Financial Report Analysis: Comparing Sirtex and Altech Chemicals

VerifiedAdded on 2020/05/16

|25

|5240

|87

Report

AI Summary

This report provides a comprehensive analysis of the financial statements of Sirtex Medical Limited and Altech Chemical Limited, two companies from different industries. The analysis focuses on four key areas: leases, liabilities (including contingent liabilities and provisions), earnings per share (EPS), and intangible assets. The report examines the companies' policies, the impact of accounting standards (particularly AASB 16 on leases), and compares their financial performance in these areas. It includes a literature review of relevant studies and offers findings and recommendations based on the analysis. The report also covers the concept of EPS, its calculation, and its significance for investors, highlighting the contrasting EPS performance of the two companies. The report provides a clear understanding of the financial health and performance of these two companies based on the specific financial statement areas highlighted in the report.

Running head: CORPORATE FINANCIAL REPORT ANALYSIS

CORPORATE FINANCIAL REPORT ANALYSIS

Name of the Student:

Name of the University:

Author’s Note:

CORPORATE FINANCIAL REPORT ANALYSIS

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE FINANCIAL REPORT ANALYSIS

Executive Summary

The main purpose of this report is to analyze the financial statements of two separate companies

which belong to different industries. The report will be analyzing four different area of the

financial statement and what impacts theses assets have on the financial report of the companies.

The area which this report will be discussing are leases, liabilities including contingent liabilities

and provisions, Earning per share, intangible assets. The two selected companies for this

assignment are Sirtex Medical Limited and Altech Chemical Limited.

CORPORATE FINANCIAL REPORT ANALYSIS

Executive Summary

The main purpose of this report is to analyze the financial statements of two separate companies

which belong to different industries. The report will be analyzing four different area of the

financial statement and what impacts theses assets have on the financial report of the companies.

The area which this report will be discussing are leases, liabilities including contingent liabilities

and provisions, Earning per share, intangible assets. The two selected companies for this

assignment are Sirtex Medical Limited and Altech Chemical Limited.

2

CORPORATE FINANCIAL REPORT ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Overview......................................................................................................................................3

Part 1................................................................................................................................................3

Concept........................................................................................................................................3

Company Analysis of Leases.......................................................................................................4

Literature Review........................................................................................................................6

Measures and Findings................................................................................................................7

Part 2................................................................................................................................................7

Concept........................................................................................................................................7

Company Analysis of EPS...........................................................................................................8

Literature Review........................................................................................................................9

Measures and Findings..............................................................................................................10

Part 3..............................................................................................................................................10

Concepts....................................................................................................................................10

Company Analysis.....................................................................................................................10

Literature Review......................................................................................................................11

Measures and Findings..............................................................................................................12

Part 4..............................................................................................................................................13

Concept......................................................................................................................................13

CORPORATE FINANCIAL REPORT ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Overview......................................................................................................................................3

Part 1................................................................................................................................................3

Concept........................................................................................................................................3

Company Analysis of Leases.......................................................................................................4

Literature Review........................................................................................................................6

Measures and Findings................................................................................................................7

Part 2................................................................................................................................................7

Concept........................................................................................................................................7

Company Analysis of EPS...........................................................................................................8

Literature Review........................................................................................................................9

Measures and Findings..............................................................................................................10

Part 3..............................................................................................................................................10

Concepts....................................................................................................................................10

Company Analysis.....................................................................................................................10

Literature Review......................................................................................................................11

Measures and Findings..............................................................................................................12

Part 4..............................................................................................................................................13

Concept......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE FINANCIAL REPORT ANALYSIS

Company Analysis.....................................................................................................................13

Literature Review......................................................................................................................14

Measures and Findings..............................................................................................................15

Conclusion.....................................................................................................................................15

Reference.......................................................................................................................................17

CORPORATE FINANCIAL REPORT ANALYSIS

Company Analysis.....................................................................................................................13

Literature Review......................................................................................................................14

Measures and Findings..............................................................................................................15

Conclusion.....................................................................................................................................15

Reference.......................................................................................................................................17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE FINANCIAL REPORT ANALYSIS

Introduction

The main purpose of this report is to analyze two company’s financial report which

belong two different industries. The companies which are selected for this report are Sirtex

Medical ltd and Altech Chemical ltd. The report will also be analyzing specific areas of the

financial statement and a comparison will be made between the two companies.

Overview

Sirtex Medical Limited is an Australian company which is engaged in providing medical

treatment to the society. The company also provides medical services to the society and treats

patients. The company specializes in radioactive treatment for inoperable liver cancer. The

company has its headquarter situated in Australia and the company was established in 1997.

(Sirtex.com 2018).

The other company which is selected for this assignment is Altech Chemical Ltd which

has its headquarters in Australia and it is also listed in the Australian stock exchange

(Altechchemicals.com, 2018). The company is engaged in providing material and supply of

minerals. The company specializes in the production of alumina. The company is engaged in

exploration and mining activities.

Part 1

Concept

Leasing is the process of financing which is used by the companies in day to day

business. In a lease agreement, the lessor gives the right to use the property of the lessor to an

individual who is known as lessee for a certain rate of interest. Nowadays lease agreement are

used by businesses extensively for business purposes. The application of leases are more

CORPORATE FINANCIAL REPORT ANALYSIS

Introduction

The main purpose of this report is to analyze two company’s financial report which

belong two different industries. The companies which are selected for this report are Sirtex

Medical ltd and Altech Chemical ltd. The report will also be analyzing specific areas of the

financial statement and a comparison will be made between the two companies.

Overview

Sirtex Medical Limited is an Australian company which is engaged in providing medical

treatment to the society. The company also provides medical services to the society and treats

patients. The company specializes in radioactive treatment for inoperable liver cancer. The

company has its headquarter situated in Australia and the company was established in 1997.

(Sirtex.com 2018).

The other company which is selected for this assignment is Altech Chemical Ltd which

has its headquarters in Australia and it is also listed in the Australian stock exchange

(Altechchemicals.com, 2018). The company is engaged in providing material and supply of

minerals. The company specializes in the production of alumina. The company is engaged in

exploration and mining activities.

Part 1

Concept

Leasing is the process of financing which is used by the companies in day to day

business. In a lease agreement, the lessor gives the right to use the property of the lessor to an

individual who is known as lessee for a certain rate of interest. Nowadays lease agreement are

used by businesses extensively for business purposes. The application of leases are more

5

CORPORATE FINANCIAL REPORT ANALYSIS

prominently used in airline industry, retail industry and shipping industries (Schallheim, Wells

and Whitby 2013). Some of the airline business are also in the business of leasing the aircraft

which is used in the business. Generally leases are of two types operating leases and financial

leases. Operating leases is the lease which is of a short term basis and which is used by

businesses to acquire equipment on short term basis. Generally the useful life of the asset

acquired in an operating lease is more than the term of use of the lease. As per the previous

standard on leasing operating leases were not disclosed and represented in the balance sheet of

the company. Financial leases are more frequently used in business where assets are brought by

the lessor in order to finance theses to the lessee for a certain rate of interest. Financial leases are

recorded in the financial reports of the business.

Company Analysis of Leases

As per the balance sheet of Sirtex Medical ltd, the terms of leases of the company are that the

lease payments for operating leases, where all the risks and benefits remain with the lessor and

charged as expenses in the period in which such expenses are incurred. All leases are recognized

as a liability and amortised accordingly on the straight line basis as per the policy of the

company. Sirtex Medical ltd has recently replaced AASB 117 with the new lease standard AASB

16 which recognizes all leases as liability and are accounted for on balance sheet, other than

short term and low value leases. The new lease standard provides new effect on the definition,

application, sales and back accounting of lease transactions (Cornaggia, Franzen and Simin

2012). The new standard also requires proper disclosures of the same in the annual reports of the

company. As the management has implemented the new AASB 16 currently so the effect on the

financial report is not ascertained completely. However the management expects the following

changes will take place:

CORPORATE FINANCIAL REPORT ANALYSIS

prominently used in airline industry, retail industry and shipping industries (Schallheim, Wells

and Whitby 2013). Some of the airline business are also in the business of leasing the aircraft

which is used in the business. Generally leases are of two types operating leases and financial

leases. Operating leases is the lease which is of a short term basis and which is used by

businesses to acquire equipment on short term basis. Generally the useful life of the asset

acquired in an operating lease is more than the term of use of the lease. As per the previous

standard on leasing operating leases were not disclosed and represented in the balance sheet of

the company. Financial leases are more frequently used in business where assets are brought by

the lessor in order to finance theses to the lessee for a certain rate of interest. Financial leases are

recorded in the financial reports of the business.

Company Analysis of Leases

As per the balance sheet of Sirtex Medical ltd, the terms of leases of the company are that the

lease payments for operating leases, where all the risks and benefits remain with the lessor and

charged as expenses in the period in which such expenses are incurred. All leases are recognized

as a liability and amortised accordingly on the straight line basis as per the policy of the

company. Sirtex Medical ltd has recently replaced AASB 117 with the new lease standard AASB

16 which recognizes all leases as liability and are accounted for on balance sheet, other than

short term and low value leases. The new lease standard provides new effect on the definition,

application, sales and back accounting of lease transactions (Cornaggia, Franzen and Simin

2012). The new standard also requires proper disclosures of the same in the annual reports of the

company. As the management has implemented the new AASB 16 currently so the effect on the

financial report is not ascertained completely. However the management expects the following

changes will take place:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE FINANCIAL REPORT ANALYSIS

a. Significant increase in the leases assets and financial liabilities in the balance sheet.

b. The value of lease assets will decrease more quickly than lease liabilities due to the effect

of reported equity

c. EBIT as shown in the profit and loss account will be higher as former leases interest will

all be part of the finance cost of the business.

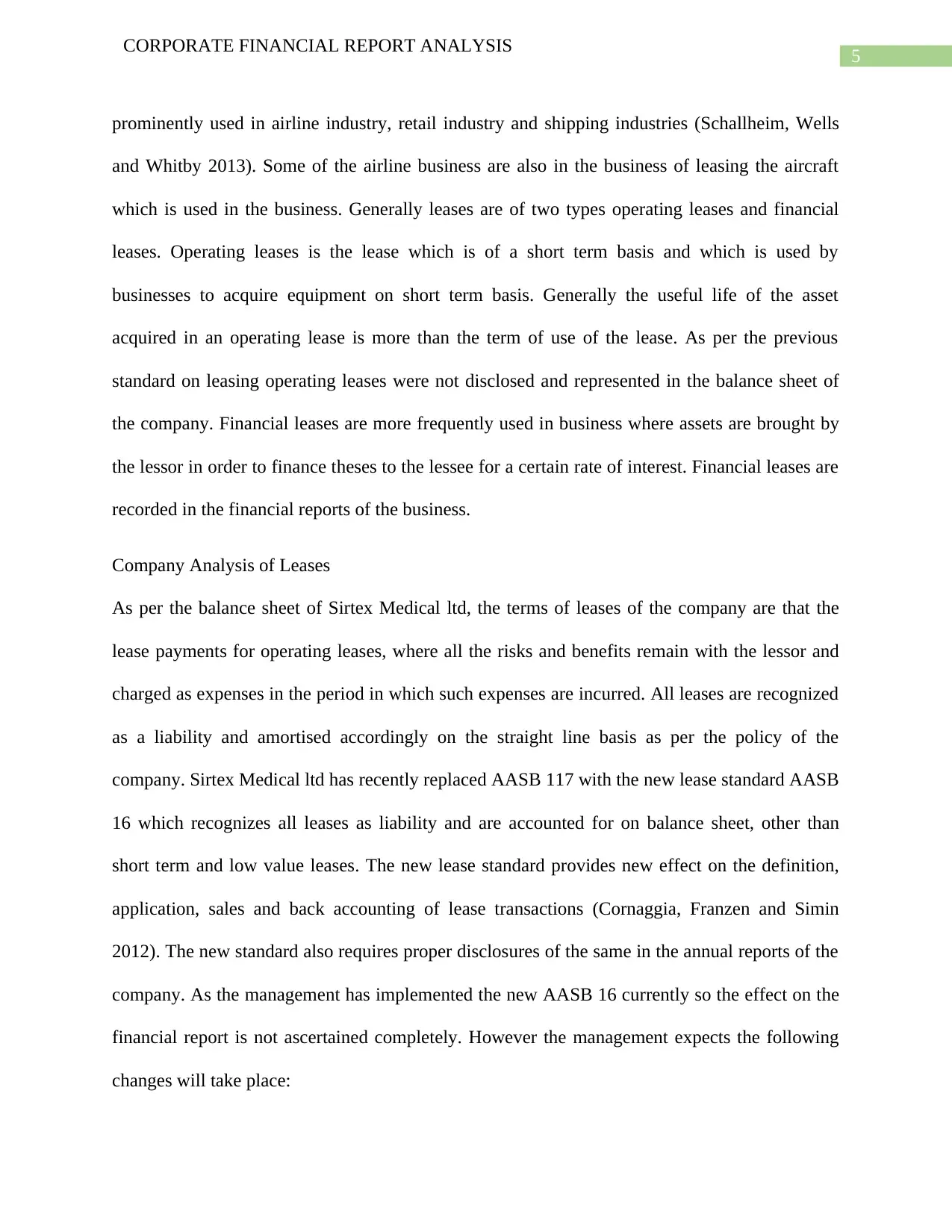

The consolidated balance sheet shows that the company has leases in Sydney, Singapore,

Germany and also in United States. The duration and the remaining useful life of such leases

are shown in the figure below:

Figure1: Table showing Operating Leases of Sirtex Medical ltd as per 2016 annual

reports

Source: (Sirtex.com 2018)

As per the annual report of Altech Chemical ltd for 2016, shows that the company has

leases in the financial statements. As per the company’s policy such leases are recognized as

operating or financial leases based on the economic substance of the lease which reflect the risk

and benefits associated with that particular lease. The company policy is to recognize the leases

as per the old standard of the company and apply straight line method of amortization on such

leases. The company plans to introduce AASB 16 from 1st January 2019, till then the old

CORPORATE FINANCIAL REPORT ANALYSIS

a. Significant increase in the leases assets and financial liabilities in the balance sheet.

b. The value of lease assets will decrease more quickly than lease liabilities due to the effect

of reported equity

c. EBIT as shown in the profit and loss account will be higher as former leases interest will

all be part of the finance cost of the business.

The consolidated balance sheet shows that the company has leases in Sydney, Singapore,

Germany and also in United States. The duration and the remaining useful life of such leases

are shown in the figure below:

Figure1: Table showing Operating Leases of Sirtex Medical ltd as per 2016 annual

reports

Source: (Sirtex.com 2018)

As per the annual report of Altech Chemical ltd for 2016, shows that the company has

leases in the financial statements. As per the company’s policy such leases are recognized as

operating or financial leases based on the economic substance of the lease which reflect the risk

and benefits associated with that particular lease. The company policy is to recognize the leases

as per the old standard of the company and apply straight line method of amortization on such

leases. The company plans to introduce AASB 16 from 1st January 2019, till then the old

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE FINANCIAL REPORT ANALYSIS

standard will be used in order to recognize leases. As per the management of Altech Chemical

ltd AASB 16 will introduce change in the management by not differentiating operating and

financial leases from each other. The management of the company is of the view that the new

standards implementation will be affecting the Group’s financial statement but the exact estimate

of impact is not possible to predict. As per the annual reports of the company for 2016, the

company holds various mineral leases which they can use for exploration. The company is in the

production of minerals and production of alumina.

Literature Review

As per studies show that as per the old standard on leases there are two types of leases

which are recognized. One is the capital leases or finance lease which is shown in the financial

statements and another is off balance sheet leases which are operating leases which are not

recorded in the balance sheet of the company (Altamuro et al. 2014). In an article it is shown

that a large number of business uses off balance sheet leases or operating leases in order to

strengthen their balance sheet as the level of debts are not shown in such a balance sheet. Various

time series data show such similar results (Cornaggia, Franzen and Simin 2012). Another study

which was conducted on Hong Kong fast food industry shows the problem of implementation of

the new standard of leasing. The lease was introduced by IASB in order to tackle the problems

which the previous standard faced. The other aim was to ensure that the financial statements

reflect true economic reality of the company (Tai 2013). A recent study shows that a research

was conducted on how much amount of operating leases companies uses in order to finance their

activities. The research was conducted on the top 40 JSE listed companies. The aim of the

research is to show how the new standard on leases will impact such companies (De Villiers and

Middelberg 2013). An investigation was undertaken to the effect of capitalizing operating

CORPORATE FINANCIAL REPORT ANALYSIS

standard will be used in order to recognize leases. As per the management of Altech Chemical

ltd AASB 16 will introduce change in the management by not differentiating operating and

financial leases from each other. The management of the company is of the view that the new

standards implementation will be affecting the Group’s financial statement but the exact estimate

of impact is not possible to predict. As per the annual reports of the company for 2016, the

company holds various mineral leases which they can use for exploration. The company is in the

production of minerals and production of alumina.

Literature Review

As per studies show that as per the old standard on leases there are two types of leases

which are recognized. One is the capital leases or finance lease which is shown in the financial

statements and another is off balance sheet leases which are operating leases which are not

recorded in the balance sheet of the company (Altamuro et al. 2014). In an article it is shown

that a large number of business uses off balance sheet leases or operating leases in order to

strengthen their balance sheet as the level of debts are not shown in such a balance sheet. Various

time series data show such similar results (Cornaggia, Franzen and Simin 2012). Another study

which was conducted on Hong Kong fast food industry shows the problem of implementation of

the new standard of leasing. The lease was introduced by IASB in order to tackle the problems

which the previous standard faced. The other aim was to ensure that the financial statements

reflect true economic reality of the company (Tai 2013). A recent study shows that a research

was conducted on how much amount of operating leases companies uses in order to finance their

activities. The research was conducted on the top 40 JSE listed companies. The aim of the

research is to show how the new standard on leases will impact such companies (De Villiers and

Middelberg 2013). An investigation was undertaken to the effect of capitalizing operating

8

CORPORATE FINANCIAL REPORT ANALYSIS

leases on firm’s immediacy to

their debt covenant violations. The results of analysis show that the US companies uses such

leases as instruments for generating capitalization in the companies (Lee, Paik and Yoon 2014).

Measures and Findings

As per the analysis of the above area on the lease of both the companies the following

recommendations can be suggested which are given below:

1. Sirtex Medical Limited has implemented the new standard AASB 16 which records all

kinds of leases, however Altech Chemical has not yet implemented the new standard and

therefore the company should implement the new standard as soon as possible earlier

than 2019.

2. The operating leases of Sirtex limited is much more as compared to Altech limited which

can be reduced as with the implementation of the new standard the cost of the company

will also be increasing.

3. Both company uses straight line of amortization of such leases.

Part 2

Concept

Earning per share is that portion of profit which can be attributed to each and every

issued share capital of the company. In other words Earning per share(EPS) is the amount of

profit per share which the investors of the company receives as dividends. As per the formula

EPS is calculated by dividing Profit after tax (PAT) by the total number of shareholders of the

company. a company which has high EPS is capable to provide dividends to the public or it can

use this profits as retained earnings and reinvest in the business for the further growth of the

CORPORATE FINANCIAL REPORT ANALYSIS

leases on firm’s immediacy to

their debt covenant violations. The results of analysis show that the US companies uses such

leases as instruments for generating capitalization in the companies (Lee, Paik and Yoon 2014).

Measures and Findings

As per the analysis of the above area on the lease of both the companies the following

recommendations can be suggested which are given below:

1. Sirtex Medical Limited has implemented the new standard AASB 16 which records all

kinds of leases, however Altech Chemical has not yet implemented the new standard and

therefore the company should implement the new standard as soon as possible earlier

than 2019.

2. The operating leases of Sirtex limited is much more as compared to Altech limited which

can be reduced as with the implementation of the new standard the cost of the company

will also be increasing.

3. Both company uses straight line of amortization of such leases.

Part 2

Concept

Earning per share is that portion of profit which can be attributed to each and every

issued share capital of the company. In other words Earning per share(EPS) is the amount of

profit per share which the investors of the company receives as dividends. As per the formula

EPS is calculated by dividing Profit after tax (PAT) by the total number of shareholders of the

company. a company which has high EPS is capable to provide dividends to the public or it can

use this profits as retained earnings and reinvest in the business for the further growth of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE FINANCIAL REPORT ANALYSIS

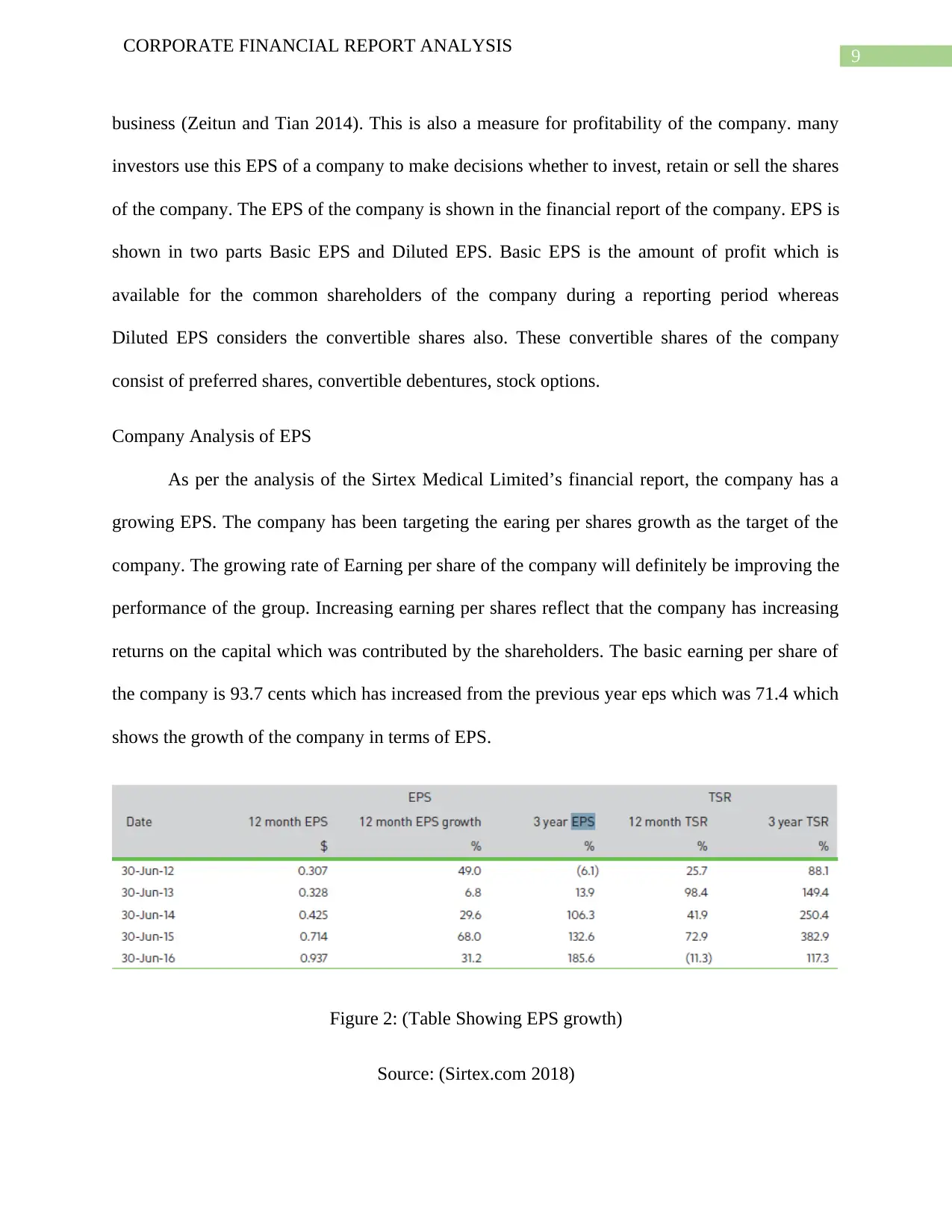

business (Zeitun and Tian 2014). This is also a measure for profitability of the company. many

investors use this EPS of a company to make decisions whether to invest, retain or sell the shares

of the company. The EPS of the company is shown in the financial report of the company. EPS is

shown in two parts Basic EPS and Diluted EPS. Basic EPS is the amount of profit which is

available for the common shareholders of the company during a reporting period whereas

Diluted EPS considers the convertible shares also. These convertible shares of the company

consist of preferred shares, convertible debentures, stock options.

Company Analysis of EPS

As per the analysis of the Sirtex Medical Limited’s financial report, the company has a

growing EPS. The company has been targeting the earing per shares growth as the target of the

company. The growing rate of Earning per share of the company will definitely be improving the

performance of the group. Increasing earning per shares reflect that the company has increasing

returns on the capital which was contributed by the shareholders. The basic earning per share of

the company is 93.7 cents which has increased from the previous year eps which was 71.4 which

shows the growth of the company in terms of EPS.

Figure 2: (Table Showing EPS growth)

Source: (Sirtex.com 2018)

CORPORATE FINANCIAL REPORT ANALYSIS

business (Zeitun and Tian 2014). This is also a measure for profitability of the company. many

investors use this EPS of a company to make decisions whether to invest, retain or sell the shares

of the company. The EPS of the company is shown in the financial report of the company. EPS is

shown in two parts Basic EPS and Diluted EPS. Basic EPS is the amount of profit which is

available for the common shareholders of the company during a reporting period whereas

Diluted EPS considers the convertible shares also. These convertible shares of the company

consist of preferred shares, convertible debentures, stock options.

Company Analysis of EPS

As per the analysis of the Sirtex Medical Limited’s financial report, the company has a

growing EPS. The company has been targeting the earing per shares growth as the target of the

company. The growing rate of Earning per share of the company will definitely be improving the

performance of the group. Increasing earning per shares reflect that the company has increasing

returns on the capital which was contributed by the shareholders. The basic earning per share of

the company is 93.7 cents which has increased from the previous year eps which was 71.4 which

shows the growth of the company in terms of EPS.

Figure 2: (Table Showing EPS growth)

Source: (Sirtex.com 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE FINANCIAL REPORT ANALYSIS

As per the balance sheet of Altech Chemical ltd, the EPS of the company is subdivided in

basic and diluted EPS. The basic earning per shares is calculated by dividing net loss by the

weighted average number of shares of the company. The diluted earning per share is calculated

by dividing net loss by weighted average number of shares and also dilutive potential shares. The

basic EPS of the company is in negative figure .0008 which has slightly improved from the

previous year figure.

While analyzing the EPS of both the companies it is easily depicted that the EPS of the

Sirtex ltd is much better than the EPS of Altech ltd. The basic reason for this is the Altech ltd has

incurred a loss in the year 2016 as well as 2015, thus the EPS depicts a negative figure.

Literature Review

The Eps of any company is a performance indicator of the company which the investors

consider in the business. It is also an indicator for the investors whether to invest in the stocks or

not. Thus investors and stock brokers consider the Eps of the company which has a growing Eps

rate in order to invest in them (Sumangala 2012). Earning per share of any company is

considered to be an important factor in order to determine the share price and value of the firm.

Recent studies show that most of the investors take their decisions about investing in a stock on

the basis of the EPS which the company has acquired (Islam et al. 2014). Any company is

required to show the Eps of the company in the financial statements. The earning per share is

divided into basic Eps and Diluted Eps (Jorgensen, Lee and Rock 2014). Earning per share is that

portion of profit which can be attributed to each and every issued share capital of the company.

In other words Earning per share(EPS) is the amount of profit per share which the investors of

the company receives as dividends. As per the formula EPS is calculated by dividing Profit after

tax (PAT) by the total number of shareholders of the company (Bonaimé 2012).

CORPORATE FINANCIAL REPORT ANALYSIS

As per the balance sheet of Altech Chemical ltd, the EPS of the company is subdivided in

basic and diluted EPS. The basic earning per shares is calculated by dividing net loss by the

weighted average number of shares of the company. The diluted earning per share is calculated

by dividing net loss by weighted average number of shares and also dilutive potential shares. The

basic EPS of the company is in negative figure .0008 which has slightly improved from the

previous year figure.

While analyzing the EPS of both the companies it is easily depicted that the EPS of the

Sirtex ltd is much better than the EPS of Altech ltd. The basic reason for this is the Altech ltd has

incurred a loss in the year 2016 as well as 2015, thus the EPS depicts a negative figure.

Literature Review

The Eps of any company is a performance indicator of the company which the investors

consider in the business. It is also an indicator for the investors whether to invest in the stocks or

not. Thus investors and stock brokers consider the Eps of the company which has a growing Eps

rate in order to invest in them (Sumangala 2012). Earning per share of any company is

considered to be an important factor in order to determine the share price and value of the firm.

Recent studies show that most of the investors take their decisions about investing in a stock on

the basis of the EPS which the company has acquired (Islam et al. 2014). Any company is

required to show the Eps of the company in the financial statements. The earning per share is

divided into basic Eps and Diluted Eps (Jorgensen, Lee and Rock 2014). Earning per share is that

portion of profit which can be attributed to each and every issued share capital of the company.

In other words Earning per share(EPS) is the amount of profit per share which the investors of

the company receives as dividends. As per the formula EPS is calculated by dividing Profit after

tax (PAT) by the total number of shareholders of the company (Bonaimé 2012).

11

CORPORATE FINANCIAL REPORT ANALYSIS

Measures and Findings

As per the analysis of the above area on the earning per share of both the companies the

following recommendations which can be provided are for Altech Chemical ltd. The company

needs to improve their earning per share as this is an important indicator of how the company is

performing. In addition to this the company needs strategies which can result in growth rates of

Eps like Sirtex ltd.

Part 3

Concepts

The liabilities of the company include the current and non current liabilities as per the

balance sheet. The current liabilities consist of all the liabilities which have to be paid off with in

a period of one year or even less such as trade payables and the non current liabilities includes

liabilities which are of long term nature such as long term debts. Trade payables or the creditors

which gives money or supplies to the company for credit (Kapan and Minoiu 2013). Long term

debts on the other hand are also credits which the business takes for a longer period say 4 to 5

years or even longer.

Company Analysis

As per the financial statement of Sirtex Medical Limited, the company has current

liabilities which includes trade payables and others, current tax liabilities and provisions. The

total of trade payables and others show a figure of $28090000 for the year 2016. The break up of

trade payable is $16296000 and the other payable as shown in the notes of accounts is

$11794000. Then comes the current tax liabilities of the business which refers to the liabilities

which relates to income tax of the company. The current tax liability of the company as per the

financial statement of 2016 shows $7239000. The provision refers to the amount which is kept

CORPORATE FINANCIAL REPORT ANALYSIS

Measures and Findings

As per the analysis of the above area on the earning per share of both the companies the

following recommendations which can be provided are for Altech Chemical ltd. The company

needs to improve their earning per share as this is an important indicator of how the company is

performing. In addition to this the company needs strategies which can result in growth rates of

Eps like Sirtex ltd.

Part 3

Concepts

The liabilities of the company include the current and non current liabilities as per the

balance sheet. The current liabilities consist of all the liabilities which have to be paid off with in

a period of one year or even less such as trade payables and the non current liabilities includes

liabilities which are of long term nature such as long term debts. Trade payables or the creditors

which gives money or supplies to the company for credit (Kapan and Minoiu 2013). Long term

debts on the other hand are also credits which the business takes for a longer period say 4 to 5

years or even longer.

Company Analysis

As per the financial statement of Sirtex Medical Limited, the company has current

liabilities which includes trade payables and others, current tax liabilities and provisions. The

total of trade payables and others show a figure of $28090000 for the year 2016. The break up of

trade payable is $16296000 and the other payable as shown in the notes of accounts is

$11794000. Then comes the current tax liabilities of the business which refers to the liabilities

which relates to income tax of the company. The current tax liability of the company as per the

financial statement of 2016 shows $7239000. The provision refers to the amount which is kept

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.