SIT718 Real World Analytics: Stock Price Prediction using R - ANZ

VerifiedAdded on 2023/03/31

|7

|1344

|324

Report

AI Summary

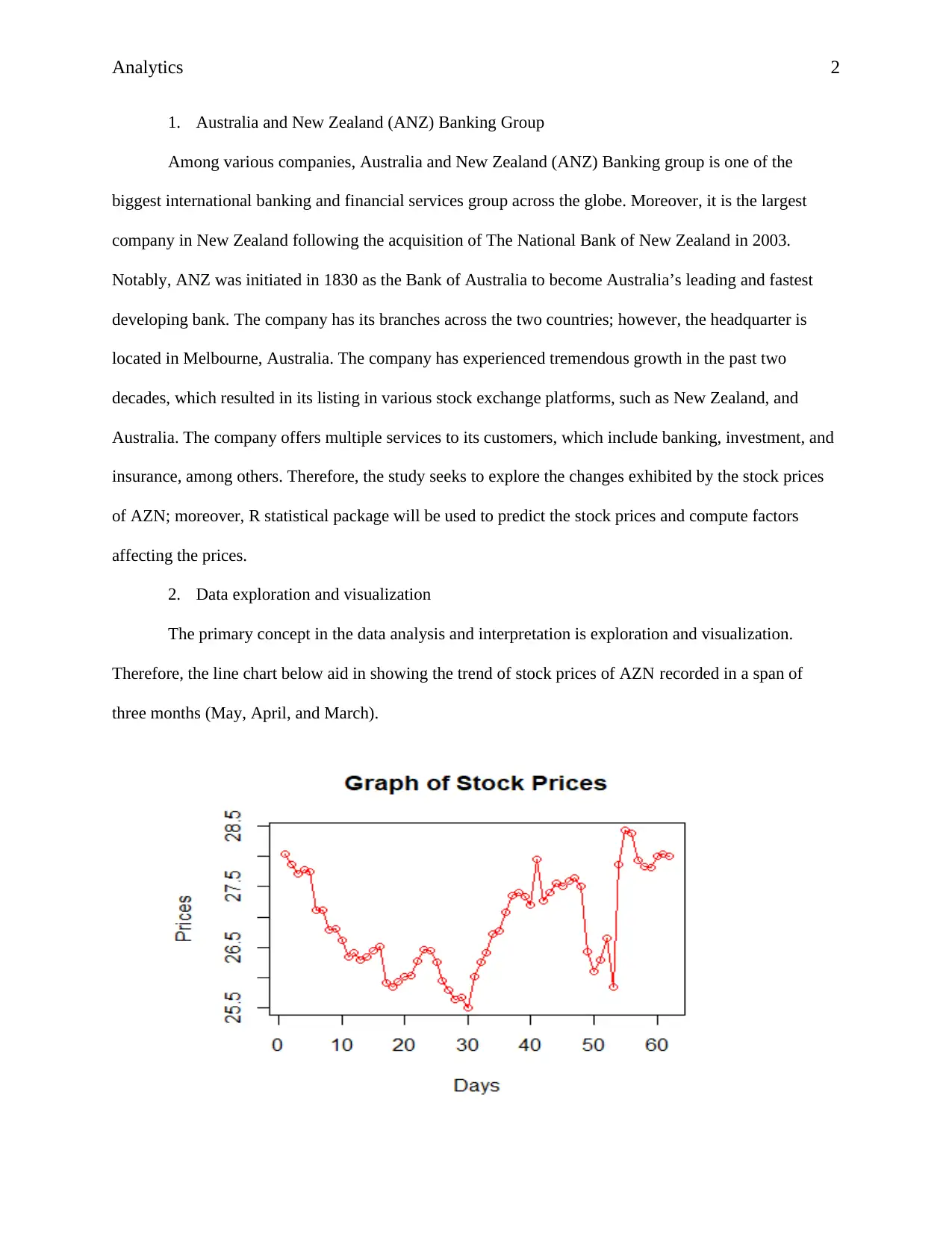

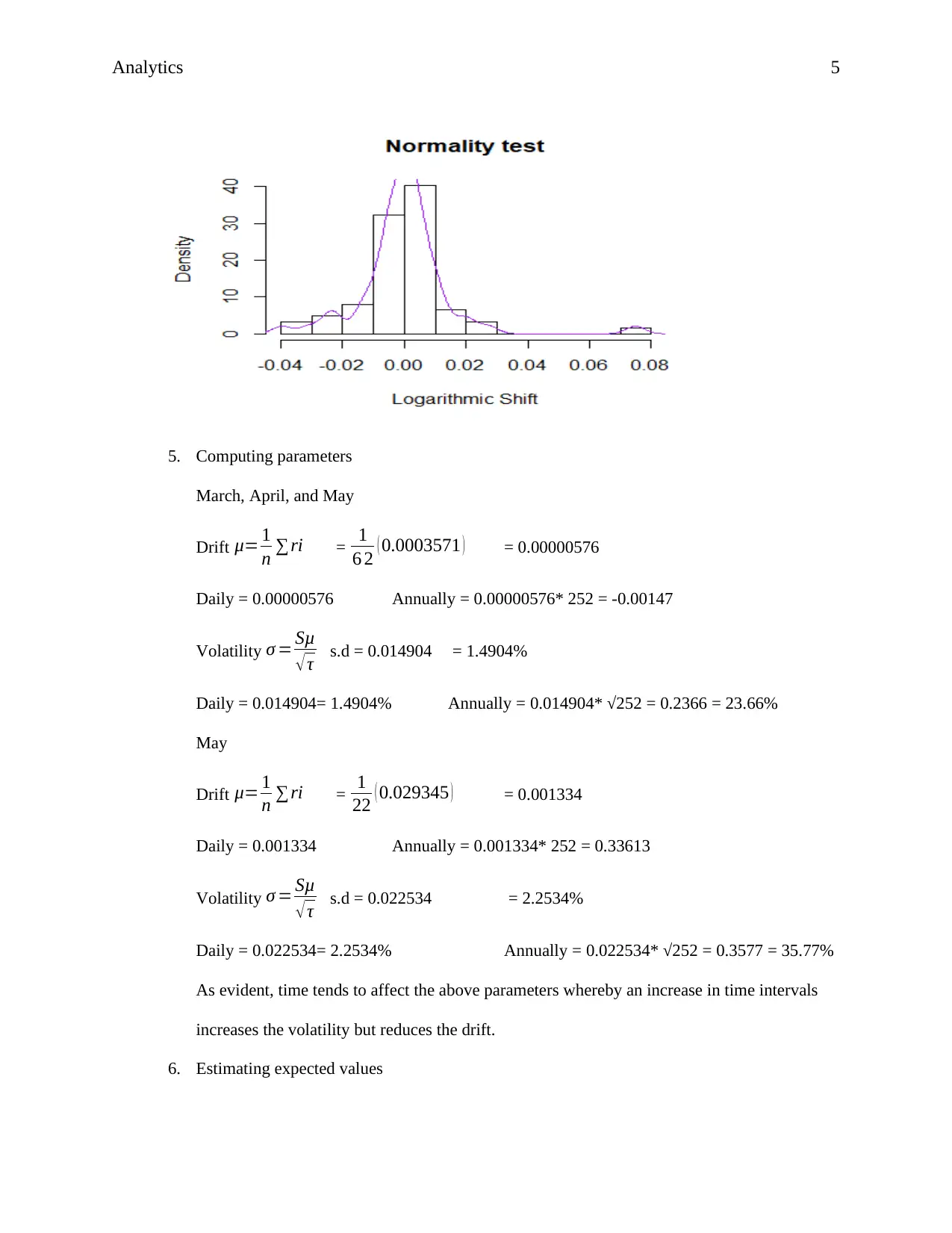

This report delves into the stock price analysis of Australia and New Zealand (ANZ) Banking Group, a major international financial institution. It utilizes R statistical package to explore and visualize stock price trends over a three-month period, employing stochastic modeling techniques, particularly Geometric Brownian Motion (GBM), to estimate and predict price movements. The analysis includes the computation of key parameters such as volatility and drift, examining their impact on stock prices. The report also assesses the normality property of the stock prices, crucial for GBM applicability, and estimates expected stock values, comparing them with actual published data. The study concludes by highlighting the factors influencing stock price instability and emphasizing the effectiveness of stochastic modeling in capturing these dynamics. It also provides the R code used for the analysis.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.