Financial Decision Making Report: BM414, Module Assignment

VerifiedAdded on 2022/12/05

|13

|3497

|246

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making, focusing on the application of management accounting techniques within SKANSKA PLC. It begins with an introduction to financial accounting and its role in preparing financial statements and making informed business decisions. Task 1 explores various management accounting techniques, including financial planning, analysis of financial statements, historical cost accounting, budgetary control, decision-making, cash flow statements, and marginal costing, and then provides a critical analysis of their importance. Task 2 delves into ratio analysis, calculating key financial ratios such as Return on Capital Employed (ROCE), net profit margin, current ratio, debtor collection period, and creditor collection period for SKANSKA PLC over two years, providing insights into the company's financial performance. The report concludes with a summary of the findings and emphasizes the importance of financial analysis in assessing and improving the company's performance and making strategic decisions. The report highlights the impact of these techniques and provides recommendations to improve performance and make financial decisions. The report also includes calculations, comparisons, and improvements of these ratios.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK -1...........................................................................................................................................3

Role of management accounting techniques...............................................................................3

Management accounting techniques............................................................................................3

Critical analysis...........................................................................................................................4

CONCLUSION................................................................................................................................5

TASK-2 RATIO ANALYSIS..........................................................................................................7

A) Calculation of ratios...............................................................................................................7

B) Performance of SKANSKA PLC...........................................................................................8

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK -1...........................................................................................................................................3

Role of management accounting techniques...............................................................................3

Management accounting techniques............................................................................................3

Critical analysis...........................................................................................................................4

CONCLUSION................................................................................................................................5

TASK-2 RATIO ANALYSIS..........................................................................................................7

A) Calculation of ratios...............................................................................................................7

B) Performance of SKANSKA PLC...........................................................................................8

REFERENCES..............................................................................................................................13

INTRODUCTION

For every business it is necessary to maintain record of their transaction so that on basis of it

financial statements are prepared. With help of statements financial performance is measured.

Also, effective and relevant decisions are taken by managers to improve financial performance.

Besides, it gives insight about profit and loss of overall organisation. Functions of accounting

include storing and analyzing financial information and make sure that all the monetary

transactions are done appropriately (Madhoun, 2020). Accounting helps in preparing the

financial statements is very important for knowing the company’s financial status. Finance

functions include financial planning, allocating funds, forecasting the cash outflows and inflows.

Finance function is important for the company to make sure that all the profits and losses are

being measured and the company is keeping account for all the transactions being done.

The present report will lay emphasis on importance of accounting function, duties, roles, etc.

within SKANSKA PLC. Also, ratios of two years will be calculated to analyse company

financial performance.

TASK -1

Role of management accounting techniques

Management accounting techniques play a crucial role in making plans for future and it

also helps managers in taking decision regarding financial position of company. There are many

techniques that can be used by SKANSKA PLC to identify all details related to financial

situation of company and it helps managers in identifying, analysing, interpreting and

communicating all information so that necessary decisions can be taken. These management

techniques help in make plans, controlling all activities and taking decisions which are beneficial

for company (Ameen and et.al., 2018).

Management accounting techniques

Financial planning – It is the technique which is used by companies to make plans which will

help in taking decision. It is a process use for estimating capital requirement in an organisation

and also helps in determining competition. It helps managers in identifying current position of

company and it will help them in making financial policies related to investment and

arrangement of funds when required.

Analysis of financial statements – It is management technique which is applied by companies

to analyse financial statements. This will help managers in identifying financial position of

For every business it is necessary to maintain record of their transaction so that on basis of it

financial statements are prepared. With help of statements financial performance is measured.

Also, effective and relevant decisions are taken by managers to improve financial performance.

Besides, it gives insight about profit and loss of overall organisation. Functions of accounting

include storing and analyzing financial information and make sure that all the monetary

transactions are done appropriately (Madhoun, 2020). Accounting helps in preparing the

financial statements is very important for knowing the company’s financial status. Finance

functions include financial planning, allocating funds, forecasting the cash outflows and inflows.

Finance function is important for the company to make sure that all the profits and losses are

being measured and the company is keeping account for all the transactions being done.

The present report will lay emphasis on importance of accounting function, duties, roles, etc.

within SKANSKA PLC. Also, ratios of two years will be calculated to analyse company

financial performance.

TASK -1

Role of management accounting techniques

Management accounting techniques play a crucial role in making plans for future and it

also helps managers in taking decision regarding financial position of company. There are many

techniques that can be used by SKANSKA PLC to identify all details related to financial

situation of company and it helps managers in identifying, analysing, interpreting and

communicating all information so that necessary decisions can be taken. These management

techniques help in make plans, controlling all activities and taking decisions which are beneficial

for company (Ameen and et.al., 2018).

Management accounting techniques

Financial planning – It is the technique which is used by companies to make plans which will

help in taking decision. It is a process use for estimating capital requirement in an organisation

and also helps in determining competition. It helps managers in identifying current position of

company and it will help them in making financial policies related to investment and

arrangement of funds when required.

Analysis of financial statements – It is management technique which is applied by companies

to analyse financial statements. This will help managers in identifying financial position of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SKANSKA PLC and evaluation of financial performance. If company requires fund then they

can make plans after analysing financial statements. It helps in taking decisions and controlling

all activities.

Historical cost accounting – This management technique will help managers in calculating

value which is used in accounting process. In historical cost accounting asset value is recorded at

its original cost in balance sheet (Madhoun, 2020). The price of asset is recorded at cost

purchased by company. Benefit of this technique is that it helps in knowing original value of

assets and liabilities in financial statement.

Budgetary control – It refers to making budgets after analysing previous year data because it

helps in making decisions which is beneficial for managers in taking decision. It helps in

managing income and expenditure. Budgets are made to make an estimate that how much

income will be generated in future and how much expenses a company has to bear.

Decision making – It is the process of identifying a decision, relevant information is collected

and alternative solutions are being find out so that it can be applied by company for future

growth. This helps managers in planning and controlling day to day activities so that

organisation can run smoothly.

Cash flow statement – Cash flow statement is a statement in which information of cash inflow

and outflow is being summarised. It helps managers in taking financial decisions and plans can

be made for future growth. It measures how well an organisation is managing it cash position,

generating revenue to pay its liabilities and expenses that are incurred (Pasch, 2019).

Marginal costing – This management accounting techniques helps in measuring variable cost

and fixed cost. Variable cost refers to cost which changes according to change in output and

fixed cost remains same, it does not change. This technique helps managers in planning,

controlling and correct decisions are taken.

Critical analysis

Management accounting techniques play an important role in taking financial decision

because it helps managers in identifying current position of an organisation and how much

revenue is being generated. It also measures overall performance by calculating expenses which

is incurred and mangers try to reduce expenses and make plans so that more revenue can be

generated. It is important for every company to apply management accounting techniques to

determine financial position of company and necessary steps can be taken to improve

can make plans after analysing financial statements. It helps in taking decisions and controlling

all activities.

Historical cost accounting – This management technique will help managers in calculating

value which is used in accounting process. In historical cost accounting asset value is recorded at

its original cost in balance sheet (Madhoun, 2020). The price of asset is recorded at cost

purchased by company. Benefit of this technique is that it helps in knowing original value of

assets and liabilities in financial statement.

Budgetary control – It refers to making budgets after analysing previous year data because it

helps in making decisions which is beneficial for managers in taking decision. It helps in

managing income and expenditure. Budgets are made to make an estimate that how much

income will be generated in future and how much expenses a company has to bear.

Decision making – It is the process of identifying a decision, relevant information is collected

and alternative solutions are being find out so that it can be applied by company for future

growth. This helps managers in planning and controlling day to day activities so that

organisation can run smoothly.

Cash flow statement – Cash flow statement is a statement in which information of cash inflow

and outflow is being summarised. It helps managers in taking financial decisions and plans can

be made for future growth. It measures how well an organisation is managing it cash position,

generating revenue to pay its liabilities and expenses that are incurred (Pasch, 2019).

Marginal costing – This management accounting techniques helps in measuring variable cost

and fixed cost. Variable cost refers to cost which changes according to change in output and

fixed cost remains same, it does not change. This technique helps managers in planning,

controlling and correct decisions are taken.

Critical analysis

Management accounting techniques play an important role in taking financial decision

because it helps managers in identifying current position of an organisation and how much

revenue is being generated. It also measures overall performance by calculating expenses which

is incurred and mangers try to reduce expenses and make plans so that more revenue can be

generated. It is important for every company to apply management accounting techniques to

determine financial position of company and necessary steps can be taken to improve

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of company. There are management techniques that can be applied by managers of

SKANSKA PLC to identify financial position and make plans for future growth of company.

These techniques such as, financial planning, analysis of financial statements, decision making,

cash flow statement, marginal costing and many other (Bangma and et.al., 2017). All these

management techniques helps managers in determining position of company and they can

identify that whether organisation should make changes or not. It also helps in determining that

how much revenue is being generated and expenses that are incurred.

It is essential to determine revenue generated because it will help managers in distributing

profit and salary. These techniques help managers to make future plans so that they can earn

more revenue and they try to reduce cost of production so that good quality products can be

made and customers will get products at low cost. Management techniques help in determining

current position of company and it also help in identifying financial position of competitors. All

the techniques are different and they have benefits, so managers can apply any technique

according to their business and they can get details which will help them in making plans. It also

helps in controlling day to day activities because when managers will know that what are the

areas in which improvement or changes is required they will make plans according to that

(Eberhardt and et.al., 2019). This will help in building good image in market and profit can also

be increased. Management techniques includes cash flow statement in which all income and

expenses are mentioned. It helps in determining that from where cash is received and what are

the expenses.

Management techniques has some negative impact as sometimes wrong decisions can be

taken by managers due to calculation mistake. Cash flow statement is being prepared by

employees so may be there is some error or they have not taken some items. So, this will affect

decisions taken by managers. Before making any plan managers should verify it properly and

check all the details so that there will be no problem in future. It is important for managers to

take correct decisions because if they will take wrong decisions then it can affect overall

performance of company and organisation has to suffer loss (Kim and et.al., 2017). So,

management accounting techniques has positive as well as negative impact. It helps company in

increasing profit and overall financial performance of company can be improved by taking

necessary steps.

SKANSKA PLC to identify financial position and make plans for future growth of company.

These techniques such as, financial planning, analysis of financial statements, decision making,

cash flow statement, marginal costing and many other (Bangma and et.al., 2017). All these

management techniques helps managers in determining position of company and they can

identify that whether organisation should make changes or not. It also helps in determining that

how much revenue is being generated and expenses that are incurred.

It is essential to determine revenue generated because it will help managers in distributing

profit and salary. These techniques help managers to make future plans so that they can earn

more revenue and they try to reduce cost of production so that good quality products can be

made and customers will get products at low cost. Management techniques help in determining

current position of company and it also help in identifying financial position of competitors. All

the techniques are different and they have benefits, so managers can apply any technique

according to their business and they can get details which will help them in making plans. It also

helps in controlling day to day activities because when managers will know that what are the

areas in which improvement or changes is required they will make plans according to that

(Eberhardt and et.al., 2019). This will help in building good image in market and profit can also

be increased. Management techniques includes cash flow statement in which all income and

expenses are mentioned. It helps in determining that from where cash is received and what are

the expenses.

Management techniques has some negative impact as sometimes wrong decisions can be

taken by managers due to calculation mistake. Cash flow statement is being prepared by

employees so may be there is some error or they have not taken some items. So, this will affect

decisions taken by managers. Before making any plan managers should verify it properly and

check all the details so that there will be no problem in future. It is important for managers to

take correct decisions because if they will take wrong decisions then it can affect overall

performance of company and organisation has to suffer loss (Kim and et.al., 2017). So,

management accounting techniques has positive as well as negative impact. It helps company in

increasing profit and overall financial performance of company can be improved by taking

necessary steps.

CONCLUSION

Thus, it is concluded from the above report that the role of management accounting

techniques and its critical analysis helped in assessing the functions which were of key

importance and through these accounting techniques, it was analysed that how SKANSKA PLC

is functioning by managing its internal and external financial affairs. As the market the company

captured is on international basis, the company is following all the finance rules and regulations

which are being processed through the business. There were various accounting techniques

which were being followed by the company such as financial planning, historical cost

accounting, cash flow statement, marginal costing, decision making, budgetary control and

analysis of financial statements was being described which provided details as to how the

company operates through these systems. Along with this, the background of the company was

elaborated as how the company started its business. Key accounting and finance functions of on

general were discussed. The key practices regarding the management accounting techniques

were described. This overall analysis helped in introducing the company as to what the key sole

purpose and the operations of the company are. Therefore, the overall analysis helped in

knowing the expansion of the company on international grounds.

Thus, it is concluded from the above report that the role of management accounting

techniques and its critical analysis helped in assessing the functions which were of key

importance and through these accounting techniques, it was analysed that how SKANSKA PLC

is functioning by managing its internal and external financial affairs. As the market the company

captured is on international basis, the company is following all the finance rules and regulations

which are being processed through the business. There were various accounting techniques

which were being followed by the company such as financial planning, historical cost

accounting, cash flow statement, marginal costing, decision making, budgetary control and

analysis of financial statements was being described which provided details as to how the

company operates through these systems. Along with this, the background of the company was

elaborated as how the company started its business. Key accounting and finance functions of on

general were discussed. The key practices regarding the management accounting techniques

were described. This overall analysis helped in introducing the company as to what the key sole

purpose and the operations of the company are. Therefore, the overall analysis helped in

knowing the expansion of the company on international grounds.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

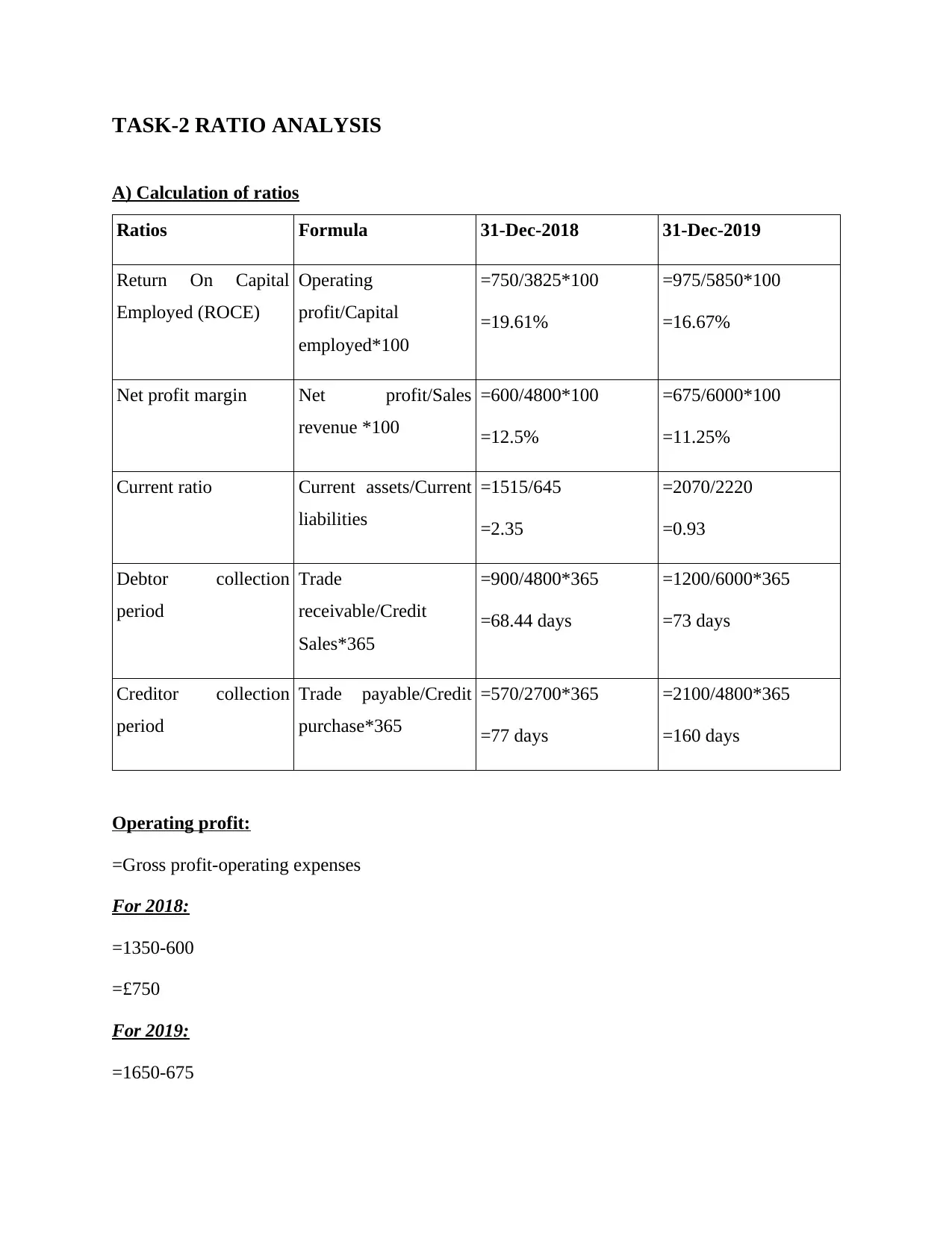

TASK-2 RATIO ANALYSIS

A) Calculation of ratios

Ratios Formula 31-Dec-2018 31-Dec-2019

Return On Capital

Employed (ROCE)

Operating

profit/Capital

employed*100

=750/3825*100

=19.61%

=975/5850*100

=16.67%

Net profit margin Net profit/Sales

revenue *100

=600/4800*100

=12.5%

=675/6000*100

=11.25%

Current ratio Current assets/Current

liabilities

=1515/645

=2.35

=2070/2220

=0.93

Debtor collection

period

Trade

receivable/Credit

Sales*365

=900/4800*365

=68.44 days

=1200/6000*365

=73 days

Creditor collection

period

Trade payable/Credit

purchase*365

=570/2700*365

=77 days

=2100/4800*365

=160 days

Operating profit:

=Gross profit-operating expenses

For 2018:

=1350-600

=£750

For 2019:

=1650-675

A) Calculation of ratios

Ratios Formula 31-Dec-2018 31-Dec-2019

Return On Capital

Employed (ROCE)

Operating

profit/Capital

employed*100

=750/3825*100

=19.61%

=975/5850*100

=16.67%

Net profit margin Net profit/Sales

revenue *100

=600/4800*100

=12.5%

=675/6000*100

=11.25%

Current ratio Current assets/Current

liabilities

=1515/645

=2.35

=2070/2220

=0.93

Debtor collection

period

Trade

receivable/Credit

Sales*365

=900/4800*365

=68.44 days

=1200/6000*365

=73 days

Creditor collection

period

Trade payable/Credit

purchase*365

=570/2700*365

=77 days

=2100/4800*365

=160 days

Operating profit:

=Gross profit-operating expenses

For 2018:

=1350-600

=£750

For 2019:

=1650-675

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=£975

Capital employed:

=Total assets- current liabilities

For 2018:

=4470-645

=3825

For 2019:

=8070-2220

= 5850

B) Performance of SKANSKA PLC

Accounting ratio and their importance:

Accounting ratio:

It refers to the ratio that are concerned with accounting and calculated on the basis of

accounting information. These ratios are concerned and assist the company to measure the

financial performance of the business. Under the accounting ratio analysis the comparison of the

financial data of the company is being performed through which the growth and success is being

measured.

Importance:

Accounting ratios are important both for the company and its stakeholders. This is

because through the calculation of these ratios the company can determine their own financial

performance. Likewise, the investors can also take investment decision regarding the company

(Andjelic and Vesic, 2017). These are also important to be calculated by the business including

the SKANSKA PLC because through these they can measure the profitability as well as

efficiency of their business operations.

Return on capital employed:

It refers to a ratio that is concerned with the calculation of return on the basis of capital

employed. This means that through this ratio it is being calculated that what is the amount of

return that the company has earned from the capital it employed.

Importance:

Capital employed:

=Total assets- current liabilities

For 2018:

=4470-645

=3825

For 2019:

=8070-2220

= 5850

B) Performance of SKANSKA PLC

Accounting ratio and their importance:

Accounting ratio:

It refers to the ratio that are concerned with accounting and calculated on the basis of

accounting information. These ratios are concerned and assist the company to measure the

financial performance of the business. Under the accounting ratio analysis the comparison of the

financial data of the company is being performed through which the growth and success is being

measured.

Importance:

Accounting ratios are important both for the company and its stakeholders. This is

because through the calculation of these ratios the company can determine their own financial

performance. Likewise, the investors can also take investment decision regarding the company

(Andjelic and Vesic, 2017). These are also important to be calculated by the business including

the SKANSKA PLC because through these they can measure the profitability as well as

efficiency of their business operations.

Return on capital employed:

It refers to a ratio that is concerned with the calculation of return on the basis of capital

employed. This means that through this ratio it is being calculated that what is the amount of

return that the company has earned from the capital it employed.

Importance:

This is important ratio because through this the company can determine its efficiency in

terms of its business operation along with using of the capital. Through this ratio the company

can also analyse that whether they are running their business on correct direction or not or

whether the business is generating adequate return or not (Das and Swain, 2018).

Comparison:

While having a comparison of the ROCE of the SKANSKA PLC it is analysed that the

ratio is being declining from 19.61 to 16.67% from 2018 to 2019. This clearly shows that the

performance or the return generation capacity of the company is being declining from the last

year.

Cause:

There could be many causes for this declining ratio including declining the percentage of

sales or the low efficiency of the company with regard to the generation of return. Low

performance of business operation or the employing the capital is also counted as its reason.

Improvement:

This can be improved with the raising or focussing over the percentage of sales. This

means that if the sales will raise then the percentage of the profit will automatically raise.

Likewise, timely disposal of the non-useful assets of the company may also work in the direction

of raising the ROCE percentage.

Net profit margin

This ratio calculate that how much net income or profit is generated as percentage of

revenue. The ratio calculates net profit to revenue of organisation. Here, a good net profit ratio

that is considered is 20% and 10% is considered as average and 5% as low.

Importance

It is important ratio as it shows how much profit or revenue is generated by company.

This means that how much is net income from profit. By that it becomes easy to find out whether

company is profitable in long term growth or not.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 12.5% and in 2019 it was 11.25%. thus, it clearly shows that

net profit ratio is declining. It simple means that company performance is decreasing along with

decline in revenue and profit.

terms of its business operation along with using of the capital. Through this ratio the company

can also analyse that whether they are running their business on correct direction or not or

whether the business is generating adequate return or not (Das and Swain, 2018).

Comparison:

While having a comparison of the ROCE of the SKANSKA PLC it is analysed that the

ratio is being declining from 19.61 to 16.67% from 2018 to 2019. This clearly shows that the

performance or the return generation capacity of the company is being declining from the last

year.

Cause:

There could be many causes for this declining ratio including declining the percentage of

sales or the low efficiency of the company with regard to the generation of return. Low

performance of business operation or the employing the capital is also counted as its reason.

Improvement:

This can be improved with the raising or focussing over the percentage of sales. This

means that if the sales will raise then the percentage of the profit will automatically raise.

Likewise, timely disposal of the non-useful assets of the company may also work in the direction

of raising the ROCE percentage.

Net profit margin

This ratio calculate that how much net income or profit is generated as percentage of

revenue. The ratio calculates net profit to revenue of organisation. Here, a good net profit ratio

that is considered is 20% and 10% is considered as average and 5% as low.

Importance

It is important ratio as it shows how much profit or revenue is generated by company.

This means that how much is net income from profit. By that it becomes easy to find out whether

company is profitable in long term growth or not.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 12.5% and in 2019 it was 11.25%. thus, it clearly shows that

net profit ratio is declining. It simple means that company performance is decreasing along with

decline in revenue and profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cause

There can be several causes or reason for decline in net profit ration. It might be due to

decrease in sales, increase in expenses, etc. besides that, there can be another reason of decrease

in gross profit or revenue of SKANSKA PLC.

Improvement

The ratio can be improved by making some improvement in sales. In this sales

percentage can be increased so that net and gross profit margin or revenue increases. This will

help in rise in net profit ratio. In addition to that, expenses can be decreased as well so that net

profit margin ratio increases.

Current ratio

It is a liquidity ratio which helps in measuring company ability to pay short term debts

within one year. Also, it helps in finding out how business can maximise their current asset on

balance sheet to satisfy creditors.

Importance

This ratio is important because it helps to understand that how rich company is. It enables

in examining short term financial strength of firm. With that it can be evaluated how quickly is

business able to convert inventory into cash.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 2.35% and in 2019 it was 0.93%. thus, it clearly shows that

current ratio is declining. Thus, in 2018 SKANSKA PLC was having 2 times asset than liability

but in 2019 they are having only 1 time asset than liability.

Cause

It can be stated that there are certain reasons for this. it can be due to increase in liability

and decrease in asset. Moreover, it may be due to that SKANSKA PLC has sold some asset and

took more debt in 2019 as compared to 2018. Due to this current ratio has decreased.

Improvement

The ratio can be improved by focusing on asset. Here, SKANSKA PLC can buy more

asset in order to pay debt within one year. Besides that, they can keep more cash in bank and in

land, building, current asset, etc. so that current ratio is improved.

Average receivable days

There can be several causes or reason for decline in net profit ration. It might be due to

decrease in sales, increase in expenses, etc. besides that, there can be another reason of decrease

in gross profit or revenue of SKANSKA PLC.

Improvement

The ratio can be improved by making some improvement in sales. In this sales

percentage can be increased so that net and gross profit margin or revenue increases. This will

help in rise in net profit ratio. In addition to that, expenses can be decreased as well so that net

profit margin ratio increases.

Current ratio

It is a liquidity ratio which helps in measuring company ability to pay short term debts

within one year. Also, it helps in finding out how business can maximise their current asset on

balance sheet to satisfy creditors.

Importance

This ratio is important because it helps to understand that how rich company is. It enables

in examining short term financial strength of firm. With that it can be evaluated how quickly is

business able to convert inventory into cash.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 2.35% and in 2019 it was 0.93%. thus, it clearly shows that

current ratio is declining. Thus, in 2018 SKANSKA PLC was having 2 times asset than liability

but in 2019 they are having only 1 time asset than liability.

Cause

It can be stated that there are certain reasons for this. it can be due to increase in liability

and decrease in asset. Moreover, it may be due to that SKANSKA PLC has sold some asset and

took more debt in 2019 as compared to 2018. Due to this current ratio has decreased.

Improvement

The ratio can be improved by focusing on asset. Here, SKANSKA PLC can buy more

asset in order to pay debt within one year. Besides that, they can keep more cash in bank and in

land, building, current asset, etc. so that current ratio is improved.

Average receivable days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The days helps in finding out how long it takes for company to clear accounts receivable

during a year. This means in how much time payment will be received.

Importance

This is important because it is useful in finding out how quickly business receive their

short term payment within a year. By that it can be evaluated that how financially strong

business is in receiving cash.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 68.4 and in 2019 it was 73. thus, it clearly shows that average

receivable days has increased.

Cause

Here, the cause can be many. It may be due to that business may not be able to focus on

receiving cash from others. Besides, there might be delay in collecting of short term payment.

Improvement

This can be improved by focusing on collection of short term payment. The business can

collect all due payment quickly by taking regular follow up.

Average payable days

It measures the average number of days it takes for a company to pay its suppliers. By

that it shows how much time business make payment.

Importance

The ratio is important because it shows ability of business that how quickly they make

payment to suppliers. So, having less days means firm quickly make payment to supplier and

meet their financial obligation towards suppliers.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 77 and in 2019 it was 160. thus, it clearly shows that average

payable days has increased.

Cause

The cause for this can be that business might not be having enough cash to make payment

to suppliers. It also might be possible that due to low sales and revenue the profits are less due to

during a year. This means in how much time payment will be received.

Importance

This is important because it is useful in finding out how quickly business receive their

short term payment within a year. By that it can be evaluated that how financially strong

business is in receiving cash.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 68.4 and in 2019 it was 73. thus, it clearly shows that average

receivable days has increased.

Cause

Here, the cause can be many. It may be due to that business may not be able to focus on

receiving cash from others. Besides, there might be delay in collecting of short term payment.

Improvement

This can be improved by focusing on collection of short term payment. The business can

collect all due payment quickly by taking regular follow up.

Average payable days

It measures the average number of days it takes for a company to pay its suppliers. By

that it shows how much time business make payment.

Importance

The ratio is important because it shows ability of business that how quickly they make

payment to suppliers. So, having less days means firm quickly make payment to supplier and

meet their financial obligation towards suppliers.

Comparison

By comparing the ratio of two years that is 2018 and 2019 it can be analysed that in 2018

the ratio of SKANSKA PLC was 77 and in 2019 it was 160. thus, it clearly shows that average

payable days has increased.

Cause

The cause for this can be that business might not be having enough cash to make payment

to suppliers. It also might be possible that due to low sales and revenue the profits are less due to

which payment is not made. Along with it, SKANSKA PLC might not have got cash from

debtors due to which they are not able to make payment.

Improvement

It can be improved by reducing the average payable ratio so that payment is made to

supplier. Moreover, they can use cash kept in bank to make payment.

CONCLUSION

Thus, it can be concluded by analysing the performance of SKANSKA PLC it can be said

that financial performance of company is low. They are having low net profit ratio. Also, the

average payable days are 160 so they take a long time to make payment to suppliers. Hence,

investor should not invest in SKANSKA PLC as their financial performance is not good for long

term. Besides that, investing in SKANSKA PLC will be risky as it may result in loss in future.

Even if there is increase in gross profit but the ratios of company are not good. This clearly

shows that financial performance of SKANSKA PLC is average.

debtors due to which they are not able to make payment.

Improvement

It can be improved by reducing the average payable ratio so that payment is made to

supplier. Moreover, they can use cash kept in bank to make payment.

CONCLUSION

Thus, it can be concluded by analysing the performance of SKANSKA PLC it can be said

that financial performance of company is low. They are having low net profit ratio. Also, the

average payable days are 160 so they take a long time to make payment to suppliers. Hence,

investor should not invest in SKANSKA PLC as their financial performance is not good for long

term. Besides that, investing in SKANSKA PLC will be risky as it may result in loss in future.

Even if there is increase in gross profit but the ratios of company are not good. This clearly

shows that financial performance of SKANSKA PLC is average.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.