Financial Analysis Report: Skanska PLC Performance and Recommendations

VerifiedAdded on 2023/01/05

|13

|3774

|33

Report

AI Summary

This report presents a financial analysis of Skanska PLC, a multinational construction and development company. It begins by defining the roles of the accounting and finance departments, emphasizing their importance in financial management, investment decisions, and tax functions. The report then delves into a detailed analysis of Skanska PLC's financial performance using ratio analysis, specifically examining profitability, liquidity, and efficiency ratios for the years 2017 and 2018. The analysis includes calculations of key ratios such as return on capital employed, net profit margin, current ratio, quick ratio, and various efficiency ratios. The report highlights the company's strengths and weaknesses based on the ratio analysis, with an overall assessment suggesting adequate financial management but a need for improvement in profitability and liquidity. The report also discusses the roles of the accounting and finance departments, including financial management, management accounting, tax function, auditing function, investment function, financing function, dividend function, and working capital function. The conclusion summarizes the key findings and suggests strategies for enhancing Skanska PLC's financial performance.

FINANCIAL ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial analysis could be defined as process of evaluating the business, budgets, projects

and other financial transactions for determining the suitability and performance of organisation.

Financial analysis is also used for assessing the stability, solvency, liquidity or profitability of teh

organisation. Report has revealed about the accounting and the finance departments. They both

play a significant role in the success of organisation, it is difficult to run the operations without

adequate management. The ratio analysis has been performed to assess the financial performance

of Skanska plc. It has been evaluated from the analysis that company is having adequate

financial management but have weak profitability and liquidity which has to be improved using

effective strategies and policies.

Financial analysis could be defined as process of evaluating the business, budgets, projects

and other financial transactions for determining the suitability and performance of organisation.

Financial analysis is also used for assessing the stability, solvency, liquidity or profitability of teh

organisation. Report has revealed about the accounting and the finance departments. They both

play a significant role in the success of organisation, it is difficult to run the operations without

adequate management. The ratio analysis has been performed to assess the financial performance

of Skanska plc. It has been evaluated from the analysis that company is having adequate

financial management but have weak profitability and liquidity which has to be improved using

effective strategies and policies.

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

TABLE OF CONTENTS................................................................................................................3

TASK 1............................................................................................................................................1

Introduction of Skanska PLc.......................................................................................................1

Define Accounting and Finance Department..............................................................................1

Importance of Accounting and Finance Department...................................................................1

Role of Accounts department......................................................................................................2

Role of finance Department.........................................................................................................3

TASK 2............................................................................................................................................4

a) Calculation of Ratios...............................................................................................................4

b) Financial analysis of Skanska Plc using the ratio analysis between two years.......................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................2

TABLE OF CONTENTS................................................................................................................3

TASK 1............................................................................................................................................1

Introduction of Skanska PLc.......................................................................................................1

Define Accounting and Finance Department..............................................................................1

Importance of Accounting and Finance Department...................................................................1

Role of Accounts department......................................................................................................2

Role of finance Department.........................................................................................................3

TASK 2............................................................................................................................................4

a) Calculation of Ratios...............................................................................................................4

b) Financial analysis of Skanska Plc using the ratio analysis between two years.......................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

Introduction of Skanska PLc

Skanska Plc is the multinational construction and development company situated in

Sweden. It is fifth largest construction company of the world. The company is established since

133 years and is having headquarters in Stockholm Sweden. The construction projects of

company include renovations of UN headquarters, world trade centre, Moynihan Station and

many others

Define Accounting and Finance Department

Accounting and financial department of all the organization is regarded as a centre of all

the organization. Accounting and financial department generally ensures that financial

management and financial control are effectively controlled in the organization (Olbe, 2016).

Financial and accounting department generally controls the flow of money in and out of

business. Also, they make sure about the Payroll of all the employee and also perform the

activity of preparing financial report in the organization i.e. Profit and Loss Statement, Balance

sheet and budget. In simple words it can be said that it is the department which looks at

preparing financial statement, maintaining ledger, paying bills, manage payroll and flow of

money in & out of the business. Both the department used to operate same type of function but

the different is that Accounting department used to focus on the past, at the same time Finance

department used to focus on the future functioning of organization.

Importance of Accounting and Finance Department

Accounting and Finance department of Shanska PLc helps the company in managing the

finance in the organization. They generally make it sure that company is having a good amount

of the finance to overcome the variety of the issue which may be faced by the company. Not only

that financial department of the company also help the company in improving the level of

investment decision in the organization. Accounting department also help the company in

presenting and making of a financial report for the company. Not only that this department of

company also help the company in managing the tax liability of the company by coordinating

with the legal department of the company (Mumford, 2017).

1

Introduction of Skanska PLc

Skanska Plc is the multinational construction and development company situated in

Sweden. It is fifth largest construction company of the world. The company is established since

133 years and is having headquarters in Stockholm Sweden. The construction projects of

company include renovations of UN headquarters, world trade centre, Moynihan Station and

many others

Define Accounting and Finance Department

Accounting and financial department of all the organization is regarded as a centre of all

the organization. Accounting and financial department generally ensures that financial

management and financial control are effectively controlled in the organization (Olbe, 2016).

Financial and accounting department generally controls the flow of money in and out of

business. Also, they make sure about the Payroll of all the employee and also perform the

activity of preparing financial report in the organization i.e. Profit and Loss Statement, Balance

sheet and budget. In simple words it can be said that it is the department which looks at

preparing financial statement, maintaining ledger, paying bills, manage payroll and flow of

money in & out of the business. Both the department used to operate same type of function but

the different is that Accounting department used to focus on the past, at the same time Finance

department used to focus on the future functioning of organization.

Importance of Accounting and Finance Department

Accounting and Finance department of Shanska PLc helps the company in managing the

finance in the organization. They generally make it sure that company is having a good amount

of the finance to overcome the variety of the issue which may be faced by the company. Not only

that financial department of the company also help the company in improving the level of

investment decision in the organization. Accounting department also help the company in

presenting and making of a financial report for the company. Not only that this department of

company also help the company in managing the tax liability of the company by coordinating

with the legal department of the company (Mumford, 2017).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Role of Accounts department

Financial Management: Accounting department generally used to play the role of financial

management in an organization. Accounting department of the organization looks at planning,

organizing, controlling and monitoring financial resources in a way that it help the company in

achieving the goal of the business. At the same time it has been critically analysed that

Accounting department of company individually are not capable of managing the finance in the

organization, they has to take the help of different department for performing the same activity.

For example, to plan budget of company they generally take help of different management

individual and departmental head.

Management Accounting: At the time of performing the activity related to the

management accounting in the organization, accounting department generally used to provide the

different financial report to the manager in the organization. On the basis of the same report in

the organization manager generally used to make different decision to find out the solution of the

issue which is faced by the company in current scenario (Balakrishnan, Prakash and Ramesh,

2018). At the same time it has been also seen that report which are provided by the accounting

department does not prove sufficient for the manager to make different decision. Hence, it can be

said that accounting department just play a part or small role in management accounting function

of an organization.

Tax Function: Accounting department in organization also used to play a critically role

in performing the tax function in the organization. Accounting department generally used to

consider nature of all the transaction which generally take place in the organization and on the

basis of the same make sure that tax liability of the company is fulfilled efficiently. Accounting

department also used to keep track of critical tax document. At the same time it has been also

seen that tax function is not only handled by the accounts department, Legal department of the

company also used to provide good hand of support to accounts department in carrying out the

different activity very efficiently in the organization.

Auditing Function: Under Auditing function of accounts department, department

generally looks to compile different policies and procedure with the current operation of the

business. Accounting department of the organization generally consider looking at the current

performance of business and evaluating the same. Accounting department of company assess the

compliance with the accounting standard of the company. In simple words accounting

2

Financial Management: Accounting department generally used to play the role of financial

management in an organization. Accounting department of the organization looks at planning,

organizing, controlling and monitoring financial resources in a way that it help the company in

achieving the goal of the business. At the same time it has been critically analysed that

Accounting department of company individually are not capable of managing the finance in the

organization, they has to take the help of different department for performing the same activity.

For example, to plan budget of company they generally take help of different management

individual and departmental head.

Management Accounting: At the time of performing the activity related to the

management accounting in the organization, accounting department generally used to provide the

different financial report to the manager in the organization. On the basis of the same report in

the organization manager generally used to make different decision to find out the solution of the

issue which is faced by the company in current scenario (Balakrishnan, Prakash and Ramesh,

2018). At the same time it has been also seen that report which are provided by the accounting

department does not prove sufficient for the manager to make different decision. Hence, it can be

said that accounting department just play a part or small role in management accounting function

of an organization.

Tax Function: Accounting department in organization also used to play a critically role

in performing the tax function in the organization. Accounting department generally used to

consider nature of all the transaction which generally take place in the organization and on the

basis of the same make sure that tax liability of the company is fulfilled efficiently. Accounting

department also used to keep track of critical tax document. At the same time it has been also

seen that tax function is not only handled by the accounts department, Legal department of the

company also used to provide good hand of support to accounts department in carrying out the

different activity very efficiently in the organization.

Auditing Function: Under Auditing function of accounts department, department

generally looks to compile different policies and procedure with the current operation of the

business. Accounting department of the organization generally consider looking at the current

performance of business and evaluating the same. Accounting department of company assess the

compliance with the accounting standard of the company. In simple words accounting

2

department used to play the role of supervisor of different operation in organization. It has been

also seen that in many organization accounting department do not play any kind of role in

Auditing function of organization. Auditing department is a separate department who generally

looks at the different operation of auditing in the organization. It is essential for the business to

have proper inspection of the accounting records prepared by the organisations. This function of

the accounts departments plays critical role as auditors certify whether the financial statements

are free from errors and mistakes. They ensure that the financial statements present true and fair

view of the financial position and performance of company.

Role of finance Department

Investment Function: Financial department of company generally looks at the present of

money in the organization and supports the senior management of the company at the time of

making any sort of decision in regards of new investment. Financial Department used to play the

supporting role at the time of making any sort of Investment decision in an organization. They

generally used to provider of the information about the amount of financial resources which is

possessed by them in general. At the same time it has been also analysed that some time

Financial department of the company has to change their opinion in the investment decision if

management of the company is more than keen to make a investment in the market. Management

has to make analysis of the proposed investments or the project that will be providing it adequate

return. The short term finances help the organisation in supporting their working capital

requirements.

Financing Function: Financing Function of finance department generally looks at

selecting the source through which finance can be recruited in the organization to carry out

different operation of the organization (O'Leary, 2020). Financial department generally looks at

understanding different sources through which organization can have a fund and on the basis of

same touch them whenever there is need of the same in the organization. At the same time it has

been critically understand that any wrong selection of sources of finance in the organization used

to create the variety of the issue for the organization to dealt with in future. They have to analyse

all the factors attached with the procurement of funds. Finance is considered as an important

accounting function as it provides funds for running the operations of business successfully.

Dividend Function: The dividend function of the finance department play a critical role

3

also seen that in many organization accounting department do not play any kind of role in

Auditing function of organization. Auditing department is a separate department who generally

looks at the different operation of auditing in the organization. It is essential for the business to

have proper inspection of the accounting records prepared by the organisations. This function of

the accounts departments plays critical role as auditors certify whether the financial statements

are free from errors and mistakes. They ensure that the financial statements present true and fair

view of the financial position and performance of company.

Role of finance Department

Investment Function: Financial department of company generally looks at the present of

money in the organization and supports the senior management of the company at the time of

making any sort of decision in regards of new investment. Financial Department used to play the

supporting role at the time of making any sort of Investment decision in an organization. They

generally used to provider of the information about the amount of financial resources which is

possessed by them in general. At the same time it has been also analysed that some time

Financial department of the company has to change their opinion in the investment decision if

management of the company is more than keen to make a investment in the market. Management

has to make analysis of the proposed investments or the project that will be providing it adequate

return. The short term finances help the organisation in supporting their working capital

requirements.

Financing Function: Financing Function of finance department generally looks at

selecting the source through which finance can be recruited in the organization to carry out

different operation of the organization (O'Leary, 2020). Financial department generally looks at

understanding different sources through which organization can have a fund and on the basis of

same touch them whenever there is need of the same in the organization. At the same time it has

been critically understand that any wrong selection of sources of finance in the organization used

to create the variety of the issue for the organization to dealt with in future. They have to analyse

all the factors attached with the procurement of funds. Finance is considered as an important

accounting function as it provides funds for running the operations of business successfully.

Dividend Function: The dividend function of the finance department play a critical role

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in the business. Profit earnings or the positive return are common objectives of the organisations.

Key function of finance department is to assess whether the company should distribute profits in

form of dividends to shareholders or retaining profits or making partial distributions. It is the role

of financial department to frame optimum dividend policy that will be maximising market value

of the company. Common practices of firm includes payment of dividends in case of profits. But

deciding about the dividends in case of inadequate profits is a challenging task for the financial

managers. Dividend policies have direct impact over the cash flows of business. The wealth is

decreased by the amount of dividend paid by company. In case of inadequate profits company

could make dividend cuts for managing the cash flows. The dividend decisions of the finance

department are directly associated with the shareholders’ equity. Also the company has to ensure

that there are adequate cash funds available to be distributed in the form of dividends.

Working Capital Function: This function of the financial department of the

organisation play an effective role in the success of the organisations. Working capital

management helps to ensure that the tied up capital in the company that could be utilised

otherwise over productive uses are released by the organisation for generating returns. It is the

effective tool that guarantees long term success of the business. Working capital helps to get

cheaper sources of the finance that could be used for the expansion of the existing projects for

new investments for company. One of the methods used by financial department for increasing

the profitability of the business is by effective working capital management. Improper

management of the working capital could lead to negative consequences for the business like

increase in loans or borrowing raising the finance cost of the business. This function has

significant attention of the managers as it is essential for the company to arrange different

functions in manner that effective operating cash cycle is maintained for meeting working capital

requirements.

TASK 2

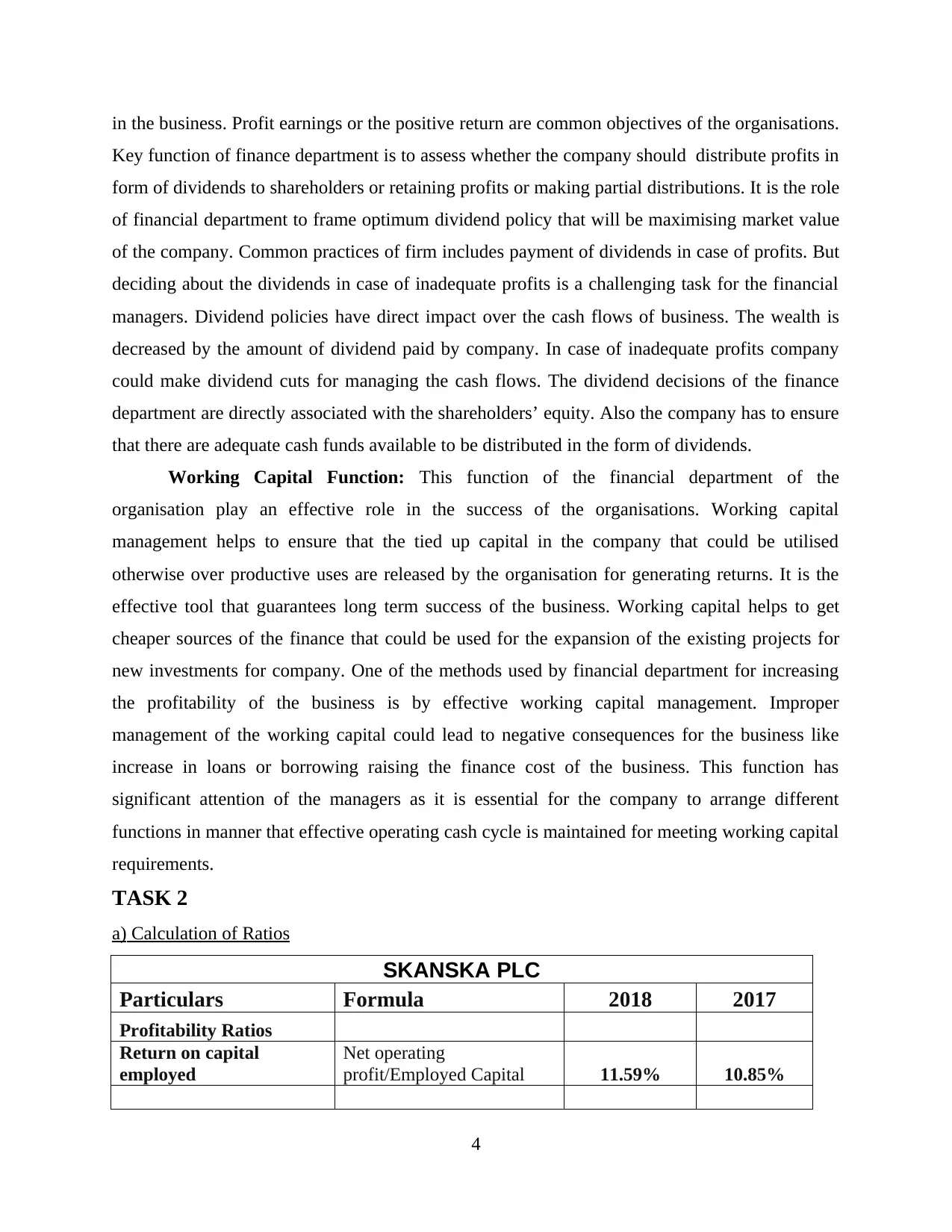

a) Calculation of Ratios

SKANSKA PLC

Particulars Formula 2018 2017

Profitability Ratios

Return on capital

employed

Net operating

profit/Employed Capital 11.59% 10.85%

4

Key function of finance department is to assess whether the company should distribute profits in

form of dividends to shareholders or retaining profits or making partial distributions. It is the role

of financial department to frame optimum dividend policy that will be maximising market value

of the company. Common practices of firm includes payment of dividends in case of profits. But

deciding about the dividends in case of inadequate profits is a challenging task for the financial

managers. Dividend policies have direct impact over the cash flows of business. The wealth is

decreased by the amount of dividend paid by company. In case of inadequate profits company

could make dividend cuts for managing the cash flows. The dividend decisions of the finance

department are directly associated with the shareholders’ equity. Also the company has to ensure

that there are adequate cash funds available to be distributed in the form of dividends.

Working Capital Function: This function of the financial department of the

organisation play an effective role in the success of the organisations. Working capital

management helps to ensure that the tied up capital in the company that could be utilised

otherwise over productive uses are released by the organisation for generating returns. It is the

effective tool that guarantees long term success of the business. Working capital helps to get

cheaper sources of the finance that could be used for the expansion of the existing projects for

new investments for company. One of the methods used by financial department for increasing

the profitability of the business is by effective working capital management. Improper

management of the working capital could lead to negative consequences for the business like

increase in loans or borrowing raising the finance cost of the business. This function has

significant attention of the managers as it is essential for the company to arrange different

functions in manner that effective operating cash cycle is maintained for meeting working capital

requirements.

TASK 2

a) Calculation of Ratios

SKANSKA PLC

Particulars Formula 2018 2017

Profitability Ratios

Return on capital

employed

Net operating

profit/Employed Capital 11.59% 10.85%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

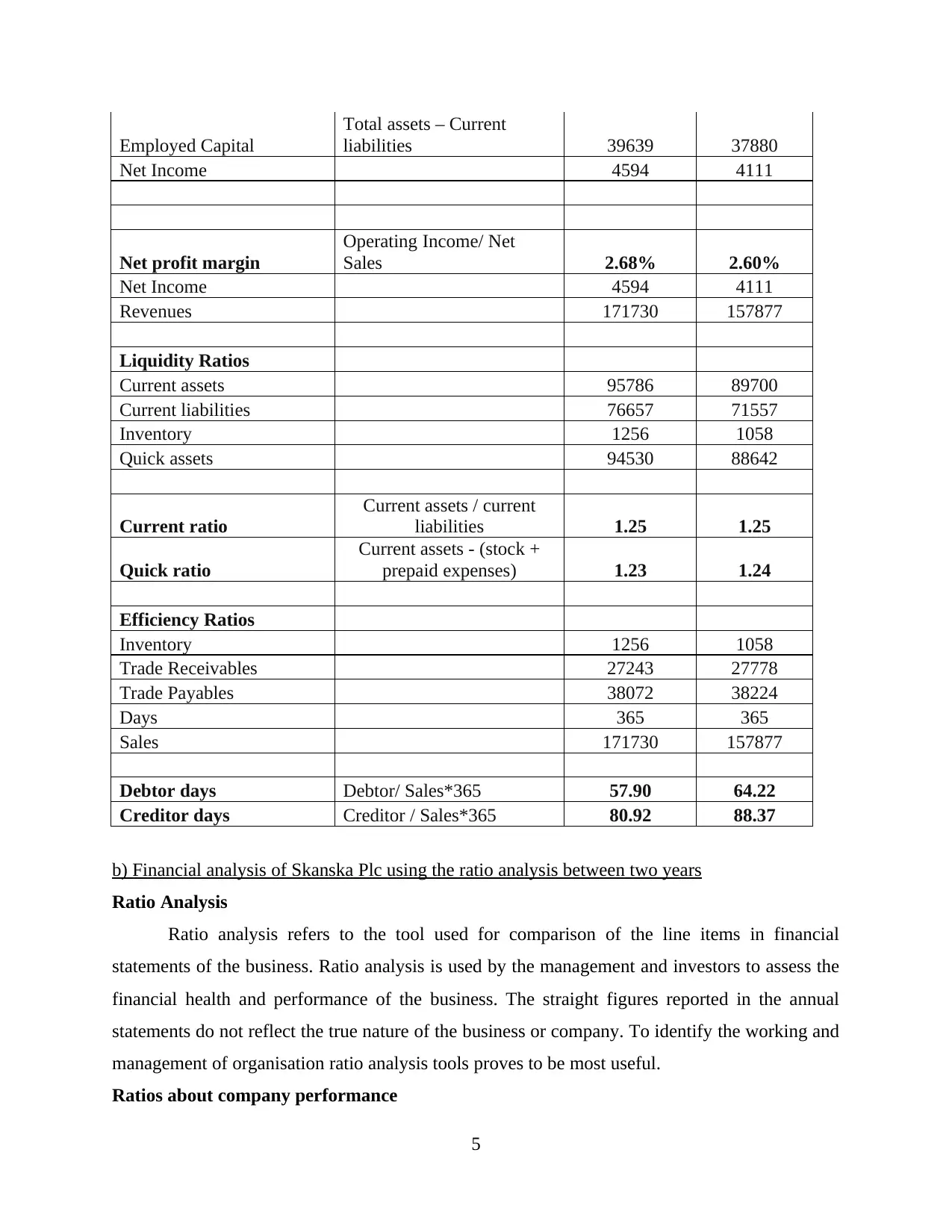

Employed Capital

Total assets – Current

liabilities 39639 37880

Net Income 4594 4111

Net profit margin

Operating Income/ Net

Sales 2.68% 2.60%

Net Income 4594 4111

Revenues 171730 157877

Liquidity Ratios

Current assets 95786 89700

Current liabilities 76657 71557

Inventory 1256 1058

Quick assets 94530 88642

Current ratio

Current assets / current

liabilities 1.25 1.25

Quick ratio

Current assets - (stock +

prepaid expenses) 1.23 1.24

Efficiency Ratios

Inventory 1256 1058

Trade Receivables 27243 27778

Trade Payables 38072 38224

Days 365 365

Sales 171730 157877

Debtor days Debtor/ Sales*365 57.90 64.22

Creditor days Creditor / Sales*365 80.92 88.37

b) Financial analysis of Skanska Plc using the ratio analysis between two years

Ratio Analysis

Ratio analysis refers to the tool used for comparison of the line items in financial

statements of the business. Ratio analysis is used by the management and investors to assess the

financial health and performance of the business. The straight figures reported in the annual

statements do not reflect the true nature of the business or company. To identify the working and

management of organisation ratio analysis tools proves to be most useful.

Ratios about company performance

5

Total assets – Current

liabilities 39639 37880

Net Income 4594 4111

Net profit margin

Operating Income/ Net

Sales 2.68% 2.60%

Net Income 4594 4111

Revenues 171730 157877

Liquidity Ratios

Current assets 95786 89700

Current liabilities 76657 71557

Inventory 1256 1058

Quick assets 94530 88642

Current ratio

Current assets / current

liabilities 1.25 1.25

Quick ratio

Current assets - (stock +

prepaid expenses) 1.23 1.24

Efficiency Ratios

Inventory 1256 1058

Trade Receivables 27243 27778

Trade Payables 38072 38224

Days 365 365

Sales 171730 157877

Debtor days Debtor/ Sales*365 57.90 64.22

Creditor days Creditor / Sales*365 80.92 88.37

b) Financial analysis of Skanska Plc using the ratio analysis between two years

Ratio Analysis

Ratio analysis refers to the tool used for comparison of the line items in financial

statements of the business. Ratio analysis is used by the management and investors to assess the

financial health and performance of the business. The straight figures reported in the annual

statements do not reflect the true nature of the business or company. To identify the working and

management of organisation ratio analysis tools proves to be most useful.

Ratios about company performance

5

It is very essential for the managers and investors to analyse the performance and position

of company before making investments in any of the company. Management identify whether

the strategies and policies implemented for the business have drawn the desired results or not. It

enables the management to frame more efficient strategies or to make improvements in the

existing framework (Bayrakdaroglu, Mirgen and Kuyu, 2017). Investors using ratio analysis

identify the profitability, liquidity position, efficiency and the solvency of an organisation. In the

present report ratio analysis of Skanska plc has been carried out for assessing the financial health

and performance of business.

Return on Capital employed

It is a ratio that is used by the investors to evaluate the efficiency of management and

profitability of the organisation. The ratio identifies the strength and capability of the

management in generating returns over capital employed in organisation. Business is started with

the motive of earning greater returns. Company is required to have adequate level of returns over

capital employed for building confidence in the investors. It could be analysed from the above

table that ROCE of Skanska Plc was 10.85% in 2017 and it has increased to 11.59% which

shows that the company has showed upward movement in the ROCE. It shows that the ROCE of

company is adequate however it has to be increased further for reflecting strong management

efficiency. It could also be seen that upward movement is seen in the ratio due to higher returns

generated by the company in comparison with last year (Almumani, 2018).

Increase in revenues have raised the return over capital employed. It could also be

evaluated that the management strategies for making effective utilisation of the existing

resources are becoming successful. The effectiveness of the strategies will also enable to build

strong confidence in the managers and will enable the organisation to frame more effective

policies. It could further increase the ratio by evaluating the assets that are unproductive and not

adding value to business. This will reduce the assets that are consuming unnecessary cost of

organisation. Skanska plc is having strong management that is enabling it to generate adequate

returns over the capital employed by the business.

Net Profit margin

This is one of the ratios used to assess profitability of the organisation. It is used mainly

for evaluating the net returns generated from carrying out the business throughout the year. Net

profit is the amount left with organisation after meeting all the costs and expenditures of the

6

of company before making investments in any of the company. Management identify whether

the strategies and policies implemented for the business have drawn the desired results or not. It

enables the management to frame more efficient strategies or to make improvements in the

existing framework (Bayrakdaroglu, Mirgen and Kuyu, 2017). Investors using ratio analysis

identify the profitability, liquidity position, efficiency and the solvency of an organisation. In the

present report ratio analysis of Skanska plc has been carried out for assessing the financial health

and performance of business.

Return on Capital employed

It is a ratio that is used by the investors to evaluate the efficiency of management and

profitability of the organisation. The ratio identifies the strength and capability of the

management in generating returns over capital employed in organisation. Business is started with

the motive of earning greater returns. Company is required to have adequate level of returns over

capital employed for building confidence in the investors. It could be analysed from the above

table that ROCE of Skanska Plc was 10.85% in 2017 and it has increased to 11.59% which

shows that the company has showed upward movement in the ROCE. It shows that the ROCE of

company is adequate however it has to be increased further for reflecting strong management

efficiency. It could also be seen that upward movement is seen in the ratio due to higher returns

generated by the company in comparison with last year (Almumani, 2018).

Increase in revenues have raised the return over capital employed. It could also be

evaluated that the management strategies for making effective utilisation of the existing

resources are becoming successful. The effectiveness of the strategies will also enable to build

strong confidence in the managers and will enable the organisation to frame more effective

policies. It could further increase the ratio by evaluating the assets that are unproductive and not

adding value to business. This will reduce the assets that are consuming unnecessary cost of

organisation. Skanska plc is having strong management that is enabling it to generate adequate

returns over the capital employed by the business.

Net Profit margin

This is one of the ratios used to assess profitability of the organisation. It is used mainly

for evaluating the net returns generated from carrying out the business throughout the year. Net

profit is the amount left with organisation after meeting all the costs and expenditures of the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organisation. It reflects the operating effectiveness of organisation and ability of management in

meeting the costs and expenditures of organisation adequately. In the above table it could be

evaluated that net profit margin is 2.68% in 2018 where in year 2017 the ratio was 2.60%. The

net profit margin of company is very low. There has been very low movement in the ratio from

last year. It could be evaluated from the ratio that net profit margin of company has to be

strengthened as it could face negative consequences with lower profit margin. The profit margin

of Skanska is low as costs are very high (Laitinen and Laitinen, 2018). Cost of sales of company

are very high as against the revenues. It could also be evaluated that company has controlled the

costs in comparison to last year as against the sales but growth is not seen as income from joint

ventures was low. It had made divestment from many joint ventures causing decrease in income.

Also the tax expense for the year is double in current year that has declined the profit to further

lower level. It has to adopt new policies and strategies for meeting the costs effectively and

increasing the profits (Erin and Oduwole, 2018). Profits are most attractive source for investors

through which companies could expand the business.

Current Ratio

The current ratio is used for analysing the liquidity of company. The current ratio reflects

the ability of company to make payment for short term obligations. Funds are required for

running the operations of business smoothly. They have to manage the operations of business by

effectively managing the cash flows (Ardekani, Distinguin and Tarazi, 2020). Current ratio of

Skanska plc in the year 2018 is 1.25 and it was same in the year 2017 at 1.25. The current ratio

of the company is adequate which shows that the business is making effective utilisation of the

financial resources. There is no movement in the ratios over the two years that shows that the

management has effectively maintained the liquidity position. Company has increased the

current assets and liabilities in the same proportion. The standard current ratio is 2:1 where ratio

of company is below the standard.

The reason behind no change in the movement of current ratio could be said that the

company has adopted adequate level of strategies for maintaining the cash flows. Current assets

have increased from last year and so is the liabilities that enabled it to maintain the ratio. It has to

ensure that the ratio does not goes beyond this level as maintaining current ratio is essential.

Many stakeholders of the organisation are concerned with the liquidity position of the business

7

meeting the costs and expenditures of organisation adequately. In the above table it could be

evaluated that net profit margin is 2.68% in 2018 where in year 2017 the ratio was 2.60%. The

net profit margin of company is very low. There has been very low movement in the ratio from

last year. It could be evaluated from the ratio that net profit margin of company has to be

strengthened as it could face negative consequences with lower profit margin. The profit margin

of Skanska is low as costs are very high (Laitinen and Laitinen, 2018). Cost of sales of company

are very high as against the revenues. It could also be evaluated that company has controlled the

costs in comparison to last year as against the sales but growth is not seen as income from joint

ventures was low. It had made divestment from many joint ventures causing decrease in income.

Also the tax expense for the year is double in current year that has declined the profit to further

lower level. It has to adopt new policies and strategies for meeting the costs effectively and

increasing the profits (Erin and Oduwole, 2018). Profits are most attractive source for investors

through which companies could expand the business.

Current Ratio

The current ratio is used for analysing the liquidity of company. The current ratio reflects

the ability of company to make payment for short term obligations. Funds are required for

running the operations of business smoothly. They have to manage the operations of business by

effectively managing the cash flows (Ardekani, Distinguin and Tarazi, 2020). Current ratio of

Skanska plc in the year 2018 is 1.25 and it was same in the year 2017 at 1.25. The current ratio

of the company is adequate which shows that the business is making effective utilisation of the

financial resources. There is no movement in the ratios over the two years that shows that the

management has effectively maintained the liquidity position. Company has increased the

current assets and liabilities in the same proportion. The standard current ratio is 2:1 where ratio

of company is below the standard.

The reason behind no change in the movement of current ratio could be said that the

company has adopted adequate level of strategies for maintaining the cash flows. Current assets

have increased from last year and so is the liabilities that enabled it to maintain the ratio. It has to

ensure that the ratio does not goes beyond this level as maintaining current ratio is essential.

Many stakeholders of the organisation are concerned with the liquidity position of the business

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as they have interest in the financial liquidity and position of the enterprise. Suppliers do not

make further transactions with company have weak liquidity position.

It is essential for the organisation to enhance its liquidity position by effective working capital

management. It has to ensure that the operating cash cycle of the company is running effectively.

The revenues have to be increased and for meeting the working capital requirements it could

reduce the short term borrowings and make long term borrowing for decreasing the current

liabilities. The cash flows have to be managed over effective places only.

Debtor’s collection Period

Debtor collection period refers to the time taken by the company to collect all the trade

debts. Smaller amount of time firm takes to collect the debts, more efficient company seems to

be. Longer time indicates that firm have problems or issues in collecting the payments or have

less efficiency. The management ensures that the company has adequate debtor collection days

where it could manage the cash cycle.

Debtor collection period of Skanska was 64 days in the year 2017 and has reduced to 58

days. There is downward movement in the collection days which is a good sign. This reflects that

the management is able to collect dues timely as compared with last year (Stana and Brazis,

2019). The lower collection period has happened due to increasing the interest rate over late

payments and reducing trade with customers having bad trade records that are not able to make

timely payments.

Creditor’s payable period

It refers to the time that indicates time taken by company to make payments to the

suppliers. The creditor payment period are suggested to be greater as they enable the company to

utilise funds elsewhere over more productive uses. The creditor payment period has reduced to

80 days from the 88 days in last year. The management of the company is efficient as it reduced

the creditor period along with debtor period for maintaining the effective cash cycle.

CONCLUSION

It could be summarised from the above report that the financial management plays an

effective role in the success of organisation. They have to manage the operations of business in

manner for generating adequate returns. From the ratio analysis it could be concluded that the

financial management of company is adequate and also the company is profitable with adequate

liquidity position. Funds will help the organisation to enhance the marketing efforts and business

8

make further transactions with company have weak liquidity position.

It is essential for the organisation to enhance its liquidity position by effective working capital

management. It has to ensure that the operating cash cycle of the company is running effectively.

The revenues have to be increased and for meeting the working capital requirements it could

reduce the short term borrowings and make long term borrowing for decreasing the current

liabilities. The cash flows have to be managed over effective places only.

Debtor’s collection Period

Debtor collection period refers to the time taken by the company to collect all the trade

debts. Smaller amount of time firm takes to collect the debts, more efficient company seems to

be. Longer time indicates that firm have problems or issues in collecting the payments or have

less efficiency. The management ensures that the company has adequate debtor collection days

where it could manage the cash cycle.

Debtor collection period of Skanska was 64 days in the year 2017 and has reduced to 58

days. There is downward movement in the collection days which is a good sign. This reflects that

the management is able to collect dues timely as compared with last year (Stana and Brazis,

2019). The lower collection period has happened due to increasing the interest rate over late

payments and reducing trade with customers having bad trade records that are not able to make

timely payments.

Creditor’s payable period

It refers to the time that indicates time taken by company to make payments to the

suppliers. The creditor payment period are suggested to be greater as they enable the company to

utilise funds elsewhere over more productive uses. The creditor payment period has reduced to

80 days from the 88 days in last year. The management of the company is efficient as it reduced

the creditor period along with debtor period for maintaining the effective cash cycle.

CONCLUSION

It could be summarised from the above report that the financial management plays an

effective role in the success of organisation. They have to manage the operations of business in

manner for generating adequate returns. From the ratio analysis it could be concluded that the

financial management of company is adequate and also the company is profitable with adequate

liquidity position. Funds will help the organisation to enhance the marketing efforts and business

8

operations. Ratio analysis is an effective tool used by the management and investors to evaluate

the performance of organisation.

9

the performance of organisation.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.