Comprehensive Budget and Variance Analysis for Sky Cafe

VerifiedAdded on 2021/09/15

|11

|2152

|83

Report

AI Summary

This report provides a comprehensive financial analysis of Sky Cafe's budget for the month of July. It begins by outlining the objectives of preparing a budget, emphasizing its role in financial planning, resource allocation, and risk management. The core of the report focuses on a detailed examination of revenue and spending variances, comparing budgeted figures with actual performance. The analysis highlights unfavorable variances in revenue, facility rent, insurance, and fuel costs. The report then identifies specific management concerns arising from these variances, such as overestimation of sales volume and increased operational expenses. Finally, the report offers actionable recommendations to support Sky Cafe's objectives, including enhanced marketing efforts to boost sales, and the appointment of a qualified management accountant to investigate and address spending variances. The report concludes by reiterating the importance of budgeting for effective financial control and performance improvement.

Running head: ACCOUNTS AND FINANCE

Accounts and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounts and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTS AND FINANCE

Table of Contents

Introduction:....................................................................................................................................2

1. Objectives of preparing budget for Sky Café:.............................................................................2

2. Revenue and spending variance of Sky Café for the month of July:...........................................3

3. Identification of those activities of variances having management concerns:.............................5

4. Recommendation to Sky Café for supporting its objectives:......................................................7

Conclusion:......................................................................................................................................7

References:......................................................................................................................................9

Table of Contents

Introduction:....................................................................................................................................2

1. Objectives of preparing budget for Sky Café:.............................................................................2

2. Revenue and spending variance of Sky Café for the month of July:...........................................3

3. Identification of those activities of variances having management concerns:.............................5

4. Recommendation to Sky Café for supporting its objectives:......................................................7

Conclusion:......................................................................................................................................7

References:......................................................................................................................................9

2ACCOUNTS AND FINANCE

Introduction:

All business organisations aim to achieve success, competitive advantage, low costs,

increased revenues, long-term customer loyalty, greater earnings per share and increased market

value. For accomplishing the above-stated objectives, it is necessary to plan out the objectives in

an optimal way by considering plans like budgets. In business environment, a budget is

considered as a plan for the outgoing expenses and incoming revenues for an organisation for a

particular timeframe (Arnaboldi, Lapsley and Steccolini 2015). The main reason for preparing

budgets is to forecast the future outcomes after considering the likely changes to take place in the

upcoming years. Thus, annual budgets are the most widely used mechanism in order to control

expenditure and establish related performance targets. This paper would intend to explore the

objectives of preparing budget for Sky Café along with finding out budgetary variances by

highlighting on those areas that are of significant concern to the management. Finally, after

identification of such variances, recommendations have been provided to the organisation for

supporting its objectives.

1. Objectives of preparing budget for Sky Café:

Sky Café is an organisation, which is involved in preparing meals for its tourists and

citizens near the airport. Therefore, it is necessary for the management of the organisation to

prepare budget by keeping in mind the following set of objectives:

The budget planning process would assist the management of Sky Café in identifying and

reviewing the effect on the cash flows, balance sheet and inventory planning of the

Introduction:

All business organisations aim to achieve success, competitive advantage, low costs,

increased revenues, long-term customer loyalty, greater earnings per share and increased market

value. For accomplishing the above-stated objectives, it is necessary to plan out the objectives in

an optimal way by considering plans like budgets. In business environment, a budget is

considered as a plan for the outgoing expenses and incoming revenues for an organisation for a

particular timeframe (Arnaboldi, Lapsley and Steccolini 2015). The main reason for preparing

budgets is to forecast the future outcomes after considering the likely changes to take place in the

upcoming years. Thus, annual budgets are the most widely used mechanism in order to control

expenditure and establish related performance targets. This paper would intend to explore the

objectives of preparing budget for Sky Café along with finding out budgetary variances by

highlighting on those areas that are of significant concern to the management. Finally, after

identification of such variances, recommendations have been provided to the organisation for

supporting its objectives.

1. Objectives of preparing budget for Sky Café:

Sky Café is an organisation, which is involved in preparing meals for its tourists and

citizens near the airport. Therefore, it is necessary for the management of the organisation to

prepare budget by keeping in mind the following set of objectives:

The budget planning process would assist the management of Sky Café in identifying and

reviewing the effect on the cash flows, balance sheet and inventory planning of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTS AND FINANCE

organisation. Moreover, it would assist the organisation in assessing its financial position

and borrowing needs from the market (Bedford 2015).

Another objective of preparing budget for Sky Café is that it allows the apportionment of

financial resources towards an important strategic plan developed by the management.

The management could only consider the task of accomplishing the particular identified

target after resource allocation.

With the help of budget, the organisational management could respond effectively to the

market conditions for tracking quickly the process of goal accomplishment (Bedford,

Malmi and Sandelin 2016). The identification of risks would assist Sky Café in

implementing measures, which would result in minimisation of financial risk.

Finally, with the help of a financial plan like budget, the management of Sky Café could

identify risk and return. It assists in the identification of gap between financing plans and

investment (Chenhall and Moers 2015). For instance, at the time of preparing budget, Sky

Café would be able to apportion resources as well as inventory for fulfilling the customer

demands adequately. These resources could be both short-term and long-term.

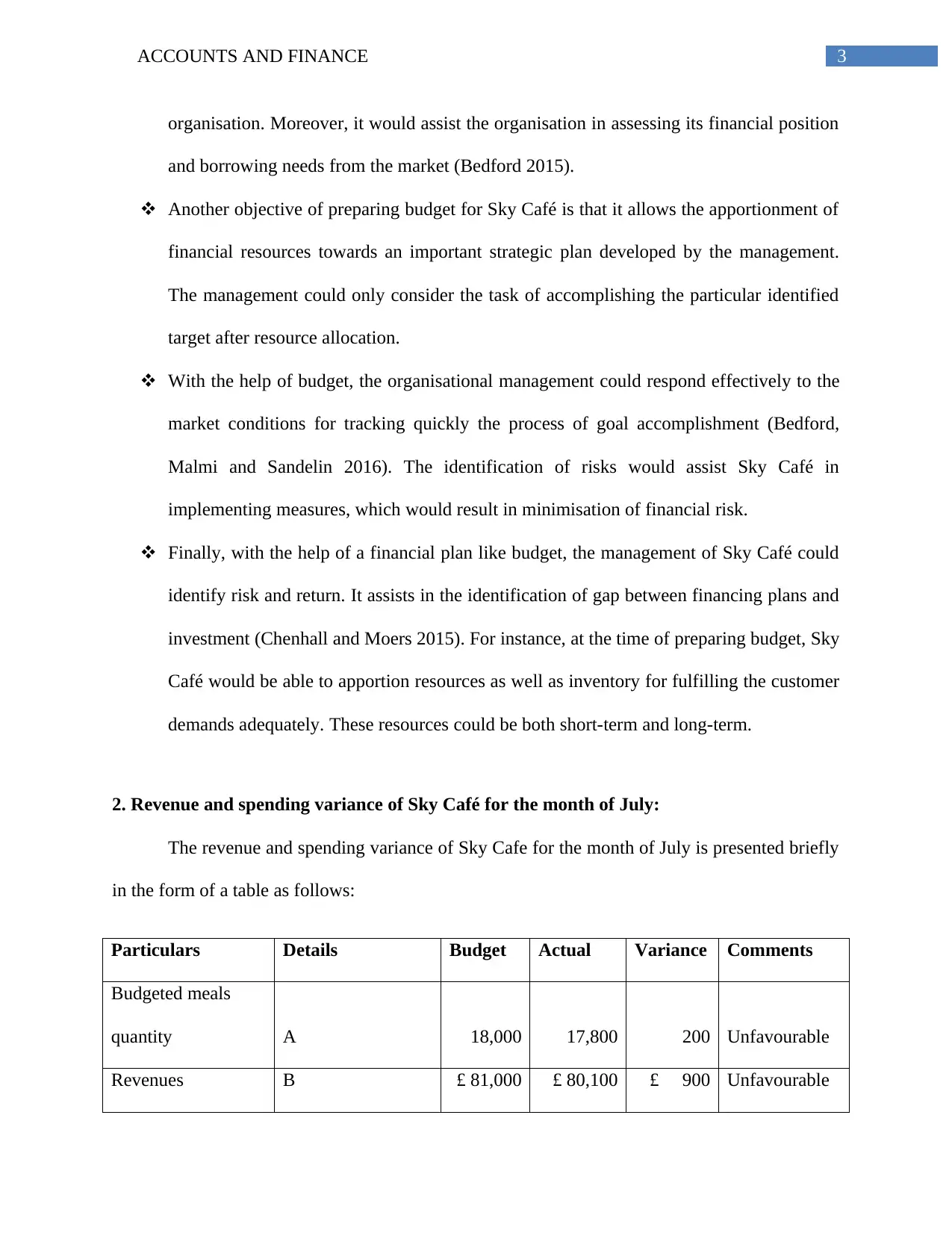

2. Revenue and spending variance of Sky Café for the month of July:

The revenue and spending variance of Sky Cafe for the month of July is presented briefly

in the form of a table as follows:

Particulars Details Budget Actual Variance Comments

Budgeted meals

quantity A 18,000 17,800 200 Unfavourable

Revenues B £ 81,000 £ 80,100 £ 900 Unfavourable

organisation. Moreover, it would assist the organisation in assessing its financial position

and borrowing needs from the market (Bedford 2015).

Another objective of preparing budget for Sky Café is that it allows the apportionment of

financial resources towards an important strategic plan developed by the management.

The management could only consider the task of accomplishing the particular identified

target after resource allocation.

With the help of budget, the organisational management could respond effectively to the

market conditions for tracking quickly the process of goal accomplishment (Bedford,

Malmi and Sandelin 2016). The identification of risks would assist Sky Café in

implementing measures, which would result in minimisation of financial risk.

Finally, with the help of a financial plan like budget, the management of Sky Café could

identify risk and return. It assists in the identification of gap between financing plans and

investment (Chenhall and Moers 2015). For instance, at the time of preparing budget, Sky

Café would be able to apportion resources as well as inventory for fulfilling the customer

demands adequately. These resources could be both short-term and long-term.

2. Revenue and spending variance of Sky Café for the month of July:

The revenue and spending variance of Sky Cafe for the month of July is presented briefly

in the form of a table as follows:

Particulars Details Budget Actual Variance Comments

Budgeted meals

quantity A 18,000 17,800 200 Unfavourable

Revenues B £ 81,000 £ 80,100 £ 900 Unfavourable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTS AND FINANCE

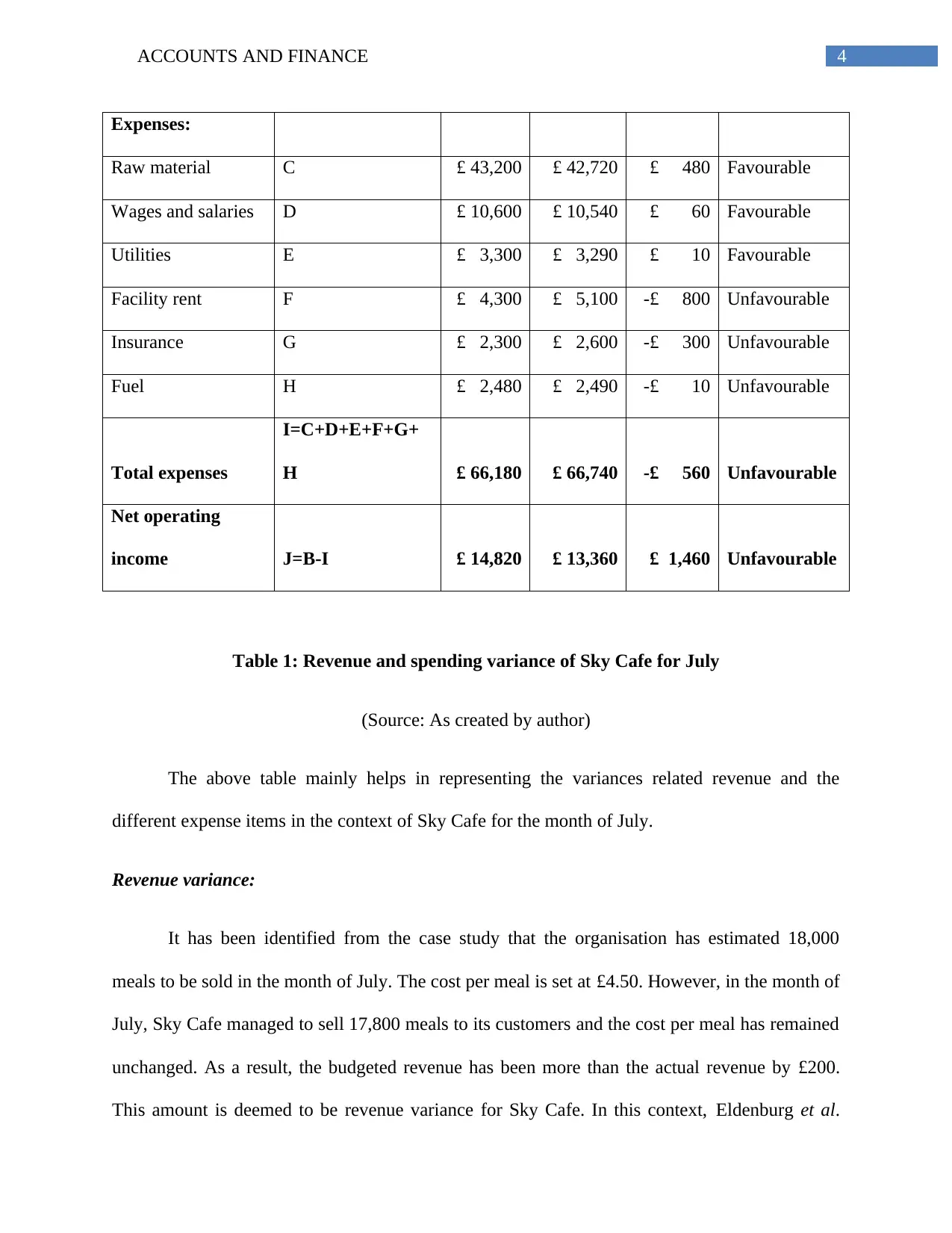

Expenses:

Raw material C £ 43,200 £ 42,720 £ 480 Favourable

Wages and salaries D £ 10,600 £ 10,540 £ 60 Favourable

Utilities E £ 3,300 £ 3,290 £ 10 Favourable

Facility rent F £ 4,300 £ 5,100 -£ 800 Unfavourable

Insurance G £ 2,300 £ 2,600 -£ 300 Unfavourable

Fuel H £ 2,480 £ 2,490 -£ 10 Unfavourable

Total expenses

I=C+D+E+F+G+

H £ 66,180 £ 66,740 -£ 560 Unfavourable

Net operating

income J=B-I £ 14,820 £ 13,360 £ 1,460 Unfavourable

Table 1: Revenue and spending variance of Sky Cafe for July

(Source: As created by author)

The above table mainly helps in representing the variances related revenue and the

different expense items in the context of Sky Cafe for the month of July.

Revenue variance:

It has been identified from the case study that the organisation has estimated 18,000

meals to be sold in the month of July. The cost per meal is set at £4.50. However, in the month of

July, Sky Cafe managed to sell 17,800 meals to its customers and the cost per meal has remained

unchanged. As a result, the budgeted revenue has been more than the actual revenue by £200.

This amount is deemed to be revenue variance for Sky Cafe. In this context, Eldenburg et al.

Expenses:

Raw material C £ 43,200 £ 42,720 £ 480 Favourable

Wages and salaries D £ 10,600 £ 10,540 £ 60 Favourable

Utilities E £ 3,300 £ 3,290 £ 10 Favourable

Facility rent F £ 4,300 £ 5,100 -£ 800 Unfavourable

Insurance G £ 2,300 £ 2,600 -£ 300 Unfavourable

Fuel H £ 2,480 £ 2,490 -£ 10 Unfavourable

Total expenses

I=C+D+E+F+G+

H £ 66,180 £ 66,740 -£ 560 Unfavourable

Net operating

income J=B-I £ 14,820 £ 13,360 £ 1,460 Unfavourable

Table 1: Revenue and spending variance of Sky Cafe for July

(Source: As created by author)

The above table mainly helps in representing the variances related revenue and the

different expense items in the context of Sky Cafe for the month of July.

Revenue variance:

It has been identified from the case study that the organisation has estimated 18,000

meals to be sold in the month of July. The cost per meal is set at £4.50. However, in the month of

July, Sky Cafe managed to sell 17,800 meals to its customers and the cost per meal has remained

unchanged. As a result, the budgeted revenue has been more than the actual revenue by £200.

This amount is deemed to be revenue variance for Sky Cafe. In this context, Eldenburg et al.

5ACCOUNTS AND FINANCE

(2016) cited that revenue variance is used for measuring the difference between budgeted and

actual sales. This information is crucial for ascertaining the success of the selling activities and

perceived attractiveness of the products of an organisation.

In case of Sky Cafe, the selling price per unit has remained unchanged at the budgeted

and actual activity levels. However, a change could be observed in the number of units sold

between the budgeted quantity and the actual quantity. The budgeted revenue is obtained as

£81,000, while the actual revenue earned is £80,100. As a result, this has lead to unfavourable

revenue variance of £900.

Spending variance:

In the words of Heupel and Schmitz (2015), spending variance is the difference between

budgeted expenses and actual expenses. It mainly takes place at the time the budgeted figures are

not met. With the help of spending variance, the management of Sky Cafe could analyse the

departments and the managers on their capabilities in setting and fulfilling expense objectives.

These expenses could vary from direct materials to direct labour, as spending variance considers

all kinds of expenses (Isaac, Lawal and Okoli 2015). In case of Sky Cafe, the budgeted expenses

are obtained as £66,180, while the actual expenses incurred for the month are £66,740.

Therefore, the spending variance for Sky Cafe is deemed to be unfavourable.

3. Identification of those activities of variances having management concerns:

Certain activities of variances are deemed to have management concerns for Sky Cafe,

which are demonstrated briefly as follows:

Revenue:

(2016) cited that revenue variance is used for measuring the difference between budgeted and

actual sales. This information is crucial for ascertaining the success of the selling activities and

perceived attractiveness of the products of an organisation.

In case of Sky Cafe, the selling price per unit has remained unchanged at the budgeted

and actual activity levels. However, a change could be observed in the number of units sold

between the budgeted quantity and the actual quantity. The budgeted revenue is obtained as

£81,000, while the actual revenue earned is £80,100. As a result, this has lead to unfavourable

revenue variance of £900.

Spending variance:

In the words of Heupel and Schmitz (2015), spending variance is the difference between

budgeted expenses and actual expenses. It mainly takes place at the time the budgeted figures are

not met. With the help of spending variance, the management of Sky Cafe could analyse the

departments and the managers on their capabilities in setting and fulfilling expense objectives.

These expenses could vary from direct materials to direct labour, as spending variance considers

all kinds of expenses (Isaac, Lawal and Okoli 2015). In case of Sky Cafe, the budgeted expenses

are obtained as £66,180, while the actual expenses incurred for the month are £66,740.

Therefore, the spending variance for Sky Cafe is deemed to be unfavourable.

3. Identification of those activities of variances having management concerns:

Certain activities of variances are deemed to have management concerns for Sky Cafe,

which are demonstrated briefly as follows:

Revenue:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTS AND FINANCE

Revenue is identified as the first item, which requires management attention of Sky Cafe.

This is because Sky Cafe has overestimated the sales volume for the month of July, due to which

it has earned £900 less than the budgeted amount. This might be due to the reason that the

competitors of the organisation might have introduced new products at attractive points having

identical or better features than its products (Kotas 2014). Moreover, another chance that the

organisation has generated lower revenue is that the competitors have offered similar types of

meals at lower charges and as a result, this has minimised the number of meals sold. Finally, as

Sky Cafe is mainly dependent on tourists for generating sales, there might be chances that it has

overestimated the number of likely customers to enter into the organisation. Therefore, all these

reasons could be summed up to support the adverse revenue variance for Sky Cafe.

Facility rent:

It has been identified that Sky Cafe has estimated the facility rent to be £4,300 for the

month of July. However, it has to incur £5,100 in the same month, which is £800 more than the

budgeted amount. As the management of Sky Cafe has overestimated the sales volume, it might

have leased additional equipment for preparing the meals for the tourists. Moreover, the

mobilisation as well demobilisation expenses change considerably with the equipment size,

which might be the reason behind unfavourable variance for Sky Cafe (Otley 2016).

Insurance:

An unfavourable insurance variance of £300 is deemed to be observed for Sky Cafe,

which might be due to the fact that it has hired additional employees during the month to meet

the estimated demand and they are not taken into consideration while estimating insurance

expense.

Revenue is identified as the first item, which requires management attention of Sky Cafe.

This is because Sky Cafe has overestimated the sales volume for the month of July, due to which

it has earned £900 less than the budgeted amount. This might be due to the reason that the

competitors of the organisation might have introduced new products at attractive points having

identical or better features than its products (Kotas 2014). Moreover, another chance that the

organisation has generated lower revenue is that the competitors have offered similar types of

meals at lower charges and as a result, this has minimised the number of meals sold. Finally, as

Sky Cafe is mainly dependent on tourists for generating sales, there might be chances that it has

overestimated the number of likely customers to enter into the organisation. Therefore, all these

reasons could be summed up to support the adverse revenue variance for Sky Cafe.

Facility rent:

It has been identified that Sky Cafe has estimated the facility rent to be £4,300 for the

month of July. However, it has to incur £5,100 in the same month, which is £800 more than the

budgeted amount. As the management of Sky Cafe has overestimated the sales volume, it might

have leased additional equipment for preparing the meals for the tourists. Moreover, the

mobilisation as well demobilisation expenses change considerably with the equipment size,

which might be the reason behind unfavourable variance for Sky Cafe (Otley 2016).

Insurance:

An unfavourable insurance variance of £300 is deemed to be observed for Sky Cafe,

which might be due to the fact that it has hired additional employees during the month to meet

the estimated demand and they are not taken into consideration while estimating insurance

expense.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTS AND FINANCE

Fuel:

As observed from the above table, actual fuel expense is £10 more than the budgeted fuel

expense. This is because the organisation has to incur higher transportation cost for transferring

raw materials from the origin to the manufacturing area (Segun and Olamide 2015).

4. Recommendation to Sky Café for supporting its objectives:

In order to deal with the above-stated concern areas, the following recommendations are

provided to the management of Sky Cafe in order to support its business objectives:

The organisation needs to emphasise on its marketing efforts for increasing the overall

sales margin. For instance, as Sky Cafe is located near an airport, it could use billboards,

leaflets and banners for drawing the attention of the customers. Special packages like

discounts and free gifts need to be provided to the customers for generating additional

sales revenue (Sponem and Lambert 2016).

Sky Cafe needs to appoint an experienced and competent management accountant for

analysing the reasons behind unfavourable spending variance. Accordingly, corrective

actions could be taken for minimising such variance (Weygandt, Kimmel and Kieso

2015).

Conclusion:

It is apparent from the above discussion that Sky Cafe is required to prepare budget for

resource allocation and providing response to the market conditions appropriately. By comparing

the budgeted income and expenses, it has been evaluated that the organisation both revenue and

spending variance are deemed to be unfavourable. The activities that are of concern to the

Fuel:

As observed from the above table, actual fuel expense is £10 more than the budgeted fuel

expense. This is because the organisation has to incur higher transportation cost for transferring

raw materials from the origin to the manufacturing area (Segun and Olamide 2015).

4. Recommendation to Sky Café for supporting its objectives:

In order to deal with the above-stated concern areas, the following recommendations are

provided to the management of Sky Cafe in order to support its business objectives:

The organisation needs to emphasise on its marketing efforts for increasing the overall

sales margin. For instance, as Sky Cafe is located near an airport, it could use billboards,

leaflets and banners for drawing the attention of the customers. Special packages like

discounts and free gifts need to be provided to the customers for generating additional

sales revenue (Sponem and Lambert 2016).

Sky Cafe needs to appoint an experienced and competent management accountant for

analysing the reasons behind unfavourable spending variance. Accordingly, corrective

actions could be taken for minimising such variance (Weygandt, Kimmel and Kieso

2015).

Conclusion:

It is apparent from the above discussion that Sky Cafe is required to prepare budget for

resource allocation and providing response to the market conditions appropriately. By comparing

the budgeted income and expenses, it has been evaluated that the organisation both revenue and

spending variance are deemed to be unfavourable. The activities that are of concern to the

8ACCOUNTS AND FINANCE

management include facility rent, insurance, fuel and revenue. Therefore, for dealing with these

issues, the management of Sky Cafe needs to increase its marketing efforts for boosting sales

performance and assess adverse variances for undertaking corrective actions.

management include facility rent, insurance, fuel and revenue. Therefore, for dealing with these

issues, the management of Sky Cafe needs to increase its marketing efforts for boosting sales

performance and assess adverse variances for undertaking corrective actions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTS AND FINANCE

References:

Arnaboldi, M., Lapsley, I. and Steccolini, I., 2015. Performance management in the public

sector: The ultimate challenge. Financial Accountability & Management, 31(1), pp.1-22.

Bedford, D.S., 2015. Management control systems across different modes of innovation:

Implications for firm performance. Management Accounting Research, 28, pp.12-30.

Bedford, D.S., Malmi, T. and Sandelin, M., 2016. Management control effectiveness and

strategy: An empirical analysis of packages and systems. Accounting, Organizations and

Society, 51, pp.12-28.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Eldenburg, L.G., Wolcott, S.K., Chen, L.H. and Cook, G., 2016. Cost management: Measuring,

monitoring, and motivating performance. Wiley Global Education.

Heupel, T. and Schmitz, S., 2015. Beyond Budgeting-a high-hanging fruit The impact of

managers’ mindset on the advantages of Beyond Budgeting. Procedia Economics and

Finance, 26, pp.729-736.

Isaac, L., Lawal, M. and Okoli, T., 2015. A systematic review of budgeting and budgetary

control in government owned organizations. Research Journal of Finance and Accounting, 6(6),

pp.1-11.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

References:

Arnaboldi, M., Lapsley, I. and Steccolini, I., 2015. Performance management in the public

sector: The ultimate challenge. Financial Accountability & Management, 31(1), pp.1-22.

Bedford, D.S., 2015. Management control systems across different modes of innovation:

Implications for firm performance. Management Accounting Research, 28, pp.12-30.

Bedford, D.S., Malmi, T. and Sandelin, M., 2016. Management control effectiveness and

strategy: An empirical analysis of packages and systems. Accounting, Organizations and

Society, 51, pp.12-28.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Eldenburg, L.G., Wolcott, S.K., Chen, L.H. and Cook, G., 2016. Cost management: Measuring,

monitoring, and motivating performance. Wiley Global Education.

Heupel, T. and Schmitz, S., 2015. Beyond Budgeting-a high-hanging fruit The impact of

managers’ mindset on the advantages of Beyond Budgeting. Procedia Economics and

Finance, 26, pp.729-736.

Isaac, L., Lawal, M. and Okoli, T., 2015. A systematic review of budgeting and budgetary

control in government owned organizations. Research Journal of Finance and Accounting, 6(6),

pp.1-11.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTS AND FINANCE

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Segun, A. and Olamide, F.T., 2015. The global debate on budgeting: Empirical evidence from

Nigeria. Business Management Review, 13(1).

Sponem, S. and Lambert, C., 2016. Exploring differences in budget characteristics, roles and

satisfaction: A configurational approach. Management Accounting Research, 30, pp.47-61.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Managerial accounting. Wiley.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Segun, A. and Olamide, F.T., 2015. The global debate on budgeting: Empirical evidence from

Nigeria. Business Management Review, 13(1).

Sponem, S. and Lambert, C., 2016. Exploring differences in budget characteristics, roles and

satisfaction: A configurational approach. Management Accounting Research, 30, pp.47-61.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Managerial accounting. Wiley.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.