Financial Performance Analysis Report for SKANSA PLC (2018-2019)

VerifiedAdded on 2023/01/05

|12

|3454

|294

Report

AI Summary

This report provides a financial analysis of SKANSA PLC, focusing on its accounting and finance functions. The first part discusses the importance of these functions within the company, detailing the roles and responsibilities of the accounting and finance team in reporting and decision-making. The second part presents a ratio analysis for 2018 and 2019, including Return on Capital Employed (ROCE), Net Profit Margin (NPM), Current Ratio, Debtors Collection Period, and Creditors Collection Period. The report interprets these ratios to assess the company's financial performance from an investor's perspective. The analysis highlights trends in profitability, liquidity, and efficiency, offering insights into SKANSA PLC's financial health and providing a basis for future strategic decisions. The report concludes with an overall assessment of the company's financial standing and recommendations.

Financial Decision

Making

1

Making

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report has been prepared for the management of SKANSA PLC keeping the financial

information of company in context. In first part of this report, importance of accounting and

finance functions within company have been discussed. It also includes discussions on duties and

roles of accounting and finance team in company. In second part of the report, various ratios

have been calculated for two years of the company, using information from its financial accounts

and comments have been developed about company’s performance from an investor’s point of

view.

2

This report has been prepared for the management of SKANSA PLC keeping the financial

information of company in context. In first part of this report, importance of accounting and

finance functions within company have been discussed. It also includes discussions on duties and

roles of accounting and finance team in company. In second part of the report, various ratios

have been calculated for two years of the company, using information from its financial accounts

and comments have been developed about company’s performance from an investor’s point of

view.

2

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

Importance of accounting and finance functions....................................................................4

Roles and responsibilities of accounting and finance department in reporting and decision-

making....................................................................................................................................6

Task 2...............................................................................................................................................7

A. Ratio analysis.....................................................................................................................7

B. Comment on financial performance of SKANSA PLC.....................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

Importance of accounting and finance functions....................................................................4

Roles and responsibilities of accounting and finance department in reporting and decision-

making....................................................................................................................................6

Task 2...............................................................................................................................................7

A. Ratio analysis.....................................................................................................................7

B. Comment on financial performance of SKANSA PLC.....................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Finance is known as bloodline of a company. The accounting and finance department of a

company is responsible for ensuring stable financial health of the company (Cannon, Hillebrandt

and Lansley, 2016.). This report has been prepared for the management of SKANSA PLC,

keeping the financial information of company in context. SKANSA PLC operates in construction

industry. It is based in UK and was founded in 1984. It plans to expand its operation

internationally within a decade. This report has been prepared with an objective of discuss scope,

duties and importance of accounting and finance function in the company. Also, financial ratio

calculation and analysis have also been discussed in this report.

Task 1

Importance of accounting and finance functions

Every business requires funds and finances to keep its operations going. Accounting and

finance functions do that part for the organisation. Accounting involves recording, summarising

and presentation of financial information in financial statements while finance is concerned with

analysing and reporting financial information to senior management, in order to assist them in

policy formulation (Harris and et.al., 2020). There are three key financial statements in a

company:

Statement of Income – It is a period statement that is used to ascertain financial

performance of the company for a specific accounting period. It contains revenues and

expenses of the business to generate profit/loss.

Balance Sheet – It is a point statement that is used to ascertain financial position of the

company at a specified date. It contains information about standings of assets, liabilities

and capital as on the specific date.

Cash Flow Statement – It is also a period statement that is used to ascertain cash inflow

and outflow within the specified accounting period. It is prepared in three forms – cash

flow from operations, investments and finance.

Accounting and management functions are important as it helps in:

4

Finance is known as bloodline of a company. The accounting and finance department of a

company is responsible for ensuring stable financial health of the company (Cannon, Hillebrandt

and Lansley, 2016.). This report has been prepared for the management of SKANSA PLC,

keeping the financial information of company in context. SKANSA PLC operates in construction

industry. It is based in UK and was founded in 1984. It plans to expand its operation

internationally within a decade. This report has been prepared with an objective of discuss scope,

duties and importance of accounting and finance function in the company. Also, financial ratio

calculation and analysis have also been discussed in this report.

Task 1

Importance of accounting and finance functions

Every business requires funds and finances to keep its operations going. Accounting and

finance functions do that part for the organisation. Accounting involves recording, summarising

and presentation of financial information in financial statements while finance is concerned with

analysing and reporting financial information to senior management, in order to assist them in

policy formulation (Harris and et.al., 2020). There are three key financial statements in a

company:

Statement of Income – It is a period statement that is used to ascertain financial

performance of the company for a specific accounting period. It contains revenues and

expenses of the business to generate profit/loss.

Balance Sheet – It is a point statement that is used to ascertain financial position of the

company at a specified date. It contains information about standings of assets, liabilities

and capital as on the specific date.

Cash Flow Statement – It is also a period statement that is used to ascertain cash inflow

and outflow within the specified accounting period. It is prepared in three forms – cash

flow from operations, investments and finance.

Accounting and management functions are important as it helps in:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Creating budgets and financial projection – Budgets are culmination of good financial

record keeping. All businesses prepare budgets to act as standards for performance

control (Clough and et.al., 2015). Financial statement helps a company prepare those

budgets. Accounting and finance manager of SKANSA PLC understands the flow of

money to anticipate revenues and other operational measures by studying financial

accounts to prepare various budgets for a specified future accounting period. Financial

data is most appropriate when it is prepared according to well-structured accounting

processes as trends and projections are based on historical financial data.

Analysing financial performance – Financial accounts are reflection of performance of

the business operations as well as position of the business. Its analysis helps a company

learn about its past performance to keep it as yardstick for future performances.

Accounting and finance manager of SKANSA PLC uses it to assess contribution of

expenses in overall value addition in the operation. It is a construction company and uses

this information to make decisions as to which operation it shall continue as it is, which it

should downsize and which it should discontinue in whole.

Developing business strategy – A company needs both financial and non-financial data

to develop its strategies. Data from financial accounts serves the part for financial data

analysis which is responsibility of accounting and finance department. Finance manager

of SKANSA PLC uses it to analyse whether it is on correct road to growth or not. It also

helps it analyse where it is lacking from budgets so that it can develop appropriate

corrective strategies. It keeps track of expenses, gross and net margin, debt cost, etc. so

that it can assist senior management in making flexible strategies that are able to change

path midway to ensure it is on right path to achieve company’s targets.

Ensuring statutory compliance – Companies have to prepare financial statements

according to the proforma provided in Companies Act (Ahangar and Ozturk, 2019). It is

the accounts department that ensures compliance with all necessary statute and

guidelines. Effective accounts and finance manager of SKANSA PLC maintains all

records necessary to be maintained under different laws such as Company Act, Income

Tax Act, etc. Accounts are to be filed with Registrar of Companies which is done by

accounts department. It is also responsible for paying right tax at right time under right

5

record keeping. All businesses prepare budgets to act as standards for performance

control (Clough and et.al., 2015). Financial statement helps a company prepare those

budgets. Accounting and finance manager of SKANSA PLC understands the flow of

money to anticipate revenues and other operational measures by studying financial

accounts to prepare various budgets for a specified future accounting period. Financial

data is most appropriate when it is prepared according to well-structured accounting

processes as trends and projections are based on historical financial data.

Analysing financial performance – Financial accounts are reflection of performance of

the business operations as well as position of the business. Its analysis helps a company

learn about its past performance to keep it as yardstick for future performances.

Accounting and finance manager of SKANSA PLC uses it to assess contribution of

expenses in overall value addition in the operation. It is a construction company and uses

this information to make decisions as to which operation it shall continue as it is, which it

should downsize and which it should discontinue in whole.

Developing business strategy – A company needs both financial and non-financial data

to develop its strategies. Data from financial accounts serves the part for financial data

analysis which is responsibility of accounting and finance department. Finance manager

of SKANSA PLC uses it to analyse whether it is on correct road to growth or not. It also

helps it analyse where it is lacking from budgets so that it can develop appropriate

corrective strategies. It keeps track of expenses, gross and net margin, debt cost, etc. so

that it can assist senior management in making flexible strategies that are able to change

path midway to ensure it is on right path to achieve company’s targets.

Ensuring statutory compliance – Companies have to prepare financial statements

according to the proforma provided in Companies Act (Ahangar and Ozturk, 2019). It is

the accounts department that ensures compliance with all necessary statute and

guidelines. Effective accounts and finance manager of SKANSA PLC maintains all

records necessary to be maintained under different laws such as Company Act, Income

Tax Act, etc. Accounts are to be filed with Registrar of Companies which is done by

accounts department. It is also responsible for paying right tax at right time under right

5

law to right authority. It also saves company form litigation cost needed by practicing

ineffective or poor accounting practices.

Roles and responsibilities of accounting and finance department in reporting and decision-

making

Below mentioned are few roles and responsibilities that accounting and finance department

carry out:

Reporting and financial statements – Most basic responsibility of accounts department

is recording, measuring and summarising financial information of the company to prepare

financial statements that serve as basis for budgeting, forecasting and various other

decision-making processes (Grossmann, Mooney and Dugan, 2019). Accounts managers

of SKANSA PLC play a very important role in preparing these reports accurately which

are used by management, investors, banks, etc. for making decisions that are pivotal for

business growth. They also perform payroll function which ensures that all employees of

company are paid accurately and timely. It is also entrusted with responsibility to assess

various taxes that are due to business and ensure their timely payment to government

agencies. Tracking cash inflow/outflows – Businesses deals in credit with multiple suppliers and

customers and also, are various other sources from where regular cash inflow and outflow

takes place. Tracking all these inflows and outflows are responsibility of accounting and

finance department and its managers play an active role in booking of these transactions.

Accounts manager of SKANSA PLC are also responsible for developing system so that

payables are paid on time and receivables are received on time. Also, they play an active

role in identifying opportunities to save money such as discount on early payment. Financial control – It includes various reconciliations between internal accounts and

external accounts (like Bank Reconciliation Statement), following GAAP standards or

accounting principles, etc. (Messer, 2020) Complying with all of these is responsibility of

accounting and finance department. Accounts manager of SKANSA PLC is entrusted to

play a role in setting up a system that will comply with all processes which are necessary

for producing accurate financial and other statements.

Financial planning – Business operates with an objective of earning maximum profit.

For it, it is important for company to sound financial plan which is one of the main

6

ineffective or poor accounting practices.

Roles and responsibilities of accounting and finance department in reporting and decision-

making

Below mentioned are few roles and responsibilities that accounting and finance department

carry out:

Reporting and financial statements – Most basic responsibility of accounts department

is recording, measuring and summarising financial information of the company to prepare

financial statements that serve as basis for budgeting, forecasting and various other

decision-making processes (Grossmann, Mooney and Dugan, 2019). Accounts managers

of SKANSA PLC play a very important role in preparing these reports accurately which

are used by management, investors, banks, etc. for making decisions that are pivotal for

business growth. They also perform payroll function which ensures that all employees of

company are paid accurately and timely. It is also entrusted with responsibility to assess

various taxes that are due to business and ensure their timely payment to government

agencies. Tracking cash inflow/outflows – Businesses deals in credit with multiple suppliers and

customers and also, are various other sources from where regular cash inflow and outflow

takes place. Tracking all these inflows and outflows are responsibility of accounting and

finance department and its managers play an active role in booking of these transactions.

Accounts manager of SKANSA PLC are also responsible for developing system so that

payables are paid on time and receivables are received on time. Also, they play an active

role in identifying opportunities to save money such as discount on early payment. Financial control – It includes various reconciliations between internal accounts and

external accounts (like Bank Reconciliation Statement), following GAAP standards or

accounting principles, etc. (Messer, 2020) Complying with all of these is responsibility of

accounting and finance department. Accounts manager of SKANSA PLC is entrusted to

play a role in setting up a system that will comply with all processes which are necessary

for producing accurate financial and other statements.

Financial planning – Business operates with an objective of earning maximum profit.

For it, it is important for company to sound financial plan which is one of the main

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

responsibilities to be carried out by finance managers. SKANSA PLC is a construction

company and has irregular funds inflow/outflow. Therefore, it is very important for

company to make a financial plan. It is the role and responsibility of accounts and finance

managers to make a plan for effective treasury management and efficient provision,

investment and use of funds.

Management accounting – Accounting and finance department is entrusted with

responsibility to analyse and set up control functions that helps management in day-to-

day business operations (Bradbury and Scott, 2020). Financial accounting and

management accounting are both part of accounting process of organisation and it is the

role of finance manager to perform financial part of management accounting. For

example, cost accounting, it is a part of financial management accounting. There are

various tools and techniques of management accounting that are used by finance

managers of SKANSA PLC to generate such reports that on clubbing with non-financial

data will provide basis for strategic decision-making. This role has been given to

accounts and finance managers of the company to analyse financial statements through

ratio analysis, comparative statements, trends, graphs, fund and cash flow analysis, etc.

They are also entrusted to perform cost accounting techniques such as cost volume profit

analysis, incremental costing, standard costing, analysis of cost variances, etc. For

estimating future projection, they are to use techniques like budgeting, budgetary control,

business forecasting, project appraisal, etc. All these management accounting techniques

are used for planning, control and decision making within the company.

Task 2

A. Ratio analysis

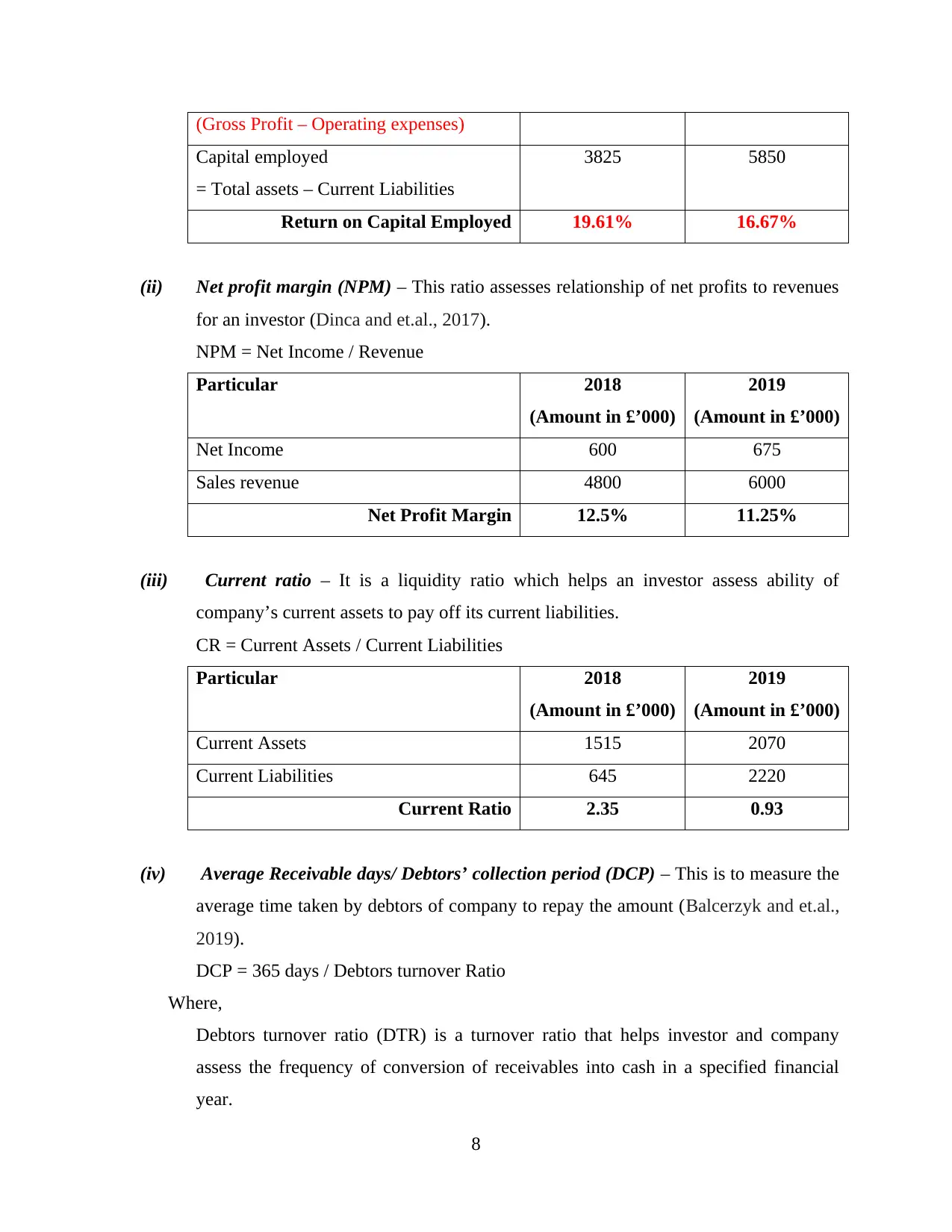

(i) Return on capital employed (ROCE) – It is a financial ratio which helps an investor

in assessing whether a company is capital efficient and generating enough profit from

it (Islam, 2020).

ROCE = Operating Profit / Capital employed

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Operating Profit = 750 975

7

company and has irregular funds inflow/outflow. Therefore, it is very important for

company to make a financial plan. It is the role and responsibility of accounts and finance

managers to make a plan for effective treasury management and efficient provision,

investment and use of funds.

Management accounting – Accounting and finance department is entrusted with

responsibility to analyse and set up control functions that helps management in day-to-

day business operations (Bradbury and Scott, 2020). Financial accounting and

management accounting are both part of accounting process of organisation and it is the

role of finance manager to perform financial part of management accounting. For

example, cost accounting, it is a part of financial management accounting. There are

various tools and techniques of management accounting that are used by finance

managers of SKANSA PLC to generate such reports that on clubbing with non-financial

data will provide basis for strategic decision-making. This role has been given to

accounts and finance managers of the company to analyse financial statements through

ratio analysis, comparative statements, trends, graphs, fund and cash flow analysis, etc.

They are also entrusted to perform cost accounting techniques such as cost volume profit

analysis, incremental costing, standard costing, analysis of cost variances, etc. For

estimating future projection, they are to use techniques like budgeting, budgetary control,

business forecasting, project appraisal, etc. All these management accounting techniques

are used for planning, control and decision making within the company.

Task 2

A. Ratio analysis

(i) Return on capital employed (ROCE) – It is a financial ratio which helps an investor

in assessing whether a company is capital efficient and generating enough profit from

it (Islam, 2020).

ROCE = Operating Profit / Capital employed

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Operating Profit = 750 975

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Gross Profit – Operating expenses)

Capital employed

= Total assets – Current Liabilities

3825 5850

Return on Capital Employed 19.61% 16.67%

(ii) Net profit margin (NPM) – This ratio assesses relationship of net profits to revenues

for an investor (Dinca and et.al., 2017).

NPM = Net Income / Revenue

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Net Income 600 675

Sales revenue 4800 6000

Net Profit Margin 12.5% 11.25%

(iii) Current ratio – It is a liquidity ratio which helps an investor assess ability of

company’s current assets to pay off its current liabilities.

CR = Current Assets / Current Liabilities

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Current Assets 1515 2070

Current Liabilities 645 2220

Current Ratio 2.35 0.93

(iv) Average Receivable days/ Debtors’ collection period (DCP) – This is to measure the

average time taken by debtors of company to repay the amount (Balcerzyk and et.al.,

2019).

DCP = 365 days / Debtors turnover Ratio

Where,

Debtors turnover ratio (DTR) is a turnover ratio that helps investor and company

assess the frequency of conversion of receivables into cash in a specified financial

year.

8

Capital employed

= Total assets – Current Liabilities

3825 5850

Return on Capital Employed 19.61% 16.67%

(ii) Net profit margin (NPM) – This ratio assesses relationship of net profits to revenues

for an investor (Dinca and et.al., 2017).

NPM = Net Income / Revenue

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Net Income 600 675

Sales revenue 4800 6000

Net Profit Margin 12.5% 11.25%

(iii) Current ratio – It is a liquidity ratio which helps an investor assess ability of

company’s current assets to pay off its current liabilities.

CR = Current Assets / Current Liabilities

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Current Assets 1515 2070

Current Liabilities 645 2220

Current Ratio 2.35 0.93

(iv) Average Receivable days/ Debtors’ collection period (DCP) – This is to measure the

average time taken by debtors of company to repay the amount (Balcerzyk and et.al.,

2019).

DCP = 365 days / Debtors turnover Ratio

Where,

Debtors turnover ratio (DTR) is a turnover ratio that helps investor and company

assess the frequency of conversion of receivables into cash in a specified financial

year.

8

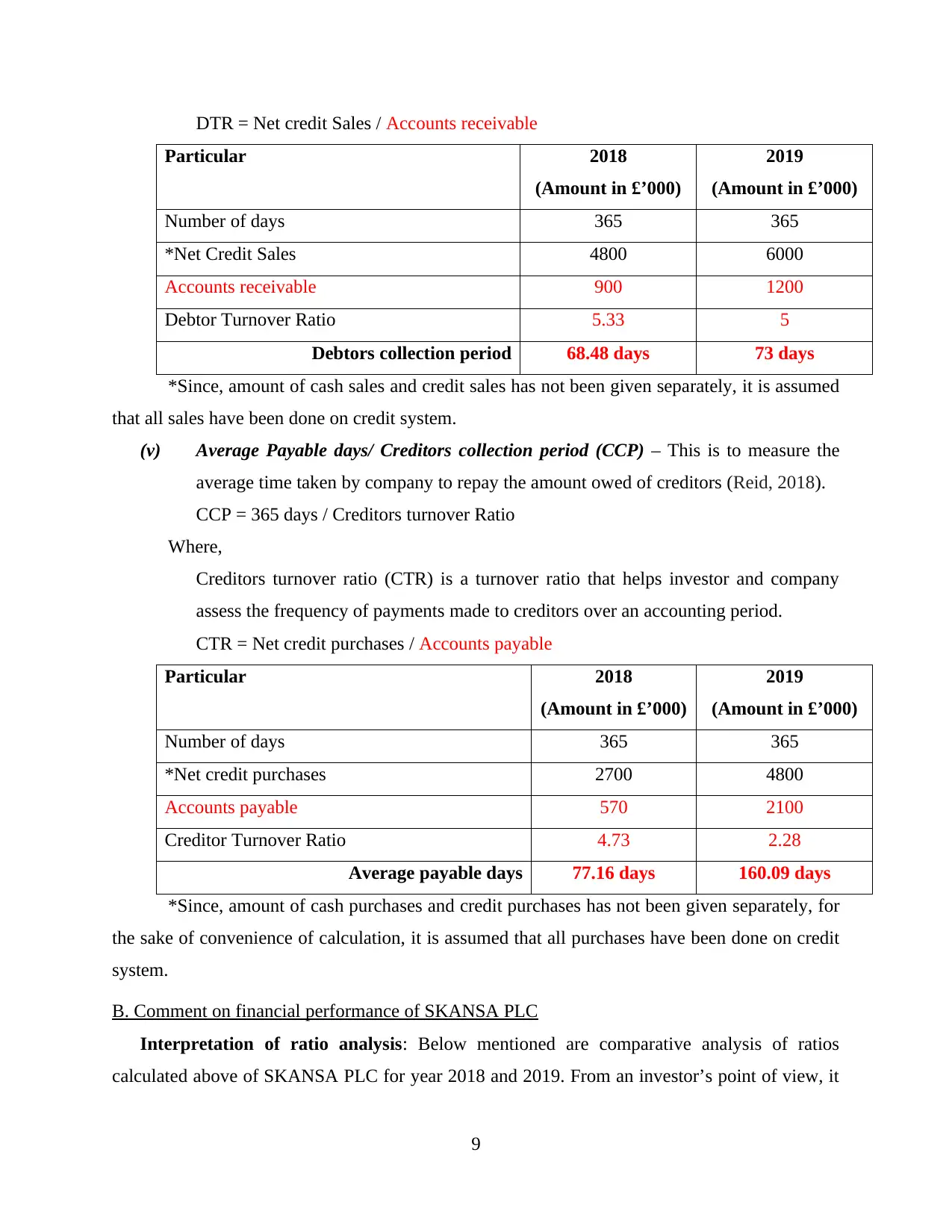

DTR = Net credit Sales / Accounts receivable

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Number of days 365 365

*Net Credit Sales 4800 6000

Accounts receivable 900 1200

Debtor Turnover Ratio 5.33 5

Debtors collection period 68.48 days 73 days

*Since, amount of cash sales and credit sales has not been given separately, it is assumed

that all sales have been done on credit system.

(v) Average Payable days/ Creditors collection period (CCP) – This is to measure the

average time taken by company to repay the amount owed of creditors (Reid, 2018).

CCP = 365 days / Creditors turnover Ratio

Where,

Creditors turnover ratio (CTR) is a turnover ratio that helps investor and company

assess the frequency of payments made to creditors over an accounting period.

CTR = Net credit purchases / Accounts payable

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Number of days 365 365

*Net credit purchases 2700 4800

Accounts payable 570 2100

Creditor Turnover Ratio 4.73 2.28

Average payable days 77.16 days 160.09 days

*Since, amount of cash purchases and credit purchases has not been given separately, for

the sake of convenience of calculation, it is assumed that all purchases have been done on credit

system.

B. Comment on financial performance of SKANSA PLC

Interpretation of ratio analysis: Below mentioned are comparative analysis of ratios

calculated above of SKANSA PLC for year 2018 and 2019. From an investor’s point of view, it

9

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Number of days 365 365

*Net Credit Sales 4800 6000

Accounts receivable 900 1200

Debtor Turnover Ratio 5.33 5

Debtors collection period 68.48 days 73 days

*Since, amount of cash sales and credit sales has not been given separately, it is assumed

that all sales have been done on credit system.

(v) Average Payable days/ Creditors collection period (CCP) – This is to measure the

average time taken by company to repay the amount owed of creditors (Reid, 2018).

CCP = 365 days / Creditors turnover Ratio

Where,

Creditors turnover ratio (CTR) is a turnover ratio that helps investor and company

assess the frequency of payments made to creditors over an accounting period.

CTR = Net credit purchases / Accounts payable

Particular 2018

(Amount in £’000)

2019

(Amount in £’000)

Number of days 365 365

*Net credit purchases 2700 4800

Accounts payable 570 2100

Creditor Turnover Ratio 4.73 2.28

Average payable days 77.16 days 160.09 days

*Since, amount of cash purchases and credit purchases has not been given separately, for

the sake of convenience of calculation, it is assumed that all purchases have been done on credit

system.

B. Comment on financial performance of SKANSA PLC

Interpretation of ratio analysis: Below mentioned are comparative analysis of ratios

calculated above of SKANSA PLC for year 2018 and 2019. From an investor’s point of view, it

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is also advised that investor compare ratios of the company with industry benchmarks and

similar companies in competition with SKANSA PLC.

(i) Return on capital employed – ROCE assesses both debt and equity component

(Chandra, 2017). It also tells the amount of profit a company is generating per £1 of

capital employed. Therefore, higher ROCE is considered better as it indicates

stronger profitability. It can be seen that it has decreased from 19.61% in 2018 to

16.67% in 2019. This shows that either the ROCE of SKANSA PLC is volatile or is

trending at lower side. Investor shall prefer companies with stable ROCE. This owes

its reason to unprecedented changes in non-current assets and trade payables.

(ii) Net Profit Margin – Net profit margin is a primary indicator of a company’s financial

performance. It helps investors in tracking whether company is generating enough

revenues that it can contain its operating costs and other overheads. SKANSA PLC’s

net profit margin has decreased from 12.5% to 11.25% which does not paint a good

picture for the company. It looks because of regular business operations which did not

increase homogeneously in proportion. Decreasing net margin can lead to decrease in

share price growth which is neither in investor’s favour nor company’s.

(iii) Current Ratio – Current ratio is a liquidity ratio which assesses ability of a company

to pay off liabilities due to it within a year. Generally, a ratio of 2:1 is considered

acceptable (Warren and Farmer, 2020). SKANSA PLC had a current ratio of 2.35:1 in

2018 and 0.93:1in 2019. This is a huge downward shift and indicates a higher risk of

default or distress over company’s assets. Ratio of less than 1 can be indication that

company’s capital might prove unable to meet its short-term debt obligations, if they

become due all at once. This looks superficially because of more than proportionate

increase in trade payables and decrease in cash in hand. Company needs to take care

of their cash flows as they are volatile and can hamper business operations.

(iv) Average Collection Period – It refers to those average number of days for which

payment is due to be received from a debtor against an outstanding invoice. It helps in

determining effectiveness of credit collection process of company. SKANSA PLC is

a construction company and must have been relying on its receivables for its stable

cash flows and smooth operations. It had a collection period of 68.48 days in 2018

which stretched to unfavourable 73 days in 2019. This might be possibly because

10

similar companies in competition with SKANSA PLC.

(i) Return on capital employed – ROCE assesses both debt and equity component

(Chandra, 2017). It also tells the amount of profit a company is generating per £1 of

capital employed. Therefore, higher ROCE is considered better as it indicates

stronger profitability. It can be seen that it has decreased from 19.61% in 2018 to

16.67% in 2019. This shows that either the ROCE of SKANSA PLC is volatile or is

trending at lower side. Investor shall prefer companies with stable ROCE. This owes

its reason to unprecedented changes in non-current assets and trade payables.

(ii) Net Profit Margin – Net profit margin is a primary indicator of a company’s financial

performance. It helps investors in tracking whether company is generating enough

revenues that it can contain its operating costs and other overheads. SKANSA PLC’s

net profit margin has decreased from 12.5% to 11.25% which does not paint a good

picture for the company. It looks because of regular business operations which did not

increase homogeneously in proportion. Decreasing net margin can lead to decrease in

share price growth which is neither in investor’s favour nor company’s.

(iii) Current Ratio – Current ratio is a liquidity ratio which assesses ability of a company

to pay off liabilities due to it within a year. Generally, a ratio of 2:1 is considered

acceptable (Warren and Farmer, 2020). SKANSA PLC had a current ratio of 2.35:1 in

2018 and 0.93:1in 2019. This is a huge downward shift and indicates a higher risk of

default or distress over company’s assets. Ratio of less than 1 can be indication that

company’s capital might prove unable to meet its short-term debt obligations, if they

become due all at once. This looks superficially because of more than proportionate

increase in trade payables and decrease in cash in hand. Company needs to take care

of their cash flows as they are volatile and can hamper business operations.

(iv) Average Collection Period – It refers to those average number of days for which

payment is due to be received from a debtor against an outstanding invoice. It helps in

determining effectiveness of credit collection process of company. SKANSA PLC is

a construction company and must have been relying on its receivables for its stable

cash flows and smooth operations. It had a collection period of 68.48 days in 2018

which stretched to unfavourable 73 days in 2019. This might be possibly because

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

either the company’s receivables management practises are not effective or it has

made its credit terms more flexible to attract more business (Weygandt and et.al.,

2019). Both the cases are capable of having direct effect over company’s cash flows.

Therefore, it shall be trade cautiously.

(v) Average Payment Period – It refers to those average number of days which a

company takes to pay off its outstanding creditors. It helps in streamlining credit

management process of the company. SKANSA PLC being a construction company

must have lots of suppliers which serve as trade payables. As longer company can

secure payment days from them, more funds it will be able to retains which it can put

to another better use. It had average payment period of 77.16 days in 2018 which

went up to 160.09 days in 2019. This might be possible due to two reasons, either

company is able to secure lenient payment terms from its suppliers or, there is a red

flag that company is not able to pay its creditors on time. If it is because of former, it

is favourable for company and safe for investor to invest but if it is because of latter,

it flashes red flags. Longer it will take to pay creditors back, in more jeopardy

company’s relations with creditors will be. Creditors might refuse to extend more

credit to company or might extend at unfavourable terms. In, both the case, it is

unfavourable to company and risky for investor to invest (Warren and Jones, 2018).

Conclusion

From the above report, it can be concluded that accounting and finance department of a

company is responsible for efficient financial management and implementing effective financial

controls. They provide services of planning, recording and managing finances of the company. It

was also concluded that various ratios help both company and investors in assessing financial

information of the company and developing further course of action. It is not advisable to

investor to invest in the company analysed above.

11

made its credit terms more flexible to attract more business (Weygandt and et.al.,

2019). Both the cases are capable of having direct effect over company’s cash flows.

Therefore, it shall be trade cautiously.

(v) Average Payment Period – It refers to those average number of days which a

company takes to pay off its outstanding creditors. It helps in streamlining credit

management process of the company. SKANSA PLC being a construction company

must have lots of suppliers which serve as trade payables. As longer company can

secure payment days from them, more funds it will be able to retains which it can put

to another better use. It had average payment period of 77.16 days in 2018 which

went up to 160.09 days in 2019. This might be possible due to two reasons, either

company is able to secure lenient payment terms from its suppliers or, there is a red

flag that company is not able to pay its creditors on time. If it is because of former, it

is favourable for company and safe for investor to invest but if it is because of latter,

it flashes red flags. Longer it will take to pay creditors back, in more jeopardy

company’s relations with creditors will be. Creditors might refuse to extend more

credit to company or might extend at unfavourable terms. In, both the case, it is

unfavourable to company and risky for investor to invest (Warren and Jones, 2018).

Conclusion

From the above report, it can be concluded that accounting and finance department of a

company is responsible for efficient financial management and implementing effective financial

controls. They provide services of planning, recording and managing finances of the company. It

was also concluded that various ratios help both company and investors in assessing financial

information of the company and developing further course of action. It is not advisable to

investor to invest in the company analysed above.

11

References

Books and Journal

Ahangar, R.G. and Ozturk, C. eds., 2019. Accounting and Finance: New Perspectives on

Banking, Financial Statements and Reporting. BoD–Books on Demand.

Balcerzyk, R. and et.al., 2019, July. Fluctuation of employees in construction company as a

measurable phenomenon. In AIP Conference Proceedings (Vol. 2116, No. 1, p.

180009). AIP Publishing LLC.

Bradbury, M.E. and Scott, T., 2020. What accounting standards were the cause of enforcement

actions following IFRS adoption?. Accounting & Finance.

Cannon, J., Hillebrandt, P.M. and Lansley, P., 2016. The Construction Company in and out of

Recession. Springer.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Clough, R.H. and et.al., 2015. Construction contracting: A practical guide to company

management. John Wiley & Sons.

Dinca, M.S. and et.al., 2017. Integrated analysis of EU construction companies’ financial

performances. Journal of construction engineering and management. 143(6).

p.04017002.

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance, and

management: An investigation of A-star publications on the ABDC journal list. Journal

of Business Research. 95. pp.232-241.

Harris, F. and et.al., 2020. Modern construction management. John Wiley & Sons.

Islam, N., 2020. Management Accounting Practices-a Case Study on Small Scale Construction

Companies.

Messer, R., 2020. Capital Budgeting Decisions. In Financial Modeling for Decision Making:

Using MS-Excel in Accounting and Finance. Emerald Publishing Limited.

Reid, W., 2018. The meaning of company accounts. Routledge.

Warren, C.S. and Farmer, A., 2020. Survey of accounting. Cengage Learning.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weygandt, J.J. and et.al., 2019. Accounting Principles, Volume 2. John Wiley & Sons.

12

Books and Journal

Ahangar, R.G. and Ozturk, C. eds., 2019. Accounting and Finance: New Perspectives on

Banking, Financial Statements and Reporting. BoD–Books on Demand.

Balcerzyk, R. and et.al., 2019, July. Fluctuation of employees in construction company as a

measurable phenomenon. In AIP Conference Proceedings (Vol. 2116, No. 1, p.

180009). AIP Publishing LLC.

Bradbury, M.E. and Scott, T., 2020. What accounting standards were the cause of enforcement

actions following IFRS adoption?. Accounting & Finance.

Cannon, J., Hillebrandt, P.M. and Lansley, P., 2016. The Construction Company in and out of

Recession. Springer.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Clough, R.H. and et.al., 2015. Construction contracting: A practical guide to company

management. John Wiley & Sons.

Dinca, M.S. and et.al., 2017. Integrated analysis of EU construction companies’ financial

performances. Journal of construction engineering and management. 143(6).

p.04017002.

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance, and

management: An investigation of A-star publications on the ABDC journal list. Journal

of Business Research. 95. pp.232-241.

Harris, F. and et.al., 2020. Modern construction management. John Wiley & Sons.

Islam, N., 2020. Management Accounting Practices-a Case Study on Small Scale Construction

Companies.

Messer, R., 2020. Capital Budgeting Decisions. In Financial Modeling for Decision Making:

Using MS-Excel in Accounting and Finance. Emerald Publishing Limited.

Reid, W., 2018. The meaning of company accounts. Routledge.

Warren, C.S. and Farmer, A., 2020. Survey of accounting. Cengage Learning.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weygandt, J.J. and et.al., 2019. Accounting Principles, Volume 2. John Wiley & Sons.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.