Financial Decision Making Report: SKANSKA PLC Analysis, BM414

VerifiedAdded on 2022/12/26

|12

|3861

|67

Report

AI Summary

This report provides an in-depth analysis of the financial decision-making processes within an organization, specifically focusing on SKANSKA PLC, a UK-based construction company. The report begins by evaluating the significance of the accounting and finance departments, detailing their key functions such as financial accounting, management accounting, taxation, auditing, investment, financing, dividend, and working capital management. The core of the report involves a comprehensive financial ratio analysis of SKANSKA PLC's financial statements for two years. The calculations include Return on Capital Employed (ROCE), Net Profit Margin, Current Ratio, Debtor's Collection Period, and Creditor's Collection Period. The report then provides a detailed interpretation of these ratios, highlighting trends and offering insights into the company's financial health and performance. The analysis includes recommendations for improvement and strategic financial decisions, with emphasis on ROCE and net profit margins. The report concludes with an overview of the key findings and the implications for SKANSKA PLC's financial strategy and future growth, demonstrating the importance of effective financial management in achieving business objectives.

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

Evaluating the importance of accounting and finance function within an organization........3

TASK 2......................................................................................................................................6

Part a: Calculation of the financial ratios for the two years...................................................6

Part b: Analysis and interpretation of the financial ratios......................................................8

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

Evaluating the importance of accounting and finance function within an organization........3

TASK 2......................................................................................................................................6

Part a: Calculation of the financial ratios for the two years...................................................6

Part b: Analysis and interpretation of the financial ratios......................................................8

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

INTRODUCTION

There are various roles and function played by the accounting and finance

department of an organization which helps in effectively carrying out the financial decision-

making process pertaining to the business. In this report, SKANSKA PLC is taken as an

organization which is a construction company located in UK. It was established in the year

1984 and is having locations in most of European countries which can be considered as its

key strength. The company is looking to expand its business in the other nations as well in the

coming 10 years. This report provides an understanding about the relevance of accounting

and finance functions with respect to the organization. In addition, it carries out ratio analysis

of the financial statements of the company.

TASK 1

Evaluating the importance of accounting and finance function within an organization

1. Accounting department: Financial accounting

The accounting department’s major role is to keeping track of the financial

transactions of the business. It is mainly focused on recording the monetary business

events in the books of accounting which is further utilized by the organization in

respect to decision making. In case of SKANSKA PLC, accounts team works on

creation of different types of financial reports which is useful to the top management

in terms of communicating and stating about the financial health of the company to its

stakeholders (Farhi and Gourio, 2018). On account of this role played by the

account’s division, the users of the financial reports of the company can easily take

decision in respect to whether to make an investment into the company or not. In

addition to this, it can be used in carrying out the comparative analysis with the firms

within the same industry which helps in gaining better insight over the business

performance. On the other hand, it is essential to note that the company requires

employing highly experienced and proficient employees having relevant knowledge

in the field of financial accounting. Management accounting (MA)

The MA is also a branch of accounting in which the management takes the

accounting information from the accounts department and then conducts deep analysis

of the same in order to gain a meaningful information. This information collected is

shared with the internal managerial team who based upon this takes the decision

There are various roles and function played by the accounting and finance

department of an organization which helps in effectively carrying out the financial decision-

making process pertaining to the business. In this report, SKANSKA PLC is taken as an

organization which is a construction company located in UK. It was established in the year

1984 and is having locations in most of European countries which can be considered as its

key strength. The company is looking to expand its business in the other nations as well in the

coming 10 years. This report provides an understanding about the relevance of accounting

and finance functions with respect to the organization. In addition, it carries out ratio analysis

of the financial statements of the company.

TASK 1

Evaluating the importance of accounting and finance function within an organization

1. Accounting department: Financial accounting

The accounting department’s major role is to keeping track of the financial

transactions of the business. It is mainly focused on recording the monetary business

events in the books of accounting which is further utilized by the organization in

respect to decision making. In case of SKANSKA PLC, accounts team works on

creation of different types of financial reports which is useful to the top management

in terms of communicating and stating about the financial health of the company to its

stakeholders (Farhi and Gourio, 2018). On account of this role played by the

account’s division, the users of the financial reports of the company can easily take

decision in respect to whether to make an investment into the company or not. In

addition to this, it can be used in carrying out the comparative analysis with the firms

within the same industry which helps in gaining better insight over the business

performance. On the other hand, it is essential to note that the company requires

employing highly experienced and proficient employees having relevant knowledge

in the field of financial accounting. Management accounting (MA)

The MA is also a branch of accounting in which the management takes the

accounting information from the accounts department and then conducts deep analysis

of the same in order to gain a meaningful information. This information collected is

shared with the internal managerial team who based upon this takes the decision

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which will advantageous to the company. It is mainly useful in the planning process

and the formulation of the business strategies. It involves creation of estimated

budgets along with other useful reports which provides assistance in the planning and

execution of the business activities. SKANSKA PLC by effectively making use of the

MA techniques and reports, can undertake meaningful business-related decision

which will be beneficial for it in long run (Cockcroft and Russell, 2018). This

function is more useful while expanding the business or launching new product in the

market. It will provide assistance in various stages of panning till the time it is

properly executed. It provides complete breakdown of the production capacities.

Therefore, this function of accounts team is important pertaining to decision making.

In contrast to it, in order to make it accurate, the company requires skilled

professionals having relevant qualification and work experience. Tax function

The taxation function of the organization helps in making sure that the

company is effective in complying the legal and statutory requirements. The core role

of this department is to properly determining, analyzing and meeting with the legal

aspects of the business, for instance, filling the tax return on time, conducting

accounting practices with honesty, consulting, appropriately determining the income

tax obligation and so forth (Accounting department responsibilities. 2020). In respect

to the organization like SKANSKA PLC, this function will involve tax filling along

with meeting with the other legal requirement of the business. This helps in ensuring

that the entity is operating as per the set standard. On the other side of this, for the

purpose of proper tax functioning, the employees of the company should be having in-

depth knowledge about the taxation as it is a difficult task which everyone cannot do.

Auditing function

Under this function of accounting, the company can identify the areas where

there is any error or mistake which will help in preparation of the reports in a true and

fair view. This function assist in determining those areas or weaknesses of the

business which requires additional time, money and efforts for the purpose of

improvement (Osadchy and et.al., 2018). Through this, the management can get to

know the categories or parts which is a complete waste for the company as it is not

generating any revenue for the busines so that funds can be shifted to the profitable

areas. It also helps in identifying the frauds or misappropriation of the resources of the

entity by the employees. For example, SKANSKA PLC an internal audit will involve

and the formulation of the business strategies. It involves creation of estimated

budgets along with other useful reports which provides assistance in the planning and

execution of the business activities. SKANSKA PLC by effectively making use of the

MA techniques and reports, can undertake meaningful business-related decision

which will be beneficial for it in long run (Cockcroft and Russell, 2018). This

function is more useful while expanding the business or launching new product in the

market. It will provide assistance in various stages of panning till the time it is

properly executed. It provides complete breakdown of the production capacities.

Therefore, this function of accounts team is important pertaining to decision making.

In contrast to it, in order to make it accurate, the company requires skilled

professionals having relevant qualification and work experience. Tax function

The taxation function of the organization helps in making sure that the

company is effective in complying the legal and statutory requirements. The core role

of this department is to properly determining, analyzing and meeting with the legal

aspects of the business, for instance, filling the tax return on time, conducting

accounting practices with honesty, consulting, appropriately determining the income

tax obligation and so forth (Accounting department responsibilities. 2020). In respect

to the organization like SKANSKA PLC, this function will involve tax filling along

with meeting with the other legal requirement of the business. This helps in ensuring

that the entity is operating as per the set standard. On the other side of this, for the

purpose of proper tax functioning, the employees of the company should be having in-

depth knowledge about the taxation as it is a difficult task which everyone cannot do.

Auditing function

Under this function of accounting, the company can identify the areas where

there is any error or mistake which will help in preparation of the reports in a true and

fair view. This function assist in determining those areas or weaknesses of the

business which requires additional time, money and efforts for the purpose of

improvement (Osadchy and et.al., 2018). Through this, the management can get to

know the categories or parts which is a complete waste for the company as it is not

generating any revenue for the busines so that funds can be shifted to the profitable

areas. It also helps in identifying the frauds or misappropriation of the resources of the

entity by the employees. For example, SKANSKA PLC an internal audit will involve

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

different tasks apart from the fraud identification. In addition to this, it will also

review and measure the credit lines which is being provided to the clients in order to

decrease the chances of losses which is mainly done through internal audits. On the

other side, it is fundamental for the association to guarantee that the business entity is

having exceptionally qualified staff who is eligible for directing the audit by the

highly experienced, professional and experts. Along these lines, this role of accounts

department is vital for an association for checking and improving the association's

operations.

2. Finance department: Investment function

This function is considered to be the most important function of the finance division

in an organization as it works on effective allocation of the financial resources of the

business. It is in simple terms also called as capital budgeting decision, in which the

decisions are undertaken pertaining to where to invest the funds. It involves proper

evaluation of the available investment proposals with the help of various investment

appraisal techniques and that option is selected which will give higher profits in the

future (Bakhodirovna, 2019). For example, investment function will assist

SKANSKA PLC in taking decision about the allocation of capital to the various

sources in order to generate better return in the future. It likewise includes the choice

in association with the depreciable assets which isn't enhancing the business and can

be utilized for using those assets to get other advantageous resources. But this requires

the personnel having greater knowledge and understanding about the investment. Financing function

The role of finance department is mainly in concerned with the financial management

of the company. It is involved into the control and planning of the organizational

financial resources. From the perspective of the business, finance function works on

ensuring that the company is acquiring the right sources of funds and utilizing the

funds which is essential for the efficient business operation (Gartenstein, 2019).

Finance is considered as the lifeblood of the business and ineffective and

inappropriate management of it will result into business failure. For instance,

SKANSKA PLC having a highly talented and skilled finance team who are having

deep understanding about the finance and its various prospects. The main aim of the

financing function is that to make sure that the investors of the company get better

review and measure the credit lines which is being provided to the clients in order to

decrease the chances of losses which is mainly done through internal audits. On the

other side, it is fundamental for the association to guarantee that the business entity is

having exceptionally qualified staff who is eligible for directing the audit by the

highly experienced, professional and experts. Along these lines, this role of accounts

department is vital for an association for checking and improving the association's

operations.

2. Finance department: Investment function

This function is considered to be the most important function of the finance division

in an organization as it works on effective allocation of the financial resources of the

business. It is in simple terms also called as capital budgeting decision, in which the

decisions are undertaken pertaining to where to invest the funds. It involves proper

evaluation of the available investment proposals with the help of various investment

appraisal techniques and that option is selected which will give higher profits in the

future (Bakhodirovna, 2019). For example, investment function will assist

SKANSKA PLC in taking decision about the allocation of capital to the various

sources in order to generate better return in the future. It likewise includes the choice

in association with the depreciable assets which isn't enhancing the business and can

be utilized for using those assets to get other advantageous resources. But this requires

the personnel having greater knowledge and understanding about the investment. Financing function

The role of finance department is mainly in concerned with the financial management

of the company. It is involved into the control and planning of the organizational

financial resources. From the perspective of the business, finance function works on

ensuring that the company is acquiring the right sources of funds and utilizing the

funds which is essential for the efficient business operation (Gartenstein, 2019).

Finance is considered as the lifeblood of the business and ineffective and

inappropriate management of it will result into business failure. For instance,

SKANSKA PLC having a highly talented and skilled finance team who are having

deep understanding about the finance and its various prospects. The main aim of the

financing function is that to make sure that the investors of the company get better

and timely return along with reducing the chances of risk. On the other side, it is

important to understand that there are different sources of financial instruments each

having pros and cons which is essential to be taken account for in order to avoid the

situation of risk and this is the most difficult task. Dividend function

The dividend function involves the decision pertaining to the decision which

incorporates the level of income delivered to investors in terms of dividend, it states

about the determining the stability of the absolute dividend in respect to the trend and

the repurchase of stock. The dividend payout ratio of the company decides the which

has been retained into the business and should be assessed in the light of the goal of

expanding investor wealth (Hope and Vyas, 2017). Procuring higher earnings and a

positive return is the main aim and objective of every business organizations.

However, the major role and function of the finance manager is to determine the

amount which is to be distributed as dividend while retaining the remaining the profits

into the business. In addition to this, SKANSKA PLC is needed to comply with the

various legal and contractual responsibility and criteria in order to avail the funds

from the desired sources. Therefore, the dividend distribution policy should not be

formulated such that it affects the terms and conditions pertaining to procurement of

finances.

Working capital (WC) function

The WC function of finance division makes sure that the company is having

enough funds for meeting with its daily and short-term requirement of the business

(Baker and et.al., 2017). In respect to SKANSKA PLC, finance team has made sure

that there is sufficient amount of funds which is being available with the company for

the purpose of carrying its daily business activities. In contrast to this, SKANSKA

PLC has to regularly monitor its working capital in order to make sure is maintaining

the minimum amount so that timely remedial measures can be taken to overcome the

problem of insufficient working capital.

TASK 2

Part a: Calculation of the financial ratios for the two years

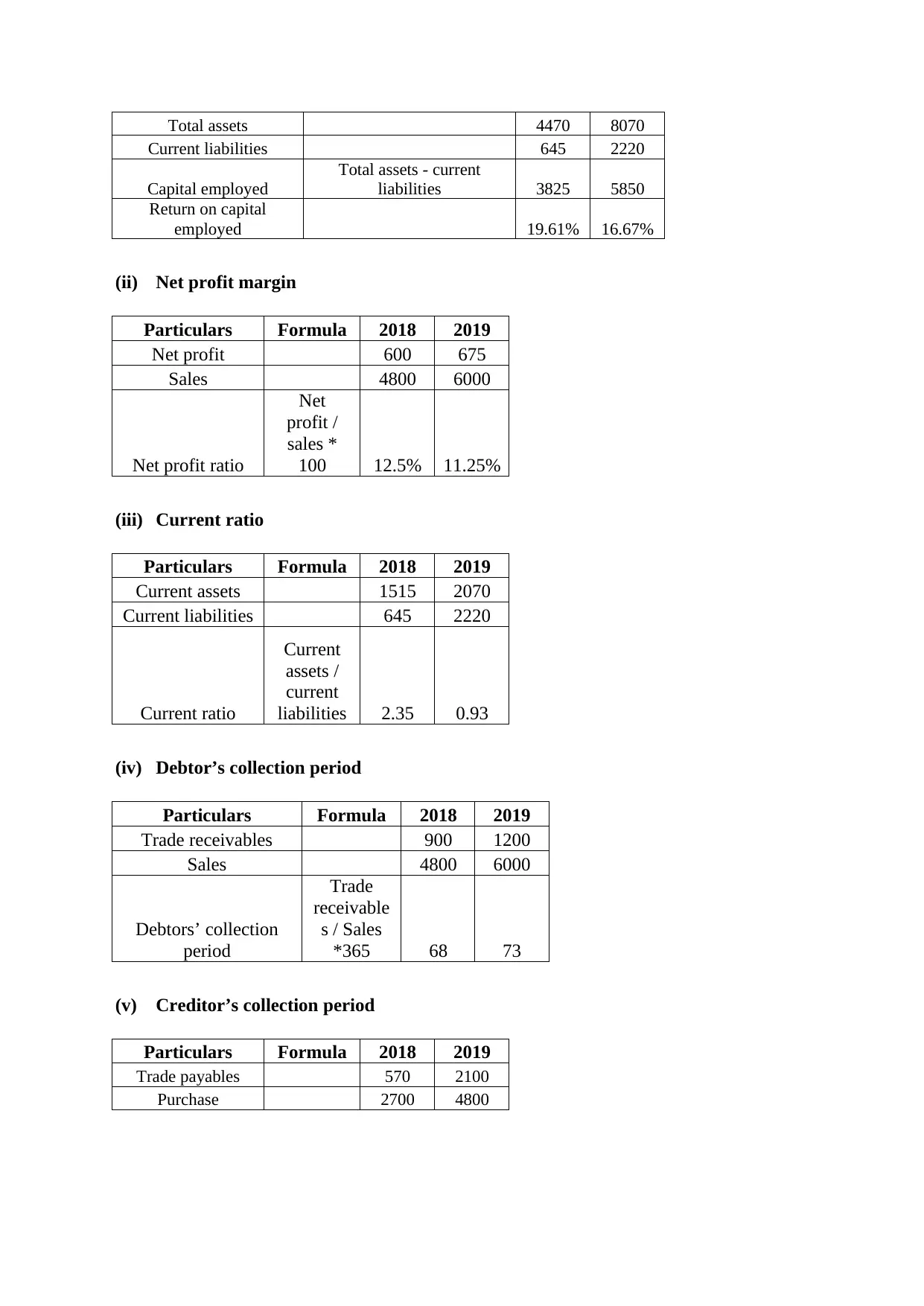

(i) Return on capital employed

Particulars Formula 2018 2019

EBIT 750 975

important to understand that there are different sources of financial instruments each

having pros and cons which is essential to be taken account for in order to avoid the

situation of risk and this is the most difficult task. Dividend function

The dividend function involves the decision pertaining to the decision which

incorporates the level of income delivered to investors in terms of dividend, it states

about the determining the stability of the absolute dividend in respect to the trend and

the repurchase of stock. The dividend payout ratio of the company decides the which

has been retained into the business and should be assessed in the light of the goal of

expanding investor wealth (Hope and Vyas, 2017). Procuring higher earnings and a

positive return is the main aim and objective of every business organizations.

However, the major role and function of the finance manager is to determine the

amount which is to be distributed as dividend while retaining the remaining the profits

into the business. In addition to this, SKANSKA PLC is needed to comply with the

various legal and contractual responsibility and criteria in order to avail the funds

from the desired sources. Therefore, the dividend distribution policy should not be

formulated such that it affects the terms and conditions pertaining to procurement of

finances.

Working capital (WC) function

The WC function of finance division makes sure that the company is having

enough funds for meeting with its daily and short-term requirement of the business

(Baker and et.al., 2017). In respect to SKANSKA PLC, finance team has made sure

that there is sufficient amount of funds which is being available with the company for

the purpose of carrying its daily business activities. In contrast to this, SKANSKA

PLC has to regularly monitor its working capital in order to make sure is maintaining

the minimum amount so that timely remedial measures can be taken to overcome the

problem of insufficient working capital.

TASK 2

Part a: Calculation of the financial ratios for the two years

(i) Return on capital employed

Particulars Formula 2018 2019

EBIT 750 975

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total assets 4470 8070

Current liabilities 645 2220

Capital employed

Total assets - current

liabilities 3825 5850

Return on capital

employed 19.61% 16.67%

(ii) Net profit margin

Particulars Formula 2018 2019

Net profit 600 675

Sales 4800 6000

Net profit ratio

Net

profit /

sales *

100 12.5% 11.25%

(iii) Current ratio

Particulars Formula 2018 2019

Current assets 1515 2070

Current liabilities 645 2220

Current ratio

Current

assets /

current

liabilities 2.35 0.93

(iv) Debtor’s collection period

Particulars Formula 2018 2019

Trade receivables 900 1200

Sales 4800 6000

Debtors’ collection

period

Trade

receivable

s / Sales

*365 68 73

(v) Creditor’s collection period

Particulars Formula 2018 2019

Trade payables 570 2100

Purchase 2700 4800

Current liabilities 645 2220

Capital employed

Total assets - current

liabilities 3825 5850

Return on capital

employed 19.61% 16.67%

(ii) Net profit margin

Particulars Formula 2018 2019

Net profit 600 675

Sales 4800 6000

Net profit ratio

Net

profit /

sales *

100 12.5% 11.25%

(iii) Current ratio

Particulars Formula 2018 2019

Current assets 1515 2070

Current liabilities 645 2220

Current ratio

Current

assets /

current

liabilities 2.35 0.93

(iv) Debtor’s collection period

Particulars Formula 2018 2019

Trade receivables 900 1200

Sales 4800 6000

Debtors’ collection

period

Trade

receivable

s / Sales

*365 68 73

(v) Creditor’s collection period

Particulars Formula 2018 2019

Trade payables 570 2100

Purchase 2700 4800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Creditor’s

collection period

Trade

payables /

purchase

*365 77 160

Part b: Analysis and interpretation of the financial ratios

(i) Return on capital employed (ROCE)

The ROCE ratio is used for determining the ability of the company in generating

greater profits from the capital employed into the business. This is the most important

financial metrics which is being used by the investors and creditor in order to determine

whether the company is right for making an investment. High ratio is considered to be

favorable for the company. In respect to the SKANSKA PLC, there is a decrease in the

ROCE from 20% to the 17% in the year 2019 which is point of concern (Adjirackor and

et.al., 2017). The cause behind this decline can be increase in the amount employed by the

organization with little or no change in the operational profits of the company. In simple

terms the change in the ratio is not adequate or equivalent which ahs consequently lead to

decline in ROCE. Therefore, it is suggested to the SKANSKA PLC to implement corrective

steps which will assist in increasing the effectiveness of the entity in effectively making

utilization of its capital employed. This will lead to attaining greater profits and leading

increase in ROCE.

(ii) Net profit (NP) margin

Under this, the proportion of net profit of the company in respect to the net sales of

the business is determined. This ratio is useful in evaluating the capability of the company in

earning higher profits by its revenue from the operational activities. This is a very good

indicator of the financial health of the entity and is mostly mad use by the investors and

creditors which helps in determining the ability of the firm in converting its sales into profits

(Rawan, 2019). Pertaining to the case of SKANSKA PLC, there is a drop in the NP margin as

in the previous year it was 13% while in the year 2019, it was 11% and this decrease in

percentage indicates that there is company is not able to properly manage its business

expenses which ahs resulted into reduction in profits. In order to improve this situation, the

company is required to implement relevant strategies like reducing the price of its product or

services or by the way of implementing better marketing and promotional practices for

grabbing the attention of the clients. In addition to this, the company can work on identifying

the areas where the major cost is incurred so that actions can be taken to reduce it.

collection period

Trade

payables /

purchase

*365 77 160

Part b: Analysis and interpretation of the financial ratios

(i) Return on capital employed (ROCE)

The ROCE ratio is used for determining the ability of the company in generating

greater profits from the capital employed into the business. This is the most important

financial metrics which is being used by the investors and creditor in order to determine

whether the company is right for making an investment. High ratio is considered to be

favorable for the company. In respect to the SKANSKA PLC, there is a decrease in the

ROCE from 20% to the 17% in the year 2019 which is point of concern (Adjirackor and

et.al., 2017). The cause behind this decline can be increase in the amount employed by the

organization with little or no change in the operational profits of the company. In simple

terms the change in the ratio is not adequate or equivalent which ahs consequently lead to

decline in ROCE. Therefore, it is suggested to the SKANSKA PLC to implement corrective

steps which will assist in increasing the effectiveness of the entity in effectively making

utilization of its capital employed. This will lead to attaining greater profits and leading

increase in ROCE.

(ii) Net profit (NP) margin

Under this, the proportion of net profit of the company in respect to the net sales of

the business is determined. This ratio is useful in evaluating the capability of the company in

earning higher profits by its revenue from the operational activities. This is a very good

indicator of the financial health of the entity and is mostly mad use by the investors and

creditors which helps in determining the ability of the firm in converting its sales into profits

(Rawan, 2019). Pertaining to the case of SKANSKA PLC, there is a drop in the NP margin as

in the previous year it was 13% while in the year 2019, it was 11% and this decrease in

percentage indicates that there is company is not able to properly manage its business

expenses which ahs resulted into reduction in profits. In order to improve this situation, the

company is required to implement relevant strategies like reducing the price of its product or

services or by the way of implementing better marketing and promotional practices for

grabbing the attention of the clients. In addition to this, the company can work on identifying

the areas where the major cost is incurred so that actions can be taken to reduce it.

(iii) Current ratio

This ratio measures the ability of the company pertaining to effectively meeting with

its short-term obligations through the help of its existing current assets. Along with liquidity,

this ratio also provides for the efficiency ratio and this ratio indicates that the firm is limited

amount of time in order to raise the funds for the for meeting with the requirement of the

sudden liabilities. This ratio provides assistance to the management and investors for the

purpose of gaining knowledge and understanding about et liquidity position of the entity

(Ahmed Abdul-Aziz and et.al., 2019). It is desirable to have greater proportion as it is more

ideal for the business which validates that the association is having adequate amount for

settling its present charges. Likewise, note that a lot higher proportion is additionally not

satisfactory as it implies that the business is having overabundance money which isn't

increasing the value of the entity. In respect to the SKANSKA PLC, the current proportion is

0.93 in 2019 when contrasted with 2.35 in 2018. In the wake of assessing this proportion, it

very well may be said that SKANSKA PLC is required to undertake the restorative remedial

actions which can be either to expand its present resources or for diminishing its present

accountabilities to meet with the desired proportion (Zinkevičienė, Stončiuvienė and

Juočiūnienė, 2018). The lower ratio conveys that the association isn't having adequate

amount of money to take care of its present obligation and is needed to work adequately to

keep away from the circumstance of money crunch. Likewise, SKANSKA PLC needs to

guarantee that its present proportion doesn't reach the more higher value, that is, above 2.35

which implies that organization is having a very sizable amount of money which has stayed

inactive adding no worth to the business.

(iv) Debtor’s collection period (DCP)

The DCP is the ratio which is determines the amount of it will take to recover the

due amount from the customers to whom the company ahs sold its products or provided

services on credit. It is highly desirable to have shorter duration as the longer duration

indicates that the business organization is not having the capability to recover the due amount

from its clients within the given time frame (Sergeev and Chaplinska, 2017). In addition to

this, it also conveys that there is a greater chance of the company to face higher bad and

doubtful debts. In respect to ratios of SKANSKA PLC, in the year 2018, the DCP was 68

days which increased to 73 days in 2019, therefore, there is an increase in days which is

concerning situation for the entity. There can be various reasons for this increase like

improper formulation of credit terms of the company which has led to providing credit to the

customers for the longer term. In addition to this, there can be the reason like the economic

This ratio measures the ability of the company pertaining to effectively meeting with

its short-term obligations through the help of its existing current assets. Along with liquidity,

this ratio also provides for the efficiency ratio and this ratio indicates that the firm is limited

amount of time in order to raise the funds for the for meeting with the requirement of the

sudden liabilities. This ratio provides assistance to the management and investors for the

purpose of gaining knowledge and understanding about et liquidity position of the entity

(Ahmed Abdul-Aziz and et.al., 2019). It is desirable to have greater proportion as it is more

ideal for the business which validates that the association is having adequate amount for

settling its present charges. Likewise, note that a lot higher proportion is additionally not

satisfactory as it implies that the business is having overabundance money which isn't

increasing the value of the entity. In respect to the SKANSKA PLC, the current proportion is

0.93 in 2019 when contrasted with 2.35 in 2018. In the wake of assessing this proportion, it

very well may be said that SKANSKA PLC is required to undertake the restorative remedial

actions which can be either to expand its present resources or for diminishing its present

accountabilities to meet with the desired proportion (Zinkevičienė, Stončiuvienė and

Juočiūnienė, 2018). The lower ratio conveys that the association isn't having adequate

amount of money to take care of its present obligation and is needed to work adequately to

keep away from the circumstance of money crunch. Likewise, SKANSKA PLC needs to

guarantee that its present proportion doesn't reach the more higher value, that is, above 2.35

which implies that organization is having a very sizable amount of money which has stayed

inactive adding no worth to the business.

(iv) Debtor’s collection period (DCP)

The DCP is the ratio which is determines the amount of it will take to recover the

due amount from the customers to whom the company ahs sold its products or provided

services on credit. It is highly desirable to have shorter duration as the longer duration

indicates that the business organization is not having the capability to recover the due amount

from its clients within the given time frame (Sergeev and Chaplinska, 2017). In addition to

this, it also conveys that there is a greater chance of the company to face higher bad and

doubtful debts. In respect to ratios of SKANSKA PLC, in the year 2018, the DCP was 68

days which increased to 73 days in 2019, therefore, there is an increase in days which is

concerning situation for the entity. There can be various reasons for this increase like

improper formulation of credit terms of the company which has led to providing credit to the

customers for the longer term. In addition to this, there can be the reason like the economic

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

slowdown or recession which has resulted into influencing the cash inflow of the entity in

order to overcome this risky situation, the company can make modification in its sales credit

terms and condition and along with this, the company should focus on providing training to

its collection team so that can be hard and effective in recovering the due amount.

(v) Creditor’s collection period (CCP)

The CCP ratio is the opposite of DCP as in this the business entity is required to

make payment to its creditors from whom it has purchased goods on credit. In comparison to

DCP, it is favorable to have higher CCP ratio but it is also restricted to a certain limit.

Organizations generally really like to have high payable days so it can utilize the accessible

money for other various usage like putting it in profitable venture and furthermore expanding

its working capital (Pret and Carter, 2017). As beyond this limit, it might look like the

company is facing problem pertaining to making timely payment of its due amount. Along

with this, it might indicate to its creditors and vendors that the company is intentionally not

willing to pay and this affects the reputation and image of the organization. In regard to

SKANSKA PLC there is a huge rise in the CCP from 77 days to 170 days in the year 2019

and it can be considered as beneficial for the organization as now SKANSKA PLC can retain

its cash for a longer term and even can make an investment for short duration over which it

can earn return as well (Jia and et.al., 2020). But in contrast to it, it is important to understand

that the much higher ratio is also not good for the company because of the reason stated

above. Therefore, it is important for SKANSKA PLC to implement strategic actions and plan

in place for repaying the money to its creditors on time otherwise, it might upset or

disappoint the creditors or vendors.

From the above, it can be inferred that the financial health of SKANSKA PLC is not

good and attractive and thus, it is recommended to not invest funds in the entity.

CONCLUSION

It can be summarized from the above that the current financial position and health of

the company SKANSKA PLC is not sound and therefore, it is recommended to Camden

Limited to not invest into the company as its ROCE along with the current ratio and debtor

receivable period is not good enough which result into making the company risky. Apart

from this, it is important to note that the company facing challenge in overcoming its liquidity

crisis and needs immediate action for exercising control over the situation. In order to do this,

the ole of accounts and finance department is crucial.

order to overcome this risky situation, the company can make modification in its sales credit

terms and condition and along with this, the company should focus on providing training to

its collection team so that can be hard and effective in recovering the due amount.

(v) Creditor’s collection period (CCP)

The CCP ratio is the opposite of DCP as in this the business entity is required to

make payment to its creditors from whom it has purchased goods on credit. In comparison to

DCP, it is favorable to have higher CCP ratio but it is also restricted to a certain limit.

Organizations generally really like to have high payable days so it can utilize the accessible

money for other various usage like putting it in profitable venture and furthermore expanding

its working capital (Pret and Carter, 2017). As beyond this limit, it might look like the

company is facing problem pertaining to making timely payment of its due amount. Along

with this, it might indicate to its creditors and vendors that the company is intentionally not

willing to pay and this affects the reputation and image of the organization. In regard to

SKANSKA PLC there is a huge rise in the CCP from 77 days to 170 days in the year 2019

and it can be considered as beneficial for the organization as now SKANSKA PLC can retain

its cash for a longer term and even can make an investment for short duration over which it

can earn return as well (Jia and et.al., 2020). But in contrast to it, it is important to understand

that the much higher ratio is also not good for the company because of the reason stated

above. Therefore, it is important for SKANSKA PLC to implement strategic actions and plan

in place for repaying the money to its creditors on time otherwise, it might upset or

disappoint the creditors or vendors.

From the above, it can be inferred that the financial health of SKANSKA PLC is not

good and attractive and thus, it is recommended to not invest funds in the entity.

CONCLUSION

It can be summarized from the above that the current financial position and health of

the company SKANSKA PLC is not sound and therefore, it is recommended to Camden

Limited to not invest into the company as its ROCE along with the current ratio and debtor

receivable period is not good enough which result into making the company risky. Apart

from this, it is important to note that the company facing challenge in overcoming its liquidity

crisis and needs immediate action for exercising control over the situation. In order to do this,

the ole of accounts and finance department is crucial.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Adjirackor, T. and et.al., 2017. Financial Ratios as a Tool for Profitability in Aryton

Drugs. Research Journal of Finance and Accounting. 8(1). pp.1-10.

Ahmed Abdul-Aziz, S. and et.al., 2019. Financial Ratios as Predictors of Failure.

Baker, H. K. and et.al., 2017. Working capital management practices in India: survey

evidence. Managerial Finance.

Bakhodirovna, A. N., 2019. Ways of efficient cost management by acounting

policy. International Journal of Research in Social Sciences. 9(2). pp.700-710.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance

practice and research. Australian Accounting Review. 28(3). pp.323-333.

Farhi, E. and Gourio, F., 2018. Accounting for macro-finance trends: Market power,

intangibles, and risk premia (No. w25282). National Bureau of Economic Research.

Hope, O. K. and Vyas, D., 2017. Private company finance and financial

reporting. Accounting and Business Research. 47(5). pp.506-537.

Jia, F. and et.al., 2020. Towards an integrated conceptual framework of supply chain finance:

An information processing perspective. International Journal of Production

Economics. 219. pp.18-30.

Osadchy, E. A. and et.al., 2018. Financial statements of a company as an information base

for decision-making in a transforming economy.

Pret, T. and Carter, S., 2017. The importance of ‘fitting in’: collaboration and social value

creation in response to community norms and expectations. Entrepreneurship &

Regional Development. 29(7-8). pp.639-667.

Rawan, A., 2019. Evaluating Banks Financial Performance Using Financial Ratios: A Case

Study Of Kuwait Local Commercial Banks. Oradea Journal of Business and

Economics. 4(2). pp.56-68.

Sergeev, E. and Chaplinska, A., 2017. METHODOLOGY FOR DETERMINING THE

NORMS OF FINANCIAL RATIOS. Reģionālais Ziņojums. Pētījumu Materiāli. (13).

pp.5-86.

Zinkevičienė, D., Stončiuvienė, N. and Juočiūnienė, D., 2018. Relation between animal

depreciation and financial ratios. Apskaita ir finansai: mokslo, verslo ir viešojo

sektoriaus partnerystė: 11-osios tarptautinės mokslinės konferencijos programa ir

santraukos, 2018 m. lapkričio 29-30 d./Aleksandro Stulginskio universitetas.

Akademija, 2018.

Online

Accounting department responsibilities. 2020. [Online]. Available Through:<

https://www.accountingtools.com/articles/accounting-department-

responsibilities.html>.

Gartenstein, D., 2019. What Roles Does the Finance Department Play in a Business?

[Online]. Available Through:< https://bizfluent.com/facts-5683333-role-finance-

department-play-business-.html>.

Books and Journals

Adjirackor, T. and et.al., 2017. Financial Ratios as a Tool for Profitability in Aryton

Drugs. Research Journal of Finance and Accounting. 8(1). pp.1-10.

Ahmed Abdul-Aziz, S. and et.al., 2019. Financial Ratios as Predictors of Failure.

Baker, H. K. and et.al., 2017. Working capital management practices in India: survey

evidence. Managerial Finance.

Bakhodirovna, A. N., 2019. Ways of efficient cost management by acounting

policy. International Journal of Research in Social Sciences. 9(2). pp.700-710.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance

practice and research. Australian Accounting Review. 28(3). pp.323-333.

Farhi, E. and Gourio, F., 2018. Accounting for macro-finance trends: Market power,

intangibles, and risk premia (No. w25282). National Bureau of Economic Research.

Hope, O. K. and Vyas, D., 2017. Private company finance and financial

reporting. Accounting and Business Research. 47(5). pp.506-537.

Jia, F. and et.al., 2020. Towards an integrated conceptual framework of supply chain finance:

An information processing perspective. International Journal of Production

Economics. 219. pp.18-30.

Osadchy, E. A. and et.al., 2018. Financial statements of a company as an information base

for decision-making in a transforming economy.

Pret, T. and Carter, S., 2017. The importance of ‘fitting in’: collaboration and social value

creation in response to community norms and expectations. Entrepreneurship &

Regional Development. 29(7-8). pp.639-667.

Rawan, A., 2019. Evaluating Banks Financial Performance Using Financial Ratios: A Case

Study Of Kuwait Local Commercial Banks. Oradea Journal of Business and

Economics. 4(2). pp.56-68.

Sergeev, E. and Chaplinska, A., 2017. METHODOLOGY FOR DETERMINING THE

NORMS OF FINANCIAL RATIOS. Reģionālais Ziņojums. Pētījumu Materiāli. (13).

pp.5-86.

Zinkevičienė, D., Stončiuvienė, N. and Juočiūnienė, D., 2018. Relation between animal

depreciation and financial ratios. Apskaita ir finansai: mokslo, verslo ir viešojo

sektoriaus partnerystė: 11-osios tarptautinės mokslinės konferencijos programa ir

santraukos, 2018 m. lapkričio 29-30 d./Aleksandro Stulginskio universitetas.

Akademija, 2018.

Online

Accounting department responsibilities. 2020. [Online]. Available Through:<

https://www.accountingtools.com/articles/accounting-department-

responsibilities.html>.

Gartenstein, D., 2019. What Roles Does the Finance Department Play in a Business?

[Online]. Available Through:< https://bizfluent.com/facts-5683333-role-finance-

department-play-business-.html>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.