards to financial reporting and Audit reporting.

2

The main purpose of executing this report is to analyze the process of an audit conducted by

SingTel Optus Pty. Limited which is operating in Australia. This report has successfully

concluded that a process of the audit can have a direct and substantial impact on the decision-

making process of a stakeholder. After the analysis of this report, it can be said that all the

processes are within the perspective of rules and regulation implemented in Australia with

regards to financial reporting and Audit reporting.

2

Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Analysis of the annual report.....................................................................................................5

Conclusion................................................................................................................................11

References................................................................................................................................12

3

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Analysis of the annual report.....................................................................................................5

Conclusion................................................................................................................................11

References................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The auditing process is not only important for shareholders, it is also important for other

stakeholders in business such as management, directors, suppliers, creditors etc. there are

various stakeholders in a business organization whose decision depends on the opinion

presented by auditors of the company on financial statements (Eilifsen et.al, 2013).

Generally, the opinion of the auditor is provided in four paragraphs that only states that if the

company has complied with all the rules and regulations and if financial statements of the

company are presented correctly according to the financial position of the company in the

market. This was not presenting the true picture of the financial position of the company to

stakeholders of the company. Therefore the auditing authorities in Australia regulated the

inclusion of key audit matters paragraph along with the audit report. These key audit matters

were focused on the difficulties faced by an auditor in the process of audit during a particular

financial year (Louwers et.al, 2015). The general purpose of these audit matters is to present a

brief description of audit procedures used by an auditor to collect audit evidence in relation to

difficult matters faced by an auditor during the process of audit. It is important for

stakeholders to analyze these matters so that relevant and accurate decision can be taken by

such stakeholders in relation to investment or doing business with the company. This report

will analyze these audit matters reported by the auditor while conducting an audit of SingTel

Optus limited. Optus is a telecommunication business organization operating in Australia. In

addition to that this report will also analyze the rules and regulations that should be followed

by auditor and management of the company during an independent audit of the company.

4

The auditing process is not only important for shareholders, it is also important for other

stakeholders in business such as management, directors, suppliers, creditors etc. there are

various stakeholders in a business organization whose decision depends on the opinion

presented by auditors of the company on financial statements (Eilifsen et.al, 2013).

Generally, the opinion of the auditor is provided in four paragraphs that only states that if the

company has complied with all the rules and regulations and if financial statements of the

company are presented correctly according to the financial position of the company in the

market. This was not presenting the true picture of the financial position of the company to

stakeholders of the company. Therefore the auditing authorities in Australia regulated the

inclusion of key audit matters paragraph along with the audit report. These key audit matters

were focused on the difficulties faced by an auditor in the process of audit during a particular

financial year (Louwers et.al, 2015). The general purpose of these audit matters is to present a

brief description of audit procedures used by an auditor to collect audit evidence in relation to

difficult matters faced by an auditor during the process of audit. It is important for

stakeholders to analyze these matters so that relevant and accurate decision can be taken by

such stakeholders in relation to investment or doing business with the company. This report

will analyze these audit matters reported by the auditor while conducting an audit of SingTel

Optus limited. Optus is a telecommunication business organization operating in Australia. In

addition to that this report will also analyze the rules and regulations that should be followed

by auditor and management of the company during an independent audit of the company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of the annual report

Auditor’s independence

According to codes and conduct issued by the governing authority of audit in Australia,

auditors of the company has to comply with certain professional standards and independence

is one of such characteristics. The primary objective of an external audit is that the auditor

should assess whether financial statement and internal business environment of the company

is in the best interest of stakeholders or not. This objective cannot be achieved by the auditor

unless the unbiased process of the audit is conducted by the auditor. Therefore it is important

that the auditor is not influenced by any action of management by giving an audit opinion on

financial statements (Leipziger, 2017).

For the financial year ending 2016, all the requirement of independence is correctly followed

by the auditor while giving its opinion on financial statements. This is a specific requirement

for an auditor of the company to prepare and file a statement declaring their independence

before starting the process of audit and all the requirements in relation to the independence of

auditor are assessed by audit committee formed by the board of directors in the company. For

the year ending 2016, all these requirements are checked by the audit committee and

declaration of auditor’s independence is filed by the auditor (Arruñada, 2013). With the help

of all these evidence, it can be said that the requirement of auditor’s independence is followed

by auditor i.e. Deloitte & Touche LLP.

Nonaudit services

During the process of the audit, there are various other services that are provided

management such as taxation consultancy. There are various restrictions that are implied by

governing authorities on the type of non-audit services provided by an auditor during the

process of audit. In addition to that restrictions are also applied to the fees that are paid for

non-audit services to the external auditor of the company. According to current rules in

relation to non-audit service fees, it should not be greater than 70% of total audit fees paid to

the auditor. During the year under consideration, Deloitte has provided services of tax

consultancy, revision of regulatory regulations and other services (Causholli, Chambers and

Payne, 2015).

All the rules and regulations in relation to non-audit services and fees paid for non-audit

services are properly followed by the management of the company. Total fees paid for non-

5

Auditor’s independence

According to codes and conduct issued by the governing authority of audit in Australia,

auditors of the company has to comply with certain professional standards and independence

is one of such characteristics. The primary objective of an external audit is that the auditor

should assess whether financial statement and internal business environment of the company

is in the best interest of stakeholders or not. This objective cannot be achieved by the auditor

unless the unbiased process of the audit is conducted by the auditor. Therefore it is important

that the auditor is not influenced by any action of management by giving an audit opinion on

financial statements (Leipziger, 2017).

For the financial year ending 2016, all the requirement of independence is correctly followed

by the auditor while giving its opinion on financial statements. This is a specific requirement

for an auditor of the company to prepare and file a statement declaring their independence

before starting the process of audit and all the requirements in relation to the independence of

auditor are assessed by audit committee formed by the board of directors in the company. For

the year ending 2016, all these requirements are checked by the audit committee and

declaration of auditor’s independence is filed by the auditor (Arruñada, 2013). With the help

of all these evidence, it can be said that the requirement of auditor’s independence is followed

by auditor i.e. Deloitte & Touche LLP.

Nonaudit services

During the process of the audit, there are various other services that are provided

management such as taxation consultancy. There are various restrictions that are implied by

governing authorities on the type of non-audit services provided by an auditor during the

process of audit. In addition to that restrictions are also applied to the fees that are paid for

non-audit services to the external auditor of the company. According to current rules in

relation to non-audit service fees, it should not be greater than 70% of total audit fees paid to

the auditor. During the year under consideration, Deloitte has provided services of tax

consultancy, revision of regulatory regulations and other services (Causholli, Chambers and

Payne, 2015).

All the rules and regulations in relation to non-audit services and fees paid for non-audit

services are properly followed by the management of the company. Total fees paid for non-

5

audit service does not exceed total allowed fees for such services (Sharma, 2014). Nature of

audit services provided by auditor also permitted according to rules provided in Corporation

Act 2001. Taxation services provided include the preparation of income tax return and filing

of income tax return to the Australian government. Other Consultancy Services include

consultancy provided by Deloitte for the improvement of internal control of the company.

These services and fees paid for these services do not contravene any rules and regulations in

relation to professional code of conduct issued for auditor.

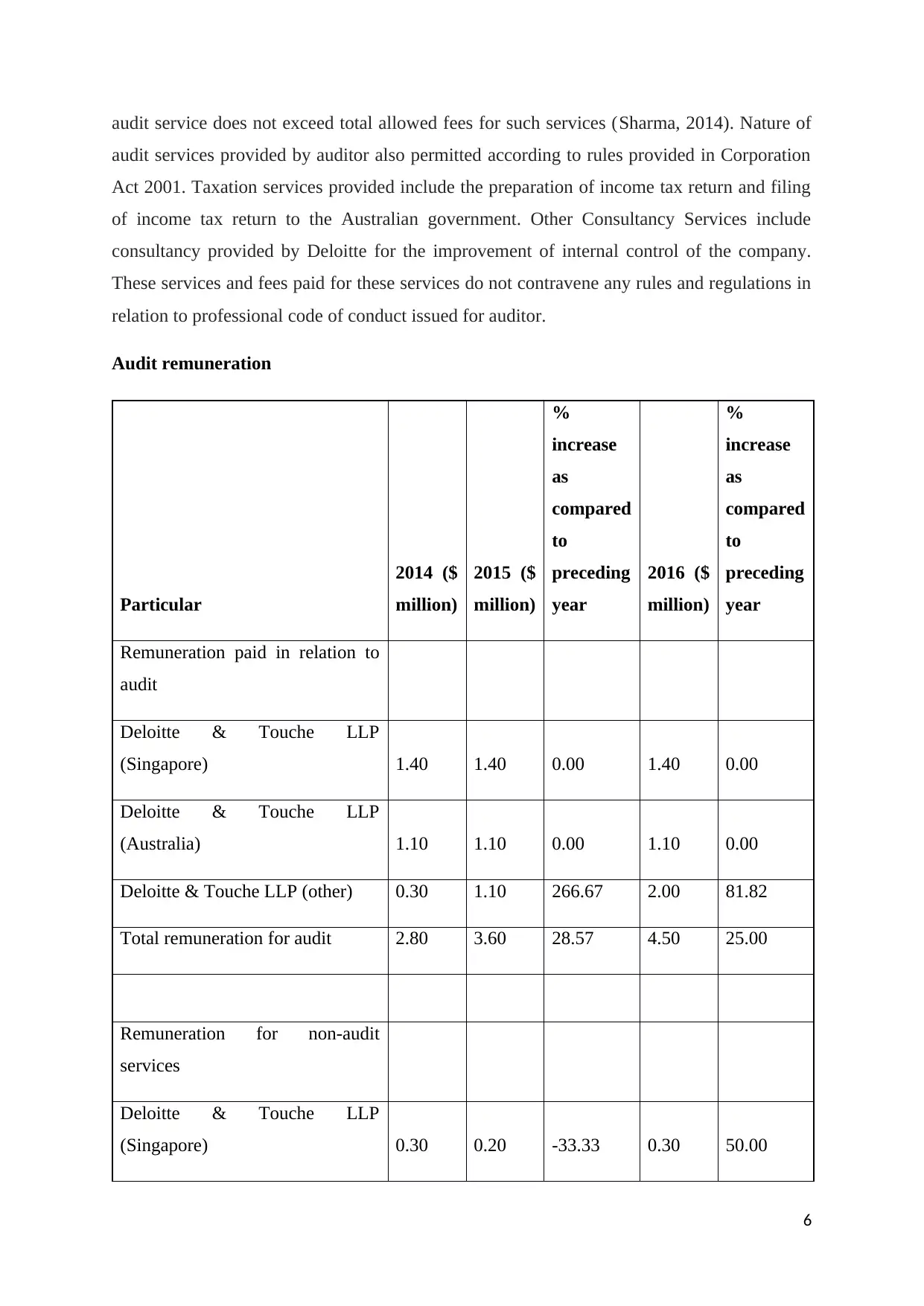

Audit remuneration

Particular

2014 ($

million)

2015 ($

million)

%

increase

as

compared

to

preceding

year

2016 ($

million)

%

increase

as

compared

to

preceding

year

Remuneration paid in relation to

audit

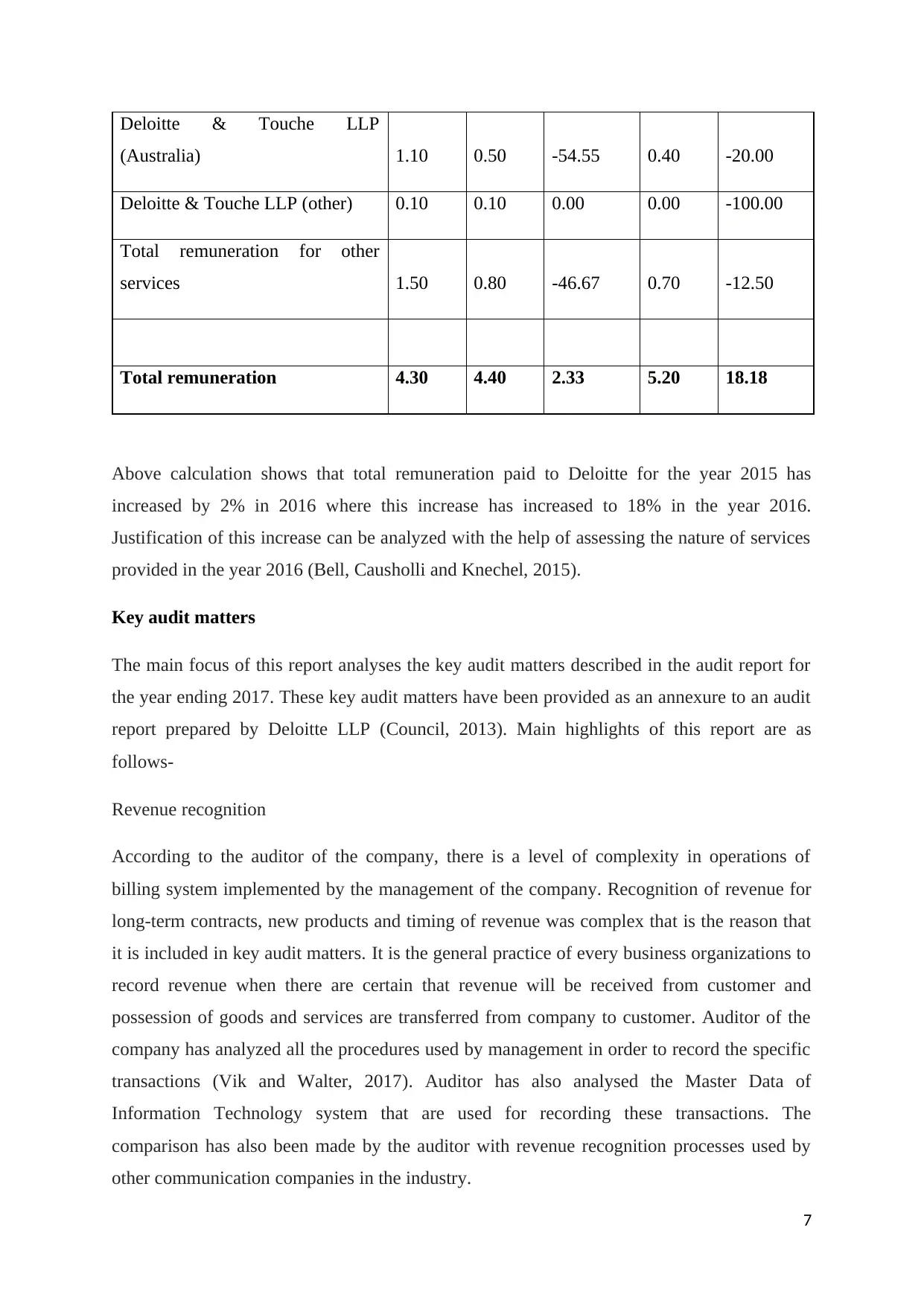

Deloitte & Touche LLP

(Singapore) 1.40 1.40 0.00 1.40 0.00

Deloitte & Touche LLP

(Australia) 1.10 1.10 0.00 1.10 0.00

Deloitte & Touche LLP (other) 0.30 1.10 266.67 2.00 81.82

Total remuneration for audit 2.80 3.60 28.57 4.50 25.00

Remuneration for non-audit

services

Deloitte & Touche LLP

(Singapore) 0.30 0.20 -33.33 0.30 50.00

6

audit services provided by auditor also permitted according to rules provided in Corporation

Act 2001. Taxation services provided include the preparation of income tax return and filing

of income tax return to the Australian government. Other Consultancy Services include

consultancy provided by Deloitte for the improvement of internal control of the company.

These services and fees paid for these services do not contravene any rules and regulations in

relation to professional code of conduct issued for auditor.

Audit remuneration

Particular

2014 ($

million)

2015 ($

million)

%

increase

as

compared

to

preceding

year

2016 ($

million)

%

increase

as

compared

to

preceding

year

Remuneration paid in relation to

audit

Deloitte & Touche LLP

(Singapore) 1.40 1.40 0.00 1.40 0.00

Deloitte & Touche LLP

(Australia) 1.10 1.10 0.00 1.10 0.00

Deloitte & Touche LLP (other) 0.30 1.10 266.67 2.00 81.82

Total remuneration for audit 2.80 3.60 28.57 4.50 25.00

Remuneration for non-audit

services

Deloitte & Touche LLP

(Singapore) 0.30 0.20 -33.33 0.30 50.00

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Deloitte & Touche LLP

(Australia) 1.10 0.50 -54.55 0.40 -20.00

Deloitte & Touche LLP (other) 0.10 0.10 0.00 0.00 -100.00

Total remuneration for other

services 1.50 0.80 -46.67 0.70 -12.50

Total remuneration 4.30 4.40 2.33 5.20 18.18

Above calculation shows that total remuneration paid to Deloitte for the year 2015 has

increased by 2% in 2016 where this increase has increased to 18% in the year 2016.

Justification of this increase can be analyzed with the help of assessing the nature of services

provided in the year 2016 (Bell, Causholli and Knechel, 2015).

Key audit matters

The main focus of this report analyses the key audit matters described in the audit report for

the year ending 2017. These key audit matters have been provided as an annexure to an audit

report prepared by Deloitte LLP (Council, 2013). Main highlights of this report are as

follows-

Revenue recognition

According to the auditor of the company, there is a level of complexity in operations of

billing system implemented by the management of the company. Recognition of revenue for

long-term contracts, new products and timing of revenue was complex that is the reason that

it is included in key audit matters. It is the general practice of every business organizations to

record revenue when there are certain that revenue will be received from customer and

possession of goods and services are transferred from company to customer. Auditor of the

company has analyzed all the procedures used by management in order to record the specific

transactions (Vik and Walter, 2017). Auditor has also analysed the Master Data of

Information Technology system that are used for recording these transactions. The

comparison has also been made by the auditor with revenue recognition processes used by

other communication companies in the industry.

7

(Australia) 1.10 0.50 -54.55 0.40 -20.00

Deloitte & Touche LLP (other) 0.10 0.10 0.00 0.00 -100.00

Total remuneration for other

services 1.50 0.80 -46.67 0.70 -12.50

Total remuneration 4.30 4.40 2.33 5.20 18.18

Above calculation shows that total remuneration paid to Deloitte for the year 2015 has

increased by 2% in 2016 where this increase has increased to 18% in the year 2016.

Justification of this increase can be analyzed with the help of assessing the nature of services

provided in the year 2016 (Bell, Causholli and Knechel, 2015).

Key audit matters

The main focus of this report analyses the key audit matters described in the audit report for

the year ending 2017. These key audit matters have been provided as an annexure to an audit

report prepared by Deloitte LLP (Council, 2013). Main highlights of this report are as

follows-

Revenue recognition

According to the auditor of the company, there is a level of complexity in operations of

billing system implemented by the management of the company. Recognition of revenue for

long-term contracts, new products and timing of revenue was complex that is the reason that

it is included in key audit matters. It is the general practice of every business organizations to

record revenue when there are certain that revenue will be received from customer and

possession of goods and services are transferred from company to customer. Auditor of the

company has analyzed all the procedures used by management in order to record the specific

transactions (Vik and Walter, 2017). Auditor has also analysed the Master Data of

Information Technology system that are used for recording these transactions. The

comparison has also been made by the auditor with revenue recognition processes used by

other communication companies in the industry.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acquisition of Trustwave

Business decisions in relation to merger and acquisition are always very important for

stakeholders of the company as they are acquiring a substantial interest in other companies.

During the financial year under consideration, Optus has acquired the business of Trustwave

holding Incorporation. According to the accounting principle in relation to business

acquisition and business combination, there are specific rules and regulations that should be

followed by management while accounting for merger and acquisition (Cordoş and Fülöp,

2015). Management of office has valued intangible assets 186.8 million dollars and Goodwill

at 1069.8 million dollars.

The discussion has been conducted with management and directors of Optus in order to

identify the process used by them in order to acquire the business of Trustwave. Auditor has

also hired business experts in the field of merger and acquisition as an expert in order to

verify the processes used by management for business combinations. After analyzing all

these processes, auditor as identified that all the processes are in accordance with FRS 103

which describes Accounting Principles in relation to a business combination (McKee, 2015).

Auditors have also noted that all the valuations in relation to Goodwill and intangible assets

are based on reasonable assumptions.

Taxation

Optus is operating in various accession jurisdictions, therefore they have to follow taxation

rules and regulations in relation to different jurisdictions. Due to complexities in tax rules

applicable to the company, this matter has been included in key audit matters. Auditor of the

company has consulted with other taxation experts in the audit firm in order to verify the

accuracy of tax paid by the organisation for the current year. Relevance and completeness of

all the disclosures made by management in financial statements of the company are also

evaluated. After conducting this analysis, the auditor of the company is satisfied with the

Calculation and representation of taxation policies.

Goodwill impairment

According to the accounting principles of FRS, good values required to be evaluated at the

end of every financial year (Velte, 2018). Goodwill valuation at the end of year requires a lot

of assumptions on the part of management which can be very subjective. Auditor of the

company has evaluated all these assumptions and calculations made by management for

8

Business decisions in relation to merger and acquisition are always very important for

stakeholders of the company as they are acquiring a substantial interest in other companies.

During the financial year under consideration, Optus has acquired the business of Trustwave

holding Incorporation. According to the accounting principle in relation to business

acquisition and business combination, there are specific rules and regulations that should be

followed by management while accounting for merger and acquisition (Cordoş and Fülöp,

2015). Management of office has valued intangible assets 186.8 million dollars and Goodwill

at 1069.8 million dollars.

The discussion has been conducted with management and directors of Optus in order to

identify the process used by them in order to acquire the business of Trustwave. Auditor has

also hired business experts in the field of merger and acquisition as an expert in order to

verify the processes used by management for business combinations. After analyzing all

these processes, auditor as identified that all the processes are in accordance with FRS 103

which describes Accounting Principles in relation to a business combination (McKee, 2015).

Auditors have also noted that all the valuations in relation to Goodwill and intangible assets

are based on reasonable assumptions.

Taxation

Optus is operating in various accession jurisdictions, therefore they have to follow taxation

rules and regulations in relation to different jurisdictions. Due to complexities in tax rules

applicable to the company, this matter has been included in key audit matters. Auditor of the

company has consulted with other taxation experts in the audit firm in order to verify the

accuracy of tax paid by the organisation for the current year. Relevance and completeness of

all the disclosures made by management in financial statements of the company are also

evaluated. After conducting this analysis, the auditor of the company is satisfied with the

Calculation and representation of taxation policies.

Goodwill impairment

According to the accounting principles of FRS, good values required to be evaluated at the

end of every financial year (Velte, 2018). Goodwill valuation at the end of year requires a lot

of assumptions on the part of management which can be very subjective. Auditor of the

company has evaluated all these assumptions and calculations made by management for

8

Goodwill valuation and calculation of goodwill impairment. The auditor is satisfied with the

Calculation and accounting treatment are done by management in relation to Goodwill.

Audit committee

Audit committee

There was an audit committee that was watching the function of audit for the year ending

2016. This audit committee includes 4 members that are Bobby Chin (Chairman), Christina

Ong, Peter Ong, and Teo Swee Lian. Detailed charter is maintained by the board of directors

of the company that defines the structure, functions, responsibilities, and accountability of the

audit committee. According to this charter, there should be minimum three members in the

audit committee and the primary goal of this audit committee is to conduct effective and

efficient internal as well as external audit. Financial statements prepared by management are

also required to be approved by this audit committee before initiating the process of audit. It

is essential for the audit committee to conduct meetings in every financial year for the

discussion of improving the quality of the internal and external audit (Sultana, Singh and Van

der Zahn, 2015). All the suggestions made and discussion done in this audit committee will

be included in a minute of the company.

Audit opinion

The audit opinion is the views presented by the auditor of the company on accuracy and

relevance of financial statements maintained by management. This is the statement that

stakeholders of the company rely on for making investment decisions. for the financial year

and in 2016, Deloitte LLP has expressed their opinion that the financial position of the

company increases properly represented in financial statements i.e. they are representing the

true and fair value of the company (Cohen and Simnett, 2014). They also stated that all the

accounting principles and other rules regulated by accounting authorities and government of

Australia are effectively followed by management. On the basis of this opinion, it can be said

that the stakeholders of the company can rely upon financial statements of the country.

Director’s responsibility

1. To act in best interest of the company, management, employees and society in which

business organization is operating.

9

Calculation and accounting treatment are done by management in relation to Goodwill.

Audit committee

Audit committee

There was an audit committee that was watching the function of audit for the year ending

2016. This audit committee includes 4 members that are Bobby Chin (Chairman), Christina

Ong, Peter Ong, and Teo Swee Lian. Detailed charter is maintained by the board of directors

of the company that defines the structure, functions, responsibilities, and accountability of the

audit committee. According to this charter, there should be minimum three members in the

audit committee and the primary goal of this audit committee is to conduct effective and

efficient internal as well as external audit. Financial statements prepared by management are

also required to be approved by this audit committee before initiating the process of audit. It

is essential for the audit committee to conduct meetings in every financial year for the

discussion of improving the quality of the internal and external audit (Sultana, Singh and Van

der Zahn, 2015). All the suggestions made and discussion done in this audit committee will

be included in a minute of the company.

Audit opinion

The audit opinion is the views presented by the auditor of the company on accuracy and

relevance of financial statements maintained by management. This is the statement that

stakeholders of the company rely on for making investment decisions. for the financial year

and in 2016, Deloitte LLP has expressed their opinion that the financial position of the

company increases properly represented in financial statements i.e. they are representing the

true and fair value of the company (Cohen and Simnett, 2014). They also stated that all the

accounting principles and other rules regulated by accounting authorities and government of

Australia are effectively followed by management. On the basis of this opinion, it can be said

that the stakeholders of the company can rely upon financial statements of the country.

Director’s responsibility

1. To act in best interest of the company, management, employees and society in which

business organization is operating.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Ensuring that management of the company is achieving its goals and objectives in a given

period of time.

3. Directors are also responsible for the planning of internal controls and to ensure that these

internal controls are properly implemented in the organization.

Auditor of the company is not responsible for implementing internal controls or checking the

execution of internal control (Knechel and Salterio, 2016). The auditor is only responsible for

checking the efficiency and effectiveness of these internal controls.

Management’s responsibility

Management of the company is responsible for the execution of all the plans and policies

prepared by directors of the company. Management is accountable towards directors of the

company in relation to operations performed according to plans prepared by them.

Responsibilities of directors, management and auditor are totally different from each other.

Financial statements are prepared by management, approved by the board of directors and

verified by the auditor of a company (Goetsch and Davis, 2014). Another aspect of these

difference can also be effectively evaluated with the help of identifying the responsibilities of

detection of fraud. The primary responsibility of detection of fraud lies with management and

directors. Auditor of the company is responsible for Risk identification but they are not

responsible for correcting these frauds. Auditor of the company is liable to report all the

frauds conducted by management to shareholders and government of the country.

Audit report and financial statements analysis

From the perspective of stakeholders, it can be said that the audit process conducted in the

year ending 2016 was effective and efficient. As mentioned by auditor all the rules and

regulations that should be followed by management in order to prepare financial statements

are identified and followed correctly during the preparation of financial statements (Cheng,

Ioannou and Serafeim, 2014).

Subsequent events

During the financial year under consideration, there were no subsequent events that can affect

the decision of stakeholders. These events generally occur between the date of financial

statements and date of presenting financial statements to stakeholders. In this financial year,

there was no any material events that that can have a positive or negative impact on the

10

period of time.

3. Directors are also responsible for the planning of internal controls and to ensure that these

internal controls are properly implemented in the organization.

Auditor of the company is not responsible for implementing internal controls or checking the

execution of internal control (Knechel and Salterio, 2016). The auditor is only responsible for

checking the efficiency and effectiveness of these internal controls.

Management’s responsibility

Management of the company is responsible for the execution of all the plans and policies

prepared by directors of the company. Management is accountable towards directors of the

company in relation to operations performed according to plans prepared by them.

Responsibilities of directors, management and auditor are totally different from each other.

Financial statements are prepared by management, approved by the board of directors and

verified by the auditor of a company (Goetsch and Davis, 2014). Another aspect of these

difference can also be effectively evaluated with the help of identifying the responsibilities of

detection of fraud. The primary responsibility of detection of fraud lies with management and

directors. Auditor of the company is responsible for Risk identification but they are not

responsible for correcting these frauds. Auditor of the company is liable to report all the

frauds conducted by management to shareholders and government of the country.

Audit report and financial statements analysis

From the perspective of stakeholders, it can be said that the audit process conducted in the

year ending 2016 was effective and efficient. As mentioned by auditor all the rules and

regulations that should be followed by management in order to prepare financial statements

are identified and followed correctly during the preparation of financial statements (Cheng,

Ioannou and Serafeim, 2014).

Subsequent events

During the financial year under consideration, there were no subsequent events that can affect

the decision of stakeholders. These events generally occur between the date of financial

statements and date of presenting financial statements to stakeholders. In this financial year,

there was no any material events that that can have a positive or negative impact on the

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial position of the company (Nobes, 2014). Identification of this subsequent event is

very important as management is required to alter their financial accounts in order to

incorporate these events before presenting financial statements in the Annual General

Meeting.

Underreporting of material misstatement

It is already established that audit conducted in Optus limited is effective and according to

rules and regulations maintained by the government of Australia. It can be said that all the

material in statements is identified and reported in the audit report. Follow up a question that

can be asked in Annual General Meeting from management and auditor is to provide more

information in relation to acquisition done by Optus in 2016. Merger and business

acquisitions are very important decisions that can affect to ownership of shareholders and

return on Investments. Therefore shareholders of the company have the right to evaluate all

the particulars of such decision.

11

very important as management is required to alter their financial accounts in order to

incorporate these events before presenting financial statements in the Annual General

Meeting.

Underreporting of material misstatement

It is already established that audit conducted in Optus limited is effective and according to

rules and regulations maintained by the government of Australia. It can be said that all the

material in statements is identified and reported in the audit report. Follow up a question that

can be asked in Annual General Meeting from management and auditor is to provide more

information in relation to acquisition done by Optus in 2016. Merger and business

acquisitions are very important decisions that can affect to ownership of shareholders and

return on Investments. Therefore shareholders of the company have the right to evaluate all

the particulars of such decision.

11

Conclusion

This report has successfully identified and evaluated all the audit matters discussed in audit

report issued by Auditor. In addition to key audit matters, other audit matters are so discussed

in this report such as independent of auditor, audit committee, roles, and responsibility of

Management and directors, role of auditor, etc. after analyzing all the particulars given in

annual report, it can be said that relevant and accurate information is provided in financial

statements by management. There are no frauds or material misstatements in financial

statements that can expect decision-making process of stakeholder.

12

This report has successfully identified and evaluated all the audit matters discussed in audit

report issued by Auditor. In addition to key audit matters, other audit matters are so discussed

in this report such as independent of auditor, audit committee, roles, and responsibility of

Management and directors, role of auditor, etc. after analyzing all the particulars given in

annual report, it can be said that relevant and accurate information is provided in financial

statements by management. There are no frauds or material misstatements in financial

statements that can expect decision-making process of stakeholder.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.