SITXFIN003 Manage Finances: Short Answer Assessment Questions

VerifiedAdded on 2023/06/03

|10

|2838

|322

Homework Assignment

AI Summary

This assignment presents a comprehensive exploration of financial management within a budgetary framework, focusing on the unit SITXFIN003. The document begins by defining a budget and its role in achieving business goals, followed by a discussion on resource allocation across departments and projects, differentiating between fixed and flexible budgets, and explaining cash flow and profit and loss budgets. It delves into key financial concepts like financial viability, profitability, and liquidity, while also examining the budget cycle and the importance of prioritizing and communicating budget decisions. The assignment then transitions to monitoring financial activities, comparing actual figures with budgeted amounts, and exploring the use of financial records, including the impact of computerized systems. It covers financial commitments, different types of expenses (fixed, variable, direct, and indirect), and the formulas for calculating budget variance. The document concludes by analyzing budget deviations, including the reasons for their occurrence and the steps for effective management, such as trend analysis, cost assessment, and the identification of options to improve budget performance, including revenue generation, payroll management and accounts payable.

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

ASSESSMENT B – SHORT ANSWER

INSTRUCTIONS

You are to answer all questions.

Read each question carefully. Ensure you have provided all required information.

On completion, submit your assessment to your assessor.

SECTION 1: ALLOCATE BUDGET RESOURCES

Q1: What is a budget and how does it help a business achieve its goals?

Definition

Is a detailed financial plan that shows estimated revenue and expenses for the given time

period.

Purpose

A budget is both planning and performance evaluation tool. They are prepared prior to a

specific period to assist in the business’ s planning processes and allocation of funds with

business.

Q2: What determines how business funds are divided amongst different departments and

projects?

The following are some of the factors that need to be considered when deciding the apt amount

of the business funds to be allocated to each department:

The projected amounts of the sale for the budget period for that department

The direct amount of the costs of sales for that department

The fixed and the variable costs that would be incurred for that department

Q3: What is the difference between a fixed (static) and flexible (variable) budget?

Fixed (static) budgets- this budget is usually prepared at the start of a budget period for an area

or outlet, for specific goals, for areas which do not have a direct relation to production or sales.

Flexible (variable) budgets – allow for the adjustments based on changing conditions and can

show figures based on various scenarios.

Q4: What is a cash flow budget and what is it used for?

Cash flow budget is based on information from the sales and operational budgets and how

predicts the cash flow into and out of the business. This allows you to determine how much

cash or funds are available or must be outlaid during any given period.

© Didasko Digital 2016 www.didasko.com1

ASSESSMENT B – SHORT ANSWER

INSTRUCTIONS

You are to answer all questions.

Read each question carefully. Ensure you have provided all required information.

On completion, submit your assessment to your assessor.

SECTION 1: ALLOCATE BUDGET RESOURCES

Q1: What is a budget and how does it help a business achieve its goals?

Definition

Is a detailed financial plan that shows estimated revenue and expenses for the given time

period.

Purpose

A budget is both planning and performance evaluation tool. They are prepared prior to a

specific period to assist in the business’ s planning processes and allocation of funds with

business.

Q2: What determines how business funds are divided amongst different departments and

projects?

The following are some of the factors that need to be considered when deciding the apt amount

of the business funds to be allocated to each department:

The projected amounts of the sale for the budget period for that department

The direct amount of the costs of sales for that department

The fixed and the variable costs that would be incurred for that department

Q3: What is the difference between a fixed (static) and flexible (variable) budget?

Fixed (static) budgets- this budget is usually prepared at the start of a budget period for an area

or outlet, for specific goals, for areas which do not have a direct relation to production or sales.

Flexible (variable) budgets – allow for the adjustments based on changing conditions and can

show figures based on various scenarios.

Q4: What is a cash flow budget and what is it used for?

Cash flow budget is based on information from the sales and operational budgets and how

predicts the cash flow into and out of the business. This allows you to determine how much

cash or funds are available or must be outlaid during any given period.

© Didasko Digital 2016 www.didasko.com1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

Q5: What is a profit and loss budget and what is it used for?

Profit and Loss budget, also known as revenue or income budgets, are a forecast of what you

hope or anticipate your profit and loss statement will show at the end of that period. It indicates

your forecasted revenue and expenses for a specific period of time and shows whether you

might make or lose money at the end of the period.

Q6: What do the following terms mean?

Financial viability

Means the business has generated enough income to pay all their liabilities and still make

a profit.

Profitability

This is a business ability to achieve an adequate return from its assets to cover all

costs associated with operating the business. It shows the profit earned by the

business measured against the amount invested in assets.

Liquidity

This refer to the availability of cash , or assets that can be quickly converted into cash,

and used to pay for the purchase of goods, services and capital assets.

Q7: What is a budget cycle?

It is the process which begins with the initial development of the budget and ends with the final

transaction in the budget period.

Q8: What must you do when budget priorities are changed? Explain why.

Priorities are determined by departmental goals and or the primary concerns of business

owners, shareholders or financial backers.

To manage budgets and allocate funds, you need to know that these priorities and how they

relate to the budgets.

Meet with all department leaders and orient them on the budgeting allocations in order for them

to know which areas and operations to prioritize.

Q9: Your budget allows only a limited amount of funding for wages. Who needs to know about

these types of resource decisions? Explain why.

Anyone who has impact on the budget needs to know wherever the budget is changed. This

includes staff who generate revenue or incur expenses as a result of their daily duties.

2016 Edition2

Q5: What is a profit and loss budget and what is it used for?

Profit and Loss budget, also known as revenue or income budgets, are a forecast of what you

hope or anticipate your profit and loss statement will show at the end of that period. It indicates

your forecasted revenue and expenses for a specific period of time and shows whether you

might make or lose money at the end of the period.

Q6: What do the following terms mean?

Financial viability

Means the business has generated enough income to pay all their liabilities and still make

a profit.

Profitability

This is a business ability to achieve an adequate return from its assets to cover all

costs associated with operating the business. It shows the profit earned by the

business measured against the amount invested in assets.

Liquidity

This refer to the availability of cash , or assets that can be quickly converted into cash,

and used to pay for the purchase of goods, services and capital assets.

Q7: What is a budget cycle?

It is the process which begins with the initial development of the budget and ends with the final

transaction in the budget period.

Q8: What must you do when budget priorities are changed? Explain why.

Priorities are determined by departmental goals and or the primary concerns of business

owners, shareholders or financial backers.

To manage budgets and allocate funds, you need to know that these priorities and how they

relate to the budgets.

Meet with all department leaders and orient them on the budgeting allocations in order for them

to know which areas and operations to prioritize.

Q9: Your budget allows only a limited amount of funding for wages. Who needs to know about

these types of resource decisions? Explain why.

Anyone who has impact on the budget needs to know wherever the budget is changed. This

includes staff who generate revenue or incur expenses as a result of their daily duties.

2016 Edition2

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

Q10: List two ways you can promote awareness of the importance of budget control.

Hold a team meeting

Notice boards

Posters

Wall charts

Q11: How does promoting the importance of budget control help you achieve team or work area

goals?

The company can maximize its resources depending on the budget allocated for each

section of the operations at the same time it makes a more efficient workflow with the

proper budget distribution.

Q12: Why is it important to record resource allocation?

To track performance

To analyse efficiency and productivity

To manage cost and cash flow

To identify and rectify deviations

To report on opportunities for future improvements

Q13: Budgets are not the only source of information relating to where resources are allocated

and controlled within a business. List four other records used to show resource allocation.

Profit and loss or ( income ) statements

Balance sheets

Purchasing documentation

Payroll documentation

Bank account records

© Didasko Digital 2016 www.didasko.com3

Q10: List two ways you can promote awareness of the importance of budget control.

Hold a team meeting

Notice boards

Posters

Wall charts

Q11: How does promoting the importance of budget control help you achieve team or work area

goals?

The company can maximize its resources depending on the budget allocated for each

section of the operations at the same time it makes a more efficient workflow with the

proper budget distribution.

Q12: Why is it important to record resource allocation?

To track performance

To analyse efficiency and productivity

To manage cost and cash flow

To identify and rectify deviations

To report on opportunities for future improvements

Q13: Budgets are not the only source of information relating to where resources are allocated

and controlled within a business. List four other records used to show resource allocation.

Profit and loss or ( income ) statements

Balance sheets

Purchasing documentation

Payroll documentation

Bank account records

© Didasko Digital 2016 www.didasko.com3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

SECTION 2: MONITOR FINANCIAL ACTIVITIES AGAINST BUDGET

Q14: Why do we record and compare actual performance figures with budgeted figures?

To find out if the budgets are being adhered to

To discover if the resources you’ve allocated are appropriate to the level of business

generated

To work out if the budgets are realistic

Q15: How often should you check actual income and expenditure figures against budgets?

You need to check annually, at the end of the financial year.

Q16: List six types of financial records you can use to check income and expenditure

information.

Bank deposit documentation

Bank statements

Bank summaries

Business activity statement (BAS)

Cheque books

Credit card transaction statements

Invoices

Journal entries

Q17: What is one benefit of using computerised systems to maintain financial records?

Computerized system provide quicker turnaround times compared to manual systems.

They can more quickly process ,update and distribute information when the various

system are linked together and can share data

Q18: What are financial commitments in a business?

Are usually shown as expenses in operational budgets as they are costs incurred by the

business.

Q19: List two examples of financial commitments for a business in your industry sector.

The following are the examples of the financial commitments:

Financial commitment with the lenders which means the amounts that have to be paid to

the lenders in respect of the amount that has been borrowed from them

Financial commitment with the suppliers with whom the business has to purchase orders

and pledges to pay the money in future.

2016 Edition4

SECTION 2: MONITOR FINANCIAL ACTIVITIES AGAINST BUDGET

Q14: Why do we record and compare actual performance figures with budgeted figures?

To find out if the budgets are being adhered to

To discover if the resources you’ve allocated are appropriate to the level of business

generated

To work out if the budgets are realistic

Q15: How often should you check actual income and expenditure figures against budgets?

You need to check annually, at the end of the financial year.

Q16: List six types of financial records you can use to check income and expenditure

information.

Bank deposit documentation

Bank statements

Bank summaries

Business activity statement (BAS)

Cheque books

Credit card transaction statements

Invoices

Journal entries

Q17: What is one benefit of using computerised systems to maintain financial records?

Computerized system provide quicker turnaround times compared to manual systems.

They can more quickly process ,update and distribute information when the various

system are linked together and can share data

Q18: What are financial commitments in a business?

Are usually shown as expenses in operational budgets as they are costs incurred by the

business.

Q19: List two examples of financial commitments for a business in your industry sector.

The following are the examples of the financial commitments:

Financial commitment with the lenders which means the amounts that have to be paid to

the lenders in respect of the amount that has been borrowed from them

Financial commitment with the suppliers with whom the business has to purchase orders

and pledges to pay the money in future.

2016 Edition4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

Q20: There are four basic types of expenses you need to record in financial documents to

ensure accurate monitoring. Describe and give one example for each type.

Fixed costs

Include rent or lease payments, salaries, loan repayments and some aspects of the

marketing budget. These don’t vary (no matter how busy or quiet you are, how many

people you serve or tours you sell.

Variable costs

The most obvious examples are wages and inventory (food, beverage, dry goods

souvenirs, etc. These costs fluctuate with the level of activity within the business. If

sales increase, so do the variable costs.

Direct costs

Are those directly linked to the provision of products and services. This include the

costs of wages, souvenirs and equipment purchased as well as food and beverage

items produced and sold.

Indirect costs

These are costs which can be directly attributed to a sales item or operational outlet.

Indirect costs are included in master and profit and loss budgets ,with a percentage of

total allocated to individual budgets.

Q21: What are the formulas used to calculate a budget variance and a budget variance

percentage?

(Actual $ - budget $) / budget $ x 100 variance %

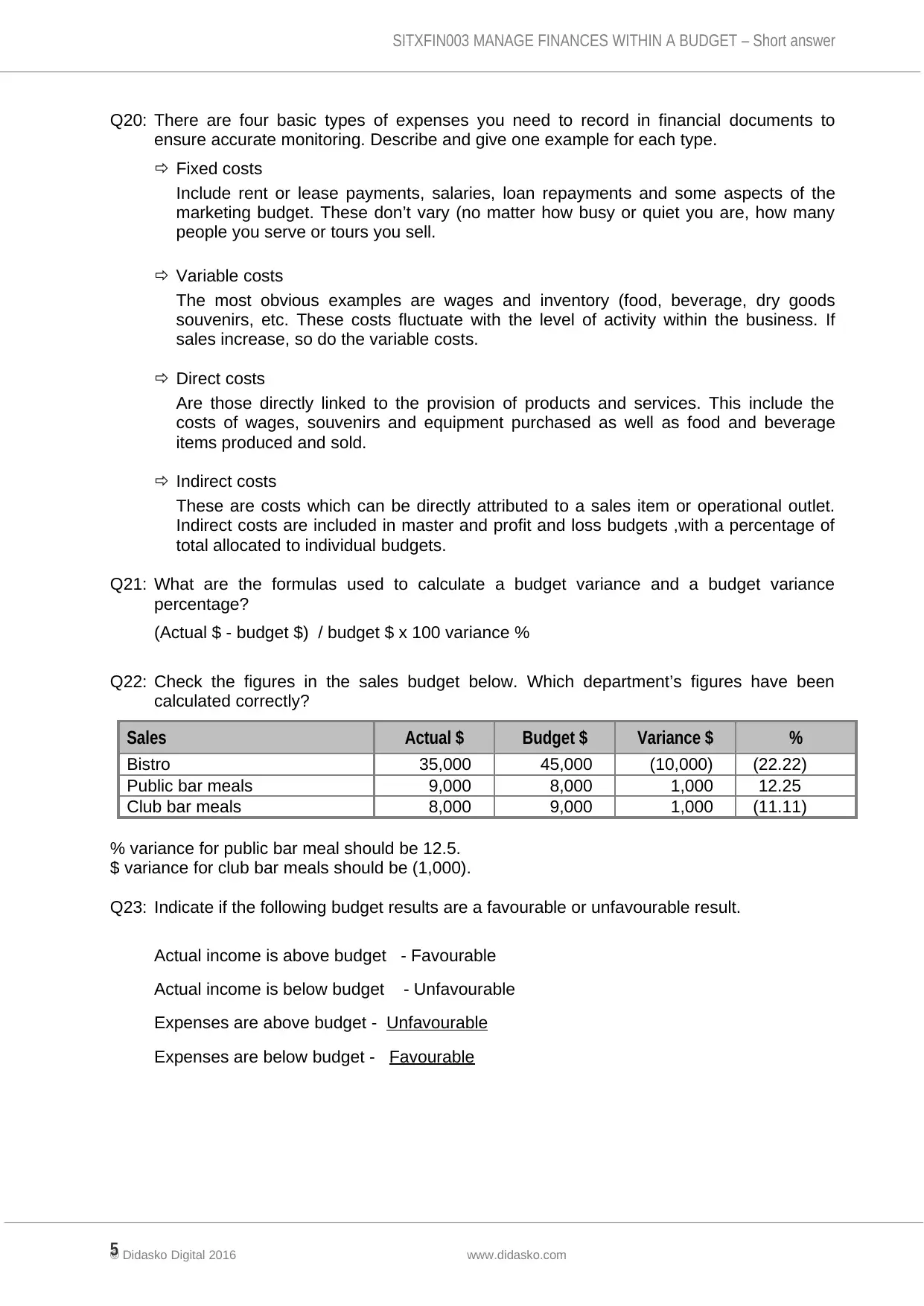

Q22: Check the figures in the sales budget below. Which department’s figures have been

calculated correctly?

Sales Actual $ Budget $ Variance $ %

Bistro 35,000 45,000 (10,000) (22.22)

Public bar meals 9,000 8,000 1,000 12.25

Club bar meals 8,000 9,000 1,000 (11.11)

% variance for public bar meal should be 12.5.

$ variance for club bar meals should be (1,000).

Q23: Indicate if the following budget results are a favourable or unfavourable result.

Actual income is above budget - Favourable

Actual income is below budget - Unfavourable

Expenses are above budget - Unfavourable

Expenses are below budget - Favourable

© Didasko Digital 2016 www.didasko.com5

Q20: There are four basic types of expenses you need to record in financial documents to

ensure accurate monitoring. Describe and give one example for each type.

Fixed costs

Include rent or lease payments, salaries, loan repayments and some aspects of the

marketing budget. These don’t vary (no matter how busy or quiet you are, how many

people you serve or tours you sell.

Variable costs

The most obvious examples are wages and inventory (food, beverage, dry goods

souvenirs, etc. These costs fluctuate with the level of activity within the business. If

sales increase, so do the variable costs.

Direct costs

Are those directly linked to the provision of products and services. This include the

costs of wages, souvenirs and equipment purchased as well as food and beverage

items produced and sold.

Indirect costs

These are costs which can be directly attributed to a sales item or operational outlet.

Indirect costs are included in master and profit and loss budgets ,with a percentage of

total allocated to individual budgets.

Q21: What are the formulas used to calculate a budget variance and a budget variance

percentage?

(Actual $ - budget $) / budget $ x 100 variance %

Q22: Check the figures in the sales budget below. Which department’s figures have been

calculated correctly?

Sales Actual $ Budget $ Variance $ %

Bistro 35,000 45,000 (10,000) (22.22)

Public bar meals 9,000 8,000 1,000 12.25

Club bar meals 8,000 9,000 1,000 (11.11)

% variance for public bar meal should be 12.5.

$ variance for club bar meals should be (1,000).

Q23: Indicate if the following budget results are a favourable or unfavourable result.

Actual income is above budget - Favourable

Actual income is below budget - Unfavourable

Expenses are above budget - Unfavourable

Expenses are below budget - Favourable

© Didasko Digital 2016 www.didasko.com5

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

Q24: What are the four main reasons budget deviations occur?

Too high /too low

Unforseen circumstances

Changed conditions

Operational factors

Q25: What factors do you need to consider when deciding whether or not a budget deviation

should be investigated further?

Dollar cut – off – a specific dollar value is set as trigger point for further investigation.

Percentage cut – off – a percentage can be set as trigger point for investigation instead

of a specific value.

Q26: List three options you might consider to help manage budget deviations effectively.

Update actual figures regularly so that the deviation trends can be identified quickly.

If a trend in the figures begins to appear, investigate it immediately. Don’t leave it until

the end of the budget period.

Investigate the options for reducing variable expenses with the purchasing and finance

managers and other appropriate personnel

Control staffing levels and rosters. Ensure payroll costs are managed shift by shift, not

just weekly or monthly.

Q27: List four types of information about budget targets you should discuss with staff members.

Successes

Concerns

Improvements

New goals

2016 Edition6

Q24: What are the four main reasons budget deviations occur?

Too high /too low

Unforseen circumstances

Changed conditions

Operational factors

Q25: What factors do you need to consider when deciding whether or not a budget deviation

should be investigated further?

Dollar cut – off – a specific dollar value is set as trigger point for further investigation.

Percentage cut – off – a percentage can be set as trigger point for investigation instead

of a specific value.

Q26: List three options you might consider to help manage budget deviations effectively.

Update actual figures regularly so that the deviation trends can be identified quickly.

If a trend in the figures begins to appear, investigate it immediately. Don’t leave it until

the end of the budget period.

Investigate the options for reducing variable expenses with the purchasing and finance

managers and other appropriate personnel

Control staffing levels and rosters. Ensure payroll costs are managed shift by shift, not

just weekly or monthly.

Q27: List four types of information about budget targets you should discuss with staff members.

Successes

Concerns

Improvements

New goals

2016 Edition6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

SECTION 3: IDENTIFY AND EVALUATE OPTIONS FOR IMPROVED BUDGET

PERFORMANCE

Q28: How does trend analysis help identify areas for improvement in budget performance?

The trend analysis is the process wherein the business data is compared for two or more

years. It helps in understanding the way the business has performed and also helps in the

predicting of the future business operations. If it’s done in the correct way, then it helps in

giving the ideas to the business so that it moves in the right direction.

Q29: What are two questions you should be asking when assessing existing costs and

resources?

How can you lower cots?

How can you increase sales?

How can you use resource more efficiently?

Q30: When identifying new approaches to budget management, who should you discuss

desired budget outcomes with? Give a generic answer or name the appropriate job

role/positions in your workplace or training environment.

The budget outcomes or the expected costs must be discussed with the senior and the

officers of the budget departments since they are the right people to discuss the expected

outcomes.

Q31: What approaches or possible options can you investigate further to control and improve

the management of expenses in a business?

Have discussions with existing suppliers to reduce stock costs.

Source new supplier if required.

Evaluate staffing and rostering requirements to reduce wage costs.

Investigate potential roster changes

Review operating procedures.

Q32: What approaches or possible options can you investigate further to control and improve

the management of payroll expenses in a business?

Increasing par stock levels

Decreasing par stock levels

Sourcing new suppliers

Reviewing stock

Conducting spot checks

Q33: List three approaches or possible options you can investigate further to control and

improve the management of accounts payable in a business.

© Didasko Digital 2016 www.didasko.com7

SECTION 3: IDENTIFY AND EVALUATE OPTIONS FOR IMPROVED BUDGET

PERFORMANCE

Q28: How does trend analysis help identify areas for improvement in budget performance?

The trend analysis is the process wherein the business data is compared for two or more

years. It helps in understanding the way the business has performed and also helps in the

predicting of the future business operations. If it’s done in the correct way, then it helps in

giving the ideas to the business so that it moves in the right direction.

Q29: What are two questions you should be asking when assessing existing costs and

resources?

How can you lower cots?

How can you increase sales?

How can you use resource more efficiently?

Q30: When identifying new approaches to budget management, who should you discuss

desired budget outcomes with? Give a generic answer or name the appropriate job

role/positions in your workplace or training environment.

The budget outcomes or the expected costs must be discussed with the senior and the

officers of the budget departments since they are the right people to discuss the expected

outcomes.

Q31: What approaches or possible options can you investigate further to control and improve

the management of expenses in a business?

Have discussions with existing suppliers to reduce stock costs.

Source new supplier if required.

Evaluate staffing and rostering requirements to reduce wage costs.

Investigate potential roster changes

Review operating procedures.

Q32: What approaches or possible options can you investigate further to control and improve

the management of payroll expenses in a business?

Increasing par stock levels

Decreasing par stock levels

Sourcing new suppliers

Reviewing stock

Conducting spot checks

Q33: List three approaches or possible options you can investigate further to control and

improve the management of accounts payable in a business.

© Didasko Digital 2016 www.didasko.com7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

Provide training

Make or buy

Use new software and hardware

Review operating policies and procedures

Establish contingency plan

Q34: List three main methods businesses use to increase their profits.

Increase volume of business

Create more output.

Change price structure

Improve profitability

Q35: You want to make recommendations for improved budget management and set new

budget targets. List two people you should present your recommendations to.

The following are the people:

Your supervisor or senior

Head of the budgeting department

Q36: The impact of any changes must be considered when developing new approaches or

changes to budget management. List one potential benefit or disadvantage that may

occur when implementing changes in the following areas.

Customer service

No business can afford deterioration in their level of customer service

Staff morale

Changes in the budget can impact employee engagement activities and benefits, it

either these events will be improved or removed

Q37: How should you present your recommendations for improved budget management?

The following are the recommendations for improving the budget management:

The budgets must be made keeping in mind the current scenarios.

The rolling forecasts and the budget must be prepare on the present results and not on

the results that were based on the facts several months ago.

Budget must include all of the expense that have an impact on the business.

Communicate all of the findings to the management

Suggestions must be invited from all of the team and not just by one

The budget must be prepared keeping in mind the goals of the organisation

The various different scenarios must be well planned in future

Each and every expenditure must be well tracked

The goals of the profit and loss and the cash flow must be included in each and every

budget

Q38: List three examples of the type of information you should include when presenting or

communicating about recommendations for budget management.

2016 Edition8

Provide training

Make or buy

Use new software and hardware

Review operating policies and procedures

Establish contingency plan

Q34: List three main methods businesses use to increase their profits.

Increase volume of business

Create more output.

Change price structure

Improve profitability

Q35: You want to make recommendations for improved budget management and set new

budget targets. List two people you should present your recommendations to.

The following are the people:

Your supervisor or senior

Head of the budgeting department

Q36: The impact of any changes must be considered when developing new approaches or

changes to budget management. List one potential benefit or disadvantage that may

occur when implementing changes in the following areas.

Customer service

No business can afford deterioration in their level of customer service

Staff morale

Changes in the budget can impact employee engagement activities and benefits, it

either these events will be improved or removed

Q37: How should you present your recommendations for improved budget management?

The following are the recommendations for improving the budget management:

The budgets must be made keeping in mind the current scenarios.

The rolling forecasts and the budget must be prepare on the present results and not on

the results that were based on the facts several months ago.

Budget must include all of the expense that have an impact on the business.

Communicate all of the findings to the management

Suggestions must be invited from all of the team and not just by one

The budget must be prepared keeping in mind the goals of the organisation

The various different scenarios must be well planned in future

Each and every expenditure must be well tracked

The goals of the profit and loss and the cash flow must be included in each and every

budget

Q38: List three examples of the type of information you should include when presenting or

communicating about recommendations for budget management.

2016 Edition8

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

The following are the different types of the information:

The costs as per the current scenarios

Procedures about the budget over run

Can the underutilised budget could be carried forward on to the next month or quarter

© Didasko Digital 2016 www.didasko.com9

The following are the different types of the information:

The costs as per the current scenarios

Procedures about the budget over run

Can the underutilised budget could be carried forward on to the next month or quarter

© Didasko Digital 2016 www.didasko.com9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SITXFIN003 MANAGE FINANCES WITHIN A BUDGET – Short answer

SECTION 4: COMPLETE FINANCIAL AND STATISTICAL REPORTS

Q39: What information might you need to include when preparing a statistical or financial report

for the supervisors in a suburban hotel? List five examples.

The following are the required examples:

The revenue that has been earned

The cost of sales

Fixed and variable expenses

The rate of the mark up

The bar graph of the above

Q40: What information might you need to include when preparing a formal statistical report for

the management team of a large events or reception centre? List five examples.

The following are the required examples:

The revenue that has been earned

The cost of organising that event

Fixed and variable expenses

The bar graph of the above

The rate of the mark-up that has been charged or added

Q41: How can your present reports to enable informed decision-making?

The reports presented must contain only the useful information, say about the revenue charged

and the variable and the fixed expenses that have been incurred. The information supplied must

be accurate and must be supplied at the right time.

Q42: How do you know when to complete reports?

The reports must be completed when the accounting period or the period ends for which the

budget is being prepared has ended and no further variations are expected.

Q43: Explain how the features of accounting software programs can assist you to manage

budgets.

The following are the ways in which they could be successful:

It reduces the chances of any error since there is a minimum human intervention

The reports are extracted automatically

It draws in the learning curve

Information and reports pulled out are fairly accurate.

2016 Edition10

SECTION 4: COMPLETE FINANCIAL AND STATISTICAL REPORTS

Q39: What information might you need to include when preparing a statistical or financial report

for the supervisors in a suburban hotel? List five examples.

The following are the required examples:

The revenue that has been earned

The cost of sales

Fixed and variable expenses

The rate of the mark up

The bar graph of the above

Q40: What information might you need to include when preparing a formal statistical report for

the management team of a large events or reception centre? List five examples.

The following are the required examples:

The revenue that has been earned

The cost of organising that event

Fixed and variable expenses

The bar graph of the above

The rate of the mark-up that has been charged or added

Q41: How can your present reports to enable informed decision-making?

The reports presented must contain only the useful information, say about the revenue charged

and the variable and the fixed expenses that have been incurred. The information supplied must

be accurate and must be supplied at the right time.

Q42: How do you know when to complete reports?

The reports must be completed when the accounting period or the period ends for which the

budget is being prepared has ended and no further variations are expected.

Q43: Explain how the features of accounting software programs can assist you to manage

budgets.

The following are the ways in which they could be successful:

It reduces the chances of any error since there is a minimum human intervention

The reports are extracted automatically

It draws in the learning curve

Information and reports pulled out are fairly accurate.

2016 Edition10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.