BM414 Financial Decision Making: SKANSKA PLC Performance Report

VerifiedAdded on 2023/01/09

|13

|3927

|91

Report

AI Summary

This report provides a detailed analysis of financial decision-making, focusing on the application of various management accounting techniques within the context of SKANSKA PLC, a construction company. The report begins by exploring the roles and functions of financial and accounting divisions, highlighting the importance of financial forecasting, financial statement reviews, and traditional costing methods. It then delves into a critical analysis of these techniques, assessing their significance in planning, control, and decision-making processes. The report further evaluates SKANSKA PLC's financial performance using key ratios such as Return on Capital Employed (ROCE), net profit margin, current ratio, and collection periods, providing insights into the company's efficiency and profitability. The analysis includes a comparison of the company's performance over two years, drawing conclusions on the effectiveness of its financial strategies. The report emphasizes the importance of financial analysis in driving internal progress and making informed decisions, offering a comprehensive overview of the financial aspects of SKANSKA PLC.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Role of management accounting techniques in planning, Control and decision making process

................................................................................................................................................3

Critical analysis of management accounting techniques........................................................5

CONCLUSION......................................................................................................................6

TASK 2............................................................................................................................................8

Assessing key ratios of SKANSKA PLC evaluate organisation's performance....................8

Comment on performance of SKANSKA PLC, based on computed ratios:..........................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Role of management accounting techniques in planning, Control and decision making process

................................................................................................................................................3

Critical analysis of management accounting techniques........................................................5

CONCLUSION......................................................................................................................6

TASK 2............................................................................................................................................8

Assessing key ratios of SKANSKA PLC evaluate organisation's performance....................8

Comment on performance of SKANSKA PLC, based on computed ratios:..........................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Decision-making is among the key factors in managing every company and it relies mostly

on management knowledge and expertise. The phrase "financial decision-making" is

described as a method in which a firm financial management team determines the desire for

resources to conduct out additional activities and distribute money for productive activities. This

decision-making method needs to be carried out in an acceptable way since in the long term any

kind of error could result to a variety of problems (Bryer, 2013). In addition, Decision-making

plays an influencing role in every company's progress. The enterprises typically make their

proposals and spending planning with particular goals and priorities. Better qualified decisions

move the company towards a new direction, but much of that depends on financial management,

how policies are executed and how action objectives are pursued. The report is based on

SKANSKA plc, it is a construction company founded in in United Kingdom. In fact, it is a

building firm that works on massive civil tasks. The business is using a variety of financial

management methods to handle its activities efficiently. The Company plans to expand its

operations to other European nations within the next ten (10) years.

In this report, the first task is related with roles and functions of the finance and accounting

divisions. Various forms of accounting management strategies are listed in the study alongside

their functions in improved strategic planning (Cescon, Costantini and Grassetti, 2019).

Accounting and financial unit of company plays a crucial role in the dimension that they have of

careful while controlling financial capital. Essentially, a company's reputation depends upon how

much the division of finance and accounting executes its functions. Both divisions have duties

and responsibilities which are their own. Nevertheless, finance and accounting agencies are

interconnected. The finance department perform a crucial part in the processing of financial

reports at the close of the budget year as well as in the compilation of correct financial

statements.

TASK 1

Role of management accounting techniques in planning, Control and decision making process

The word accounting management (MA) involves giving monetary and non-monetary

information to managers, which help to look each activity closely and make suitable decision.

Although, the accounting division is responsible for regularly tracking all banking transactions in

Decision-making is among the key factors in managing every company and it relies mostly

on management knowledge and expertise. The phrase "financial decision-making" is

described as a method in which a firm financial management team determines the desire for

resources to conduct out additional activities and distribute money for productive activities. This

decision-making method needs to be carried out in an acceptable way since in the long term any

kind of error could result to a variety of problems (Bryer, 2013). In addition, Decision-making

plays an influencing role in every company's progress. The enterprises typically make their

proposals and spending planning with particular goals and priorities. Better qualified decisions

move the company towards a new direction, but much of that depends on financial management,

how policies are executed and how action objectives are pursued. The report is based on

SKANSKA plc, it is a construction company founded in in United Kingdom. In fact, it is a

building firm that works on massive civil tasks. The business is using a variety of financial

management methods to handle its activities efficiently. The Company plans to expand its

operations to other European nations within the next ten (10) years.

In this report, the first task is related with roles and functions of the finance and accounting

divisions. Various forms of accounting management strategies are listed in the study alongside

their functions in improved strategic planning (Cescon, Costantini and Grassetti, 2019).

Accounting and financial unit of company plays a crucial role in the dimension that they have of

careful while controlling financial capital. Essentially, a company's reputation depends upon how

much the division of finance and accounting executes its functions. Both divisions have duties

and responsibilities which are their own. Nevertheless, finance and accounting agencies are

interconnected. The finance department perform a crucial part in the processing of financial

reports at the close of the budget year as well as in the compilation of correct financial

statements.

TASK 1

Role of management accounting techniques in planning, Control and decision making process

The word accounting management (MA) involves giving monetary and non-monetary

information to managers, which help to look each activity closely and make suitable decision.

Although, the accounting division is responsible for regularly tracking all banking transactions in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

order to provide necessary details to operation manager. Some MA techniques which are very

important for company are discussed below:

Financial forecasting: This is a sort of financial asset related to the currency preparation

process focused on predicting projected sales and expenditures (Alsharari and Al-Shboul, 2019).

Financial planning can be advantageous, as in the SKANSKA business, because they can

regulate their capital effectively on the premises of respective information. This will also allow

manager of company to properly allocate the financial resources to the different types of

exercises.

Financial Report Review: The annual report is comprised of various forms of records such

as sales analysis, balance sheet, cash flow, ratio Analysis. Comprehensive review of these annual

records may be helpful in determining company's actual role. As in the preferred business

SKANSKA, financial statement is useful in determining their present position.

Traditional accounting technique: The term traditional cost accounting can be interpreted

as an accounting being used resources in compliance with commonly agreed reporting

requirements (Pelz, 2019). Like in the SKANSKA, the valuation of the property will be

measured as per the original outlay which eases in making current decision.

Standard costing: This type of costing approach related to estimating the possible costs of

various activities can be defined. This method for expense accounting is called normal costing.

As for the aforementioned SKANSKA group, financial managers should use this costing

approach to better calculate the potential costs of manufacturing activities and keep matching

current costs with this calculation.

Budgetary management: It mainly applies to controlling the budgetary performance of

organisations by implementing preparation of spending. They manage the financial performance

of the above listed SKANSKA business by managing budgets including cash forecasts, capital

spending etc.

Marginal method of costing: This technique, includes all expenses (fixed and variable)

are viewed equally such as fixed costs as regular expenses and variable costs as service expenses.

For example, in respective company, manager can use this costing approach to

formulate financial statements and determine the net profit.

Fund balance statement: It provides detailed information about changes in financial

position of the company in specified time period (Burritt, Schaltegger and Viere, 2019). With

important for company are discussed below:

Financial forecasting: This is a sort of financial asset related to the currency preparation

process focused on predicting projected sales and expenditures (Alsharari and Al-Shboul, 2019).

Financial planning can be advantageous, as in the SKANSKA business, because they can

regulate their capital effectively on the premises of respective information. This will also allow

manager of company to properly allocate the financial resources to the different types of

exercises.

Financial Report Review: The annual report is comprised of various forms of records such

as sales analysis, balance sheet, cash flow, ratio Analysis. Comprehensive review of these annual

records may be helpful in determining company's actual role. As in the preferred business

SKANSKA, financial statement is useful in determining their present position.

Traditional accounting technique: The term traditional cost accounting can be interpreted

as an accounting being used resources in compliance with commonly agreed reporting

requirements (Pelz, 2019). Like in the SKANSKA, the valuation of the property will be

measured as per the original outlay which eases in making current decision.

Standard costing: This type of costing approach related to estimating the possible costs of

various activities can be defined. This method for expense accounting is called normal costing.

As for the aforementioned SKANSKA group, financial managers should use this costing

approach to better calculate the potential costs of manufacturing activities and keep matching

current costs with this calculation.

Budgetary management: It mainly applies to controlling the budgetary performance of

organisations by implementing preparation of spending. They manage the financial performance

of the above listed SKANSKA business by managing budgets including cash forecasts, capital

spending etc.

Marginal method of costing: This technique, includes all expenses (fixed and variable)

are viewed equally such as fixed costs as regular expenses and variable costs as service expenses.

For example, in respective company, manager can use this costing approach to

formulate financial statements and determine the net profit.

Fund balance statement: It provides detailed information about changes in financial

position of the company in specified time period (Burritt, Schaltegger and Viere, 2019). With

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this tool, SKANSKA Company will determine their financial position and

make necessary decision.

Interactive and dynamic methodology: These approaches are linked to evaluating and

describing the financial activities of companies using diagrams. Within this process, graph

analysis is conducted to assess the financial position. Like the above-mentioned organisation, its

financial situation can be evaluated by perusing the business results in charts and graphs.

Communicating: This technique in management accounting is linked to interacting with

monetary and non - monetary information to managers, so that they can make further decisions.

Cash balance statement: This provides details about the cash flow of an entity. This is

designed through 3 types of running, funding, and acquisition activities. Within SKANSKA

manager should manage the actions involving quite enough cash out flow.

Revaluation accounting: This is an accounting approach related to the valuation of the

company by comparing between the actual values of the assets versus the original cost. They will

discover differences, including in the above company, between the equal and classical worth of

their current capital.

Critical analysis of management accounting techniques

The above-mentioned MA approaches are too relevant for companies as they are valuable

for providing detailed data on monetary and non - monetary dimensions. The significance of

these approaches is defined below:

Performance assessment: These approaches are helpful in evaluating the favourable

business of the companies' operations (Setiawan, Rahmawati, and Widagdo, 2019). In the

context of SKANSKA, normal costing approach is supportive in the equation of actual costs

with expected costs may be helpful. If the actual value is lower than expected, the financial

performance of the enterprise would have been significant.

Increase market productivity: The crucial thing of these approaches is that they really are

successful in enhancing the success of the organization. This is because management processes

like financial modelling can be beneficial in developing the efficiency of business. Such

techniques, in SKANSKA market, are useful for improving the utilization of their various

production activities.

The above-mentioned advantages are general to all and apart from these advantages; there is

a certain special function to be played under such approaches as:

make necessary decision.

Interactive and dynamic methodology: These approaches are linked to evaluating and

describing the financial activities of companies using diagrams. Within this process, graph

analysis is conducted to assess the financial position. Like the above-mentioned organisation, its

financial situation can be evaluated by perusing the business results in charts and graphs.

Communicating: This technique in management accounting is linked to interacting with

monetary and non - monetary information to managers, so that they can make further decisions.

Cash balance statement: This provides details about the cash flow of an entity. This is

designed through 3 types of running, funding, and acquisition activities. Within SKANSKA

manager should manage the actions involving quite enough cash out flow.

Revaluation accounting: This is an accounting approach related to the valuation of the

company by comparing between the actual values of the assets versus the original cost. They will

discover differences, including in the above company, between the equal and classical worth of

their current capital.

Critical analysis of management accounting techniques

The above-mentioned MA approaches are too relevant for companies as they are valuable

for providing detailed data on monetary and non - monetary dimensions. The significance of

these approaches is defined below:

Performance assessment: These approaches are helpful in evaluating the favourable

business of the companies' operations (Setiawan, Rahmawati, and Widagdo, 2019). In the

context of SKANSKA, normal costing approach is supportive in the equation of actual costs

with expected costs may be helpful. If the actual value is lower than expected, the financial

performance of the enterprise would have been significant.

Increase market productivity: The crucial thing of these approaches is that they really are

successful in enhancing the success of the organization. This is because management processes

like financial modelling can be beneficial in developing the efficiency of business. Such

techniques, in SKANSKA market, are useful for improving the utilization of their various

production activities.

The above-mentioned advantages are general to all and apart from these advantages; there is

a certain special function to be played under such approaches as:

1. Significance in planning: MA methodologies are helpful in making preparations

profitable. This is partially because there are a wide variety of techniques available, such

as financial modelling, fixed costs etc. Companies can create reliable predictions based

on these techniques and can easily formulate statements. As with the SKANSKA

Company described above, they could use MA approaches to formulate their financial

plan.

2. Significance in controlling-The valuation of accrual accounting methods is that it help to

manage business policies effectively (Hariyati, Tjahjadi and Soewarno, 2019). That is

because companies like SKANSKA can monitor their manufacturing plants using all

these managerial accounting. They can also collect main income and expenditure relevant

data that may contribute to improvement preparing for the forthcoming financial

accounting.

3. Significance of decision-making: It is the most critical things about any form of

company. In addition to these advantages of MA approaches, decision-making is often

important element in which strategies play a major role. Like in the case of the above-

mentioned SKANSKA Company, they will take business choices to expand their UK

business within the next 10 years.

Therefore all these additional value of the accounting management techniques in the

SKANSKA sector will lead to grow business in different part of world without any big issue.

These accounting techniques will also play a vital part for them and also focussing on increasing

their firms. Financial analysis and examination is a process that requires and transforms raw

accounting inputs into reliable, available, and comparable financial statements. A finance

department contributes to internal progress by constantly measuring and tracking key items

which are important for business development. In Skanska Plc, it includes a summary of all

sources of income, expenditures and funds available for future use (apart from those currently

allocated and scheduled for the reporting period) and certain non-monetary information.

However usually they are presented to managers in a transparent and substantive manner.

CONCLUSION

It can be inferred on the grounds of the above section of the project study, each process or

strategy has its own role and significance in the context of the company entities. Such

approaches are important for businesses to deal with in order to be able to maintain them in a

profitable. This is partially because there are a wide variety of techniques available, such

as financial modelling, fixed costs etc. Companies can create reliable predictions based

on these techniques and can easily formulate statements. As with the SKANSKA

Company described above, they could use MA approaches to formulate their financial

plan.

2. Significance in controlling-The valuation of accrual accounting methods is that it help to

manage business policies effectively (Hariyati, Tjahjadi and Soewarno, 2019). That is

because companies like SKANSKA can monitor their manufacturing plants using all

these managerial accounting. They can also collect main income and expenditure relevant

data that may contribute to improvement preparing for the forthcoming financial

accounting.

3. Significance of decision-making: It is the most critical things about any form of

company. In addition to these advantages of MA approaches, decision-making is often

important element in which strategies play a major role. Like in the case of the above-

mentioned SKANSKA Company, they will take business choices to expand their UK

business within the next 10 years.

Therefore all these additional value of the accounting management techniques in the

SKANSKA sector will lead to grow business in different part of world without any big issue.

These accounting techniques will also play a vital part for them and also focussing on increasing

their firms. Financial analysis and examination is a process that requires and transforms raw

accounting inputs into reliable, available, and comparable financial statements. A finance

department contributes to internal progress by constantly measuring and tracking key items

which are important for business development. In Skanska Plc, it includes a summary of all

sources of income, expenditures and funds available for future use (apart from those currently

allocated and scheduled for the reporting period) and certain non-monetary information.

However usually they are presented to managers in a transparent and substantive manner.

CONCLUSION

It can be inferred on the grounds of the above section of the project study, each process or

strategy has its own role and significance in the context of the company entities. Such

approaches are important for businesses to deal with in order to be able to maintain them in a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

competitive world. In addition to their significance, the article provides a thorough overview of

the MA techniques. That strategy has to do with a business entity’s development, such as

approaches relating to expense control have to do with the business department's finance

department. Unlike other approaches, there is also a partnership with all kinds of business things.

the MA techniques. That strategy has to do with a business entity’s development, such as

approaches relating to expense control have to do with the business department's finance

department. Unlike other approaches, there is also a partnership with all kinds of business things.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

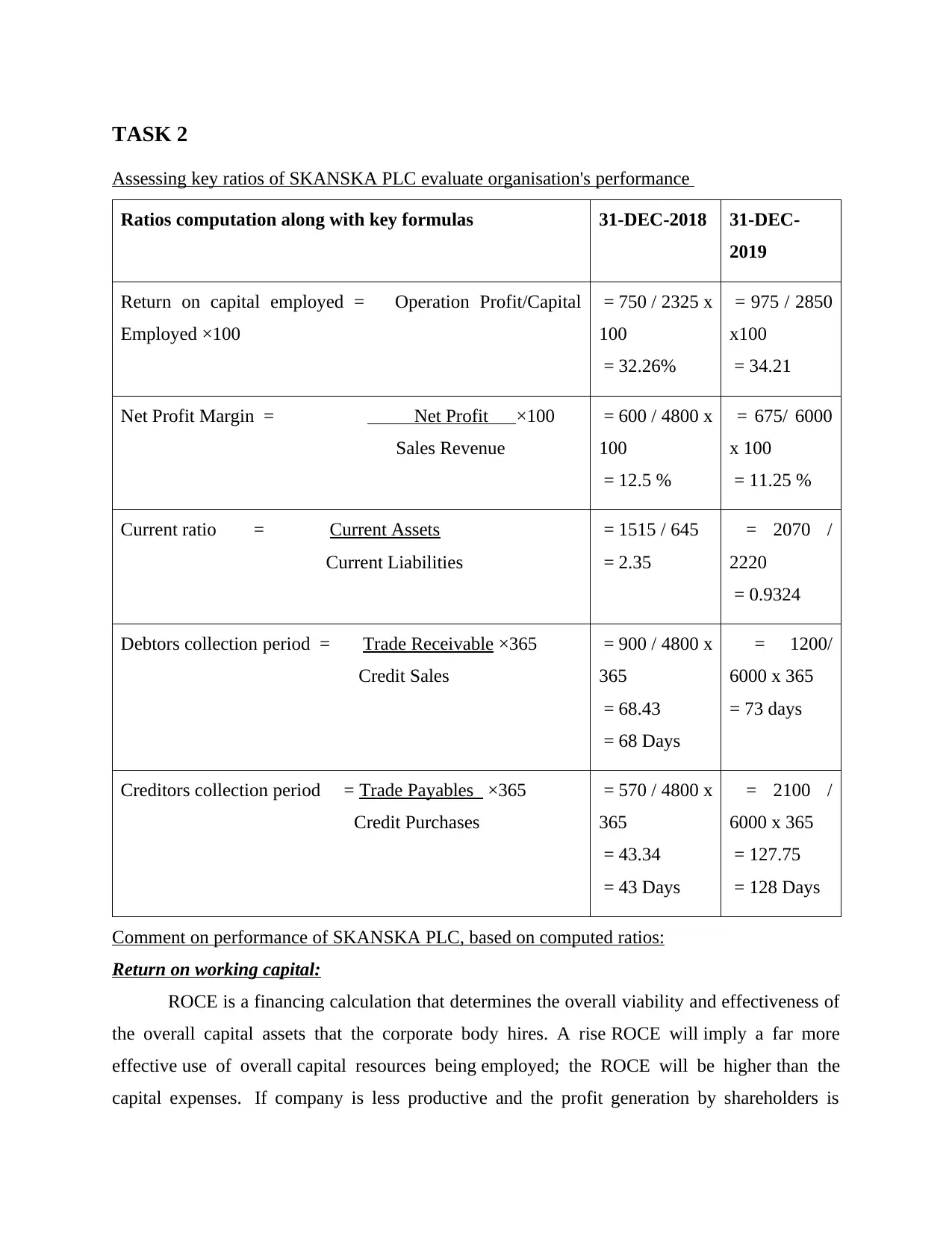

Assessing key ratios of SKANSKA PLC evaluate organisation's performance

Ratios computation along with key formulas 31-DEC-2018 31-DEC-

2019

Return on capital employed = Operation Profit/Capital

Employed ×100

= 750 / 2325 x

100

= 32.26%

= 975 / 2850

x100

= 34.21

Net Profit Margin = Net Profit ×100

Sales Revenue

= 600 / 4800 x

100

= 12.5 %

= 675/ 6000

x 100

= 11.25 %

Current ratio = Current Assets

Current Liabilities

= 1515 / 645

= 2.35

= 2070 /

2220

= 0.9324

Debtors collection period = Trade Receivable ×365

Credit Sales

= 900 / 4800 x

365

= 68.43

= 68 Days

= 1200/

6000 x 365

= 73 days

Creditors collection period = Trade Payables ×365

Credit Purchases

= 570 / 4800 x

365

= 43.34

= 43 Days

= 2100 /

6000 x 365

= 127.75

= 128 Days

Comment on performance of SKANSKA PLC, based on computed ratios:

Return on working capital:

ROCE is a financing calculation that determines the overall viability and effectiveness of

the overall capital assets that the corporate body hires. A rise ROCE will imply a far more

effective use of overall capital resources being employed; the ROCE will be higher than the

capital expenses. If company is less productive and the profit generation by shareholders is

Assessing key ratios of SKANSKA PLC evaluate organisation's performance

Ratios computation along with key formulas 31-DEC-2018 31-DEC-

2019

Return on capital employed = Operation Profit/Capital

Employed ×100

= 750 / 2325 x

100

= 32.26%

= 975 / 2850

x100

= 34.21

Net Profit Margin = Net Profit ×100

Sales Revenue

= 600 / 4800 x

100

= 12.5 %

= 675/ 6000

x 100

= 11.25 %

Current ratio = Current Assets

Current Liabilities

= 1515 / 645

= 2.35

= 2070 /

2220

= 0.9324

Debtors collection period = Trade Receivable ×365

Credit Sales

= 900 / 4800 x

365

= 68.43

= 68 Days

= 1200/

6000 x 365

= 73 days

Creditors collection period = Trade Payables ×365

Credit Purchases

= 570 / 4800 x

365

= 43.34

= 43 Days

= 2100 /

6000 x 365

= 127.75

= 128 Days

Comment on performance of SKANSKA PLC, based on computed ratios:

Return on working capital:

ROCE is a financing calculation that determines the overall viability and effectiveness of

the overall capital assets that the corporate body hires. A rise ROCE will imply a far more

effective use of overall capital resources being employed; the ROCE will be higher than the

capital expenses. If company is less productive and the profit generation by shareholders is

negligible that it has higher allocation of resources. ROCE calculation is a practical tool in which

benefits through companies are compared based on the amount of capital spent. The only focus

is on determining the company is a worthy option at EBIT alone (Hatefi, 2019). Investors must

look at portfolios to calculate ROCE and find pretty realistic method then ROE to examine the

possible earnings of the company leading to variations outstanding loans and spending.

As defined in above table, Skanska Plc's ROCE proportion is 32.26% in 2018, compared

with 34.21% in 2019 for a rightward increase in the ROCE. A high ROCE is helpful in

suggesting that the firm owns more revenue than just a pound of spending. A higher proportion

of ROCE is beneficial, meaning that the company is delivering greater income to its shareholder

on the money spent inside the enterprise. A smaller proportion of ROCE means company leading

to lower production. A business with fewer capital reserves with the same income / profits than

its rival firms would see better returns on the gross amount of investment money. Furthermore,

in the sense of Skanska Plc, such an improvement indicates that the capacity of the company to

produce on the maximum capital invested in the business has increased over the duration.

Net margin on profit:

Net margin defines how successful a company is in getting profit from a unit of income.

It is perhaps the most important metrics of productivity. The net margin includes all factors that

have an influence on the productivity position of the company, within or outside under the

management power. The higher the number, the more cost-control-effective the business

organization is (Paudel, Nagana Gowda and Raftery 2019).

In the respect of above estimation about the Skanska Plc Company’s factors, it was

evaluated that perhaps the operating profit margin in 2019 was only 11.25 % and 12.5 % in 2018.

The result shows of a small reduction in overall NP per share. Here, this reduction in NP margin

reveals that the real success of Skanska Plc in turning its total sales into earnings has decreased

over the timeframe mentioned. The company will focus on this dimension to improve their

results. Sales output will be improved for this company, and the gross market expenses / costs

must be reduced.

Current proportion measurement:

Current proportion is important in short-run and is consider part of liquidity ratio that

is used to assess the company’s real liquidity position, taking into consideration the relation

between all total assets as well as all existing liabilities. In simple terms, it is the method used to

benefits through companies are compared based on the amount of capital spent. The only focus

is on determining the company is a worthy option at EBIT alone (Hatefi, 2019). Investors must

look at portfolios to calculate ROCE and find pretty realistic method then ROE to examine the

possible earnings of the company leading to variations outstanding loans and spending.

As defined in above table, Skanska Plc's ROCE proportion is 32.26% in 2018, compared

with 34.21% in 2019 for a rightward increase in the ROCE. A high ROCE is helpful in

suggesting that the firm owns more revenue than just a pound of spending. A higher proportion

of ROCE is beneficial, meaning that the company is delivering greater income to its shareholder

on the money spent inside the enterprise. A smaller proportion of ROCE means company leading

to lower production. A business with fewer capital reserves with the same income / profits than

its rival firms would see better returns on the gross amount of investment money. Furthermore,

in the sense of Skanska Plc, such an improvement indicates that the capacity of the company to

produce on the maximum capital invested in the business has increased over the duration.

Net margin on profit:

Net margin defines how successful a company is in getting profit from a unit of income.

It is perhaps the most important metrics of productivity. The net margin includes all factors that

have an influence on the productivity position of the company, within or outside under the

management power. The higher the number, the more cost-control-effective the business

organization is (Paudel, Nagana Gowda and Raftery 2019).

In the respect of above estimation about the Skanska Plc Company’s factors, it was

evaluated that perhaps the operating profit margin in 2019 was only 11.25 % and 12.5 % in 2018.

The result shows of a small reduction in overall NP per share. Here, this reduction in NP margin

reveals that the real success of Skanska Plc in turning its total sales into earnings has decreased

over the timeframe mentioned. The company will focus on this dimension to improve their

results. Sales output will be improved for this company, and the gross market expenses / costs

must be reduced.

Current proportion measurement:

Current proportion is important in short-run and is consider part of liquidity ratio that

is used to assess the company’s real liquidity position, taking into consideration the relation

between all total assets as well as all existing liabilities. In simple terms, it is the method used to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

deduce whether or not the outstanding obligations can be compensated by using the existing

asset account individual. This ratio is meant not only to measure the liquidity challenges, and

also to decide exactly the uses of working resources. The operating cash flow state will

automatically look favourable if that ratio approaches 2 (Stanley, 2020). A current ratio gives

guarantees to consumers and other interested stakeholders that by using available funds resources

as well as other financial assets, companies which or may not have problems in covering off

short-term fees or existing liabilities. This mix helps executives to learn about the potential

approach on retained earnings and fix current liquidity issues. Negotiations with banking are

more likely to delay such charges in late payments or discussions with distributors.

From the above table reflecting Skanska Plc current proportions, it was estimated that the

firm's existing ratios in 2018 were 2.34, which plummeted to 0.9324, indicating a major decrease

in this proportion. This big decrease in the proportion is an unfavourable sign for the liquidity

position of company Skanska Plc. This change in the existing ratio suggests a dramatic decline in

the organization's ability to meet its short-term payables / liabilities. This item should be given

priority by the company, and that might have a longer impact on Skanska business growth

prospects. While this only suggests the corporation's short-term liquidity position, lack of this

proportion outcome may result in the firm's unfavourable financial situation (Bakhtavar, Yousefi

and Jafarpour, 2019).

Average-receivable days/ Debtors:

Debtors collection period simply corresponds to an estimated average usually of days that

and company needs to recover purchases of its trading credits over a given period of time. The

company calculates this amount in an effort to manage credit practices and payment process

efficiency and utility. It means the company spends more days earning credits than collecting

trade receivables where the ratio is high. The lower amount in this situation includes that the

payment policies or the selection process of the company operate very well (Hausmann,

Kokkinaki and Leng, 2019).

As stated in the above table, Skanska Plc's credit reporting cycle in 2018 and 2019 is 68

days as well as 73 days respectively. This indicating an increase in the billing cycle which is not

a positive sign for the company as the enterprise requires more money in 2019 than those in 2018

to collect the sum of the receivable accounts. This could lead to negative cash flow situation

asset account individual. This ratio is meant not only to measure the liquidity challenges, and

also to decide exactly the uses of working resources. The operating cash flow state will

automatically look favourable if that ratio approaches 2 (Stanley, 2020). A current ratio gives

guarantees to consumers and other interested stakeholders that by using available funds resources

as well as other financial assets, companies which or may not have problems in covering off

short-term fees or existing liabilities. This mix helps executives to learn about the potential

approach on retained earnings and fix current liquidity issues. Negotiations with banking are

more likely to delay such charges in late payments or discussions with distributors.

From the above table reflecting Skanska Plc current proportions, it was estimated that the

firm's existing ratios in 2018 were 2.34, which plummeted to 0.9324, indicating a major decrease

in this proportion. This big decrease in the proportion is an unfavourable sign for the liquidity

position of company Skanska Plc. This change in the existing ratio suggests a dramatic decline in

the organization's ability to meet its short-term payables / liabilities. This item should be given

priority by the company, and that might have a longer impact on Skanska business growth

prospects. While this only suggests the corporation's short-term liquidity position, lack of this

proportion outcome may result in the firm's unfavourable financial situation (Bakhtavar, Yousefi

and Jafarpour, 2019).

Average-receivable days/ Debtors:

Debtors collection period simply corresponds to an estimated average usually of days that

and company needs to recover purchases of its trading credits over a given period of time. The

company calculates this amount in an effort to manage credit practices and payment process

efficiency and utility. It means the company spends more days earning credits than collecting

trade receivables where the ratio is high. The lower amount in this situation includes that the

payment policies or the selection process of the company operate very well (Hausmann,

Kokkinaki and Leng, 2019).

As stated in the above table, Skanska Plc's credit reporting cycle in 2018 and 2019 is 68

days as well as 73 days respectively. This indicating an increase in the billing cycle which is not

a positive sign for the company as the enterprise requires more money in 2019 than those in 2018

to collect the sum of the receivable accounts. This could lead to negative cash flow situation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

within the organization. The growth in that proportion will also have a significant effect on the

business short-term liquidity position.

Creditors-period of collection:

The measure essentially indicates the average time period a business company usually

needs to make contributions to the payable or creditor-party exchange. In general not all cash

transactions are made by a company; the main component of the entity's transaction is on credit

terms. Depending on total average debt sales and market creditors, this measure dictates that the

company normally parses to its trade creditors about total days. A shorter time period contributes

to the greater financial status of the company because it requires less time to pay corporate

creditors. Thus a longer length of an avg-payable period indicates that the company has

insufficient discretionary capital or assets to pay any of its short-term obligations and creditors

for trading. Consequently, longer total payment duration is an indication that the firm will

concentrate on cash flow including cash flow because the short-run equity status of the company

is not really beneficial.

The figures obtained from the above table of Skanska Plc reflect the collecting times of

the creditors: 128-days and 43-days simultaneously during the years 2019 and 2018, suggesting a

large gap in the payment process for creditors. The dramatic rise throughout the timeline shows

that the commercial entity's willingness to allow pay-outs to its investors has declined during the

period. This increase in the timeframe suggests that the firm does not have sufficient or fair sums

to pay shareholders in a quick interval of time indicating a disaffected liquidity state. As in

manufacturing, if a company makes late payments to its vendors, it may as have an effect on the

reputation of the entity that may lead to the loss of large suppliers' assistance (Lee, Hyun and

Jung, 2019).

CONCLUSION

In the end of report, it is founded that financial decision-making within a corporation or

enterprise setting is a significant factor given that it enables the enterprise to be recognized as

successful and the entity to be maintained. To promote more rational decision-making it takes a

wide spectrum of factors and strategies. Executives must consider specific aspects of strategic

decision-making to achieve the company's goals and aims within a given time period. This also

involves ratio calculation and analysis, allowing managers to assess the company's real success

over a given time period and to make decisions based on specific ratio outcomes. In addition,

business short-term liquidity position.

Creditors-period of collection:

The measure essentially indicates the average time period a business company usually

needs to make contributions to the payable or creditor-party exchange. In general not all cash

transactions are made by a company; the main component of the entity's transaction is on credit

terms. Depending on total average debt sales and market creditors, this measure dictates that the

company normally parses to its trade creditors about total days. A shorter time period contributes

to the greater financial status of the company because it requires less time to pay corporate

creditors. Thus a longer length of an avg-payable period indicates that the company has

insufficient discretionary capital or assets to pay any of its short-term obligations and creditors

for trading. Consequently, longer total payment duration is an indication that the firm will

concentrate on cash flow including cash flow because the short-run equity status of the company

is not really beneficial.

The figures obtained from the above table of Skanska Plc reflect the collecting times of

the creditors: 128-days and 43-days simultaneously during the years 2019 and 2018, suggesting a

large gap in the payment process for creditors. The dramatic rise throughout the timeline shows

that the commercial entity's willingness to allow pay-outs to its investors has declined during the

period. This increase in the timeframe suggests that the firm does not have sufficient or fair sums

to pay shareholders in a quick interval of time indicating a disaffected liquidity state. As in

manufacturing, if a company makes late payments to its vendors, it may as have an effect on the

reputation of the entity that may lead to the loss of large suppliers' assistance (Lee, Hyun and

Jung, 2019).

CONCLUSION

In the end of report, it is founded that financial decision-making within a corporation or

enterprise setting is a significant factor given that it enables the enterprise to be recognized as

successful and the entity to be maintained. To promote more rational decision-making it takes a

wide spectrum of factors and strategies. Executives must consider specific aspects of strategic

decision-making to achieve the company's goals and aims within a given time period. This also

involves ratio calculation and analysis, allowing managers to assess the company's real success

over a given time period and to make decisions based on specific ratio outcomes. In addition,

stockholders and other main actors may use enterprise profitability statements or ratio analysis to

better determine the viability of funds raised in the sale of shares or other corporate means.

better determine the viability of funds raised in the sale of shares or other corporate means.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.