Financial Decision Making Report: SKANSKA PLC Performance Analysis

VerifiedAdded on 2023/01/09

|12

|3915

|74

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making within SKANSKA PLC, a leading UK building projects company. The introduction highlights the significance of financial decisions for corporate progress and the importance of effective financial management. The main body of the report is divided into two tasks. Task 1 examines the roles and responsibilities of the accounting and finance departments, detailing their functions and duties such as bookkeeping, payroll, cash management, budgeting, and investment management. Task 2 focuses on the computation and interpretation of key financial ratios, including ROCE, net profit margin, current ratio, debtor and creditor collection periods, to evaluate SKANSKA PLC's performance in 2018 and 2019. The report concludes with an overview of the company's financial health based on these ratios, providing insights into its profitability, liquidity, and efficiency. This assignment is a valuable resource for students studying finance, offering a practical application of financial analysis techniques.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Decision-making plays an influencing part in any corporation's progress. The companies

usually make their preparations and financial choices with common goals and objectives.

Smarter choices move the company down a new direction, but much of that depends on financial

management, how policies are executed and how action objectives are pursued (Greenberg and

Hershfield, 2019). The method of making financial decisions is the most important for effective

management. Decision-taking systems are focused on professional experience and skills. Strong

financial judgments help the organization to make successful profits if judgments are accurate

and reasonable, the organization will thrive over a given period of time. The entire analysis is

divided into two sections. The first phase consisted of a comprehensive review of numerous

accounting & financial features, key responsibilities and important tasks in the sense of

SKANSKA PLC. This is UK's leading building projects company that was established in 1984.

The Company aims to expand its activities to other European nations for the next ten years. The

part of the project report also encompasses the calculation of various form of ratio bases on

SKANSKA PLC's financial reports with the aim of providing remarks on the current

performance form of the company's investment point of view.

MAIN BODY

TASK 1

Accounting and financing contribute to an entity's in the highly realistic sector and perform

important activities. They facilitate better tracking and proper implementation of the financial

resources and financial investments of the organization to help make sure that the business is

able to perform the functioning of the company efficiently and effectively in accordance with all

relevant compliance requirements. Such two activities are usually performed and managed

within the company by particular department (Lu, Won and Cheng, 2016). Accounting and

linked activities are carried out and handled by the accounting department, whilst provided by

financial actions are governed and carried out by the financial department. In the further part of

report analysis of financing and accounting department is done in such manner:

Accounting Department: Staff members in an accounting company or organization are

generally known as the branch of finance. The accounting team of small companies usually

Decision-making plays an influencing part in any corporation's progress. The companies

usually make their preparations and financial choices with common goals and objectives.

Smarter choices move the company down a new direction, but much of that depends on financial

management, how policies are executed and how action objectives are pursued (Greenberg and

Hershfield, 2019). The method of making financial decisions is the most important for effective

management. Decision-taking systems are focused on professional experience and skills. Strong

financial judgments help the organization to make successful profits if judgments are accurate

and reasonable, the organization will thrive over a given period of time. The entire analysis is

divided into two sections. The first phase consisted of a comprehensive review of numerous

accounting & financial features, key responsibilities and important tasks in the sense of

SKANSKA PLC. This is UK's leading building projects company that was established in 1984.

The Company aims to expand its activities to other European nations for the next ten years. The

part of the project report also encompasses the calculation of various form of ratio bases on

SKANSKA PLC's financial reports with the aim of providing remarks on the current

performance form of the company's investment point of view.

MAIN BODY

TASK 1

Accounting and financing contribute to an entity's in the highly realistic sector and perform

important activities. They facilitate better tracking and proper implementation of the financial

resources and financial investments of the organization to help make sure that the business is

able to perform the functioning of the company efficiently and effectively in accordance with all

relevant compliance requirements. Such two activities are usually performed and managed

within the company by particular department (Lu, Won and Cheng, 2016). Accounting and

linked activities are carried out and handled by the accounting department, whilst provided by

financial actions are governed and carried out by the financial department. In the further part of

report analysis of financing and accounting department is done in such manner:

Accounting Department: Staff members in an accounting company or organization are

generally known as the branch of finance. The accounting team of small companies usually

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

consists of 1 or 2 people engaged with accounting matters. Although there can be many

accounting sub-units in larger companies; for example, one unit can tackle taxes, while another

unit may tackle payable, deferred revenue dealing, and so on.

Finance Department: It is an important unit of a company which handles its assets. Finance

department 's corporate duties usually involve preparation, organising, auditing, accounting, and

maintaining the company's financial support. Typically, the financial department also conducted

procedures for drafting and finalizing the financial reports of the organization.

Role and Importance of Accounting and Finance Department:

Accounting department: This department supports the business it refers to with account-related

resources and financial assistance (Loughran and McDonald, 2016). The company must record

receipts and payments reports, product information, payroll sheets, capital investments and all

other sources of funding. Accounting firms shall examine each company's records to determine

the company's financial position and any changes that are necessary for the company's cost-

effective operation. The accountant in Skanska Plc usually includes a committed team of experts

who manage the financing of the business. Though not every member of the team will be a

professional accountant, team leaders will usually be trained under the expertise of accountant.

Through setting up an accounting department, companies may also ensure full transparency of

their financial records and give detailed, organized support to other staff and members.

Finance Department: The significance of the finance department of the corporate entity comes

from its ability to maintain that money is available or sufficient for operational structure and that

the institution can manage the time especially enough to fulfil the liabilities that are exceptional.

Almost all of the crucial importance of the Finance department of the organization lies in its

assignment of combining day-to-day financial choices with longer-term business governance.

Long-term and short-term goals ought to be balanced together with a holistic understanding of

why the enterprise was founded or how the business measures results. Individuals who function

the finance team may not have been top-level employees in Skanska Plc, although they are liable

for providing these senior members with the data and facts that they need to continue providing

leadership qualities.

Functions and Duties of Accounting and Finance department:

accounting sub-units in larger companies; for example, one unit can tackle taxes, while another

unit may tackle payable, deferred revenue dealing, and so on.

Finance Department: It is an important unit of a company which handles its assets. Finance

department 's corporate duties usually involve preparation, organising, auditing, accounting, and

maintaining the company's financial support. Typically, the financial department also conducted

procedures for drafting and finalizing the financial reports of the organization.

Role and Importance of Accounting and Finance Department:

Accounting department: This department supports the business it refers to with account-related

resources and financial assistance (Loughran and McDonald, 2016). The company must record

receipts and payments reports, product information, payroll sheets, capital investments and all

other sources of funding. Accounting firms shall examine each company's records to determine

the company's financial position and any changes that are necessary for the company's cost-

effective operation. The accountant in Skanska Plc usually includes a committed team of experts

who manage the financing of the business. Though not every member of the team will be a

professional accountant, team leaders will usually be trained under the expertise of accountant.

Through setting up an accounting department, companies may also ensure full transparency of

their financial records and give detailed, organized support to other staff and members.

Finance Department: The significance of the finance department of the corporate entity comes

from its ability to maintain that money is available or sufficient for operational structure and that

the institution can manage the time especially enough to fulfil the liabilities that are exceptional.

Almost all of the crucial importance of the Finance department of the organization lies in its

assignment of combining day-to-day financial choices with longer-term business governance.

Long-term and short-term goals ought to be balanced together with a holistic understanding of

why the enterprise was founded or how the business measures results. Individuals who function

the finance team may not have been top-level employees in Skanska Plc, although they are liable

for providing these senior members with the data and facts that they need to continue providing

leadership qualities.

Functions and Duties of Accounting and Finance department:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Duties and roles are primary duties delegated to a specific organization. Those might be standard

management activities, or focused on a company's priorities and gaols (Cockcroft and Russell,

2018). There are several other essential roles and tasks related to the accounting and finance

departments in this respect, as mentioned below with reference to Skanska Plc:

Bookkeeping: This is most critical accounting department feature. This contains day-to-day

monitoring, reviewing, and assessing of all a company's financial exchanges. It will help viewers

of all expenses (exchanges, fees, etc.) and sale of finished goods. In Skanska Plc, this role is

mostly carried out by bookkeepers who may be replaced by more specialist payables and

receivable companies as the company grow or applies its actions.

Payroll: The total wages and incentives received by each employee over each salary period,

refers to as net compensation or average salaries, will be calculated. The correct levels of taxes,

corporate tax as well as certain gross compensation incentives have to be determined by finance

department on the basis of detailed private information of staff accounts and up-to - date

documents. Stubs, that disclose detailed information to staff throughout each pay period, should

be introduced to the salary sheets. Full sums of income tax and social benefit contributions,

including the job tax imposed on employees, will be paid to government departments on

schedule. Pay check, weekends, holiday pay and other employee-gained incentives should be

adapted for each pay cycle. In short, payroll is a fundamental and necessary task that the

accounting department performs

Cash collections: Any cash received from sales and any other purchases must be registered and

recorded correctly, not just in the cash account of the company, but also in due consideration of

the source of revenue gained. In Skanska Plc, the accounting team guarantees that cash is added

to the corporation's right records, so that a sufficient volume of coins so money is kept on board

to allow customer changes. Accountants maintain the financial statements of the organization,

check-books and track all cash transaction outlets.

Cash payments (disbursements): A business files numerous more checks during the period of

the year along with payroll accounts to compensate for a broad variety of expenses, compensate

various fees, repay debts, and distribute some of the earnings to the firm's members (Conley,

Gonçalves and Hansen, 2018). All these checks must be prepared by an accounting department

for the documents of officials authorized to approve of that kind cheques. In Skanska Plc

management activities, or focused on a company's priorities and gaols (Cockcroft and Russell,

2018). There are several other essential roles and tasks related to the accounting and finance

departments in this respect, as mentioned below with reference to Skanska Plc:

Bookkeeping: This is most critical accounting department feature. This contains day-to-day

monitoring, reviewing, and assessing of all a company's financial exchanges. It will help viewers

of all expenses (exchanges, fees, etc.) and sale of finished goods. In Skanska Plc, this role is

mostly carried out by bookkeepers who may be replaced by more specialist payables and

receivable companies as the company grow or applies its actions.

Payroll: The total wages and incentives received by each employee over each salary period,

refers to as net compensation or average salaries, will be calculated. The correct levels of taxes,

corporate tax as well as certain gross compensation incentives have to be determined by finance

department on the basis of detailed private information of staff accounts and up-to - date

documents. Stubs, that disclose detailed information to staff throughout each pay period, should

be introduced to the salary sheets. Full sums of income tax and social benefit contributions,

including the job tax imposed on employees, will be paid to government departments on

schedule. Pay check, weekends, holiday pay and other employee-gained incentives should be

adapted for each pay cycle. In short, payroll is a fundamental and necessary task that the

accounting department performs

Cash collections: Any cash received from sales and any other purchases must be registered and

recorded correctly, not just in the cash account of the company, but also in due consideration of

the source of revenue gained. In Skanska Plc, the accounting team guarantees that cash is added

to the corporation's right records, so that a sufficient volume of coins so money is kept on board

to allow customer changes. Accountants maintain the financial statements of the organization,

check-books and track all cash transaction outlets.

Cash payments (disbursements): A business files numerous more checks during the period of

the year along with payroll accounts to compensate for a broad variety of expenses, compensate

various fees, repay debts, and distribute some of the earnings to the firm's members (Conley,

Gonçalves and Hansen, 2018). All these checks must be prepared by an accounting department

for the documents of officials authorized to approve of that kind cheques. In Skanska Plc

accounting department keeps all appropriate financial documents and files to know when bills

are due, guarantees proper reimbursement of the balance and forward reviews for signing.

Procurement and inventory: Accounting divisions are usually charged with controlling the

procurement orders given for inventory (items to be sold / supplied by the client) and all the

products and services acquired by the business. Skanska Plc allows several purchases across the

course of the year, most of which are credit-based, meaning that products bought are bought

now, with payment for afterwards. It also helps to keep track of all liabilities arising from card

payments, so that pay-outs can be analysed until deadlines. Also, an accounting department

keeps adequate data of sustained reductions for sale by the corporation and reviews the cost of

goods finally purchased when the products are purchased.

Functions and Duties of Finance department-

Budgets and forecasting: The finance team works with managers in this role to prepare the

financial planning activities and forecasts of the company, and to offer guidance on the financial

position of the organization. Such details will be used to satisfy the cash needs of each company,

to schedule the staffing level of the enterprise, to prepare for the purchase of assets and to expand

at a lower cost before they are necessary. Within Skanska Plc, the finance team frequently

utilizes statistical evidence from the relevant departments to provide reliable forecasts and

predictions for the shorter term.

Suggesting and sourcing lengthy-term financing: It is also a major role of the finance

department of the group to advise businesses on the right funding combination that will provide

the maximum returns to the sector and also enable them to provide long-term financing at the

lowest possible cost, with the goal of retaining a fair amount of leverage in Skanska Plc.

Management of Company’s Investments: Aside from selecting appropriate capital

investments, the finance team also has a duty to regulate existing organizational assets (Floyd

and List, 2016). Within Skanska Plc the finance team must work with current investments rather

than capital assets. Working capital of the company has to be managed efficiently in a manner

that optimizes profitability relative to the amount of attached funds, since this has a larger impact

on competitiveness of the business than fixed assets.

Financial Reporting and analysis: Financial analysis and examination is a process that requires

and transforms raw accounting input into reliable, available, and comparative financial reports. A

are due, guarantees proper reimbursement of the balance and forward reviews for signing.

Procurement and inventory: Accounting divisions are usually charged with controlling the

procurement orders given for inventory (items to be sold / supplied by the client) and all the

products and services acquired by the business. Skanska Plc allows several purchases across the

course of the year, most of which are credit-based, meaning that products bought are bought

now, with payment for afterwards. It also helps to keep track of all liabilities arising from card

payments, so that pay-outs can be analysed until deadlines. Also, an accounting department

keeps adequate data of sustained reductions for sale by the corporation and reviews the cost of

goods finally purchased when the products are purchased.

Functions and Duties of Finance department-

Budgets and forecasting: The finance team works with managers in this role to prepare the

financial planning activities and forecasts of the company, and to offer guidance on the financial

position of the organization. Such details will be used to satisfy the cash needs of each company,

to schedule the staffing level of the enterprise, to prepare for the purchase of assets and to expand

at a lower cost before they are necessary. Within Skanska Plc, the finance team frequently

utilizes statistical evidence from the relevant departments to provide reliable forecasts and

predictions for the shorter term.

Suggesting and sourcing lengthy-term financing: It is also a major role of the finance

department of the group to advise businesses on the right funding combination that will provide

the maximum returns to the sector and also enable them to provide long-term financing at the

lowest possible cost, with the goal of retaining a fair amount of leverage in Skanska Plc.

Management of Company’s Investments: Aside from selecting appropriate capital

investments, the finance team also has a duty to regulate existing organizational assets (Floyd

and List, 2016). Within Skanska Plc the finance team must work with current investments rather

than capital assets. Working capital of the company has to be managed efficiently in a manner

that optimizes profitability relative to the amount of attached funds, since this has a larger impact

on competitiveness of the business than fixed assets.

Financial Reporting and analysis: Financial analysis and examination is a process that requires

and transforms raw accounting input into reliable, available, and comparative financial reports. A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial manager leads to internal advancement by continuously measuring and documenting

key items which are critical to business expansion (Smith and Urquhart, 2018). In Skanska Plc, it

includes an overview of all sources of income, expenditures and funds available for future usage

(except those currently spent and scheduled for the period ending) and certain non-monetary

information. And usually they are presented to managers in a transparent and substantive

manner.

TASK 2

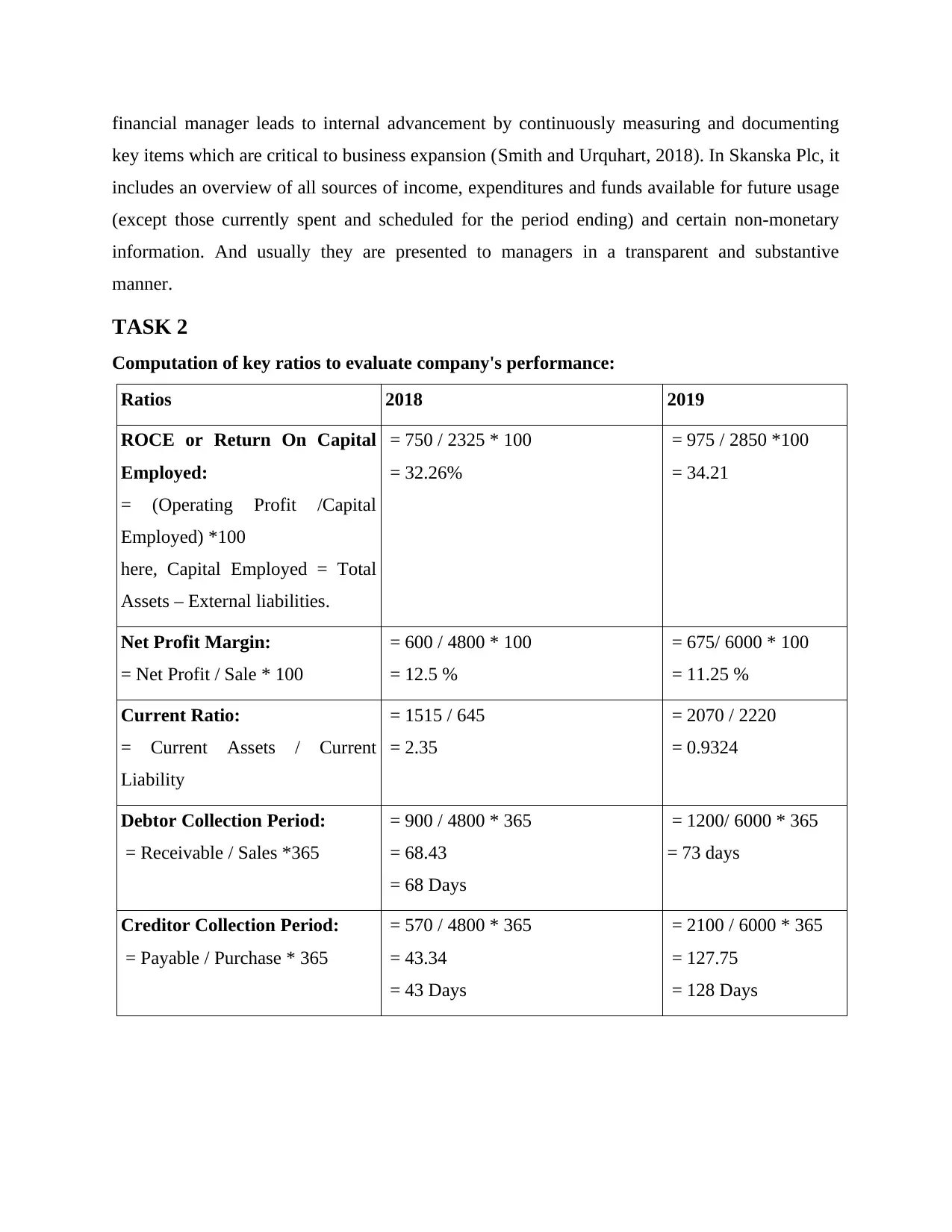

Computation of key ratios to evaluate company's performance:

Ratios 2018 2019

ROCE or Return On Capital

Employed:

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 750 / 2325 * 100

= 32.26%

= 975 / 2850 *100

= 34.21

Net Profit Margin:

= Net Profit / Sale * 100

= 600 / 4800 * 100

= 12.5 %

= 675/ 6000 * 100

= 11.25 %

Current Ratio:

= Current Assets / Current

Liability

= 1515 / 645

= 2.35

= 2070 / 2220

= 0.9324

Debtor Collection Period:

= Receivable / Sales *365

= 900 / 4800 * 365

= 68.43

= 68 Days

= 1200/ 6000 * 365

= 73 days

Creditor Collection Period:

= Payable / Purchase * 365

= 570 / 4800 * 365

= 43.34

= 43 Days

= 2100 / 6000 * 365

= 127.75

= 128 Days

key items which are critical to business expansion (Smith and Urquhart, 2018). In Skanska Plc, it

includes an overview of all sources of income, expenditures and funds available for future usage

(except those currently spent and scheduled for the period ending) and certain non-monetary

information. And usually they are presented to managers in a transparent and substantive

manner.

TASK 2

Computation of key ratios to evaluate company's performance:

Ratios 2018 2019

ROCE or Return On Capital

Employed:

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 750 / 2325 * 100

= 32.26%

= 975 / 2850 *100

= 34.21

Net Profit Margin:

= Net Profit / Sale * 100

= 600 / 4800 * 100

= 12.5 %

= 675/ 6000 * 100

= 11.25 %

Current Ratio:

= Current Assets / Current

Liability

= 1515 / 645

= 2.35

= 2070 / 2220

= 0.9324

Debtor Collection Period:

= Receivable / Sales *365

= 900 / 4800 * 365

= 68.43

= 68 Days

= 1200/ 6000 * 365

= 73 days

Creditor Collection Period:

= Payable / Purchase * 365

= 570 / 4800 * 365

= 43.34

= 43 Days

= 2100 / 6000 * 365

= 127.75

= 128 Days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Comment on performance of SKANSKA PLC, based on computed ratios:

Return on capital employed: ROCE corresponds to profitability ratio which contributes to

measure a corporation 's profit for overall capital it engages. ROCE is calculated by representing

Net After Tax Operating Profit (NOPAT) as percentage of total long-term fund capital

employed. In simple words, this can be interpreted as rate (%) of return enterprise as a whole

earns. Example ROE (equity), which computes the percentage returns of shareholders, ROCE

computes the percentage returns of all investors together (Myšková and Hájek, 2017). When an

organization is funded entirely by equity, then ROE and ROCE will same. ROCE is quantifiable

through a simplistic equation. ROCE measurement is straightforward, and it could be easily

assessed based on company's financial statements like P&L account, balance sheet. NOPAT

could be drawn through P / L a / c and while CE form balance sheet.

As computed above, Skanska Plc 's ROCE ratio in year 2018 was 32.26 % while in year

2019 it has been reached to 34.21 % indicting an upward trend in ROCE. The greater ROCE is

beneficial suggesting that the business produces more profits pound of engaged capital in

business. A lesser ROCE level implies a lesser return. A business with fewer assets but the same

profits as its rivals would have greater returns on entire capital employed and higher efficiency

as a result. Here in case of Skanska Plc, this increase indicates that company's officiousness to

generate return on aggregate capital invested in company has been increased over the said

period.

Net profit margin: This ratio is often described in percent terms. Such figures reflect the

corporation 's excellence in operation. Net profit margin is crucial way of comparing businesses

within a same sector, and these entities are usually subject to various conditions. Net profit

margin, also regarded as percent net margin, shows how much sum of net profits a business

produces with overall sales reached. A larger net profit ratio implies a business is more effective

in transforming revenues into profit. Review of net profit margin isn't really equivalent to gross

profit margin. The fixed expenditures are precluded from measurement of gross profit. While

in net profit margin all expenses are considered in order to determine the final worth of company'

income. The rise in net-profit margin relative to the preceding year signifies a rise in both

operating performance as well as profitability-level (Linares-Mustarós, Coenders and Vives-

Mestres, 2018).

Return on capital employed: ROCE corresponds to profitability ratio which contributes to

measure a corporation 's profit for overall capital it engages. ROCE is calculated by representing

Net After Tax Operating Profit (NOPAT) as percentage of total long-term fund capital

employed. In simple words, this can be interpreted as rate (%) of return enterprise as a whole

earns. Example ROE (equity), which computes the percentage returns of shareholders, ROCE

computes the percentage returns of all investors together (Myšková and Hájek, 2017). When an

organization is funded entirely by equity, then ROE and ROCE will same. ROCE is quantifiable

through a simplistic equation. ROCE measurement is straightforward, and it could be easily

assessed based on company's financial statements like P&L account, balance sheet. NOPAT

could be drawn through P / L a / c and while CE form balance sheet.

As computed above, Skanska Plc 's ROCE ratio in year 2018 was 32.26 % while in year

2019 it has been reached to 34.21 % indicting an upward trend in ROCE. The greater ROCE is

beneficial suggesting that the business produces more profits pound of engaged capital in

business. A lesser ROCE level implies a lesser return. A business with fewer assets but the same

profits as its rivals would have greater returns on entire capital employed and higher efficiency

as a result. Here in case of Skanska Plc, this increase indicates that company's officiousness to

generate return on aggregate capital invested in company has been increased over the said

period.

Net profit margin: This ratio is often described in percent terms. Such figures reflect the

corporation 's excellence in operation. Net profit margin is crucial way of comparing businesses

within a same sector, and these entities are usually subject to various conditions. Net profit

margin, also regarded as percent net margin, shows how much sum of net profits a business

produces with overall sales reached. A larger net profit ratio implies a business is more effective

in transforming revenues into profit. Review of net profit margin isn't really equivalent to gross

profit margin. The fixed expenditures are precluded from measurement of gross profit. While

in net profit margin all expenses are considered in order to determine the final worth of company'

income. The rise in net-profit margin relative to the preceding year signifies a rise in both

operating performance as well as profitability-level (Linares-Mustarós, Coenders and Vives-

Mestres, 2018).

In this regard, based on computation of ratios of Skanska Plc it has been analysed that

net-profit margin of corporation in year 2019 is only 11.25 % which 12.5 % in year 2018

reflecting slight decrement in overall NP margin. Here this decrease in net-profit percentage

shows that Skanska Plc 's actual efficiency to transform their total sales/revenue into profit has

been decreased over the period. Company should focus on this area to enhance their profitability

level. For this corporation should improve the sales volume and minimise overall business

expenditures.

Current ratio: This implies to liquidity ratio which determines the capacity of a corporation to

cover off its shorter-term liabilities with its all current assets. The current ratio allows to give

insights into the capacity of a firm to repay its short-term liabilities with its short-term (fluid)

assets (practically, if a firm has sufficient cash funds to repay its current obligations,

when required). If a organization has higher ratio, they will be able to fulfil their shorter-term

debts/obligations. The higher number, more efficient the organization is. At another side,

if current ratio figure is less than 1, this implies that the corporation is not in a position to

repay its shorter-term liabilities/debts with cash funds (Zorn, Esteves, Baur and Lips, 2018).

As per the above table containing current ratio of Skanska Plc, it has been evaluated that

corporation's current ratio in year 2018 was 2.34 that has been declined to 0.9324 indicating a

significant decrease in ratio. This major decline in ratio in unfavourable sign for Skanska Plc's

liquidity position. Such decrement in current ratio shows that corporation's capabilities to meet

its short-term liabilities/obligations has been decreased considerably. Company should

emphasise on this aspect as in long run this can impact Skanska's ability to survive in industry.

Although it shows only short-term liquidity position of company but ignorance of this ratio result

can lead to adverse financial conditions for corporation.

Average Receivable days’/ Debtors collection period: The number of days’ company takes to

recover its debt payments with respect of its trade receivables/debtors or credit selling is

recognized as average collection period or days outstanding sales (DSO). This metric is useful

since it underlines how the corporation's trade receivables are being handled. That estimate

allows company executives flexibility to make required changes in order to plan for any potential

commitments that may require cash-fund from sales. As a basic guideline, lower average

collection time frame for trade receivable is viewed to be quite advantageous because it implies

that clients are paying outstanding sum faster. But at other hand, a greater average collection

net-profit margin of corporation in year 2019 is only 11.25 % which 12.5 % in year 2018

reflecting slight decrement in overall NP margin. Here this decrease in net-profit percentage

shows that Skanska Plc 's actual efficiency to transform their total sales/revenue into profit has

been decreased over the period. Company should focus on this area to enhance their profitability

level. For this corporation should improve the sales volume and minimise overall business

expenditures.

Current ratio: This implies to liquidity ratio which determines the capacity of a corporation to

cover off its shorter-term liabilities with its all current assets. The current ratio allows to give

insights into the capacity of a firm to repay its short-term liabilities with its short-term (fluid)

assets (practically, if a firm has sufficient cash funds to repay its current obligations,

when required). If a organization has higher ratio, they will be able to fulfil their shorter-term

debts/obligations. The higher number, more efficient the organization is. At another side,

if current ratio figure is less than 1, this implies that the corporation is not in a position to

repay its shorter-term liabilities/debts with cash funds (Zorn, Esteves, Baur and Lips, 2018).

As per the above table containing current ratio of Skanska Plc, it has been evaluated that

corporation's current ratio in year 2018 was 2.34 that has been declined to 0.9324 indicating a

significant decrease in ratio. This major decline in ratio in unfavourable sign for Skanska Plc's

liquidity position. Such decrement in current ratio shows that corporation's capabilities to meet

its short-term liabilities/obligations has been decreased considerably. Company should

emphasise on this aspect as in long run this can impact Skanska's ability to survive in industry.

Although it shows only short-term liquidity position of company but ignorance of this ratio result

can lead to adverse financial conditions for corporation.

Average Receivable days’/ Debtors collection period: The number of days’ company takes to

recover its debt payments with respect of its trade receivables/debtors or credit selling is

recognized as average collection period or days outstanding sales (DSO). This metric is useful

since it underlines how the corporation's trade receivables are being handled. That estimate

allows company executives flexibility to make required changes in order to plan for any potential

commitments that may require cash-fund from sales. As a basic guideline, lower average

collection time frame for trade receivable is viewed to be quite advantageous because it implies

that clients are paying outstanding sum faster. But at other hand, a greater average collection

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

period may indicate that revenues are being transformed to cash funds much slower than is

needed (Arkan, 2016).

As stated here in above table, company Skanska Plc's debtor collection-period in years

2019 and 2018 are 73 days and 68 days respectively indicating increment in collection period

which is not a favourable indicator for corporation as companies is taking more days in 2019 as

compare to 2018 to collect sum form trade receivables or debtors. This can lead to adverse

working capital position within company. Increase in this ratio can also affect corporation's short

term liquidity position as well. The average collection duration of receivables should be handled

under credit terms laid out to the client. If buyers pay dues later than expected, this can result to

cash flows problems as the time between transaction and actual payment is extended. It may, at

this level, be a concept to give a slight discount on making payment within a certain period or

under other favourable conditions in order to raise speed of payments.

Average Payable days’/ Creditors collection period: The organization may not buy all of its

products on cash basis. Often, there might be a purchase of credits. This measure is determined

to assess the period in days taken to pay sum to creditors. That ratio shows degree of

management performance of the sum charged by the creditors/lenders. Typically,

lower ratio, liquidity of the market issues is in stronger position and vice-versa. Simply,

higher ratio, the business enjoys credit period permitted by suppliers and the sum can be

utilised for any other effective aim. Around same time, the higher proportion can often mean

fewer discount options available or higher rates charged for products bought on credit (Le and

Viviani, 2018).

Shown figures of Average Payable days of Skanska Plc shows that corporation's creditor

collection periods are 43 days and 128 days respectively during year 2018 and 2019 reflecting a

increased delay in period of making payment to its creditors. This increase in period shows that

corporation's ability to make payments to their creditors has been declined over the period. This

increase in period is indication that company has not adequate or sufficient funds to pay its

creditors in short displaying poor liquidity position.

needed (Arkan, 2016).

As stated here in above table, company Skanska Plc's debtor collection-period in years

2019 and 2018 are 73 days and 68 days respectively indicating increment in collection period

which is not a favourable indicator for corporation as companies is taking more days in 2019 as

compare to 2018 to collect sum form trade receivables or debtors. This can lead to adverse

working capital position within company. Increase in this ratio can also affect corporation's short

term liquidity position as well. The average collection duration of receivables should be handled

under credit terms laid out to the client. If buyers pay dues later than expected, this can result to

cash flows problems as the time between transaction and actual payment is extended. It may, at

this level, be a concept to give a slight discount on making payment within a certain period or

under other favourable conditions in order to raise speed of payments.

Average Payable days’/ Creditors collection period: The organization may not buy all of its

products on cash basis. Often, there might be a purchase of credits. This measure is determined

to assess the period in days taken to pay sum to creditors. That ratio shows degree of

management performance of the sum charged by the creditors/lenders. Typically,

lower ratio, liquidity of the market issues is in stronger position and vice-versa. Simply,

higher ratio, the business enjoys credit period permitted by suppliers and the sum can be

utilised for any other effective aim. Around same time, the higher proportion can often mean

fewer discount options available or higher rates charged for products bought on credit (Le and

Viviani, 2018).

Shown figures of Average Payable days of Skanska Plc shows that corporation's creditor

collection periods are 43 days and 128 days respectively during year 2018 and 2019 reflecting a

increased delay in period of making payment to its creditors. This increase in period shows that

corporation's ability to make payments to their creditors has been declined over the period. This

increase in period is indication that company has not adequate or sufficient funds to pay its

creditors in short displaying poor liquidity position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From above study it has been articulated that financial decision-making within a

corporation or firm context is crucial aspect as it helps to define the corporation's performance

and ensure the sustainable success of entity. This covers a massive range of factors and measures

to support more accurate decision-making. Management must consider multiple aspects of

financial decision-making in attempt to attain organisation's objectives and goals within present

period. Further it covers assessment and evaluation of financial ratio which help management to

assess the actual performance of corporation over a specific period as well as to make decisions

according to the results of ratios. Investors and other external stakeholders may also use the

corporation's financial ratios to assess the viability of investment made in a company.

From above study it has been articulated that financial decision-making within a

corporation or firm context is crucial aspect as it helps to define the corporation's performance

and ensure the sustainable success of entity. This covers a massive range of factors and measures

to support more accurate decision-making. Management must consider multiple aspects of

financial decision-making in attempt to attain organisation's objectives and goals within present

period. Further it covers assessment and evaluation of financial ratio which help management to

assess the actual performance of corporation over a specific period as well as to make decisions

according to the results of ratios. Investors and other external stakeholders may also use the

corporation's financial ratios to assess the viability of investment made in a company.

REFERENCES

Books and Journal:

Myšková, R. and Hájek, P., 2017. Comprehensive assessment of firm financial performance

using financial ratios and linguistic analysis of annual reports. Journal of International

Studies, volume 10, issue: 4.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting, 40, pp.1-10.

Zorn, A., Esteves, M., Baur, I. and Lips, M., 2018. Financial ratios as indicators of economic

sustainability: A quantitative analysis for Swiss Dairy Farms. Sustainability, 10(8),

p.2942.

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case study

in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, (79), pp.13-26.

Le, H.H. and Viviani, J.L., 2018. Predicting bank failure: An improvement by implementing a

machine-learning approach to classical financial ratios. Research in International

Business and Finance, 44, pp.16-25.

Greenberg, A.E. and Hershfield, H.E., 2019. Financial decision making. Consumer Psychology

Review, 2(1), pp.17-29.

Lu, Q., Won, J. and Cheng, J.C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management, 34(1), pp.3-21.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review, 28(3), pp.323-333.

Conley, T., Gonçalves, S. and Hansen, C., 2018. Inference with dependent data in accounting

and finance applications. Journal of Accounting Research, 56(4), pp.1139-1203.

Floyd, E. and List, J.A., 2016. Using field experiments in accounting and finance. Journal of

Accounting Research, 54(2), pp.437-475.

Smith, S.J. and Urquhart, V., 2018. Accounting and finance in UK universities: Academic

labour, shortages and strategies. The British Accounting Review, 50(6), pp.588-601.

Books and Journal:

Myšková, R. and Hájek, P., 2017. Comprehensive assessment of firm financial performance

using financial ratios and linguistic analysis of annual reports. Journal of International

Studies, volume 10, issue: 4.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting, 40, pp.1-10.

Zorn, A., Esteves, M., Baur, I. and Lips, M., 2018. Financial ratios as indicators of economic

sustainability: A quantitative analysis for Swiss Dairy Farms. Sustainability, 10(8),

p.2942.

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case study

in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, (79), pp.13-26.

Le, H.H. and Viviani, J.L., 2018. Predicting bank failure: An improvement by implementing a

machine-learning approach to classical financial ratios. Research in International

Business and Finance, 44, pp.16-25.

Greenberg, A.E. and Hershfield, H.E., 2019. Financial decision making. Consumer Psychology

Review, 2(1), pp.17-29.

Lu, Q., Won, J. and Cheng, J.C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management, 34(1), pp.3-21.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review, 28(3), pp.323-333.

Conley, T., Gonçalves, S. and Hansen, C., 2018. Inference with dependent data in accounting

and finance applications. Journal of Accounting Research, 56(4), pp.1139-1203.

Floyd, E. and List, J.A., 2016. Using field experiments in accounting and finance. Journal of

Accounting Research, 54(2), pp.437-475.

Smith, S.J. and Urquhart, V., 2018. Accounting and finance in UK universities: Academic

labour, shortages and strategies. The British Accounting Review, 50(6), pp.588-601.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.